Sample Category Title

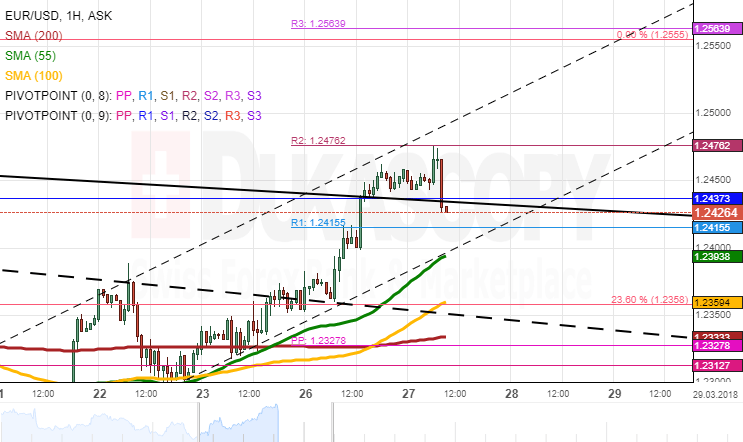

EUR/USD Analysis: Breaches Medium-Term Pattern

Despite receding fears of trade wars, the US Dollar failed to pick up momentum on Monday, thus allowing EUR/USD to breach the psychological 1.24 level and reach a new six-week high of 1.2450.

The rate managed to breach the monthly R1 and a medium-term channel along the way. Further advance, however, did not follow, as the pair remained located slightly below the weekly R2.

From technical point of view, the last few trading sessions show that the Euro has initiated a new wave up after reversing from the senior channel on March 20. This suggests that the Euro could continue climbing even further this week. However, bulls might allow for a slight correction south down to the 1.24 area today.

In case bulls continue to dominate, upside target is 1.2550 which has provided strong support beforehand.

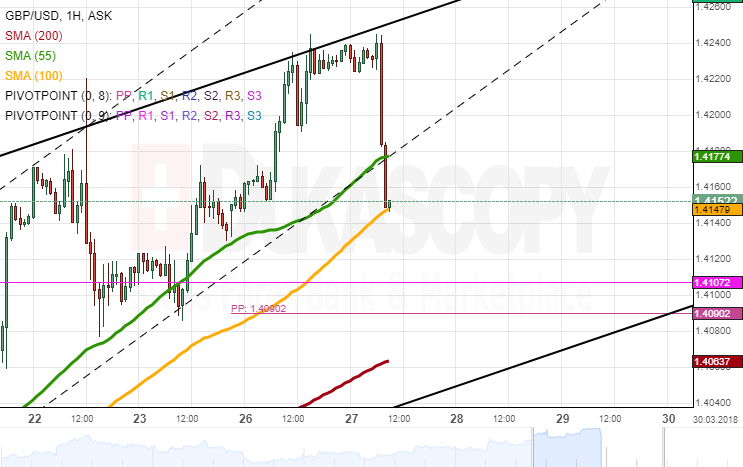

GBP/USD Analysis: Calm On Tuesday Morning

The inability of the US Dollar to gain momentum on Monday had positive impact on the GBP/USD exchange rate. The morning and evening sessions did not introduce significant changes to the overall price level, while mid-day was dominated by bulls.

The pair remains bullish for this week, and it seems that traders might target the 2017/2018 high of 1.4313. In case this level is breached, the current surge is expected to continue. This move is unlikely to day, as bulls still need to gather the necessary momentum to do so.

Given that technical indicators are gradually moving away from the overbought area might suggest either consolidation or a minor decline today.

In case no fundamentals erase this assumption, this movement south should not exceed the 55– and 100-hour SMAs near 1.4150.

