Sample Category Title

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4322; (P) 1.4348; (R1) 1.4381; More...

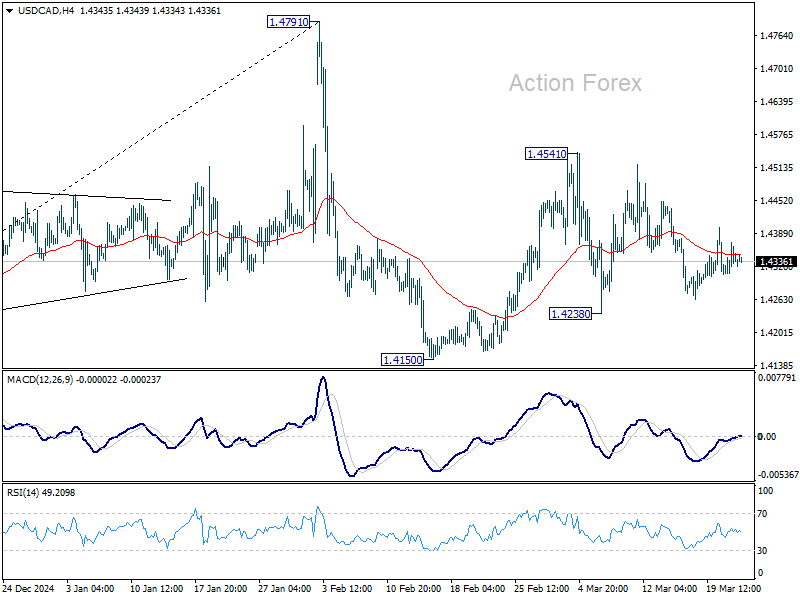

Intraday bias in USD/CAD remains neutral for the moment as range trading continues. Overall, price actions from 1.4791 are seen as a corrective pattern. On the upside, break of 1.4541 will extend the second leg from 1.4150 to retest 1.4791 high. On the downside, break of 1.4238 will argue that the third leg has already started through 1.4150 support.

