Sample Category Title

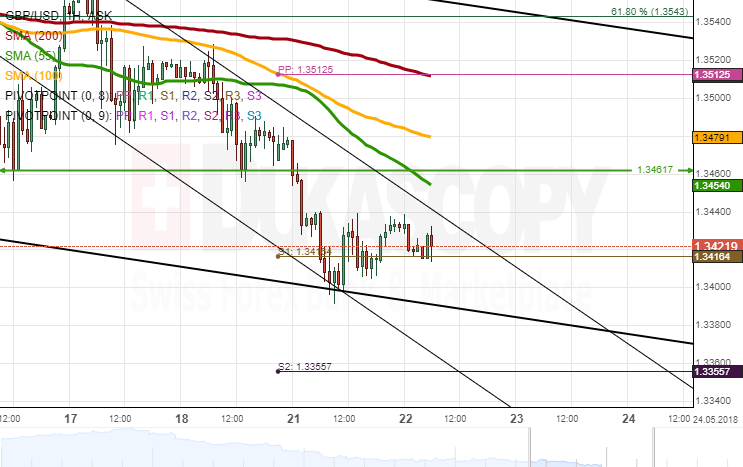

GBP/USD Analysis: Halts At 1.34

After breaching the previous 2018 low and a strong support level, GBP/USD remained under bearish pressure until the psychological 1.34 level and the bottom channel line were reached. The pair's subsequent movement was sideways in a very narrow range.

Technical indicators are starting to recover which might point to appreciation in this session. However, the pair faces the combined resistance of the 55– and 100-hour SMA at 1.3460—the level which might not surrender unless strong bullish sentiment pushes the pair higher. This upside momentum might be provided by UK Inflation Report Hearings at 0900GMT.

In this case, the next target is the weekly PP and the 200-hour SMA at 1.3520. Conversely, a breakout of 1.34 should send the pair for the weekly S2 at 1.3360.

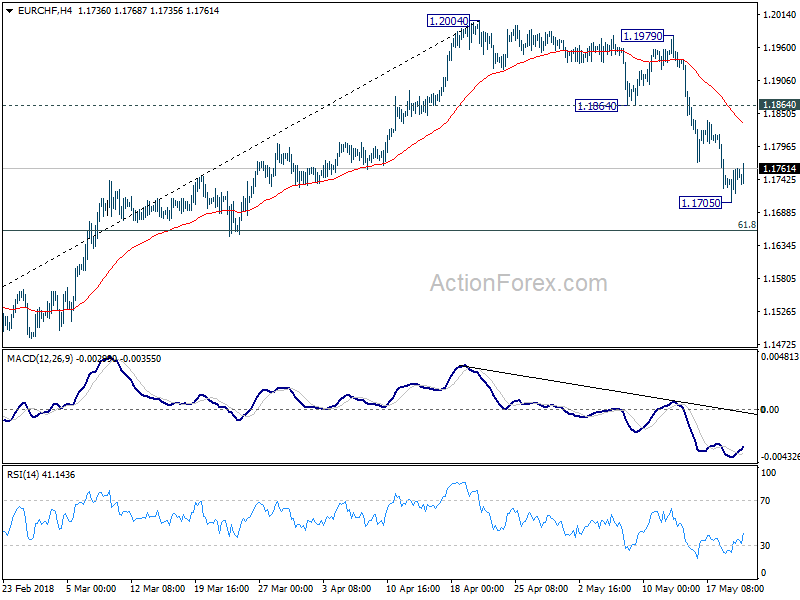

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1721; (P) 1.1743; (R1) 1.1781; More...

A temporary low is formed at 1.1705 in EUR/CHF with the current recovery. Intraday bias is turned neutral for consolidations. Upside of recovery should be limited by 1.1864 support turned resistance to bring another decline. Below 1.1705 will target 61.8% retracement of 1.1445 to 1.2004 at 1.1659. Sustained break will target key support level at 1.1445.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 could be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Hence, for now, deeper fall could be seen back to 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern.