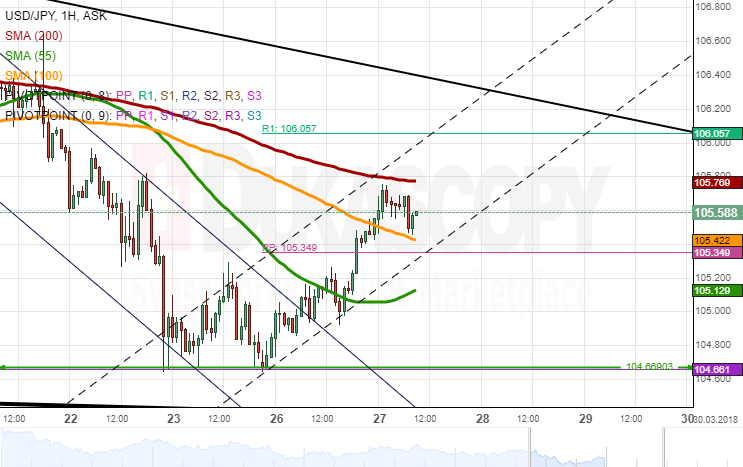

USD/JPY Analysis: Moves Away From Yearly Low

After reaching a new 2017/2018 low of 104.67 late on Friday, the US Dollar picked up momentum and had therefore shot up to 105.80 by Tuesday morning..

This rapid change in sentiment was due to investors re-gaining confidence in global markets and thus relocating their funds from safe-haven currencies, including the Japanese Yen. The Greenback dashed through the 55– and 100-hour SMAs and the weekly PP during the previous session and, at the time of this analysis, was testing the 200-hour moving average. This line is located near the weekly R1 and the prevailing trend-line circa 106.00.

It is likely that bulls do not have sufficient strength to overcame this resistance after yesterday's surge, thus allowing for a minor decline today. A possible downside target is the 55-hour SMA at 105.00.

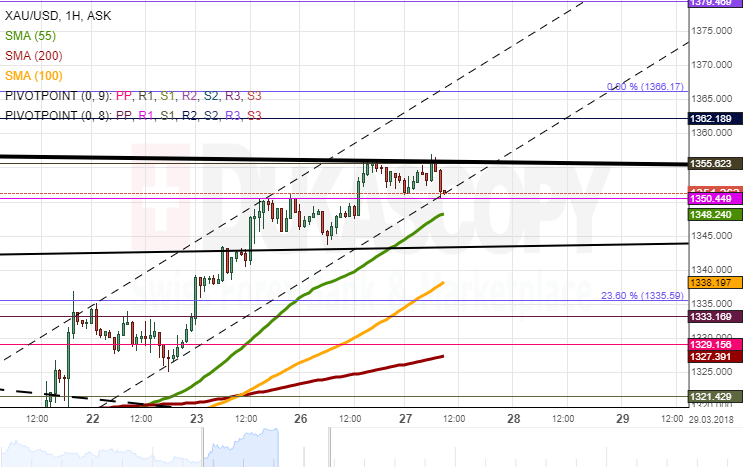

XAU/USD Analysis: Tests Senior Channel

Gold continues to appreciate against the US Dollar for the sixth consecutive session. Despite a few hours of consolidation on Monday morning, the yellow metal managed to gather momentum and push towards the 1,355.00 mark mid-session.

Further climb did not follow, as it was restricted by the monthly R1 and the senior channel. As a result, the pair failed to reach the upper boundary of the junior formation near 1,360.00.

Even though technical indicators are still flashing bullish signals, they are gradually moving away from the overbought territory. Thus, some bearish pressure could prevail in the market today.

This scenario would be confirmed by a breakout of the 55-hour SMA and the junior channel. A possible trading range for today is the 1,345.00/1.360.00 area.

Abating US-China Trade Tensions Boost Sentiment With Equities Rising And Yen Falling

Here are the latest developments in global markets:

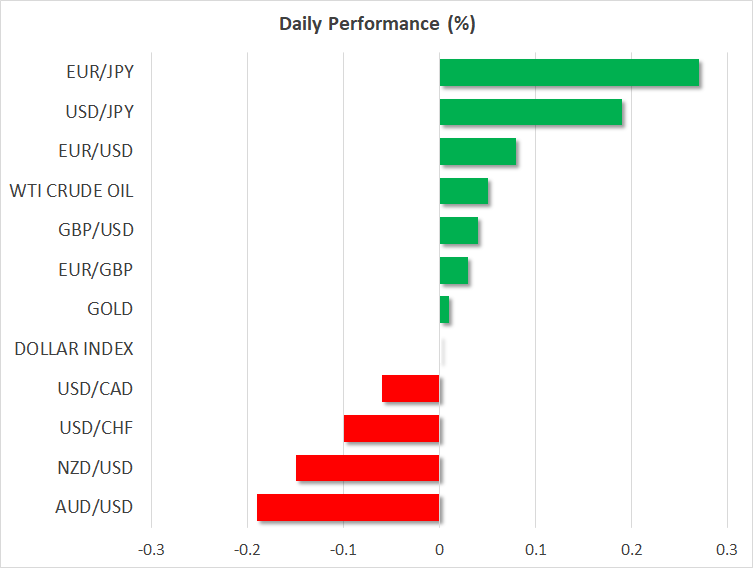

FOREX: The dollar was not much changed against a basket of currencies on Tuesday, consolidating its losses from yesterday that saw it lose 0.5%, recording a more than one-month low along the way. Elsewhere, the yen was extending its losses from yesterday on the back of risk appetite returning to the markets.

STOCKS: US markets staged a spectacular comeback yesterday, as headlines of progress being made in US-China trade talks helped to diminish concerns of an imminent trade war and revive risk appetite. The Nasdaq Composite led the recovery, gaining a whooping 3.3%, while the Dow Jones and S&P 500 followed closely in its tracks, climbing by 2.8% and 2.7% respectively; the Dow recorded its third-biggest point gain in its history on Monday. This positive shift in sentiment looks set to continue today, as futures tracking the Dow, S&P and Nasdaq 100 are all currently pointing to a higher open. Asia was a sea of green today as well, with Japan's Nikkei 225 and Topix surging by 2.65% and 2.75% correspondingly. In Hong Kong, the Hang Seng was 0.8% higher. Demand for riskier assets seems to have returned to Europe as well, with futures tracking all the major benchmarks currently flashing green.

COMMODITIES: Oil prices are marginally higher today, with both WTI crude and Brent being up by roughly 0.1%. The main theme driving the oil market appears to be speculation around new sanctions being imposed on Iran soon, which would remove a significant chunk of oil supply from the market. Besides any news on Iran, oil prices will also remain sensitive to changes in risk appetite, any major movements in the dollar, as well as the weekly API crude inventory data due out later today. In precious metals, gold prices surged yesterday, breaking above the $1350 resistance hurdle to currently trade at $1355, even despite the risk-on market environment. The safe haven's gains are probably owed to the decline in the US dollar. Since gold is denominated in dollars, it tends to benefit when the greenback depreciates as investors using foreign currencies find it cheaper to buy the yellow metal.

Major movers: Dollar consolidates losses while yen continues declining as positive risk sentiment makes a comeback

The dollar's index against a basket of currencies was close to flat, trading not far above 88.98, its lowest since February 19 recorded yesterday. Majors including the euro and sterling posted notable gains versus the greenback on Monday and today they were consolidating those gains. At 0630 GMT, euro/dollar and pound/dollar were trading within breathing distance of yesterday's near six-week and near eight-week highs of 1.2462 and 1.4244 respectively.

China and the United States appearing willing to enter into discussions on trade, deviating from the inflammatory rhetoric of recent days, acted as a major boost to risk sentiment, supporting equities and diverting funds out of traditional safe-havens such as the Japanese currency. The dollar, euro and sterling were all building on yesterday's advances versus the yen, with their gains ranging from 0.2-0.3%. Dollar/yen was at 105.60, around a yen above Monday's 16-month low for the pair, while pound/yen was trading close to a one-month high of 150.42 recorded earlier in the day. It is notable that euro/yen added an impressive 1.4% on Monday, for the common currency to post its best daily performance versus the yen since June 2017.

The euro was broadly higher yesterday, in part being helped by remarks from Jens Weidmann, the Bundesbank's president and Germany's likely candidate to replace Mario Draghi as the European Central Bank's next chair in late 2019. Weidmann said market expectations of an ECB interest rate increase towards mid-2019 were “not completely unrealistic”. While these comments were not new, the repetition may have added some further credibility to that prospect.