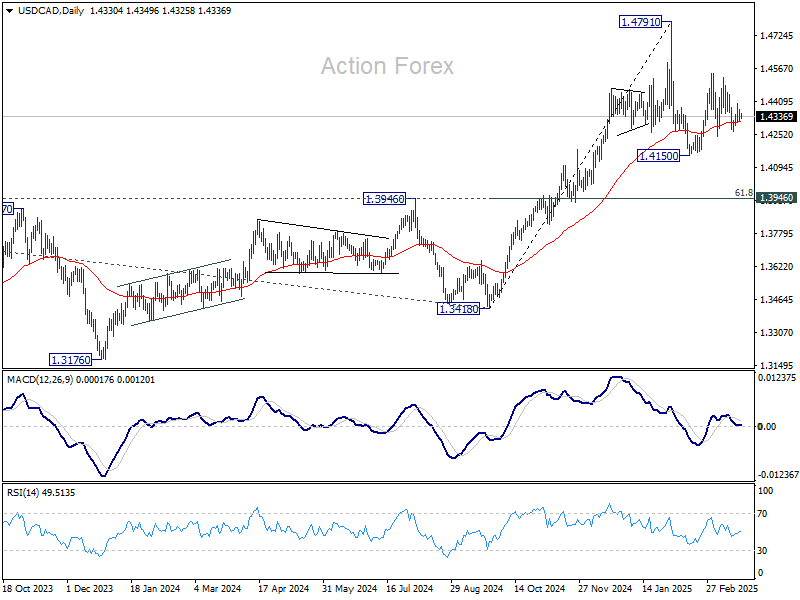

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

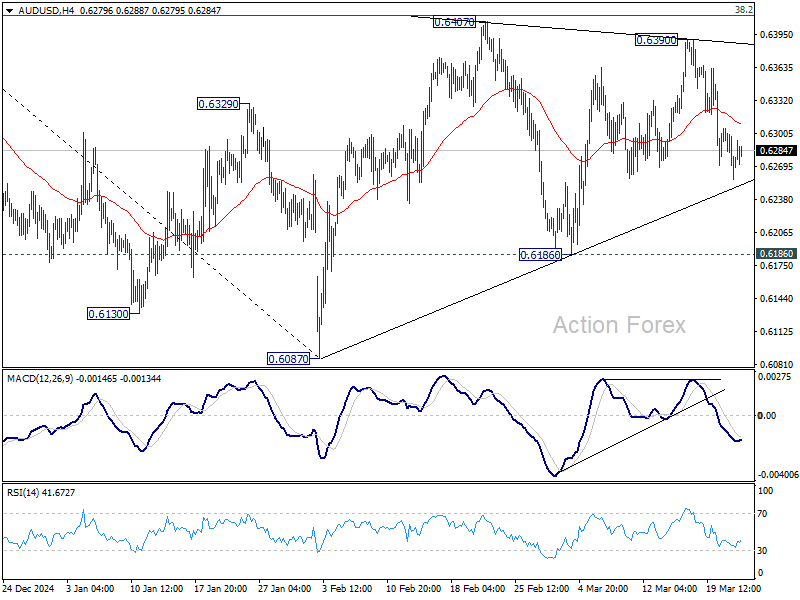

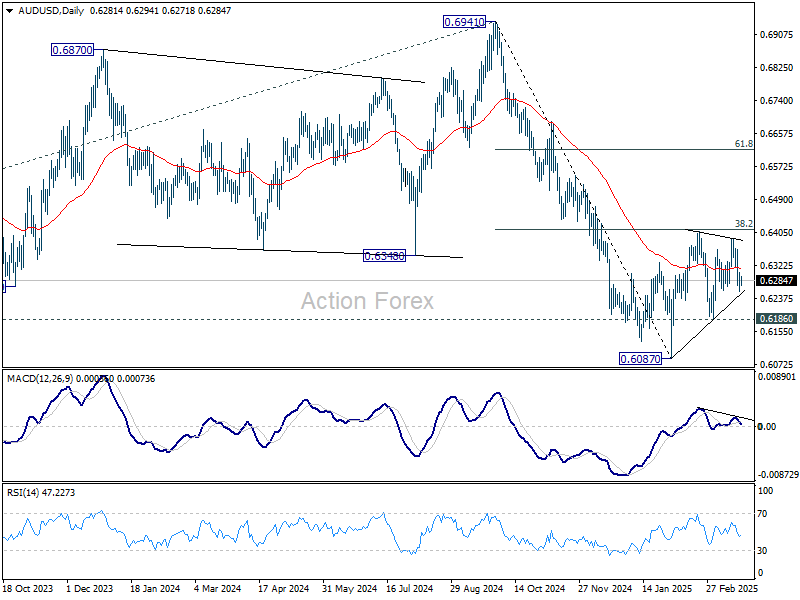

AUD/USD Daily Report

Daily Pivots: (S1) 0.6252; (P) 0.6279; (R1) 0.6300; More...

Intraday bias in AUD/USD stays neutral for the moment. On the downside, firm break of near term trend line support (now at 0.6250) will argue that corrective pattern from 0.6087 has already completed. Intraday bias will be back on the downside for 0.6186 support. Further break there will solidify this bearish case and target 0.6087 low. For now, in case of another rise, upside should be limited by 38.2% retracement of 0.6941 to 0.6087 at 0.6413.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6467) holds.

