Sample Category Title

Dollar Stabilized from Post CPI Selloff, Sterling also Found Footing

The post CPI selloff in Dollar was relatively shallow and the greenback is regaining some footing today. Similar Sterling stays week after post BoE selling, but loss is so far limited. On the other hand, Canadian Dollar remains the strongest one for the week and stays firm ahead of today's employment data release. In other markets, WTI crude oil reached as high as 71.89 overnight and stays firm at around 71.25 at the time of writing. US equity indices ended broadly higher with DOW 8- 0.8% to 24739.53. Nikkei followed and rose 1.16% to 22758.48. Gold edged higher yesterday but struggled to stay above 1320.

US House Speaker Ryan urged NAFTA agreement notification by May 17

US House Speaker Paul Ryan told the NAFTA negotiation parties that May 17 is the deadline for the new NAFTA deal for eventual passage for the current Congress to vote on within this year. Ryan said "We have to have the paper – not just an agreement, we have to have the paper – from USTR by May 17 for us to vote on it this year, in December, in the lame duck". But later, his spokesman said he referred to a notification of intent to sign the NAFTA agreement, not the full text. The new elected Congress will take office in January.

Canadian Foreign Minister Chrystia Freeland said after meeting with US legislators that "we are definitely getting closer to the final objective." Mexico's Economy Minister Ildefonso Guajardo said he'll know by the end of Friday " if we really have what it takes to be able to land these things in the short run."

BoJ Kuroda: Some steps remaining for government on fiscal reforms

BoJ Governor Haruhiko Kuroda spoke to the parliament today and hailed that the government has made significant progress on fiscal reforms. And, there is "some lag before the steps already taken begin to affect the economy". But he also emphasized that there are "still some steps remaining that the government needs to take on structural reform and growth strategy."

New Zealand BusinessNZ PMI rose to 58.9, highest since Jan 2016

New Zealand BusinessNZ Performance of Manufacturing Index rose to 58.9 in April, up from 53.1. That's also the highest level since January 2016. BusinessNZ's executive director for manufacturing Catherine Beard noted that "although April represents a good result for the sector, the key will be to continue the expansion momentum over the coming months."

Also release in Asian session, Australia home loans dropped -2.2% mom in March, Japan M2 rose 3.3% yoy in April.

Looking ahead

Canadian job data will be the main focus for today. US will release import price index and U of Michigan consumer sentiment.

