Sample Category Title

BoE cut 2018 GDP forecast. Also lowered 2018, 2019, 2020 inflation forecasts

In the updated projections, BoE revised down four-quarter real GDP growth forecast in Q2 2018 to 1.4%, down from February's 1.8%. Four-quarter GDP real GDP growth forecast in Q2 2019, Q2 2020 are held unchanged at 1.7%.

Four-quarter inflation rate forecast for Q2 2018 was revised down to 2.4%, down from February's 2.7%. For Q2 2019, inflation forecast was revised down from to 2.1%, from 2.2%. Q2 2020 inflation forecast was revised down to 2.0%, from 2.1%.

The updaed conditioning path for Bank Rate showed that the economic projections are based on the assumption of 1 rate hike this year, in Q3. That is, probably in August.

Markets Flat Ahead Of BoE Decision

- BoE Expected to Leave Rates on Hold;

- Projections, Voting and Press Conference Key;

- Oil Makes Further Gains After Trump Announcement.

'While policy makers have appeared to be preparing markets for such a hike, the data has turned'

It's been a relatively flat start to trading on Thursday as we await the latest monetary policy announcement from the Bank of England and the economic projections and press conference that follow.

The BoE is due to announce its decision on interest rates shortly and, following an apparent U-turn in recent weeks, policy makers are widely expected to leave them unchanged for now. There has been a clear and growing desire on the Monetary Policy Committee in recent months to lift the Bank Rate above 0.5% for the first time since 2009 after inflation rose above 3%, far surpassing the central bank's target of 2%.

While policy makers have appeared to be preparing markets for such a hike, the data has turned, with inflation falling back to more acceptable levels – albeit still above target – while quarterly growth fell to only 0.1% in Q1 and surveys on services, manufacturing and construction have underwhelmed. It may be the case that the 'beast from the east' was largely responsible for much of the slowdown later in the quarter but it seems policy makers would like to see evidence of a rebound before committing to higher rates.

'The claim that the MPC is conscious that there are other meetings this year appeared to be a clear nod to the fact that May is no longer the favoured time for a hike'

Of course there are some that may dismiss the data due to the one-off factors associated with it and so the vote may not be unanimous but the recent comments from Governor Mark Carney appeared to be an attempt to manage market expectations. The claim that the MPC is conscious that there are other meetings this year appeared to be a clear nod to the fact that May is no longer the favoured time for a hike and triggered a substantial change in pricing for it, with the implied probability having since fallen to only 13%.

With that in mind, a rate hike today looks very unlikely – albeit still possible – which makes the new economic projections, voting and press conference all the more interesting. Traders are very keen to know when we can now expect a hike which could make UK markets quite volatile in the hours after the announcement. With Brexit discussions hoping to be wrapped up in the next six months, it will be interesting to see whether the BoE hints at holding off until November until the outlook become much clearer or simply delays the decision until August.

'While it remains unclear what impact the sanctions will have on output, the moves we've so far seen suggest there is a belief it will be significant'

In the aftermath of Donald Trump's announcement on the Iran nuclear deal, oil has continued to rally on Thursday although the gains the are being made are now slowing. While it remains unclear what impact the sanctions – which are not backed by the other countries that signed up to the initial agreement – will have on output, the moves we've so far seen suggest there is a belief it will be significant.

While the countries that have been cutting production in recent years to rebalance the market could offset the void left by the sanctions, it's not clear that the appetite will be there to do so and the reaction in the markets suggest traders are assuming they won't. With Brent crude fast approaching $80 a barrel and WTI above $70, it will be interesting whether the same appetite for cuts will remain in the months ahead and if not, whether prices may be peaking.

BoE keeps Bank Rate unchanged at 0.50% with 7-2 vote. Full Statement

BoE keeps Bank Rate unchanged at 0.50% with 7-2 vote. Asset purchast target held at GBP 435B by 9-0 vote.

Statement below. Full Inflation Report here.

Bank Rate Maintained at 0.50%

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 9 May 2018, the MPC voted by a majority of 7-2 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

The MPC's updated projections for inflation and activity are set out in the May Inflation Report. The outlook and the main factors shaping it are broadly similar to those set out in the previous Report.

