Sample Category Title

Sterling Lower ahead of Important Week Brexit Talks, CPI and GDP Revision

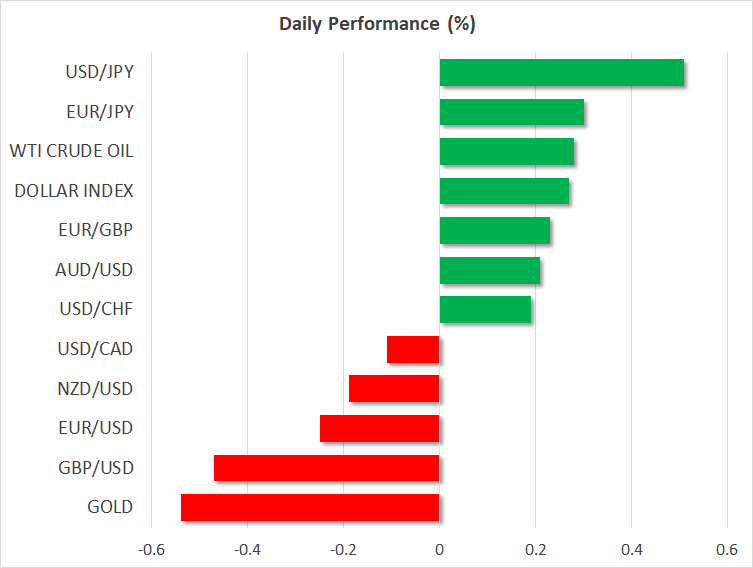

The development in the forex markets are pretty much unchanged. Australian, Canadian and US Dollar remain the strongest ones for the day. On the other hand, Japanese Yen and British Pound have been taking turns to be the weakest. Receding risks of US-China trade war is a key focus in driving risk appetite and hammers the Yen. On the other hand, Sterling is soft as traders turned more cautious ahead of an important week. Brexit negotiations will release in Brussels on Tuesday. April CPI and Q1 UK GDP to be featured this week will possibly decide whether there is still chance for an August BoE hike. Meanwhile, Euro is mixed as the meeting between the new populist Italian government leaders and President Mattarella is awaited.

Sterling facing an important week

Sterling is facing and important week ahead. The next Brexit negotiations session will begin in Brussels on Tuesday. The topic of Irish border remains unresolved. There were rumors that UK could stay in the customs union after Brexit but they were quickly denied. Some progress has to be made before another EU summit in June but time is running out.

Further more, whether BoE is ready to raise interest rate in August, November, or no at all remains a key question. That's a question to BoE policymakers as well as the markets. BoE Governor Mark Carney viewed Q1 slowdown as temporary. And he expected upward revision from the dismal 0.1% qoq growth. We'll have that revision, if any, on Friday. In addition, there will be inflation report hearing on Tuesday, CPI on Wednesday, and retail sales on Thursday too. We believe that by the end of this week, we'll see if there is any chance of August hike.

CBI Drechsler: Customs union is a "pragmatic decision" after Brexit

Paul Drechsler, President of the Confederation of British Industry, will use an upcoming speech to urge UK Prime Minister Theresa May to "break the Brexit logjam and fast". And he added that UK should remain in the customs union with the EU "unless and until an alternative is ready and workable".

And he emphasized that any solution must meet four customs tests:

- Maintain friction-free trade at the UK-EU border

- Ensure no extra burdens are incurred behind the border

- Guarantee there are no border barriers for Northern Ireland

- Boost export growth with countries both inside and outside the EU.

Before any solution, he added "a pragmatic decision to be in a customs union with the EU would allow us to move on."

Italian populist duo to seek endorsement from President Mattarella

Leaders of anti-establishment 5-Star Movement and the far-right League will meet with President Sergio Mattarella today at 1530 GMT. If they could clear this last hurdle, the coalition government could be formed quickly. And a confidence votes might be pushed through the parliament as soon as this week.

The latest version of the the coalition's economy policy excludes the request for a 250B euro debt relief from the ECB while a mechanism under which countries could leave the EU is not proposed. Yet, it indicates that ECB's purchase of government under the QE program should not count towards the debt-to-GDP ratio. Meanwhile, it calls for a reevaluation of the EU budget and a review of "European economic governance", which the parties criticizes as based more on the "predominance of the market" than on economic and social needs.

The focus of the plan was on fiscal stimulus. According to former fiscal commissioner and IMF alumnus Cottarelli, the measures might result in a deficit slippage of 108-125B euro (6-7% GDP), in addition to the current 30B euro (1.7% GDP).

