Sample Category Title

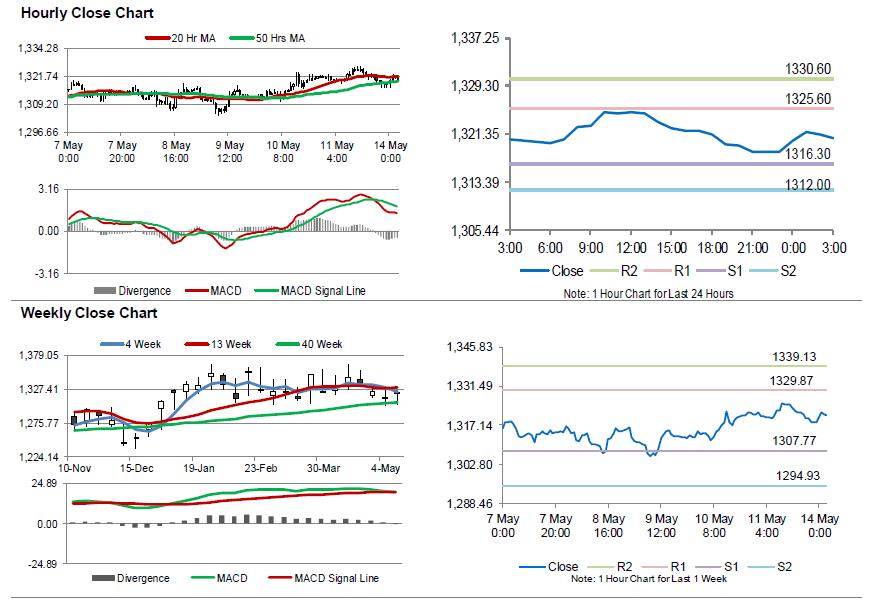

Gold: Yellow Metal Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, Gold declined 0.13% against the USD and closed at USD1319.60 per ounce on Friday, reversing its previous session gains.

In the Asian session, at GMT0300, the pair is trading at 1320.60, with gold trading 0.08% higher against the USD from Friday’s close.

The pair is expected to find support at 1316.30, and a fall through could take it to the next support level of 1312.00. The pair is expected to find its first resistance at 1325.60, and a rise through could take it to the next resistance level of 1330.60.

The yellow metal is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

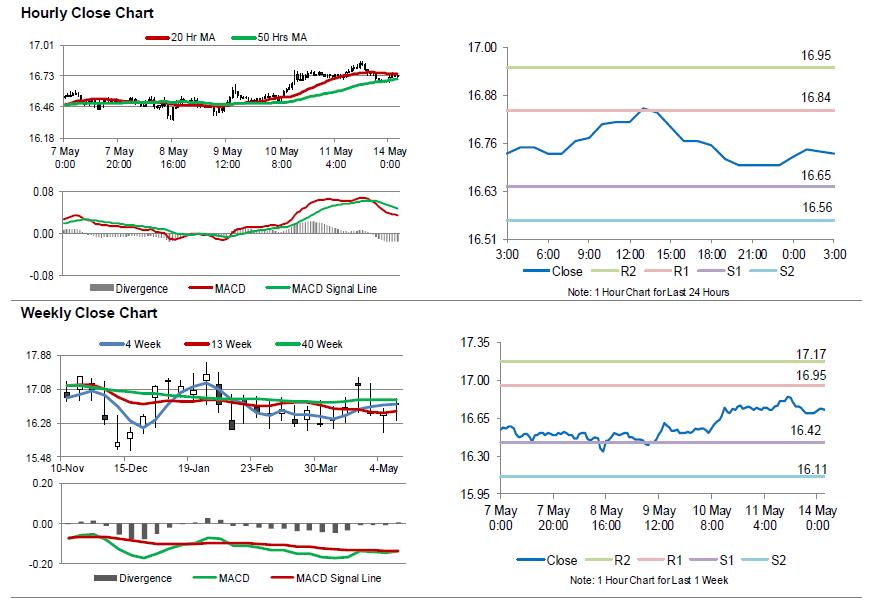

Silver: White Metal Trading Between Its MA’s

For the 24 hours to 23:00 GMT, Silver declined 0.30% against the USD and closed at USD16.70 per ounce on Friday.

In the Asian session, at GMT0300, the pair is trading at 16.73, with silver trading 0.18% higher against the USD from Friday's close.

The pair is expected to find support at 16.65, and a fall through could take it to the next support level of 16.56. The pair is expected to find its first resistance at 16.84, and a rise through could take it to the next resistance level of 16.95.

