Sample Category Title

Risk Appetite Returns as Trump Offers Concession ahead of US-China Trade Talks, Yen Weighed Down

Yen trades broadly lower today, expect versus New Zealand Dollar. Solid risk appetite is a factor pressuring the Yen. Nikkei closed up 0.47% at 28865.86, hitting the highest level in more than three months. Strong performance of cosmetics maker Shiseido is a factor driving the Japanese markets up. But mood in Asian is generally lifted by US President Donald Trump's concession to China. Trump tweeted that he wanted to help Chinese tech company ZTE to "get back into business, fast". That came just before Chinese Vice Premier Liu He's visit to Washington to resume trade talks. Hong Kong HSI also responded positively to the news and is trading up over 1.1% at the time of writing.

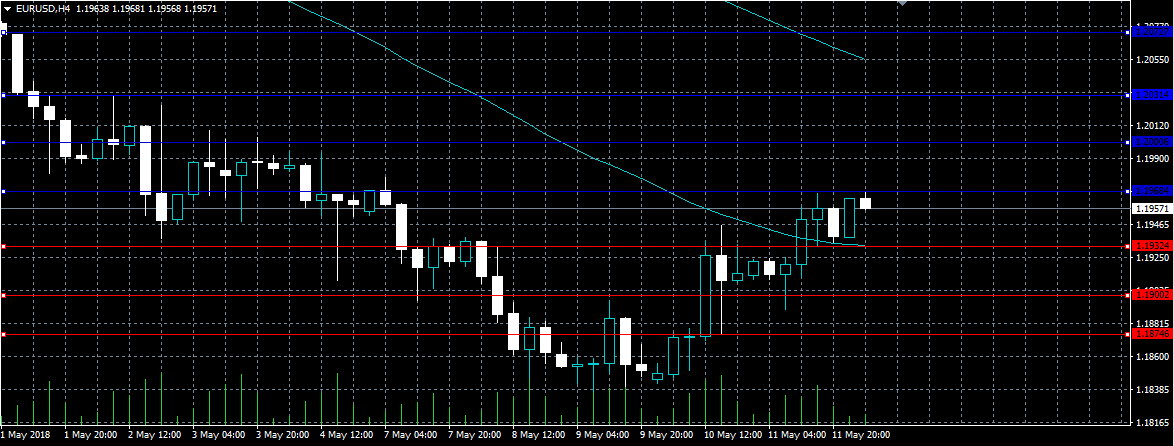

Elsewhere in the forex markets, Euro and Sterling are trading generally higher for the moment. But momentum is not too apparent. Technically, EUR/USD is struggling to take out 4 hour 55 EMA (now at 1.1961) and there is some distance from 1.2 handle. GBP/USD is also held below 1.3617 minor resistance and this is no sign of follow through rebound yet.

US Bolton: Europeans companies could face US sanctions

Trump's national security advisor John Bolton talked bout the decision to withdraw from the Iran nuclear pact on Sunday. He indicated that it's "possible" for the US to impose sanctions on European companies that continue to do business with Iran. And, he noted that "it depends on the conduct of other governments".

Bolton also added, "the president said in his statement on Tuesday that countries that countries that continue to deal with Iran could face U.S. sanctions. Europeans are going to face the effective U.S. sanctions, already are really, because much of what they would like to sell to Iran involves U.S. technology, for which the licenses will not be available." But he said he's "hopeful in the days and weeks ahead" there would be a deal that really works.

France Le Maire: US not economic gendarme of the planet

Separately, French Finance Minister Bruno Le Maire urged EU to " to work among ourselves in Europe to defend our economic sovereignty." And, EU should hold "collective discussions with the United States to obtain... different rules" covering European companies that do business with Iran. Le Maire added that "Do we accept extraterritorial sanctions? The answer is no." And, "Do we accept that the United States is the economic gendarme of the planet? The answer is no."

UK PM May reiterated commitment on nuclear pact to Iran

UK Prime Minister Theresa May reiterated UK's commitment to the Iran nuclear deal to Iran President Hassan Rouhani over a phone call during the weekend. And she urged release of jailed British Iranians "on humanitarian grounds". A Downing Street spokesman said that " it is in both the UK and Iran's national security interests to maintain the deal and welcomed president Rouhani's public commitment to abide by its terms, adding that it is essential that Iran continues to meet its obligations."

Foreign Ministers of the UK, Germany and France will meet this Tuesday to discuss on keeping the Iran nuclear after after US withdrawal.

No breakthrough in NAFTA talks as May 17 deadline looms

The latest round of NAFTA negotiations ended last week without a breakthrough. US Trade Representative Robert Lighthizer just said pledge to continue working with Mexico and Canada. House Speaker Paul Ryan has given a May 17 deadline for notification of the new agreement. That's a working deadline for having the new agreement to go through the current Congress by December.

