Sample Category Title

USD/JPY Slight Decrease

USD/JPY is slightly weakening following recent bounce from 104.56 low, currently trading at the 105.50 range. The pair is expected to decline along 105.45. The bearish pattern started in January 2018 is maintained. The short-term technical structure suggests short-term decrease.

We favor a long-term bearish bias. Support remains at 101.20 (09/11/2016 low). A gradual rise toward the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 101.20 (09/11/2016 low). The pair trades largely below its 200 DMA.

GBP/USD Decreasing

GBP/USD is decreasing from 1.4244 high, currently trading below 1.42 and heading along the 1.4155 range. The pair is contained between hourly support and resistance given at 1.4023 (15/02/2018 low) and 1.4278 (02/02/2018 high). The technical structure suggests short-term decrease.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Consolidation Below 1.25

EUR/USD is starting a consolidation phase along the 1.2440 range, just below hourly resistance at 1.2506 (25/01/2018 high). Hourly support remains at 1.2165 (17/01/2018 low). The technical structure suggests short-term sideways trading moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

European Confidence Data Continues Its Retreat From Recent Cycle Highs

Notes/Observations

- Risk appetite finding fresh legs thanks to diplomatic tones as US officials indicated efforts to diffuse rising trade tensions between the world’s two leading economies were ongoing

- Spain Mar Preliminary CPI data comes in below expectations (YoY: 1.2% v 1.4%e) while Euro Zone M3 Money Supply misses (4.2% v 4.6%e)

- European confidence data continues its retreat from recent cycle highs as technical indicators did not appear to be generating a robust signal in the region

Asia:

- North Korea leader Kim Jong Un reportedly was visiting China (Note: First known trip outside North Korea since taking power). Note: Neither China or North Korea made any official comment but such a visit would be seen as being a significant development

- China PBoC sets yuan reference rate at 6.2816 v 6.3193 prior (strongest setting since August 11, 2015)

- Japan former tax agency head Sagawa: PM Abe, his wife Akie, Fin Min Aso and their top aides did not give instructions to change documents about a land deal

Europe:

- IMF chief Lagarde said to see no risk of currency war

Americas:

- Reportedly USTR could announce the list of specific tariffs against China as soon as Tuesday; will still be a 30 comment period

- Fed's Mester (FOMC voter, hawk): Further gradual rate hikes were appropriate. Saw unemployment falling below 4% through 2019

Economic Data:

- (DE) Germany Feb Import Price Index M/M: -0.6% v -0.3%e; Y/Y: -0.6% v -0.3%e

- (FI) Finland Mar Consumer Confidence: 24.7 v 25.8 prior; Business Confidence: 11 v 14 prior

- (ES) Spain Mar Preliminary CPI M/M: 0.1% v 0.3%e; Y/Y: 1.2% v 1.4%e

- (ES) Spain Mar Preliminary CPI EU Harmonized M/M: 1.2% v 1.7%e; Y/Y: 1.3% v 1.6%e

- (SE) Sweden Mar Consumer Confidence: 101.5 v 104.6e; Manufacturing Confidence: 114.5 v 112.2e, Economic Tendency Survey: 108.4 v 108.0e

- (TR) Turkey Mar Economic Confidence: 100.2 v 103.0 prior

- (SE) Sweden Feb Household Lending Y/Y: 7.0% v 7.0%e

- (SE) Sweden Feb PPI M/M: -0.5% v +0.8% prior; Y/Y: 2.8% v 2.5% prior

- (SE) Sweden Feb Trade Balance (SEK): -3.4B v -1.5Be

- (EU) Euro Zone Feb M3 Money Supply Y/Y: 4.2% v 4.6%e

- (IT) Italy Mar Consumer Confidence: 117.5 v 115.0e; Manufacturing Confidence: 109.1 v 109.9e, Economic Sentiment: 106.0 v 108.5 prior

- (PT) Portugal Mar Consumer Confidence: 2.0 v 1.3 prior; Economic Climate Indicator: 2.1 v 1.9 prior

- (HK) Hong Kong Feb Trade Balance (HKD): -42.7B v -40.0Be; Exports Y/Y: 1.7% v 7.0%e; Imports Y/Y: -3.2% v +2.3%e

- (EU) Euro Zone Mar Business Climate Indicator: 1.34 v 1.36e; Consumer Confidence (Final): 0.1 v 0.1e, Economic Confidence: 112.6 v 113.3e, Industrial Confidence: 6.4 v 6.9e, Services Confidence: 16.3 v 16.5e

