Sample Category Title

Currencies: USD Hardly Profits From Improved Risk Sentiment

- Rates: No strong trading themes

Core bonds held rather strong despite yesterday's significant improvement in risk sentiment. US Treasuries still underperformed German Bunds ahead this week's first auction, which eventually went well. We expect technical-driven trading today, but the topside should be capped if risk sentiment doesn't deteriorate again. - Currencies: USD hardly profits from improved risk sentiment

Trade tensions eased yesterday. Last week's negative risk sentiment was a negative rather than a positive for the dollar. However, for now, there is no symmetrical positive USD reaction as risk sentiment improves. USD/JPY gains modestly. At the same time; EUR/USD is drifting higher in the 1.2155/1.2555 consolidation pattern

The Sunrise Headlines

- US stocks posted a very strong daily gain (+3%), rebounding after last week's trade war-related weakness. Asian stock markets gain up to 1% with Japan outperforming (+2.25%).

- Top Trump administration officials are asking China to cut tariffs on imported cars, allow foreign majority ownership of financial services firms and buy more US-made semiconductors in negotiations to avoid plans to slap tariffs on a host of Chinese goods and a potential trade war.

- Chinese industrial profits picked up pace in the first two months of the year from December but still lagged 2017 growth, backing expectations that the economy is set to cool as Beijing clamps down on debt risks.

- Washington-based Fed governor Quarles said that the economy is performing well and unemployment is low. Cleveland Fed Mester said that the US central bank will be striking the right balance if it continues a gradual pace of rate hikes.

- EU and Turkish leaders held a tense summit, as friction overt the Turkish president's human-rights record and concern over new military intervention in Syria eroded remaining hopes of the country's accession to the EU.

- A reshuffled Slovak government led by Peter Pellegrini won a parliamentary confidence vote, a month after the murder of an investigative journalist sparked mass protests and forced long-serving leader Robert Fico to resign

- Today's eco calendar contains EMU M3 money data, EC economic confidence, US housing prices and consumer confidence. The US continues its refinancing operation while Fed Bostic and ECB Nowotny speak

Currencies: USD Hardly Profits From Improved Risk Sentiment

Dollar hardly profits from easing trade tensions

Global risk sentiment improved yesterday on signs that the US tried to solve issues with its trading partners (including China) via negotiations. (US) Equities rebounded after Friday's sell-off. Trade tensions were a negative rather than a positive for the dollar last week, but the price pattern wasn't really symmetrical as tensions eased. USD/JPY rebounded north of 105 and closed the day at 105.41. However; the dollar lost further ground against most other majors. EUR/USD trended higher throughout the day and close at 1.2444.

Asian equities join the risk rebound from WS overnight. There is little concrete news. Markets are just growing more confident as the ‘provocation/retaliation phase' in the trade dispute apparently moved to negotiations on specific topics. FX/USD trading is in line with yesterday. USD/JPY profits modestly from the improved risk sentiment. USD/JPY filled offers in the 105.75 area. At the same time, the euro is holding strong against the dollar (EUR/USD 1.2450 currently).

The eco calendar is moderately interesting today with EMU money supply data and the EC confidence data. In the US, house price data, the Richmond Fed manufacturing index and consumer confidence will be published. EC confidence data are expected to ease in line with recent other survey evidence. A modest setback won't change expectations on ECB policy. US consumer confidence is expected to hold near the cycle high. We keep an eye at the price measures of the report. CB speakers (Nowotny/Bostic) remain a wildcard. Yesterday's price action showed that a positive risk sentiment and cautiously higher yields are not enough to trigger a meaningful USD rally. The dollar needs outright positive news, especially on prices. That news isn't available at this stage. The dollar remains vulnerable in this context. We keep a close eye on the ST dynamics in EUR/JPY to assess the fate of EUR/USD. For now a test of the topside of the 1.2155/1.2555 range looks more likely than a downside test. We see no need for a (topside) break.

Sterling trading mostly followed the overall trades in the euro and the dollar yesterday. There was little UK specific news. There are no UK eco data today. We expect more order-driven, technical price action in the lower part of the EUR/GBP 0.8652-68/0.8950 trading range

DXY (USD trade-weighted): USD struggles to prevent further losses even as trade tensions ease

Risk On/Risk Off

Shifts from extreme pessimism to wild optimism aredriving markets today. Last week, U.S. stocks had their worst performance since January 2016 while on Monday, the S&P 500 posted its biggest one-day jump since August 2015. With President Trump's negotiation style, expect to see more of such action. Like traders, he uses a leveraged approach when making deals. When Trump's administration first announced tariffs on U.S. imports of steel and aluminum markets had a similar reaction, but fears of a trade war eased when he later exempted the biggest importers to the U.S. including Canada, Mexico, the EU and later, South Korea. The same scenario now seems in play for China. The original plan was to impose tariffs of up to $60 billion on Chinese imports. Now urgent negotiations have opened, I won't be surprised if it ends up with better trade deals between the world's two biggest economies.

Investors should get used to President Trump talking big to make the business news headlines, only to follow up with much less radical action. Since he took office, the administration has been shaken by many high-profile departures- fiveof whom were fired - but the one “key advisor” he cannot fire is the U.S. stock market. He needs the S&P 500 to appreciate above January highs before November's midterm electionsto rock his Twitter account. This means an appreciation of more than 8% over the next seven months. I think this is achievable, but it will be a bumpy ride.

Currency markets are steady this Tuesday morning after the U.S. dollar plunged on Monday. Neither risk appetite nor risk aversion seems to be supporting the greenback. In theory, higher yields should attract inflows to U.S. bonds, but the argument against this theory is the growing U.S. debt and growth in other markets- particularly emerging economies, which will continue to lead to outflows from the U.S.

There are also high expectations that major central banks will start following the Fed's path in tightening monetary policy, leading to further losses in the greenback. ECB's Weidmann said market expectations of a rate hike towards the middle of 2019 are completely unrealistic, suggesting the ECB will likely move much earlier in raising rates. The Euro is trying to flirt with the 1.25 level and a break above is likely to test 2018 highs of 1.2555.

Gold has clearly ignored the surge in U.S. equities and easing concerns about U.S. -China trade tensions. The yellow metal is benefiting from the weaker dollar and rising political conflicts between Russia and the U.S., after Trump expelled 60 Russian diplomats. Expect gold prices to remain firm as a result of increasing geopolitical tensions and extreme volatility in equity markets.