But both Canadian Foreign Minister Chrystia Freeland and Mexican Economy Minister Ildefonso Guajardo are more focused on the "quality" of the deal rather than the pressure of time. Freeland said that "the negotiations will take as long as it takes to get a good deal." Guajardo emphasized that "we're not going to sacrifice the quality of an agreement because of pressure of time."

In the calendar

On the data front, Japan domestic CGPI rose 2.0% yoy in April. Machine tools orders rose 22.2% yoy. The calendar is empty today and markets would listen to comments from a number of ECB and Fed officials.

Looking ahead, there is no central bank activities except RBA minutes on Tuesday. Politically, trade will be a major theme as US-China negotiation will resume in Washington. Also, there is a working deadline of May 17 for NAFTA negotiations. New Zealand will also release its annual budget. On the data front, UK and Australian employment data, Japan GDP and Canadian CPI, could be the most market moving. US retail sales and regional Fed surveys would be watched too. Here are some highlights for the week:

- Tuesday: RBA minutes; China fixed asset investment, industrial production, retail sales; Japan tertiary industry index; German GDP, ZEW; Eurozone GDP, industrial production; Swiss PPI; UK employment; US retail sales, Empire state manufacturing, business inventories, NAHB housing index

- Wednesday: Australia wage price index; Japan GDP; German CPI final, Eurozone CPI final; Canada manufacturing sales; US housing starts and building permits, industrial production;

- Thursday: New Zealand PPI; Australia employment; New Zealand budget; Canada foreign securities purchases; US Philly Fed survey, jobless claims, leading index

- Friday: Japan CPI; German PPI; Eurozone current account, trade balance; Canada CPI

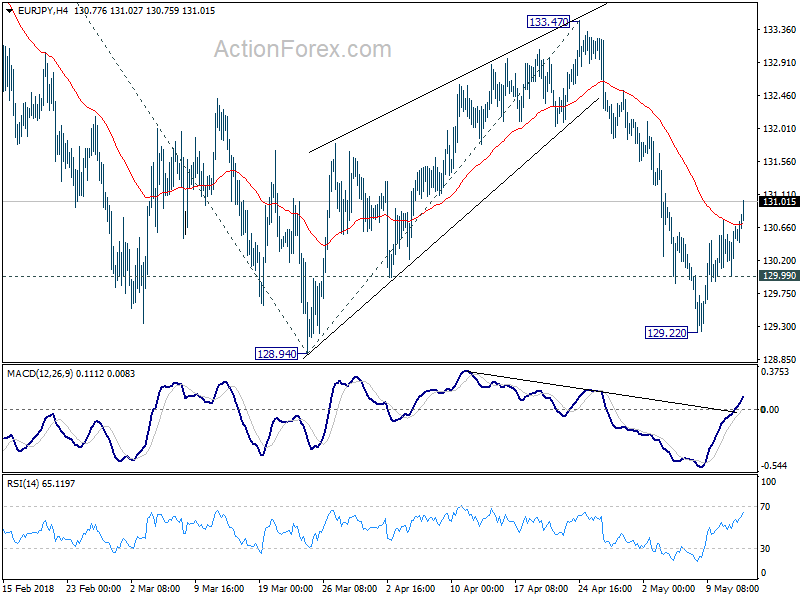

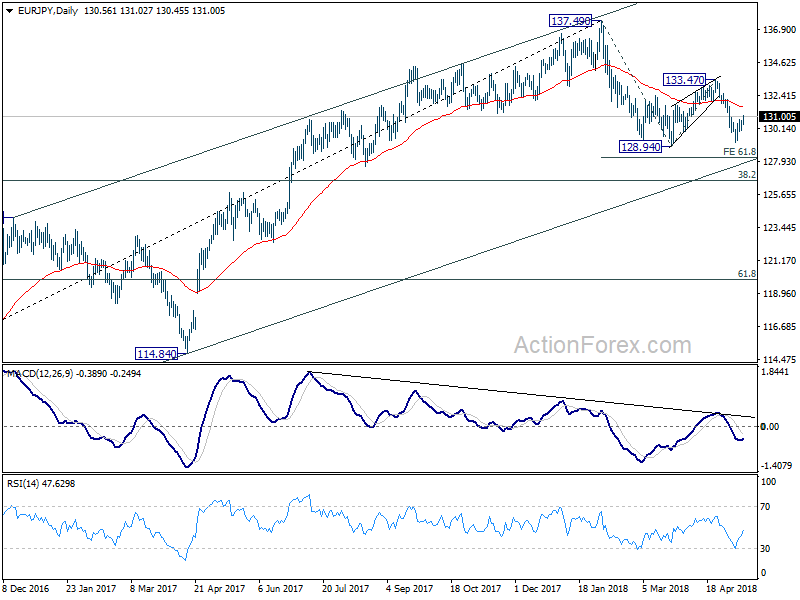

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.14; (P) 130.41; (R1) 130.83; More....