More in Italy Policy Turmoil Not Yet Resolved although More Hurdles Cleared for New Government

China Liu on US trade talk: Increase imports, re-balance the economy and expand domestic demand is our national policy

China's Vice Premier Liu He was interviewed by the CGTN TV network after the trip to Washington. He noted the trade talks were "constructive, positive and fruitful", and "very practical". There were "lots of concrete consensus" reached in terms of trade and structural issues. And, "both sides pledged to stop the trade war and develop good relations."

The concrete issues include agricultural and energy exports to China. Liu added that "the Chinese market will become the largest world market. So to increase imports, re-balance the economy and expand domestic demand is our national policy." Also, Liu said "we expand our domestic market and increase imports because we want to serve the needs of our people, our economy, and our growth. Speeding reform and growth by means of opening up is a very important national strategy. It worked for China for the past 40 years, and we will continue down that path."

But he emphasized that "exporting to China or making China buy more, one must make the Chinese consumers happy".

Both sides issued a joint statement outlining the framework for further trade talks. US Treasury Secretary Steven Mnuchin said trade war is now put on hold.

NAB pushed forecast of first RBA hike away to May 2019

The National Australia Bank finally gave up on their forecast of an RBA rate hike within 2018. Their expectation on the next move is now pushed from November to May 2019. The change put them back in line with market pricing, as well as with other major bank forecasters.

RBA chief economist Alan Oster noted that the " change reflects the fact there is no sign yet of stronger wages growth and unemployment has been stuck around 5.5% for the best part of a year." Also, he added that once the tightening cycle starts "further rate increases will be very gradual". And after the first move in May 2019, the next move will be "not until November 2019".

Oster also noted that the economy is still expected to strengthen and lead to falling unemployment. And that should "eventually translate into stronger wages growth and give the RBA confidence that inflation will track back to its 2.5% target". However, there is "considerable uncertainty around the timing at which wages growth will strengthen".

New Zealand retail sales grew 0.1% qoq in Q1, big disappointment

New Zealand retail sales was a big disappointment to the markets. Ex-inflation retail sales volume grew merely 0.1% qoq in Q1, much lower than expectation of 1.0% qoq. That's also a sharp slowdown from Q4's 1.4% qoq. Besides, it's the weakest quarter since 2015.

Stats NZ noted in the release that "retail spending in the first three months of the year was relatively flat despite rising job numbers, high migration, and record international tourism."

"Of the 15 retail industries, seven had higher sales volumes in the March 2018 quarter, and eight experienced lower sales volumes."

