Sample Category Title

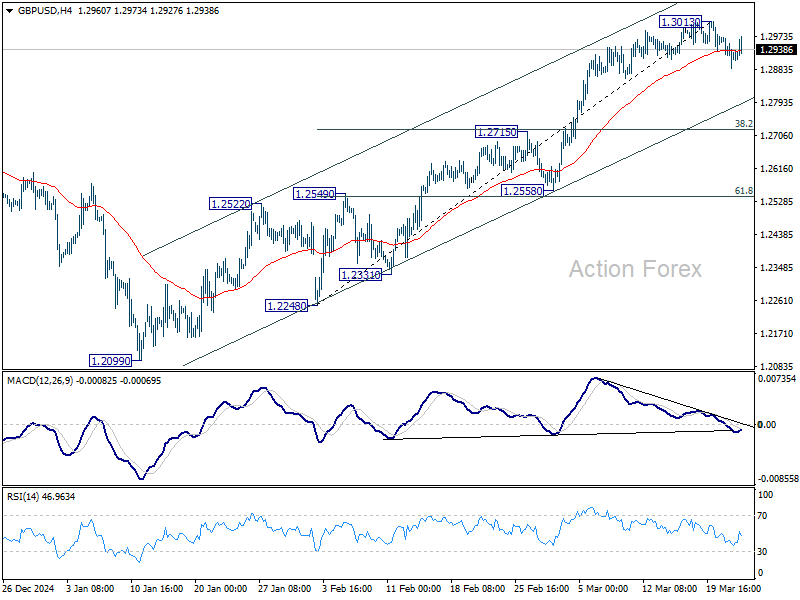

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2878; (P) 1.2926; (R1) 1.2965; More...

Intraday bias in GBP/USD stays mildly on the downside despite today's recovery. Correction from 1.3013 short term top would extend to 38.2% retracement of 1.2248 to 1.3013 at 1.2721. Strong support should be seen there to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099.

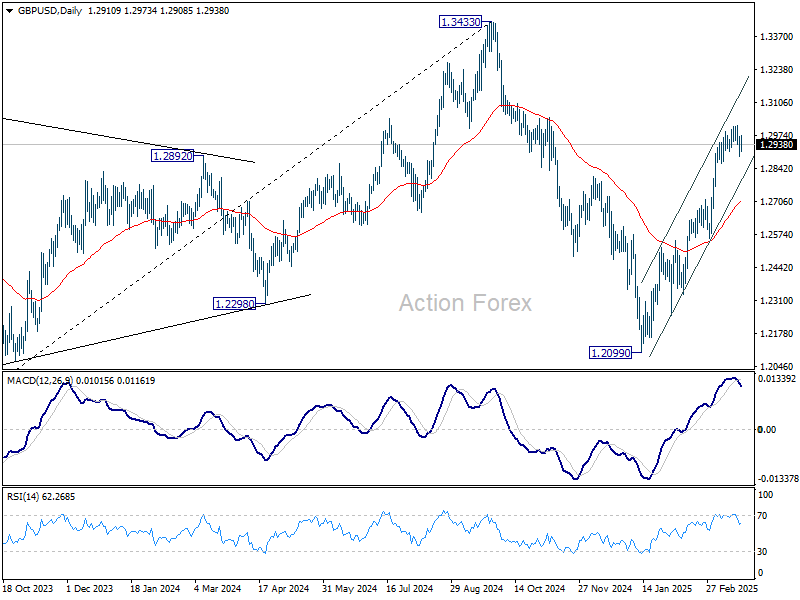

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

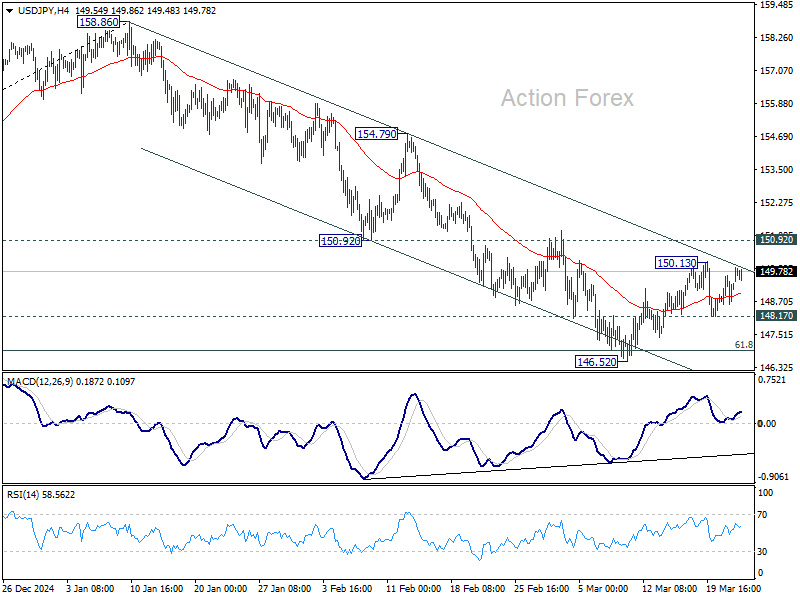

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.71; (P) 149.19; (R1) 149.79; More...