EUR/JPY's rebound from 129.22 short term bottom extends higher to as high as 131.02 so far. With 4 hour 55 EMA taken out, intraday bias is on the upside for further rise to 55 day EMA (now at 131.62). Nonetheless, we'd expect strong resistance below 133.47 resistance to bring fall resumption. Below 129.99 minor support will turn bias back to the downside for 128.94. Break will resume the corrective fall from 137.49 and target 61.8% projection of 137.49 to 128.94 from 133.47 at 128.18 next.

In the bigger picture, for now, price actions from 137.49 are viewed as a corrective pattern only. Hence, while, deeper decline would be seen, strong support is expected at 38.2% retracement of 109.03 to 137.49 at 126.61 to contain downside and bring rebound. Up trend from 109.03 (2016 low) is expected to resume afterwards. Though, sustained break of 126.61 will be an important sign of trend reversal and will turn focus to 124.08 resistance turned support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Apr | 2.00% | 2.00% | 2.10% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Apr P | 22.00% | 28.10% |

Iran Deal Back In The Headlines As Potential Fallout Comes To Light

Following on from the US withdrawal from the Iran Deal, UK PM May reaffirmed her commitment to ensuring the deal is upheld. She spoke via phone with the Iranian President yesterday, in advance of a meeting of the UK, France, Germany and Iran in Brussels tomorrow. Over the weekend, US National Security Advisor John Bolton said that US sanctions on European companies that maintain business dealings with Iran were possible. It remains to be seen if this threat will be upheld, which would be a further blow to US/European relations. EURUSD is higher at 1.19600, having risen as far as 1.19690 earlier. Elsewhere, Canadian PM Trudeau has said he is optimistic a NAFTA agreement can be reached. US Lawmakers want a deal by Thursday in order to give enough time to get it through Congress. USDCAD dropped to 1.27693 after closing at 1.27985 on Friday.

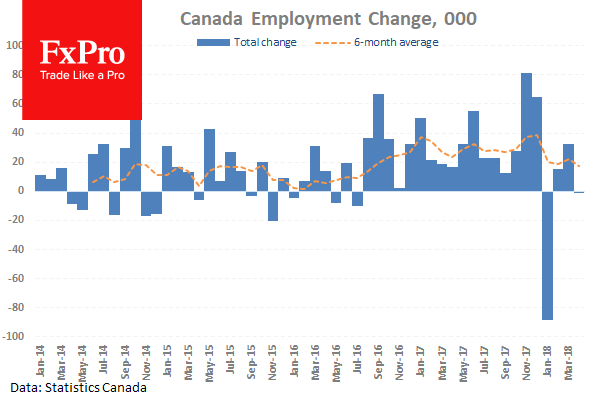

Canadian Unemployment Rate (Apr) was as expected, unchanged at 5.8%. Participation Rate (Apr) was 65.4% versus an expected 65.5%, against 65.5% prior. Net Change in Employment (Apr) was -1.1K versus an expected 17.4K, against a prior 32.3K. USDCAD moved up from 1.27321 to 1.27764 after this data release.

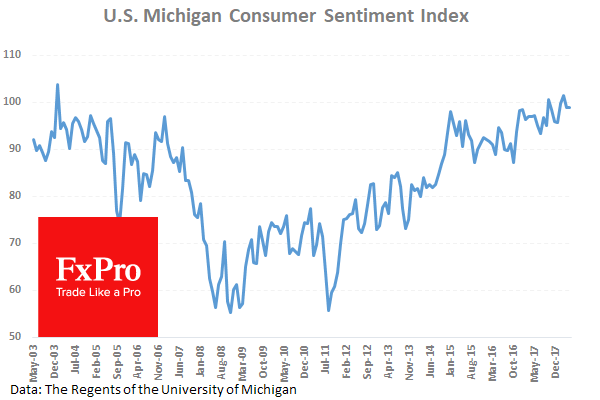

US Michigan Consumer Sentiment Index (May) was 98.8 versus an expected 98.5, against a previous 98.8. USDJPY rose from 109.256 to 109.328 following this data release.

