Sample Category Title

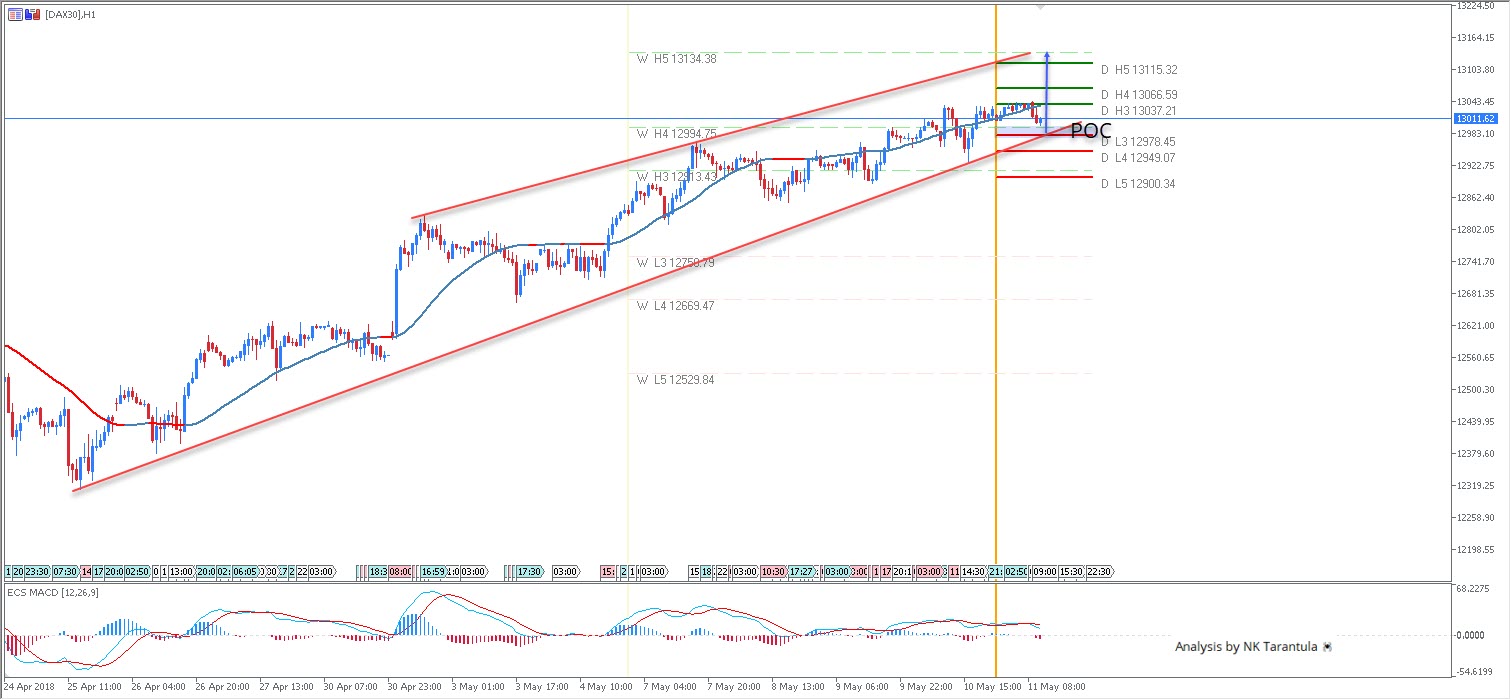

DAX30 Ascending Channel Confirms The Uptrend

This week we saw Trump renege the Iran deal, which saw Oil prices climb, and despite the uncertainty, Equities markets continued to rise. There was talk from Macron that we should look for solutions to continue to trade with Iran. In addition, we saw signs of USD strength during the week, followed by weakness and now we may see more strength again. During USD strength, we see the Dax has the ability to climb higher, especially when during Equities are rising.

The POC zone 12950-80 could reject the price in the case of a retracement. The price is trapped in an ascending channel and we could see 13.030, 13.060 and 13.115. Only below 12900 the DAX will be bearish on intraday time frames.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

EUR/USD Expected To Consolidate

The Euro managed to maintain its upward movement against the US Dollar and consequently breach the 100-hour SMA on Thursday. This appreciation ended near the 1.1940 level, as the rate was unable to surpass its weekly resistance. The 200-hour SMA is likewise located nearby at 1.1943.