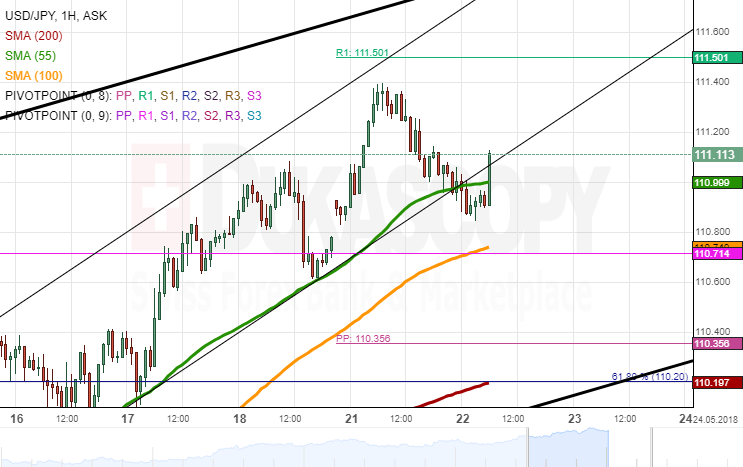

USD/JPY Analysis: Breaches Junior Pattern

Bulls guided USD/JPY during the first part of Monday, thus pushing the Greenback 43 pips higher against the Yen. This slight advantage was lost later in the day, following a bearish reversal from the 111.40 mark.

Due to this move, the pair failed to reach the upper boundary of a four-week channel up and subsequently fell below the junior pattern and the 55-hour SMA early today. From the theoretical perspective, a decline should follow.

A breakout of the 100-hour SMA and the monthly R1 at 110.70 would send the pair towards its next target of the 200-hour SMA, the weekly PP and the senior channel line at 110.20. In case the 110.70 area remains intact, the US Dollar should continue approaching the senior channel and the monthly R2 at 112.00 during the following days.

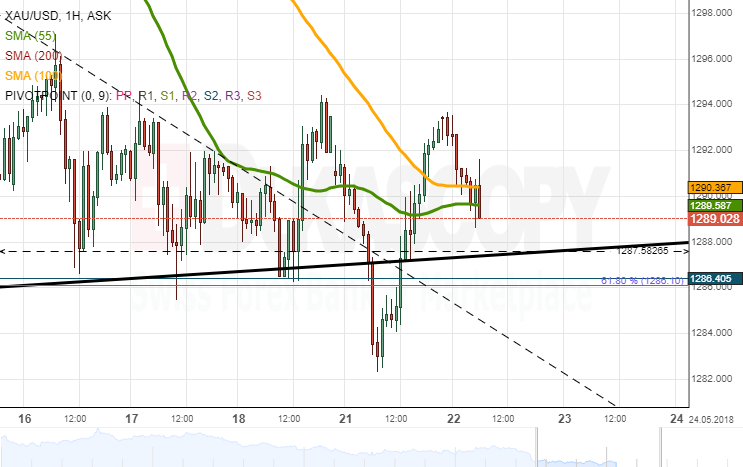

Gold Analysis: More Bullish Today

Following an upside breakout of the short-term triangle, Gold was expected to surge towards the 1,300.00 area. This scenario, however, was not fulfilled as the pair fell back again, made a false breakout from the senior channel and went for another surge on Monday.

Even though the 55- and 100-hour SMAs were breached during the second part of that session, the yellow metal failed to surpass the 1,295.00 mark which has provided strong resistance within the past week.

In general, the base scenario for today favours further advance up to the 1,300,00 mark, as the aforementioned moving averages could provide strong support. Meanwhile, it is unlikely that a fall goes beyond 1,280.00.

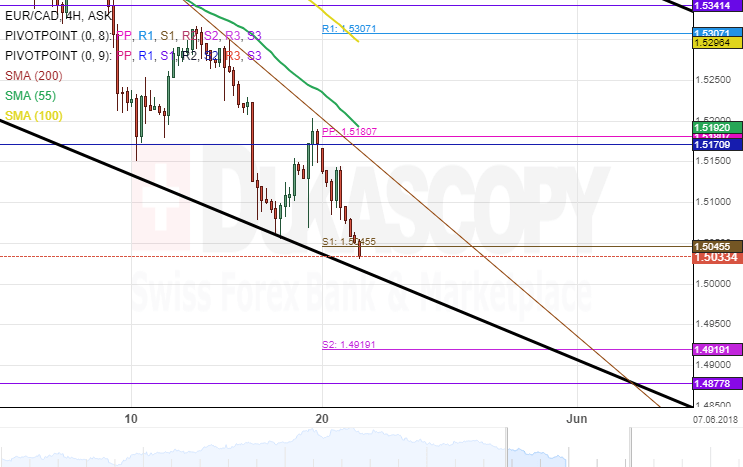

EUR/CAD 4H Chart: Reaches Five-Month Low Level

The common European currency movement against the Canadian Dollar has been guided by two months descending channel. The currency pair reversed from the upper boundary of a senior channel on March 20 and has since reached a five-month low level at 1.55.

