Sample Category Title

EURUSD – 10SMA To Cap Extended Upticks Before Bears Continue

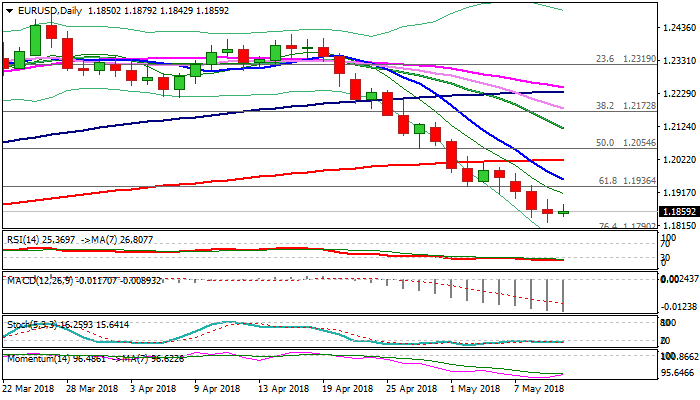

Bears are taking a breather in early Thursday's trading and holding within narrow consolidation above new 4 ½ month low at 1.1822, posted on Wednesday.

Overall structure remains bearish and favors further weakness for test of initial target at 1.1790 (Fibo 76.4% of 1.1553/1.2555 ascend), with extension towards next key support at 1.1709 (Fibo 38.2% of 1.0340/1.2555 rally).

Meanwhile, the pair may bounce higher on positioning for fresh weakness, as 14-d momentum turns higher and provides positive signal.

Initial resistance lies at 1.1936 (broken Fibo 61.8% of 1.1553/1.2555 upleg), with falling 10SMA (1.1960) expected to cap upticks and keep bears intact.

Traders focusing on release of US inflation data due later today, which could show acceleration in inflation and further boost the dollar.

Res: 1.1879, 1.1897, 1.1936, 1.1960

Sup: 1.1816, 1.1790, 1.1737, 1.1709

Kiwi Tumbles, BoE Decision And US Inflation In Focus

Here are the latest developments in global markets:

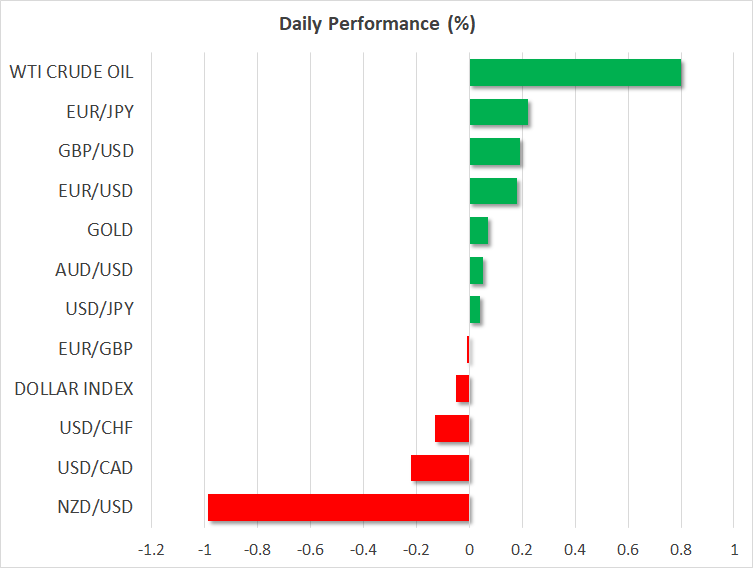

FOREX: The US dollar index was practically flat on Thursday, ahead of the release of the US CPI data for April at 1230 GMT. Kiwi/dollar plunged nearly 1.0% overnight, after the RBNZ kept its policy unchanged but shifted to a more dovish bias, keeping the possibility of a rate cut on the table. Sterling/dollar traded 0.2% higher, as investors awaited the BoE's rate decision today at 1100 GMT.

STOCKS: Wall Street closed higher yesterday, with energy shares leading the way higher amid a surge in oil prices. The Nasdaq Composite climbed by 1.0%, while the S&P 500 and Dow Jones followed in its tracks, rising by 0.97% and 0.75% respectively. Futures tracking the Dow, S&P, and Nasdaq 100 are also pointing to a higher open today. That said, the performance of these indices today may depend to a large extent on the upcoming US CPI data. Most indices in Asia were in the green as well. Japan's Nikkei 225 and Topix indices rose by 0.39% and 0.27% correspondingly, while in Hong Kong, the Hang Seng gained 0.96%. In Europe, futures tracking the major benchmarks were also signaling a higher open today, especially for the UK FTSE 100.

COMMODITIES: Oil prices posted another day of spectacular advances on Wednesday, and continued pushing higher today as well, with WTI and Brent crude climbing by 0.8% and 0.7% respectively. Both benchmarks touched fresh multi-year highs. The US decision to leave the Iran nuclear accord, a surprising drawdown in the EIA weekly crude inventories, and reports of armed conflict between Israel and Iran appear to be the main forces behind oil's latest gains. In precious metals, gold is higher today but by less than 0.1%, recouping some of the losses it posted yesterday. It has been trading in a very narrow range so far this month, between $1,301 and $1,318, largely overlooking reports of rising tensions in the Middle East.