The white metal is trading between its 20 Hr and 50 Hr moving averages.

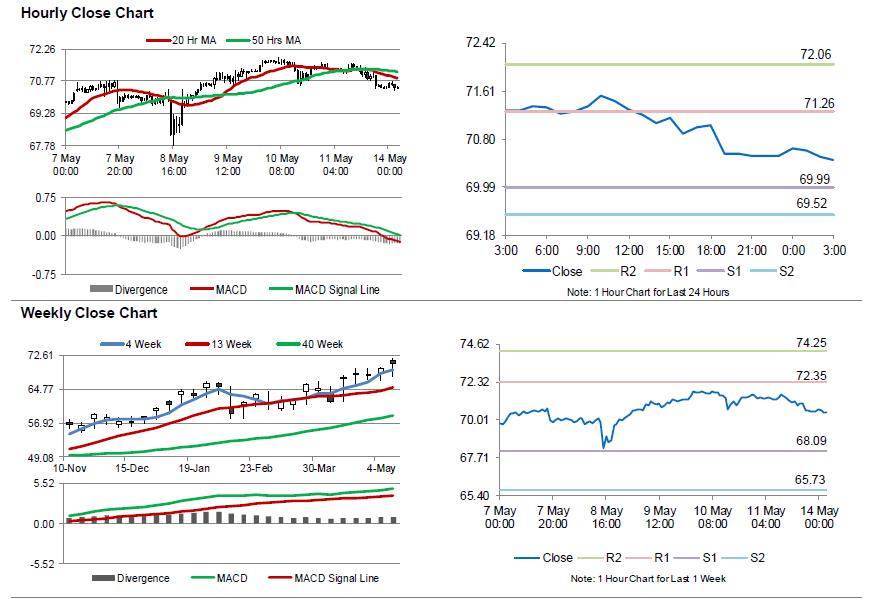

Crude Oil: Oil Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, Crude Oil declined 1.36% against the USD and closed at USD70.56 per barrel on Friday, after fresh figures from Baker Hughes disclosed that active oil rigs in the US rose for the sixth straight session by 10 to 844 in the week ended 11 May and amid uncertainty over the US sanctions against Iran.

In the Asian session, at GMT0300, the pair is trading at 70.45, with oil trading 0.16% lower against the USD from Friday’s close.

The pair is expected to find support at 69.99, and a fall through could take it to the next support level of 69.52. The pair is expected to find its first resistance at 71.26, and a rise through could take it to the next resistance level of 72.06.

Crude oil is trading below its 20 Hr and 50 Hr moving averages.

Traders Getting More Bearish on AUD and Less Bullish on GBP

We initiate coverage on speculators' activities on major FX futures. According to CFTC's Commitments of Traders, speculators were bearish (NET SHORT) on CHF, JPY, AUD and CAD in the week ended May 8. Meanwhile, they remained bullish (NET LENGTH) over EUR, GBP and NZD. However, the positive sentiment has deteriorated of late. As such, NET SHORT for USD Index markedly reduced to 549 contracts, from 1 734 contracts in the prior week. A return to Net LENGTH, for the first time since March, in weeks ahead is likely, if the trend continues.

NET SHORT for CHF futures increased +13 146 contracts to 32 602, while those for JPY and AUD contracts rose +4 057 and +11 094 contracts to 5 462 and 16 766, respectively. Bears have been dominating AUD recently. NET SHORT has reached the widest level not seen since early January, after drifting from NET LONG in April. This appears consistent with the Aussie's selloff. NET SHORT for CAD futures dropped -3 674 contracts to 57 017 for the week. The sentiment for CAD has improved recently with net position stabilized since early April.

With speculations added to both sides, NET LENGTH for EUR futures dipped slightly, by -63 contracts, to 120 505. NET LENGTH for GBP futures slumped -17 384 contracts to 8 988. The decline in speculative long positions was more than quadrupling that in speculative short positions during the week. Indeed, sentiment in sterling has soured since three weeks ago and the decrease in Net LENGTH has been accelerating. The situation is likely driven by the disappointing 1Q18 GDP growth data and a more dovish BOE. For three weeks in a row, NET LENGTH for NZD futures has been narrowing. down -4 027 contracts to 12 546 last week. Over the past week, ongoing drop (-895 contracts) in speculative long positions was accompanied with a significant increase in speculative short (+3 132 contracts), sending the NET LENGTH to 12 546 contracts, down -4 027 from a week ago.

