Sample Category Title

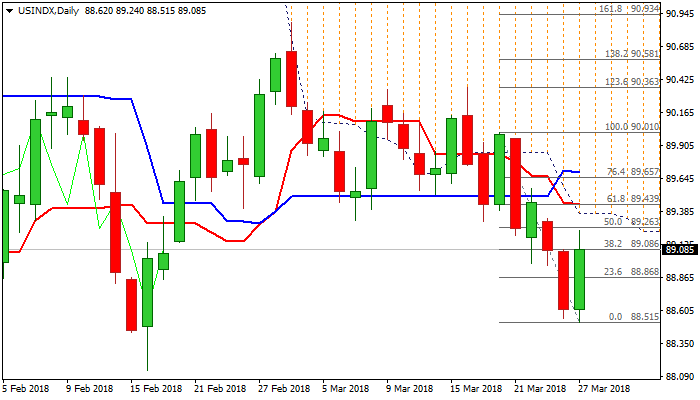

Dollar Index – Base of Thick Daily Cloud Marks Strong Obstacle for Fresh Recovery Rally

The dollar rallies on Tuesday, boosted by fading fears about trade war between the US and China. The dollar index accelerated from 88.50 zone where weakness of past three weeks found support and subsequent bounce signals formation of base.

Fresh rally already retraced losses from the previous day and generated initial bullish signal on break above pivotal barrier at 89.08 (Fibo 38.2% of 90.01/88.51 bear-leg).

Today’s rally is on track to form bullish outside day which would generate fresh signal for stronger recovery.

Fresh bullish sentiment is building and could help for further recovery, however, firmly bearish daily techs warn of possible recovery stall, as very thick daily cloud heavily weighs. Cloud is spanned between 89.37 and 91.16 and strong barrier provided by cloud base is reinforced by falling 10SMA and Fibo 61.8% of 90.01/88.51 (89.45).

Close above here is required to generate stronger bullish signal of extended recovery.

Caution on repeated failure under cloud base (falling daily cloud caps upside attempts and maintains strong bearish pressure since 01 Mar), which could signal fresh weakness and shift near-term focus lower.

Res: 89.24; 89.45; 89.85; 90.01

Sup: 88.86; 88.50; 88.24; 88.14

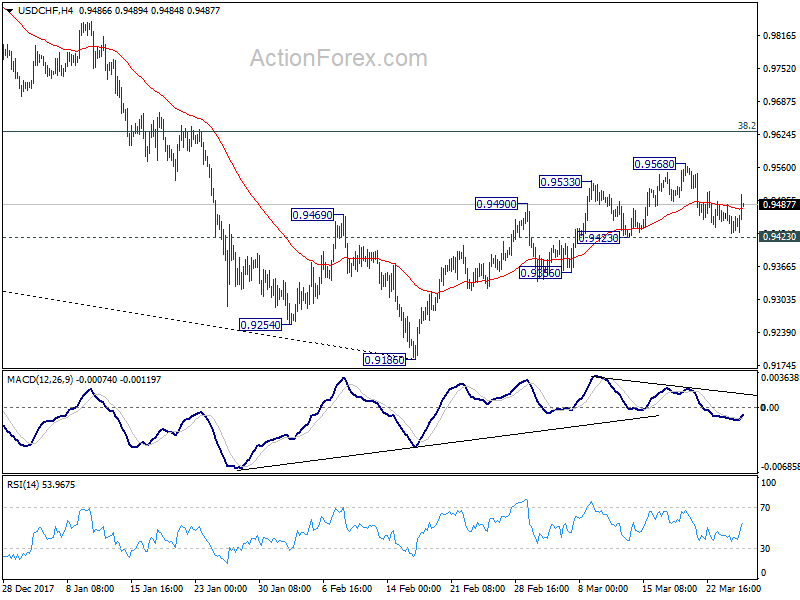

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9442; (P) 0.9469; (R1) 0.9493; More...

USD/CHF recovered ahead of 0.9423 near term support and intraday bias remains neutral. While rebound from 0.9186 might extend higher, we'd expect strong resistance from0.9626 key fibonacci level to limit upside. That's supported by divergence condition in 4 hour MACD. On the downside, break of 0.9432 support will indicate near term reversal and completion of rebound from 0.9186. In this case, intraday bias will be turned back to the downside for retesting 0.9186 low. However, sustained break of 0.9626 will carry larger bullish implications.