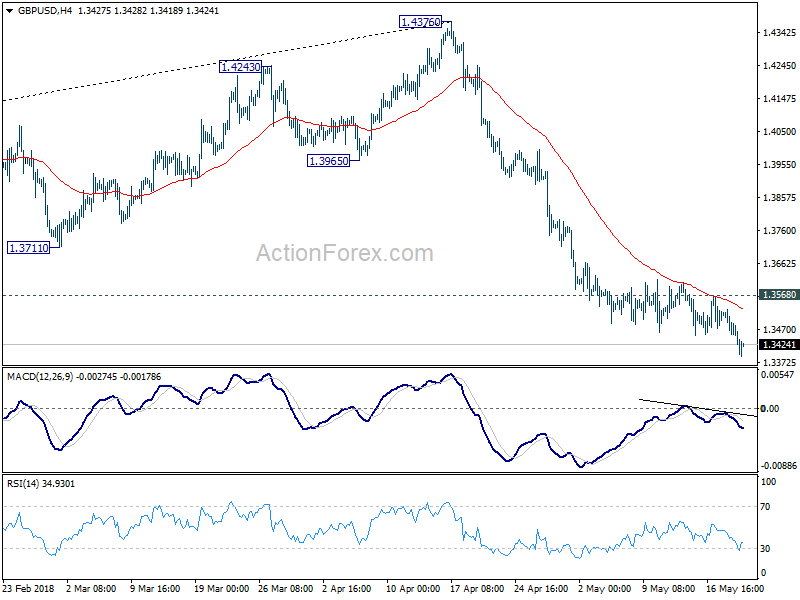

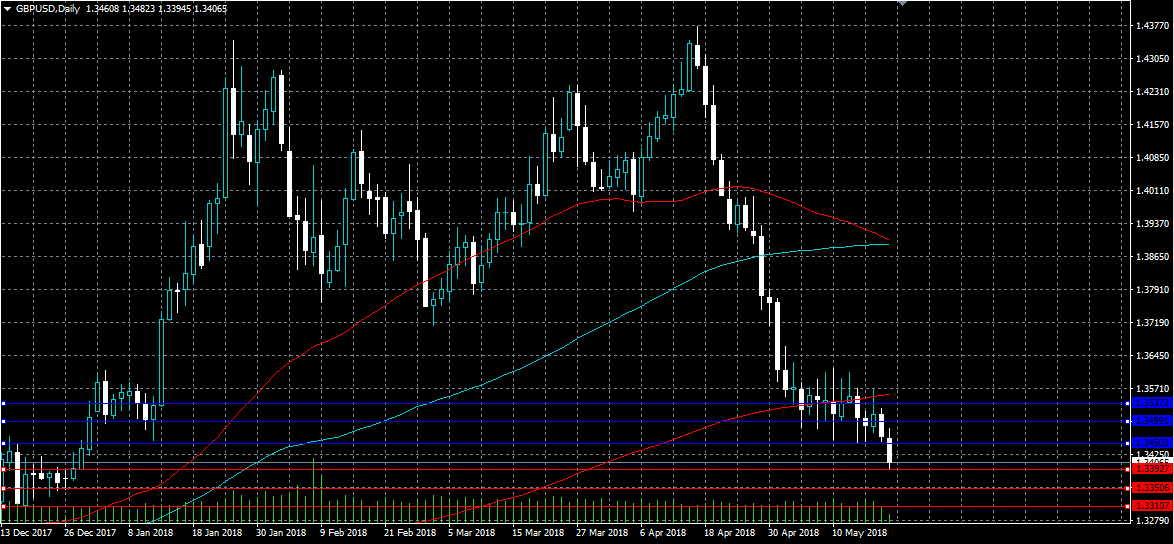

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3442; (P) 1.3485; (R1) 1.3515; More...

Intraday bias in GBP/USD remains on the downside as fall from 1.4376 is in progress. Next target will be 50% retracement of 1.1946 to 1.4376 at 1.3161. On the upside, break of 1.3568 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 should now be firmly taken out. Next target will be 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3801) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Ex Inflation Q/Q Q1 | 0.10% | 1.00% | 1.70% | 1.40% |

| 23:01 | GBP | Rightmove House Prices M/M May | 0.80% | 0.40% | ||

| 23:50 | JPY | Trade Balance (JPY) Apr | 0.55T | 0.11T | 0.12T | 0.17T |

| 8:00 | EUR | ECB Financial Stability Review | ||||

| 12:30 | USD | Chicago Fed Nat Activity Index Apr | 0.34 | 0.48 | 0.1 0 | 0.32 |

Euro Falls The Stairs Down Amid Political Risks

Here are the latest developments in global markets:

FOREX: The US dollar advanced considerably versus the Japanese yen on Monday (+0.46%) after the US Treasury Secretary Steven Mnuchin said on Sunday that the US trade war with China is “on hold”. Dollar/yen created a fresh 4-month high of 111.38, while the US dollar index added 0.31% to its performance, creating a 5-month high at 94.05. Pound/dollar plunged to a 5-month low of 1.3394 (-0.46%) ahead of key data this week which could the timing of monetary tightening by the Bank of England (BOE) this year. Euro/dollar slipped to 1.1715, hitting its lowest level in 6 months early on Monday (-0.25%) on the back of a stronger dollar. Antipodean currencies were mixed, with aussie/dollar up at 0.7519 (+0.12%), but kiwi/dollar down at 0.6892 (-0.26%). Dollar/loonie was last seen at 1.2866 (-0.11%). Dollar/lira strengthened to a record high of 4.5634 (+1.43%) as there are worries about the Central Bank of the Republic of Turkey (CBRT) ability to lead in double-digit inflation and President Tayyip Erdogan influence over monetary policy.

STOCKS: European equities were a sea of green on Monday, with Swiss’s blue-chip index and the Italian FTSE MIB being the only exception. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.31% and 0.16% respectively at 1100 GMT. The French CAC 40 surged 0.66%. In Italy, the FTSE MIB 100 declined 0.37%, as the two anti-establishment parties are close to form a coalition government. The British FTSE 100 moved significantly higher (+0.78%), creating a new record high at 7,848. The Swiss index was down by 0.53%, led by losses in consumer cyclicals. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in positive territory, pointing to a higher open today.

COMMODITIES: Oil prices retreated during the early European afternoon but remained up on the day, gaining from easing trade tensions between the US and China. West Texas Intermediate (WTI) crude oil and Brent were last seen at $71.45 (+0.24%) and $78.57 (+0.05%) per barrel. In precious metals, gold dived to a 5-month low of $1,281.76 (-0.52%).

