Sample Category Title

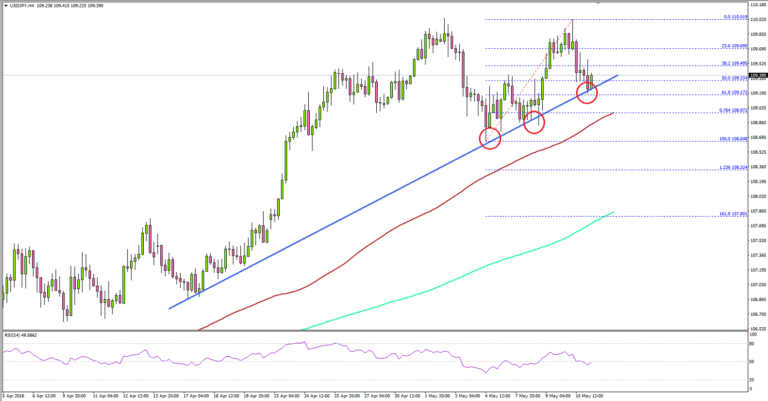

USD/JPY Testing Key Bullish Trend Support

Key Highlights

- The US Dollar corrected lower after trading as high as 110.01 against the Japanese Yen.

- There is a crucial bullish trend line formed with support 109.15 on the 4-hour chart of USD/JPY.

- The US Consumer Price Index in April 2018 posted a rise of 0.2%, less than the +0.3% forecast (MoM).

- Today, Canada’s Net Employment Change for April 2018 will be released, which is forecasted to post 17.4K.

USDJPY Technical Analysis

The US Dollar remained in a decent uptrend above 108.50 this week against the Japanese Yen. The USD/JPY pair traded a few pips above 110.00 before starting a downside correction.

It declined and traded below the 23.6% Fib retracement level of the last wave from the 108.64 low to 110.01 high. It seems like there were two rejections from the 110.00 resistance level, which ignited the current downside reaction.

However, on the downside, there is a crucial bullish trend line formed with support 109.15 on the 4-hour chart of USD/JPY. Moreover, the 61.8% Fib retracement level of the last wave from the 108.64 low to 110.01 high is at 109.17, acting as a support.

Therefore, as long as the pair is above 109.00-15, it remains supported for more gains. A break below this last could push the pair towards the 108.50 support. On the upside, an initial resistance is at 109.80, followed by the all-important 110.00 level.

Recently, the US Consumer Price Index for April 2018 was released by the US Bureau of Labor Statistics. The market was looking for a rise of 0.3% in the CPI in April 2018 compared with the previous month.

However, the actual result was a bit lower, as the CPI increased 0.2%. In terms of the yearly change, there was a rise of 2.5%, similar to the forecast. Moreover, the Consumer Price Index (CPI) Ex Food & Energy came in at 2.1%, less than the forecast of 2.2%.

The report added that:

The indexes for gasoline and shelter were the largest factors in the seasonally adjusted increase in the all items index, although the food index increased as well. The gasoline index increased 3.0 percent, more than offsetting declines in other energy component indexes and led to a 1.4-percent rise in the energy index.

Overall, the pair has to stay above the 109.00 level to avoid more losses. In the short term, there could be ranging moves above 109.00 before the next move.

Economic Releases to Watch Today

- US Import Price Index April 2018 (MoM) – Forecast +0.5%, versus 0.0% previous.

- US Export Price Index April 2018 (MoM) – Forecast +0.3%, versus +0.3% previous.

- Canada’s employment Change payrolls April 2018 – Forecast 17.4K, versus 32.3K previous.

- Canada’s Unemployment Rate April 2018 – Forecast 5.8%, versus 5.8% previous.

US CPI Takes The Dollar Off The Boil

Currency Markets

U.S. Consumer Price Index increased 0.2 percent in April, less than the 0.3 percent rise projected. Naturally, there was a bit of disappointment from the Dollar Bulls after the critical index fell a notch short of quenching bullish views on the US inflation outlook.

Mind you, the markets had already moved off the EURUSD YTD low point on profit taking before the inflation print, so the USD setback was quite tame given the breadth of the recent dollar rally, and dollar buyers are far from being knocked for six.