Intraday bias in USD/JPY remains neutral for the moment. Recovery from 146.52 is seen as a corrective move. In case of stronger rise, upside should be limited by 150.92 support turned resistance. On the downside, break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support.

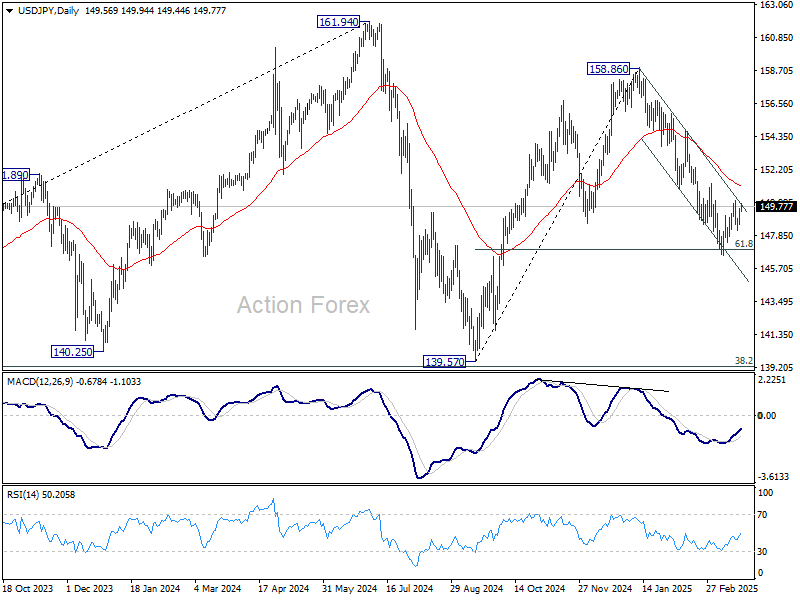

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

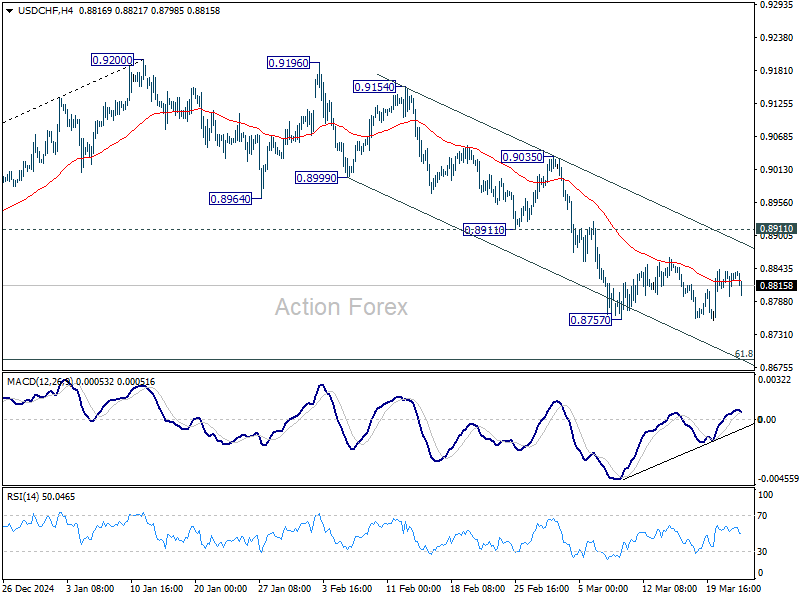

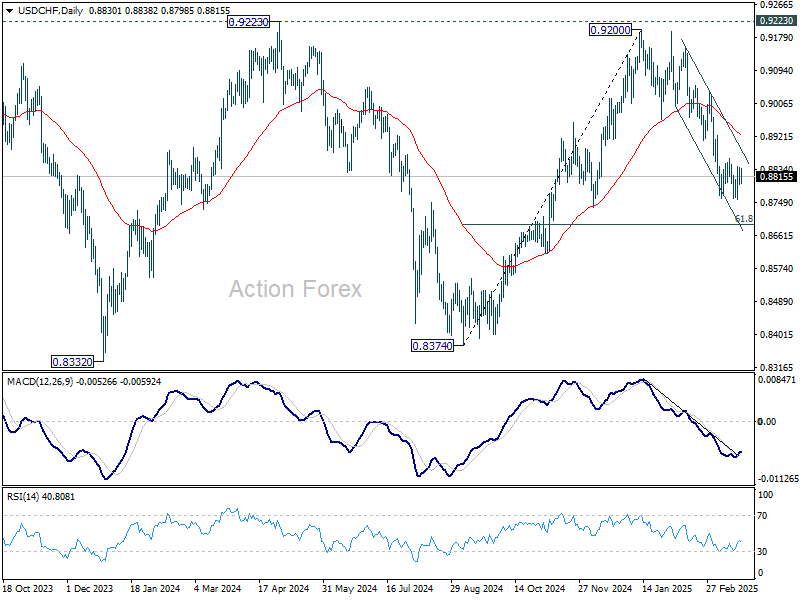

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8805; (P) 0.8823; (R1) 0.8849; More…