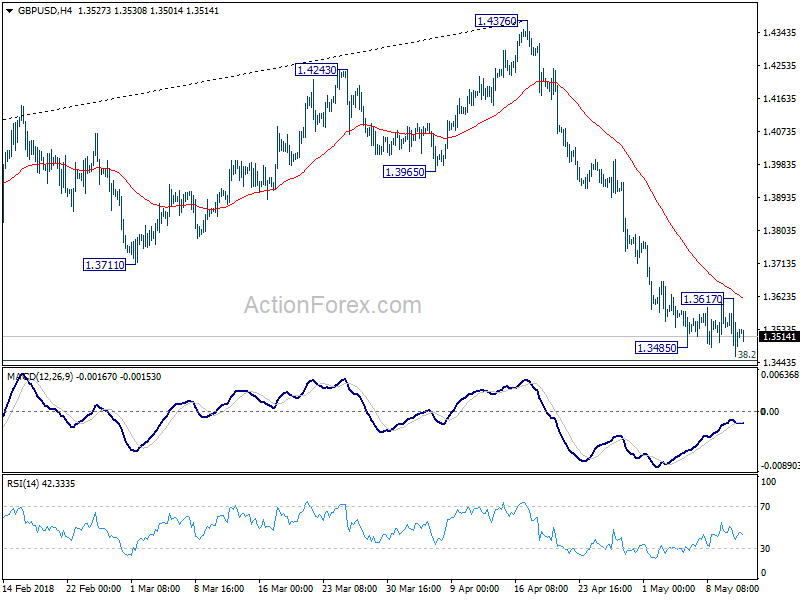

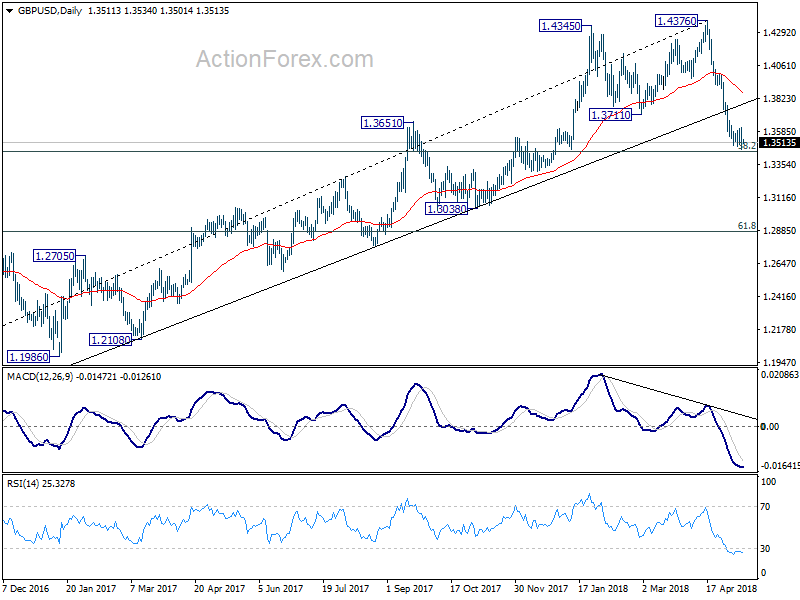

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3444; (P) 1.3530; (R1) 1.3602; More...

GBP/USD dipped to 1.3459 as recent decline resumed. But downside momentum is a bit week. Nonetheless, intraday bias is back on the downside. Firm break of 1.3448 fibonacci level will pave the way to next fibonacci level at 1.2874. On the upside, break of 1.3617 will indicate short term bottoming. In that case, bias will be turned to the upside for stronger rebound, possibly back to 55 day EMA (now at 1.3869).

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). Deeper decline should be seen to 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3925) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing PMI Apr | 58.9 | 52.2 | 53.1 | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Apr | 3.30% | 3.20% | 3.20% | 3.10% |