The preliminary estimate of GDP growth in the first quarter was 0.1%, 0.3 percentage points lower than expected in February. This is likely in part to have reflected adverse weather in late February and early March. Survey indicators suggest that growth was somewhat stronger in Q1 than implied by the preliminary estimate.

Despite the near-term softness, the MPC's central forecast for economic activity is little changed from that in the previous Report. In the MPC's central forecast, conditioned on the gently rising path of Bank Rate implied by current market yields, GDP is expected to grow by around 1¾% per year on average over the forecast period. On the expenditure side, growth continues to rotate towards net trade and business investment and away from consumption. Although business investment is still restrained by Brexit-related uncertainties, it is being supported, like exports, by strong global demand and accommodative financial conditions. Household consumption growth remains subdued, in line with the modest growth in real income over the forecast period.

Wage growth and domestic cost pressures are firming gradually, broadly as expected. The MPC continues to judge that the UK economy has a very limited degree of slack. Hiring intentions have remained strong and, over the past three months, the unemployment rate has fallen slightly further. While modest by historical standards, the projected pace of GDP growth over the forecast is nonetheless slightly faster than the diminished rate of supply growth, which averages around 1½% per year. In the MPC's central projection, therefore, a small margin of excess demand still emerges by early 2020, feeding through into higher rates of pay growth and domestic cost pressures.

CPI inflation fell to 2.5% in March, lower than expected at the time of the February Report. The inflation rates of the most import-intensive components of the CPI appear to have peaked. The MPC judges that the impact of the past depreciation of sterling on CPI inflation, while remaining significant, is likely to fade a little faster than previously thought. Taking external and domestic influences together, CPI inflation is projected to fall back slightly more quickly than in February, reaching the target in two years. These projections are conditioned on a gently rising path for Bank Rate over the next three years.

In the exceptional circumstances presented by Brexit, as specified in its remit, the MPC has been balancing any significant trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity. The prospect of excess demand over the forecast period has reduced the degree to which it is appropriate for the MPC to accommodate an extended period of inflation above the target. The Committee's best collective judgement therefore remains that, were the economy to develop broadly in line with the May Inflation Report projections, an ongoing tightening of monetary policy over the forecast period would be appropriate to return inflation sustainably to its target at a conventional horizon. As previously, however, that judgement relies on the economic data evolving broadly in line with the Committee's projections. For the majority of members, an increase in Bank Rate was not required at this meeting. All members agree that any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent.

(BOE) Bank Rate Maintained at 0.50%

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 9 May 2018, the MPC voted by a majority of 7-2 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

The MPC's updated projections for inflation and activity are set out in the May Inflation Report. The outlook and the main factors shaping it are broadly similar to those set out in the previous Report.

The preliminary estimate of GDP growth in the first quarter was 0.1%, 0.3 percentage points lower than expected in February. This is likely in part to have reflected adverse weather in late February and early March. Survey indicators suggest that growth was somewhat stronger in Q1 than implied by the preliminary estimate.

Despite the near-term softness, the MPC's central forecast for economic activity is little changed from that in the previous Report. In the MPC's central forecast, conditioned on the gently rising path of Bank Rate implied by current market yields, GDP is expected to grow by around 1¾% per year on average over the forecast period. On the expenditure side, growth continues to rotate towards net trade and business investment and away from consumption. Although business investment is still restrained by Brexit-related uncertainties, it is being supported, like exports, by strong global demand and accommodative financial conditions. Household consumption growth remains subdued, in line with the modest growth in real income over the forecast period.

Wage growth and domestic cost pressures are firming gradually, broadly as expected. The MPC continues to judge that the UK economy has a very limited degree of slack. Hiring intentions have remained strong and, over the past three months, the unemployment rate has fallen slightly further. While modest by historical standards, the projected pace of GDP growth over the forecast is nonetheless slightly faster than the diminished rate of supply growth, which averages around 1½% per year. In the MPC's central projection, therefore, a small margin of excess demand still emerges by early 2020, feeding through into higher rates of pay growth and domestic cost pressures.