No change in USD/CHF's outlook as consolidations continue in established range above 0.8757. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

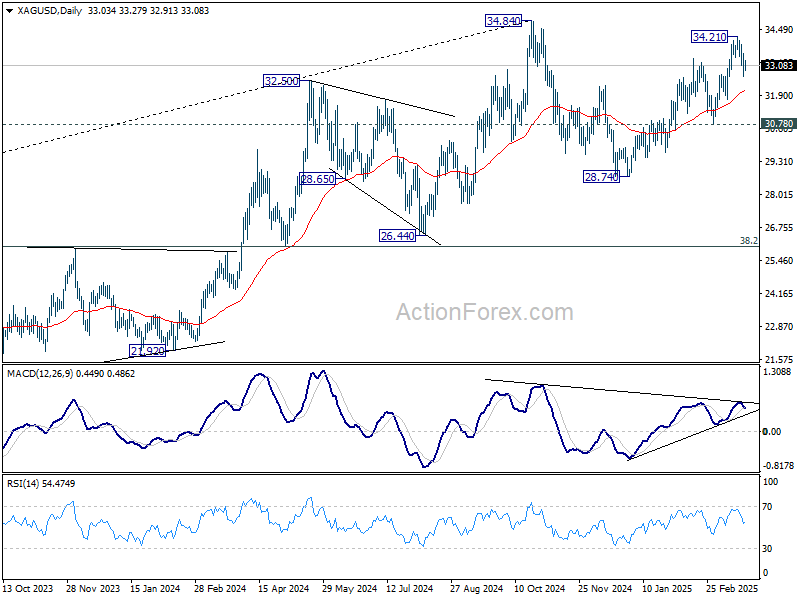

Markets Driven by PMI Data and Tariff Speculations, Silver at Risk of Reversal

Market sentiment today is largely influenced by a mix of global PMI releases and ongoing uncertainty around US tariff policy. There are reports suggesting the Trump administration may exclude a set of sector-specific tariffs from the sweeping reciprocal levies set to begin on April 2. US futures are pointing to a solid open, suggesting investors are hoping for a more surgical, less disruptive approach to trade action.

However, clarity is still lacking. It’s unclear whether excluded sectors will be spared entirely or if reciprocal tariffs will blanket all imports, with sectoral levies added on top later. Despite the ambiguity, sentiment has been lifted, with US futures pointing to a solid open.

European currencies are also finding some support alongside gains in regional equities. However, upside in both Euro and Sterling is capped by mixed PMI data. In the Eurozone, manufacturing showed a smaller contraction and even a bounce in output, signaling green shoots. Yet, service sector growth lost momentum, adding to the sense of an uneven recovery. In the UK, services surprised with strong growth, but manufacturing activity deteriorated sharply, dragging down the overall tone of the report.

Meanwhile, Australia outperformed, with both sectors registering improvements and supporting Aussie’s strength today. On the other hand, Yen is under pressure as Japan’s services PMI fell into contraction territory, raising concerns about domestic demand and the broader economic outlook.

Currency performance reflects this divergence. Aussie is currently the strongest performer for the day, followed by Sterling and Swiss Franc. At the bottom of the table, Yen leads losses, followed by Kiwi and Dollar. Loonie and Euro sit in the middle of the pack.

Technically, Silver could have formed a short term top at 34.21, ahead of 34.84 resistance. Break of 55 D EMA (now at 32.07) will suggest that rebound from 28.74 has already completed. Further break of 30.78 support will indicate that corrective pattern from 34.84 has already started the third leg back to 28.74 support and possibly below.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is down -0.06%. CAC is down -0.12%. UK 10-year yield is up 0.001 at 4.723. Germany 10-year yield is up 0.028 at 2.797. Earlier in Asia, Nikkei fell -0.18%. Hong Kong HSI rose 0.91%. China Shanghai SSE rose 0.15%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.028 to 1.545.