| 1:30 | AUD | Home Loans M/M Mar | -2.20% | -2.00% | -0.20% | |

| 12:30 | CAD | Net Change in Employment Apr | 20.5k | 32.3k | ||

| 12:30 | CAD | Unemployment Rate Apr | 5.80% | 5.80% | ||

| 12:30 | USD | Import Price Index M/M Apr | 0.50% | 0.00% | ||

| 14:00 | USD | U. of Mich. Sentiment May P | 98.4 | 98.8 |

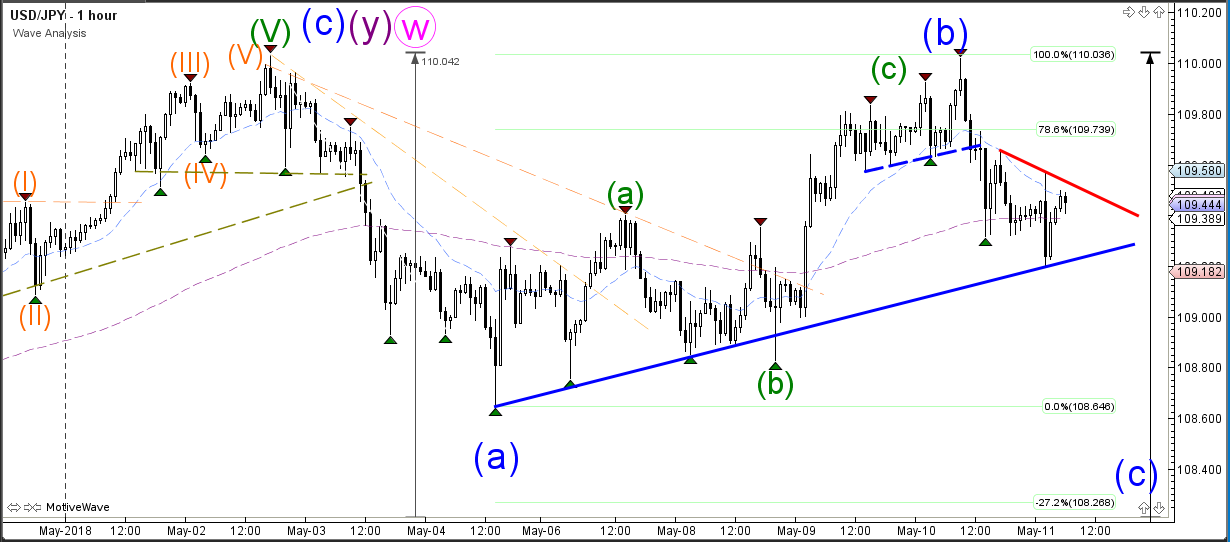

USD/JPY Bounces At 110 Resistance For Double Top Reversal Pattern

The USD/JPY uptrend failed to break above the resistance and previous top at 110, which could indicate a potential double bottom reversal chart pattern. The bearish bounce could confirm a larger ABC (blue) correction if price manages to break below the support trend line (blue). In that case price could move towards that Fib targets of wave X (pink). A bullish break however above the previous high could still indicate a continuation of the uptrend.

The USD/JPY chart looks corrective and choppy. A breakout below the resistance (red) or support (blue) trend line is needed before a larger impulsive price action can start.

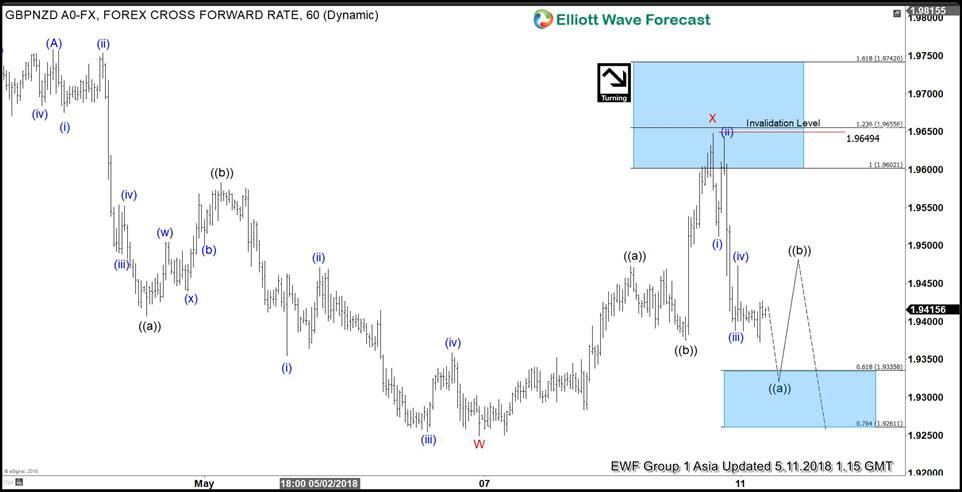

Elliott Wave View: GBPNZD Ending An Impulse Move

GBPNZD short-term Elliott wave view suggests that the rally to 1.9758 on 4/26 high ended Intermediate wave (A). Down from there, Intermediate wave (B) remains in progress as a double three Elliott Wave structure. The internals of each leg in double three (WXY) sub-divides into 3 waves corrective sequence and usually is the combination of two corrective patterns i.e Flat, Zigzag, triangle etc.

Down from 1.9758 high, Minor wave W ended as a zigzag Elliott Wave structure (5-3-5) where Minute wave ((a)) ended at 1.9407, Minute wave ((b)) ended at 1.9582, and Minute wave ((c)) of W ended at 1.925. Above from there, the pair bounced higher in Minor wave X with internals also unfolded as a zigzag Elliott Wave structure. Minute wave ((a)) of X ended at 1.9472, Minute wave ((b)) of X ended at 1.9376 and Minute wave ((c)) of X ended at 1.9648 high.