Understandably, the road to inflation has been a directionless and frustrating one, and while short-term market views become all too consumed by the headline print, but the NY Feds underlying inflation gauge as measured by many disaggregated price series in the CPI index is punching higher. Suggesting the elusive US inflation is not too far away from taking the stage. Certainly, the CPI miss is not cause enough to shift the Fed outlook, but inherently, the markets will be more cognizant for Fed speak and US retail sales to provide the next USD guidepost.

Given the dovish display by other central banks, the lonely Federal Reserve Board appears to be the last man standing as speculation about interest rate rises and policy normalisation in the eurozone, Japan and Britain get kicked down the road. Suggesting the dollar should remain rented at the minimum over the next few weeks, none the less the politically challenged greenback is building a convincing argument for some longer-term views. But overall it remains challenging to see just how much the EURUSD can fall given the inflationary aspect of the weaker EUR not to mention the staggering rally in crude oil over the past two months which could reignite inflation on the continent.

Oil Markets

Oil prices are here to stay, and that is a tame view. Besides the fillip from the middle east geopolitical flare-ups, the fragile supply and demand dynamics continue to tighten on the prospects of an ongoing collapse in Venezuelan output and impact of US sanctions on Iran which will be felt toward the end of 2018. The 2018 price floor it is well entrenched, so now the real work begins on 2019 forecasts. From a geopolitical perspective, it’s highly unlikely there will be a melding of minds from Syria, Israel, Saudi Arabia and Iran. And with US oil supply is being soaked up by the foreign marketplace as quickly as it can get pumped out of the ground when combined with continued OPEC compliance, the path of least resistance looks higher.

Gold Markets

A slightly weaker US dollar and heightened geopolitical risk have pumped gold higher overnight. Pick your Middle East hotspots, whether it’s s the tremors on the Iran front or the latest Israel – Syrian flare-up, the middle east powder keg is set to ignite once again. Also, the US CPI headlines suggest that the Federal Reserve Board will maintain a very gradual pace of interest rate normalisation, which is provided some much need shine to gold market overnight.

Equity Markets

US equity markets raced to a seven-week high as traders reprice lower the more hawkish expectation from the Fed. Risk continues to trade symmetrical with US interest rates, so Asia shares should open slightly higher on the back the Wall Street gains. The market singularly focused on this CPI print, which could have been a critical signpost for Fed policy if it came in above expectations. With Wall Street breathing a sigh of relief , investor were gingerly bargain hunting as the 10-Year US Treasury fell to 2.96 percent

Around the currency horn:

G-10

EURUSD: Short-term views will continue to be driven by economic surprise indexes which continued to favour a long USD position over the near-term. But just how much more juice can be extracted from the differential play remains a question. EURUSD YTD lows should form a significant base.

NZDUSD: dovish outcome from RBNZ’s Governor Orr’s inauguration has increased the spectre of NZDUSD weakness especially on a charged-up greenback

USDJPY failure to crack the 110 level has again frustrated the dollar bulls after being undermined by the CPI disappointment. General desk housekeeping will dominate today’s session as traders get recharged for next week.

USDASIA

USDMYR: The Market remains closed Friday, but the bellicose move yesterday on the sparsely traded one-month NDF to 4.255 + had everyone frantically searching for that USD bid. But this move was more about fragmented liquidly than anything else which has been a huge part of the Ringgit experience since BNM banned the collaboration of offshore markets vis a vis NDF’s. I think Monday open, however, locals will respect the implied one-month NDF which is predicated on foreign money risk transfer expectations. And despite my rather overly optimistic 4.05 USDMYR Monday open view, I still maintain this will be much closer to the plot than some of the outrageous 4.50 calls. But the resurgent USD and higher US yields remain the biggest headwinds for the local sentiment and should keep investors on the defensive over the near to medium term.

Korean Won: On the first sign of dollar weakness the Won continues to be the go-to regional currency. Very difficult to ignore the communal benefits from Panmunjom Declaration by the two Koreas. Also, Trump -Kim meeting in Singapore Jun 12 is taking on very congenial swag.