CPI inflation fell to 2.5% in March, lower than expected at the time of the February Report. The inflation rates of the most import-intensive components of the CPI appear to have peaked. The MPC judges that the impact of the past depreciation of sterling on CPI inflation, while remaining significant, is likely to fade a little faster than previously thought. Taking external and domestic influences together, CPI inflation is projected to fall back slightly more quickly than in February, reaching the target in two years. These projections are conditioned on a gently rising path for Bank Rate over the next three years.

In the exceptional circumstances presented by Brexit, as specified in its remit, the MPC has been balancing any significant trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity. The prospect of excess demand over the forecast period has reduced the degree to which it is appropriate for the MPC to accommodate an extended period of inflation above the target. The Committee's best collective judgement therefore remains that, were the economy to develop broadly in line with the May Inflation Report projections, an ongoing tightening of monetary policy over the forecast period would be appropriate to return inflation sustainably to its target at a conventional horizon. As previously, however, that judgement relies on the economic data evolving broadly in line with the Committee's projections. For the majority of members, an increase in Bank Rate was not required at this meeting. All members agree that any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent.

Euro Steady In Holiday-Thin Trade, US Consumer Inflation Next

EUR/USD is showing little movement in the Wednesday session. Currently, the pair is trading at 1.1884, up 0.27% on the day. In economic news, German and French banks are closed for a holiday. ECB releases an economic bulletin, and the US will publish consumer inflation reports. CPI is expected to rebound with a gain of 0.3%, while Core CPI is expected to remain unchanged at 0.2%. On Friday, ECB President Mario Draghi will speak at an event in Florence and the US releases UoM Consumer Sentiment.

The currency markets have not shown much interest in President Trump’s dramatic speech on Tuesday. Trump announced that the US would withdraw from the Iran nuclear deal. Trump blasted the agreement and said that the US would impose stiff sanctions on Iran. However, Britain, France and Germany have said they plan to remain in the deal, and will be holding a high-level meeting with Iranian leaders on how the agreement can be salvaged. With the US acknowledging that the White House does not have a ‘Plan B’, it’s unclear what happens next. Meanwhile, tensions between Israel and Iran are at a fever pitch after Israel struck dozens of military targets in Syria on Tuesday.

The ECB continues to send a message of cautious optimism to the markets, and this was underscored by the ECB Economic Bulletin. The report stated that the eurozone economy continues to show “solid and broad-based expansion” but did acknowledge that growth in the first quarter slowed. As for inflation, policymakers remain confident that inflation will continue to move towards the inflation target of 2 percent. However, inflation remains subdued and has not shown signs of an upward trend. The report reaffirmed that the ECB plans to maintain interest rates at current levels for an “extended period of time, and well past the horizon of the net asset purchases.”