Major movers: Kiwi retreats as RBNZ appears dovish; oil races higher amid geopolitical tensions

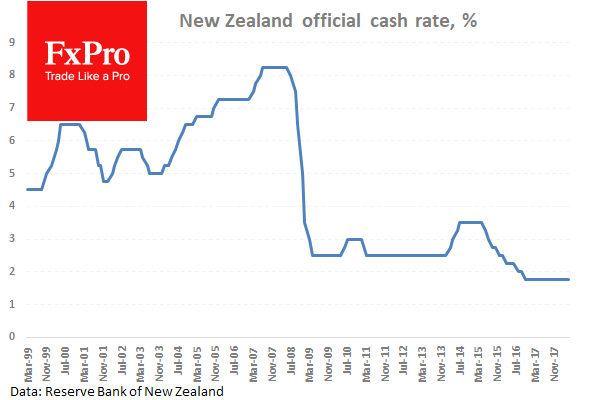

Overnight, kiwi/dollar sank nearly 1.0% after the RBNZ kept its policy unchanged but shifted to a more dovish stance, putting the possibility of a rate cut on the table. In the introductory paragraph of the accompanying statement, the new Governor Adrian Orr noted that “the direction of our next move is equally balanced, up or down. Only time and events will tell”. While the prospect of a rate cut appears quite unlikely, this probably signaled the new RBNZ chief will be even more cautious in raising rates than his predecessor, pushing further back rate-hike expectations.

Oil continued racing higher yesterday, as markets digested the US decision to impose new sanctions on Iran and after a surprising drawdown in the weekly EIA inventory data. The surge in crude also boosted the Canadian dollar, which posted a one-week high against its US counterpart.

Turning to geopolitics, safe-haven assets like gold and the yen paid little attention to overnight reports of hostility between Israel and Iran. The Israeli military carried out strikes against Iranian targets in Syria, after Iranian forces launched a rocket attack on Israeli army bases, Israel said. This marks a direct confrontation between the two states, raising the risk of greater escalation just hours after the US withdrew from the Iran deal. While safe havens didn't react, these reports may have been one of the factors behind oil's rally. Overall, this story is worth watching closely, as any further tensions could carry wider implications for the region's stability and consequently, for oil supply moving forward.

Day ahead: BoE decides; US CPI due; geopolitics still a play

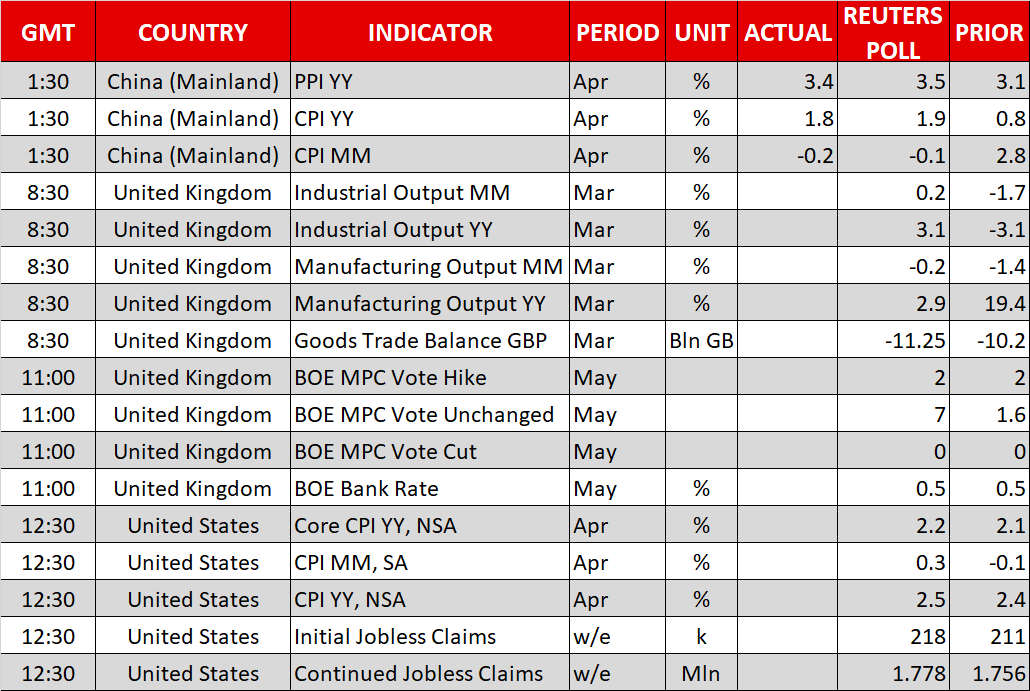

The Bank of England's decision on interest rates and US inflation figures are expected to be the most market-sensitive events out of Thursday's calendar, leading to positioning in FX markets.

At 1100 GMT, the Bank of England's rate decision will be made public, with the meeting minutes and the Bank's Inflation Report also released at the same time. Markets widely expect the central bank to maintain its base rate unchanged. It's communication and the number of Monetary Policy Committee (MPC) members voting for a rate hike though, will determine sterling's movement. Polls suggest a 7-2 vote in favor of rates remaining at current levels. More dissenters (i.e. more MPC members voting for a hike) and signaling of a “hawkish hold” that puts a hike firmly on the table in an upcoming meeting, is anticipated to push sterling higher, and vice versa.

Before the focus turning to the BoE, the UK will be on the receiving end of data on the goods trade balance, industrial output and manufacturing output. All data points are due at 0830 GMT and pertain to the month of March. Manufacturing production is forecast to fall by 0.2% m/m, the same as in February, but grow at a faster pace on an annual basis (2.9% vs 2.5% in February).