Indian Rupee: Beside the strong USD dollar and higher US yields the bulk of the stress is coming from the oil patch. And it certainly looks like Oil is here to stay if not push higher in coming months based dwindling supply narrative. Suggesting more pain for the Rupee.

Eco Data 5/11/18

[php_everywhere instance="1"]

AUD & CAD strongest for today, GBP & NZD weakest. But how real is that?

It's rather rare to see AUD/NZD as the top mover but there it is. And, just from a quick glance, AUD/NZD, GBP/AUD, NZD/CAD, GBP/CAD, we know then AUD and CAD are the strongest while GBP and NZD are the weakest.

It's easily reflected in the D heat map. But are the strong ones that strong and the weak ones that weak?

A look in the W heat map, we see that NZD is in red all the way, and is trading below last week's low against USD, JPY , CAD and AUD. Yes, the weakness is apparent.

How about GBP? It's just down again USD and CAD for the week. If BoE is as dovish as some people said, we should be seeing GBP all the way in red like NZD. But no. When BoE is still on track for a hike, it's not dovish. And as we pointed out earlier, the overall announcement was still more hawkish than the least hawkish scenario.

CAD is clearly in all deep blue, even against USD, except versus JPY and AUD. Trump's boost to oil price is apparent. Still, CAD will face a test of employment data tomorrow. We'll see when it can pocket the gains for the week.

AUD? It's just mixed. For now, it's even trading down for the week against GBP!

Bank of England Review: Keeping the Hiking Cycle Alive But Timing is Data Dependent

Hiking cycle postponed, not cancelled

As expected, the Bank of England decided not to hike the Bank Rate at this meeting (vote count unchanged 7-2, a bit dovish as some had thought it might be 6-3), as economic indicators surprised to the downside. The seven members voting for staying on hold thought that it would be good to see 'how the data unfold over the coming months to discern whether the softness in Q1 might persist', as the 'cost of waiting was likely modest', supporting our view that the hiking cycle is postponed, not cancel led, but that there will be fewer rate hikes than previously thought. BoE governor Mark Carney highlighted a couple of hawkish things at the press conference: (1) he said that growth only needs to pick up slightly to be above potential (0.25% q/q), which should tighten the labour market further, and (2) domestic cost pressure is increasing with stronger wage growth. It is interesting that the projections (inflation staying above or at 2% over the forecast horizon and the unemployment rate to drop further to 4%) are based on the market pricing from before the meeting of approximately one hike a year the next three years. We stick to our call with one hike in H2 18 and one in 2019 with the next hike likely in August. That said, the probability of August has declined slightly, as we only get three months more data in August, which may not be enough for the majority of the BoE members.

Market expectations of future rate hikes dropped slightly after the announcement and UK interest rates dropped some 3-5bp across the 2-10Y yield with a modest steepening of the yield curve, as the shorter-dated tenors declined the most. The market is now pricing around 50% probability of a rate hike in August, while the first full 25bp rate hike is priced to arrive in February 2019. Timing of the next BoE rate hike remains highly data dependent and we see market pricing as fair for now, with risks skewed to the upside for UK yields in the coming months, if we are right in our call that the BoE will hike the Bank Rate in August.

FX outlook: we still look for a lower EUR/GBP in the medium and longer term

EUR/GBP traded higher on the announcement and was shortly above the 0.88 level. Especially the 7-2 vote in favour of keeping the Bank Rate unchanged might have been a disappointment for some GBP long players who had expected a more divided MPC (i.e. a 6-3 vote). With an August rate hike still in sight in our view, we see relative interest rates as neutral for EUR/GBP for now, but expect the GBP to eventually gain support from the rate channel. We target 0.88 in 1M and 0.8650 in 3M.

Longer term, Brexit remains a key driver for the GBP and while uncertainty remains high, we still expect EUR/GBP to eventually trade lower driven by Brexit clarifications and fundamental valuations. The turn in capital flows and FDI flows back into the UK, as indicated in the latest balance of payment data, suggest that a key headwind to the GBP seen in Brexit is reversing, supporting the case for additional GBP appreciation in the medium term. We target EUR/GBP at 0.84 in 6M and 0.83 in 12M (0.84).