Fixed Income Issuance:

- (IN) India sold total INR120B vs. INR120B in 3-month, 6-month and 12-month bills

- (DK) Denmark sold total DKK1.20B in 3-month and 6-month Bills

- (ID) Indonesia sold total IDR20.7T vs. IDR17.0T target in 3-month, 6-month bills, 10-year, 15-year and 20-year Bonds

- (IT) Italy Debt Agency (Tesoro) sold total €6.0B vs. €6.0B indicated in 6-month Bills; Avg Yield: -0.43% v -0.403% prior; Bid-to-cover: 1.63x v 1.57x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 1.3% at 367.7, FTSE +1.6% at 6999, DAX +1.4% at 11976, CAC-40 +1.3% at 5133, IBEX-35 +1.0% at 9473, FTSE MIB 1.4% at 22307 , SMI +1.5% at 8639, S&P 500 Futures +0.6%]

- Market Focal Points/Key Themes: European Indices trade sharply higher following on from a strong sessions in Wallstreet and Asia overnight and positive US futures this morning following on from easing fears of a US-China trade war. M&A remained the focal point with Akzo Nobel divesting its Specialty Chemicals unit to Carlyle for €10.1B and GSK acquiring Novartis stake in Consumer Healthcare JV for $13B. On the earnings front Ferguson outperforms in the UK, with Baloise and Nordex also gaining, while H&M trades sharply lower following their Q1 results. Elsewhere IG Group trades sharply lower after cutting its FY19 outlook following the ESMA ruling. Looking ahead notable earners include Factset, McCormick and Francesca holding.

Movers

- Consumer Discretionary [Casino [CO.FR] +4.1% (Amazon and Monoprix partnership), H&M [HMB.SE] -6.6% (Earnings), Ferguson [FERG.UK] +5.0% (Earnings) ]

- Materials [Akzo Nobel [AKZA.NL] +4.0% (Divests Chemicals Unit to Carlyle)]

- Heatlthcare [ Novartis [NOVN.CH] +2.0%, GSK [GSK.UK] +4.5% (Divests consumer healthcare JV to GSK) ]

- Financial [ Deutsche Bank [DBK.DE] +1.6% (Reportedly approached Goldman Execs for CEO position), Plus 500 [PLUS.UK] +4% (ESMA ruling), IG Group [IGG.UK] -7.8% (Response to ESMA ruling), Baloise [BALN.CH] +1.5% (Earnings) ]

- Energy [Nordex [NDX1.DE] +5.7% (Earnings)]

Speakers

- ECB's Vasiliauskas (Lithuania): Saw a deeper discussion on policy changes in June. Could agree with market expectations of a rate hike in mid-2019 (in-line with Weidmann on such views).

- ECB's Liikanen (Finland): Cautioned about tightening policy too soon; reiterated Council view that patience and persistence was needed. The bond buying programs remains open-ended.

- BOE Financial Policy Committee (FPC) Minutes: Brexit still poses material risks to UK finance but progress has been made in mitigating risks

- Sweden Think Tank NIER Economic Forecasts cut its 2018 GDP from 2.9% to 2.8% while raising 2019 GDP from 2.0% to 2.1%. It maintained both 2018 and 2019 CPIF at 1.8%

- S&P raised South Africa 2018 and 2019 GDP growth forecasts noting that the country was making good progress on its fiscal path and the might have bottomed out on its rating. Raised 2018 GDP to 2.0% and 2019 GDP to 2.1%

- China Foreign Ministry: No information whether North Korea leader Kim Jong Un is in Beijing

Currencies

- USD initially probed its recent weekly lows against the major European pairs but saw its fortunes turn around as the session wore on. The greenback still well contained within its 2018 trading range.

- EUR/USD initial probed the upper end of its 2018 price range with 1.2476 as the session high. The pair drifted from its best levels after ECB's Liikanen cautioned about tightening policy too soon and reiterated Council view that patience and persistence was needed. Euro also dampened with poor data in the session. Spain Mar Preliminary CPI data came in below expectations (YoY: 1.2% v 1.4%e) while Euro Zone M3 Money Supply missed (4.2% v 4.6%e). European confidence data was also retreating from recent cycle highs. Pair testing below 1.2430 just ahead of the US session.

- GBP/USD could not sustain holding above the 1.42 level as cross-related selling in EUR/GBP weighed down the pound sterling. Cable testing the mid-1.41 area just ahead of the NY morning.