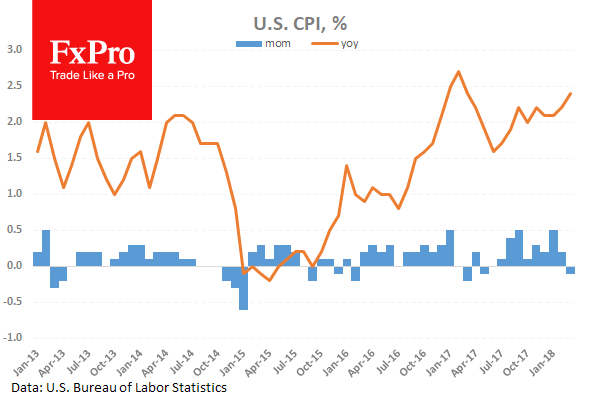

Later (1230 GMT), the attention will shift to the US which will see the release of April inflation figures, as gauged by the consumer price index (CPI). Both headline and core CPI – the latter being the measure that excludes volatile food and energy items – are expected to accelerate on a yearly basis, growing at their fastest pace in more than a year. Specifically, they're projected to expand by 2.5% and 2.2% correspondingly. Monthly headline CPI is also expected to return to positive territory after last month's contraction, which was attributed to transitory factors.

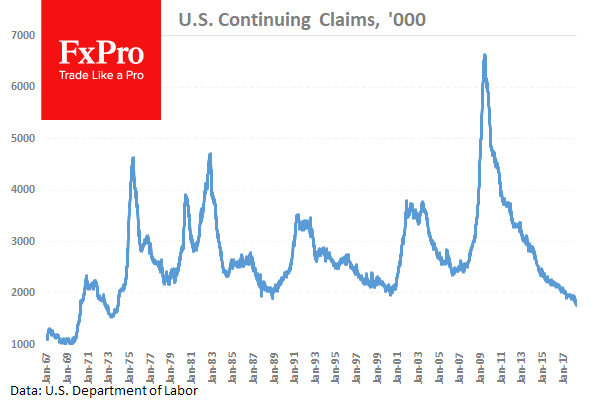

The inflation numbers do not relate to the Fed's preferred inflation gauge – that being the core PCE price index – but still can stoke expectations of a steeper interest rate outlook by the US central bank in case of an upside surprise. According to Fed fund futures, markets have fully priced in two additional hikes by the Fed in 2018, while they assign a more than 20% chance for an additional move as well. Meanwhile, weekly data on initial and continued jobless claims out of the US will be made public at the same time as CPI numbers (1230 GMT).

Nvidia is among companies releasing quarterly earnings on Thursday. The chipmaker's results will be made public after today's closing bell on Wall Street.

Lastly, geopolitical developments are a factor to be looked at, especially after President Trump's decision to pull out of the Iran nuclear deal and a possible regional conflict-escalation, as Syria (Iranian forces within the country) and Israel appear to be carrying out attacks against one another.