Elsewhere, the yen did not react much to the testimony of the former Japanese tax agency chief before parliament; the former official's comments did not implicate PM Shinzo Abe or anybody from his environment in the land scandal that has been troubling his administration in recent weeks.

Interestingly, the commodity-linked aussie and the kiwi which tend to gain on rising risk appetite were losing ground versus their US counterpart, having advanced the previous day though. Still, the two currencies were gaining versus the yen.

In emerging markets, dollar/yuan was 0.2% lower, having earlier hit a two-and-a-half-year low of 6.2352 on the back of a firmer exchange rate fix by the PBOC. The South Korean won was also a major winner versus other currencies, gaining on reports that North Korea's Kim Jong Un was planning a visit to Beijing, this marking his first known trip outside North Korea since leading the country in 2011.

Day ahead: Second-tier indicators on the agenda, trade developments still in focus

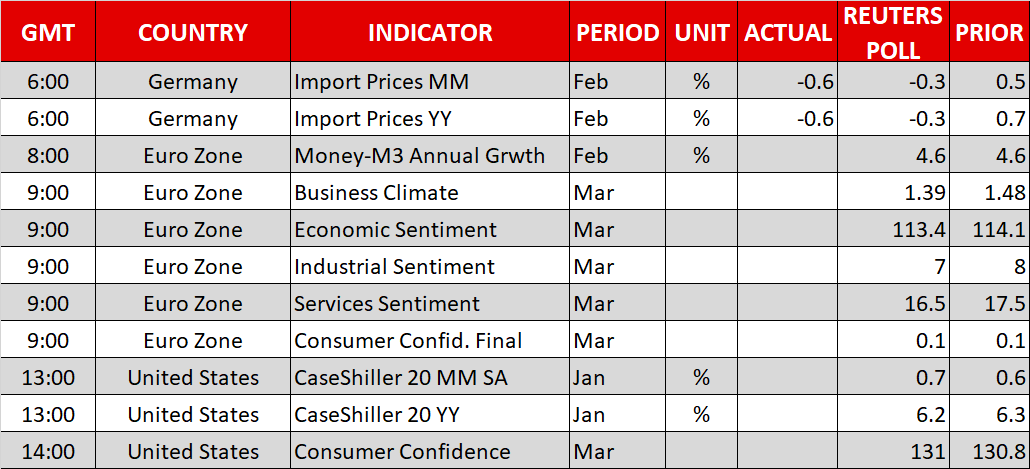

The economic calendar is filled with second-tier economic data releases today out of the eurozone and the US.

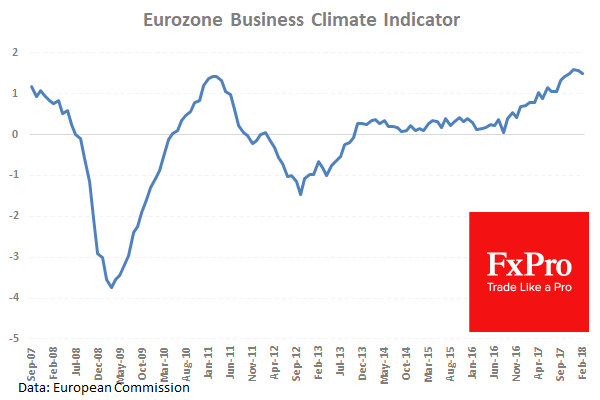

In the euro area, the most noteworthy indicator will be the economic sentiment index for March, due out at 0900 GMT. The index is anticipated to tumble to 113.4 from 114.1 in the previous month, in line with similar declines in other gauges of economic activity and sentiment, like the Markit PMIs and the ZEW survey. While this is usually not a major market mover, such a pullback would be yet another sign that the eurozone's growth momentum may be losing steam. The bloc's M3 money supply growth for February is also due for release at 0800 GMT.

In the UK, the BoE's Financial Policy Committee minutes from the March meeting are due out at 0830 GMT.

