Sample Category Title

Philadelphia Fed Harker: Appropriate to continue rate hikes judiciously

Philadelphia Fed President Patrick Harker said yesterday that he sees two more rate hike this year. He noted it's "prudent to continue to move away from the zero lower bound". And Inflation "does seem to be moving toward 2%". He added that there is "not much slack in the labor markets". Hence, it's appropriate to continue rate hikes "judiciously".

And if there is an "acceleration of inflation", then he "supportive of a third". Though, he is not yet seeing a "rapid acceleration" in inflation yet.

GBP/USD Upsides Remain Capped By 1.3500

Key Highlights

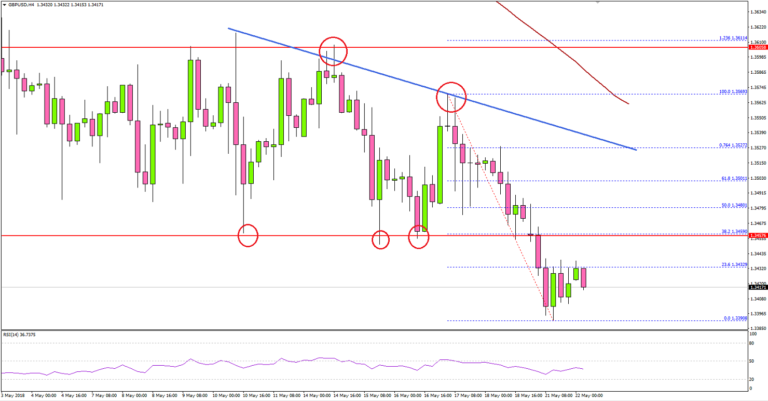

- The British Pound remained in a bearish zone during the past few days and declined below 1.3500 against the US Dollar.

- There is a key bearish trend line in place with resistance at 1.3525 on the 4-hours chart of GBP/USD.

- Chicago Fed National Activity Index (CFNAI) increased from the last revised reading of 0.32 to 0.34 in April 2018.

- Today, UK's Public Sector Net Borrowing for April 2018 will be released, which is forecasted to rise from £-0.262B to £7.000B.

GBPUSD Technical Analysis

The British Pound declined during the past few days after it failed to move above the 1.3620 resistance against the US Dollar. The GBP/USD pair declined heavily and moved below the 1.3500 and 1.3450 support levels.

Looking at the 4-hours chart, the pair recently broke the 1.3450 support and even moved below the 1.3400 handle. It seems like buyers are under a lot of pressure, capping upsides in GBP/USD.

The broken support levels at 1.3450 and 1.3500 are likely to act as resistances if the pair starts an upside correction. Moreover, there is also a key bearish trend line in place with resistance at 1.3525 on the 4-hours chart of GBP/USD.

A successful close above the trend line resistance may perhaps decrease the current bearish pressure and the pair may recover to 1.3600 and 1.3620.

On the flip side, if the pair declined further below 1.3380, the next support sits near 1.3350, followed by 1.3320.

Recently in the US, the Chicago Fed National Activity Index (CFNAI) for April 2018 was released. The market was looking for a rise from the last reading of 0.10 to 0.14.

However, the actual result was better as there was a rise in the index from the last revised reading of 0.32 to 0.34 in April 2018.

The US Dollar is currently positioned nicely in a bullish zone and any recoveries in EUR/USD and GBP/USD are likely to be capped in the near term.

Economic Releases to Watch Today

- UK's Public Sector Net Borrowing April 2018 – Forecast £7.000B, versus £-0.262B previous.

- UK's CBI Industrial Trends Survey Orders May 2018 (MoM) – Forecast 4, versus 4 previous.

Finance Ministry: Strong upturn in German economy to continue

The German Finance Ministry said in the latest monthly report that the economy is in a "strong economic upturn" even if growth in Q1 was "a bit less dynamic" than in Q4 due to "special factors".

Macroeconomic conditions "remain favorable" and indicators suggest the upturn will continue.

Market Morning Briefing: Dollar Index Made A New High Of 94.06

STOCKS

Dow (25013.29, +1.21%) moved up to test 25086. A break above 25000 if seen and sustained could turn bullish for the medium term towards 25600 or even higher.

Dax (13077.72, -0.28%) was closed yesterday but overall the index looks bullish towards 13300-13400 as mentioned yesterday. Watch immediate support near 13000.