Fixed Income

- Bund Futures trade 17 ticks higher at 158.94 as bund downside demand emerges as yield fails to break below 0.50%. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 122.02 up 2 ticks ahead of UK 2056 I/L Gilt auction. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Tuesday's liquidity report showed Monday's excess liquidity rose to €1.802T from €1.801T prior. Use of the marginal lending facility increased from €100M to €105M.

Looking Ahead

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

- 05:30 (UK) DMO to sell £600M in 0.125% 2056 I/L Gilts (UKTi)

- 05:30 (PL) Poland to sell 2020, 2023, 2024, 2028 bonds

- 05:30 (ZA) South Africa to sell combined ZAR2.4B in 2030, 2035 and 2048 bonds

- 06:45 (US) Daily Libor Fixing - 07:00 (BR) Brazil Central Bank (BCB) COPOM Mar Minutes

- 07:00 (ES) Spain Feb YTD Budget Balance: No est v -€18.2B prior

- 07:00 (RU) Russia announces weekly OFZ bond auction

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (HU) Hungary Central Bank (NBH) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

- 08:05 (UK) Baltic Dry Bulk Index

- 08:55 (US) Weekly Redbook Sales

- 09:00 (US) Jan S&P/ Case-Shiller 20-City M/M: 0.60%e v 0.64% prior; Y/Y: 6.10%e v 6.30% prior; House Price Index (HPI): No est v 204.45 prior

- 09:00 (US) Jan S&P Case-Shiller (overall) HPI Y/Y: No est v 6.27% prior, Overall HPI Index: No est v 196.23 prior

- 09:00 (EU) Weekly ECB Forex Reserves

- 09:00 (HU) Hungary Central Bank (NBH) Gov Matolcsy post rate decision statement

- 10:00 (US) Mar Consumer Confidence: 131.0e v 130.8 prior

- 10:00 (US) Mar Richmond Fed Manufacturing Index: 22e v 28 prior

- 10:00 (MX) Mexico Feb Trade Balance: +$0.5Be v -$4.4B prior

- 10:00 (MX) Mexico Feb Unemployment Rate (seasonally adj): 3.4%e v 3.4% prior; Unemployment Rate (unadj): 3.3%e v 3.4% prior

- 11:00 (US) Fed’s Bostoc (2018 voter, dove) at conference in Atlanta

- 11:30 (US) Treasury to sell 4-week and 52-Week Bills

- 12:00 (CA) Canada to sell 2-Year Bonds

- 13:00 (US) Treasury to sell 5-Year Notes

- 13:30 (BR) Brazil Feb Central Gov Budget Balance (BRL): -21.1Be v +31.1B prior

- (AR) Argentina Central Bank Interest Rate Decision: Expected to leave 7-Day Repo Reference Rate unchanged at 27.25%

- 16:30 (US) Weekly API Oil Inventories

US Futures Higher After Strong Start In Europe

- Investors Buoyed By Softening Trade Stance;

- More Countries Join UK in Expelling Russian Diplomats, Investors Not Concerned;

- US Data and Bostic Speech in Focus.

Investors Buoyed By Softening Trade Stance

There are a lot of risks that financial markets have shrugged off over the last couple of years, to the amazement at times of investors, but the prospect of a trade war is clearly not one of these.

European markets are following Monday’s lead on Wall Street and posting substantial gains this morning, while US futures are pointing to another strong start on Tuesday. It has become clear that the main target of Donald Trump’s tariffs on steel and aluminium was China, with a number of other countries being granted extensions and possible exclusions since the announcement, while the threats have intensified towards Beijing.

Naturally, the prospect of a trade war between the world’s two largest economies has weighed heavily on risk appetite over the last couple of weeks with US equity markets posting significant losses on Thursday and Friday as things heated up. The message over the weekend though was far less confrontational and suggested the US would be open to scrapping the tariffs in exchange for certain other concessions such as reduced tariffs on important cars.

Ultimately, Trump’s target was and remains to reduce the county’s sizeable trade deficit with a number of countries and while he may give the impression that a trade war is a worthwhile sacrifice, I’m not sure he’s as keen on it as he makes out. The question now is how big a concession other countries are willing to make to appease him, if any, and whether it will be sufficient enough for him to sell it to US voters as a worthwhile victory. Given the reaction we’ve seen in markets over the last couple of week’s I don’t think he’ll be keen to follow through on his threats and risk sending markets into a tailspin.