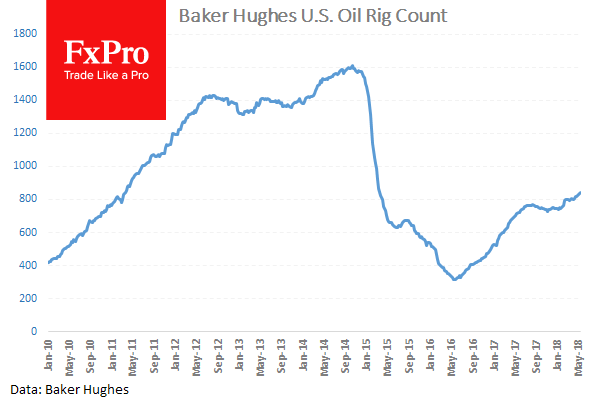

Baker Hughes US Oil Rig Counts was released with a headline number of 844 from last week’s number of 834. As this number creeps higher, more and more rigs are coming into operation, increasing the supply of oil and adding downward pressure on prices. WTI Oil fell from $71.37 to $70.41 after this data release.

EURUSD is up 0.18% overnight, trading around 1.19597.

USDJPY is up 0.03% in early session trading at around 109.395.

GBPUSD is up 0.17% this morning, trading around 1.35607.

USDCAD is down -0.03% overnight, currently trading around 1.27877.

Gold is up 0.09% in early morning trading at around $1,319.99.

WTI is down -0.13% this morning, trading around $70.43.

Fed Speakers Take Centre Stage As Markets Look To Week Ahead

At 06:45 GMT, Fed Member Mester is due to speak at the Central Banking Series hosted jointly by the Global Interdependence Center and Bank of France, in Paris. Audience questions are expected to follow. USD crosses may see spikes in volatility during this event.

At 13:40 GMT, Fed Member Bullard is expected to speak in a scheduled event at the Consensus Blockchain event in New York. USD crosses may be affected by any comments made.

Major data releases for this week:

On Tuesday, at 01:30 GMT, RBA Meeting Minutes will be released.

At 06:00 GMT, German Gross Domestic Product data will be released.

At 08:30 GMT, UK Average Earnings Data will be released.

At 09:00 GMT, Eurozone Gross Domestic Product data will be published.

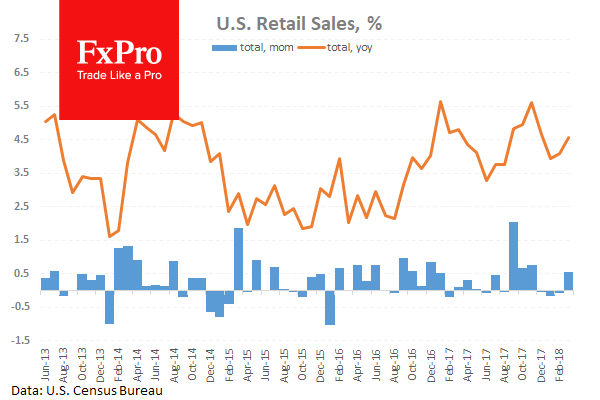

At 12:30 GMT, US Retail Sales data will be out.

On Wednesday, at 07:00 GMT, German Harmonized Index of Consumer Prices data will be published.

At 09:00 GMT, Eurozone Consumer Prices Index data will be released.

On Thursday, at 01:30 GMT, Australian Unemployment data will be out.

On Friday, at 12:30 GMT, Canadian Retail sales and Consumer Price Index data will be released.