Nikkei (22997.41, -0.022%) is testing daily channel support and while that holds, near term looks bullish. Looking at the movement , it seems as if the index is being slowly pushed to the upside. There is lack of any sharp upside momentum just now but the index has been inching up for the last few sessions now. Upside of 23200-23400 is open for the near term.

Shanghai (3196.69, -0.55%) could have some chances of moving up towards 3250 or even higher in the coming sessions. While above 3150-3200, view is bullish.

Nifty (10516.70, -0.75%) is bearish for now. A fall towards 10440-10400 is possible in the coming sessions.

COMMODITIES

Brent (79.36) and Nymex WTI (72.51) are almost stable. WTI has immediate resistance near 73 which could push the price down to 71 in the near term before the crude price again starts to rise back. Brent on the other hand, seems to have some room on the upside towards 81-82 levels which could be tested before a short dip is seen. But if the WTI comes off from current levels, upside for Brent would be limited just now.

Gold (1289.90) is likely to bounce from 1280-1275 levels back towards 1310. A break below 1275 just no looks unlikely.

Silver (16.50) may rise to 16.75 in the next few sessions. Narrow trade in the 16.00-16.75 looks probable for the near term with some possible extension to 17.25.

Copper (3.0920) has risen from levels near 3.0850 seen yesterday. Copper may rise towards 3.12-3.15 in the next few sessions before again coming off. Near term could see trade within the narrow range of 3.07-3.15.

FOREX

Dollar index (93.57) made a new high of 94.06 yesterday but has dipped from there and is currently trading at levels near 93.4-93.5. There is support on daily candles near 93.25 and lower down there is the 21 days MA near 93 which, if tested, should produce a rise back towards 94-95. Repeating yesterday’s comment, there are good chances of the Dollar Index testing its upside target near 95 in this week or max by next week. We have been saying that the upside is likely to be capped till 95. The 89 weeks MA near 95.65 is a possible extension level which should produce a dip, if tested.

Euro (1.1782) has seen a slight rise and is testing resistance in the downward channel on daily line chart. It could either dip from these levels or the current upmove could extend up till 1.1825-1.1850 after which there should be a dip. As mentioned yesterday, Euro could test 1.155 by next week, if the Dollar Index tests levels near 95. The 89 weeks MA for the Euro which could produce a bounce is near 1.145.

Dollar Yen (110.9): As per expectation, Dollar Yen rose to a high of 111.40 yesterday and has now dipped from there. It could dip further to test support on daily candles near 110.50-110.75, after which it could again rise back above 111.The revised upside target in the near term are levels near 112, which corresponds with crucial long term resistance on weekly candles.

Euro Yen (130.67): There are some chances for Euro Yen to test resistance on daily and 3 day candles near 131.5 if the Euro moves up till 1.185 and the Dollar Yen stays near 111. However, given the bearish view on Euro and the upside being capped by 112 for Dollar Yen, Euro Yen should break crucial support near 129.5-129.0 in the coming weeks.

Pound (1.3417): Our forecast of ranging movement between 1.345-1.36 did not hold as the Pound broke below support on daily and 3 day candles, thereby testing a low near 1.339 yesterday. It seems to be forming a downward channel on daily candles and could see a rise towards 1.35 in the next 1-2 sessions before dipping again.

Dollar Rupee (68.125): Dollar Rupee (68.13) made a fresh high of 68.1550 yesterday. It could come down to test 68.00 or even 67.90 over today/tomorrow but overall the outlook for the medium term is bullish.

INTEREST RATES

Repeating yesterday’s comment: US yields saw an important rally last week in which the 10 Year yield finally rose past the 3% level decisively. We now expect this rally to possibly continue in the near term towards the following upside targets:

3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.56% (2 Year)

US 10 Yr Yield (3.05%), 30 Yr (3.19%), 5 Yr (2.89%), 2 Yr (2.56%):

The 10 year yield, as we had predicted, has dipped towards support on short term chart. It could test 3.04% today and then see a rise back beyond 3.10% later this week / early next week.

The 5 Year yield is testing support currently and should rise towards 2.94%2.95% again in the next couple of sessions.

The 30 year yield has unexpectedly dipped below 3.20%, but this dip shouldn’t hold for long and the yield could rise again towards 3.25%. If the dip however persists, it shouldn’t extend below 3.15%.