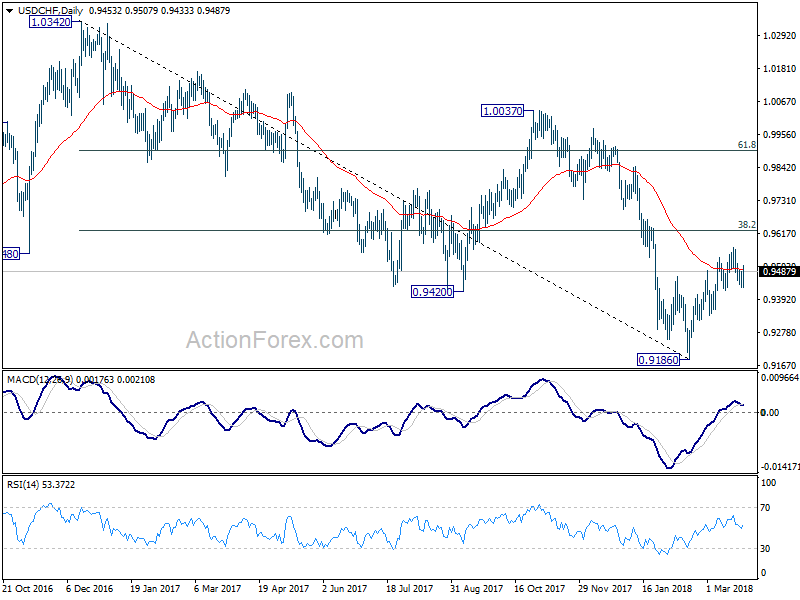

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Dollar Rebounds as Quarter End Position Squaring Starts, Stocks Lifted by Receding Trade War Fear

After being pressured initially, Dollar staged a strong come back European session. The greenback is now trading as the strongest one for day, followed by Canadian Dollar and then Yen. On the other hand, Sterling and Euro are suffering broad based selling together with Aussie. There is no apparent catalyst for the move. Fading fear of trade war, or realizing that the theme is exaggerated, or no matter what it's called, lifted global stocks. At the time of writing, DAX is trading up 1.8%, CAC up 1.4% and FTSE up 2%. If that's true, we should be seeing persistent weakness in Yen, and more rebound in Aussie. But that's not what we're seeing today. It's believed that as holiday approaches and without any real market moving events scheduled, traders are already starting quarter-end position squaring.

European Commission: Economic sentiment weakened in all the five largest euro-area economies

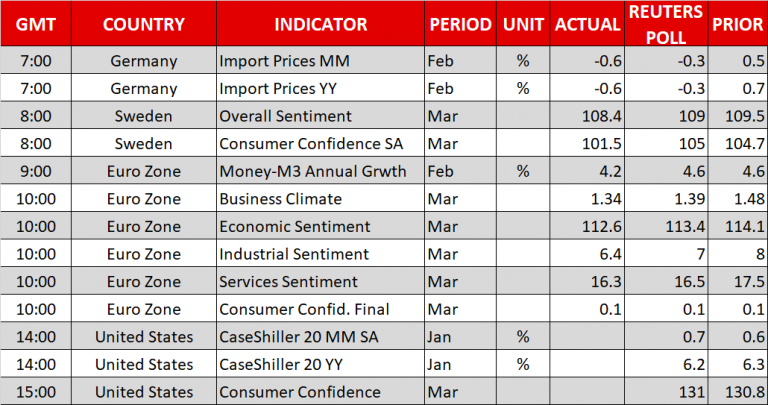

Eurozone economic confidence dropped to 112.6 in March, down from 114.2 and missed expectation of 113.3. In the release, EC noted that the deterioration of sentiment was resulted from drops in industry, services and retail trade. And, the index in all the five largest Eurozone economies also dropped. That includes Germany (-2.4), Italy (-1.8) and Spain (-1.2) and, less so, in the Netherlands (-0.5) and France (-0.4). For EU, economic confidence dropped -1.9 to 112.5. The larger decline in EU was mainly due to marked deterioration of sentiment in the largest non-euro area EU economies, the UK (-4.2), and Poland (-2.0).