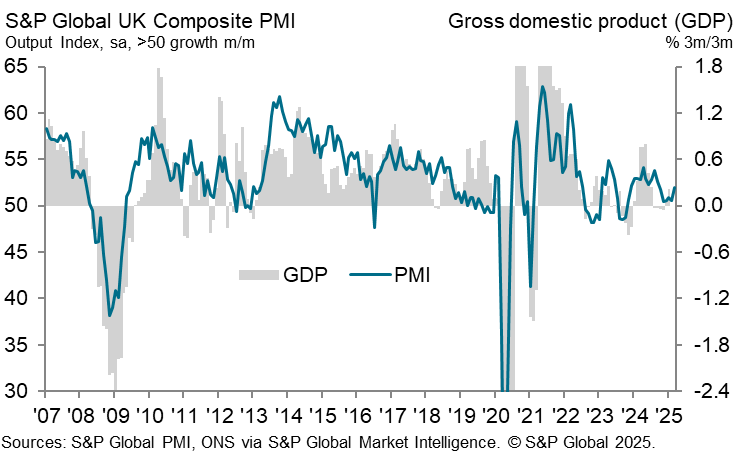

UK PMI manufacturing falls to 44.6, while services rises to 53.2

UK delivered a mixed set of PMI readings in March, with services providing a welcome surprise as the index rose from 51.0 to 53.2, a 7-month high. PMI Composite also improved from 50.5 to 52.0, suggesting modest expansion. However, the picture was clouded by a sharp deterioration in manufacturing, where the index slumped from 46.9 to 44.6 — its lowest level in 18 months.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, cautioned against over-optimism, noting that “one good PMI doesn’t signal a recovery.”

The data points to the economy barely expanding, with GDP growth tracking around 0.1% for the quarter. Employment continues to be trimmed as firms remain wary of rising costs and an uncertain economic outlook, with business confidence still hovering near January’s two-year low.

Looking ahead, challenges appear to be mounting. Businesses are bracing for higher National Insurance contributions starting in April,. Additionally, the anticipated unveiling of US tariff policy on April 2 adds another uncertainty.

ECB’s Cipollone: Case for rate cuts strengthens amid falling energy, rising Euro and trade risks

ECB Executive Board member Piero Cipollone struck a dovish tone in an interview with Expansión, signaling that recent developments have reinforced the case for further interest rate cuts.

Cipollone noted that at the time of the March meeting, ECB projections already showed inflation converging to the 2% target by early 2026—even under a rate path that included market expectations of cuts below 2%.

Since then, "not only has this narrative been confirmed, but key issues have arisen that have strengthened the arguments in favour of continuing to lower rates", he added.

Cipollone noted that energy price pressures have already begun to reverse. Meanwhile, Euro appreciation and higher real interest rates are working in tandem to cool price growth.

If US tariffs on European goods materialize, that would have a "negative impact on demand", which would "further strengthen the downward trend in inflation". Similarly, escalating U.S.-China trade conflict may push Chinese goods into Europe, adding to price suppression across the bloc.

Notably, Cipollone suggested that inflation could reach target even sooner than the ECB’s latest projections anticipate.

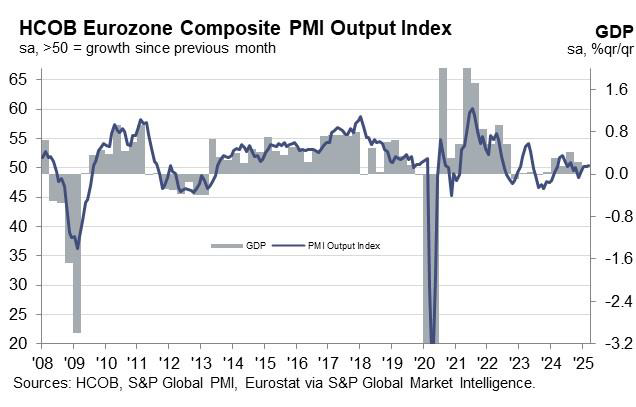

Eurozone PMI hints at green shoots, manufacturing leads the way

Eurozone PMI data for March offered fresh signs of economic stabilization, with Composite index rising to a 7-month high of 50.4, supported by a notable rebound in manufacturing. The PMI Manufacturing rose from 47.6 to 48.7, its highest level in 26 months. Manufacturing output crossed into expansion territory at 50.7, a 34-month high. Services PMI slipped slightly from 50.6 to 50.4, but remained in growth territory.

Cyrus de la Rubia of Hamburg Commercial Bank noted the possibility that "temporary tariff-related import boom" could be inflating manufacturing figures. But he also expressed optimism that with, Europe’s investment drive in defense and infrastructure, "hope for a more sustained recovery seems well founded".

Encouragingly for ECB, pricing pressures in the services sector are easing, with both input costs and output prices decelerating. In manufacturing, price pressures remain moderate as well, helped by falling energy costs.

However, risks remain. Potential retaliation tariffs from the US, trade tensions with China, and higher food prices caused by extreme weather events are all sources of uncertainty that could cloud the outlook and "make some ECB members hesitant to cut rates too aggressively."

BoJ’s Ueda reaffirms commitment to rate hikes despite market and financial pressures

BoJ Governor Kazuo Ueda told parliament today that the central bank remains committed to raise interest rate if underlying inflation is deemed to be approaching its 2% target.