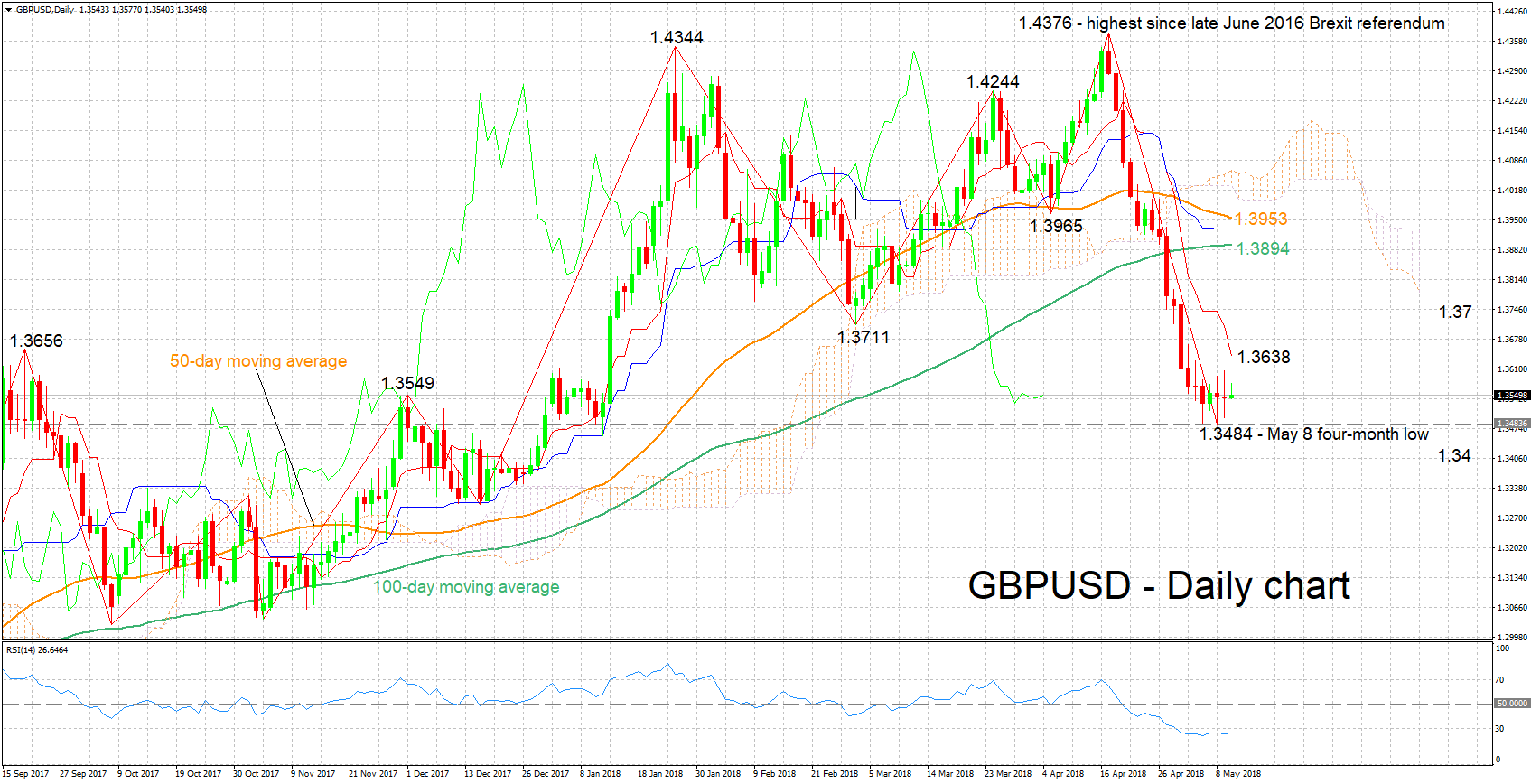

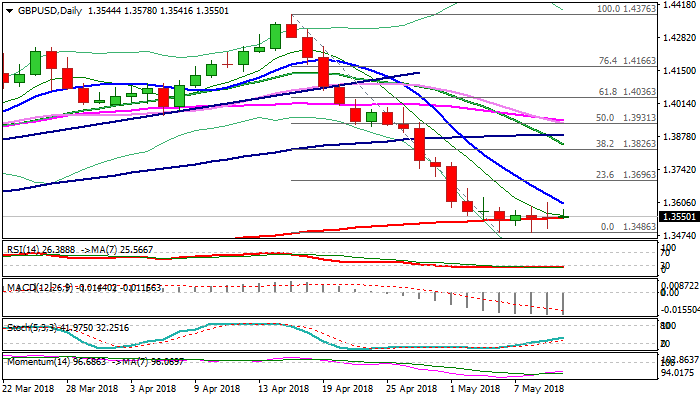

Technical Analysis: GBPUSD short-term bearish; RSI oversold

GBPUSD has contracted considerably after rising to its highest since June 2016 of 1.4376 around mid-April. On Tuesday, it touched a four-month low of 1.3484. The negatively-aligned Tenkan- and Kijun-sen lines are projecting a bearish short-term picture. The Kijun-sen has flatlined though, the implication being that negative momentum is easing. The RSI, which is moving sideways in bearish territory, supports this view as well; notice also that the indicator has entered oversold levels.

A “hawkish hold” by the BoE is anticipated to support the pair, with resistance potentially coming around the current level of the Tenkan-sen at 1.3638 and the 1.37 handle in case of steeper advances.

A dovish tone by the central bank is expected to push GBPUSD lower. Support could emerge around Tuesday's four-month low of 1.3484 and subsequently the 1.34 handle in the event of sharper losses.

US inflation figures are also likely to spur positioning on the pair.

USDJPY Approaches 110.00 Critical Level, 200-Day SMA Acts As Significant Obstacle

USDJPY has posted a strong bullish run during Wednesday’s trading session and is approaching again the three-month high near the 110.00 psychological level. This region overlaps with the 38.2% Fibonacci retracement level of the downleg from 118.60 to 104.60. The technical indicators in the short-term seem to be in agreement with the bullish scenario.

From the technical point of view, the price is ready to touch the 200-day simple moving average (SMA) near 110.20, which is acting as strong resistance in the medium-term, in case of a break of 110.00, while it is developing well above the 20- and 40-SMAs in the short-term. The RSI indicator is sloping slightly up in the positive territory, while the stochastic oscillator is moving higher below its overbought region.

If the price successfully surpasses the 38.2% Fibonacci retracement level and the 200-day SMA, this could reinforce the bullish move and drive the pair until the 110.50 resistance level taken from the peak on January 18. A jump above the aforementioned obstacle could push the price further up towards 111.50, which holds near the 50.0% Fibonacci.

Conversely, in case of a bounce off the 110.00 handle, there is a possibility of bearish movement until the next immediate support of 108.65. If the price continues the downward tendency it could open the way towards the 107.80 – 108.20 significant area, which contains the 23.6% Fibonacci.

As a side note, the pair has been consolidating within a downward sloping channel since December 2016 and touched the lower boundary at the end of March, creating a 16-month low of 104.60.

RBNZ Leaves Rates On Hold And Lowers Inflation Forecasts

The Reserve Bank of New Zealand left rates on hold at 1.75% earlier with a shift to a more dovish position, adding that the direction of the next rate move is very finely balanced. The Bank lowered its inflation forecast and lengthened its inflation target timeframe. It expects CPI at 1.6% by June 2019, revised lower from the previous 1.8%. In the press conference, Governor Orr said that inflation had surprised to the downside for some time and that this was a concern, which was why the bank was keeping monetary policy expansionary. NZDUSD fell from 0.69757 to lows of 0.69087 in response.

In other news, overnight BOJ Governor Kuroda said that the bank will continue its powerful monetary easing and that it is too early to lay out conditions for exiting easy policy. USDJPY moved higher from 109.628 to 109.831.

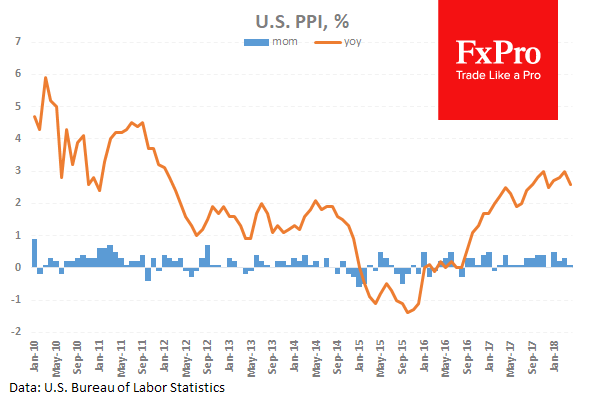

US Producer Price Index Ex-Food and Energy (YoY) (Apr) was 2.3% against an expected 2.4%, from a previous reading of 2.7%. Producer Price Index (MoM) (Apr) was 0.1% against an expected 0.2%, from 0.3% previously. Producer Price Index Ex-Food and Energy (MoM) (Apr) was as expected at, against a previous reading of 0.3%. Producer Price Index (YoY) (Apr) was 2.6% against an expected 2.8%, from 3.0% previously. The monthly readings came in as expected, slightly softer than the previous readings. The yearly readings are showing bigger percentage declines, indicating a fall in consumer inflation. GBPUSD hit a high of 1.36017 before dropping back to 1.35797 following this data release.