Global Trade Tensions Ease As China And US Talk Sending Equities Higher

General Trend:

- Markets continue to gain amid press headlines that China and US are looking to ease trade dispute

- Improvement in risk appetite supports Asian currencies

- China set yuan at highest level since 2015 devaluation

- Australia Iron Ore miner Fortescue cuts price guidance, notes subdued China demand

- South Korean chipmakers decline amid speculation China may purchase more US chips

Japan

- Nikkei 225 opened +0.9%; closed +2.7%

- Japanese automakers and steelmakers outperform

- Panasonic [6752.JP] rises over 4% after receiving positive broker commentary

- (JP) Japan Feb PPI Services y/y: 0.6% v 0.7%e

- (JP) Japan Trade Min Seko: Working steadily to deal with US tariff issue

- (JP) Japan former tax agency head Sagawa: PM Abe, his wife Akie, Fin Min Aso and their top aides did not give instructions to change documents about a land deal

- (JP) Japan MoF sells ¥500B v ¥500B indicated in 0.90% (prior 0.90%) 40-yr bonds, yield at lowest price 0.885%; bid to cover 3.19x v 3.67x prior

- (JP) 48% of respondents said Japan PM Abe should resign amid Moritomo land scandal – Asahi Poll

Korea

- Kospi opened +0.7%

- (KR) South Korea Mar Consumer Confidence: 108.1 v 108.2 prior

- (KR) North Korea leader Kim Jong Un reportedly is visiting China – press; would be his first known visit outside North Korea since taking power

- GM Korea said to plan to file for bankruptcy by April 20 if no agreement is reached - South Korea Press

China/Hong Kong

- Hang Seng opened +1.4%, Shanghai Composite +1.0%

- Hang Seng Telecom index +2.9%, Info Tech +2.1%, Materials +1.8%, Services +1.4%, Industrials +1.3%, Utilities +1.3%, Consumer Goods +1.1%, Property/Construction +1.1%, Financials +0.5%

- Angang Steel [347.HK] rises over 5% after FY17 results beat ests

- China Unicom [762.HK]: Rises over 5% amid positive broker commentary

- Tiande Chemcial [609.HK] declines over 7%: FY17 profits and margins declined

- (US) Reportedly USTR could announce the list of specific tariffs against China as soon as Tuesday; will still be a 30 comment period - CNBC

- (CN) China govt officially files WTO appeal of US steel and aluminum tariffs - press

- (CN) PBoC Open Market Operation (OMO): Skips OMO v skips prior; Net drains CNY10B v CNY70B prior (3rd consecutive skip)

- (CN) China PBoC sets yuan reference rate at 6.2816 v 6.3193 prior (strongest setting since August 11, 2015)

- (CN) China Jan-Feb Industrial Profits CNY968.9B, +16.1% y/y v 10.8% in Dec

- (CN) China said to urge northern cities to close factories amid smog concerns – financial press

- (HK) Hong Kong sells HK$11B in 6-month bills, avg yield 1.08%

- (HK) Telegraph comments on Hong Kong Monetary Authorities (HKMA’s) plan to defend its US dollar currency peg. HKD has recently hit the weakest level in 33 years amid risk of capital flight and the ‘surge’ in US dollar Libor rates.

Australia/New Zealand

- ASX 200 opened +0.3%; closed +0.7%

- ASX 200 Consumer Discretionary index +1.6%, Financials +0.2%

- Avanco Resources [AVB.AU] Receives cash and stock offer from Oz Minerals worth A$0.168/share (~118% premium to prior close)

- Fortescue [FMG.AU] Reports H1 revenue realization was 68% of avg Platts 62 CFR index v 70-75% prior; notes slower than expected recovery in contractual realizations amid weak China demand

- (AU) Australia sells A$150M v A$150M indicated in 1.25% Aug 2040 indexed bonds, avg yield 1.0113%, bid to cover 3.33x

- (AU) Australia Feb HIA New Home Sales m/m: -1.4% v -2.1% prior

Other Asia

- TSMC, 2330.TW At full capacity due to high Android chip demand - Taiwan press

- (ID) Indonesia FSA: Sets maximum surcharge for systemic banks equal to 3.5% of risk weighted assets

North America

- US equity markets ended broadly higher: Dow +2.8%, S&P500 +2.7%, Nasdaq +3.3%, Russell 2000 +2.2%

- S&P500 Technology +3.8%, Financials +3.3%

- GGP [GGP]: Brookfield revises offer to $23.50/share in cash (vs $23.00 prior); GGP shareholders can elect between cash or share proposals

- (US) Fed's Quarles (hawk, FOMC voter): US economy 'performing well'

- (US) Fed's Dudley (dove, FOMC voter): Does not discuss monetary policy in prepared remarks

Europe

- Deutsche Bank, DBK.DE Said to have approached senior executive at Goldman to replace its CEO Cryan - UK Press

- (EU) ESMA said to ban binary options and restrict CFD for retail investors

- Levels as of 02:00ET

- Hang Seng +0.9%; Shanghai Composite +0.8%; Kospi +0.7%

- Equity Futures: S&P500 +0.5%; Nasdaq100 +0.6%, Dax +0.4%; FTSE100 +0.3%

- EUR 1.2458-1.2442; JPY 105.75-105.42; AUD 0.7758-0.7728;NZD 0.7303-0.7282

- Apr Gold -0.2% at $1,352/oz; May Crude Oil +0.3% at $65.77/brl; May Copper +0.8% at $3.01/lb

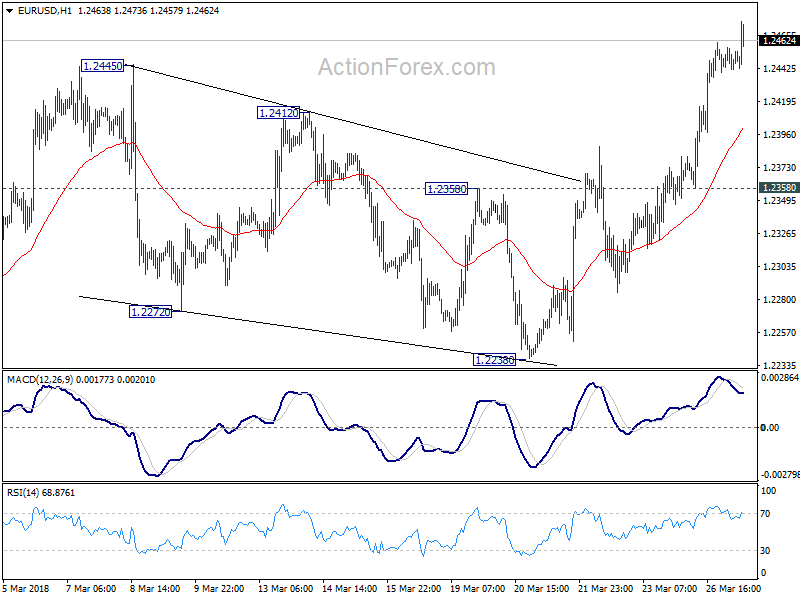

EURUSD Strongly Bullish Above 1.2430 Level

The euro has moved to its highest trading level of the month against the greenback, as the U.S dollar index slumps lower towards the 89.00 technical level. The EURUSD pair is still strongly bullish across all technical indicators, with price-action continuing to firm above the 1.2430 level. Traders now look to the next directional move in the U.S dollar index, and the release of March Consumer Confidence data from the U.S economy later today.

The EURUSD pair remains strongly bullish above the 1.2430 level, with buyers targeting the 1.2500 and 1.2555 resistance levels.

