Sample Category Title

Canadian Dollar At 3-Week High, Employment Numbers Next

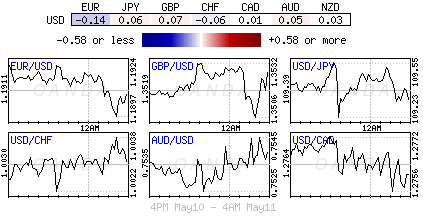

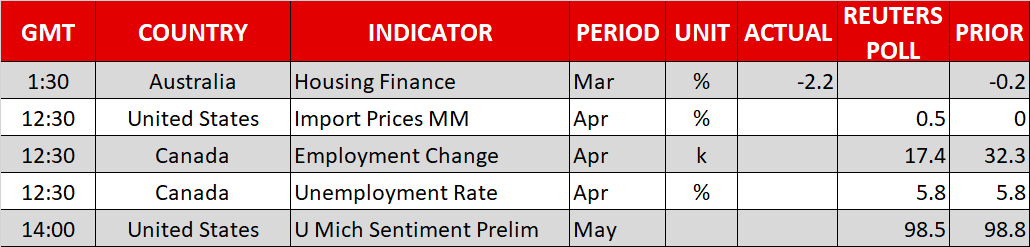

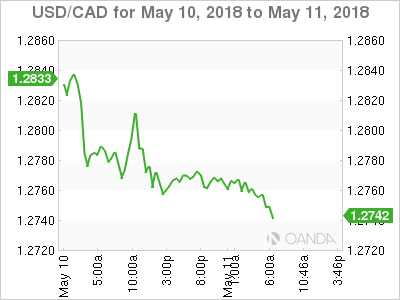

The Canadian dollar has posted slight gains in the Friday session. Currently, USD/CAD is trading at 1.2743, down 0.19% on the day. On the economic front, Canada releases key jobs data. The economy is expected to add 17.8 thousand jobs, compared to 32.3 thousand a month earlier. The unemployment rate is expected to remain steady at 5.8 percent. In the US, the markets are expecting UoM Consumer Sentiment to improve to 98.4 points.

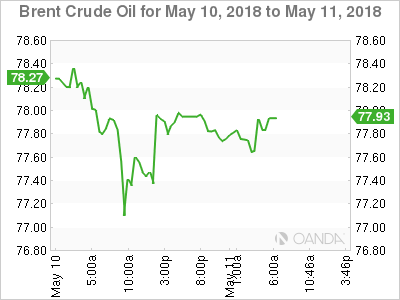

The Canadian dollar continues to make inroads against the greenback and is at its highest level since April 20. The Canadian currency has received a boost from strong oil prices, which are around $77 a barrel, the highest level in 3-1/2 years. President Trump’s bombshell announcement that the US would withdraw from the Iran nuclear deal, as well as Israeli air strikes on Iranian positions in Syria have raised concerns of supply disruptions and significantly pushed up the price of crude.

Key US indicators were mixed on Thursday. Unemployment claims impressed, remaining unchanged at 211 thousand. This easily beat the estimate of 219 thousand. The US labor market is at near or full employment, which has resulted in a slowdown in job growth due to a shortage of skilled labors. Earlier in the week, JOLTS Job Openings climbed to a record 6.6 million. At the same time, inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. According to the CME Group, the odds that the Fed will press the rate trigger at the June meeting stand at 100%.

DAX Retracts After Punching Past 13,000

The DAX index is lower on Friday, erasing the gains which marked the Thursday session. Currently, the DAX is at 12,988 points, down 0.27% on the day. On the release front, ECB President Mario Draghi will speak at an event in Florence.

French and German stock markets remain strong and continue to move upwards. On Thursday, the DAX pushed above the symbolic 13,000 level for the first time since late January. The index is poised to record a seventh straight winning week. The CAC is looking even more impressive, jumping 8.2% since late March.

The ECB continues to send a message of cautious optimism to the markets, and this was underscored by the ECB Economic Bulletin. The report stated that the eurozone economy continues to show “solid and broad-based expansion” but did acknowledge that growth in the first quarter slowed. As for inflation, policymakers remain confident that inflation will continue to move towards the inflation target of 2 percent. However, inflation remains subdued and has not shown signs of an upward trend. The report reaffirmed that the ECB plans to maintain interest rates at current levels for an “extended period of time, and well past the horizon of the net asset purchases.”