Below from there, the pair is expected to resume lower in Minor wave Y of (B) as a zigzag structure. Minute wave ((a)) of Y is in progress looking for another extension lower towards 1.9261 – 1.9335, which is 0.618%-0.764% Fibonacci extension area of Minor wave W-X from Intermediate wave (A). Afterwards, the pair should bounce in 3, 7 or 11 swings in Minute wave ((b)) to correct cycle from 5/10 high before pair resumes lower again.

GBPNZD 1 Hour Elliott Wave Chart

GBP/USD Downtrend Continues After Failing To Break 1.36 Resistance

The GBP/USD news events on Thursday had a minor impact on the price action of the 4 hour chart. Eventually price bounced at the resistance trend line (red) and tried to break below the support trend line (green) but failed. The downtrend is still intact and a 2nd break below support could see price fall towards the Fibonacci targets of wave 5 (purple). A bullish reversal would only become more likely if price is able to break above the previous tops which could indicate the completion of the wave 1 (pink) and the start of the wave 2 (pink).

The GBP/USD still respected the Fibonacci levels of wave 4 (green) despite the volatile news events on the GBP. Price made a first attempt to break support but failed to close strongly below 1.35. Price will need to break above the resistance (red) or below the support (green) trend lines before a next impulsive price action can be expected.

Equity Markets Trade Generally Higher Amid Dearth Of Economic Data

General Trend:

- Hang Seng outperforms on gains in the Info Tech, Financials and Services sectors

- Australia’s Graincorp H1 results hurt by dry weather conditions

- Rusal reports rise in Q1 results, notes sanctions limit ability to forecast

- Oil prices see little volatility during Asia

- Generally quiet session for Asian bonds

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.2%; closed flat

- ASX 200 Consumer Discretionary Index +1%, Telecom +1%, Resources +0.7%; Financials -0.4%, Utilities -0.4%, Energy -0.2%

- (AU) Australia March Home Loans M/M: -2.2% v -1.8%e; Investment Lending: -9.0% v 0.5% prior

- (AU) Australia sells A$1.0B v A$1.0B indicated in 3.25% April 2029 bonds, avg yield 2.7842%, bid to cover 3.91x

- (NZ) RBNZ Gov Orr: Move lower in Kiwi (NZD) after Thursday's rate decision 'a good thing'

- (NZ) New Zealand April Business NZ Manufacturing PMI 58.9 v 52.2 prior

China/Hong Kong

- Shanghai Composite opened +0.2%, Hang Seng +1.1%

- Hang Seng Information Technology Index +1.5%

- (CN) China PBoC sets yuan reference rate 6.3524 v 6.3768 prior

- (CN) China PBoC Open Market Operation (OMO): Skips OMO v CNY30B injected in 7-day and 14-day reverse repos prior; Net drain: CNY20B

- For the week, PBoC drained a net of CNY140B through OMOs v CNY110B drain w/w

- (CN) PBoC said to plan full custody of payment companies' reserves - China Securities Times

- (CN) Credit risks in China are controllable despite defaults - China Securities Journal

Japan

- Nikkei 225 opened +0.3%; closed +1.2%

- TOPIX Electric Appliances Index +1.8%, Marine Transportation +1.1%, Retail +0.9%

- (JP) Nikkei 225 May options said to settle at ~22,621

- (JP) Japan April Money Stock M2: 3.3% v 3.2%e; M3 2.8% v 2.8%e

Korea

- Kospi opened +0.2%

Other

- (ID) Indonesia Central Bank Gov Martowardojo: Has ample room to adjust rates; reiterates Rupiah currency (IDR) depreciation not in line with fundamentals

North America

- US equity markets ended higher: Dow +0.8%, S&P500 +0.9%, Nasdaq +0.9%, Russell 2000 +0.5%