Should EURUSD price-action trade below the 1.2430 level, a correction towards the 1.2400 and 1.2382 levels seems likely.

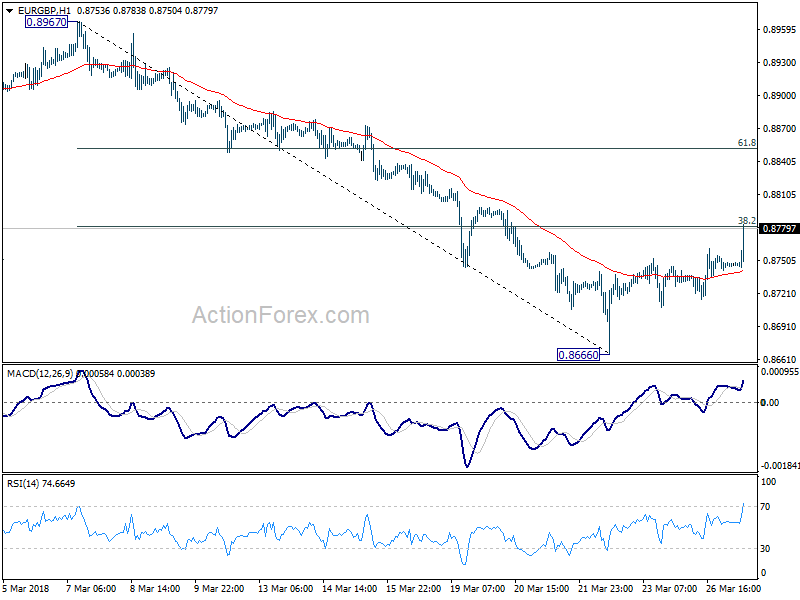

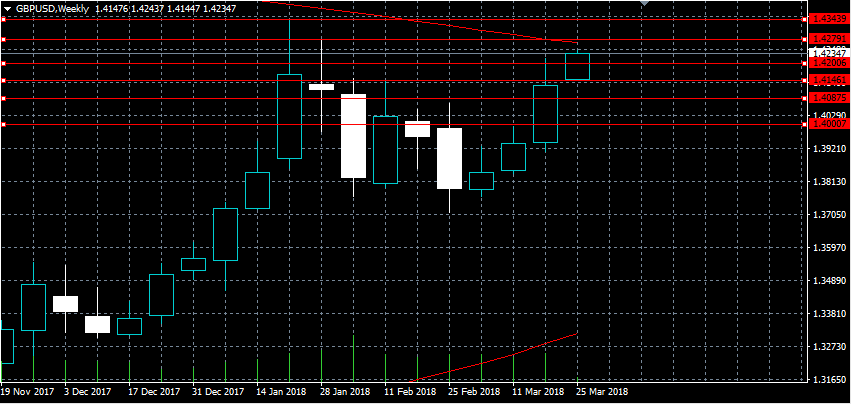

EUR/GBP rally drags down GBP/JPY and GBP/USD

EUR/GBP spikes higher in early European session, after clearing 0.8750. A major reason is believed to be Bundesbank's monthly purchase for UK's contribution to EU membership. Today's move could be exaggerated by thinner holiday liquidity. Also EUR/GBP bearish could be finally giving up after the cross failed to sustain below 0.8686 last week. But it's worth a watch to see if the rebound is turning into something sustainable. For now, based on current momentum, it could be heading back to 61.8% retracement of 0.8967 to 0.8666 at 0.8852 with a short term based formed.

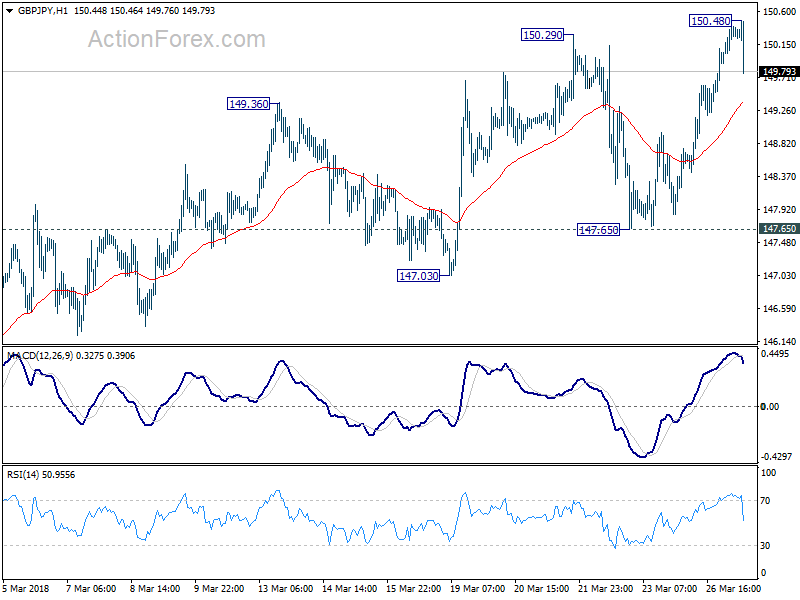

The move in EUR/GBP is also affecting other pairs. GBP/JPY dip notably lower after hitting 150.48.

The move in EUR/GBP is also affecting other pairs. GBP/JPY dip notably lower after hitting 150.48.

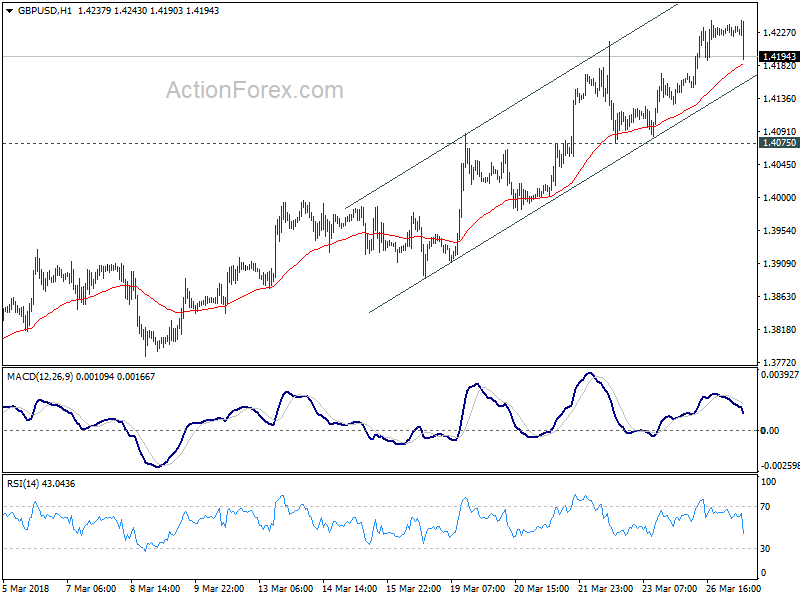

GBP/USD also dips after hitting 1.4243.

GBP/USD also dips after hitting 1.4243.

On other hand, EUR/USD is staying firm after edging higher to 1.2475.

On other hand, EUR/USD is staying firm after edging higher to 1.2475.