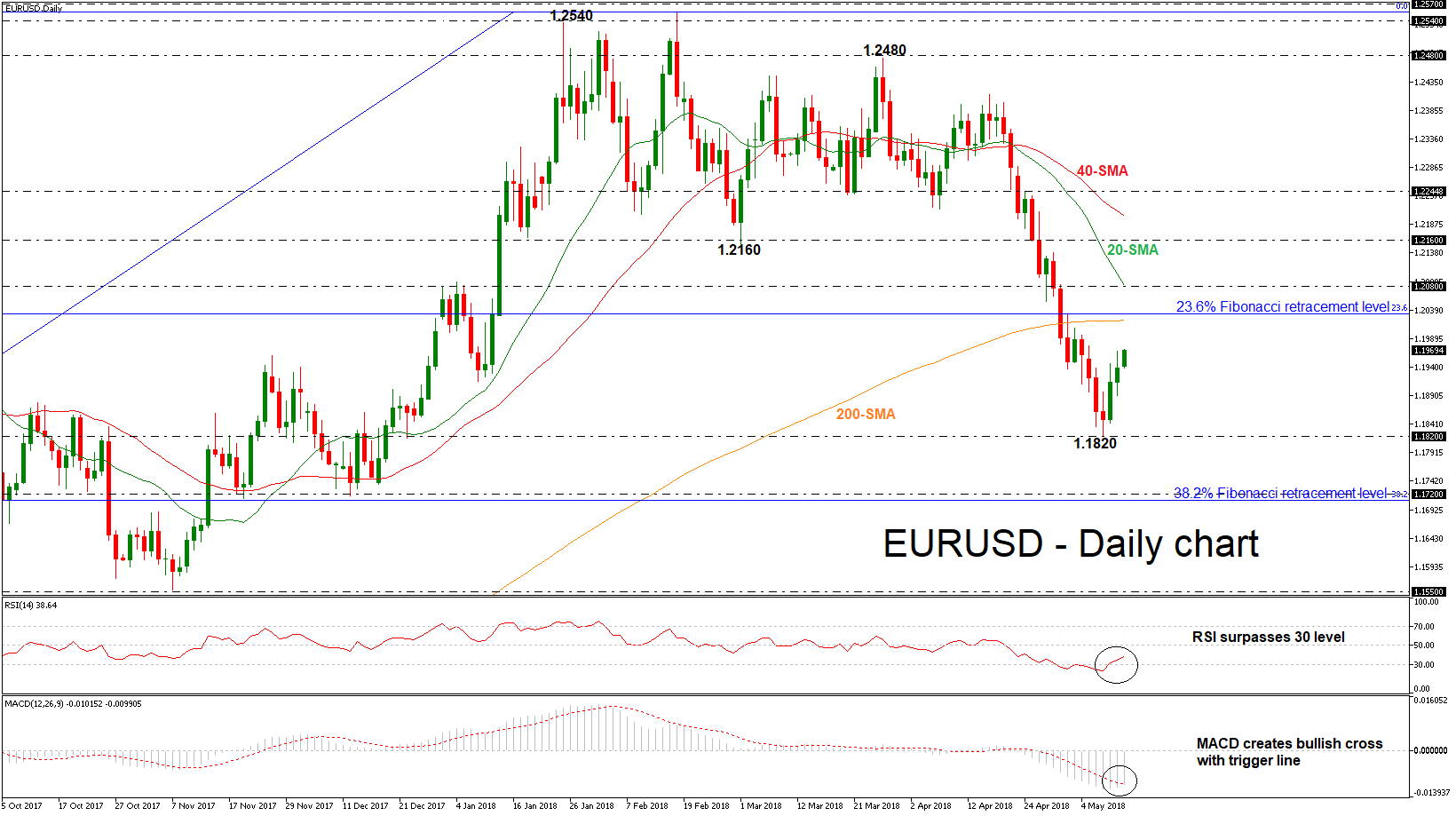

EURUSD Pares Some Losses After Hitting 5-Month Low Of 1.1820

EURUSD has been edging slightly higher since it found a strong support on the 1.1820 barrier last Wednesday, creating two consecutive bullish days and paring some of the previous weeks losses. The 1.1820 key level is a new almost five-month low and the price is still developing below the 23.6% Fibonacci retracement level of 1.2030 of the upleg from January 3 to February 16.

Short-term momentum indicators are also pointing to a continuation of the bullish bias. The RSI indicator holds just above the 30 level and is pointing upwards, while the MACD oscillator is ready for a bullish crossover with its trigger line in the negative territory.

In the event of a continuation of the upside reversal, the 23.6% Fibonacci and the 200-day SMA could act as strong resistance barriers for traders. A penetration of these critical levels would shift the medium-term outlook to a more neutral one as it would take the pair towards the 1.2080 resistance, which overlaps with the 20-day SMA at the time of writing. Further gains would lead the way towards the 1.2160 region, taken from the low on March 1.

On the flip side, further losses should see a re-challenge of the almost five-month low acting as a major support. A slip below this area would reinforce the bearish structure in the daily chart and open the way towards the 1.1720 support, which stands near the 38.2% Fibonacci mark.

To sum up, EURUSD posted four red weekly sessions, however, the last week recorded limited losses, indicating that a bullish correction is possible in the near-term.

EURO Still Correcting To The Upside

The euro continues to correct to the upside against the US dollar, with price earlier hitting 1.1968, marking the highest trading level for the EURUSD siting May 4th. The recent move lower in the value on the US dollar index has largely been driven by weaker than expected CPI and PPI inflation figures from the United States economy. As bullish momentum builds, traders will look for further upside in the EURUSD pair, with the 1.2000 level the key resistance area to watch.

The EURUSD pair is intraday bullish while trading above the 1.1932 level, further upside towards 1.2000 and 1.2031 seems possible.

If the EURUSD pair moves below the 1.1932 level, we may see a correction back towards the 1.1900 and 1.1874 support levels.

GBPUSD Still Bearish Below 1.3600

The British pound continues to struggle against the US dollar in early Monday trading, with buyers again failing to move price above the key 1.3600 level. The GBPUSD pair currently trades around the 1.3560 level, after being strongly rejected from the just below the 1.3600 level on Friday. Sterling traders now look towards a key break of the 1.3500 to 1.3600 trading-range, and the next directional move in the US dollar index.

The GBPUSD pair remains bearish while trading below the 1.3600 level. Further losses towards 1.3531 and 1.3501 seem possible.

If the GBPUSD pair starts to trade above the 1.3600 level, key intraday resistance is now found at the 1.3616 and 1.3650 levels.