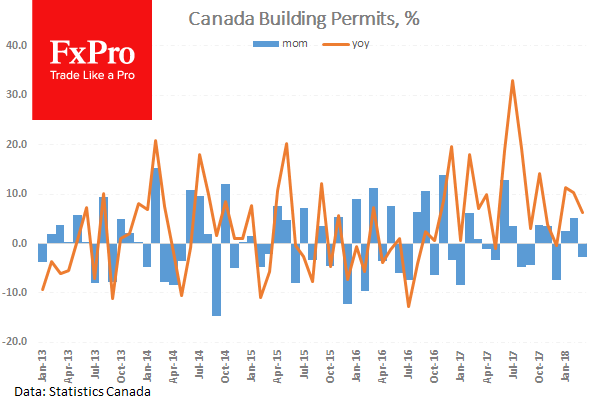

Canadian Building Permits (MoM) (Mar) were 3.1% against an expected 2.0%, from a previous -2.6%, which was revised down to -2.8%. This data exceeded expectations but the metric is showing smaller advances and declines compared with historic standards. USDCAD tested support at 1.28692 before hitting a high of 1.28992 as a result of this data release.

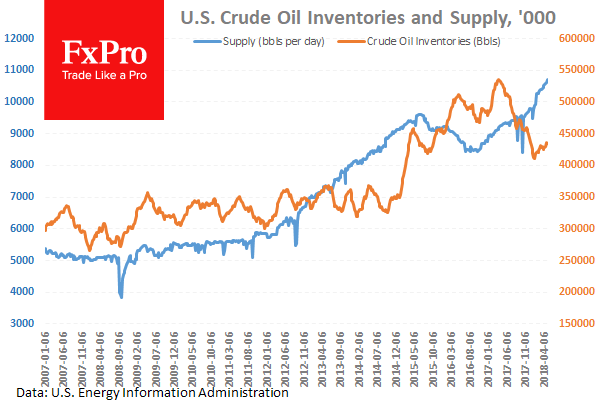

US EIA Crude Oil Stocks change (May 4) data came in at -2.197M against an expected draw of -1.167M, from a build of 6.218M last week. This data surprised to the upside last week, exceeding the expected build of 1.000M, however, this time the draw was bigger than expected. Oil markets are in focus at the moment after the US withdrew from the Iran Deal yesterday and this data release may add further volatility to the mix. WTI spiked to $71.21 before falling to support at $70.60 and rebounding higher.

EURUSD is up 0.08% overnight, trading around 1.18600.

USDJPY is up 0.07% in early session trading at around 109.816.

GBPUSD is up 0.14% this morning, trading around 1.35640.

USDCAD is down -0.12% overnight, currently trading around 1.28369.

Gold is up 0.10% in early morning trading at around $1,313.72.

WTI is up 0.43% this morning, trading around $71.61.

BOE Expected To Keep Rates At 0.5%, US CPI Expected To Increase Moderately

At 08:30 GMT, UK Industrial Production (YoY) (Mar) is expected to be 3.1% against a previous 2.2%. Industrial Production (MoM) (Feb) is expected to be 0.2% against 0.1% previously. Last month this data missed expectations. The reading today is expected to come in higher than last month. Manufacturing Production (YoY) (Mar) is expected to be 2.9% against 2.5% previously. Manufacturing Production (MoM) (Mar) is expected to be unchanged at -0.2%. This figure had been less volatile during much of 2017, with readings staying positive but close to zero. The miss last month follows on from the previous month’s marginal miss and drags data below the zero line. GBP pairs could move because of this data release.

At 11:00 GMT, Bank of England Interest Rate Decision is expected to be left unchanged at 0.5%. The BOE Minutes, BOE Quarterly Inflation Report and the Monetary Policy Statement will be released at the same time. BOE Asset Purchase Facility is expected to come in unchanged at £435B. While no change in rate is expected, the tone and language used will be examined for hints that the Bank is gearing up to increase rates in future. BOE Governor Mark Carney will lead the Press Conference at 11:30 GMT. GBP crosses could see spikes in volatility during this event.

At 12:30 GMT, US Continuing Jobless Claims (Apr 27) is expected to be 1.778M against 1.756M previously. Initial Jobless Claims (May 4) is expected to come in at 218K against 211K previously. This data is showing a continuing increase in the number of people who are jobless. US Consumer Price Index (YoY) (Apr) data will be released with an expected reading of 2.5% against 2.4% previously. Consumer Price Index Ex-Food & Energy (YoY) (Apr) data will be released with an expected reading of 2.2% against 2.1% previously. Consumer Price Index Ex-Food & Energy (MoM) (Apr) is expected to be unchanged at 0.2%. Consumer Price Index (MoM) (Apr) data will be released with an expected reading of 0.3% against -0.1% previously. Consumer Price Index Core s.a. (Apr) data will be released with an expected reading of 256.899 against 256.200 previously. These data points will provide an updated measure of the effect of inflation on consumers. Inflation is one of the main drivers of market sentiment in the US currently. The expectation is for an increase in consumer prices. USD crosses may see an increase in volatility from this data release.