Day ahead: Italian Eurosceptic parties to meet the President of Italy; Fed speakers eyed

In the Eurozone, the two populist parties, the Five-Star Movement, and the right-wing League will be meeting the Italian President, Sergio Mattarella today at 1700 GMT to inform him on their jointly-agreed plans to form a new government. During the meeting, the Eurosceptic parties are also expected to discuss the identity of the next Prime Minister to rule the coalition government after reports stated on Sunday that a potential candidate has been already agreed. Recall that neither the Five Star leader Luigi di Maio nor the League’s Matteo Salvini are willing to take over. Still, no matter who will take the role, the big question remains on the coalition strategy and particularly on potential reforms that could weigh on Eurozone’s spending program and therefore on the euro despite officials denying a proposal of a 250 billion euros debt relief from ECB last week.

Meanwhile in Brussels, Brexit negotiations are resuming this week and investors will be focused to see whether the EU and the UK are able to deliver enough progress, especially on the Irish border puzzle, needed for a productive summit of EU leaders on June 28-29. In case of successful talks in June, optimism that both sides can reach a final agreement in October could increase, months before the UK exits the bloc in March 2019. Inflation hearings report due on Tuesday, UK’s CPI numbers on Wednesday and GDP growth readings on Friday will be also closely watched to indicate whether a rate hike by BoE could come as early as in August.

On the trade front, talks between the US and China will remain in the spotlight although both countries decided to put the trade war on hold after the release of a joint statement on Saturday. On Sunday, the US Secretary Steven Mnuchin said, “Right now, we have agreed to put the tariffs on hold while we execute the framework.”, while China’s foreign ministry spokesman Lu Kang expressed hopes that trade barriers with the US will not re-emerge. However, as long as both countries have not announced any outline on how to solve their disagreement, some risk aversion could remain in the markets.

Besides trade headlines, a number of speeches by Fed members could move the dollar today in the absence of major economic releases. At 1615 GMT, Atlanta Fed President Raphael Bostic (1615 GMT) will be speaking on “Welfare Economics: Trade and a Review of Principles”, while at 1815 GMT Philadelphia Fed President Patrick Harker will be participating in conversation before the Chief Executives Organization’s CEO Financial Seminar 2018. Later at 2230 GMT, FOMC member Neel Kashkari will be making comments as well.

USD/CAD – Canadian Dollar Drifting In Holiday Trade

The Canadian dollar is steady in the Monday session. Currently, USD/CAD is trading at 1.2871, down 0.14% on the day. On the release front, Canadian banks are closed and there are no Canadian indicators. In the US, the sole event is a speech from FOMC member Raphael Bostic. On Tuesday, Canada releases Wholesales Sales and the US publishes the Richmond Manufacturing Index.

There was a dramatic development in the China-US tariff battle on Sunday, as US Treasury Secretary Steven Mnuchin said that the trade war was being ‘put on hold’. Just last week, the White House sounded pessimistic about a deal being reached with China. The two economic giants had traded stiff tit-for-tat tariffs in recent weeks, worth billions in trade. These moves had raised fears of a bilateral trade war between the two largest economies in the world. The respite in tariffs means that the US can sit down with the Chinese and discuss the US trade deficit with China, which President Trump has long complained is a result of a non-level playing field with China. The news that the sides had backed down sent stock markets higher, and traders will likely be greeted with gains when European markets reopen on Tuesday.

The Canadian dollar recorded considerable losses on Friday, after a weak core retail sales in March. The indicator declined 0.2%, well off the estimate of 0.5%. Retail Sales was stronger, with a gain of 0.6%, above the estimate of 0.3%. Inflation remained steady, as CPI came in at 0.3% in April, matching the estimate. On an annualized basis, inflation was up 2.2% in April, the third straight month it exceeded the Bank of Canada inflation target of 2.0%.

Negotiations over a new NAFTA agreement have failed to reach a conclusion, and the parties haven’t even reached an ‘agreement in principle’. Although there is no official deadline to wrap up a deal, there are upcoming events which could mean that a deal won’t be made in 2018. Mexico holds general elections in June and the U.S holds congressional mid-term elections in November. Meanwhile, the Trump administration has given both Canada and Mexico another 30-day exemption on steel and aluminum tariffs, lasting until June 1. Earlier in the week, U.S Commerce Secretary Wilbur Ross said that further extensions could be granted, depending on the progress made in the NAFTA talks. Ottawa has demanded “full and permanent” exemptions from the tariffs, but may have to cough up more concessions in the NAFTA talks in order to convince Washington to exempt Canadian steel and aluminum imports from tariffs. With US Treasury Secretary Steven Mnuchin bluntly stating on Sunday that the sides remain far apart from a deal, the NAFTA talks could be in deep trouble.