GBPUSD Buyers Look Towards 1.4268 Level

The British pound continues to build bullish upside momentum against the U.S dollar, with price-action moving to its highest trading level since February 2nd. The GBPUSD pair yesterday moved to a new March price-high, hitting 1.4240, with buyers now looking towards the pairs 200-week moving average, currently located at the 1.4268 level. Overall U.S dollar weakness and ongoing Brexit negotiation news remains the main driving force behind intraday price movements in the pair.

The GBPUSD pair retains a bullish bias whilst trading above the 1.4200 level, further upside towards 1.4268 and 1.4343 seems possible.

Should GBPUSD price-action trade below the 1.4200 level for a sustained period, a correction towards the 1.4146 and 1.4087 levels remains possible.

Eurozone Sentiment Indicators Drive Headlines On Tuesday

The economic calendar is back in full swing on Tuesday, with a steady stream of European data set to make headlines. Investors can also expect several market-moving releases from the New York session focusing on US manufacturing, housing prices and monetary policy.

Action begins at 06:00 GMT with a report on German import prices for the month of February. The import price index is forecast to fall 0.3% in February, after rising 0.5% the month before.

At 07:00 GMT, the Spanish government will release preliminary inflation data at 07:00 GMT. The harmonized index of consumer prices (HICP) is forecast to rise 1.6% annually for March, up from 1.2% the previous month.

Italy will release a pair of sentiment indicators at 08:00 GMT, including consumer confidence and business confidence. Both readings are forecast to weaken month-on-month. Meanwhile, Portugal is also scheduled to report on consumer and business confidence at 08:30 GMT.

The European Commission’s statistical agency will unveil its sentiment indicators at 09:00 GMT. Economic sentiment, business climate, industrial confidence, consumer confidence and services sentiment will all make headlines.

Shifting gears to North America, S&P/Case-Shiller will report on housing prices at 13:00 GMT. The home price indices are forecast to rise 6.2% annually in January, down from 6.3% the previous month.

The Federal Reserve Bank of Richmond will release its monthly manufacturing index at 14:00 GMT. The monthly gauge is forecast to drop to 23 in March from a reading of 28 the previous month.

In terms of monetary policy, Federal Open Market Committee (FOMC) member Raphael Bostic will deliver a speech at 15:00 GMT. Bostic was part of the policy committee that voted to raise interest rates last week.

EUR/USD

Europe’s common currency took advantage of a sliding dollar on Monday to launch itself to fresh five-week highs. The EUR/USD exchange rate is now trading in the mid-1.2500 region following an 80-pip surge at the beginning of the week. The pair is edging closer to the February high, with fundamental cues likely to support the euro in the near term.

GBP/USD

Cable opened the week in fine form, as prices surged past 1.4200 for the first time since the beginning of February. At the time of writing, GBP/USD was trading at 1.4231. Momentum returned to cable earlier this month after the UK and the European Union reached an agreement on a Brexit transition deal.

USD/JPY

After bottoming at 104.69 on Friday, the USD/JPY has gradually recovered. The pair is now trading comfortably above 105.00, although the near-term outlook remains firmly tilted to the downside. USD/JPY remains in a long-term downtrend, a picture that is unlikely to improve anytime soon as risk-off sentiment supports the yen.

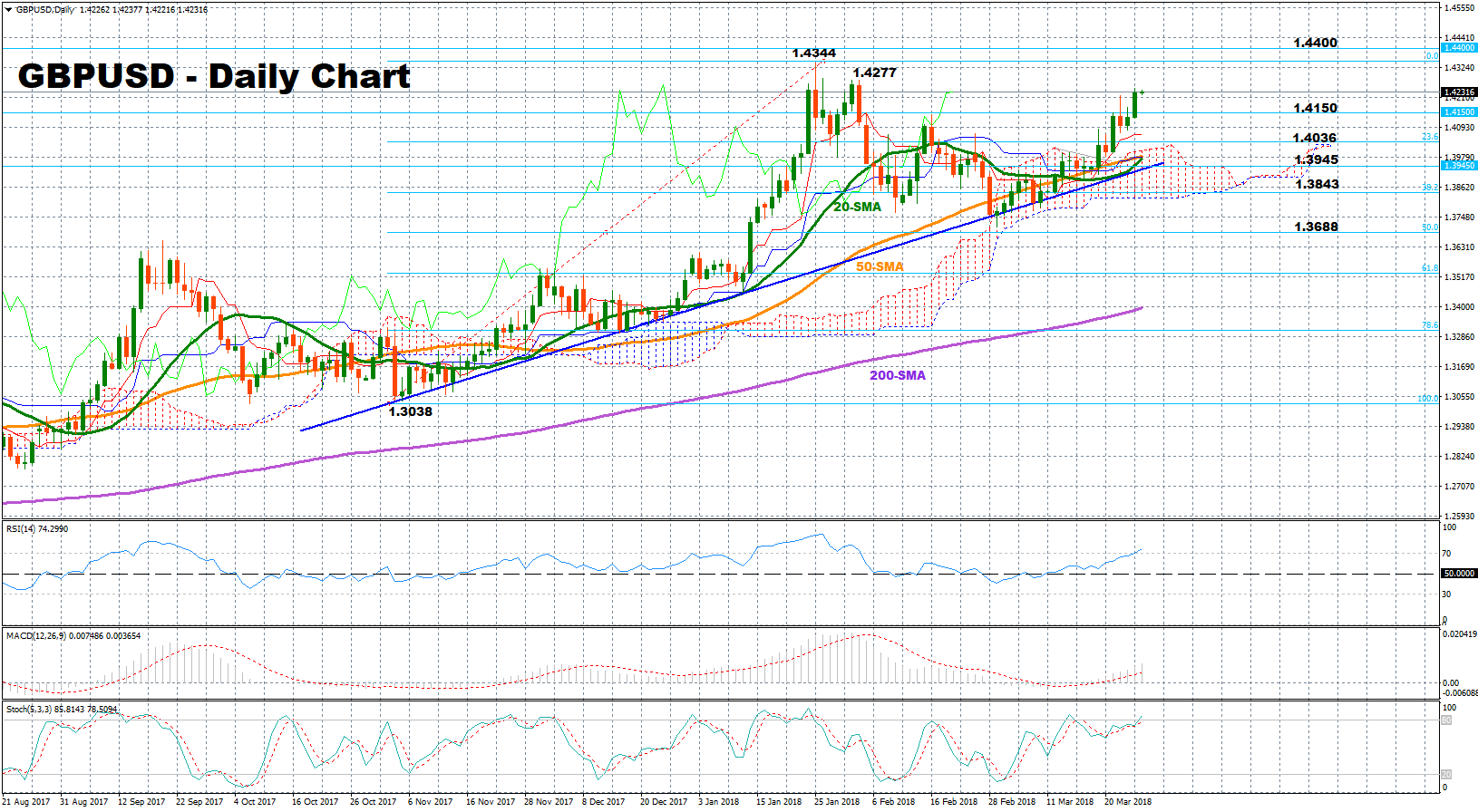

GBPUSD Bulls Still In The Game But Approach Overbought Zone

GBPUSD has almost reversed the downtrend started at the beginning of February and the backdrop is looking bullish at the moment with price actions taking place above the Ichimoku cloud and all the simple moving average lines (SMA). Yet, momentum indicators suggest that there is not much space for additional gains.