He emphasized that BoJ’s objectives remain squarely focused on price stability, and that its approach to policy "would not be disturbed by considerations for the BoJ's finances."

Ueda’s remarks come as concerns mount over the BoJ’s balance sheet in light of interest rate hikes and volatility in equity markets.

BoJ estimated in December that if short-term borrowing costs were to rise to 2%, it could incur losses of up to JPY 2 trillion.

Additionally, Ueda noted that a 1000-point drop in the Nikkei 225 index would translate into a valuation loss of about JPY 1.8 trillion in its ETF holding.

While these figures highlight the scale of financial risks, Ueda’s insistence on prioritizing price stability signals that BoJ is prepared to weather market volatility in pursuit of its monetary policy mandate.

Japan PMI composite falls to 48.5, business confidence sinks to lowest since 2020

Japan’s private sector saw a sharp loss in momentum at the end of Q1, with PMI Composite falling from 52.0 to 48.5, marking the first contraction in five months. PMI Manufacturing dropped from 49.0 to 48.3, its lowest in a year and ninth consecutive month in contraction. More concerning was the steep decline in PMI services, which fell from 53.7 to 49.5 — the weakest reading since mid-2024.

According to Annabel Fiddes of S&P Global, the downturn was driven by a "fresh fall in service sector activity" and an accelerated decline in manufacturing. Firms pointed to "strong inflationary pressure had dampened sales", with clients showing increasing hesitation to place orders.

The broader picture is one of growing pessimism. Japanese firms cited a host of structural and cyclical challenges — from persistent inflation and labor shortages to an aging population and deepening global trade uncertainty. As a result, business confidence for future activity fell to its lowest level since August 2020.

Australia's PMI manufacturing jumps to 52.6, services rises to 51.2

Australia’s PMI Manufacturing surged to 52.6 from 50.4—marking a 29-month high—while PMI Services ticked up to 51.2 from 50.8. PMI Composite , which combines both sectors, rose to a 7-month high at 51.3.

Jingyi Pan of S&P Global Market Intelligence highlighted that the output growth was not only the strongest in seven months but also "broad-based" across both manufacturing and services. Despite a decline in export orders due to weather disruptions and weak global conditions, domestic demand rebounded impressively, pushing new orders to their highest growth rate in nearly three years.

However, the report also highlighted a notable dip in business confidence. Suppressed price increases may have helped support near-term demand. But "tariff uncertainty may continue to cast a shadow on output growth in the year ahead".

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8805; (P) 0.8823; (R1) 0.8849; More…

No change in USD/CHF's outlook as consolidations continue in established range above 0.8757. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

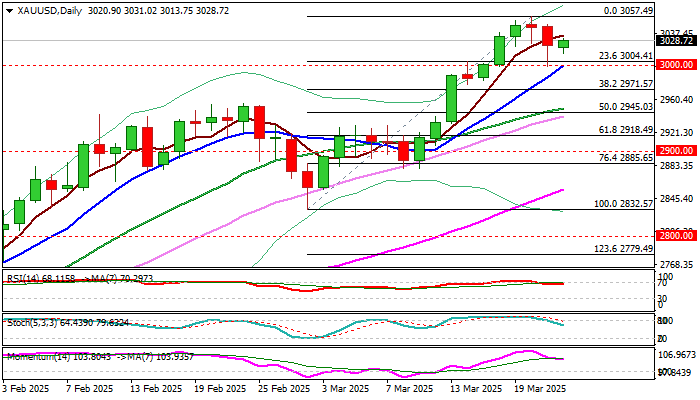

Will Gold Take a Breather After a Three-Week Rally?

- Gold slows moderately after hitting an all-time high of 3,057.

- Price finds support near 3,000, but technical signals flag caution.

- Bulls may need a close above 3,067 to attract new buyers.

Gold opened neutral around Friday’s closing price of 3,023 as the final trading week of March kicked off. The precious metal moved to the sidelines as investors speculated that Trump’s reciprocal tariffs would be less punitive than previously expected – likely excluding some countries and avoiding sector-specific barriers.

However, the bounce near the psychological 3,000 mark revealed that demand for safe-haven assets remains intact, while expectations of further rate cuts in the US also helped support prices.

Still, with the RSI and the stochastic oscillator tilting south after peaking in the overbought zone, questions arise about how long gold can maintain its footing after a strong three-week bullish streak.

The constraining line from February at 2,993 could provide protection in the coming sessions if downside pressures resurface. If not, the bears could push the price toward the crucial 2,930-2,950 zone, where the 20-day simple moving average (SMA) and the tentative support trendline from January are positioned. A break below this level would weaken the short-term outlook and likely trigger a stronger selling wave toward the 50-day SMA, currently at 2,875.

On the upside, a sustainable move above 3,067 may activate fresh buying orders, bringing the 3,100 round level next into view. A continuation higher could then challenge the 261.8% Fibonacci extension of the previous decline at 3,155.