- S&P500 Utilities +1.4%, Tech +1.3%

- (US) TREASURY'S $16B 30-YEAR BOND AUCTION DRAWS 3.130%; BID-TO-COVER RATIO: 2.38 V 2.26 PRIOR AND 2.25 AVG OVER THE LAST 4 AUCTIONS (highest yield since March 2017)

- (US) US President Trump: Hope to make better deal with Iran

Europe

- (IE) Ireland April Consumer Confidence: 104.0 v 108.1 prior

Levels as of 02:00ET

- Hang Seng +1.3%; Shanghai Composite -0.1%; Kospi +0.6%

- Equity Futures: S&P500 +0.1%; Nasdaq100 flat, Dax +0.2%; FTSE100 +0.2%

- EUR 1.1909-1.1926 ; JPY 109.19-109.58 ; AUD 0.7522-0.7544 ;NZD 0.6954-0.6978

- Jun Gold -0.2% at $1,320/oz; May Crude Oil flat at $71.36/brl; May Copper flat at $3.110/lb

BoJ Kuroda: Some steps remaining for government on fiscal reforms

BoJ Governor Haruhiko Kuroda spoke to the parliament today and hailed that the government has made significant progress on fiscal reforms. And, there is "some lagbefore the steps already taken begin to affect the economy".

But he also emphasized that there are "still some steps remaining that the government needs to take on structural reform and growth strategy."

Donald Trump Continues To Mould The International Nuclear Scene

Market movers today

A quiet day on the data front. Preliminary US Michigan consumer confidence for April is the most interesting item.

ECB President Mario Draghi is speaking in Florence today at 15:15 CEST. We expect the speech to have little market impact.

The Danish market is closed today due to the bank holiday but Danish CPI inflation data for April is still due out today.

Selected market news

US President Donald Trump continues to mould the international nuclear scene. He announced that a summit will be held on 12 June in Singapore. He will discuss North Korean denuclearisation with the country's premier Kim Jong-un.

A populist government in Italy is increasingly likely as the Five Star Movement and League parties move closer to forming a coalition government, as talks are said to have made significant strides. Peripheral spreads widened, but not dramatically.

US inflation came in below expectations yesterday. CPI core grew by just 0.1% m/m in April against expectations of 0.2%, implying an unchanged core inflation rate of 2.1% y/y. This supports our view that the Fed is not about to accelerate its hiking cycle but will stick to twothree more hikes this year depending on data, in line with the latest ‘dots' and market pricing.

In the UK, the Bank of England stayed on hold (vote count 7-2) as expected, but signalled that the hiking cycle has not been cancelled but postponed. We stick to our call that the BoE is going to hike once in the second half of 2018 and once more in 2019. See Bank of England review: Keeping the hiking cycle alive but timing is data dependent, 10 May.

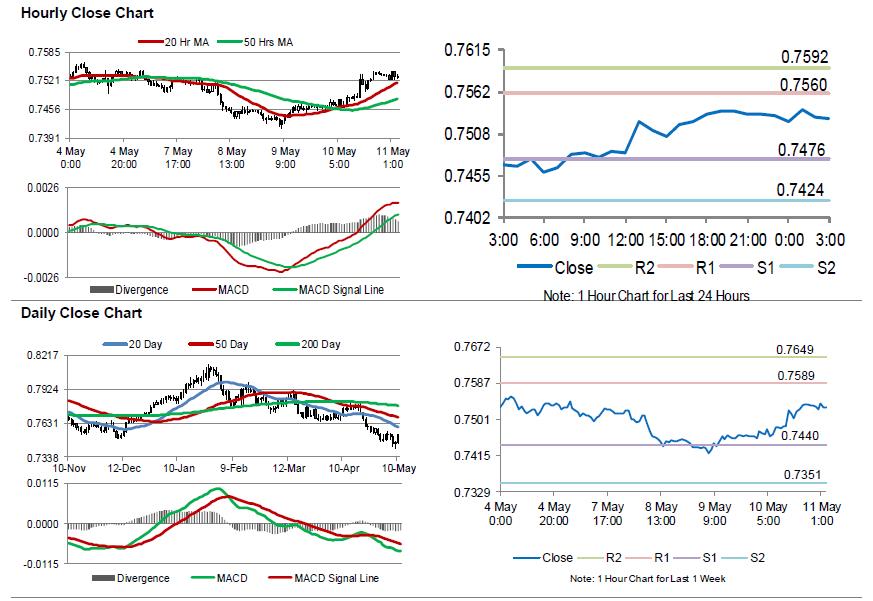

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.95% against the USD and closed at 0.7532.