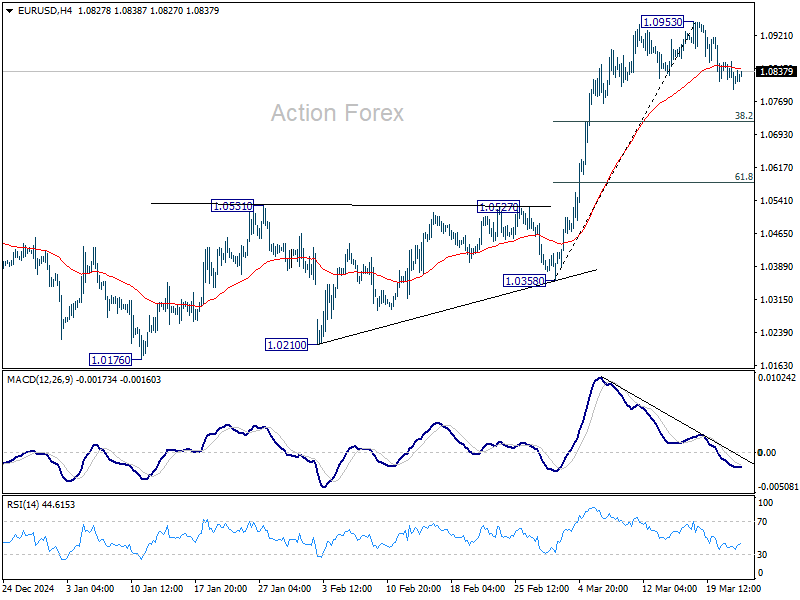

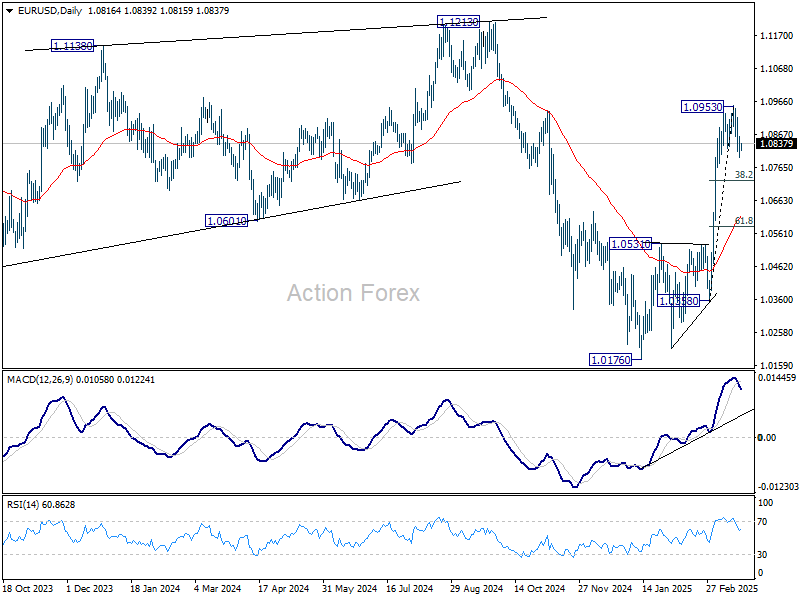

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0787; (P) 1.0824; (R1) 1.0852; More...

Intraday bias in EUR/USD remains mildly on the downside for the moment. Correction from 1.0953 short term top would extend to 38.2% retracement of 1.0358 to 1.0953 at 1.0726. Strong support should be seen there to bring rebound. On the upside, break of 1.0953 will resume the rally from 1.0176 towards 1.1274 key resistance.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

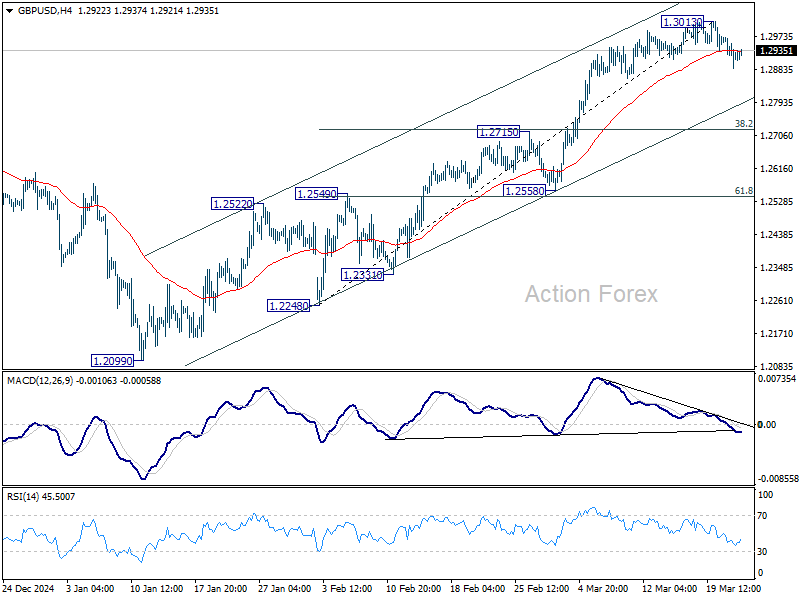

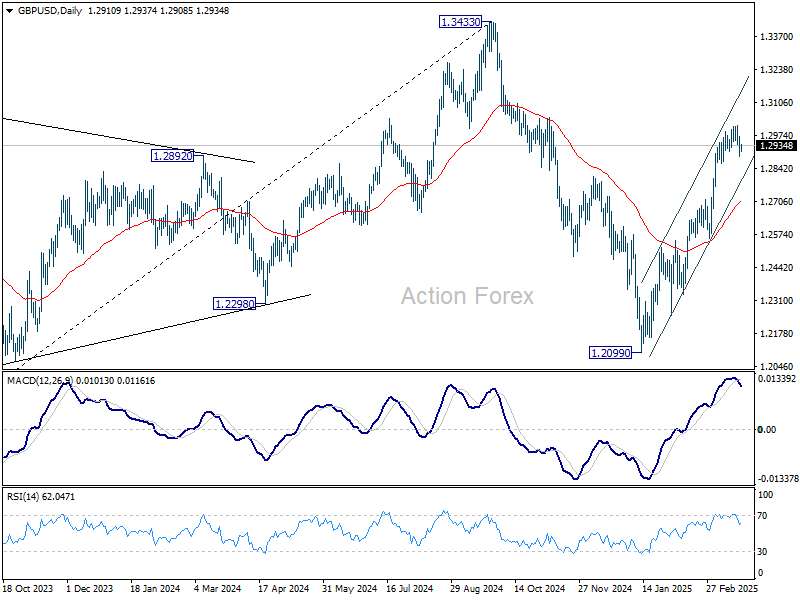

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2878; (P) 1.2926; (R1) 1.2965; More...