Summing up, gold’s positive momentum may take a breather in the coming sessions. However, only a drop beneath 2,930-2,950 would make the current uptrend less credible.

Gold: Key $3,000 Support So Far Holds Pullback from New Record High

Gold holds within a narrow range at the beginning of the week but remains constructive above $3000 level (psychological / 10DMA).

Recent pullback from new historical high ($3057) found firm ground at $3000 which was highlighted as strong support, with Friday’s strong rejection here, adding to significance of support.

Near-term action so far looks as consolidation ahead of fresh push higher after bullish stance was reinforced by weekly close above $3000.

Technical studies remain firmly bullish on daily chart, though overbought conditions may keep the price in prolonged consolidation, with potential dips below $3000 not ruled out.

Fundamentals are expected to remain a key driver, with hawkish Fed (kept rates on hold and signaled two 25bp rate cuts in 2025), escalating geopolitical situation and gloomy economic outlook, including threats that escalating trade war would fuel inflation, to continue to boost safe haven demand.

On the other hand, hope that peace talks between USA, Russia and Ukraine would give some results and ease tensions, along with the latest softer rhetoric from President Trump regarding tariffs (due to be imposed on Apr 2) would contribute to easing high uncertainty and negatively slow migration into safety.

Near term action is to remain biased higher while $3000 support holds, with sustained break above cracked $3029 barrier (50% retracement of $3057/$2999 pullback) needed to verify bullish signal.

Conversely, loss of $3000 handle would sideline bulls and open way for deeper pullback, which should find footstep above $2971 (Fibo 38.2% of $2832/$3057 bull-leg) to mark a healthy correction and keep larger bulls intact.

Res: 3035; 3047; 3057; 3079.

Sup: 3013; 3000; 2971; 2956.

EURNZD: NZD Facing Structural Weaknesses

- Interest Rate Outlook: Markets price the Official Cash Rate (OCR) above 3%, but risks suggest lower rates may be needed due to spare economic capacity.

- Economic Growth: Q4 GDP growth of 0.7% exceeded expectations but included one-off factors unlikely to persist.

- Inflation Risks: With high spare capacity (~ -1.5% output gap), disinflation remains a concern, increasing the risk of rates undershooting market expectations.

Fundamental Factors Affecting NZD

- Growth Outlook: While NZ is technically out of recession, the underlying recovery remains weak, with low consumption growth (0.1%) and a declining residential investment sector.

- Labour Market & Inflation: Unemployment has yet to peak, and inflation is close to target, meaning the RBNZ may need to keep rates neutral for longer or even cut below 3%.

- Housing Market: 44% of mortgages are fixed for six months or less, meaning homeowners may benefit from lower fixed rates. However, it is unclear whether rising unemployment will boost spending.

- External Factors: Higher commodity prices support exports, but global trade tariffs could slow growth.

- Political & Policy Uncertainty:

- RBNZ forecasts above-trend growth (2.6%)—which may be optimistic given trade risks.

- Political uncertainty, including the departure of RBNZ Governor Adrian Orr, adds to volatility.

Key Takeaway for Traders

- NZD downside risks remain as economic slack persists, and rate cuts below 3% are possible.

- Watch for inflation undershooting in the coming months. If confirmed, the RBNZ may need a longer period of neutral or lower rates, pressuring the NZD.

- Housing stabilization and strong exports could provide limited upside, but overall growth is unlikely to remove spare capacity quickly.