The German 10 Year – US 10 Year yield spread (-2.53) is continuing its break of support on medium term and long term charts and looks bearish towards long term channel support near -2.70% to -2.75%.

Commodity Currencies Are Beaming

Currency Markets

The US dollar has given up some of its gains overnight as investors keenness for Greenbacks has temporarily abated. The shifting dynamics around trade and tariffs does give pause for thought as US dollar bulls are consolidating gains at a very tricky and treacherous junction for both the USD and US bond yields. After making some significant advances last week, USD profit taking was the name of the game in Monday NY session.

Commodity currencies are beaming on the back of surging Commodity Indexes as oil prices broke through last week high water mark. The de-escalation in the US -Sino tariff and trade has put to rest, temporarily albeit, some of the market biggest fears around a Global growth slowdown and commodity markets and prices are returning in vogue.

Also, there’s the usual air of uncertainty with both May FOMC minutes and April ECB minutes due this week. Trader’s will be more inclined not to get ahead of the curve before these releases.

EM currencies performed better overnight as stretched positions unwound and the bounce in oil prices provided some idiosyncratic benefits to petrol related currencies. However, the common denominator in the EM space remains the stronger USD which could continue to run amok after the overnight profit taking inspired u-turn.

So far, the beginning of the week is shaping up to be all about consolidating and gingerly contesting last week’s significant breakouts

Oil Markets

The markets positive take on “no trade war “and Venezuela political woes are driving Oil prices higher. The global condemnation surrounding the election of incumbent Venezuelan president Nicolas Maduro has as expected trigged the Trump administration to levee new sanctions on the debt-ridden country. Tightening the economic screws will severely cripple Petróleos de Venezuela ability to export while making it virtually impossible for the country to acquire dollars.

Also, US secretary of state Mike Pompeo raised the Iran sanctions bar by promising to impose the “strongest sanctions in history” on Iran to bring it to the bargaining table for a new nuclear deal.

The effect of OPEC -Non-OPEC supply compliance and the US abandonment of the JCPOA has created ultra-tight supply conditions to the point where any hint of supply disruption will send oil prices soaring. Supply-side dynamics are apparently in the driver’s seat suggesting prices should push higher near term.

Equity Markets

Equity investors revelled as trade war fears have temporarily abated suggesting the parties are heading on a far more appealing approach than feared. But hope springs eternal that both superpowers can iron out a market-friendly bilateral trade agreement and at the minimum maintain, stay at the negotiation table until the more contentious trade issues can be ironed out. The fear is that the “no trade war “announcement is little more than kicking the can down the road., but only time will tell.

Gold Markets

Gold price movements continue to be as much as anything a USD trade. Gold prices moved off overnight lows on the back of USD profit taking. But from both a fundamental and technical picture the Gold bears continue to have the upper hand as bullish signals are non-existent. Given the resurgent dollar, a reprieve on the trade war front, equity markets stabilising and evaporated geopolitical risk premiums, the balance of risks suggests gold prices move lower over the near term.

Currencies

EUR: A bit of a mixed bag overnight with ECB’s Nowotny erring dovish but Italian Political risk premiums eased after Conte is said to be the next Prime Minister. However, given the Italian affair has little chance of a spill over into other peripheral debt and with the ECB already leaning very dovish with the first hike not priced until September 2019, the Italian risk should be of little influence on ECB policy.

JPY: After falling to move above 111.40 overnight, the dollar bulls turned more conservative without the support from higher US yields as 10 Year UST’s were little changed from last weeks levels

AUD: Strong Beta currencies are benefiting from the conciliatory actions on the US-China trade front as global equity markets soared and Wall Street has followed suit starting the week on a robust note. But the bullish case for commodities on the back of surging oil prices is building which is underpinning AUD sentiment.

MYR: We would typically expect USAsia to trade lower as the US dollar has taken a bit of a detour overnight. However, the Riggit remains vulnerable to the lack of insight into fiscal planning. But markets levels look attractive from both a Bond yield and currency perspective not to mention surging oil prices, so we are left to surmise that once fiscal clarity is offered, we could finally see the Ringgit sentiment improve. I the meantime EM Asia FX will remain susceptible to the stronger USD

BoJ Kuroda to patiently pursue powerful monetary easing

BoJ Governor Haruhiko Kuroda reiterated to the parliament today that the central bank " won't end the ultra-easy policy before inflation reaches 2 percent". And BoJ will "patiently pursue powerful monetary easing". Though, Kuroda also noted policymakers will take into account the "side effects" such as the "impact of financial institutions, particularly regional banks".