Intraday bias in GBP/USD stays mildly on the downside for the moment. Correction from 1.3013 would extend to 38.2% retracement of 1.2248 to 1.3013 at 1.2721. Strong support should be seen there to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

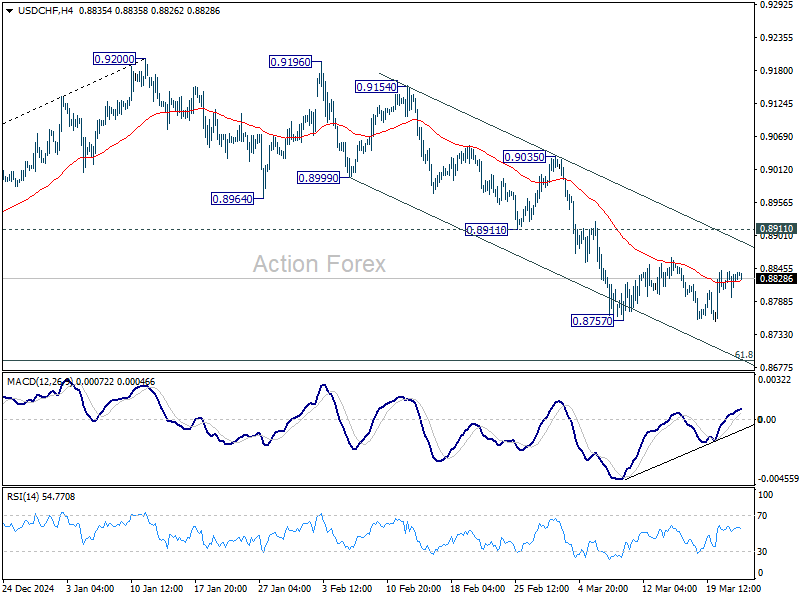

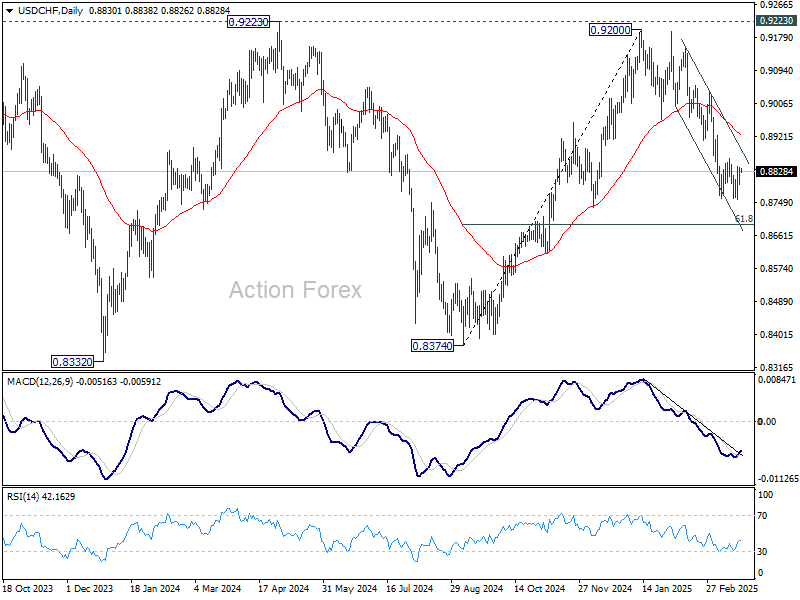

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8805; (P) 0.8823; (R1) 0.8849; More…

Intraday bias in USD/CHF remains neutral as consolidations continue above 0.8757. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