A Quiet Start To A Busy Week

By looking at Monday's economic release schedule, traders have very little to be excited about. However, that will quickly change later in the week as global data flows generate significant headlines.

There are no reports scheduled for release during European trade. In North America, a pair of Federal Reserve speakers could set the tone for monetary policy speculation throughout the week.

Federal Open Market Committee (FOMC) member, Loretta Mester, is scheduled to deliver a speech at 06:45 GMT. The Fed governor was part of the policy-setting committee that voted to keep interest rates on hold at the start of the month.

At 13:40 GMT, Federal Reserve Bank of St. Louis President, James Bullard, will deliver a speech to the fourth annual Consensus summit hosted by Coindesk. Consensus is the biggest blockchain event of the year. This year, more than 7,000 people are expected to attend, including representatives from government, industry and academia.

The economic calendar picks up on Tuesday with reports on Chinese retail sales, Eurozone Gross Domestic Product (GDP) and UK employment. In the United States, the Department of Commerce will report on retail sales for the month of April.

In currencies, the US dollar continued to trade near 2018 highs against a basket of six rivals, although gains have slowed in recent sessions. The greenback has gained more than 3% over the past month. Prior to the latest rally, the dollar had spent much of 2018 in the red.

EUR/USD

Europe's common currency is in the midst of an upward correction, with prices rebounding roughly 140 pips from last Wednesday's swing low. EUR/USD is now valued at 1.1959, having gained 0.1% from the previous close. Though the downtrend remains intact, the currency pair could be poised for bigger gains in the near term as the greenback runs into fatigue. The bulls are eyeing a return to 1.2050 levels for confirmation of an uptrend. On the opposite side of the ledger, immediate support is located at 1.1880.

GBP/USD

Cable is also in the midst of a correction, though price action remains choppy. GBP/USD bottomed at 1.3467 on Thursday but has since recovered to around 1.3560. UK employment data on Tuesday could provide the pair with the next major trading catalyst. At the time of writing, immediate support is located at the psychological 1.3500 level. On the opposite side of the spectrum, resistance is likely seen at 1.590.

USD/JPY

The USD/JPY has backed off from its recent high, as the bulls failed to extend the rally toward 110.00 and beyond. The pair is now trading around 109.24, where it continues to trade within a predefined range of 108.80 and 109.60.

Key Market Themes To Watch This Week

Trade resolution

A month after the U.S. Commerce Department banned one of China's biggest tech companies, ZTE, from exporting U.S. products, President Trump announced his willingness to help the company get back in business. Thisunusual intervention by the U.S. President comes amid tense talks with China on trade deal renegotiations. With Chinese Vice Premier, Liu He, expected to visit Washington this week to resume talks, it seems Trump’s move is a good starting point, and likely to be welcomed by markets. Many policymakers will criticize such a reversal, but from an investor’s perspective, it’s a sign of easing relations between the world’s two largest economies and should support risk-taking.

U.S. Dollar Strength

The surge in U.S. yields and USD strength has proved to be problematic for emerging markets over the past several weeks. The higher U.S. yields go, the more outflows are expected to be seen from emerging markets. As of Monday morning, the dollar index DXY appears to be showing signs of weakness, declining from 92.55 to 92.38. Currency traders should also keep an eye on the U.S. 10-year treasury yields, as failing to break above 3% may suggest a short-term top. A significant break above the 3% benchmark requires faster tightening expectations from the Federal Reserve; for this to happen, the economy must show signs of over-heating. However, we are not there yet;U.S. April retail sales figures, scheduled for release on Tuesday,isthe key economic data release to watch this week. Markets expect a 0.4% increase in April, from 0.6% in the previous month.

Did oil find a top?

Brent crude hit a new three-and-a-half year high on Thursday, reaching $78 after the U.S’s withdrawal from the Iranian nuclear deal. The 26% surge from February lows was far from expected, but the record demand from Asia, fears of supply disruption, and more importantly, the risk of war between Iran and Israel, led traders to buy call options at $100. Given thatthe risk of a direct confrontation between Iran and Israel has abated, markets will turn their focus to fundamentals and a $100 target will likely be unrealistic. While demand has been strong enough and OPEC and Russia are exceeding expectations on supply cuts, prices are likely to remain elevated. Meanwhile, soaring U.S. shale output will continue to put a cap on prices. However, the most significant downside risk is President Trump intervening in oil markets by pressuring OPEC members to increase output.

Currencies: USD Rally Slows After Modest US CPI

Rates: Sideways trading ahead

Last week's consolidation on core bond markets is expected to continue at the start of the trading week given the thin eco calendar. Central bankers are expected to confirm recent guidance on monetary policy. Italian political developments are expected to weigh on BTP's, but shouldn't influence global sentiment.