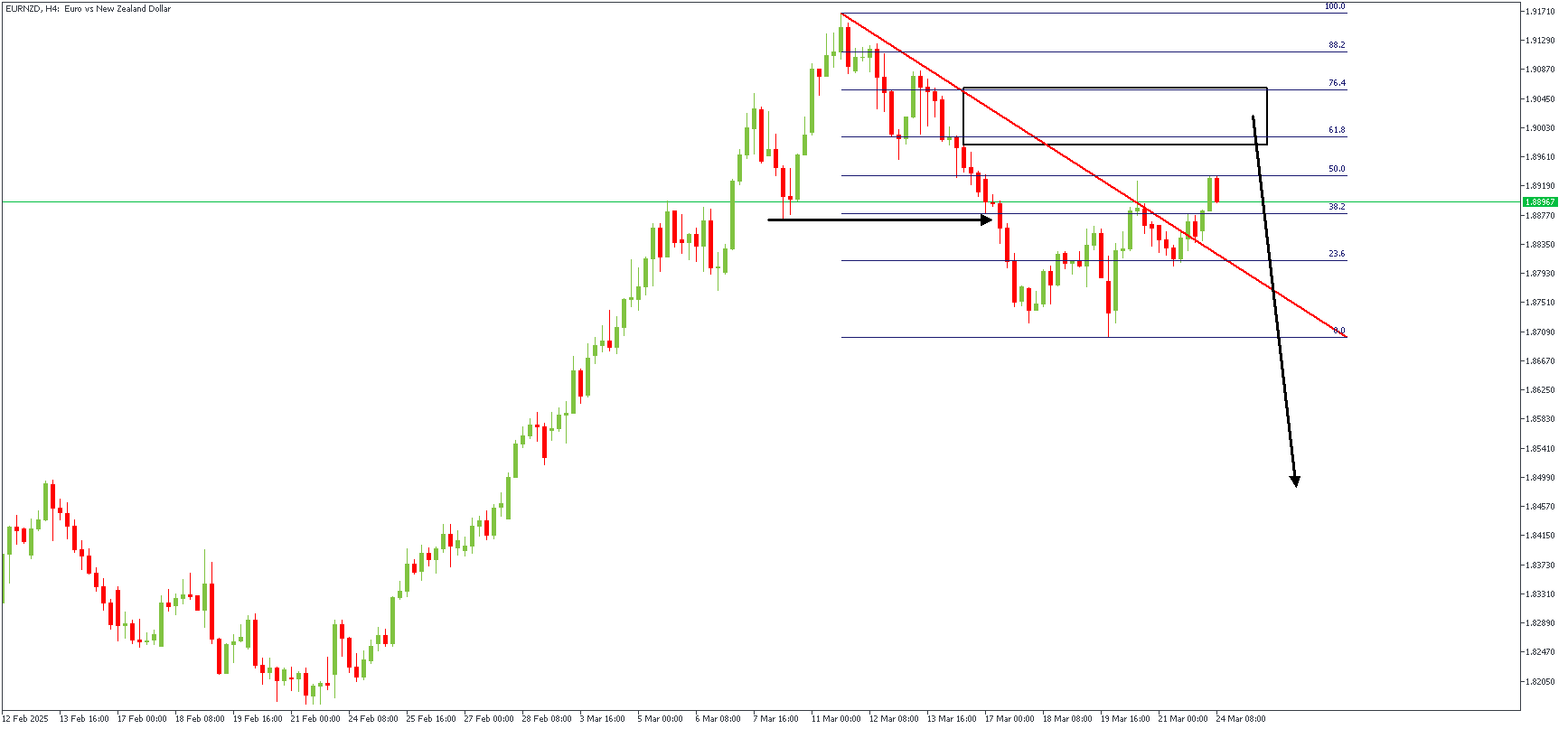

EURNZD – H4 Timeframe

Following the bearish break of structure on the 4-hour timeframe chart of EURNZD, the Fibonacci retracement tool was plotted, with levels 61% to 88% being the significant areas of focus. The subsequent retracement is approaching the supply zone that overlaps the 61.8% retracement level after having swept liquidity from the previous internal structure, leading to a bearish sentiment.