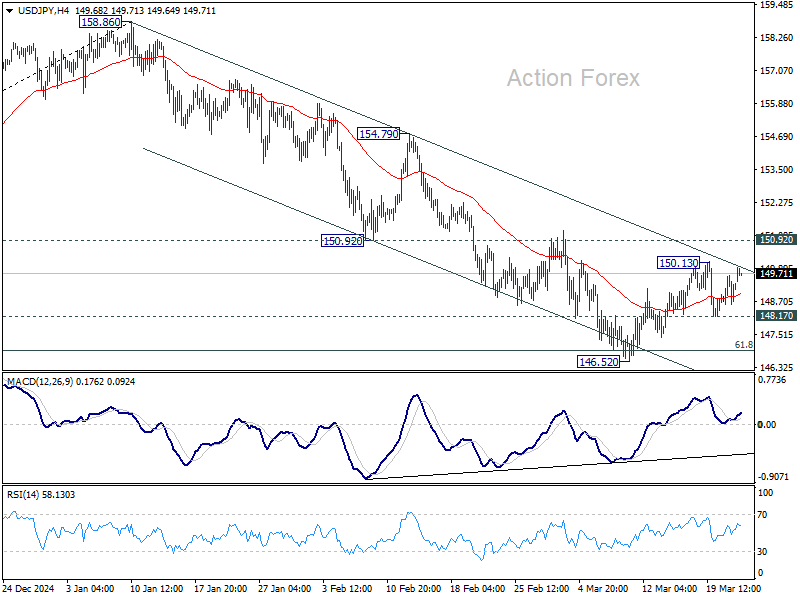

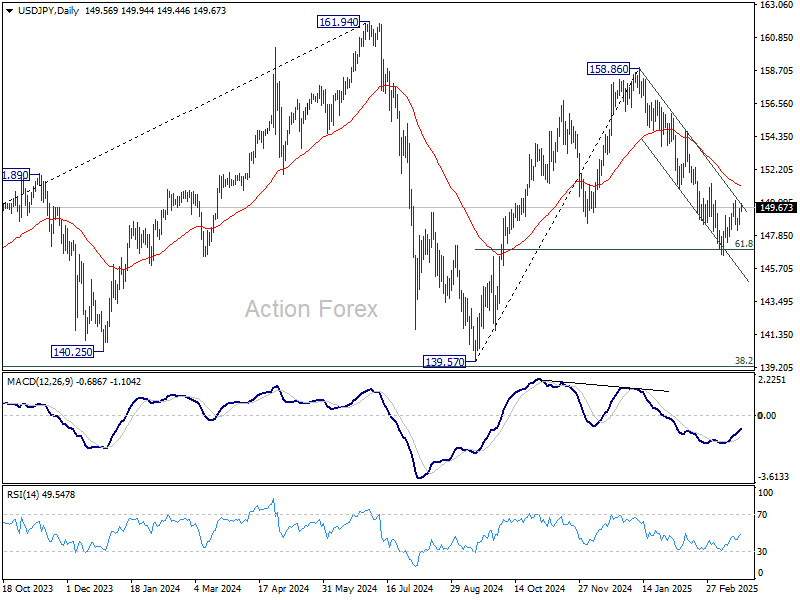

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.71; (P) 149.19; (R1) 149.79; More...

USD/JPY rises slightly today but overall outlook is unchanged. Intraday bias stays neutral first. Recovery from 146.52 is seen as a corrective move. In case of stronger rise, upside should be limited by 150.92 support turned resistance. On the downside, break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Softens on Weak Japan PMIs Disappoints, Markets Tread Water Elsewhere

Yen weakened broadly in a relatively quiet Asian session, dragged down by disappointing PMI data. The worrying sign is that both manufacturing and services sectors are now in contraction, pointing to growing signs of weakness in Japan’s economy. Despite expectations that BoJ will raise interest rates further this year, supported by strong wage growth, today's data raises fresh doubts about the timing and viability of the central bank’s tightening path.

The weakening economic backdrop also arrives at a delicate time for Japan, with the specter of new US tariffs looming. Downside risks from a global trade war could weigh on Japan’s export-dependent economy. Rising input costs and shaky external demand may ultimately delay further rate normalization.

Adding to the uncertainty, confusion over the shape and scope of US President Donald Trump’s “Liberation Day” tariffs continues to swirl. A report from the Wall Street Journal over the weekend suggested the White House is set to "narrow" its approach. The current thinking appears to be a scaled-back plan that will still include reciprocal tariffs but may delay industry-specific measures. This may align with Trump’s previous remark that there would be “flexibility”.

Until the April 2 announcement materializes, traders are likely to remain in a wait-and-see mindset, with many choosing to reduce exposure amid headline risk. Market movements in this environment may be temporary and driven more by short-term positioning than conviction. The broader direction for currencies and equities may not be defined until the full scope of the tariffs and their retaliations are well-understood.

For now, Canadian and Australian Dollars are leading the day, together with Euro. Yen and Kiwi are lagging, with Swiss Franc also on the weaker side. Dollar and Sterling are positioning in the middle.