In the US, inflation levels remain low as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. According to the CME Group, the odds that the Fed will press the rate trigger at the June meeting stand at 100%.

Dollar Ticks Lower, Canadian Jobs Data In Sight

Here are the latest developments in global markets:

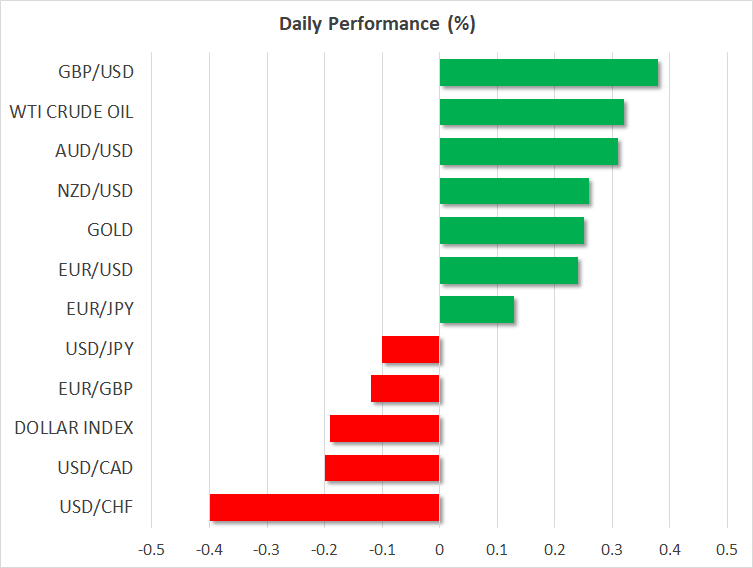

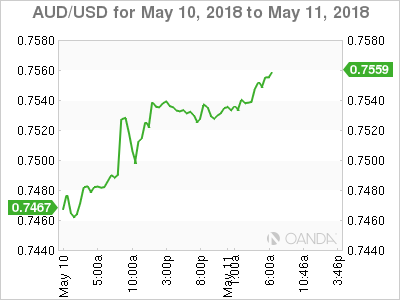

FOREX: The US dollar index edged lower on Friday (-0.17%), extending losses from Thursday on the back of disappointing US inflation data. Dollar/yen was down 0.09%, with little in the way of news or developments to guide price action. Euro/dollar inched up to 1.1943 (+0.24%), while pound/dollar touched 1.3570 (+0.39%), with the latter licking its wounds following a sharp decline on Thursday, after the Bank of England appeared cautious about near-term rate increases. In the antipodean sphere, aussie/dollar reached a one-week high of 0.7556 (+0.33%). Meanwhile, kiwi/dollar ticked up to 0.6978 (+0.26%), recovering nearly all the losses it posted earlier in the week, after the RBNZ poured cold water on expectations for any rate hikes this year. Finally, dollar/loonie fell to 1.2739 (-0.21%), as Canadian traders awaited the release of the nation’s employment data for April at 1230 GMT.

STOCKS: European equities were a sea of red on Friday, with Spain’s blue chip index being the only exception. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.10% and 0.28% respectively, dragged lower mainly by the healthcare and utilities sectors. In Germany, the DAX retreated by 0.34%, while the French CAC 40 fell 0.40%. In Italy, the FTSE MIB 100 was down by 0.05%, as talks between the anti-establishment Five Star Movement and the far-right League on forming a government appeared close to bearing fruit. The British FTSE 100 was practically flat on the day (-0.01%), while the only major index in the green was the Spanish IBEX 35 (+0.11%). Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in positive territory, pointing to a higher open today.