Currencies: USD rally slows after modest US CPI

At the end of last week, the dollar lost slightly ground. A modest US CPI report slowed the recent rise in US yields and in the dollar. The subsequent risk-on context was also a slightly USD negative. The eco calendar is thin today. Despite a rather soft US CPI, we don't see a trigger for a protracted rebound in EUR/USD at this moment.

The Sunrise Headlines

- US stock markets ended mixed on Friday with Dow Jones putting a slightly better performance (+0.4%). Most Asian equity indices trade positive overnight with China outperforming (+1%).

- Italy's leading populist parties are within striking distance of forming a government in the EMU's third-largest economy after reaching tentative agreement on a common platform — but not on a choice of prime minister. (FT)

- The US threatened to impose sanctions on European companies that do business with Iran, as the remaining participants in the Iran nuclear accord stiffened their resolve to keep that agreement operational. (Reuters)

- The UK must spell out plans for post-Brexit co-operation on foreign and security policy before next month's European Council if it is to live up to its goal of continuing to work closely with its EU allies, lawmakers said (BB)

- Andrej Babis's Ano party and the Czech Social Democrats have agreed a draft coalition agreement, edging the Czech Republic closer to a government nearly seven months after an inconclusive parliamentary election. (FT)

- St. Louis Fed Bullard (dove) spelled out the case against any further interest rate increases, saying rates may already have reached a "neutral" level that is no longer stimulating the economy. (Reuters)

- Today's eco calendar only contains second tier eco data, but a lot of central bank governors are scheduled to speak.

Currencies: USD Rally Slows After Modest US CPI

USD running into resistance after modest US CPI .

Thursday's softer than expected US CPI caused some kind of change in the mind-set on global markets. The report was close to consensus, but convinced markets that the Fed won't change its gradual path to policy normalisation. This slowed the rise in US yields and in the dollar and supported equities. EUR/USD rebounded to close the week at 1.1946. USD/JPY tested the 110 area on Thursday, but closed at 109.39.

Overnight, last week's trends continue in Asia. Asian equities mostly show modest gains and US equity futures suggest that the US equity rally might continue. USD/JPY hovers in the lower half of the 109 big figure. EUR/USD revisited last week's correction top in the 1.1968 area, but no follow-through gain occurred. Euro investors probably keep an eye at the political developments in Italy as the 5SM and League parties are making good progress to reach an agreement to form a government.

Today, there are few eco data in Europe or in the US, but several ECB and Fed members will speak. Investors will also keep an eye at the geopolitical developments. Tension in Korea are apparently easing. US president Trump recently also held a more constructive tone on the trade talks with China. The picture in the Middle East looks more complicated. In a day-to-day perspective, the risk-on context combined with relative calm on the (US) interest rate markets looks a tentatively negative for the dollar. However, in somewhat longer term perspective, we don't see profound change. Short-term developments (both economically and from a monetary point of view) still look modestly USD supportive. EUR/USD returning north of 1.20 would cause some doubts on the USD, but even in that scenario we don't see a trigger for a powerfull EUR/USD comeback in the very near future.

On Thursday, sterling lost substantial ground as the BoE left its policy rate unchanged at 0.5%. The BoE admitted that CPI inflation has declined faster than expected, but still sees some excess demand over time. This keeps the door open for a very gradual tightening over the policy horizon. EUR/GBP rebounded north of 0.88. The markt now sees a chance of about 65% of a rate hike In november. EUR/GBP 0.8850 is a first resistance. Brexit remains a wild card, but unless the process swirls completely out of control, we expect EUR/GBP to hold the 0.89/0.86 trading range. Decent UK eco data might make investors reconsidering the chances for an August rate hike

EUR/USD: downtrend taking a breather

Trump Working With China’s Xi To Resolve ZTE Issue

General Trend

- Asian equity markets trade generally higher; Hang Seng again outperforms

- US President Trump says he is working with China regarding telecom name ZTE

- Australia’s Telstra declines over 3% after giving cautious outlook

- China PBoC conducts 1-year medium-term lending facility (MLF) to offset maturing funds

- Malaysian assets face selling pressure in first trading session since last week’s elections; later pare losses

- Indonesia government bonds rally

- US/China trade talks are expected to be held on Tuesday (US financial press)

- OPEC expected to be able to offset oil losses from Iran sanctions - press

Headlines/Economic Data

Japan

Nikkei 225 opened -0.2%; closed +0.5%

- Topix Real Estate Index +2.9%, Securities +1%. Marine Transportation +0.9%, Iron & Steel +0.9%, Retail trade +0.7%

- (JP) JAPAN APR PPI M/M: 0.1% V 0.1%E; Y/Y: 2.0% V 2.0%E

- (JP) BoJ Gov Kuroda: Govt has made progress to restore fiscal health; more needs to be done on structural reforms - Parliament comments (Friday after the close)