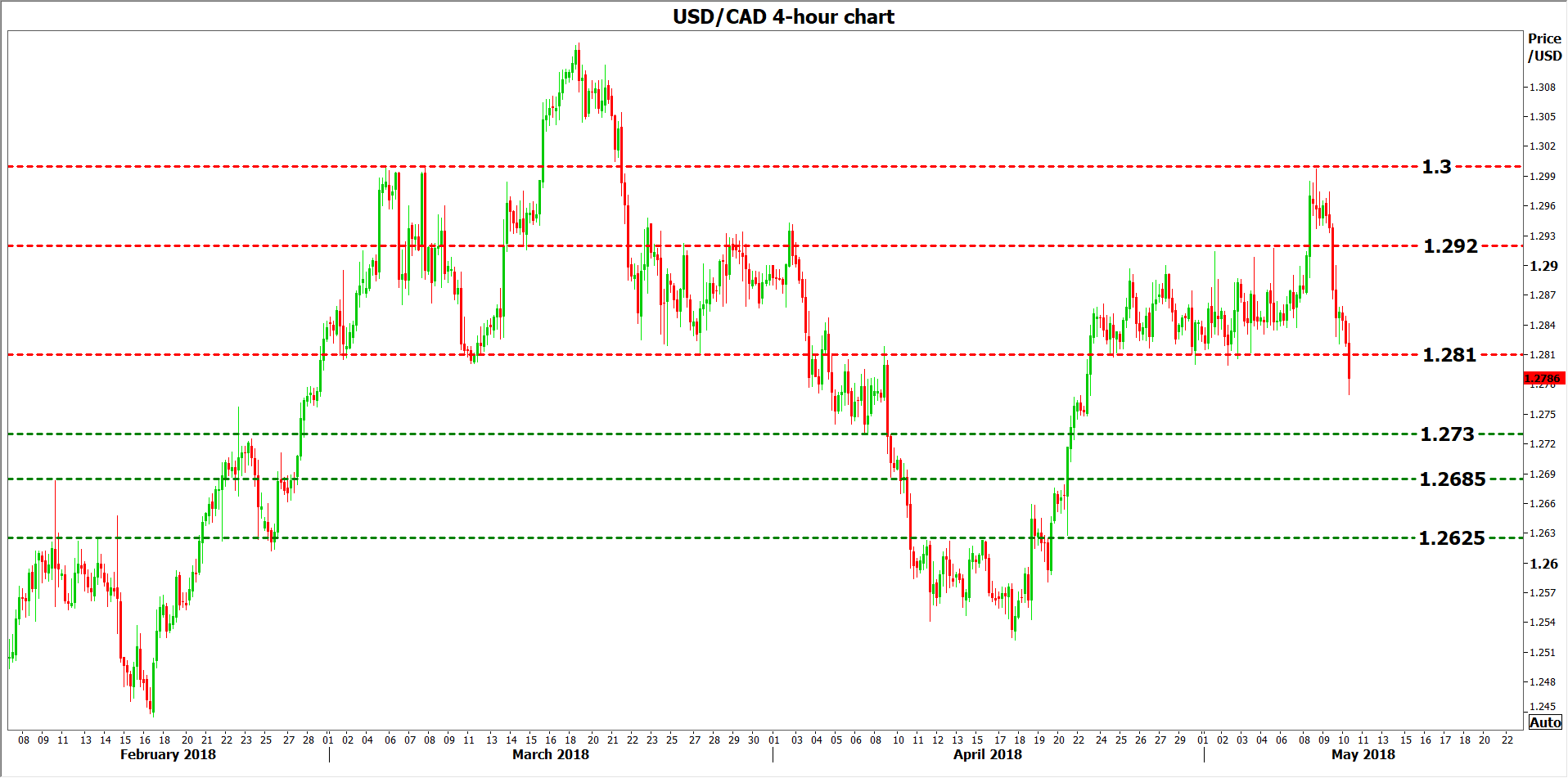

Canadian Jobs Data Next In Line To Shake The Loonie

Canada's employment data for April are due out on Friday at 1330 GMT. Forecasts point to another solid report, which would confirm the Bank of Canada's (BoC) view that any remaining labor market slack is quickly being absorbed. While a strong set of figures may support the loonie on the news, the currency's broader direction will also depend on any movements in oil prices.

Canada's labor market posted a soft start to the year, but that seems to have been transitory, as jobs data have rebounded strongly recently. The unemployment rate has fallen back to a decade low of 5.8%, while the monthly net change in employment has remained well-within positive territory. It appears the jobs market is firing on all cylinders, something that the upcoming numbers are expected to confirm.

In April, the unemployment rate is forecast to have held steady at 5.8%, while the net change in employment is anticipated to have moderated a little, but to have remained within positive territory. Adding some credence to these forecasts is the Markit manufacturing PMI for the month, which showed another “robust increase in staff recruitment”.

While there are still a lot of risks surrounding Canada – including headwinds around trade, high household debt levels and competitiveness challenges – another set of solid jobs data would still be pleasant news for the BoC and could raise the likelihood for a near-term rate increase. The probability for a rate hike at the upcoming meeting in May is only 30%, according to Canada's overnight index swaps. That said, investors are much more confident about the July gathering, assigning a 90% probability to a hike then.

If the employment data are stronger than anticipated, that may seal the deal for a July hike, bringing the loonie under renewed buying interest. Declines in dollar/loonie could find initial support near the 1.2730 barrier, the low of April 6. Further down, focus would shift to 1.2685, the peak of February 9, and then to the April 16 high at 1.2625.