Traders Stayed Mixed about Energy as Trump Pulled Out of Iran Deal

Speculators were mixed over the energy complex in the week ended May 8. Net LENGTH for crude oil futures plunged -10 799 contracts from a week ago to 679 928. NET LENGTH of heating oil rose +5 463 contracts to 32 460 while net LENGTH for gasoline added +1 726 contracts to 84 753. Net SHORT for natural gas increased -124 023 contracts to 124 023 for the week.

Speculators were also mixed over the precious metal complex last week. Net LENGTH for gold added +661 contracts to 107 440. Silver's net SHORT slipped -7 075 contracts to 121 for the week. For PGMs, net LENGTH for platinum dropped -376 contracts to 10 388 while that for palladium was down -469 contracts to 10 296.

No breakthrough in NAFTA talks as May 17 deadline looms

The latest round of NAFTA negotiations ended last week without a breakthrough. US Trade Representative Robert Lighthizer just said pledge to continue working with Mexico and Canada.

House Speaker Paul Ryan has given a May 17 deadline for notification of the new agreement. That's a working deadline for having the new agreement to go through the current Congress by December.

But both Canadian Foreign Minister Chrystia Freeland and Mexican Economy Minister Ildefonso Guajardo are more focused on the "quality" of the deal rather than the pressure of time.

Freeland said that "the negotiations will take as long as it takes to get a good deal."

Guajardo emphasized that "we're not going to sacrifice the quality of an agreement because of pressure of time."

Bolton: Europeans Companies could face US sanctions

Trump's national security advisor John Bolton talked bout the decision to withdraw from the Iran nuclear pact on Sunday. He indicated that it's "possible" for the US to impose sanctions on European companies that continue to do business with Iran. And, he noted that "it depends on the conduct of other governments".

Bolton also added, "the president said in his statement on Tuesday that countries that countries that continue to deal with Iran could face U.S. sanctions. Europeans are going to face the effective U.S. sanctions, already are really, because much of what they would like to sell to Iran involves U.S. technology, for which the licenses will not be available." But he said he's "hopeful in the days and weeks ahead" there would be a deal that really works.

Market Morning Briefing: Dollar Yen Has Broken Support

STOCKS

Dow (24831.17, +0.37%) is rising and could test 25000-25200 on the upside in the coming sessions. 25200 could act as an immediate resistance as seen on the daily charts. A break above 25200, if seen could indicate further bullishness for the medium term.

Dax (13001.24, -0.17%) is almost near 10300 as expected and looks bullish for the near term. While the index manages to break above 13300, it could head towards 13600 levels in the medium term.

Upside possibilities for Nikkei (22810.87, +0.23%) could well be 23400 or higher looking at the 3-day charts. The recent break above 22600 indicates strong bullishness for the coming sessions.

Shanghai (3182.88, +0.62%) could test resistance near 3200 and may come off from there. Immediate upside over today and tomorrow could take it to 3200 followed by a sharp fall towards 3150 or lower in the medium term.

Nifty (10806.50, +0.84%) has scope of moving up while support near 10600 holds. Today if the index remains above 10800, it may inch up towards 10850. Near term looks bullish.

COMMODITIES

Brent (76.75) and Nymex WTI (70.47) are taking a pause after the sharp rise seen in the last few sessions. WTI could test support near 69.5-70.0 before again trying to move up while Brent could come off towards 76.0-75.50 levels in the near term. A couple of sessions of consolidation or a dip is likely before the prices again start to move up.

Gold (1320.70) could find some respite this week from the otherwise trap in the 1320-1300 region for the last few sessions. If the price manages to break above 1320, there could be some scope of rising towards 1330 or higher; else a fall towards 1300 and lower towards 1280 looks more likely.

Copper (3.1155, +0.13%) has some room on the upside towards 3.16 from where a dip back towards 3.07-3.05 levels could be possible.

FOREX

Dollar index (92.43) as per expectation, has dipped to test the 13 days moving average line near 92.45, where it could get some support. If it dips below 92.4-92.3, it could test the 21 days moving average near 91.6 and then move up from there. It could resume its broader uptrend towards the medium term target of 94-95 later this week.

Euro (1.1962) as predicted is currently trading in the 1.1960-1.1990 resistance zone (1.1960 is a crucial retracement level of the downmove from 1.24 to 1.182 and 1.199 is seen as the 13 day moving average). Above the 13 days MA, it could even test the 21 days MA near 1.209, after which it could dip to continue its broader downmove.

Dollar Yen (109.33) has broken support on daily candles but is yet to do so on the 3 day candles. While it stays above 109, a rise back towards 110.5-111.0 in this week is still possible. If it breaks below 109.2, it could turn bearish for the medium term.