LME Copper prices rose 1.12% or $76.0/MT to $6862.0/MT. Aluminium prices rose 1.39% or $32.0/MT to $2327.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7528, with the AUD trading 0.05% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7476, and a fall through could take it to the next support level of 0.7424. The pair is expected to find its first resistance at 0.7560, and a rise through could take it to the next resistance level of 0.7592.

Next week, traders would closely monitor the Reserve Bank of Australia’s May meeting minutes as well as Australia’s unemployment rate data.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

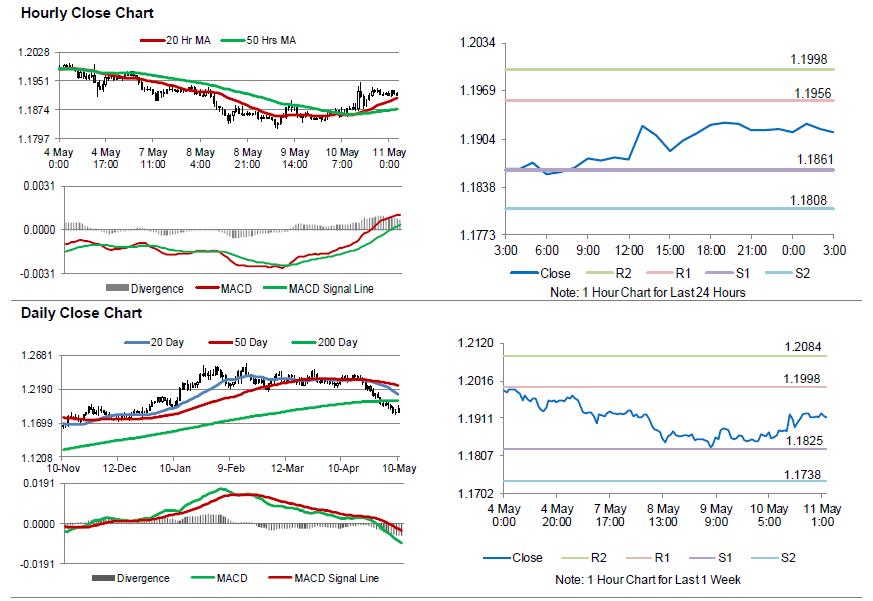

Euro-Bloc’s Economy On A Steady Growth Track: ECB Bulletin

For the 24 hours to 23:00 GMT, the EUR rose 0.55% against the USD and closed at 1.1917.

Yesterday, the European Central Bank (ECB), in its latest economic bulletin report, stated that Euro-zone's economic growth continues to show “solid and broad-based expansion” and expressed confidence that inflation will converge towards its target over the medium term. However, the central bank acknowledged a moderation in economic growth in the first quarter of this year.

The US Dollar declined against a basket of major currencies, after the US consumer price index (CPI) rose less-than-anticipated by 0.2% on a monthly basis in April, compared to market expectations for a rise of 0.3%, thus highlighting a steady build-up in inflationary pressures that will likely keep the Federal Reserve on track to raise interest rates gradually this year. The CPI had registered a drop of 0.1% in the previous month. Meanwhile, the nation's initial jobless claims remained unchanged at a level of 211.0K in the week ended 05 May, whereas investors had envisaged for a rise to a level of 219.0K.

In other economic news, budget surplus in the US recorded a reading of $214.3 billion in April, undershooting market consensus for a surplus of $215.0billion. The US had registered a budget deficit of $208.7 billion in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1913, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.1861, and a fall through could take it to the next support level of 1.1808. The pair is expected to find its first resistance at 1.1956, and a rise through could take it to the next resistance level of 1.1998.