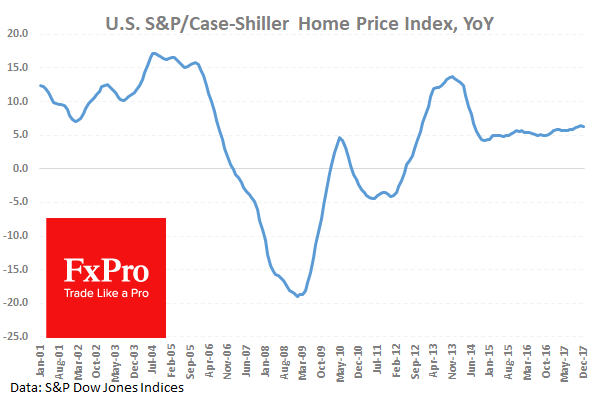

Over in the US, the main publications will be the S&P/Case-Shiller house price index for January and the Conference Board consumer confidence print for March. House prices in 20 of the largest US cities are expected to have risen at a slightly slower pace in yearly terms. Meanwhile, consumer optimism is expected to have ticked up again, which would mark a fresh high last seen in 2000 for the index, painting a rosier picture for American consumption.

In energy markets, the private API weekly crude inventory data will be in focus at 2030 GMT. More broadly, the prospect of new sanctions on Iran will probably remain a key driver for the oil market. Such expectations have largely been fueled by the visit of the Saudi Crown Prince to the US, as well as the replacement of several moderate figures in the Trump administration with Iran-hawks.

Equity markets will likely continue to focus on the possibility of a trade war, which is currently seen as becoming less likely amid signs of progress in talks. Nonetheless, risk sentiment remains very fragile despite the latest recovery, and price action is likely to remain very much headline-driven.

In terms of policymakers' appearances, we have two on the schedule. ECB Governing Council member Erkki Liikanen will deliver remarks at 0800 GMT, while Atlanta Fed President Raphael Bostic (voter) is due to speak at 1500 GMT.