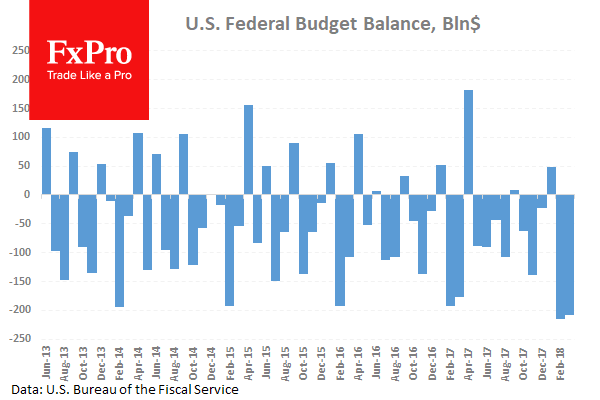

At 18:00 GMT, The US Monthly Budget Statement (Apr) will be released with an expected balance of $193.75B from a previous $-209.00B. This data is expected to show a $400B swing into positive territory, as seasonal factors affect the calculation of this metric. This reading is expected to exceed the high from April 2017 of 182.4B. USD pairs may be moved by this data.

At 22:45 GMT, New Zealand’s PMI (Apr) reading is expected to be released with the previous reading coming in at 52.2. This was a further fall from the February reading of 55.6. NZD crosses could be impacted by this data release.

GBPUSD Holds Within Extended Consolidation Range, Awaiting BoE For Fresh Direction Signal

Cable ticked higher in early European trading on Thursday but remains within four-day range and holds above key support – 200SMA, despite several spikes lower.

Double long-legged Doji in past two days signals strong indecision, which resulted in extended consolidation following steep descend from 1.4376 (2018 high).

Daily techs show mixed signals as MA’s in bearish setup weigh, while momentum and slow stochastic head north.

Basing attempts are evident on daily chart, but the pair was so far unable to break above the upper boundary of near-term consolidation range, reinforced by falling 10SMA (1.3602) and generate initial bullish signal.

Batch of data from the UK is due today, starting with releases of Industrial/Manufacturing Production and trade balance, but all eyes are on BoE’s super Thursday, as the key event for pound today.

The central bank is expected to keep interest rates unchanged, but minutes of the previous meeting are forecasted for a split vote, with focus also on Inflation report and Governor Carney’s speech.

Hawkish tone from BoE would increase expectations for rate hike in August and boost pound, which could result in eventual break above congestion top and spark recovery rally.

Conversely, dovish BoE would sell pound and risk firm break below 200SMA pivot for continuation of downtrend from 1.4376.

Res: 1.3602, 1.3629, 1.3665, 1.3696

Sup: 1.3542, 1.3484, 1.3442, 1.3400

BOE’s Super Thursday In Focus, Ringgit Flattened In Offshore Markets

The story defining the painful depreciation of the British Sterling in recent weeks has been rapidly fading expectations over the Bank of England raising UK interest rates today.

Only one month ago, the markets were predicting a more than 90% probability of a UK interest rate increase this month. Today, this probability has evaporated to less than 15%. A crippling combination of negative economic data, disappointing growth figures and another reversal in tone from BoE Governor Mark Carney has been the driver behind these minimal expectations of a UK interest rate rise today.

With it already being a foregone conclusion that UK interest rates will probably be left unchanged, attention will be directed towards the language of the policy statement and whether there was a split in the MPC vote.

The Sterling still appears oversold and could be thrown a lifeline, if the BoE delivers a “hawkish hold” thatleaves the door open for future rate hikes. Expectations over the central bank possibly taking action in August are likely to heighten, if more than two MPC members vote, or at least signal a desire for higher UK interest rates.

What would be seen as a major threat to the Sterling resuming its horrific downward spiral is if the BoE issues a downbeat policy statement, suggesting a downgrade in UK economic growth, and a potential change in inflation forecasts limits the need to raise UK interest rates. This would likely to spell more pain for the Pound.

Taking a look at the technical picture, the GPUSD is firmly bearish on the daily charts. Previous support around 1.3750could transform into a dynamic resistance that encourages a decline towards 1.3500 and 1.3440, respectively.

Malaysia election shock rocks offshore Ringgit

Malaysian bonds tumbled while the Ringgit received punishment, after the opposition claimed a shocking victory in the nation's general election.Mahathir Mohamad, who will become the world's oldest elected leader at 92 years old,pulled off an unexpected victory on Wednesday, overthrowing Prime Minister Najib Razak's ruling coalition, Barisan Nasional.

International investors are certainly going to be surprised at the election outcome, especially considering that it was not priced in that Najib's ruling coalition would be delivered with such a stunning defeat.

There is likely to be a period of heightened uncertainty in Malaysia following the surprising election results. The Ringgit is going to be at threat to domestic political uncertainty, and the onshore market could find itself vulnerable to downside losses when the market reopens as expected at the beginning of next week.

It will also be interesting to monitor how both international investors and ratings agencies react to the developments in Malaysia. The new leader has promised to abolish a controversial GST tax in Malaysia, and although this would improve sentiment domestically as a result of no more GST being added to items, it does present a risk to reduced government revenues.

Dollar softens ahead of US CPI

The Dollar retreated from 2018 highs on Thursday as investors engaged in a bout of profit-taking ahead of the US inflation report scheduled for release this afternoon.

US Consumer prices are expected to rise 2.5% in April,while core inflation is forecasted to remain unchanged at 2.1%. The argument in favour of higher US interest rates is likely to strengthen if inflation figures exceed market expectations.

Taking a look at the technical picture, the Dollar Index is firmly bullish on the daily charts. Prices are trading above the daily 200 SMA while the MACD has crossed to the upside. With the widening interest rate differential in favour of the Dollar, prices have scope to venture higher and even challenge fresh 2018 highs. A breakout and daily close above 93.20 could encourage an incline higher towards 93.50 and 94.00, respectively.

Emerging market currencies feel the burn

It is shaping up to be a miserable trading week for emerging market currencies, which have fallen victim to an appreciating Dollar and heightened geopolitical risk. With the Dollar poised to appreciate further amid US rate hike expectations and uncertainty denting appetite for risk, most EM currencies could be exposed to further downside risks.