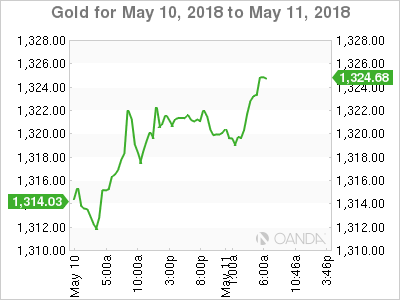

COMMODITIES: Oil prices edged up during the European trading session Friday, paring earlier losses and remaining elevated near the multi-year highs reached earlier in the week. WTI was up by 0.30%, but Brent crude was lagging behind, rising only 0.03%. Market participants were still assessing the potential impact of US sanctions against Iran in the oil market, and whether or not other major producers like Saudi Arabia would raise their production to “fill the gap” left behind by Iranian supply taken off the market. Technically, it will be crucial to see if prices can post a higher high. Looking at WTI, it is currently trading near $71.50, just below the three-and-a-half year high of $71.89 recorded on Wednesday. In precious metals, gold prices were up by 0.26%, trading close to the $1,325 per ounce level. Without any major headlines driving price action, the metal’s gains appear to be owed to the correction lower in the dollar.

Day Ahead: Canadian jobs figures on the agenda; University of Michigan consumer sentiment pending

Friday is a relatively quiet day in terms of data releases, with the US and Canada being the only ones set to submit reports giving clues on economic trends.

Canada will see the release of its own employment data for April at 1230 GMT. The unemployment rate is forecast to have held steady at 5.8%, creating a near-decade low, while the employment change is forecast to have risen by 17.4k versus 32.3k in the prior month. An upward surprise in these data and a potential continuation of the rally in oil prices could drive the loonie even higher.

Shifting to the US, at 1400 GMT, the University of Michigan will deliver preliminary readings on consumer sentiment and inflation expectations for the month of May. Estimates on consumer sentiment are forecasting that the index might inch down to 98.5 compared to 98.8 in the previous month, while the survey related to inflation expectations will attract interest after the US CPI announcement on Thursday. Also, at the same time, US import and export prices for April will be announced.

In energy markets, investors will keep a close eye on the US oil rig count issued by the Baker Hughes company at 1700 GMT. Potential increases in active drilling rigs may trigger some losses in oil prices after they reached a new three-and-a-half year high.

In terms of public appearances, at 1230 GMT, Fed President James Bullard will be giving a presentation on the US economy and monetary policy, while at 1315 GMT, ECB President Mario Draghi will deliver a speech in Italy. Another policymaker delivering remarks today is Bank of Canada Deputy Governor Carolyn Wilkins (1310 GMT).

EURUSD Now Bullish Above 1.1900

The euro currency has started to find short-term buying interest against the US dollar, after the United States economy posted weaker than expected CPI inflation data on Thursday. The EURUSD pair continues to trade above the 1.1900 level, as the greenback comes under selling pressure from overbought levels. Moving into the US trading session, traders will likely look towards the key 1.1900 level for intraday directional guidance.

The EURUSD pair is bullish while trading above the 1.1900 level, key resistance is found at the 1.1925 and 1.1945 levels.

If the EURUSD pair starts to trade below the 1.1900 level, we may see a correction back toward the 1.1874 and 1.1840 support levels.

USDJPY Intraday Bearish Below 109.39 Level

The US dollar remains under selling pressure against the Japanese yen, as the greenback continues to retreat lower after yesterday’s weaker US CPI data. The USDJPY pair currently trades around the 109.30 level, with bearish pressure building while price trades below the key 109.39 level. Moving into the US session, traders look to the release of the Michigan Consumer Sentiment Index for the month of May.

The USDJPY pair is intraday bearish while trading below the key 109.39 level, support is found at the 109.00 and 108.64 levels.

If the USDJPY pair starts to move higher, key resistance is found at the 109.80 and 110.03 levels.

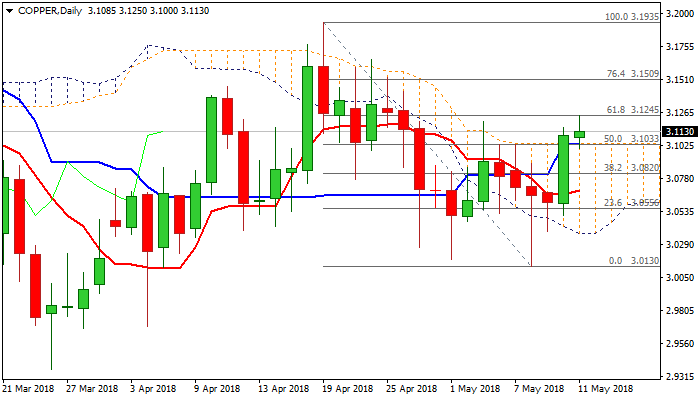

COPPER Rallies Further On Lower Inventories And Signs Of Strong Demand

Copper rallies further on Friday and extends previous day's 1.6% rally which generated strong bullish signal on break and close above daily cloud (cloud top lies at $3.1033, reinforced by daily Kijun-sen).