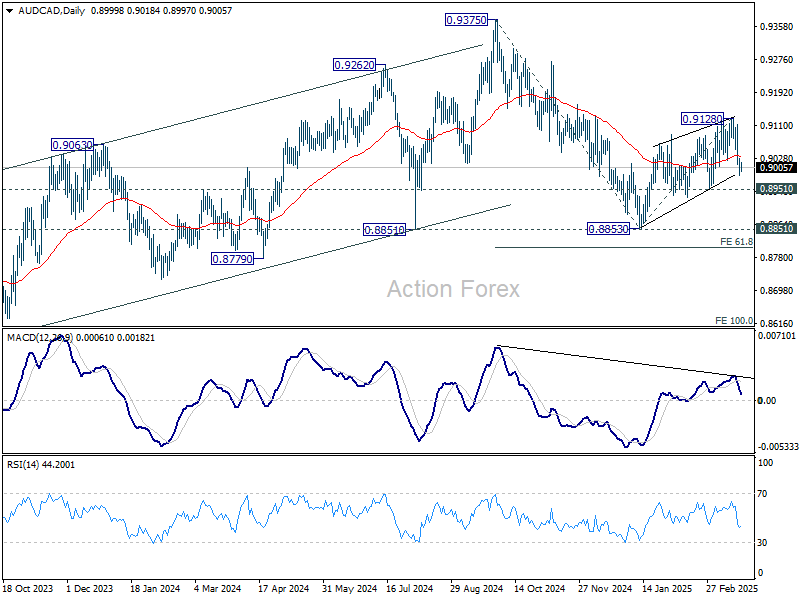

Technically, AUD/CAD's rebound from 0.8853 (Jan low) is so far seen as a corrective move based on its structure. Break of 0.8951 support will argue that the correction has completed. Fall from 0.9375 would then be ready to resume through 0.8853 to 61.8% projection of 0.9375 to 0.8853 from 0.9128 at 0.8805 next.

In Asia, at the time of writing, Nikkei is down -0.01%. Hong Kong HSI is down -0.21%. China Shanghai SSE is down -0.49%. Singapore Strait Times is up 0.17%. Japan 10-year JGB yield is up 0.027 at 1.544.

In Asia, at the time of writing, Nikkei is down -0.01%. Hong Kong HSI is down -0.21%. China Shanghai SSE is down -0.49%. Singapore Strait Times is up 0.17%. Japan 10-year JGB yield is up 0.027 at 1.544.

BoJ’s Ueda reaffirms commitment to rate hikes despite market and financial pressures

BoJ Governor Kazuo Ueda told parliament today that the central bank remains committed to raise interest rate if underlying inflation is deemed to be approaching its 2% target.

He emphasized that BoJ’s objectives remain squarely focused on price stability, and that its approach to policy "would not be disturbed by considerations for the BoJ's finances."

Ueda’s remarks come as concerns mount over the BoJ’s balance sheet in light of interest rate hikes and volatility in equity markets.

BoJ estimated in December that if short-term borrowing costs were to rise to 2%, it could incur losses of up to JPY 2 trillion.

Additionally, Ueda noted that a 1000-point drop in the Nikkei 225 index would translate into a valuation loss of about JPY 1.8 trillion in its ETF holding.

While these figures highlight the scale of financial risks, Ueda’s insistence on prioritizing price stability signals that BoJ is prepared to weather market volatility in pursuit of its monetary policy mandate.

Japan PMI composite falls to 48.5, business confidence sinks to lowest since 2020

Japan’s private sector saw a sharp loss in momentum at the end of Q1, with PMI Composite falling from 52.0 to 48.5, marking the first contraction in five months. PMI Manufacturing dropped from 49.0 to 48.3, its lowest in a year and ninth consecutive month in contraction. More concerning was the steep decline in PMI services, which fell from 53.7 to 49.5 — the weakest reading since mid-2024.

According to Annabel Fiddes of S&P Global, the downturn was driven by a "fresh fall in service sector activity" and an accelerated decline in manufacturing. Firms pointed to "strong inflationary pressure had dampened sales", with clients showing increasing hesitation to place orders.

The broader picture is one of growing pessimism. Japanese firms cited a host of structural and cyclical challenges — from persistent inflation and labor shortages to an aging population and deepening global trade uncertainty. As a result, business confidence for future activity fell to its lowest level since August 2020.

Australia's PMI manufacturing jumps to 52.6, services rises to 51.2

Australia’s PMI Manufacturing surged to 52.6 from 50.4—marking a 29-month high—while PMI Services ticked up to 51.2 from 50.8. PMI Composite , which combines both sectors, rose to a 7-month high at 51.3.

Jingyi Pan of S&P Global Market Intelligence highlighted that the output growth was not only the strongest in seven months but also "broad-based" across both manufacturing and services. Despite a decline in export orders due to weather disruptions and weak global conditions, domestic demand rebounded impressively, pushing new orders to their highest growth rate in nearly three years.

However, the report also highlighted a notable dip in business confidence. Suppressed price increases may have helped support near-term demand. But "tariff uncertainty may continue to cast a shadow on output growth in the year ahead".

Markets Eye Data Avalanche to Close Q1

The final week of Q1 will be marked by a flood of high-impact economic data from around the world, covering everything from PMIs to inflation and consumer sentiment. The central narrative across many regions will be the lingering uncertainty and fallout from the escalating tariff war, particularly between the US and its trading partners.

In the US, the spotlight remains squarely on how the trade war is affecting consumers and businesses. Consumer confidence will be critical, following a sharp deterioration since the beginning of the year due to tariff anxiety. Even more important will be whether this shift in sentiment is already impacting spending. Business PMIs, especially in the services sector, will be examined for hiring trends, while manufacturers may reveal pricing pressures and cost concerns as they brace for more tariffs.