The price has been stranded between the aforementioned SMAs for several hours. The current positioning and direction of technical indicators favour more the prevalence of bears in this session. However, the pair does face a strong support cluster formed by the 55– and 100-hour SMAs and the weekly S1 at 1.1880.

These two barriers are likely to bound the rate within the 1.1880/1.1940 range until Monday morning in case the current geopolitical tensions do not weight heavily on the US Dollar.

Pound Calm After Yesterday’s Volatility

GBP/USD's movement was driven by fundamental events on Thursday. The Sterling was trading at its weekly high of 1.36 early in the day with further advance being halted by the weekly PP and 200-hour SMA.

The pair fell aggressively in the wake of the BOE release, as rather disappointing economic data restricted the bank from hiking interest rates. Meanwhile, the pair's subsequent move in the opposite direction was caused by missed US CPI estimates.

By Friday morning, the Sterling had returned to the 55– and 100-hour SMAs at 1.3550. It is likely that this resistance level, likewise reinforced by the nearby-located 200-hour moving average, proves to be an unbreakable barrier today. Thus, a bearish move down to the weekly S1 at 1.3417 is a more probable scenario.

USD/JPY Tangled Between Moving Averages

The weekly R1 at 109.90 proved to be an unbreakable resistance for USD/JPY during the previous session; thus, the pair was pressured down to the bottom boundary of a five-week channel. This fall was limited by the 55-, 100– and 200-hour SMAs which have since restricted solid advances either direction.

By the time of this analysis, the US Dollar had surpass the two longer-term SMAs and was moving towards the 109.70 level. Technical indicators suggest that it could still push higher, thus setting the 61.80% Fibo at 110.20 as today's high.

However, it should still be taken into account that the rate could continue trading in line with the prevailing wedge pattern and therefore fall down to its lower boundary located at 109.00. This bearish scenario should occur if 109.30 is breached.