Currency spotlight – EURUSD

The EURUSD tumbled to a fresh 2018 low at 1.1823 on Wednesday, thanks to a strengthening Dollar.

Although the currency pair has recovered some its losses this morning, the outlook remains heavily bearish. Taking a look at the technical picture, there have been consistently lower lows and lower highs on the daily charts. Previous support around 1.1900 could transform into a dynamic resistance that encourages a decline towards 1.1810 and 1.1770, respectively. Alternatively, a breakout above 1.1900 could trigger a technical rebound which pushes prices back towards 1.1970.

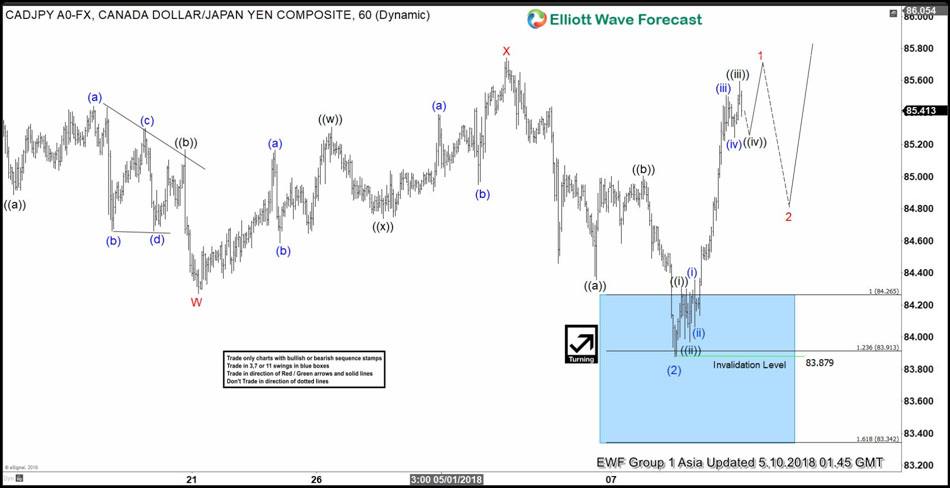

Elliott Wave View: CADJPY Calling Strength Higher

CADJPY Short Term Elliott Wave view suggests that the decline from 4/13 peak at 85.76 to 83.87 low ended Intermediate wave (2) as a double three Elliott Wave structure. The internal subdivision of the decline from 85.76 high shows an overlapping structure. This suggests the decline is corrective in nature. We label the correctin as W-X-Y.

Down from 4/13 peak (85.76), Minor wave W unfolded as a Zigzag Elliott wave structure. Minute wave ((a)) of W ended at 84.88, Minute wave ((b)) of W ended at 85.17 high, and Minute wave ((c)) of W ended at 84.27 low. Up from there, Minor wave X bounce also unfolded as a double three Elliott Wave structure. Minute wave ((w)) of X ended at 85.31, Minute wave ((x)) of X ended at 84.74 and Minute wave ((y)) of X ended at 85.74. The internal of Minor wave Y subdivided as a zigzag structure. Minute wave ((a)) of Y ended at 84.36, Minute wave ((b)) of Y ended at 85, and Minute wave ((c)) of Y ended at 83.87 low. The move lower to 83.87 also ended Intermediate wave (2) upon reaching 100%-123.6% Fibonacci extension area of Minor W-X at 83.91 – 84.26.

Above from there, the pair has made a strong rally to the upside in an impulse Elliott Wave structure. Due to the 5 waves impulse, it favors the continuation higher in Intermediate wave (3). However, a break above 4/13 high 85.75 is needed for the final confirmation of the next leg higher. Until then, a double correction lower in intermediate wave (2) still can’t be ruled out. Near-term, as far as dips remain above 83.87 low, expect pair to resume higher. We don’t like selling it.

CADJPY Elliott Wave 1 hour Chart

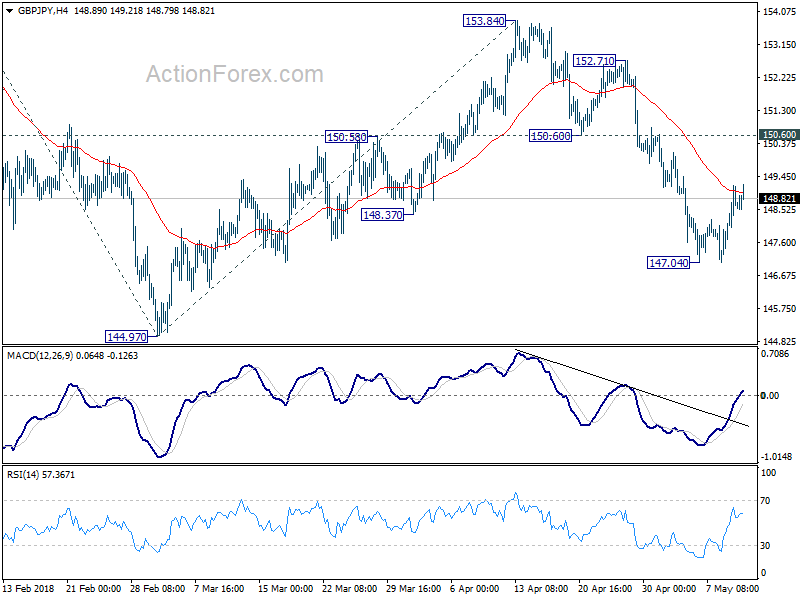

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.82; (P) 148.51; (R1) 149.32; More...

GBP/JPY's consolidation from 147.04 is still in progress and intraday bias remains neutral. While further rise cannot be ruled out, upside should be limited below 150.60 support turned resistance to bring another decline. Below 147.04 will target 144.97 first. Break there will resume the fall from 156.59 and target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next.