Macro charts

Bank of England’s projections

Bank of England’s projections

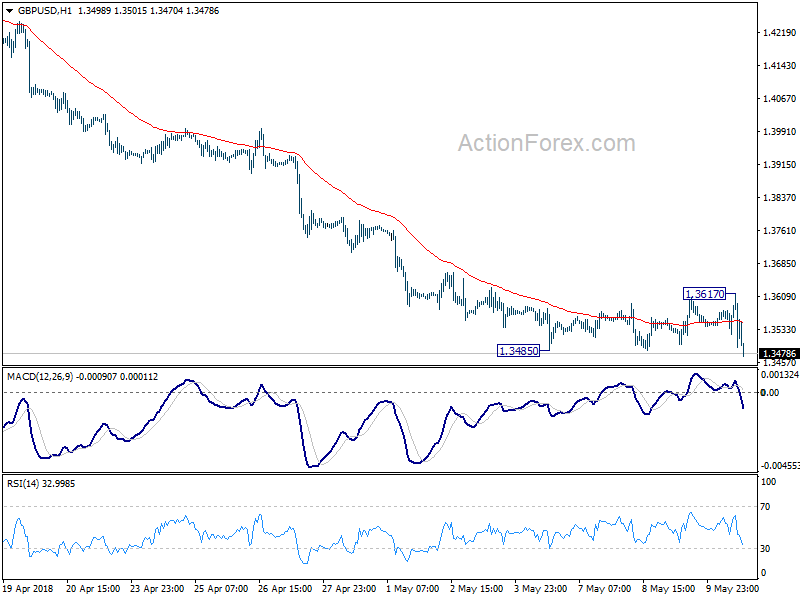

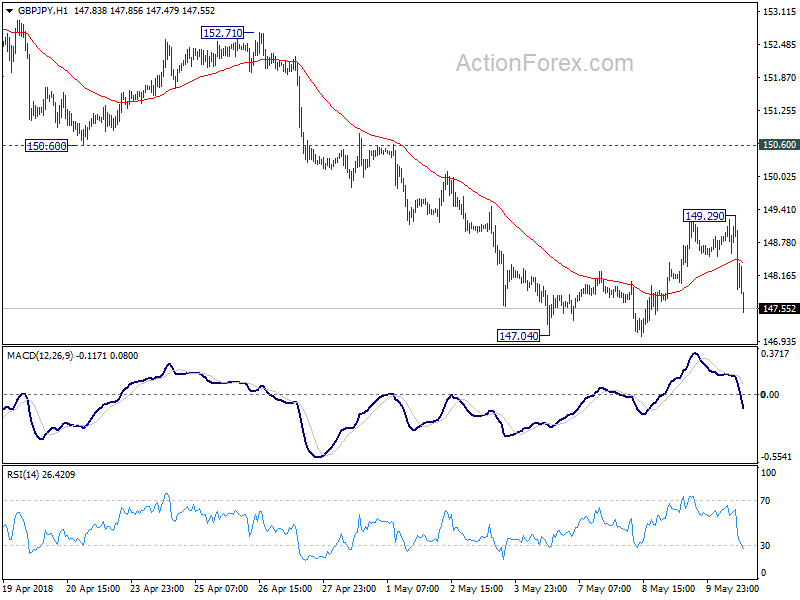

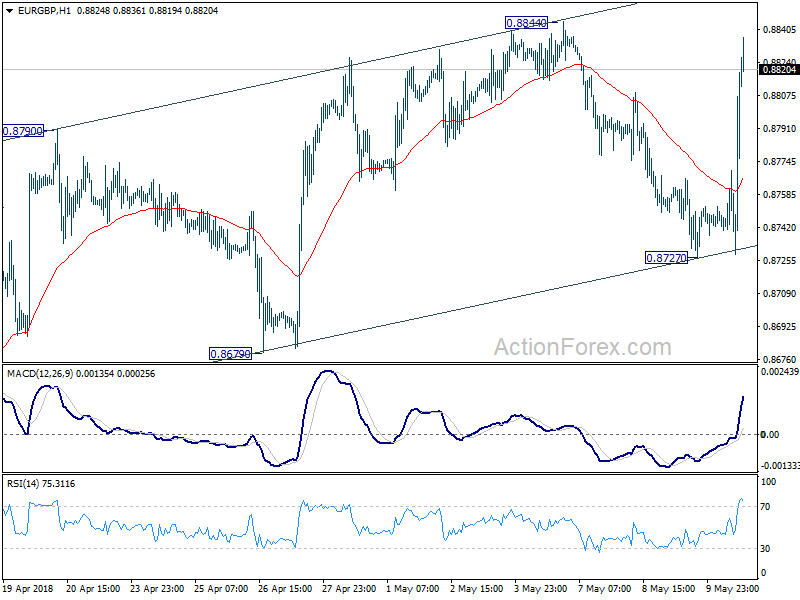

GBP/USD breaks 1.3485 support. But bears need to show more commitment

Fresh selling is seen in GBP three hours after BoE rate announcement. GBP/USD breaches 1.3485 to 1.3470 so far. We'll see if it can settle below this support to confirm decline resumption.

For now, GBP/JPY is still holding above 147.04 support.

EUR/GBP is also held below 0.8844 resistance.

GBP bearish will need to show more commitment.

Energy and Food Drive Pickup in April CPI

CPI came in a little softer than expected in April (up 0.2 percent) amid a more tempered gain in the core index (up 0.1 percent). The softer core print likely reflects some exaggerated strength in Q1. The trend remains higher.

CPI Rebound in April

After slipping 0.1 percent in March, consumer price inflation strengthened in April with the index rising 0.2 percent. The pickup stemmed largely from the volatile energy and food components.

Energy prices reversed course in April, rising 1.4 percent after a pullback in March. Gasoline prices are beginning to put a noticeable dent in consumer purchasing power, having risen 13.4 percent over the past year.

Food prices increased 0.3 percent, which was the largest monthly gain in a little over a year. Although still running below overall CPI, food inflation has been strengthening over the past year as related commodity prices have been little changed and restaurants and other prepared food establishments have been contending with rising labor costs.

Core Eases, But Path Still Higher

After a hot first quarter, where core CPI rose at the fastest clip in 12 years, inflation ex-food and energy cooled in April. In our view, the slowdown likely reflects exaggerated strength early in the year, rather than an end to the strengthening trend in underlying inflation.

Core services inflation in April eased to 0.2 percent. Shelter prices, which account for about 40 percent of the core index, continue to be a primary source of support, having increased 0.3 percent. Softer monthly readings were seen in that category, however, as well as in medical and transportation services. Meanwhile, core goods were back in deflation territory for a second straight month (down 0.1 percent). Vehicle prices were the primary drag, down 0.9 percent, as demand for new vehicles has ebbed and the used car market is contending with a flood of off-lease vehicles.