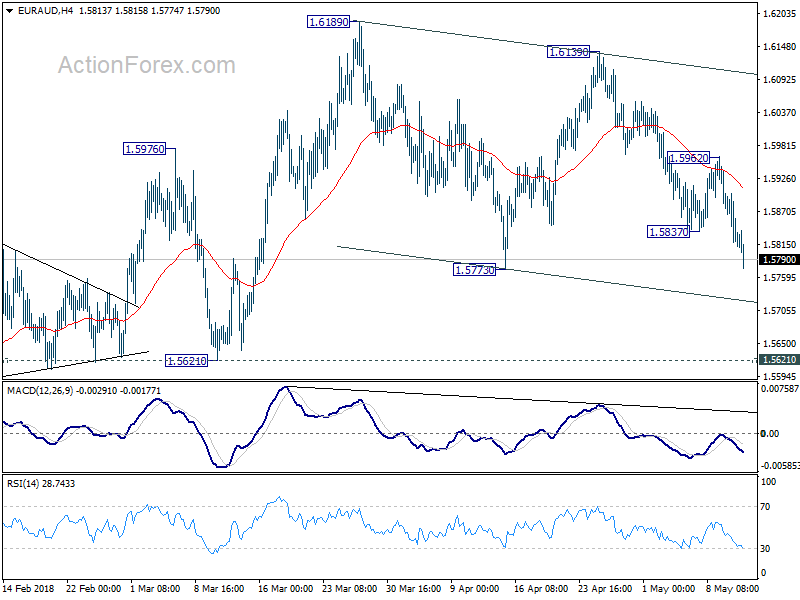

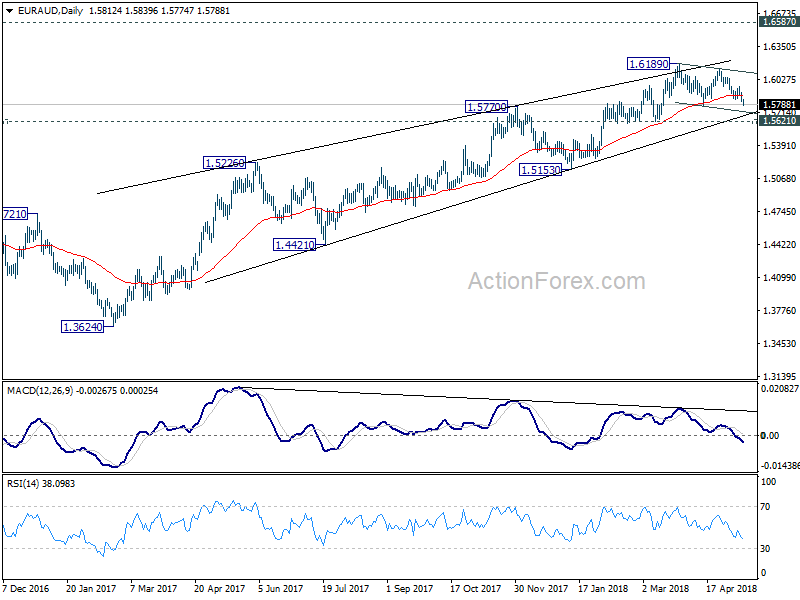

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5785; (P) 1.5843; (R1) 1.5874; More....

EUR/AUD's decline from 1.6139 resumed by taking out 1.5837 and reaches as low as 1.5774 so far. Intraday bias is back on the downside for further fall. But still, as price actions from 1.6189 are viewed as a consolidation pattern, downside should be contained above 1.5621 support to bring rebound. Above 1.5962 will turn bias to the upside for 1.6139 resistance.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. Current rally from 1.3624 could extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal. On the downside, sustained break of 1.5621 support should confirm reversal and turn outlook bearish for 1.5153 support and below.

XAU/USD Likely To Remain Stable

The yellow metal strengthened against the US Dollar for the second consecutive session on Thursday. Additional upside momentum for this appreciation was provided by the strong support cluster set by all three SMAs at 1,313.00.

Gold breached the four-week descending channel and the 38.50% Fibonacci retracement and allayed near 1,322.00. The upper boundary of the two-week channel was altered to the upside in order to include this latest up-move.

The pair's direction during the first part of the day should be southwards until the aforementioned SMAs are reached. Given that no significant US fundamentals are scheduled today, this area could remain intact, thus allowing the rate to resume its movement north until 1,320.00.

In case bulls prevail, gains should be capped at 1,330.00.