Europe’s attention will be on whether recent optimism over Germany and the EU’s fiscal expansion is filtering into economic activity. Although the spending plan is still in its early stages, it could lift sentiment—particularly in manufacturing PMI data. Additionally, Germany’s Ifo business climate and GfK consumer confidence surveys will be closely watched for signs of a sustainable rebound.

The UK will deliver CPI and retail sales, two key indicators that could influence BoE's policy path. However, barring a significant downside surprise in inflation, BoE is unlikely to deviate from its slow-and-steady approach — one cut per quarter.

In Japan, BoJ’s Summary of Opinions will offer critical insights into policymakers’ sentiment following last week’s rate hold. The focus will be on how optimistic they are about wage growth after strong Shunto results, as well as their assessment of risks posed by global trade tensions and spillovers into financial markets. The tone will be key in gauging how close BoJ is to delivering another rate hike.

Canada’s GDP print, while important, is likely too early to fully capture tariff effects. Australia’s monthly CPI will offer clues on the inflation trend, though not as complete as the quarterly update. RBA has made clear that February’s cut was not the start of an easing cycle, so it would take notable downside surprise to revive bets on more cuts in the near term.

Here are some highlights for the week:

- Monday: Australia PMIs; Japan PMIs; Eurozone PMIs; UK PMIs; US PMIs.

- Tuesday: BoJ minutes; Germany Ifo business climate;US house price index, consumer confidence, new home sales.

- Wednesday: Japan corporate service prices; Australia monthly CPI; UK CPI; Swiss UBS economic expectations; US durable goods orders.

- Thursday: Eurozone M3 money supply; US Q4 GDP final, jobless claims, goods trade balance, pending home sales.

- Friday: Japan Tokyo CPI, BoJ summary of opinions; Germany Gfk consumer sentiment, unemployment; UK Q4 GDP final, goods trade balance, retail sales; Swiss KOF economic barometer; Canada GDP; US personal income and spending, PCE inflation

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.71; (P) 149.19; (R1) 149.79; More...

USD/JPY rises slightly today but overall outlook is unchanged. Intraday bias stays neutral first. Recovery from 146.52 is seen as a corrective move. In case of stronger rise, upside should be limited by 150.92 support turned resistance. On the downside, break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

BoJ’s Ueda reaffirms commitment to rate hikes despite market and financial pressures

BoJ Governor Kazuo Ueda told parliament today that the central bank remains committed to raise interest rate if underlying inflation is deemed to be approaching its 2% target.

He emphasized that BoJ’s objectives remain squarely focused on price stability, and that its approach to policy "would not be disturbed by considerations for the BoJ's finances."

Ueda’s remarks come as concerns mount over the BoJ’s balance sheet in light of interest rate hikes and volatility in equity markets.

BoJ estimated in December that if short-term borrowing costs were to rise to 2%, it could incur losses of up to JPY 2 trillion.

Additionally, Ueda noted that a 1000-point drop in the Nikkei 225 index would translate into a valuation loss of about JPY 1.8 trillion in its ETF holding.

While these figures highlight the scale of financial risks, Ueda’s insistence on prioritizing price stability signals that BoJ is prepared to weather market volatility in pursuit of its monetary policy mandate.