During the past few weeks, the 55– hour simple moving average has been directing the price movement down. Meanwhile, the EUR/CAD currency pair has reached the lower boundary of a dominant descending pattern and could be set for a breakout within this session.

If and when the aforementioned breakout occurs, the currency exchange rate could start a second-round of decline during the following weeks.

China to put words into action by lowering passenger car levy

Bloomberg reported that China is going to lower levy on import passenger cars from the current 25% to 15%. That's seen as Chinese President Xi Jinping putting his word into actions. Xi has already reiterated the initiative at the Boao Forum back in April.

As in 2017, the total sales of automobiles in China added up to 28.9m. Only 1.22m, or 4.2%, are imported. The lowering of tariff is seen as a strong boost to European vehicle makers and less so the US ones.

For domestic car makers, the levy cut to 15% is the better case scenario in the rumored range of 10-15%.

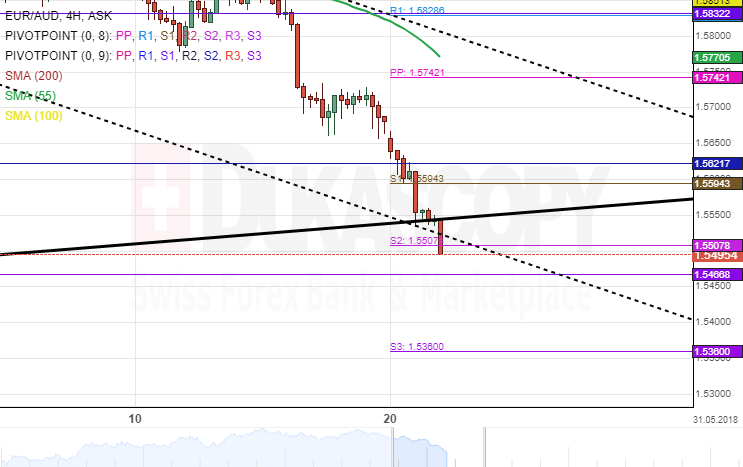

EUR/AUD 4H Chart: Pair Breaches Dominant Channel

The price movement of the EUR/AUD currency pair has been steered by a junior descending channel. The exchange rate has breached the lower boundary of a dominant ascending pattern on May 21 and this could indicate a long-term decline for the pair.

A strong resistance set by the 55– hour simple moving average has proved to have enough momentum to drive the rate further south. Furthermore, during this short period of decline, the pair has reached a five-month low level.

As for near future, it is likely that bears could continue their dominance in the market during the following trading sessions. However, a brief retracement to the upside is likely to occur within the next 48hrs.

EUR/USD Tested The 1.1718 Support Area

Markets

Yesterday, US and European Bond markets showed quite a different picture. US yields were little changed and held near recent highs. Markets didn't change their positive assessment on the US economy for the near future even as geopolitical tensions continue to linger. Positive investor sentiment was supported by comforting comments from US Treasury Secretary Mnuchin and from President Trump indicating that the trade talks between the US and China will continue and that the immediate threat of a trade war has eased. The picture in Europa was different. Bunds rallied and peripheral spreads widened sharply as markets still pondered the potential consequences of a populist government in Italy. Fitch rating agency warned that the policy of the new Government increases the risks to the country's credit profile. Markets were also worried on the potential consequences of the issuances of mini-BOT's . Italian 10-y yield spreads widened 22 bp to 187 bp. Portugal (+ 19 bp) and to a lesser extent Spain (+ 12 bp) also felt the fall-out from Italy. The Bund future jumped sharply higher. The move might have been slightly distorted as some European markets including Germany, were in holiday modus. Germany yields declined between 3.8 bp (2-year ) and 5.6 bp for the 10-year. Today, the eco calendar is thin. So global market sentiment will continue to drive bond trading. In the US, yields are holding within reach of the recent peaks, but the rise is slowing. Markets want clarity on the geopolitical issues and, even more, look out whether recent positive eco data will be confirmed. In Europe, there remains a lot of uncertainty on the exact path that the new Italian coalition will go. The uncertainty on Italy also trigged quite a sharp rebound in the Bund. The 159.69/42 resistance are is coming with reach. In yield terms, 0.47% support area is also again on the radar. A re-break would be highly significant from a technical point of view. The jury is still out, but for now, we assume that a break won't be evident.