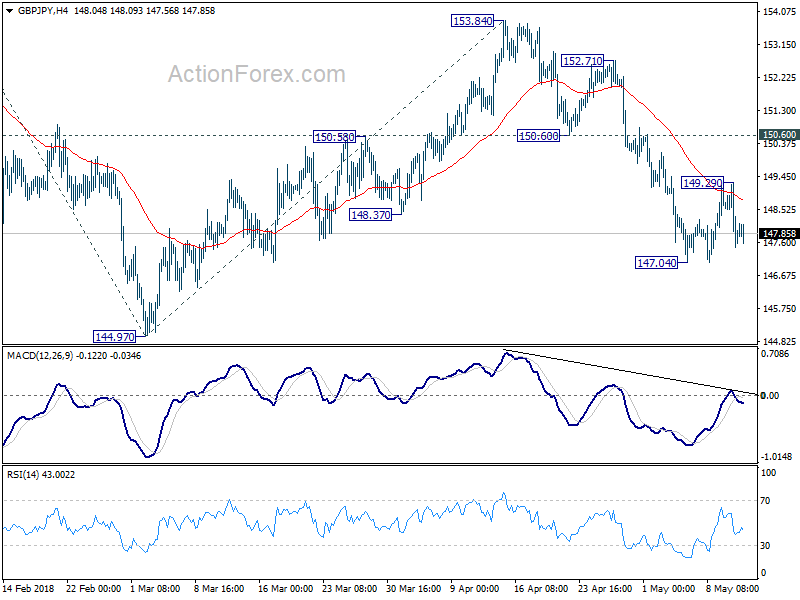

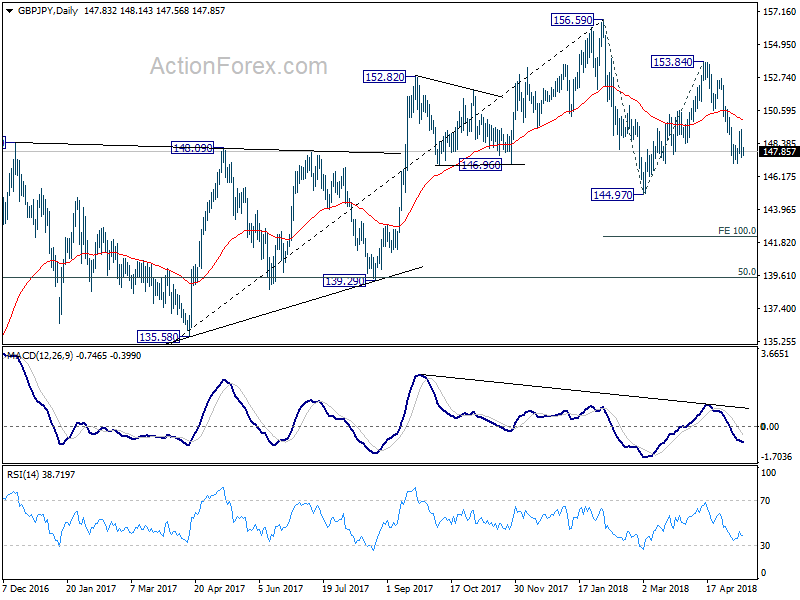

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.11; (P) 148.20; (R1) 148.94; More...

GBP/JPY is staying above 147.04 so far despite the sharp fall from 149.29. Intraday bias remains neutral first. Consolidation from 147.04 could extend further. But in case of another rise, upside should be limited below 150.60 support turned resistance to bring fall resumption. Below 147.04 will target 144.97 first. Break there will resume the fall from 156.59 and target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next.

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

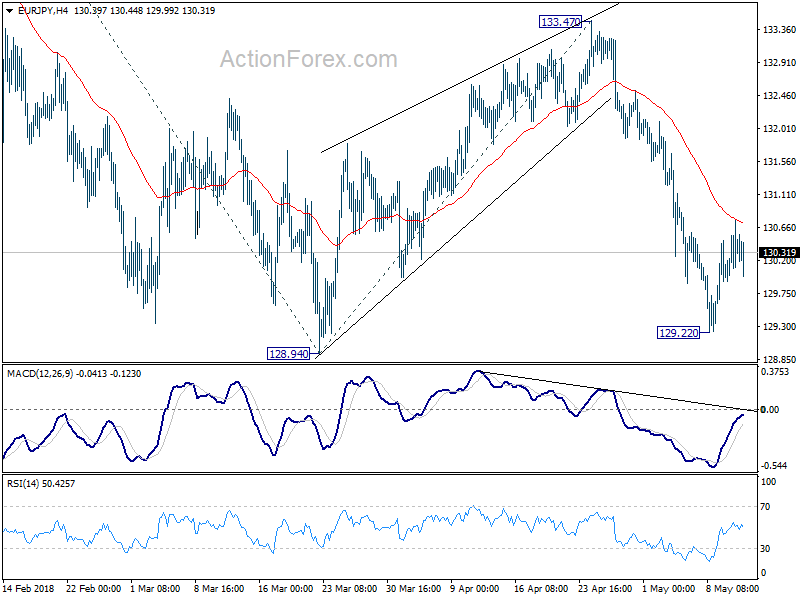

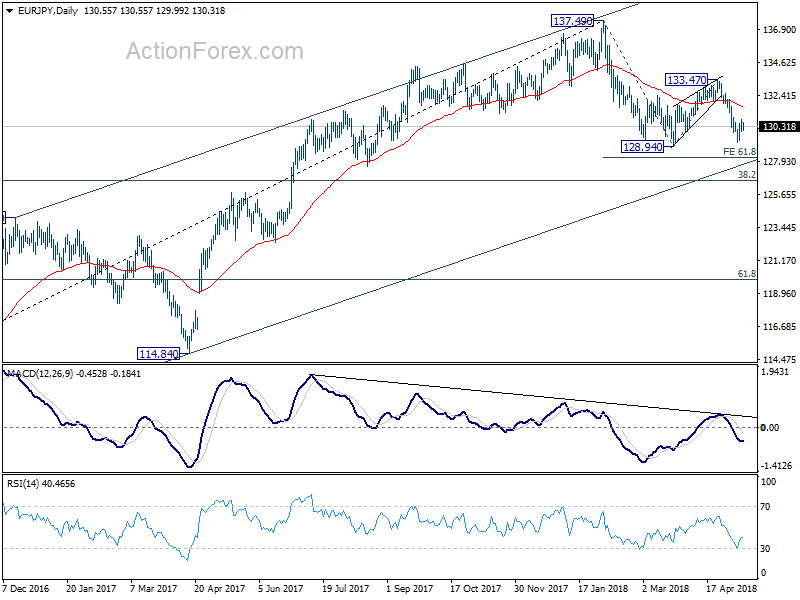

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.93; (P) 130.34; (R1) 130.76; More....