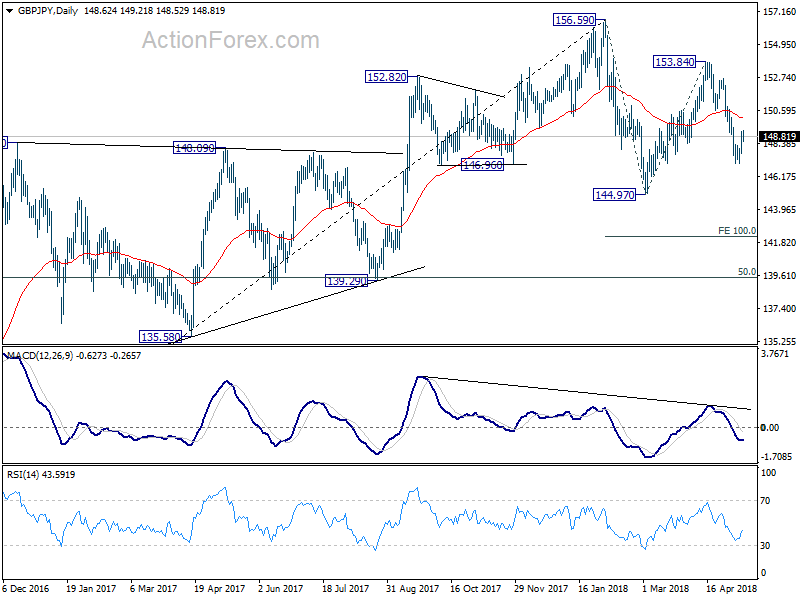

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

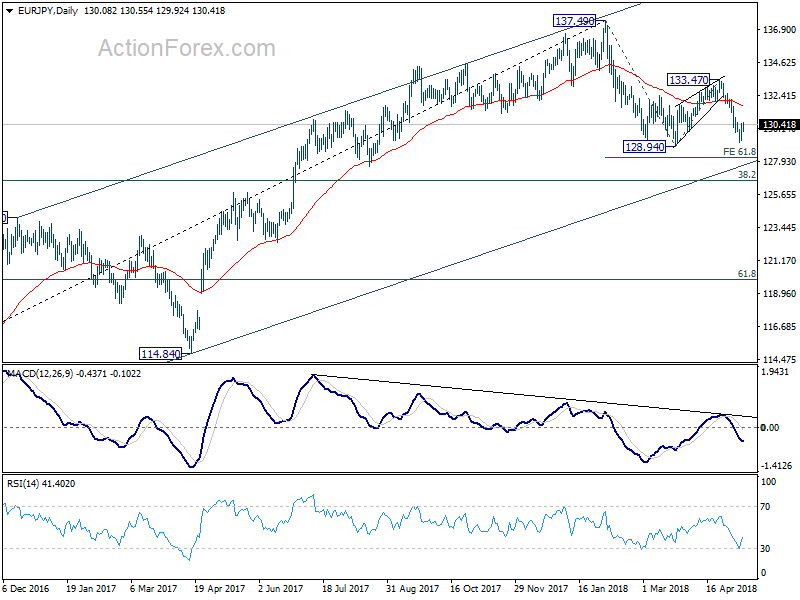

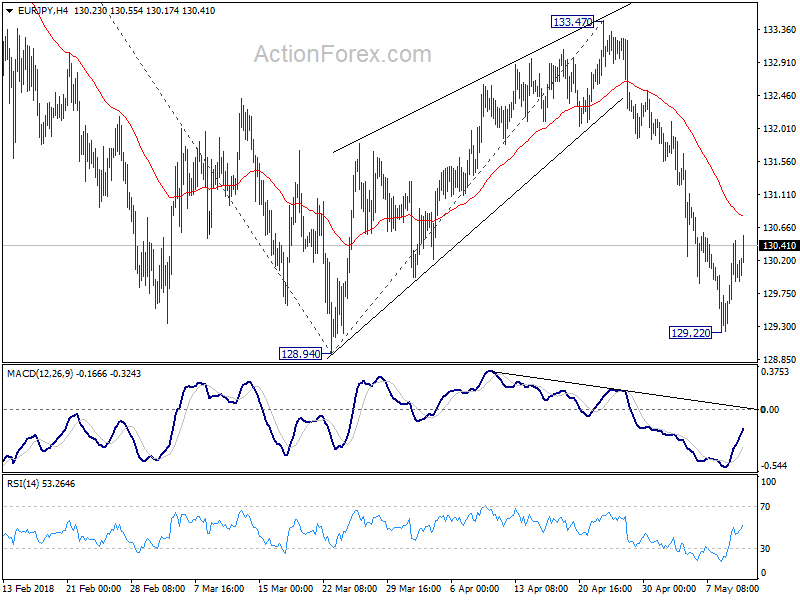

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.43; (P) 129.96; (R1) 130.57; More....

Intraday bias in EUR/JPY stays neutral for consolidation above 129.22. As long as 4 hour 55 EMA holds (now at 130.81). the consolidation should be relatively brief. Below 129.22 will target 128.94 support. Break will resume whole decline from 137.49 and target 61.8% projection of 137.49 to 128.94 from 133.47 at 128.18 next. Overall, near term outlook will stay bearish as long as 133.47 resistance holds and downside breakout is expected eventually.

In the bigger picture, for now, price actions from 137.49 are viewed as a corrective pattern only. Hence, while, deeper decline would be seen, strong support is expected at 38.2% retracement of 109.03 to 137.49 at 126.61 to contain downside and bring rebound. Up trend from 109.03 (2016 low) is expected to resume afterwards. Though, sustained break of 126.61 will be an important sign of trend reversal and will turn focus to 124.08 resistance turned support.