Regarding the economy, Kuroda said it's expanding moderately, with consumption helped by loose monetary policy. While there is sustaining momentum in growth, prices lack so. And there is still some distance to inflation target. BoJ will remain mindful of uncertainties on economic and price outlook.

Deputy Governor Masazumi Wakatabe said that BoJ can achieve the inflation target "with the current policy". Though, "if conditions change and our current policy becomes inappropriate, we may need to change policy."

Eco Data 5/22/18

[php_everywhere instance="1"]

Sterling in Focus amid Flurry of Data, BoE Speeches, and Brexit Talks

This will be a decisive week for the British pound, as a raft of crucial economic data releases and remarks by BoE policymakers could make or break expectations around a potential rate increase at the August policy meeting. While economic forecasts are quite upbeat, other gauges of the UK economy are not as optimistic, which suggests that sterling may be at risk from these data releases. Brexit talks resume this week as well.

The British currency has come under fire over the past weeks, losing ground against all its major counterparts besides the battered kiwi, as a streak of disappointing UK economic data quickly curtailed market expectations for a near-term rate increase by the Bank of England (BoE). Investors were proven right – the Bank held off from raising rates at its May policy gathering and maintained a relatively cautious stance, indicating that the timing of any future rate hike will be guided by the quality of incoming data. As such, this week’s data releases alongside public appearances from key BoE officials will be closely scrutinized by traders trying to gauge when, and whether, the Bank will act next.

The events kick off on Tuesday at 0900 GMT, when BoE Governor Mark Carney will appear before the UK Parliament’s Treasury Committee for a testimony on the May Inflation Report, alongside his fellow BoE members Dave Ramsden, Gertjan Vlieghe, and Michael Saunders. In that Inflation Report, the Bank downgraded its GDP forecasts for this year, while it also revised down its inflation projections for the coming years. Both developments ease some pressure on policymakers to raise rates in an aggressive fashion, so it wouldn’t be a surprise to see a similar message being echoed at these hearings.

After that, attention will turn to the release of inflation data on Wednesday at 0930 GMT, followed by retail sales figures on Thursday at the same time. With respect to inflation, the UK CPI rate is projected to have held steady at 2.5% year-over-year (yoy) in April, while the core rate that excludes food and energy items is anticipated to tick down to 2.2%, from 2.3% previously. As for retail sales for April, they are expected to have risen in monthly terms, a rebound following a sharp decline in March. However, that would still cause the yearly rate to decline notably, because the print of April 2017 – which will be dropping out of the yearly calculation now – was exceptionally strong.