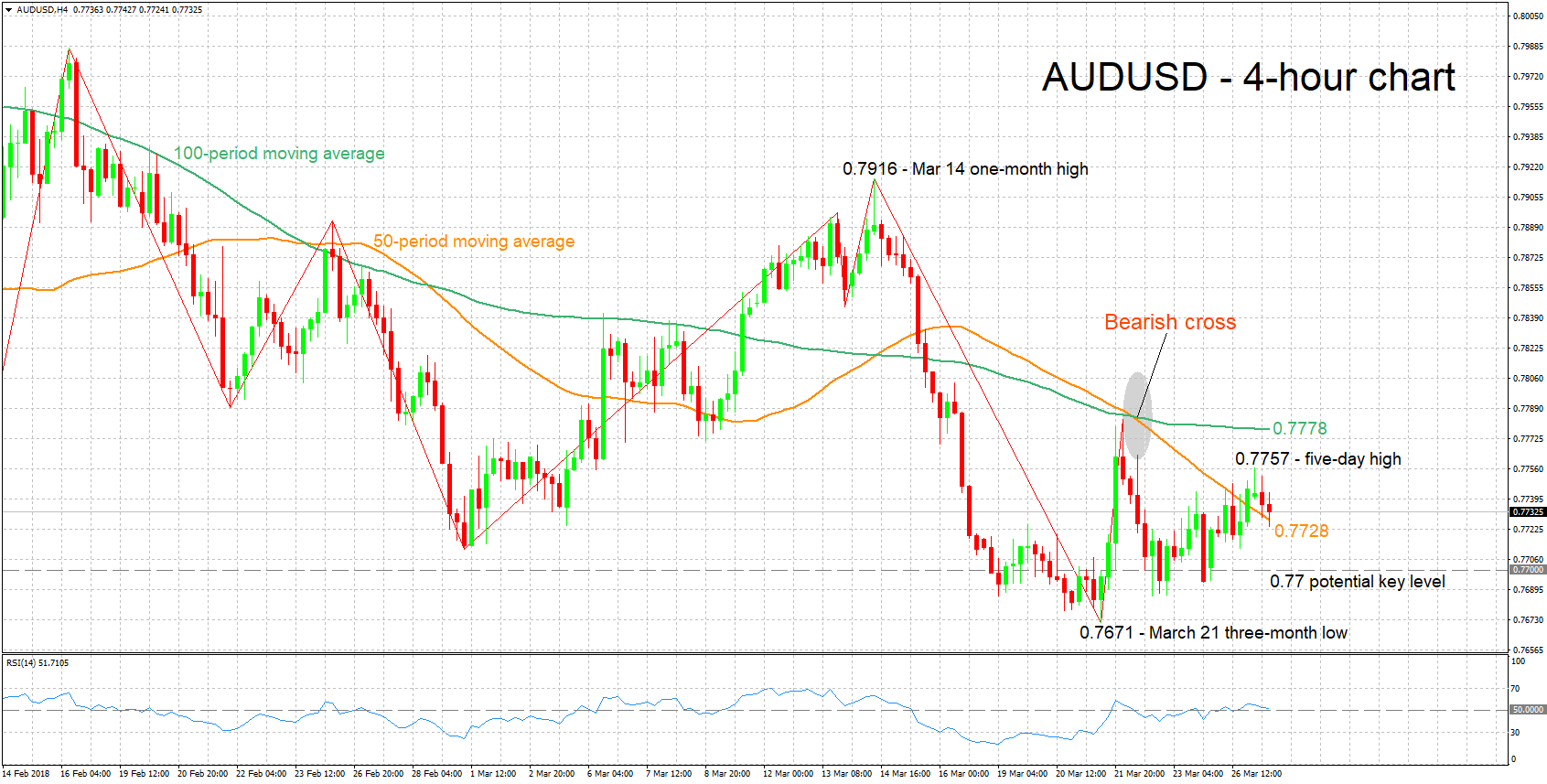

Technical Analysis: AUDUSD looking neutral in the short-term

AUDUSD recorded a five-day high of 0.7757 earlier on Tuesday but it has since retreated from that level. The pair has in large part been moving sideways over the last few trading days, with the RSI which is hovering around the 50 neutral-perceived level pointing to the absence of momentum in either direction in the short-term. Australia's economy heavily relies on commodity exports and its currency tends to benefit on upbeat views on global trade and the global economy; the implication being that the country's economy stands to gain from higher exports.

An escalation of trade tensions that consequently weigh on positive views on global growth could hurt AUDUSD. Support to declines might come around the current level of the 50-period moving average at 0.7728, with steeper declines turning the focus to the 0.77 round figure; the area around this handle was one of congestion recently. Further below, additional support could come around the three-month low of 0.7671 from March 21.

Conversely, should concerns over global trade ease further and boost risk appetite, then AUDUSD is likely to be supported. Resistance to advances could take place around the 100-day MA at 0.7778, given that price action first clears the five-day high of 0.7757 posted earlier in the day.

European Commission: Economic sentiment weakend in all the five largest euro-area economies

Eurozone confidence indciators generally deteriorated in March.

The European commission noted in the release:

The European commission noted in the release:

Euro area developments

In March, the Economic Sentiment Indicator (ESI) decreased markedly in both the euro area (by 1.6 points to 112.6) and the EU (by 1.9 points to 112.5).1 While this is the third consecutive drop, the indicators remain at elevated levels.

The deterioration of euro-area sentiment resulted from drops in industry, services and retail trade. Confidence among consumers remained unchanged, while it increased among construction managers. The ESI weakened in all the five largest euro-area economies; significantly so in Germany (-2.4), Italy (-1.8) and Spain (-1.2) and, less so, in the Netherlands (-0.5) and France (-0.4).

EU developments

The marginally stronger decrease of the headline indicator for the EU (-1.9) was mainly due to the marked deterioration of sentiment in the largest non-euro area EU economies, the UK (-4.2), and Poland (-2.0). In line with the euro area, confidence deteriorated strongly in industry, services, and retail trade, while it increased slightly in the construction sector and remained unchanged among consumers. The fall in EU confidence in the financial services sector was slightly less pronounced than in the euro area.