Yesterday, uncertainty on Italy initially also weighed on the euro. EUR/USD tested the 1.1718 support area. However, a break didn't occur and this helped to put a floor for the single currency. Later in the session, EUR/USD even reversed the initial decline and close the session with a small gain at 1.1791. So, the performance of the euro clearly was more constructive compared to the developments on the on the European bond markets. There was probably also some USD profit taking at work as USD/JPY drifted back south from an intraday top near 111.40 back to the 111 area. Today, eco data will probably again only be of second tier importance. Uncertainty on Italy will probably continue to dominated trading on European markets. If the spread widening in Italy were to ease and the decline in German yields slows, it might not be that easy for EUR/USD to break the 1.17 support area short-term.

Yesterday, sterling didn't profit from the uncertainty on Italy. Global uncertainty and rumours that at least part of the Conservative party is considering the idea of new snap elections, probably weighed on sterling. EUR/GBP rebounded back higher in the 0.87big figure. Cable touched a new correction low below 1.34. Today, the UK monthly budget data and the CBI retail data will be published. Several BoE members including governor Carney will attend a Parliamentary hearing on the inflation report. A constructive tone from the BoE might be slightly sterling supportive.

News Headlines

Italy's anti-establishment Five Star Movement and the far-right League have proposed Giuseppe Conte, a civil lawyer and academic, as the country's new prime minister to lead their populist government. (FT) Meanwhile, rating agency Fitch warns Italy's new government (policy) would increase risks to the country's sovereign credit profile.

US Treasury Secretary Steven Mnuchin declared the US-China trade war "on hold" after Beijing vaguely promised to buy more American agriculture and energy exports. On the other hand, Mike Pompeo, the US Secretary of State, threatened Iran with the "strongest sanctions in history". However, the US remains open to a new deal that should entail amongst others the shutdown of any enrichment of uranium.

BOE Governor To Testify Before Treasury Committee This Morning

At 08:15 GMT, UK MPC Member Vlieghe is due to testify at his parliamentary reappointment hearing before the Treasury Committee, in London. GBP volatility can increase during this event.

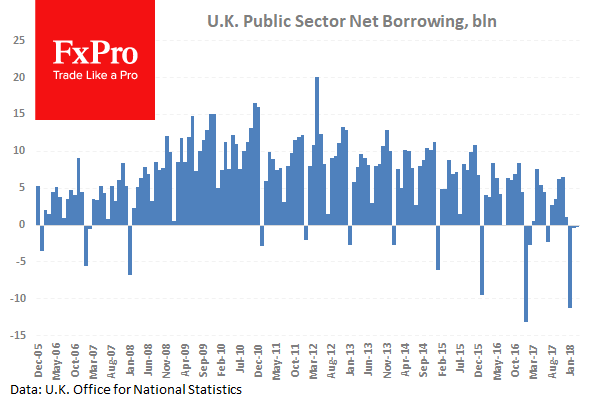

At 08:30 GMT, UK Public Sector Net Borrowing (Apr) is expected to be £7.000B against a previous £-0.262B. This shows a surplus in the figures for April. The surpluses have been decreasing and trend down since peaking in 2010. GBP crosses may react to this data release.

At 08:15 GMT, UK MPC Member Vlieghe is due to testify at his parliamentary reappointment hearing before the Treasury Committee, in London. GBP volatility can increase during this event.

At 08:30 GMT, UK Public Sector Net Borrowing (Apr) is expected to be £7.000B against a previous £-0.262B. This shows a surplus in the figures for April. The surpluses have been decreasing and trend down since peaking in 2010. GBP crosses may react to this data release.

At 20:30 GMT, API Weekly Crude Oil Stock data will be released. Last week this data showed a build of 4.854M. With Oil prices back to 2014 levels any indication of price movement will be closely watched. Traders will take note of this data ahead of EIA Survey data on Wednesday. WTI Oil price volatility can increase during this event.

EU Malmstrom reiterated US should end steel tariff threats

EU trade Commissioner Cecilia Malmstrom reiterated today that the US should end the steel tariff threats to the EU. And EU's position is clear that there would be discussion of closer trade ties only if EU is granted permanent exemptions from the steel tariffs. However, Malmstrom also noted that "they don't think it is enough", referring to the lack of response from the US.

Separately, German economy minister Peter Altmaier urged more work on trade deal with the US as time is running out for a deal over the steel tariffs.

The current temporary exemption for EU will expire on June 1.