Conversely, a weaker-than-expected report could generate doubts about a July hike, and thereby weigh on the loonie. Advances in dollar/loonie may stall near 1.2810, an area that halted multiple declines in early May. An upside break of that zone could open the way for 1.2920, defined by the May 4 peak. Further up, the 1.3000 psychological barrier may provide resistance.

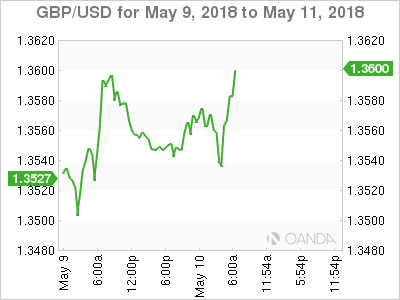

GBP/USD Rounding Bottom Shaping Up On Super Thursday

The single most important event today is Super Thursday. At 11 AM GMT (13:00 CEST) the BOE (Bank of England) will publish its latest interest rate decision, the minutes of that meeting showing what was discussed and how the voting went, and the quarterly inflation report. Depending on the vote split and the hawkish/dovish tone of the BOE governor, Mark Carney, we might expect volatile price movement on the GBP/USD. The vote is reported in an X-X-X format - the first number is how many MPC members voted to increase interest rates, the second number is how many voted to decrease rates, and the third is how many voted to hold rates.

The consensus is 2-0-7. Any deviation should move the price. On 2-0-7 the GBP/USD should still move up, but 3-0-6 and above should move it even higher. Dovish hold on current interest rates would be in a 0-0-9 format. It is crucial that traders pay attention to vote split and Carney's comments. Technically the rounded bottom is shaping up giving a slight boost for bulls. Above 1.3574 the pair is bullish, and targets are 1.3609, 1.3652 and 1.3693. Below 1.3514 we might expect 1.3482 and 1.3435. MACD is also printing higher lows, and it tells me that market is expecting a possible bullish move. But be careful, we don't know anything until the news release is live.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

M H4 - Monthly Camarilla Pivot (Very Strong Monthly Resistance)

M L3 – Monthly Camarilla Pivot (Monthly Support)

M L4 – Monthly H4 Camarilla (Very Strong Monthly Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Bank Of England To Deliver A ‘Hawkish’ Hold

With the Bank of England (BoE) widely expected to hold interest rates steady this morning (07:00 am EDT) after recent comments from Governor Carney and weaker economic data, the key focal point for many will be whether U.K policy makers will signal a rise in August. The current odd's for a hike today is +10%. The vote is expected to be a unanimous 9-0 decision.

Hawkish hold

A 'hawkish hold' from the BoE meeting would mean the central bank is expected to reiterate its commitment to raising rates in the coming months. To many, this seems justified despite the recent slowdown in economic growth – U.K GDP for Q2 rose by +0.1% q/q, below a market forecast of +0.3%.

Fixed income dealers are currently pricing in just over +50% probability of another rate hike in the BoE's August meeting. A summer hike again becomes dependent on U.K data to improve in order to keep rate-increase expectations on track.

Sterling 'bulls' will be hoping that the BoE keeps the prospect of a summer hike alive, as they will be expecting GBP (£1.3570) to find some much needed support after the poor run in the last few weeks.

Pound 'bears' will be exposed to renewed weakness if the BoE does not give a clear signal and that it's still considering raising rates further this year. For now, rate uncertainty is keeping GBP confined to tighter ranges.

A summer hike again becomes dependent on U.K data to improve in order to keep rate-increase expectations on track.

U.K manufacturing output disappoints

Sterling has risen slightly since data this morning showed that the U.K manufacturing output fell -0.1% in March – the second straight drop after almost a year of growth – in another sign that the economy is in a soft patch, though the fall was less steep than the -0.2% expected by the street. According to the ONS, the sector was dragged down by weaker electrical equipment and pharmaceutical production.