Euro Yen (130.76) had stayed above support on weekly candles near 129.3-129.2 last week. This week there could be some upmove in Euro Yen towards 132 (seen as resistance on daily candles) as the Euro possibly rises towards 1.200-1.205. However, both Euro and Dollar Yen are expected to turn bearish in the next 1-2 weeks, which should then take Euro Yen below 129.

Pound (1.3567): We had said on Friday that if Pound rises above 1.354 again, it could test levels near 1.36-1.37 in the near term. It is currently trading near 1.3567 and hence could move up this week towards 1.37, after which the broader downmove could resume.

Dollar Rupee (67.33): Support at 67.10 held on Friday. Now we need to see if 67.50 is broken over today-tomorrow or not.

INTEREST RATES

The US CPI data release last week had come out lower than expected. Headline CPI grew 0.2% m-o-m (against expectation of 0.3%), while Core CPI grew 0.1% m-o-m (against expectation of 0.2% growth). This led to the 10 Year yield coming off from the 3% level.

Bond markets are still waiting for an appropriate trigger which could take the 10 Year yield beyond 3% decisively. The 10 year yield has tested 3% twice over the past few weeks but the psychologically important level has continued acting as a resistance.

The medium term targets for US yields in our Apr ’18 US Treasury report (available on demand) are as follows: 3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.75% (2 Year). A breach of the 3% level by the 10 year yield would be vital for these targets to be achieved by June. A rate hike is expected in the June Fed meeting, which might start getting factored later this month and could henceforth lead to a rally in yields towards these medium term targets. We also expect some more yield curve flattening in the next month followed by steepening after that, as yields bounce from long term supports.

US 10 Yr Yield (2.96%), 30 Yr (3.10%), 5 Yr (2.83%), 2 Yr (2.53%):

We had said on Friday that the US 10 Year, 30 Year and 5 Year could all see a dip towards respective supports on short term charts near 2.95%-2.90%, 3.08% and 2.78%. The 30 Year has indeed dipped and we could see the dip play out for the other yields as well over the next couple of sessions.

The German 10 Year – US 10 Year yield spread (-2.4) is near support on medium term chart and could see a rise towards -2.3. This could correspond with German 10 year yield rising from support near 0.5% on short term and medium term charts towards resistance near 0.9%.

0.9% on German 10 year yield and -2.3% on the German-US spread gives a target of 3.2% for the US 10 year which syncs well with our above mentioned medium term targets.

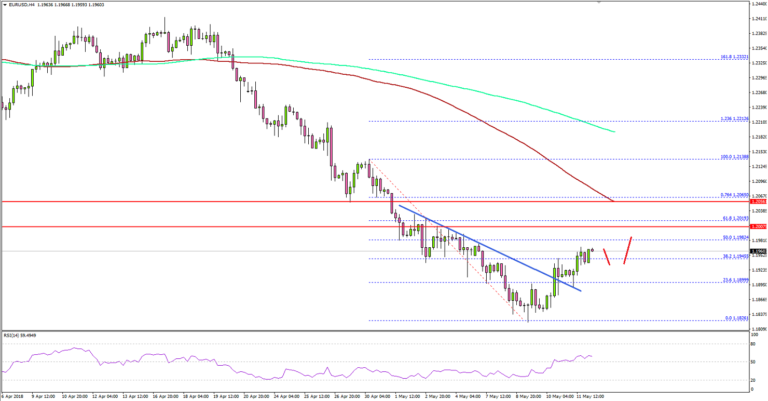

Can EUR/USD Recover Further Above 1.2000?

Key Highlights

- The Euro declined towards 1.1825 against the US Dollar where buyers appeared.

- The EUR/USD pair recovered and moved above a bearish trend line with resistance at 1.1900 on the 4-hour chart.

- The pair correct further if buyers succeed in settling the pair above 1.2000.

- The Michigan Consumer Sentiment Index released recently for May 2018 (Prelim) posted no change from 98.8.

EURUSD Technical Analysis

The Euro declined heavily this past week and traded towards the 1.1800 level against the US Dollar. The EUR/USD pair traded as low as 1.1826 before buyers appeared and protected more losses.

Later, the pair started an upside correction and traded above the 23.6% Fib retracement level of the last decline from the 1.2138 high to 1.1826 low. There was also a break above a bearish trend line with resistance at 1.1900 on the 4-hour chart.