More Countries Join UK in Expelling Russian Diplomats, Investors Not Concerned

Political stories are likely to continue to dominate financial markets this week in the absence of any major planned economic events. The calendar is looking much quieter than it did this time a week ago, putting increased focus on the developments on trade and other matters. Increased tensions between Russia and the West is another story that will continue to be monitored but hasn’t had much of a market impact, if any.

The UK will be delighted with the backing it’s had from its allies in the West, with a number of countries including the US having expelled Russian diplomats in response to the evidence offered by the UK in relation to the poisoning of former spy Sergei Skripal and his daughter. While Russia continues to deny any involvement, more than 100 diplomats have now been expelled by more than 20 countries which has threatened to increase tensions. Investors will be monitoring the situation closely to see whether the situation develops into something that could rattle the markets.

US Data and Bostic Speech in Focus

It’s looking a little light on the data side today, with CB consumer confidence from the US the only notable release. We’ll also hear from Raphael Bostic, a voter on the FOMC this year, who on Friday suggested he expects to see three rate hikes this year. It’s unlikely much has changed since then so market impact may be limited

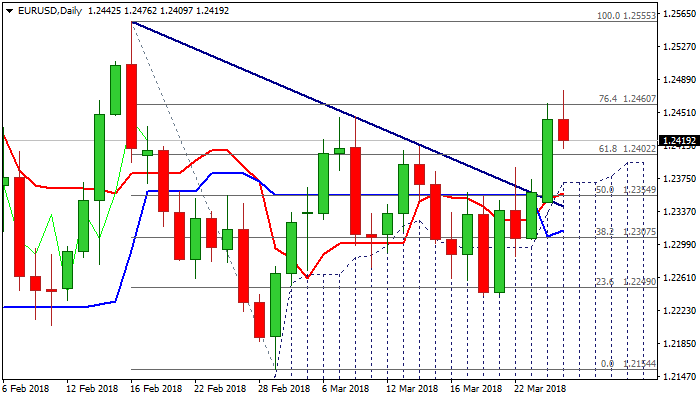

EURUSD Pulls Back After Repeated Failure Through Upper Bollinger/Fibo Barrier

The Euro eases from session high at 1.2476 after attempts through 20-d upper Bollinger band and Fibo 76.4% of 1.2555/1.2154 repeatedly failed. Stronger dollar and weaker than expected EU Business Climate data helped fresh bears, but current action could be seen as consolidation before broader bulls resume, while the price holds above broken Fibo 61.8% of 1.2555/1.2154 descend at 1.2402. Thick daily cloud continues to underpin (cloud top lies at 1.2370), with bulls expected to remain in play if extended dips will be contained above cloud top.

Res: 1.2461, 1.2476, 1.2500, 1.2522

Sup: 1.2402, 1.2370, 1.2358, 1.2331

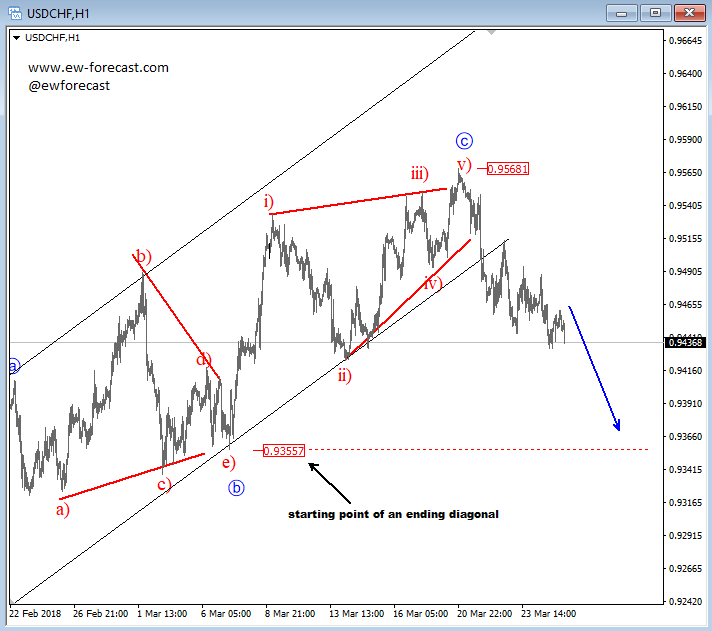

Elliott Wave Analysis: USDCHF Turning Bearish, 0.9356 In View

On the hourly chart of USDCHF, we see price slowly and steadily turning to the downside, following a possibly completed higher degree wave c at the 0.9568 level. As we look closer, we also see a completed Elliott wave ending diagonal that was located within the mentioned wave c. The speciality of this pattern is that it can indicate a sharp and strong reversal to follow into the opposite direction, and usually towards the starting point of the pattern, which in our case come in at 0.9356 level.