Today's fresh extension higher cracked pivotal barrier at $3.1245 (Fibo 61.8% of $3.1935/$3.0130 bear-leg), looking for further bullish signal on daily close above.

Daily MA's returned to bullish setup and support further advance, along with north-heading 14-d momentum which broke into positive territory.

Weaker dollar and falling copper inventories, as well as signs of strong demand from metal's top consumer China, are also supportive factors.

Copper is on track for strong bullish weekly close which could further underpin rally.

Lift above $1245 Fibo barrier would open 100SMA ($3.1433) and Fibo 76.4% barrier at $3.1509.

Broken top of thick daily cloud marks solid support which should ideally contain dips.

Res: 3.1250, 3.1433, 3.1509, 3.1660

Sup: 3.1033, 3.0909, 3.0865, 3.0772

US Stocks On Course For Perfect Week

- Oil Rally Aids Rebound in US Indices;

- Dow Faces Test Around 25,000;

- Bitcoin Dip Below $9,000 Worrying.

'General risk appetite has probably improved over the last week in spite of the latest flare up in tensions and potential strains it puts on the US, EU relationship'

It's been a relatively calm start to trading on Friday, bringing an end to what has actually been a similarly quiet week, despite the US' decision to withdraw from the Iran nuclear deal.

From a markets perspective, the reaction to Donald Trump's announcement was primarily felt in oil prices and energy stocks and didn't have a detrimental impact on wider risk appetite, which is not surprising given how indifferent they've been to geopolitical events in recent years. Even oil prices have now stabilised after hitting three and a half year highs in recent days as traders try to determine how significant an impact sanctions will have on oil output.

'If the Dow can find a way above 25,000 in the process, it could signal a shift in sentiment in equity markets'

General risk appetite has probably improved over the last week in spite of the latest flare up in tensions and potential strains it puts on the US, EU relationship. US equity markets are on course for a perfect week – five consecutive daily gains – which when you consider the drop off in sentiment and markets since the end of January is actually quite encouraging.

If the Dow can find a way above 25,000 in the process, it could signal a shift in sentiment in equity markets which have looked extremely vulnerable to another sharp decline. Of course, this may depend on whether the gains have been primarily built on the rally in energy stocks in response to the withdrawal of the US from the Iran nuclear deal, or an actual belief that the market sell-off has run its course. It's interesting though that a very good earnings season has so far no been enough to trigger such a move which makes me question whether the recent move has legs.

There isn't too much for investors to look out for today from an economic data standpoint, with Canadian employment data and US consumer sentiment figures the only notable releases. We will hear from ECB President Mario Draghi who is due to speak at the State of the Union event in Florence and investors will be keen to get his assessment of the economy and potentially any hints about what that means for the bond buying program later this year.

'A significant close below here today could signal another period of downside for bitcoin, which has seen a number of false dawns since the collapse in its price around the turn of the year'

One area where we have seen movement this morning is in cryptocurrencies, with bitcoin having fallen around 4% and broken below $9,000 in the process, a level that had provided strong support over the last couple of weeks. It's worth noting that while this could be a significant breakout to the downside, we have pierced the $9,000 level a few times throughout this time but each time price has rebounded back above.

A significant close below here today could signal another period of downside for bitcoin, which has seen a number of false dawns since the collapse in its price around the turn of the year. To the upside, $10,000 remains a significant barrier for bitcoin, with it having failed to break above here on a few occasions in recent weeks.