Euro Edges Lower, German Markets Closed For Holiday

EUR/USD continues to trade quietly. In the Monday session, the pair is trading at 1.1743, down 0.27% on the day. The On the release front, German markets are closed for Whit Day, and there are no German or eurozone indicators. In the US, the sole event is a speech from FOMC member Rafael Bostic.

The Italian election back in March was inconclusive, and the new political landscape could spell bad news for Brussels. Two euro-sceptic parties, the Lega Nord and the Five Star Movement have reached an agreement and appear poised to form the next government. The platform issued by the parties call for increased deficit spending and a review of European Union fiscal rules. So far, neither party has called for a referendum on Italian membership in the European Union or demanded that the EU cancel the portion of Italy’s debt that it holds. Still, Italy is the third largest economy in the EU (with Britain heading out the door), and any moves which will put Italy on a collision course with the EU could have a negative impact on investor sentiment towards the euro.

There was a dramatic development in the China-US tariff battle on Sunday, as US Treasury Secretary Steven Mnuchin said that the trade war was being ‘put on hold’. Just last week, the White House sounded pessimistic about a deal being reached with China. The two economic giants had traded stiff tit-for-tat tariffs in recent weeks, worth billions in trade. These moves had raised fears of a bilateral trade war between the two largest economies in the world. The respite in tariffs means that the US can sit down with the Chinese and discuss the US trade deficit with China, which President Trump has long complained is a result of a non-level playing field with China. The news that the sides had backed down sent stock markets higher, and traders will likely be greeted with gains when European markets reopen on Tuesday.

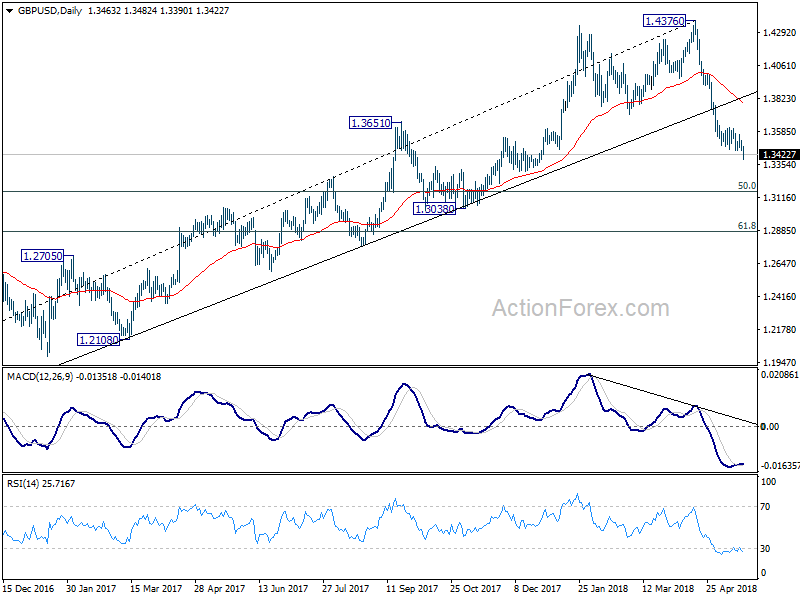

Sterling Strongly Bearish Below 1.3450

The British pound has moved to the lowest trading level of 2018 against the US dollar, hitting 1.3392 as the greenback strengthens broadly in early week trading. The GBP/USD pair currently trades around the 1.3400 level, and remains extremely weak after breaking below the key 1.3450 support level. Traders look for further sterling selling below the 1.3400 level, and now await a steady stream of FOMC speakers later today.

The GBPUSD pair remains strongly bearish while trading below the 1.3450 level. Key support is now found at the 1.3350 and 1.3310 levels.

If the GBPUSD pair moves above the 1.3450, key resistance is then found at the 1.3480 and 1.3500 resistance levels.