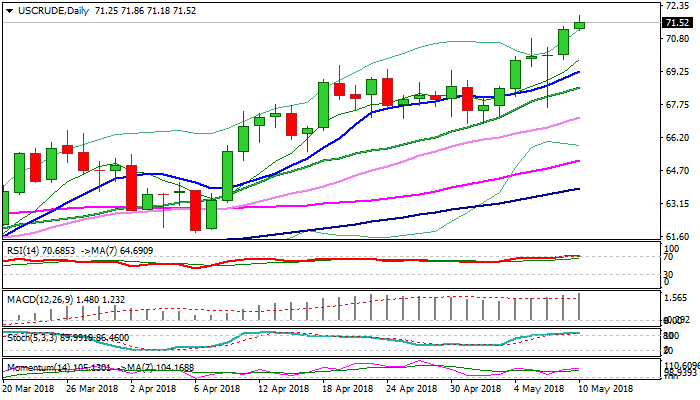

WTI Oil Rallied To New 3 ½ Year High, Boosted By Escalation Of Tensions In The Middle East/Strong Draw...

WTI oil extends strong rally into third straight day on Thursday and hit new 3 ½ year high at $71.86.

Oil prices accelerated sharply higher this week after President Trump announced US withdrawal from nuclear agreement with Iran, additionally boosted by strong draw in US crude inventories (EIA report showed 2.19 million barrels draw last week, compared to 0.2 million barrels draw forecasted) and escalation of tensions between Israel and Iran which threatens to worsen fragile situation in the Middle East and disrupt supply from the region.

In addition, reports showed further rise of US shale oil production which hit all-time high at 10.7 million barrels per day, approaching world’s top oil producer Russia which produces around 11 million barrels per day.

All these factors are supportive for oil price, which could accelerate further, if situation in the Middle East deteriorates.

Bullish studies maintain strong momentum and could drive oil price towards next target at $76.35 (Fibo 61.8% of 107.45/$26.04 fall) in coming sessions.

Corrective dips are expected to offer better buying opportunities, with rising 10SMA ($69.26) expected to keep the downside protected.