Both the RSI and Stochastics are in overbought territory, suggesting that the market might show weakness in the short-term. However, the latter still needs to post a bearish cross to confirm that negative movements are on the way; if the blue %K line crosses below the red %D line, the next price move could be to the downside. MACD, though, continues to rise above zero and its red trigger line, giving some positive signals.

On the way up, immediate resistance could be found at February’s high of 1.4277 and then at the 1 ½-year peak of 1.4344. If the market manages to break this top, stretching the uptrend from 1.3038, the pair could pick up speed towards the 1.4400 handle before eyes turn to the 1.4500 psychological level.

Should the market change direction to the downside, the first stop could be at 1.4150, a level approached several times from the beginning of February onwards. A close below from here could find support at the 23.6% Fibonacci of 1.4036 of the upleg from 1.3038 to 1.4344, where the upper bound of the Ichimoku cloud is also located at the moment. A stronger barrier, though, could come between the 50-day SMA and the blue ascending line (1.3982-1.3930) because any substantial close below this area could increase chances for further downside movements, and lead prices even lower towards the 38.2% Fiboancci of 1.3843. In the worst case, prices could meet the 50% Fibonacci of 1.3688.

In the medium-term, the picture is expected to remain bullish as long as the pair holds above the 50-day SMA and the bullish cross between the 50- and the 200-day SMA stays in place.