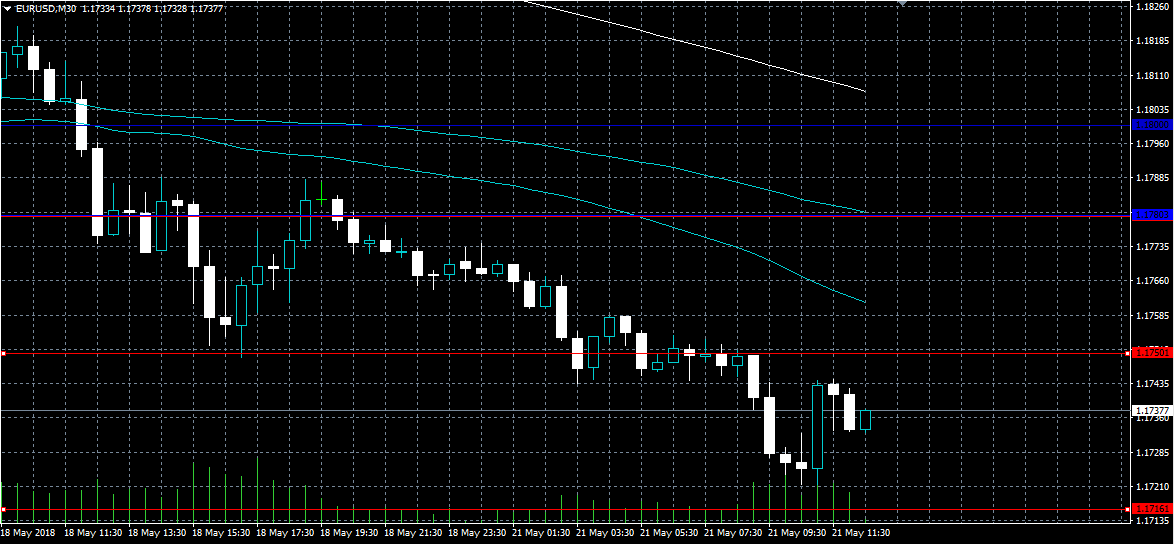

EURUSD Still Under Pressure Below 1.1750

The euro has moved to a fresh monthly trading-low against the US dollar on Monday, hitting 1.1716, as fears over the Italian economy intensify. The EURUSD pair has moved slightly higher since touching 1.1716, although bearish selling pressures are likely to remain while price clearly trades below the key 1.1750 level. Moving into the US trading session, the focus is likely to remain on rising Italian bond-yields and the increase in the value of the US dollar index.

The EURUSD pair is strongly bearish while trading below the 1.1750 level, key support is now at the 1.1716 and 1.1650 levels.

If the EURUSD pair moves back above the 1.1750 level, buyers may test back towards the 1.1780 and 1.1800 resistance level.

CBI Drechsler: Customs union is a “pragmatic decision” after Brexit

Paul Drechsler, President of the Confederation of British Industry, will use an upcoming speech to urge UK Prime Minister Theresa May to "break the Brexit logjam and fast". And he added that UK should remain in the customs union with the EU "unless and until an alternative is ready and workable".

And he emphasized that any solution must meet four customs tests:

- Maintain friction-free trade at the UK-EU border

- Ensure no extra burdens are incurred behind the border

- Guarantee there are no border barriers for Northern Ireland

- Boost export growth with countries both inside and outside the EU.

Before any solution, he added "a pragmatic decision to be in a customs union with the EU would allow us to move on."

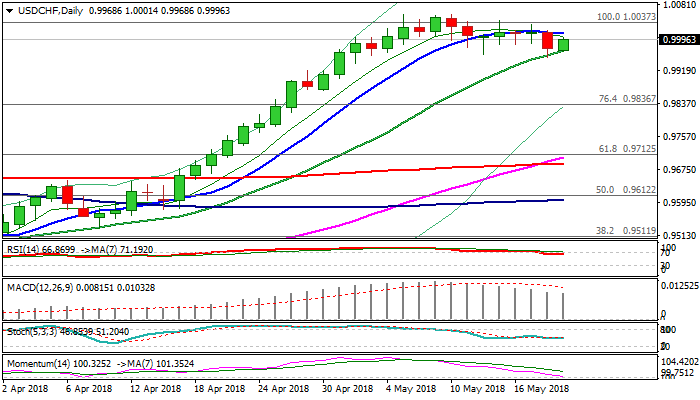

USDCHF Fresh Attempts Above Parity Ease Downside Risk But Close Above Needed For Firmer Bullish Signal

The pair probes again above parity level on Monday, following shallow 1.0056/0.9950 correction last Thu/Fri.

Fresh strength offsets negative signal on completion of Doji reversal pattern on daily chart after Friday’s close in red.

Fresh risk appetite on eased concerns over US/China trade dispute, boosted the greenback, which requires close above parity level to signal an end od corrective phase and shift near-term focus higher.

Bulls also need close above peaks at 1.0038 (27 Oct 2017) and 1.0056 (10May) to signal continuation of larger uptrend from 0.9187 (16 Feb low) towards targets at 1.0070 (Fibo 76.4% of 1.0343/0.9187) and 1.0170 (07 Mar 2017 high).

Rising 20SMA contained correction (currently at 0.9968) and continues to underpin, but bulls need to break sideways-moving 10SMA (1.0011) to generate fresh bullish signal.

Risk of deeper pullback however remains in play as momentum is weakening and approaching negative territory.