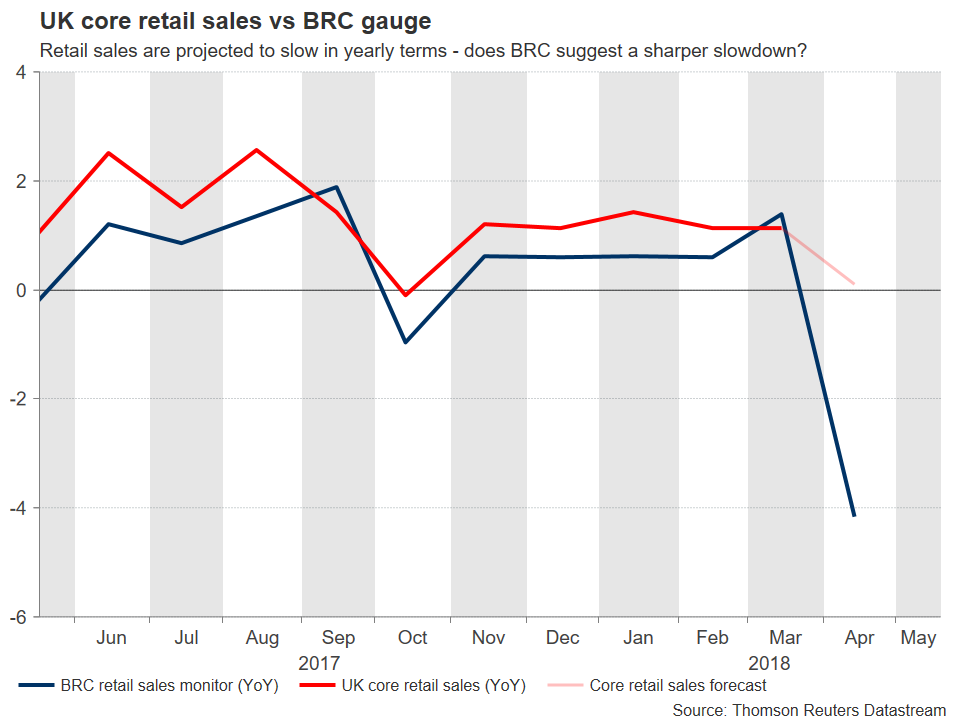

Having outlined the forecasts, one feels a little hesitant to trust them, after looking at gauges of inflationary pressures and consumer spending for April. The Markit services PMI for the month showed that service providers raised their selling prices at one of the slowest paces since last July, which suggests that the risks surrounding the CPI forecasts may be somewhat tilted to the downside. Moreover, the British Retail Consortium (BRC) retail sales monitor – that tracks quite well the yearly change in retail sales – plunged to -4.2% yoy from 1.4% previously, while credit-card provider Visa also said that spending on its cards in April was 2% lower than last year. These also imply that a downside surprise in retail sales relative to the forecasts is perhaps more likely than an upside one.

The final data release of the week will be on Friday at 0930 GMT, when the second revision of GDP for Q1 is due out. Recall that the preliminary estimate was surprisingly weak, triggering a sharp negative reaction in sterling. Elsewhere, BoE Governor Mark Carney will make public appearances on Thursday and Friday as well.