EUR/JPY's consolidation from 129.22 is still in progress and intraday bias remains neutral first. As long as 4 hour 55 EMA holds (now at 130.71), the consolidation should be relatively brief. Below 129.22 will target 128.94 support. Break will resume whole decline from 137.49 and target 61.8% projection of 137.49 to 128.94 from 133.47 at 128.18 next. Overall, near term outlook will stay bearish as long as 133.47 resistance holds and downside breakout is expected eventually.

In the bigger picture, for now, price actions from 137.49 are viewed as a corrective pattern only. Hence, while, deeper decline would be seen, strong support is expected at 38.2% retracement of 109.03 to 137.49 at 126.61 to contain downside and bring rebound. Up trend from 109.03 (2016 low) is expected to resume afterwards. Though, sustained break of 126.61 will be an important sign of trend reversal and will turn focus to 124.08 resistance turned support.

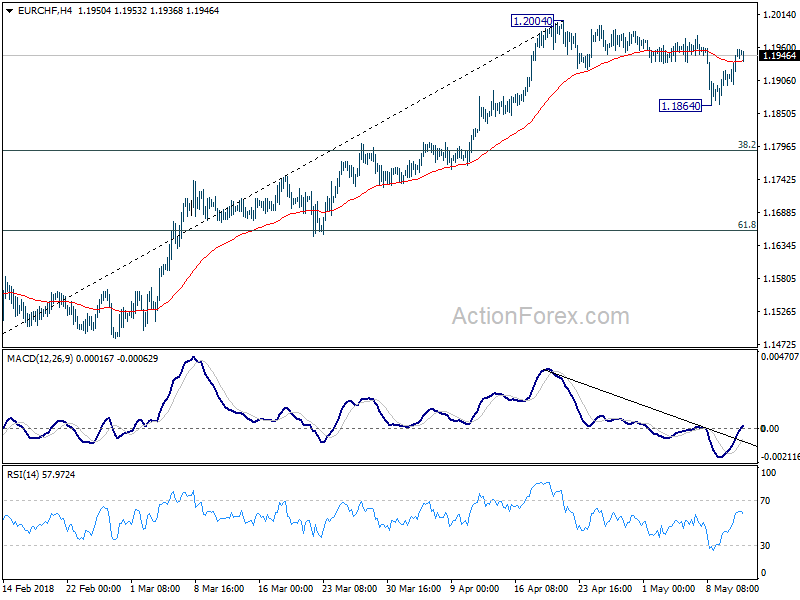

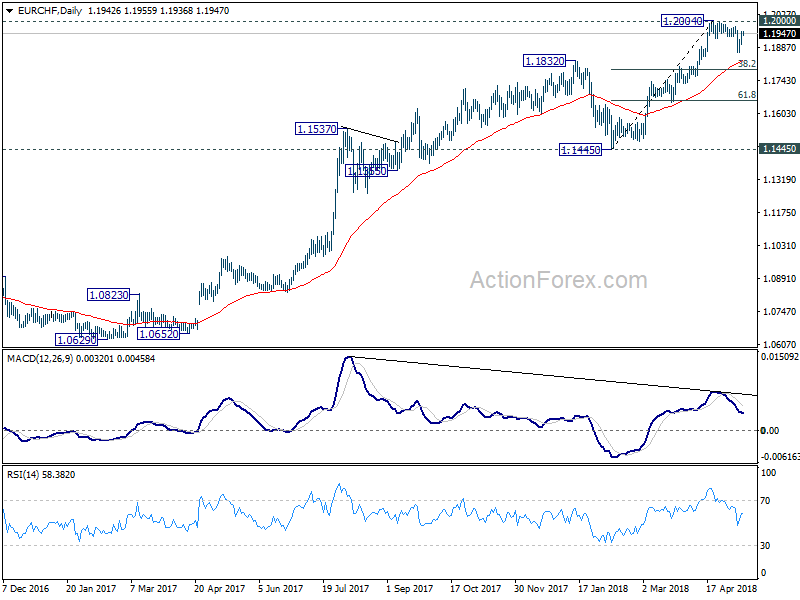

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1914; (P) 1.1935; (R1) 1.1972; More...