Initial bearish signal could be expected on break below 20SMA, which would expose key supports at 0.9881 (weekly cloud top) and 0.9851 (Fibo 23.6% of 0.9190/1.0056 rally), loss of which would generate stronger correction signal.

Res: 1.0011, 1.0038, 1.0056, 1.0070

Sup: 0.9968, 0.9950, 0.9881, 0.9851

Italian Populist Govt Beginning To Take Shape

Notes/Observations

- Italy populist govt spurs spending concerns, Italian yields continue to rise

- US-China trade war on hold for now

- Central bank divergent views continued to help USD surge -Whit Monday (Pentecost Monday) keeps European participation to a minimum (German, Austria Greece, Hungary, Iceland, Netherlands, Switzerland closed)

Asia:

- China agreed to purchase more US goods in effort to avoid trade war, but refused to commit to US demand to narrow trade gap by $200B

- Japan Apr Trade Balance ¥626B v ¥440Be; Exports registered its 17th straight rise (y/y: 7.8% v 8.7%e); Imports y/y: 5.9% v 9.8%e

Europe:

- UK Foreign Sec Johnson called on MPs to give PM May more time and space to deliver on her Brexit promises

- UK May Household Finance Index: 44.7 v 43.4 prior (highest level since Dec 2016)

- UK May Rightmove House Prices m/m: 0.8% v 0.4% prior; y/y: 1.1% v 1.6% prior

- India, EU send WTO list of U.S. imports potentially subject to additional tariffs in response to U.S. steel, aluminum tariffs

Americas:

- Treasury Sec Mnuchin: US has deal with China to cut trade deficit, will hold off on tariffs. “We have made very meaningful progress, and we agreed on a framework” (Note: Tariffs were on Chinese steel and aluminum, as well as $150B worth of other Chinese goods). President Trump was more interested in striking a good deal with Canada and Mexico than quickly finishing NAFTA talks in order to get a vote from Congress this year

- US Trade Rep Lighthizer: US might still resort to tariffs and other tools, including investment restrictions and export regulations unless China made real structural change to its economy

- Venezuela's Election Board: Incumbent Maduro won the elections (as expected, for a second term), the turnout was said to be 46.1% (US govt has said it would not recognize results)

Economic Data:

- (NG) Nigeria Q1 GDP Y/Y: 2.0% v 2.6%e

- (TW) Taiwan Apr Export Orders Y/Y: 9.8% v 7.9%e

- (PL) Poland Apr Sold Industrial Output M/M: -6.8% v -7.2%e; Y/Y: 9.3% v 8.5%e; Construction Output Y/Y: 19.7% v 24.8%e

- (PL) Poland Apr PPI M/M: 0.3% v 0.3%e; Y/Y: 1.1% v 0.9%e

- (TW) Taiwan Q1 Current Account: $20.1B v $26.6B prior

- (GR) Greece Mar Current Account -€1.0B v -€1.3B prior

- (HK) Hong Kong Apr CPI Composite Y/Y: 1.9% v 2.2%e

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 closed, FTSE +0.8% at 7,843, DAX closed, CAC-40 +0.7% at 5,651; IBEX-35 +0.2% at 10,135, FTSE MIB -0.6 at 23m319, SMI closed, S&P 500 Futures +0.5%]

- Market Focal Points/Key Themes: European markets opened mixed and moved higher as the session progressed; trading thin with little news; general optimism over easing trade war fears; several indices closed for holidays including Germany, Denmark, Austria, Switzerland, Norway, Hungary and Iceland; political considerations weigh on Italian equities; Euro weakness supports exporters in particular; in the Americas Canada and Chile closed for holidays; upcoming earnings in US session include Huami and Cheetah Mobile; focus on upcoming Fed meeting minutes to be released on Wednesday, as well as resumption of Brexit negotiations

Equities

- Consumer discretionary: AS Roma ASR.IT +6.0% (game win), Ryanair RYA.UK +1.7% (results)

- Healthcare: Astrazeneca AZN.UK +1.8% (FDA approval), Galapagos GLPG.BE +3.3 (study publication)

- Technology: Bigben Interactive BIG.FR -3.7% (analyst action)

- Speakers

- ECB’s Nowotny (Austria): Euro Area inflation would not rise dramatically, region not overheating

- Italy's Five Star and League said to have agreed on a prime minister; set to propose a cabinet to President Mattarella as early today. Florence University law professor Giuseppe Conte emerged as a possible premier. 5-star leader Di Maio noted that the cabinet lineup, if approved by the president, would include a joint minister of economic development and labor to be headed by Five Star (post could go to Di Maio himself); League leader Salvini said to be proposed as interior minister