Upward Trend Sufficient for Further Fed Hikes

Although inflation came in a bit softer than expected in April, we do not believe this will prevent the Fed from raising rates another three times this year. Over the past year, headline inflation is up 2.5 percent, compared to a 2.2 percent increase this time last year. What's more, core inflation remained steady at 2.1 percent. Over the past 15 years, core CPI has run 0.2 percentage points above the core PCE deflator, making the current rate nearly in line with the Fed's target.

We expect inflation to rise further in the months to come. Most immediately, the return of $70 oil stands to push up monthly readings of headline inflation at least through May. While we see oil falling in the second half of the year, prices are expected to remain above the levels that prevailed a year ago. Food-related commodity prices have also been fairly stable over the past year after falling from 2014 to early 2017. Core inflation should present a clearer sign of strengthening inflation. We expect core CPI to rise to 2.3 percent by Q3 as rising labor and material costs lead more firms to raise prices.

British Pound Trading Sideways as BoE Maintains Rates

The British pound continues to trade sideways this week. In Thursday’s North American trade, GBP/USD is trading at 1.3533, down 0.10% on the day. On the release front, it’s a busy day on both sides of the pond. British Manufacturing Production declined for a second straight month. The reading of -0.1% was just above the forecast of -0.2%. Britain’s trade deficit widened to GBP -12.3 billion, above the estimate of -11.2 billion. As expected, the Bank of England held the course on monetary policy, maintaining interest rates at 0.50%. In the US, unemployment claims dropped to 211 thousand, easily beating the estimate of 219 thousand. US inflation numbers were not as strong. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. On Friday, the key event is UoM Consumer Sentiment.