With no key macroeconomic releases in the Euro-zone today, investors would focus on the US flash Michigan consumer sentiment index for May, slated to release later in the day.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

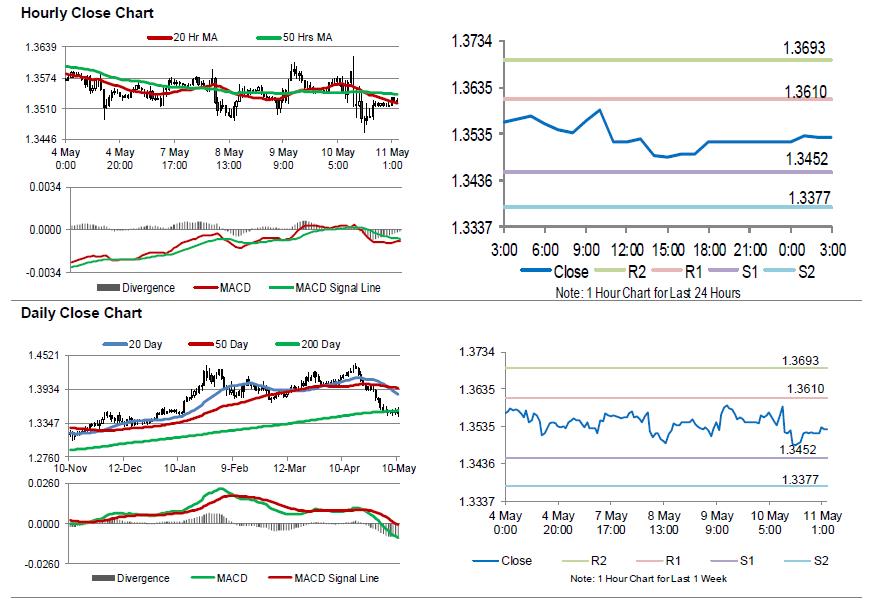

BoE Left Key Interest Rate On Hold, Slashes Its Outlook On Inflation And Growth

For the 24 hours to 23:00 GMT, the GBP declined 0.22% against the USD and closed at 1.3518, after the Bank of England (BoE) lowered Britain's growth and inflation forecast at its May monetary policy meeting.

The BoE's Monetary Policy Committee voted 7-2 to keep the benchmark interest rate on hold at 0.50%, amid a slump in the first-quarter economic growth. According to minutes of the meeting, officials believed that the recent slowdown in economic activity will prove temporary but cautioned that Britain's economy is still clouded by Brexit uncertainties. Further, the central bank trimmed its 2018 growth forecast from a moderate 1.8% to a modest 1.4%, entirely due to weak first-quarter growth and added that inflation will slow faster than previously estimated.

In economic news, Britain industrial production grew 0.1% on a monthly basis in March, compared to a similar rise in the prior month, while investors had anticipated for an advance of 0.2%. On the other hand, the nation's manufacturing production fell 0.1% on a monthly basis in March, compared to market consensus for a drop of 0.2%. In the prior month, manufacturing production had eased 0.2%. Furthermore, the nation's construction output plunged 2.3% MoM in March, meeting market expectations and posting its biggest decline since August 2012. In the prior month, construction output had registered a revised drop of 1.0%.

In other economic news, total trade deficit in the UK widened to £3.09 billion in March, from a revised deficit of £1.18 billion in the prior month. Market participants had expected the nation to record a deficit of £2.00 billion. Additionally, leading think tank, NIESR estimated that UK's gross domestic product (GDP) rose 0.1% in the three months to April 2018, following a growth of 0.2% in the January-March 2018 period.

In the Asian session, at GMT0300, the pair is trading at 1.3527, with the GBP trading 0.07% higher against the USD from yesterday's close.

The pair is expected to find support at 1.3452, and a fall through could take it to the next support level of 1.3377. The pair is expected to find its first resistance at 1.3610, and a rise through could take it to the next resistance level of 1.3693.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.