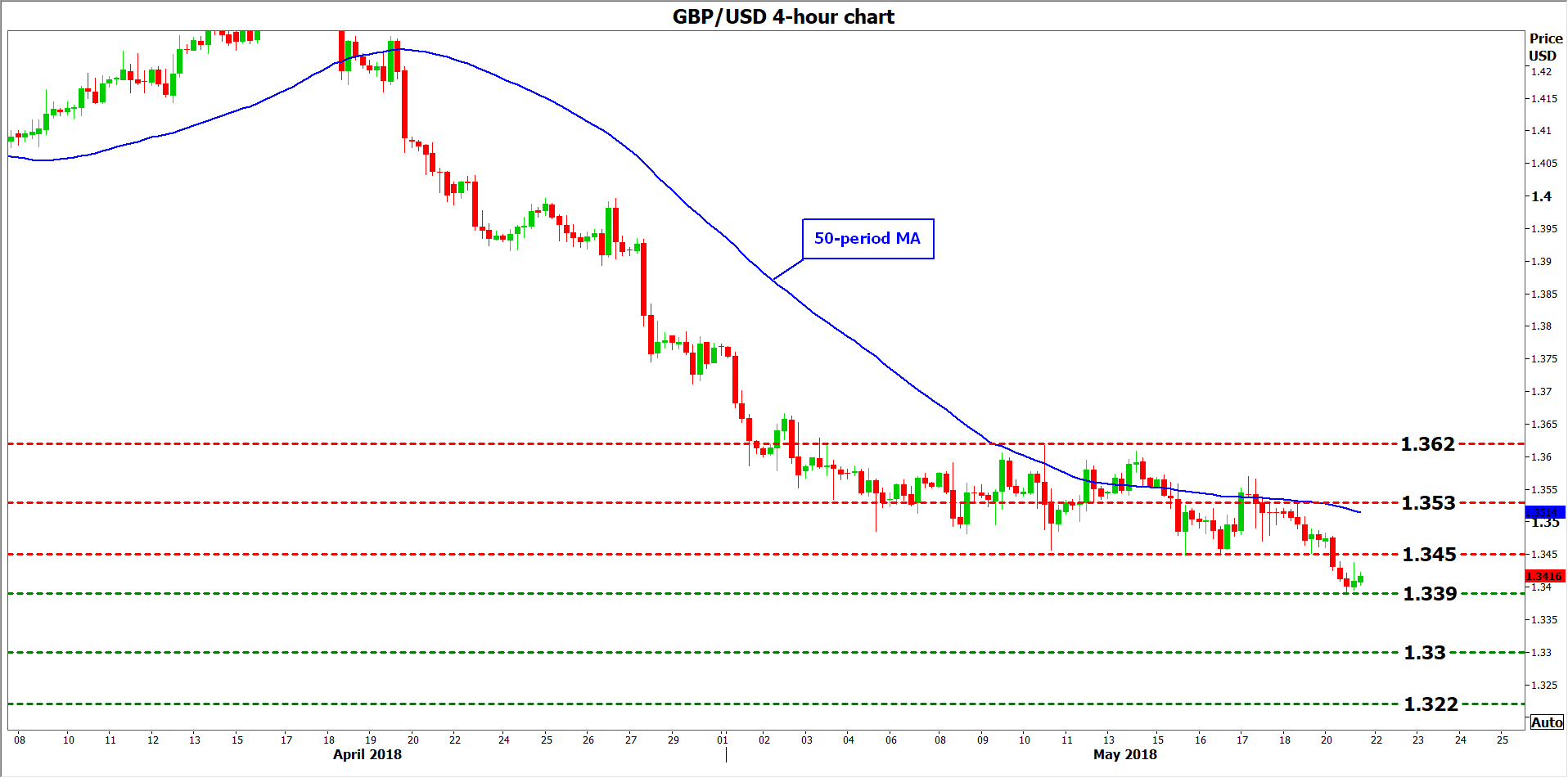

At the time of writing, futures markets indicate a 40% probability for the BoE to raise rates at its August meeting, according to UK overnight index swaps. Should these data disappoint, making investors even less confident that a hike will materialize in August, then the pound could resume its downfall. Looking at sterling/dollar, support to declines may be found near 1.3390, the low of May 21. Further down, the round figure of 1.3300 would increasingly come in focus, marked by the low of December 15. If the bears overcome that territory too, then buy orders may be found at 1.3220, a level that halted the pair’s decline on November 28.

On the other hand, and in case these data come in stronger than expected, immediate resistance to advances in Cable could come around 1.3450, the low of May 15 and 18. An upside break of that zone could open the way for 1.3530, the high from May 18, and even higher, the 1.3620 zone could come into play, defined by the peak on May 10.

Turning away from economics, the other factor that could shake the pound this week are the Brexit negotiations, the next round of which begins on Tuesday. Recent media reports suggest the UK government is willing to keep the country in the EU customs union beyond 2021 as a last-ditch solution to avoid a “hard” border in Ireland, a thorny issue that has been hindering progress in the negotiations so far.

Gold Dips as China-US Tariff Spat Eases

Gold has started the new trading week with losses. In Monday’s North American trade, the spot price for one ounce of gold is $1289.63, down 0.22% on the day. It’s a very quiet day on the release front, with no key indicators on the schedule. The sole event is a speech from FOMC member Raphael Bostic. On Tuesday, the US releases Richmond Manufacturing Index.

After weeks of an escalating trade war between the US and China, there was a breakthrough of sorts on Sunday. Treasury Secretary Steven Mnuchin announced that the two sides had made significant progress and the trade war was being ‘put on hold’. This has resulted in stronger risk appetite and has pushed gold prices lower in the Monday session. Just last week, the White House sounded pessimistic about a deal being reached with China. The two economic giants had exchanged stiff tit-for-tat tariffs in recent weeks, raised fears of a bilateral trade war between the two largest economies in the world. The respite in the rhetoric and tariffs means that the two sides can now tackle the US trade deficit with China, which President Trump has long complained is a result of a non-level playing field with China. The news that the sides had backed down has pushed the dollar and stock markets higher.

It’s a quiet start to the week, with no major US data releases until Friday. In the meantime, markets will be keeping a close eye on the Federal Reserve, which will release the minutes of its policy meeting earlier in May. The Fed did not raise rates at the meeting, but a strong US economy has raised expectations that the Fed will press the rate trigger in June – according to the CME Group, the odds of a June increase stand at 95%. The markets will be looking for some guidance from the May minutes, and is the minutes are hawkish, traders can expect the dollar to post gains against its rivals.

DOW breaks 25000, next is 25800

DOW opens strongly higher today, riding on news regarding US-China trade negotiations. At the time of writing, it's up over 1.3% and is back above 25000 handle. Rise from 23531.31 and that from 23344.52 is resuming. Solid support from 55 H EMA shows the underlying near term bullishness. However, there is no clear indication of larger up trend resumption yet. Thus, we're treating the current rise as a leg inside the range pattern from 26616.71. The real hurdle to overcome is between 25800.35 resistance and 78.6% retracement of 26616.71 to 23360.29 at 25919.83. We'll look for topping signal around there.