- (JP) Japan PM Abe to consider meeting with North Korea's Kim, but significant obstacles remain - Nikkei

Korea

- Kospi opened +0.2%

- (KR) Major South Korea financial firms are getting ready to kick off a massive recruiting effort in H2 of this year - Korean press

- (KR) North Korea planning to dismantle nuclear test site in a ceremony scheduled between May 23-25th - Korean press

- (KR) South Korea sells KRW650B v KRW650B indicated in 10-year bonds: avg yield 2.785% v 2.62% prior

China/Hong Kong

- Hang Seng opened +1.2%, Shanghai Composite +0.1%

- Hang Seng Industrial Goods index +2.4%, Property & Construction +1.7%, Financials +1.6%, Info Tech +1.5%

- 763.HK "President Xi of China, and I, are working together to give massive Chinese phone company, ZTE, a way to get back into business, fast. Too many jobs in China lost. Commerce Department has been instructed to get it done!" - Tweet from President Trump

- (CN) PBoC Adviser reiterates sees no major short-term change in yuan (CNY) rate - Chinese Press

- (CN) PBOC CONDUCTS CNY156B V CNY367.5B PRIOR IN 1-YR MEDIUM-TERM LENDING FACILITY (MLF) AT 3.3% V 3.3% PRIOR; CONDUCTS CNY80.1B IN PLEDGE SUPPLY LENDING (PSL) LOANS; the MLF injection effectively rolls over the same amount which is due to mature

- (CN) China insurers are said to be channeling funds through shadow lenders to real estate and local government infrastructure projects in a bid to boost returns - financial press

- (CN) China PBoC sets yuan reference rate 6.3345 v 6.3524 prior

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the second consecutive day

- (CN) China PBOC Quarterly Report: Will properly implement the prudent and neutral monetary policy to create a moderate financial environment for supply-side structural reform and high-quality development - Xinhua

- (CN) China Securities Journal comments on MLF operations, noting they have limitations, mainly in terms of the narrow transmission through which liquidity is provided

Australia/New Zealand

- ASX 200 opened 0.0%, closed 0.3%

- ASX 200 Resources index +1.2%, Energy +1.2%, Financials +0.1%; Telecom -3.1%, Utilities -0.5%

- (NZ) New Zealand Apr Performance of Services Index: 55.9 v 58.6 prior

- Telstra, TLS.AU Reports Q3 Postpaid handheld ARPU ex. MRO A$65.35 v A$65.92 in H1; Affirmed expects FY18 EBITDA in bottom end of A$10.1-10.6B range, total dividend of A$0.22/share

- (AU) Australia PM Turnbull’s lead as preferred PM over opposition leader Bill Shorten also jumped eight points to 46-32% - press

- Healthscope, HSO.AU Confirms rival A$2.50/share cash takeover offer from Brookfield Asset Management

- Specialty Fashion, [+48%], SFH.AU Completes strategic review: Confirms to sell some brands to Noni B for A$31M cash; To keep its ASX listing and retain City Chic brand

- (AU) Australia AOFM launches syndicated tap of June 2039 bond, pricing guidance 35-37bps/10-yr Futures

Other Asia

- Hon Hai [2317] rises over 3% on capital reduction plan

North America

- XRX Confirms it has terminated merger agreement Fujifilm; enters into new agreement with shareholders Icahn and Deason; Under the settlement agreement, John Visentin to be named as Vice Chairman and CEO

- XRX Fujifilm: Dispute's Xerox's 'unilateral' decision to terminate merger transaction; all options are available including legal action

Europe

- (UK) Apr Visa Consumer Spending 3M/3M: -1.6% v -1.3% prior (largest fall since July 2017)

- (IT) Italy 5-Star Movement and League Party reached consensus around measures that include a universal basic income, a flat tax and roll back of pension reforms from 2011

- (UK) According to CIPD, UK employers expect avg 2.1% pay settlement over next 12-months v 1.8% last quarter

- (IE) Ireland Apr Construction PMI: 60.7 v 57.5 prior

- (NO) Norway Central Bank (Norges) Gov Olsen: Outlook shows it will soon be right to hike key interest rate - Op-Ed

Levels as of 02:00ET

- Hang Seng +1.1%; Shanghai Composite +0.5%; Kospi -0.1%

- Equity Futures: S&P500 +0.4%; Nasdaq100 +0.4%, Dax +0.2%; FTSE100 +0.1%

- EUR 1.1968-1.1941; JPY 109.45-109.21; AUD 0.7565-0.7541;NZD 0.6974-0.6949

- Jun Gold -0.1% at $1,319/oz; Jun Crude Oil -0.4% at $70.45/brl; Jul Copper +0.4% at $3.12/lb