Market predictions about the Bank of England were on the money, and the pound has showed little reaction on Thursday. As expected, the BoE held rates at 0.50%, with only two of nine MPC members voting for a rate hike. In the inflation report, policymakers noted concern over softness in consumer borrowing and the housing market. The markets were not surprised by the BoE decision, given the fact that first-quarter growth was just 0.1% and consumer spending an inflation levels weakened. Policymakers are hopeful that economic growth will rebound in Q2, and are adopting a wait-and-see attitude towards rate hikes, with a rate hike unlikely before August, which is when the next inflation report will be released.

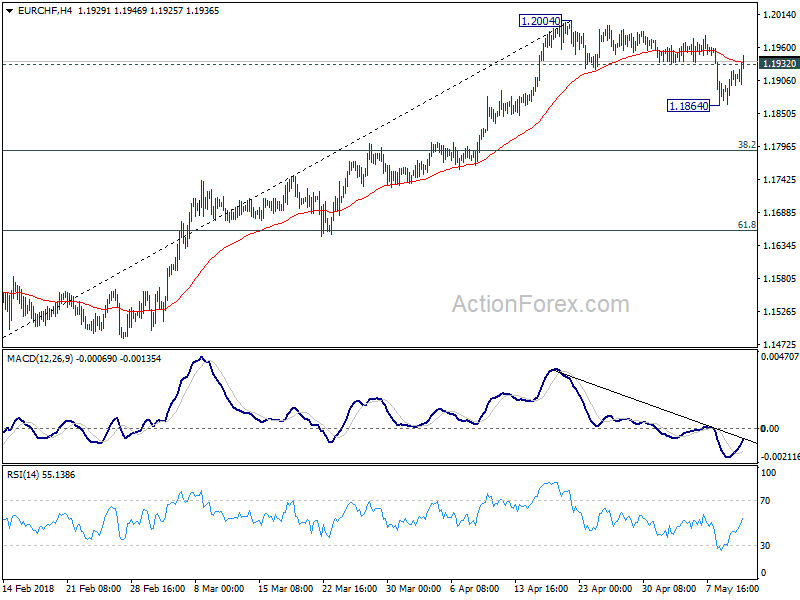

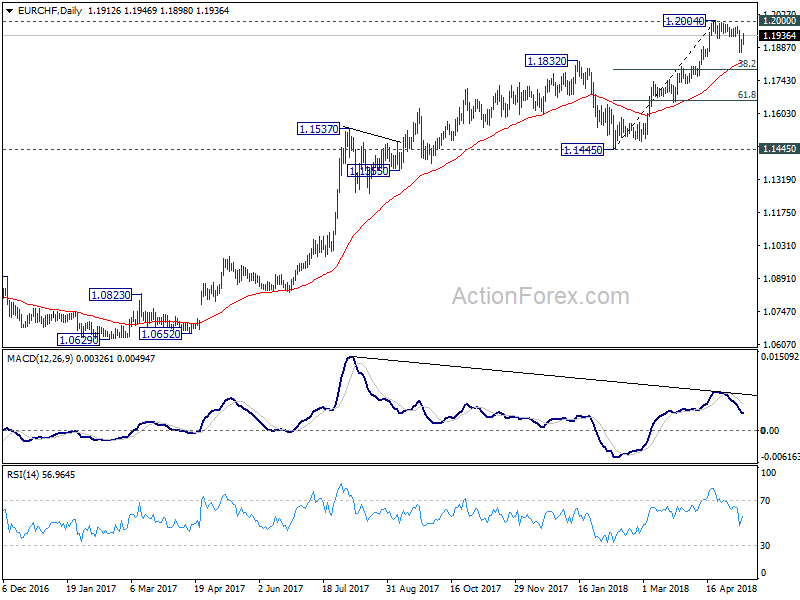

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1880; (P) 1.1901; (R1) 1.1936; More...