- Russia Central Bank Yudaeva: CPI to gradually return back to the 4% target level; gradually shifting to a neutral policy setting. CPI seen between 3-4% by end 2018 while household inflation level remained elevated

- China Foreign Ministry spokesperson Lu Kang: No guarantee that trade frictions would reemerge at some point down the road

- Japan PM Abe reiterated view that BOJ policy management was appropriate. Govt and BOJ have reaffirmed its resolve to maintain the joint statement from 2013 on beating deflation

- IEA: Venezuela one of the biggest risks in oil markets in the coming months; could see a freefall in output

Currencies

- US dollar continued to experience a powerful surge aided by on diverging central bank views (mainly due to reflection of poor developments abroad). USD Index tested the 94 level for 5-month highs

- EUR/USD at fresh 2018 lows mainly due to the Italian political drama as a new populist govt takes shape. Market participants have reacted dramatically in recent days as the Italian 10-year bond yield rises to probe the 2.30 level before settling down.

- USD/JPY stayed above the 111 handle as rising US yields kept tailwinds behind the greenback.

- Every emerging market currency seemed offered against the USD as the Turkish Lira hit another record low, Indonesia Rupiah at its weakest level since 2015 and the Indian Rupee at a 16-month low

Fixed Income

- Bund Futures trade 35 ticks higher at 159.02 continuing to rebound in relatively quiet trade as many European markets are shut in observance of Whit Monday. Continued upside targets 159.25 then 159.42 with a reversal eyeing 158.55.

- Gilt futures trade at 121.65 up 26 ticks tracking the rebound in Bunds with support continuing to stand at 120.85 then 120.25. Upside resistance at 121.89 then 122.16.

- Monday’s liquidity report showed Friday's excess liquidity fell from €1.891T to €1.873T. Use of the marginal lending facility increased from €46M to €128M.

- Corporate issuance saw the week close out with over $32B in issuance.

Looking Ahead

- 06:00 (IL) Israel to sell Bonds

- 06:00 (RO) Romania to sell Bonds - 06:45 (US) Daily Libor Fixing

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 08:00 (ES) Spain Debt Agency (Tesoro) announces of upcoming issuance

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Apr Chicago Fed National Activity Index: 0.48e v 0.10 prior

- 08:55 (FR) France Debt Agency (AFT) to sell combined €4.2-5.4B in 3-month, 6-month and 12-month bills

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

- 11:30 (IT) Italy President Mattarella meets with 5-Star leader Di Maio

- 11:30 (US) Treasury to sell 3-Month and 6-Month Bills

- 12:00 (IT) Italy President Mattarella meets with League leader Salvini

- 12:15 (US) Fed’s Bostic (voter, dove) in Atlanta

- 14:05 (US) Fed’s Harker (non-voter, moderate) in NY

- 16:00 (US) Weekly Crop Progress Report

- 17:30 (US) Fed’s Kashkari (non-voter, dove) in MI

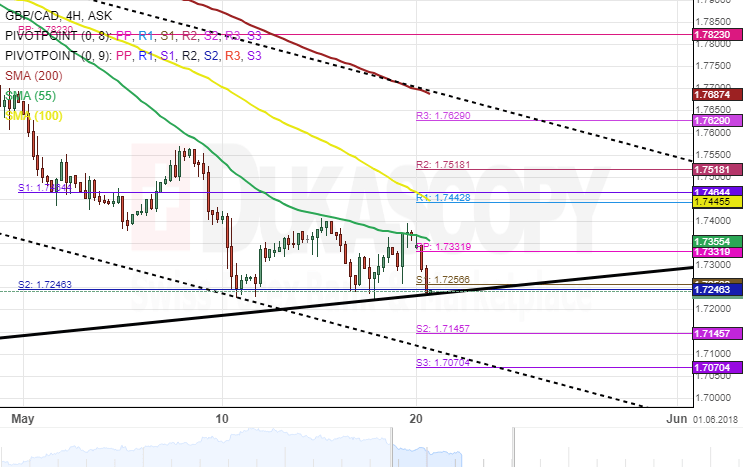

GBP/CAD 4H Chart: Bearish Momentum Continues

The Pound Sterling has declined substantially against the Canadian Dollar during the past one month. This bearish movement has pressured the exchange rate towards the lower boundary of a dominant ascending pattern.

During the morning hours of Monday's trading session, the GBP/CAD currency pair was bouncing between a resistance formed by the 55– hour simple moving average and a support cluster set by the combination of the weekly and the monthly PPs near the 1.72 area.

Everything being equal, a breakout through the bottom border of the dominant ascending channel could be expected within the following trading sessions. Meanwhile, on the daily time-frame, technical indicators flash strong sell signals.