However, there are many barriers on the upside for buyers near the 1.2000 handle. The most important one is near 1.2015 and the 61.8% Fib retracement level of the last decline from the 1.2138 high to 1.1826 low.

A proper daily close above 1.2000 could started a substantial recovery in EUR/USD during the following days. On the other hand, a failure to move above 1.2000 may perhaps call for more losses towards 1.1800.

Overall, the pair is showing signs of a recovery, but a push and close above 1.2000 and 1.2015 won’t be easy in the near term. On the downside, supports are at 1.1850, 1.1825 and 1.1800.

Looking at the USD/JPY pair, there was a downside correction from the 110.00 resistance level. The pair traded lower and tested the 109.20 support zone. There may well be more downsides, but the pair remains supported above 108.20-30.

EM Asia :Let The Chips Fall Where They May

Malaysia

Attention will be focused on the Malaysian onshore markets this morning after PM Mahathir coalition triggered the circuit breakers and imposed a cooling off period for cash markets by declaring the two-day public holiday. Without cash markets and critical Malaysian pension fund support, it’s difficult to take to much away from the post-election USD dominated arbitrage flows on the iShares MSCI Malaysia ETF (EWM). Or for that matter, the hostile moves on the fragmented and thinly supported USDMYR one-month NDF. The reaction on MYR proxy trades, including the USDSGD, were far too splintered and inconsistent exhibiting hallmarks of extremely confused markets.

While conventional logic suggests, there could be equity outflows today, however, the degree to which local Pension Fund buying supplants these moves will be the key. Not to mention the possibility of BNM intervention on the unlikely scenario the market goes completely sideways.

But the tale of the tape will likely focus on PM Mahathir pledge to scrap the GST within 100 days. As well, the market’s reaction to PM Mahathir cabinet with the inclusion of former BNM governor Zeti. But the dramatic drop in the inner cabinet number is what telling from nearly 35 during Najib era to only ten so far. And by all appearance, the new appointments are apparently based on merit, not patronage

USDMYR: Lets the chips fall where they may, and we could see traders on a cash market knee-jerk look to position long term views based on Malaysia’s the solid domestic economic performance, high external factors and of course higher oil prices. The wild card in the deck remains the GST and how the debt agencies react to PM Mahathir pledge to scrap the unpopular tax within 100 days

USDSGD: Of course the market looks to trade the tight correlation with the CNH, but in the meantime, we could see some Proxy interest regarding the MYR elections fall out take place.

China

MSCI is expected to announce the results of its semi-annual index review at 5 am HKT on Tuesday morning. China A-shares will be added to the Emerging Markets index for the first time, and the list of names to be added to the index will be confirmed. Given that most of the likely constituents have underperformed this year, the market reaction to the anticipated announcement will be crucial for short-term sentiment.

USDCNH: Short-term CNH sentiment could take its cue from the key markers retail sales and industrial production data due out later this morning. But the ongoing malaise around trade and tariffs have turned traders jaded which is being exacerbated by PBoc steering the currency ship as steady as can be.

India

Indian markets could be hit again this week as local stock exchanges could feel the repercussions from a potential MSCI de-classification of the Indian equity market from the Emerging Markets index after the Indian Finance Ministry and the Indian Exchanges where previously scolded about pulling licensing deals with foreign bourses.

USDINR: The beleaguered Rupee, hampered mostly by surging oil prices and to a lesser degree the stronger USD, could be on the offs again this week from a potential MSCI de-classification of the Indian equity market from the Emerging Markets index

Indonesia

The Bank of Indonesia on Thursday after the Central Bank Governor hinted yet again that interest rates would be raised to defend the currency and stabilise the market.

USDIDR: With the central bank putting stability ahead of growth, it suggests that any short-term IDR appreciation could be meet with cynical dollar buyers.

Philippines

The USD losses at weeks end were a welcome relief to Asian equity markets, especially twin deficit countries like The Philippines, that has been one of the weakest links in the EM Asia chain.

However, on the currency markets, the midweek reprieve should not be interpreted as a trend reversal but rather a squeeze from overbought USD positioning.

While local PSEi investors welcomed the BSP dovish rate hike, but profoundly pessimistic currency traders quickly re-engaged the long USDPHP trade who are all too knowing that one-off interest rate hike band-aids seldom produce any positive long-term currency effects

USDPHP: Some stops losses were triggered through the 52.25 after currency traders viewed the BSP one and done interest rate hike as distinctly dovish. While sentiment remains weak heading into the pivotal US retail sales print, the PHP should trade with a high level of sensitivity to the USD, but traders could look for dip buying opportunities over the near term given the dovish rate hike.