Intraday bias in EUR/CHF remains mildly on the upside for further rebound. But break of 1.2004 is needed to confirm up trend resumption. Otherwise, more consolidation would be seen with risk of another decline. In case of deeper pullback, we'd expect strong support from 38.2% retracement of 1.1445 to 1.2004 at 1.1790 to contain downside and bring rebound. Nonetheless, decisive break of 1.2004 will confirm up trend resumption.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2000 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next. However, considering bearish divergence condition in daily MACD. Break of 1.1445 will be an indication of medium term reversal and will turn outlook bearish.

Cautious BoE Sends The Pound Tumbling, Canadian Jobs Data On The Horizon

Here are the latest developments in global markets:

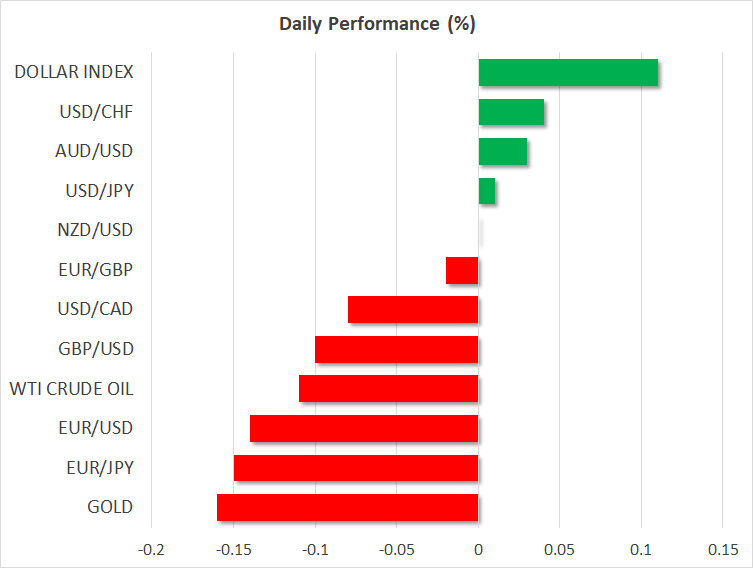

FOREX: The US dollar index, which tracks the greenback’s performance against a basket of six major currencies, traded 0.1% higher on Friday, recouping some of the losses it posted on Thursday following weaker-than-anticipated US inflation data. The British pound recorded hefty losses on Thursday too, after the BoE played down expectations for a near-term rate increase.

STOCKS: Wall Street raced higher yesterday, after disappointing US inflation figures calmed the nerves of investors worried that the Fed may raise interest rates faster this year. The S&P 500 led the charge higher, climbing by 0.94%, while the Nasdaq Composite and the Dow Jones followed in its tracks, gaining 0.89% and 0.80% respectively. As for today, futures tracking the Dow, S&P, and Nasdaq 100 are currently flashing red, pointing to a slightly lower open. In Asia, most major indices took their cue from their US counterparts and surged. Japan’s Nikkei 225 and the Topix rose by 1.16% and 0.98% correspondingly, while in Hong Kong, the Hang Seng soared 1.02%. In Europe, futures following most major benchmarks were in positive territory, albeit marginally so.

COMMODITIES: Oil prices corrected a little lower on Friday, but still remained elevated near the recent multi-year highs. WTI and Brent crude dropped by 0.1% and 0.2% respectively. Following the US decision to impose sanctions on Iran, which would throw a sizeable chunk of supply out of the market, investors appear to be shifting their focus on whether other producers can – and want to – “fill the gap” left by Iran, by raising their own production. Turning to precious metals, gold prices soared more than $10 yesterday, briefly touching the $1,322 level, before pulling back a little to $1,320 today. The gains appear to be owed mostly to the underperformance of the dollar, which sank yesterday following disappointing US inflation data. Since gold is denominated in dollars, a weaker US currency boosts demand for the metal, as it becomes cheaper for investors using foreign currencies to buy it.

Major movers: Pound drops as BoE downplays rate-hike expectations; dollar retreats after CPIs

The British pound came under renewed selling pressure yesterday, following the Bank of England’s (BoE) rate decision. While the Bank kept its policy unchanged via a 7-2 vote as was widely anticipated, it revised down both its GDP growth and its inflation forecasts, sending the message that it is in no hurry to raise rates. Policymakers acknowledged the economy’s recent slowdown, and made it clear they will sit on the sidelines for a while as they monitor whether this softness was temporary, or owed to more persistent factors.