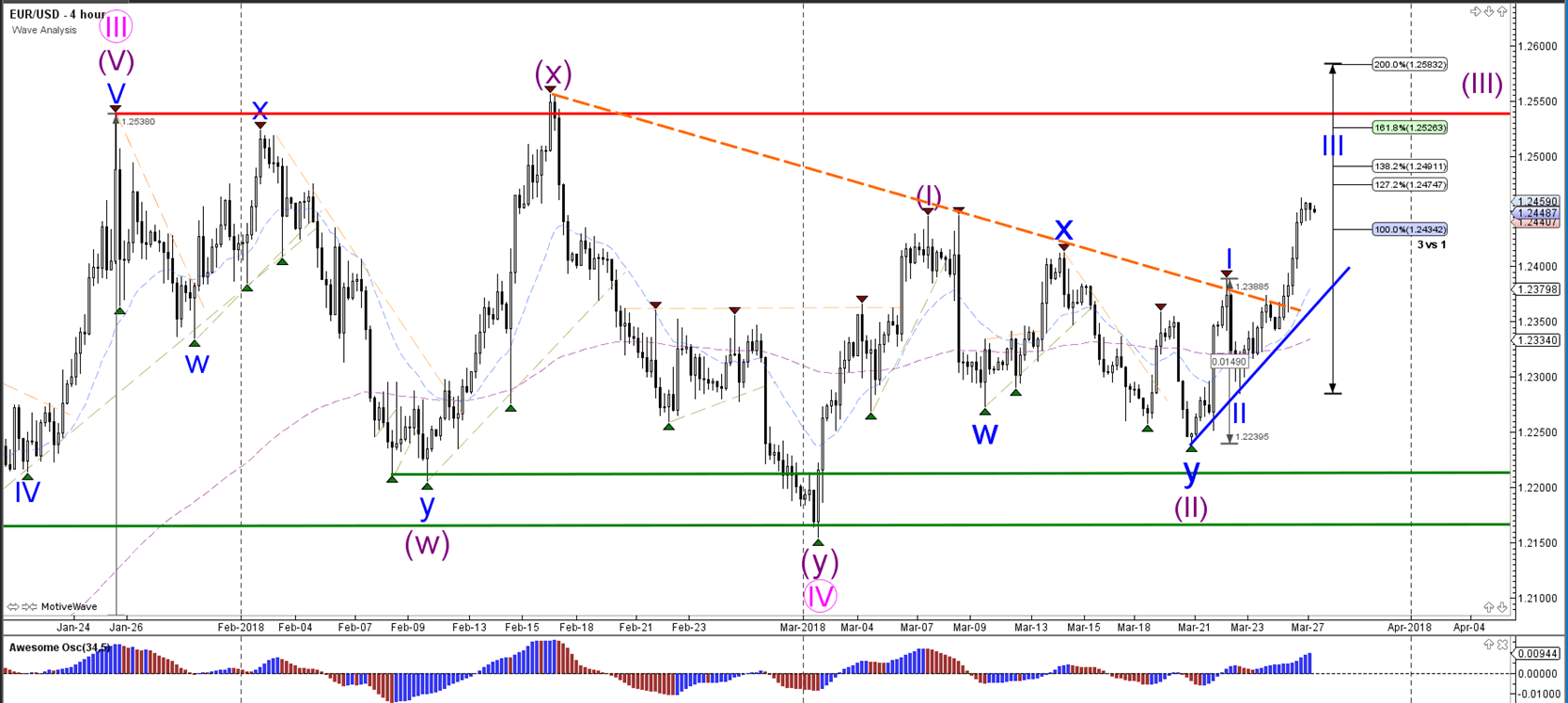

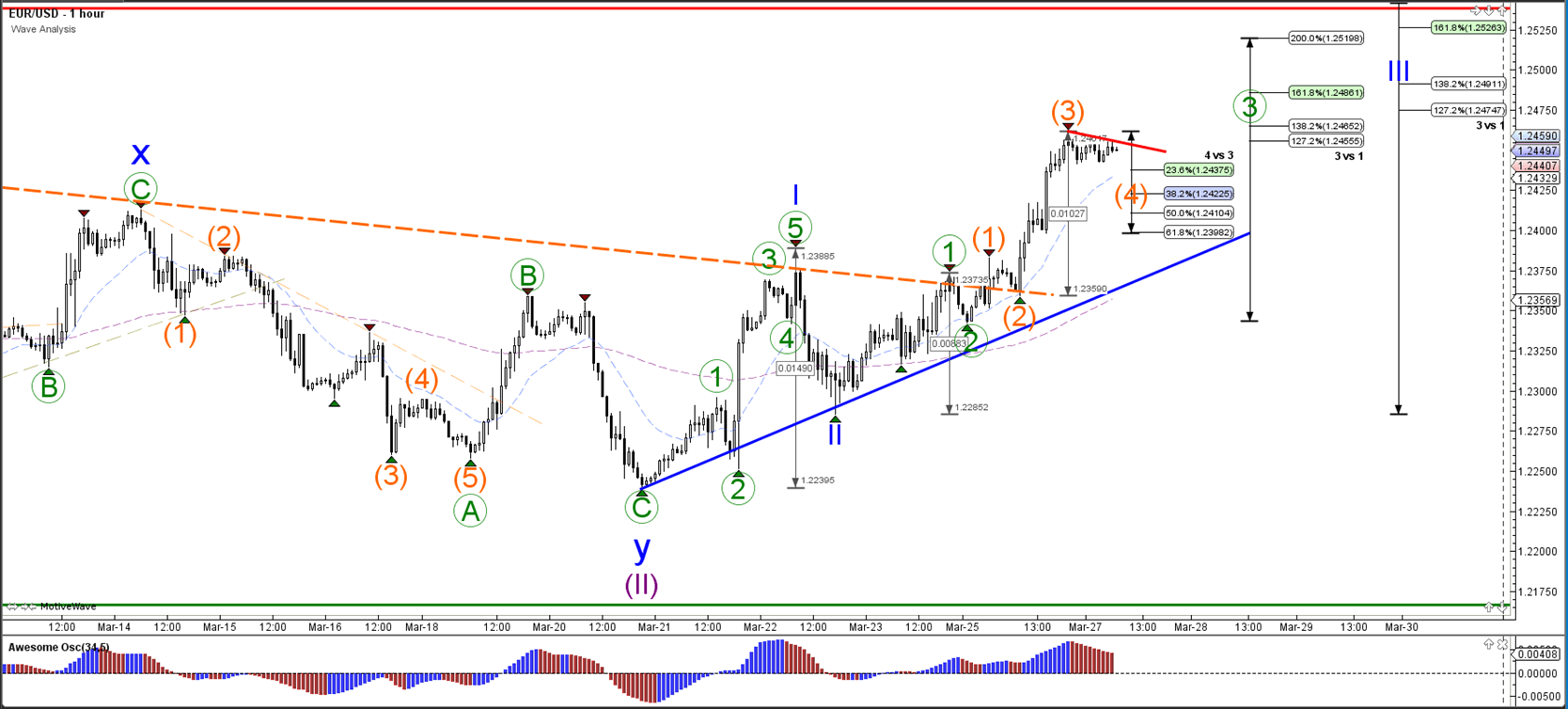

EUR/USD Bullish Breakout Prepares For Wave 4 Retracement

Currency pair EUR/USD

The EUR/USD broke above the resistance trend line (dotted orange). This bullish break seems to have started a potential wave 3 (blue) of 3 (purple).

The EUR/USD could be building a mild retracement within a shallow and corrective wave 4 (orange) pattern. The Fib levels of wave 4 vs 3 could act as support and bouncing levels.