Calm Waters In Session

Notes/Observations

- Increasingly likely that Northern League and Five Star will form an anti-euro, anti-austerity full on populist coalition in Italy

Asia:

- RBNZ Gov Orr: Move lower in NZD currency (Kiwi) after Thursday's rate decision 'a good thing'

Europe:

- PM May Cabinet said to be divided into two rival groups to fight out how Britain should manage its EU customs arrangements after Brexit. Brexiteers favor a plan called “max-fac” which relies on tech as part an attempt to minimize border checks. The other camp favor the PM’s option under which the UK would collect tariffs on Brussel’s behalf

- BOE Gov Carney stated that he expected interest rate rise this year if there were not any shocks to the economy

Americas:

- Commerce Secretary Wilbur Ross tells CNBC that he thinks China 'agreed to the concept' of reducing the trade deficit

- US Treasury Official: US/China officials set to meet in Washington on Friday, May 11th to discuss trade disputes (Note: meeting is a follow up to last week’s high-level talks and prepares the way for Vice Prem Liu He’s visit)

Energy:

- Iran Oil Min Zanganeh: prefers $65/bbl crude prices; Iran needs foreign investment but can survive without it

Economic Data:

- (DK) Denmark Apr CPI M/M: 0.5% v 0.3%e; Y/Y: 0.8% v 0.6%e

- (DK) Denmark Apr CPI EU Harmonized M/M: 0.6% v 0.3%e; Y/Y: 0.7% v 0.5%e

- (ES) Spain Apr Final CPI M/M: 0.8% v 0.8%e; Y/Y: 1.1% v 1.1%e

- (ES) Spain Apr Final CPI EU Harmonized M/M: 0.8% v 0.8%e; Y/Y: 1.1% v 1.1%e

- (ES) Spain Apr CPI Core M/M: 0.8% v 0.5% prior; Y/Y: 0.8% v 1.0%e

- (ES) Spain Mar House transactions Y/Y: -3.1% v +16.2% prior

- (HK) Hong Kong Q1 GDP Q/Q: 2.2% v 0.8%e; Y/Y: 4.7% v 3.4%e

- (CN) China Apr Aggregate Financing (CNY): 1.56T v 1.350Te

- (CN) China Apr M2 Money Supply Y/Y: 8.3% v 8.5%e

- (CN) China Apr New Yuan Loans (CNY): 1.18T v 1.100Te

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 -0.3% at 3,557, FTSE flat at 7,700, DAX -0.3% at 12,977, CAC-40 -0.4% at 5,524; IBEX-35 +0.1% at 10,258, FTSE MIB -0.1% at 24,015, SMI -0.2% at 8,970 , S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European markets opened mixed after several were closed for holiday, remaining mixed as the session progressed; commodities kept materials stocks under pressure; healthcare sector outperforming; ZPG to be acquired supporting Rightmove and Autotrader; Denmark closed for holiday; upcoming results expected in the US session include Thomson Reuters among others

Equities

- Healthcare: Cosmo Pharmaceuticals COPN.CH -21% (FDA decision)

- Industrials: OCI OCI.NL +3.0% (results, Ferrovial FER.ES -2.4% (results), Sika SIK.CH +10% (deal with Saint-Gobain)

- Materials: Arcelormittal MT.NL +2.6% (results)

- Technology: ZPG ZPG.UK +29.6% (takeover)

- Telecom: Tiscali TIS.IT +5.5% (results)

Speakers

- BOE's Broadbent: Recent slowdown seen as temporary, Q1 economic weakness was partly due to weather (in-line with recent MPC statement). Right to wait and assess the health of the economy. BOE message was that interest rates will rise gradually

- Czech Central Bank (CNB) May Minutes: Policy makers agreed that economy was facing inflation pressures from positive output growth and tight labor market. Several members argued that an immediate rate hike would not be consistent with current flexible inflation targeting framework. Weaker FX for an extended period would make it possible to tighten monetary condition via interest rates

- Turkey President Chief Adviser Ertem reiterated view that TRY currency (Lira) to stabilize after the June elections

- Philippines Central Bank (BSP) Gov Espenilla: Liquidity tools provided the scope for further reserve rate cuts

- Japan Fin Min Aso reiterated government to work together with BoJ and use all available policy means to achieve strong growth

- BoJ Gov Kuroda stated that Govt had made progress to restore fiscal health; more needed to be done on structural reforms. Reiterated shares a view with govt

- BoJ Assistant Gov Maeda stated that could continue to purchase bonds under the Yield Control scheme (YCC)

Currencies

- FX market experienced a very quiet session on Friday with the major pairs little changed from their opening levels in Asia.