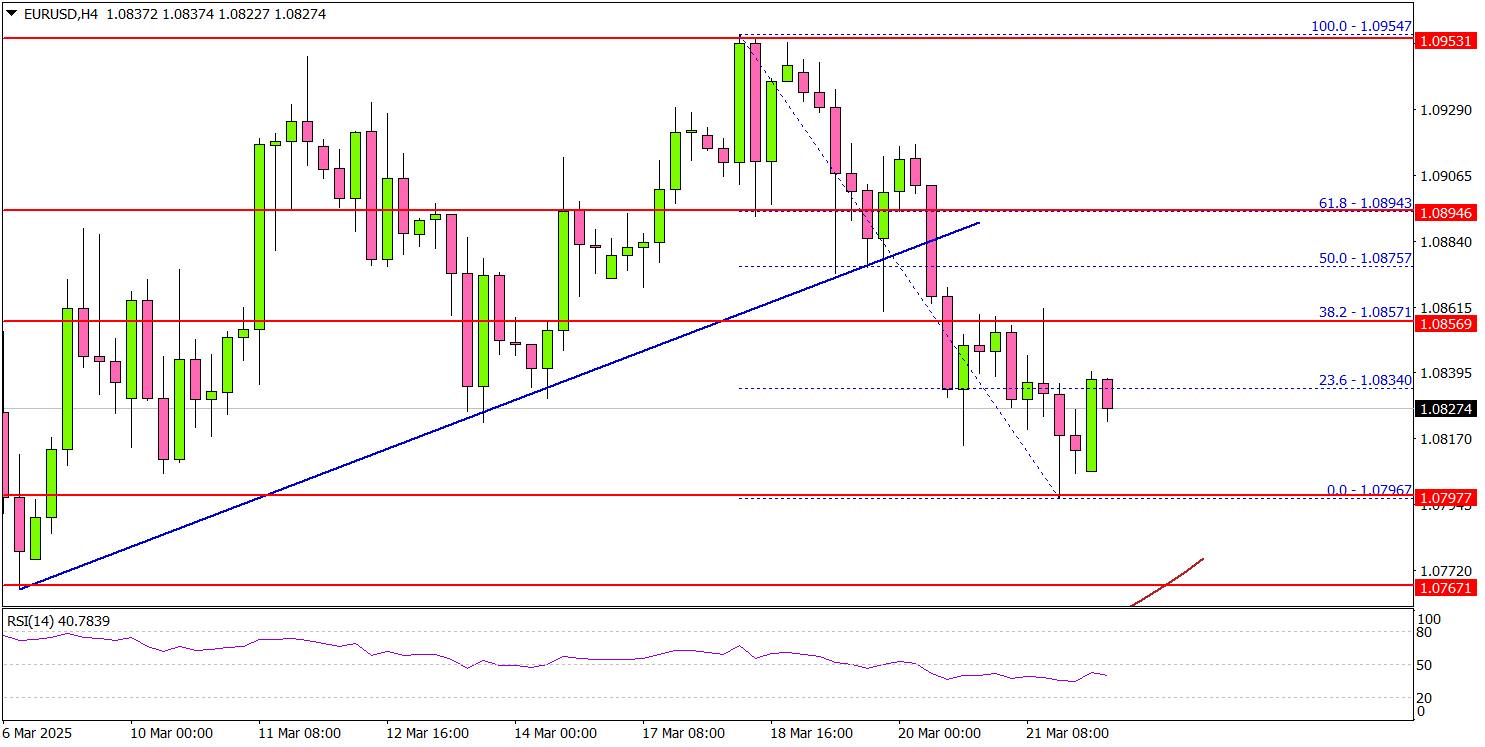

EUR/USD Pulls Back—Limited Room for Further Decline

Key Highlights

- EUR/USD started a downside correction from the 1.0950 resistance zone.

- It traded below a key bullish trend line with support at 1.0880 on the 4-hour chart.

- GBP/USD started a minor downside correction from the 1.3000 resistance.

- The US Manufacturing PMI could drop to 51.9 from 52.7 in March 2025 (Preliminary).

EUR/USD Technical Analysis

The Euro struggled to continue higher above 1.0950 against the US Dollar. EUR/USD started a downside correction below the 1.0900 level.

Looking at the 4-hour chart, the pair traded below a key bullish trend line with support at 1.0880. There was a move below the 1.0880 support, but the pair is still well above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

The pair tested the 1.0800 zone and started a consolidation. On the upside, the pair is facing resistance near the 1.0840 level. The next major resistance is near the 1.0860 level.

The main resistance is now forming near the 1.0895 zone. A close above the 1.0895 level could set the tone for another increase. In the stated case, the pair could even clear the 1.0920 resistance.

On the downside, immediate support sits near the 1.0795 level. The next key support sits near the 1.0765 level. Any more losses could send the pair toward the 1.0750 level.

Looking at GBP/USD, the pair started a short-term downside correction after the bulls failed to clear the 1.3000 resistance zone.

Upcoming Economic Events:

- Euro Zone Manufacturing PMI for March 2025 (Preliminary) – Forecast 48.0, versus 47.6 previous.

- Euro Zone Services PMI for March 2025 (Preliminary) – Forecast 51.0, versus 50.6 previous.

- US Manufacturing PMI for March 2025 (Preliminary) – Forecast 51.9, versus 52.7 previous.

- US Services PMI for March 2025 (Preliminary) – Forecast 51.2, versus 51.0 previous.

Japan PMI composite falls to 48.5, business confidence sinks to lowest since 2020

Japan’s private sector saw a sharp loss in momentum at the end of Q1, with PMI Composite falling from 52.0 to 48.5, marking the first contraction in five months. PMI Manufacturing dropped from 49.0 to 48.3, its lowest in a year and ninth consecutive month in contraction. More concerning was the steep decline in PMI services, which fell from 53.7 to 49.5 — the weakest reading since mid-2024.

According to Annabel Fiddes of S&P Global, the downturn was driven by a "fresh fall in service sector activity" and an accelerated decline in manufacturing. Firms pointed to "strong inflationary pressure had dampened sales", with clients showing increasing hesitation to place orders.

The broader picture is one of growing pessimism. Japanese firms cited a host of structural and cyclical challenges — from persistent inflation and labor shortages to an aging population and deepening global trade uncertainty. As a result, business confidence for future activity fell to its lowest level since August 2020.