USDCHF, 1h

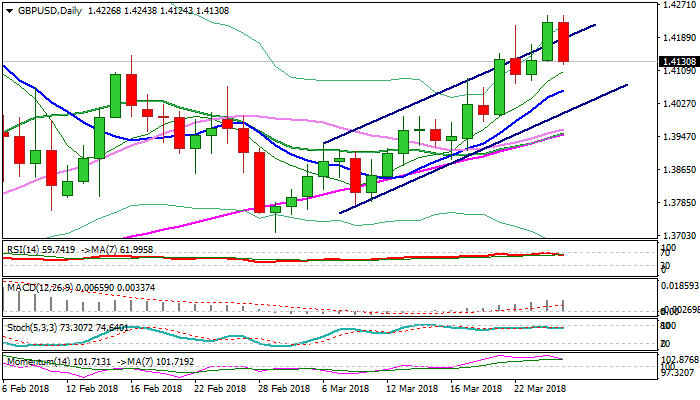

Cable – Fresh Bearish Acceleration Leaves Double-Top And Shifts Immediate Focus Lower

Sterling was sharply lower in mid-European trading and reversed Monday's rally, as report released on Monday signaled easing tensions between US and China as two sides were negotiating to improve US access to Chinese markets, which boosted dollar.

Cable fell to session low at 1.4125 after upside attempts repeatedly failed at 1.4244, where a double-top was left.

Fresh weakness broke below initial support at 1.4144 (16 Feb former high) and pressures next support at 1.4118 (Fibo 23.6% of 1.3711/1.4244). Break here would generate fresh bearish signal and risk further easing towards key supports at 1.4060/40 (rising 10SMA/Fibo 38.2% of 1.3711/1.4244 recovery leg), loss of which would signal reversal.

Daily indicators turned south and support scenario, however overall bullish structure sees current action as corrective while dips hold above 1.4060/40 pivots.

Today's close will be in focus for fresh signals.

Res: 1.4193, 1.4218, 1.4244, 1.4277

Sup: 1.4118, 1.4060, 1.4040, 1.4000

ECB Nowotny: Could reduce asset purchase “significantly” after September

Outspoken ECB Governing Council member Ewald Nowotny commented again today. He said that the central bank will decide on the future of monetary policy in the summer. This is rather apparent as the current EUR 30b per month asset purchase program is set to end in September. Nowotny also said that "if things continue as they are, ECB will be able to reduce asset purchases significantly" after that. While he cautioned not to make any abrupt change to policy, he also emphasized not to fall behind the curve.

Overall, Nowotny's comments were consistent with his usual stance, which is slightly on the hawkish side of the spectrum.

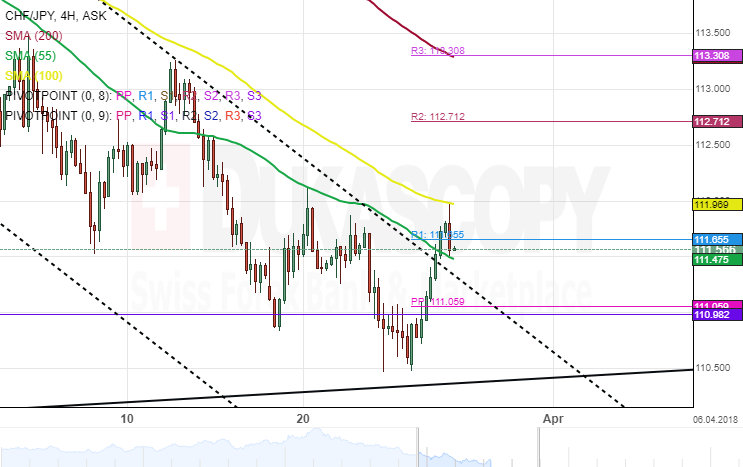

CHF/JPY 4H Chart: Breakout From Junior Channel

The Swiss Franc has been steered by a descending channel against the Japanese Yen. The rate bounced off the upper boundary of a junior pattern and has since remained bearish.

The currency pair has breached both the weekly pivot point and the 55– hour simple moving average also where the upper border of the descending channel is located.

Given that a breakout has occurred, it is likely that the CHF/JPY exchange rate should establish a new wave up during the following trading session. However, it is important to note that technical indicators suggest otherwise.