- USD consolidating its recent strength in the after math of a soft CPI reading from Thursday

- EUR/USD steady at 1.1920 area. The Italian political scene to likely see the Northern League and Five Star partie form an anti-euro, anti-austerity coalition in Italy. Markets will be on the lookout if the govt makes good on their populists promises or whether they get watered down by the realities of power. Analysts note that it would be interesting to see how it politicizes the ECB end of QE decision

Fixed Income

- Bund Futures trades at 159.09 up 2 ticks reclaiming the 159 handle in quiet range bound trade with upside momentum above 158.25 targeting 159.42. Support lies at 158.81 then 158.52.

- Gilt futures trade at 122.34 higher by 2 ticks, consolidating above 122 following the BoE rate decision. Continuation above 122.50 targets 122.69, while a move below lows targets 121.82 and 121.67.

- Friday’s liquidity report showed Thursday's excess liquidity stayed steady at €1.901T. Use of the marginal lending facility increased from €170M to €227M.

- Corporate issuance saw $14.2B come to market via 5 issuers as issuance for the week passes $30B.

Looking Ahead

- (IT) Italy Debt Agency (Tesoro) to sell €5.25-6.75B in 2021, 2025 and 2033 BTP Bonds

- 06:00 (PT) Portugal Apr Final CPI M/M: No est v 0.7% prelim; Y/Y: No est v 0.4% prelim

- 06:00 (PT) Portugal Apr Final CPI EU Harmonized M/M: No est v 1.0% prelim; Y/Y: No est v 0.3% prelim

- 06:00 (IE) Ireland Mar Industrial Production M/M: No est v -3.8%% prior; Y/Y: No est v 3.0% prior

- 06:00 (UK) DMO to sell combined £2.5B in 1-month, 6-month and 12-month Bills (£0.5B, £0.5B and £1.5B respectively)

- 06:45 (US) Daily Libor Fixing

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (IN) India Mar Industrial Production Y/Y: 6.1%e v 7.1% prior

- 08:00 (BR) Brazil Mar Retail Sales M/M: +0.2%e v -0.2% prior; Y/Y: 5.5%e v 1.3% prior

- 08:00 (BR) Brazil Mar Broad Retail Sales M/M: +0.7%e v -0.1% prior; Y/Y: 6.7%e v 5.2% prior

- 08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond issuance

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Apr Import Price Index M/M: 0.5%e v 0.0% prior; Y/Y: 3.9%e v 3.6% prior; Import Price Index ex Petroleum M/M: 0.2%e v 0.1% prior

- 08:30 (US) Apr Export Price Index M/M: 0.4%e v 0.3% prior; Y/Y: No est v 3.4% prior

- 08:30 (CA) Canada Apr Net Change in Employment: +20.0Ke v +32.3K prior; Unemployment Rate: 5.8%e v 5.8% prior

- 08:30 (US) Fed’s Bullard (non-voter)

- 09:00 (MX) Mexico Mar Industrial Production M/M: -0.5%e v +0.4% prior; Y/Y: -3.6%e v +0.7% prior; Manufacturing Production Y/Y: -2.6%e v +0.9% prior

- 09:00 (RU) Russia Mar Trade Balance: $12.9Be v $12.2B prior; Exports: $34.7Be v $31.2B prior; Imports: $21.6Be v 19.0B prior

- 09:00 (CA) Bank of Canada (BOC) Wilkins

- 09:15 (EU) ECB chief Draghi in Florence

- 10:00 (US) May Preliminary University of Michigan Confidence: 98.3e v 98.8 prior

- 11:00 (CO) Colombia Mar Industrial Production Y/Y: -2.5%e v +1.5% prior

- 11:00 (CO) Colombia Mar Retail Sales Y/Y: 2.8%e v 5.0% prior

- 11:00 (CO) Colombia Mar Trade Balance: -$0.4Be v -$0.5B prior

- 11:00 (EU) Potential sovereign ratings after European close (Egypt Sovereign Debt to be rated by S&P; Moody’s on Slovenia

- 12:00 (IS) Iceland Apr International Reserves (ISK): No est v 652B prior

- 13:00 (US) Weekly Baker Hughes Rig Count data

USD Stabilises As Market Switches To Risk-On Mode

Risk-on an temporary view

Risk appetite has improved globally as weaker US inflation data (CPI 0.2% vs. 0.3% exp) suggest that worries of a quick Fed-tightening cycle is unfounded. Yesterday read point to a significant slowdown the Fed favorite inflation indicator PCE. US equites rallied with S&P 500 trading above 100dama and demand treasuries sent 10 yr yields below 3%. With the FOMC less than 1-month away front end yields remain supportive help flatten the curves toward historical lows. USD remains supportive against EM but lost ground in the G10. We still see the sources of recent USD correction as unrealistic. Our longer term view is unchanged as markets have yet to reprice US slowing growth and EU positive growth outlook. EM inflation outlook has not changed at close to target indicated that a central banks reaction is no expected (expect from Turkey and Argentina). We remain constructive on NOK and CAD (slightly less on AUD) against USD on the commodity rebound story.