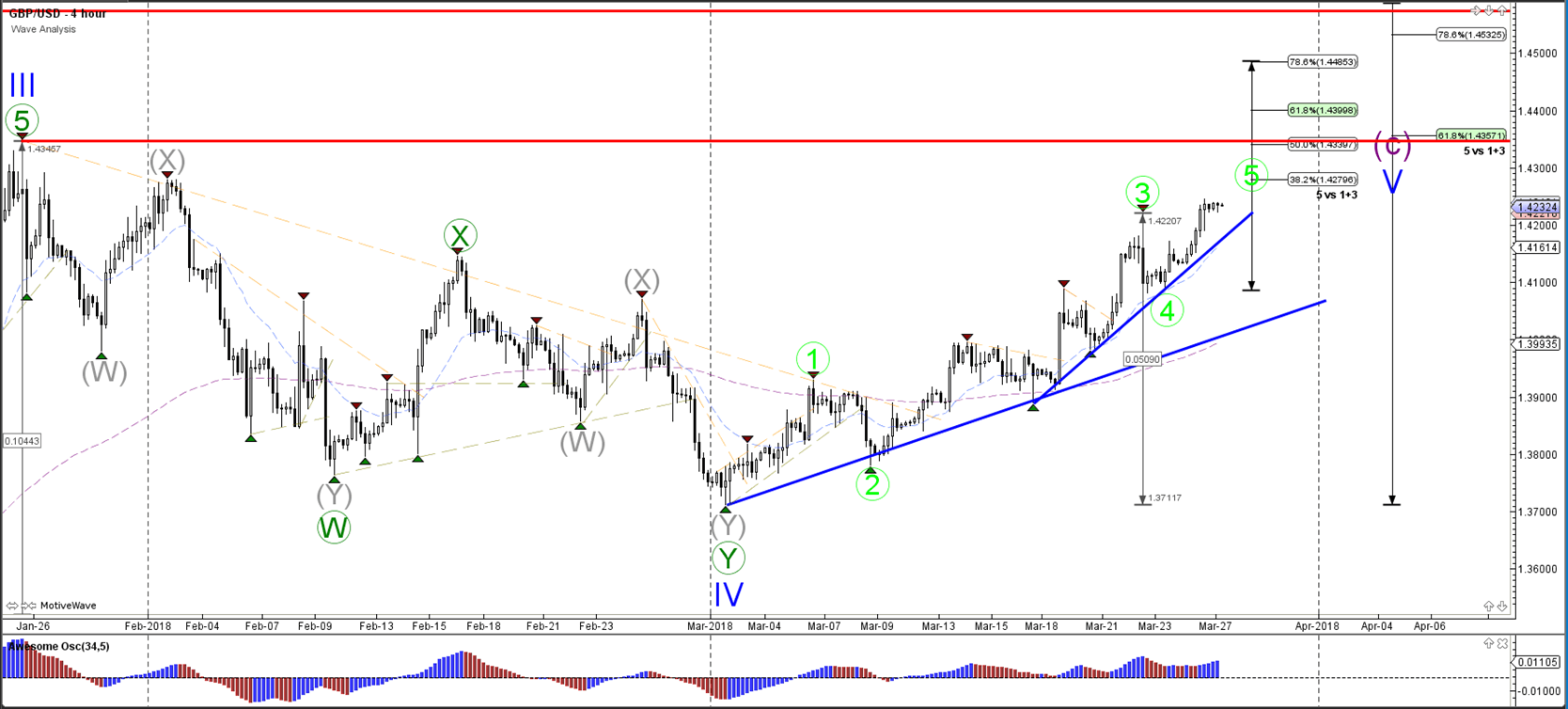

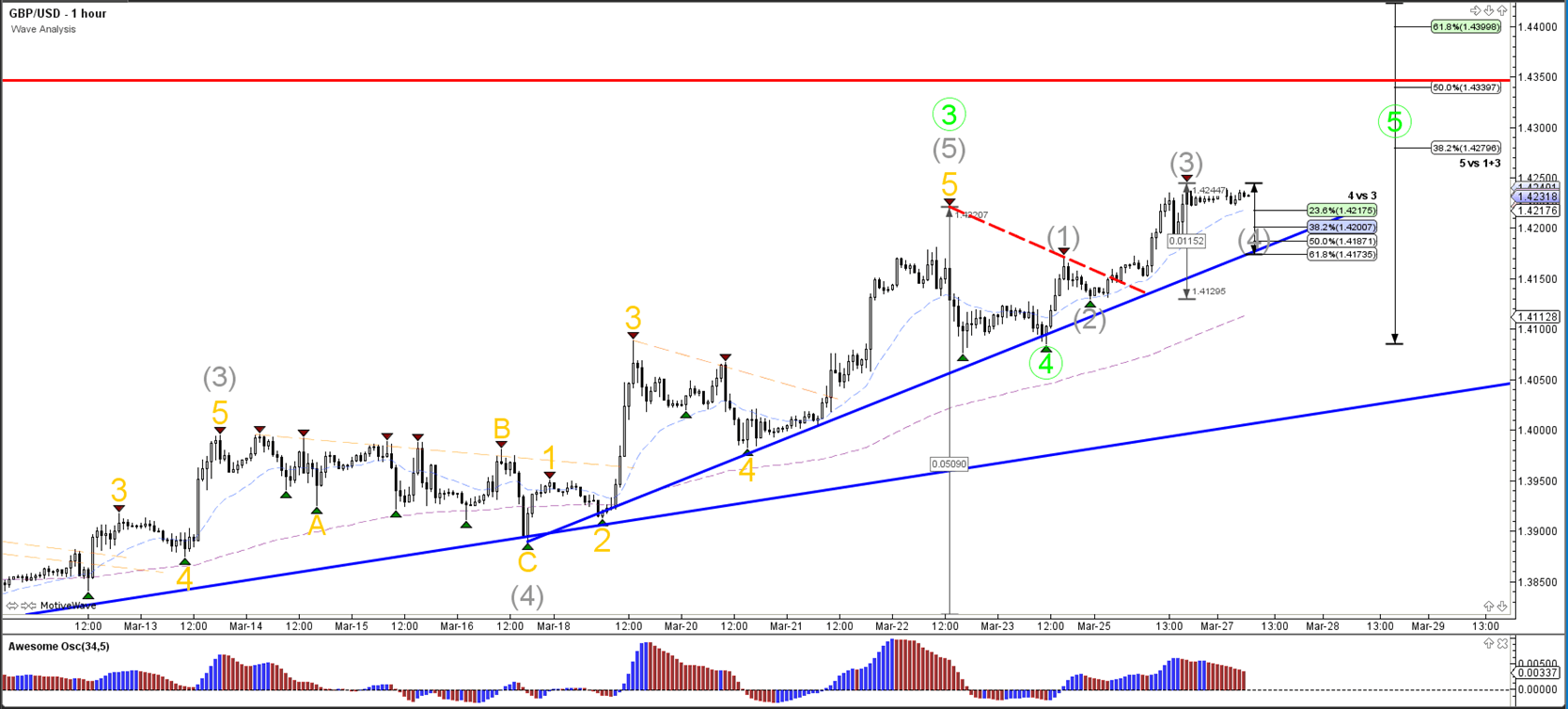

Currency pair GBP/USD

The GBP/USD seems to have completed a wave 4 (green) retracement and is continuing with its strong uptrend. But priceis now approaching the previous top (red), which is an area where price can temporarily pause or reverse.

The GBP/USD could be building a wave 4 (grey) retracement. The Fib levels of wave 4 vs 3 could act as support and bouncing levels