The key takeaway from the BoE was that the hiking cycle has been delayed for now, but not derailed. The timing of the next rate increase will depend on whether economic data begin to show signs of life again in the coming months. The implied probability for a rate hike at the August meeting dropped markedly in the aftermath, and currently rests at 42% according to the UK overnight index swaps. That probability is likely to rise or fall according to the quality of incoming UK data over the next weeks, and the pound will probably move alongside it.

Over in the US, the dollar index tumbled notably, falling back below the 93.00 handle, after the CPI data for April disappointed. While the headline CPI rate ticked up to 2.5% in yearly terms as was expected, the core rate missed its forecast for inching up, and instead held steady at 2.1%. This may have led investors to scale back positions betting that inflation will accelerate further, which could push the Fed to raise rates at a more aggressive pace.

In geopolitics, US President Trump announced yesterday that he will meet North Korean leader Kim Jong Un in Singapore, on June 12.

Day ahead: Canadian jobs data and University of Michigan consumer sentiment survey on the horizon; Italian politics eyed

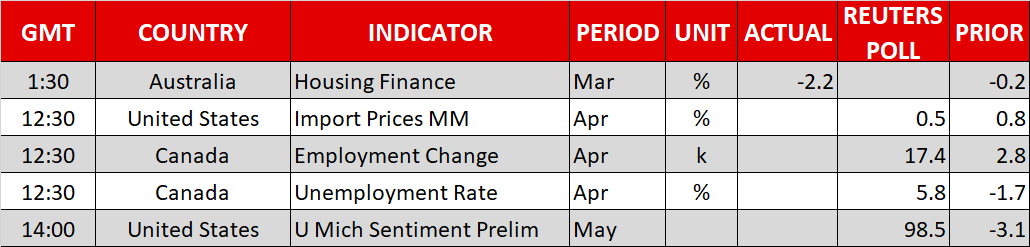

Friday’s calendar is a relatively light one, with Canada’s employment report and the University of Michigan’s gauge of consumer sentiment being among the highlights. Meanwhile, political developments in Italy will also be monitored by market participants.

Canadian jobs data for the month of April are due at 1230 GMT. The economy is anticipated to have added 17.4k positions during the month, below March’s 32.3k but still reflecting a healthy figure should expectations materialize. The unemployment rate is projected to remain at 5.8%, matching a near decade low. A data beat is likely to increase market expectations for a faster tightening cycle by the Bank of Canada, consequently boosting the loonie. Elevated oil prices are also seen as supporting the currency; Canada is a major oil exporter.

The US will see the release of the University of Michigan’s preliminary survey on consumer sentiment for the month of May at 1400 GMT. Consumer morale is forecast to edge slightly lower, with the relevant index standing at 98.5 from April’s 98.8. The surveys pertaining to inflation expectations have gathered interest in the past and will also be watched, especially in the aftermath of yesterday’s CPI figures which were weaker than forecasted and led the greenback to record some losses relative to other currencies. Earlier in the day (1230 GMT), US import and export prices for April will also be made public.

In Italy, it seems that the two anti-establishment parties, 5-Star Movement and Northern League, are getting closer to forming a government; euro pairs will be eyed in the event of any updates on this front.

With oil prices around their highest since late 2014, the US Baker Hughes oil rig count due at 1700 GMT might be attracting additional interest.

ECB chief Mario Draghi will be giving a speech at 1315 GMT, while earlier (1230 GMT), St. Louis Fed President James Bullard (non-voting FOMC member in 2018) will be giving a presentation on the US economy and monetary policy. Another policymaker delivering remarks today is Bank of Canada Deputy Governor Carolyn Wilkins (1310 GMT).

Also of interest will be a speech by President Trump on his administration’s plans to combat drug pricing. In this respect, stocks of pharmaceutical companies will be in focus.