Optimism grew as news flow indicate that President Trump might actually achieve a foreign policy coup by halting North Koreas nuclear program at summit planned to 12th June in Singapore. With liquidly lower due to holidays popular opinion is likely to drive price about deeper analysis. This has pushed to the side for now, middle-east tensions between Iran / Israel and news that anti-establishment and anti-EU 5-Star Movements and the far-right league are close to forming an Italy government. Elsewhere, oil prices fell as drop in Iranian exports could be replaced by Saudi and US supplies. Trader should stay cautions, as markets are fickle searching for the latest driver ahead of fundamentals.

Australia's tax war is on

The Australian dollar was better bid on Friday morning as the USD rally is running out of steam, while the Aussie government unveiled the details of its income tax cut. The Australia dollar had rather a rough first quarter, but it nothing compared to the debasement that took place during the second half of April. Indeed, during that period fell as much as 5.10%, sliding from $0.7813 to $0.7412, amid disappointing economic data that range from stalling inflation pressures to weak retail sales. However, traders were hoping that the much-awaited tax cut promised by the government would brighten the picture in the longer-term.

The government unveiled a tax plan that would mostly benefit the top of the income class, which will do little to effetely boost consumer spending. As expected, it didn't take very long for the opposition leader, Bill Shorten, to start a tax war with the current government, as he promised to redress this inequality. Therefore, there is now the risk that unhappy taxpayers will turn to the opposition at the next Australian election. A bigger, tax relief could only deplete further the budget balance, anything that investors don't like.

USD/CAD – Loonie Looking For Further Gains

Friday May 11: Five things the markets are talking about

Yesterday's U.S inflation data, which came in lower than expected at +0.2% vs. +0.3% m/m, has possibly removed some pressure from the Fed to step up the pace of monetary tightening. In the overnight session, the ‘mighty' dollar has steadied after dropping the most since March on Thursday.

Global stocks have taken comfort in the fact that G7 central banks may not hike as fast as previously feared. Overnight in Europe, equities have erased some of their earlier advance, although regional bourses are heading for they seventh consecutive week of increases.

Elsewhere, U.S 10-year Treasury yields are holding below the psychological + 3% as U.S President Trump's plan to meet North Korea's Kim Jong Un has aided sentiment somewhat.

In commodities, crude oil prices are steady, heading for a second-week of gains after the U.S pulled out of the Iran nuclear deal earlier this week.

On Tap: Canadian employment numbers are due at 08:30 am EDT. Market is anticipating +18k new hire and an unemployment rate to stay steady at +5.8%.

1. Stocks mixed results

In Japan, the Nikkei share average rose to a three-month high overnight, supported by tepid U.S inflation data and easing concerns over the pace of Fed hikes. The Nikkei closed the day up +1.16% and has gained +1.3% this week, while the broader Topix rallied +0.98%.

Down-under, Aussie stocks eased overnight and joined China as the only Asia-Pacific markets that were lower. At -0.04% the S&P/ASX 200 still racked up a sixth-straight weekly gain, the strongest run in two-years at +0.9%. In S. Korea, the Kospi gained +0.55%.

In Hong Kong, stocks rallied overnight after data showed China's industrial demand remains resilient even as trade tensions ratchet up with the U.S. The Hang Seng index rose +0.9%, while the China Enterprises Index gained +0.4%.

In China, stocks fell on Friday, but posted their best weekly performance in almost three-months, as interest towards Chinese blue chips continues to build. The CSI300 index fell -0.5%, while the Shanghai Composite Index lost -0.4%.

In Europe, regional bourses have opened mixed after several were closed for Ascension Day yesterday. Weaker commodity prices are keeping material stocks under pressure, while the healthcare sector is outperforming.