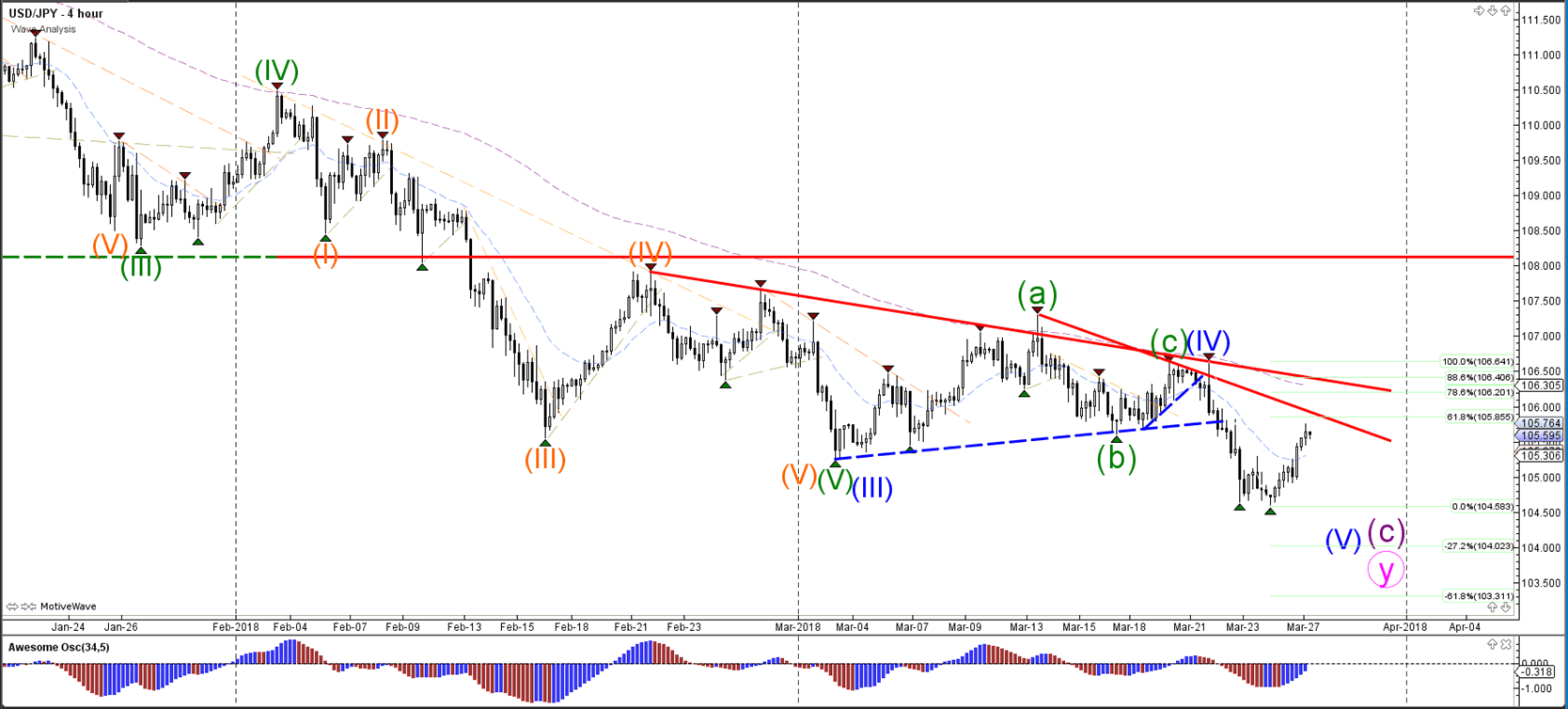

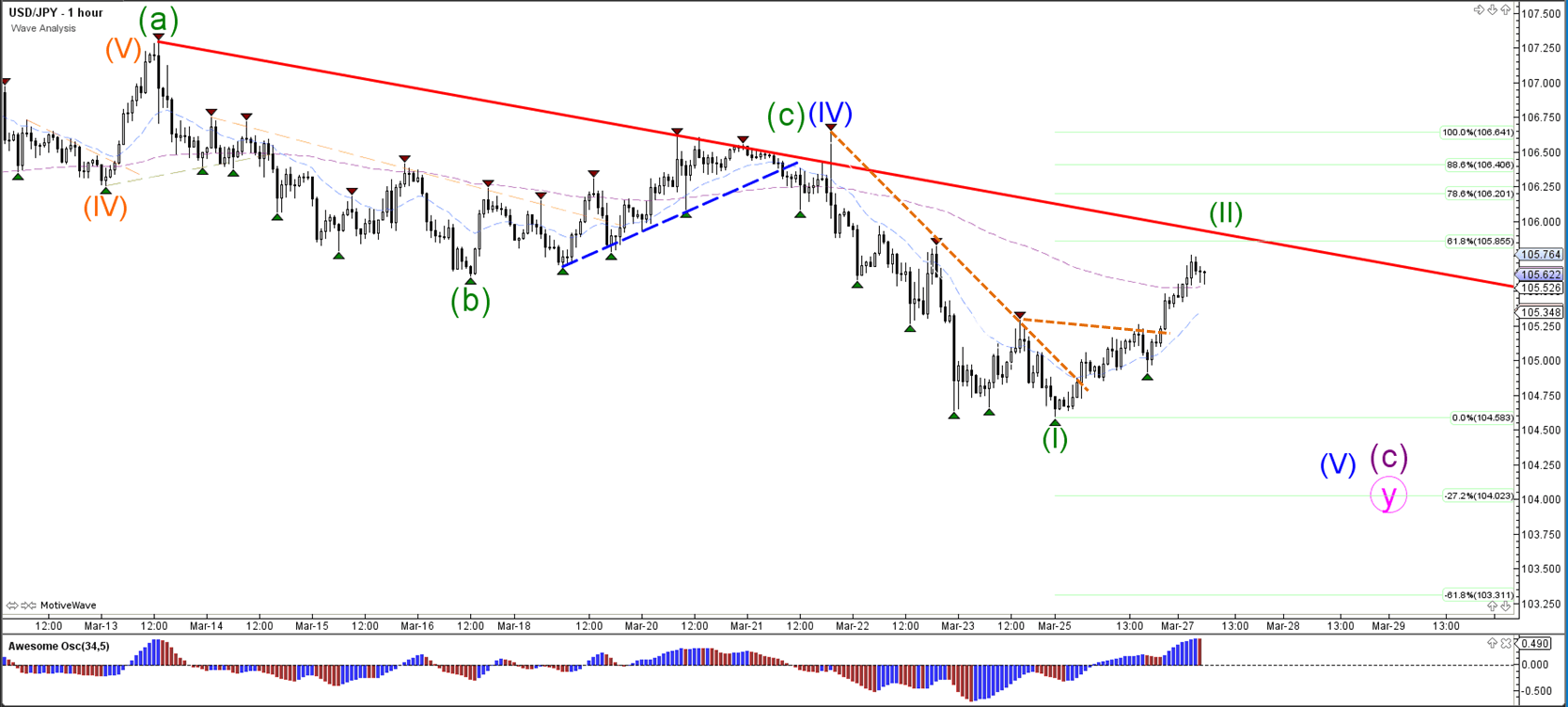

Currency pair USD/JPY

The USD/JPY downtrend broke key support levels but is now building a bullish correction. The resistance trend lines (red) are a key decision zone for a bigger reversal or downtrend continuation.

The USD/JPY could be building a wave 2 correction after breaking above resistance (dotted orange).

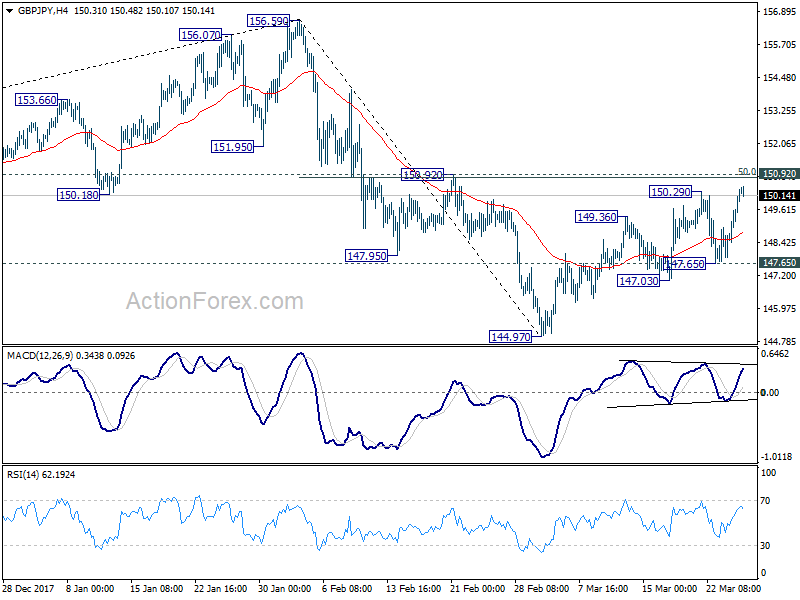

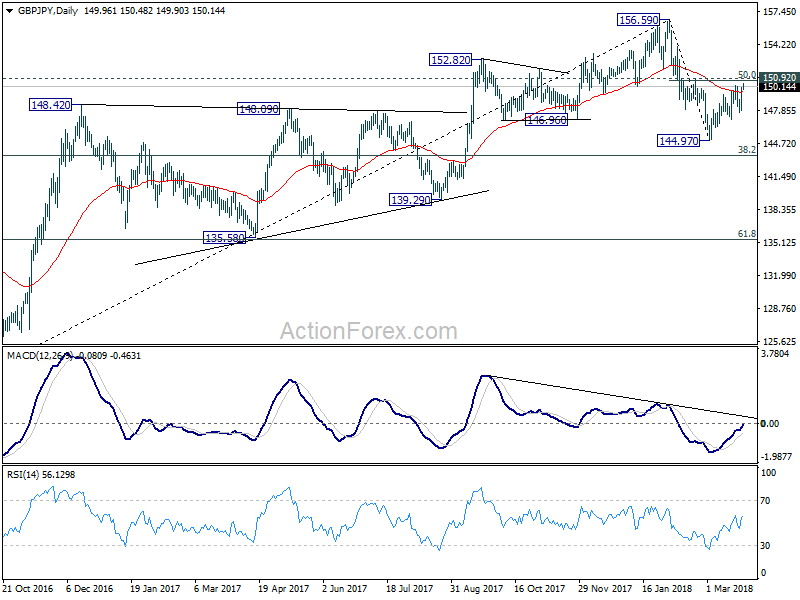

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.53; (P) 149.31; (R1) 150.76; More...

GBP/JPY's rebound from 144.97 resumed by taking out 150.29. But still outlook is unchanged. Such rebound is seen as a correction. And strong resistance is expected from 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption. On the downside, below 147.65 minor support will bring retest of 144.97 low first. However, sustained break of 150.92 will indicate near term reversal and pave the way back to retest 156.69 high.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.