By contrast to the euro area, EU managers' employment expectations improved in retail trade, while they remained broadly stable in services. Price expectations differed from the euro area mainly in retail trade, where they decreased markedly.

Forex Analysis: US Equity Markets Recover, USD Underperforms, Russian Diplomats Expelled And Kim Jong Un Visits Beijing

Lately, market participants are not just focusing on the scheduled Economic Data releases and reports. The current ongoing global volatility in equities and the forex market is also being influenced by geopolitical reports and events. The main driver for the recent US equity indices recovery was the reduction in trade war concerns that initially caused last week’s market sell-off, with a softer response from China underpinning market recovery. According to media sources, White House advisor, Peter Navaro, said that the Trump administration is actively involved in talks with China to find a suitable resolution to trade tensions.

From the geopolitical aspect, markets are paying close attention to ongoing developments relating to recent events. In a joint move from NATO and Europe, more than 100 Russian diplomats were expelled as a show of solidarity for the U.K attack. Elsewhere, according to some media sources, Kim Jong Un made a surprise visit to Beijing on his first known trip outside North Korea, ahead of a proposed meeting with US president Trump.

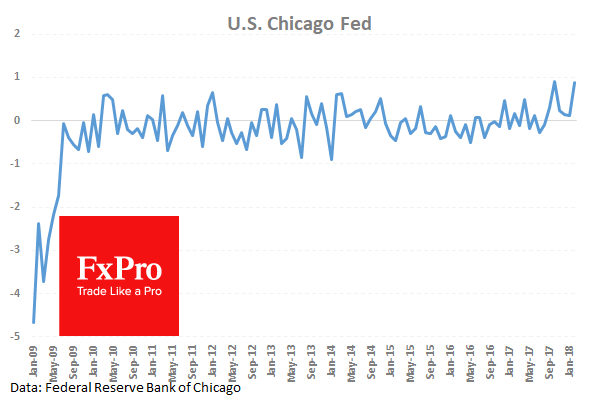

The US Chicago Fed National Activity Index (Feb) was published yesterday and came in at 0.88, significantly better than the market consensus of 0.19, against the previous 0.12. This number picked up as expected, after falling for the last two months. USD and US Equity traders were closely watching this data release.

The Dow Jones Industrial index closed the day up 2.84% at 24212, while the S&P 500 managed to close the day 2.72% higher at 2659 and the Technology Index Nasdaq 100 closed 3.26% higher at 6759 level.

The Fed's Loretta Mester, President of the Federal Reserve Bank of Cleveland, spoke last night on monetary policy at Princeton University. During her speech she stated that she sees rising US rates in 2018 and 2019, however, she also felt that the tariffs are increasing uncertainty. She said that gradual pace conveys that the Fed is not hiking rates at every meeting, however, the Fed has the ability to increase rates as needed. Also, she did not see a lot of financial market imbalances out there. She felt that the US must get back to a sustainable fiscal situation because rising debt raises economic uncertainty. USD Index futures did not react significantly to her statements and appeared bearish, trading around current lows at the 88.60 level.

- EURUSD is up overnight, trading around 1.2446.

- USDJPY is up in early session trading at around 105.60.

- GBPUSD is up this morning, trading around 1.4230.

- USDCAD is down in early trade at around 1.2830.

- Gold is down in early morning trading at around $1,353.

- WTI is higher this morning, trading around $65.60.

European Business Climate, S&P/Case-Shiller Home Price Indices & API Weekly Crude Oil Stocks

At 10:00 GMT, Business Climate (Mar), released by the European Commission, is based on monthly surveys and is designed to deliver a clear and timely assessment of the cyclical situation within the euro area. It may be interpreted as a survey result: a high reading indicates that, overall, the surveys point to a healthy cyclical situation. Conversely, a low reading points to an adverse business climate. A rise in the indicator will point to an upswing in activity and an improvement in the business climate. Alternatively, a fall will point to a deterioration in the business climate. Its movement is clearly linked to the industrial production of the euro area and, as such, it significantly impacts volatility in European Equities and also EUR FX crosses. Market consensus for today’s figure is for a reading of 1.40, from 1.48 previously.