U.S stocks are set to open in the ‘black' (+0.1%).

Indices: Stoxx50 -0.3% at 3,557, FTSE flat at 7,700, DAX -0.3% at 12,977, CAC-40 -0.4% at 5,524; IBEX-35 +0.1% at 10,258, FTSE MIB -0.1% at 24,015, SMI -0.2% at 8,970, S&P 500 Futures +0.1%

2. Oil atop multi-year highs as Iran sanctions tighten supply outlook

Oil prices are trading within striking distance of their four-year highs on Friday as the prospect of new U.S sanctions on Iran tightened the outlook for Middle East supply.

Benchmark Brent crude oil is unchanged at +$77.47 a barrel. Yesterday, Brent hit +$78, its highest since November 2014. U.S light crude is up +10c at +$71.46, having touched a 3-1/2 year high of $71.89 this week.

Currently, the global oil market is considered finely balanced, with top exporter Saudi Arabia and No.1 producer Russia having led efforts to curb oil supply to support global prices.

However, the U.S plans to reintroduce sanctions against Iran, which pumps about +4% of the world's oil, after abandoning a deal reached in late 2015 that limited Tehran's nuclear ambitions.

The market is anticipating that Iranian crude oil exports to start falling in the next few months and is expecting that Brent crude prices to trade atop of the +$80 handle.

Ahead of the U.S open, gold prices have eased a tad in range-bound trading as the dollar firmed slightly, with the market mostly brushing off a potential broadening of conflict in the Middle East. Spot gold is down -0.1% at +$1,319.61 per ounce. The precious metal is still on track to register a first weekly rise in a month. U.S gold futures, for June delivery, are -0.2% lower at +$1,320.20 per ounce.

3. Global sovereign yields slip

Investors are buying Euro bonds ahead of the U.S open, taking advantage of a rise in yields on the back of Italian political concerns, though Italian 10-year yields are still set for their biggest weekly rise in four-months.

Note: Increasingly likely that Northern League and Five Star will form an anti-euro, anti-austerity full on populist coalition in Italy. The League is reported as saying that leaving the E.U/EUR was not one of the priorities and this is giving the market some confidence to buy the dip.

Elsewhere this week, central bankers north and south appear to have become even more cautious as concerns over inflation and international trade cloud the global economic picture. The Bank of England (BoE) yesterday held rates against recent expectations and New Zealand's Reserve Bank of New Zealand (RBNZ) said the official cash rate would remain at +1.75% for the foreseeable future.

The yield on U.S 10-year notes has declined -1 bps to +2.95%, the lowest in more than a week. In Germany, the 10-year Bund yield fell -1 bps to +0.54%, while in the U.K the 10-year Gilt yield fell less than -1 bps to +1.43%.

4. Loonie Looking For Further Gains

It was a quiet FX market overnight, with the U.S dollar consolidating its recent gains just shy of their multi-year highs after yesterday's softer than expected inflation data.

USD/CAD is trading at its Euro session low at C$1.2746 ahead of this morning's Canadian jobs report (+18k expected and an unemployment rate of +5.8%).

Note: Since the beginning of the year, the loonie has lost -1.5% against the U.S dollar and retreated the least against the ‘mighty' buck since mid-April, when the dollar started to rise.

Despite trading briefly atop of its yearly lows this week (C$1.2997), many considered the CAD to still be undervalued compared with the U.S dollar. With oil prices unlikely to retreat rapidly due to tensions heating up in the Middle East and expectations remain that an agreement on a Nafta deal will ultimately be reached is certainly strong support for the CAD in the medium term.

EUR/USD is steady atop of €1.1920, despite the Italian political scene to likely see the Northern League and Five Star party form an anti-euro, anti-austerity coalition in Italy. Will the new Italian government makes good on their populists promises or will the realities of power water them down?

5. Aussie housing-investor credit slumped in March

Data down-under overnight showed that Aussie housing-finance approvals fell -2.2% in March from February, with the value of lending to housing investors down -9%.

Other housing data earlier this month already showed that Australia's housing market is soft with sales at auction falling sharply and prices in retreat in places like Sydney.

Tighter credit standards, and some negative press for banks and their practices are being blamed for the shutting off of the credit taps.