EUR/CHF's break of 1.1932 now suggests that pull back from 1.2004 could have completed at 1.1864 already. Intraday bias back on the upside for 1.2004. Firm break there will confirm up trend resumption. Nonetheless, before that, more consolidative could be seen and below 1.1864 will bring another pull back. Though, we'd expect strong support from there to bring rebound.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2000 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next. However, considering bearish divergence condition in daily MACD. Break of 1.1445 will be an indication of medium term reversal and will turn outlook bearish.

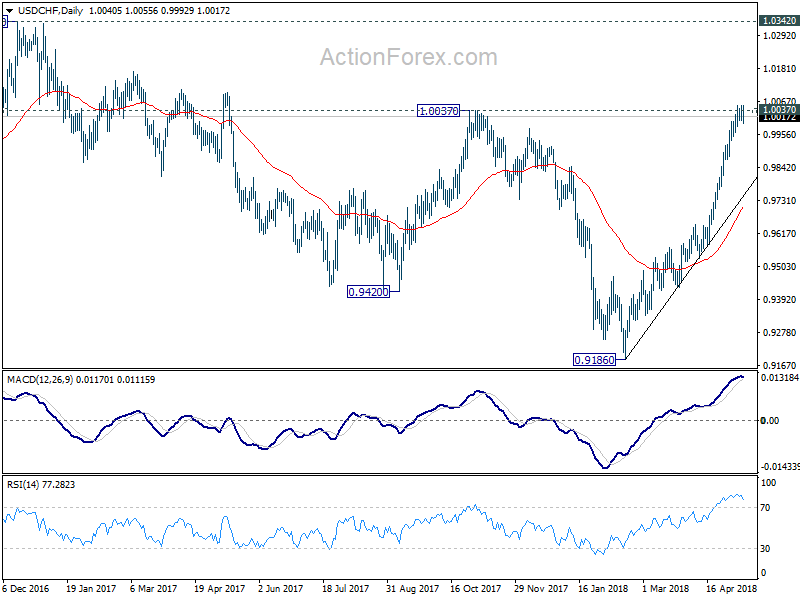

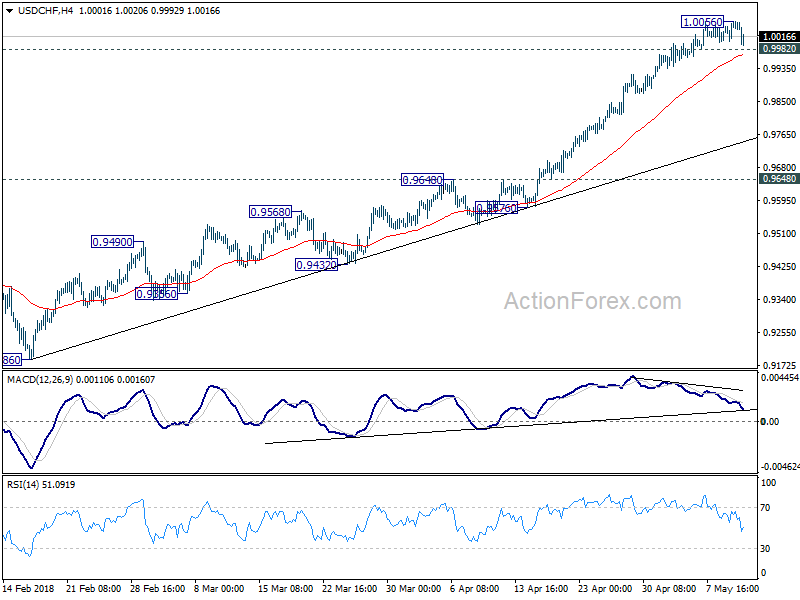

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0018; (P) 1.0036; (R1) 1.0070; More...

Intraday bias in USD/CHF is turned neutral with today's dip. But consolidation would brief as long as 0.9982 minor support holds. Break of 1.0056 will resume recent rise for 1.0342 key resistance. However, break of 0.9982 will turn bias to the downside for deeper pull back, possibly to trend line support (now at 0.9748) before staging another rally.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 0.9648 resistance turned support holds, even in case of pull back.