Res: 71.86, 72.24, 73.00, 73.27

Sup: 71.18, 70.81, 70.00, 69.84

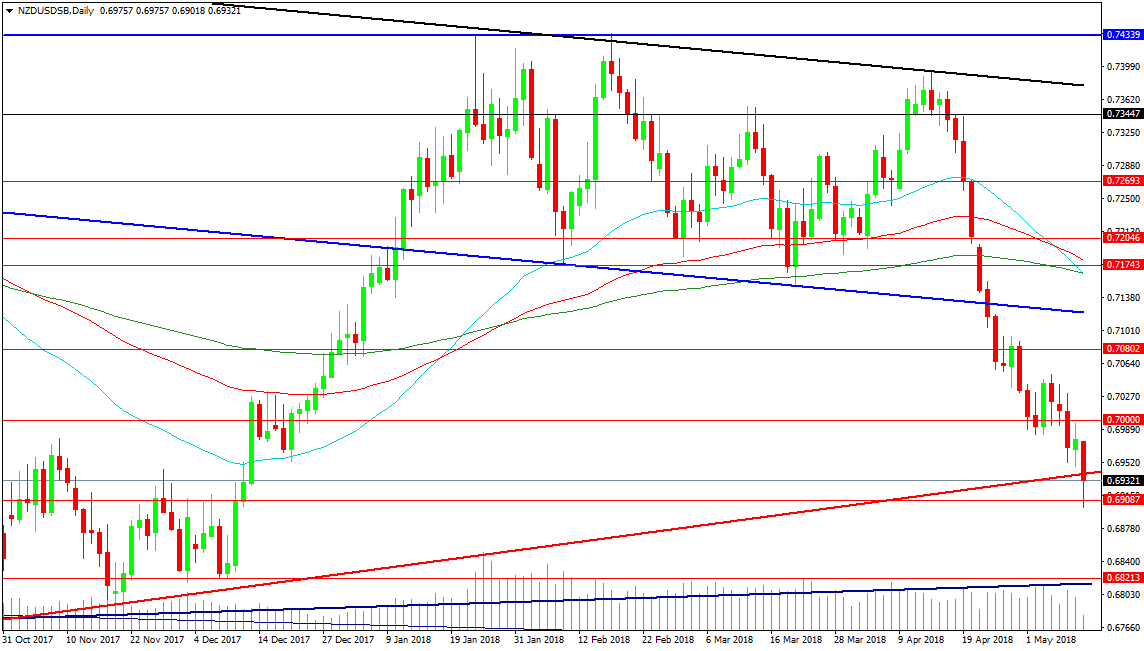

Forex Analysis: NZDUSD And GBPJPY

The RBNZ left rates on hold adding to the woes in the NZDUSD pair. The price fell to fresh lows for the year at 0.69018, pushing under the red supporting trend line on the chart. A retest of this trend line as resistance is now likely at 0.69360. The next level of support traders are watching comes in at 0.68200 and the rising blue trend line. The price is now in an area of consolidation from October/November 2017, which saw price bottom at 0.67800. A loss of this area would target 0.66800.

Resistance comes in at 0.70000, where the price consolidated for much of last week. A squeeze higher from current prices would target the falling blue resistance trend line at 0.71259 and take out stops from this week’s fall. A further push higher would have to contend with the moving averages around 0.71740 before an attempt on 0.72000. A move back into the trading range of earlier this year would see a higher low created and give long positions hope of breaking this year’s highs of 0.74340.

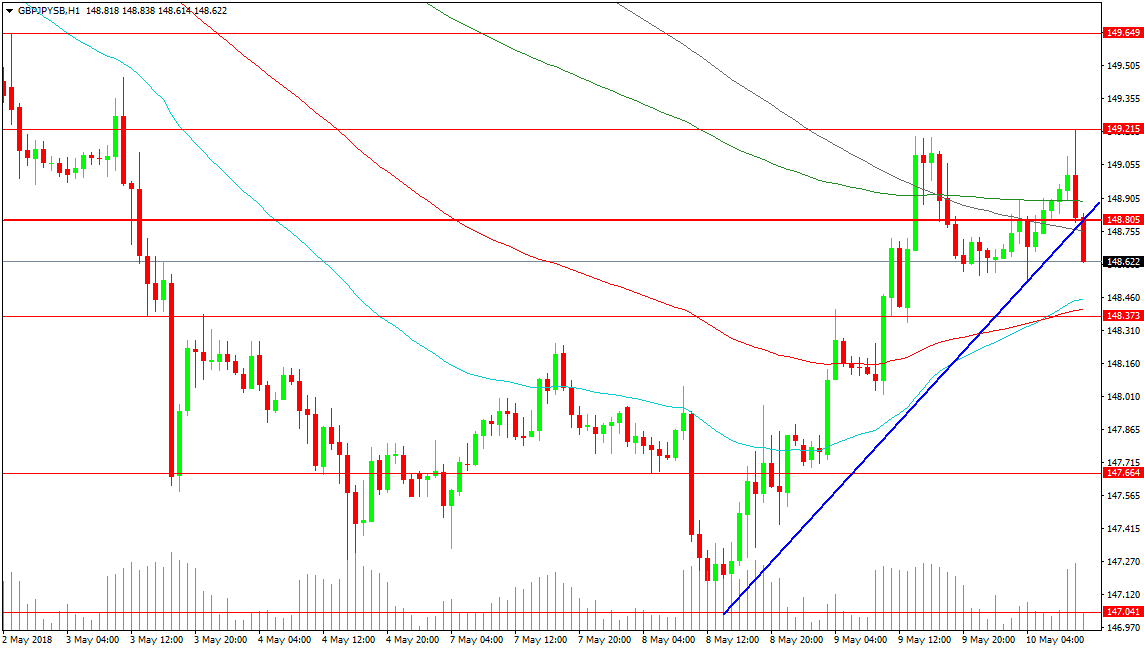

GBPJPY

This pair will be influenced by the BOE Rate Decisions and Statements later today. The price is already falling under support after being rejected from the high created at 149.215 yesterday. This morning, the 148.805 level failed along with the rising blue trend line support. The 50-hour MA at 148.454 is the next support level, closely followed by the 100-hour at 148.408 and the 148.375 level. A loss here would drive the price lower under this key area to test 148.000 and 147.664. The low from May comes in at 147.040.

Should support hold, the price can push higher or consolidate further in the current range until a break above yesterday’s high can be attempted. Resistance at 149.650 marks out the path to a retest of the 150.000 level, followed by the 150.800 area.