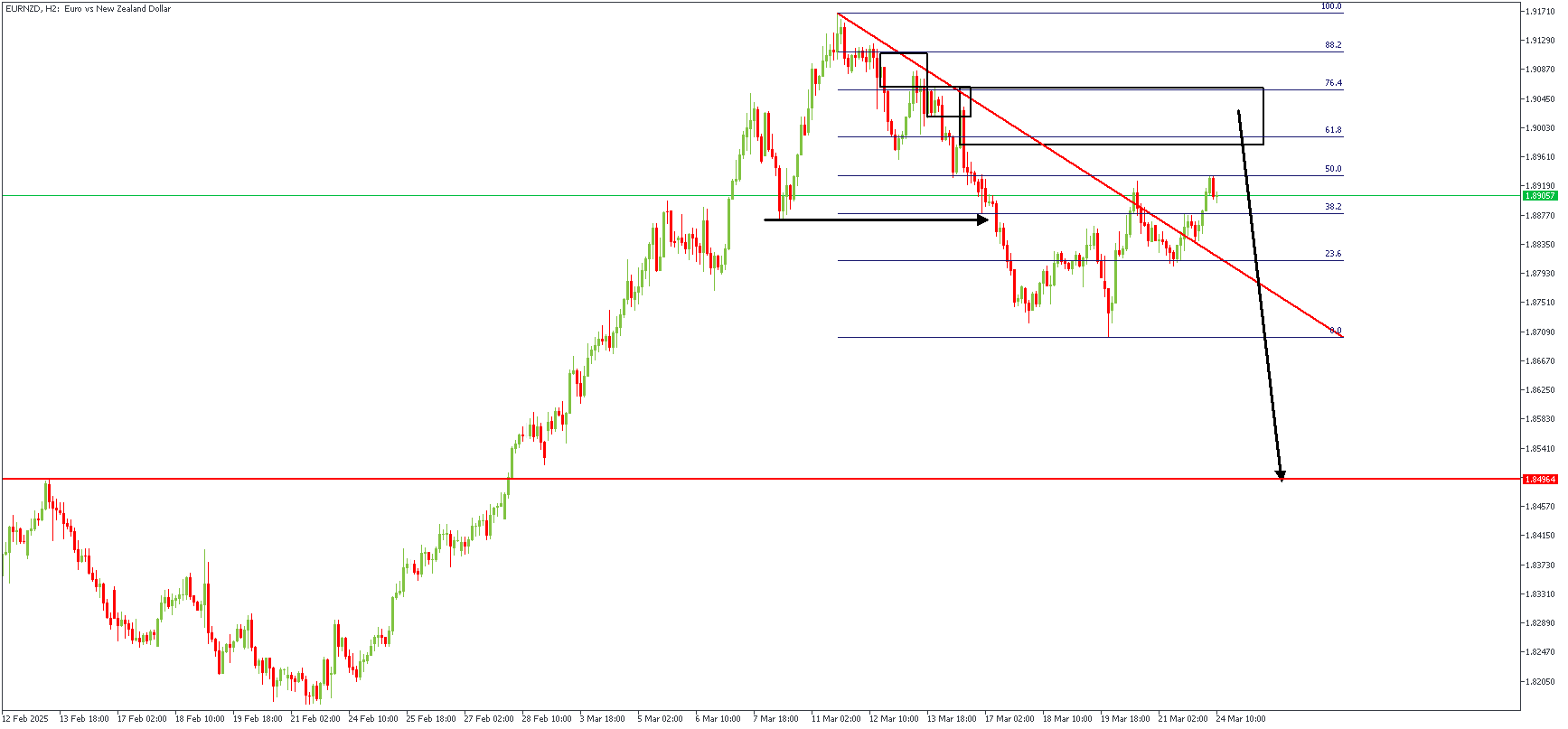

EURNZD – H2 Timeframe

The price action on EURNZD's 2-hour timeframe chart validates the 4-hour timeframe sentiment by revealing the FVG (Fair Value Gap) that the price is expected to fill before being rejected from the supply zone.

Analyst's Expectations:

- Direction: Bearish

- Target- 1.84964

- Invalidation- 1.91228

UK PMI manufacturing falls to 44.6, while services rises to 53.2

UK delivered a mixed set of PMI readings in March, with services providing a welcome surprise as the index rose from 51.0 to 53.2, a 7-month high. PMI Composite also improved from 50.5 to 52.0, suggesting modest expansion. However, the picture was clouded by a sharp deterioration in manufacturing, where the index slumped from 46.9 to 44.6 — its lowest level in 18 months.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, cautioned against over-optimism, noting that “one good PMI doesn’t signal a recovery.”

The data points to the economy barely expanding, with GDP growth tracking around 0.1% for the quarter. Employment continues to be trimmed as firms remain wary of rising costs and an uncertain economic outlook, with business confidence still hovering near January’s two-year low.

Looking ahead, challenges appear to be mounting. Businesses are bracing for higher National Insurance contributions starting in Apri. Additionally, the anticipated unveiling of US tariff policy on April 2 adds another uncertainty.

Eurozone PMI hints at green shoots, manufacturing leads the way

Eurozone PMI data for March offered fresh signs of economic stabilization, with Composite index rising to a 7-month high of 50.4, supported by a notable rebound in manufacturing. The PMI Manufacturing rose from 47.6 to 48.7, its highest level in 26 months. Manufacturing output crossed into expansion territory at 50.7, a 34-month high. Services PMI slipped slightly from 50.6 to 50.4, but remained in growth territory.

Cyrus de la Rubia of Hamburg Commercial Bank noted the possibility that "temporary tariff-related import boom" could be inflating manufacturing figures. But he also expressed optimism that with, Europe’s investment drive in defense and infrastructure, "hope for a more sustained recovery seems well founded".

Encouragingly for ECB, pricing pressures in the services sector are easing, with both input costs and output prices decelerating. In manufacturing, price pressures remain moderate as well, helped by falling energy costs.

However, risks remain. Potential retaliation tariffs from the US, trade tensions with China, and higher food prices caused by extreme weather events are all sources of uncertainty that could cloud the outlook and "make some ECB members hesitant to cut rates too aggressively."

XBR/USD Analysis: Price Near Resistance Zone

As seen on the XBR/USD chart, Brent crude oil prices are hovering near last week’s highs this morning as market participants assess various influencing factors, including:

→ New U.S. sanctions on Iran, which are limiting its export capacity and tightening global supply, particularly to China.

→ Ongoing negotiations between the U.S., Ukraine, and Russia in Saudi Arabia, which could potentially lead to increased Russian oil exports.

→ OPEC+ plans to raise oil production starting in April.

Technical Analysis of XBR/USD

From a technical perspective, Brent crude oil is trading near a key resistance zone, which consists of:

→ A bearish Fair Value Gap (highlighted in purple).

→ The upper boundary of the descending channel.

→ The upper boundary of a narrowing triangle (shown in black), which can be interpreted as a Rising Wedge pattern.

The Rising Wedge may represent a corrective rebound within a broader bearish trend. If buyers fail to break through this resistance zone, Brent crude prices could resume their downtrend within the red channel.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.