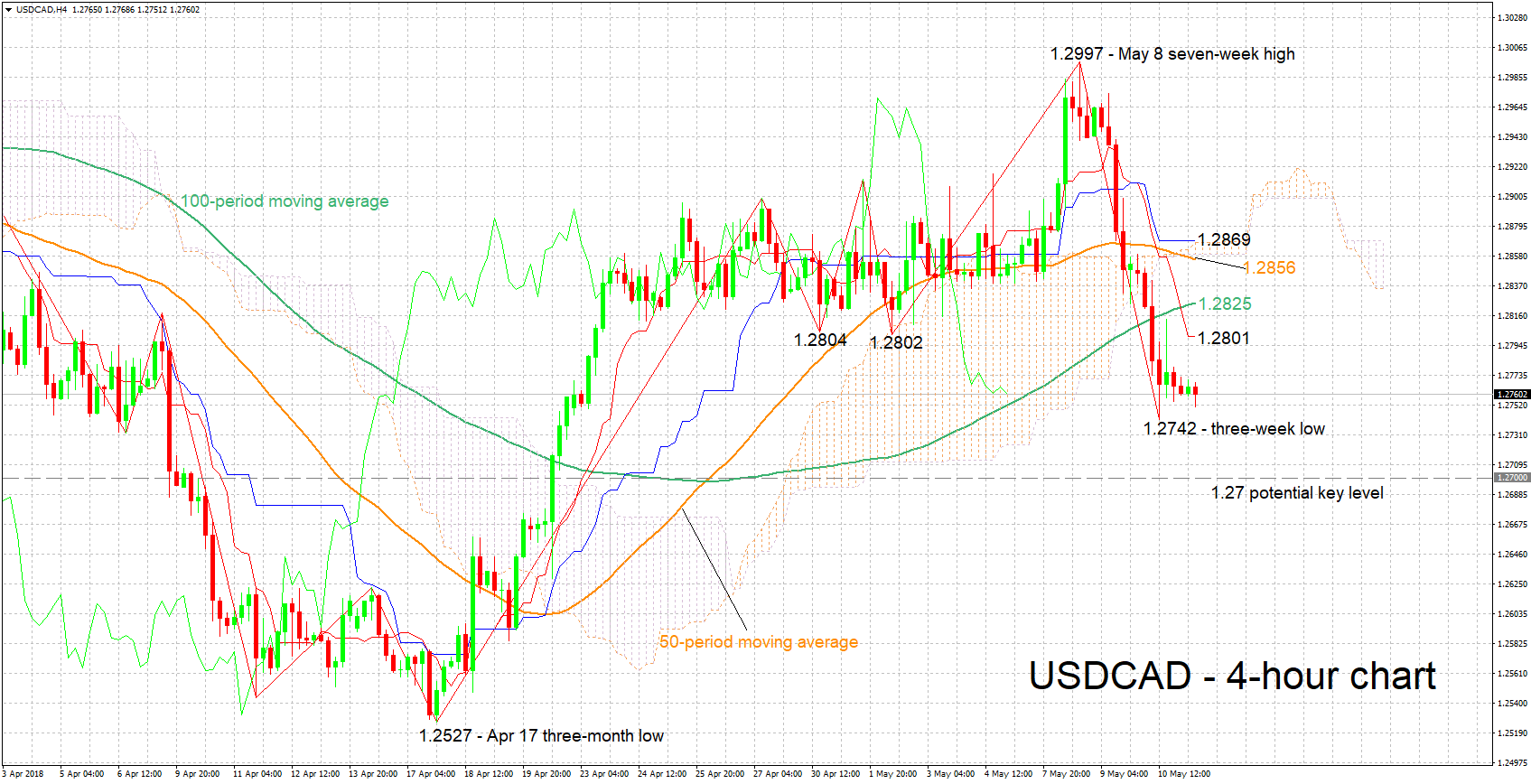

Technical Analysis: USDCAD negative momentum eases a bit

USDCAD has declined considerably after touching a seven-week high of 1.2997 on Tuesday. Yesterday, the pair posted a three-week low of 1.2742. The Tenkan-sen line is below the Kijun-sen one, pointing to a bearish short-term picture. However, negative momentum seems to have eased a bit – this is supported by the flat Kijun-sen line. Notice also that the Chikou Span may be pointing to an oversold market.

A strong Canadian employment report is expected to boost the loonie, pushing USDCAD lower. Support to declines could come around yesterday’s low of 1.2742 and the 1.27 round figure in case of steeper declines.

Conversely, weak figures out of Canada are likely to push the pair higher. Resistance to advances might come around the 1.28 handle, with the region around it encapsulating the current levels of the Tenkan-sen (1.2801) and the 100-period moving average (1.2825), as well as a few bottoms from the recent past.

The direction of oil prices can also affect the pair, with higher prices seen as benefitting the loonie and vice versa.