At 14:00 GMT, S&P/Case-Shiller Home Price Indices (YoY) (Jan), released by Standard & Poor, examines changes in the value of the residential real estate market in 20 regions across the US. This report serves as an indicator for the health of the US housing market. Generally speaking, a high reading is seen as positive or bullish for the USD, while a low reading is seen as negative, or bearish. Market expectations for today’s YoY figure for January is for a reading of 6.2%, from a previous value of 6.3%. Significant divergence from the expected number could likely increase volatility in US Dollar FX Crosses and possibly impact US Equities as well.

At 21:30 GMT, API Weekly Crude Oil Stocks are due to be released. API’s Weekly Statistical Bulletin (WSB) reports total U.S. and regional data relating to refinery operations and the production of the four major petroleum products: motor gasoline, kerosene jet fuel, distillate and residual fuel oil. These products represent more than 85% of the total petroleum industry. Published numbers normally impact volatility in WTI Crude futures and are closely watched by energy commodities traders. If the published number varies significantly from the expectations and forecasts then traders use it as a forecasting mechanism for the EIA Crude Oil weekly inventories report, which normally gets published a day later. Previously published API Stocks showed a drawdown of -2.739M barrels, which supported a bullish reaction in WTI Crude futures.

Equity Markets Roar Back | Bitcoin Falls Below 8K

Dow index posted its best day since August 2015

China is still seeking compensation from the US

Twitter joined this trend to ban cryptocurrency advertisements

The bulls returned to the market with vengeance as the Dow index posted its best day since August 2015 - with more than 700 points of gain. There is nothing surprising. When the equity markets fall thick and fast, a small correction usually takes place. The relief rally for the equity markets is global as traders have less concern about the trade war between the US and China. China is keeping its pledge to keep its market open to foreign companies - at least for now.

The US is still keeping the upper hand in the recent developments and has asked China to lower tariffs on US cars and to open their market for US financial services. Meanwhile, China is still seeking compensation from the US for the loss of trade, which occurred on the back of Trump's tariff imposition on Aluminium and Steel.

The situation is still very sensitive and we do think that the relief rally in the equity market is purely due to the heavy sell-off. It is more of a dead cat bounce than anything else; if the underlying fundamentals aren't addressed, we could see the sell triggered again. It would be more than likely that we would break this year's low.

But for now, investors have reacted positively to the surprise visit of North Korea's leader Kim Jong Un to China. This is his first trip outside his country since he became the leader of his country. Traders are considering this event as a further evidence of de-escalation of tensions in the Asia region.

The Last Straw

Advertisement bans have haunted crypto-markets for some time. First, Google banned all the crypto advertisements, with Facebook closely following. Now, Twitter joined this trend as well. Of course, the initial reaction is supposed to be adverse for the cryptocurrencies: Bitcoin dropped below the 8000 mark today. However, the move to the downside wasn't intense, it was more of a gradual move. There is no doubt that we are way oversold when you look at the price curve for Bitcoin or any other major cryptocurrency and a corrective move is strongly on the card. The reality is that all the negative news in the cryptocurrency space has started to have less impact, it appears that the industry has become immune to this kind of developments. Most of the investors that we are talking to, they only want to buy at current price.

ECB Liikanen assures no abrupt sudden changes when QE ends

ECB Governing Council member Erkki Liikanen spoke on monetary policy today:

- "We have been careful in our communication," and "we said we're extending net asset purchases until September and beyond if needed."

- "And our monetary policy is and will be data dependent. So we must follow fresh incoming data every time,"

- "A gradual tightening of monetary policy will rest on a more solid basis when indications of inflation rates to potentially temporarily exceed two percent become more prominent in inflation expectations,"

- "The euro area inflation rate is sustainable when the ECB's price stability objective can be met even without an exceptionally accommodative monetary policy,"

- " If the economy will be stronger and more convergence will take place, the role of the net asset purchase program will be smaller. And at the same time the other three elements will gain more importance especially forward guidance."

- But, "there will be no abrupt sudden changes even if one day the net purchases will be finished."

- "Downside risk is mainly political. We must follow that attentively,"