Also released from Eurozone, M3 money supply rose 4.2% yoy in February. German import price dropped -0.6% mom in February.

ECB Nowotny: Could reduce asset purchase "significantly" after September

Outspoken ECB Governing Council member Ewald Nowotny commented again today. He said that the central bank will decide on the future of monetary policy in the summer. This is rather apparent as the current EUR 30b per month asset purchase program is set to end in September. Nowotny also said that "if things continue as they are, ECB will be able to reduce asset purchases significantly" after that. While he cautioned not to make any abrupt change to policy, he also emphasized not to fall behind the curve. Overall, Nowotny's comments were consistent with his usual stance, which is slightly on the hawkish side of the spectrum.

ECB Liikanen assures no abrupt sudden changes when QE ends

Another ECB Governing Council member Erkki Liikanen spoke on monetary policy today too. He said that the central bank have been careful in the communications. And he reiterated that "we're extending net asset purchases until September and beyond if needed." He further qualified that "gradual tightening of monetary policy will rest on a more solid basis when indications of inflation rates to potentially temporarily exceed two percent become more prominent in inflation expectations." For Eurozone, "inflation rate is sustainable when the ECB's price stability objective can be met even without an exceptionally accommodative monetary policy".

Regarding the tools, interest rates, asset purchase and forward guidance, he said that " if the economy will be stronger and more convergence will take place, the role of the net asset purchase program will be smaller. And at the same time the other three elements will gain more importance especially forward guidance." But Liikanen assured that "there will be no abrupt sudden changes even if one day the net purchases will be finished."

Fed Mester supports gradual rate hike, against a steep path

Cleveland Fed President Loretta Mester said yesterday that she supports gradual rate hike "this year and next year". At the same time, she's "against a steep path" in tightening because "we want to give inflation time to move back to goal". She sounds optimistic saying that "this year is shaping up to be another good year for the economy." And for monetary policymakers, the task is to "calibrate policy to this healthy economy so that the expansion is sustained."

The government's tax cut poses "some upside risk" to the forecast, and Mester expects a better read on household spending "over the next several months". Globally, she noted that "for the first time in many years, economic activity around the world is picking up and forecasts for global growth are being revised up." And, "this should have a positive feedback effect on the U.S. economy via exports."

Meanwhile, she warned that trade developments are a "risk to the forecasts". And the uncertainty "may not be resolved quickly". But it didn't change her outlook for the over economy yet.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9442; (P) 0.9469; (R1) 0.9493; More...

USD/CHF recovered ahead of 0.9423 near term support and intraday bias remains neutral. While rebound from 0.9186 might extend higher, we'd expect strong resistance from0.9626 key fibonacci level to limit upside. That's supported by divergence condition in 4 hour MACD. On the downside, break of 0.9432 support will indicate near term reversal and completion of rebound from 0.9186. In this case, intraday bias will be turned back to the downside for retesting 0.9186 low. However, sustained break of 0.9626 will carry larger bullish implications.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Y/Y Feb | 0.60% | 0.70% | 0.70% | |

| 06:00 | EUR | German Import Price Index M/M Feb | -0.60% | -0.30% | 0.50% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | 4.20% | 4.60% | 4.60% | 4.50% |

| 09:00 | EUR | Eurozone Economic Confidence Mar | 112.6 | 113.3 | 114.1 | 114.2 |

| 09:00 | EUR | Eurozone Business Climate Indicator Mar | 1.34 | 1.36 | 1.48 | |

| 09:00 | EUR | Eurozone Industrial Confidence Mar | 6.4 | 6.9 | 8 | |

| 09:00 | EUR | Eurozone Services Confidence Mar | 16.3 | 16.5 | 17.5 | 17.6 |

| 09:00 | EUR | Eurozone Consumer Confidence Mar F | 0.1 | 0.1 | 0.1 | |

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Jan | 6.40% | 6.10% | 6.30% | |

| 14:00 | USD | Consumer Confidence Mar | 131 | 130.8 |

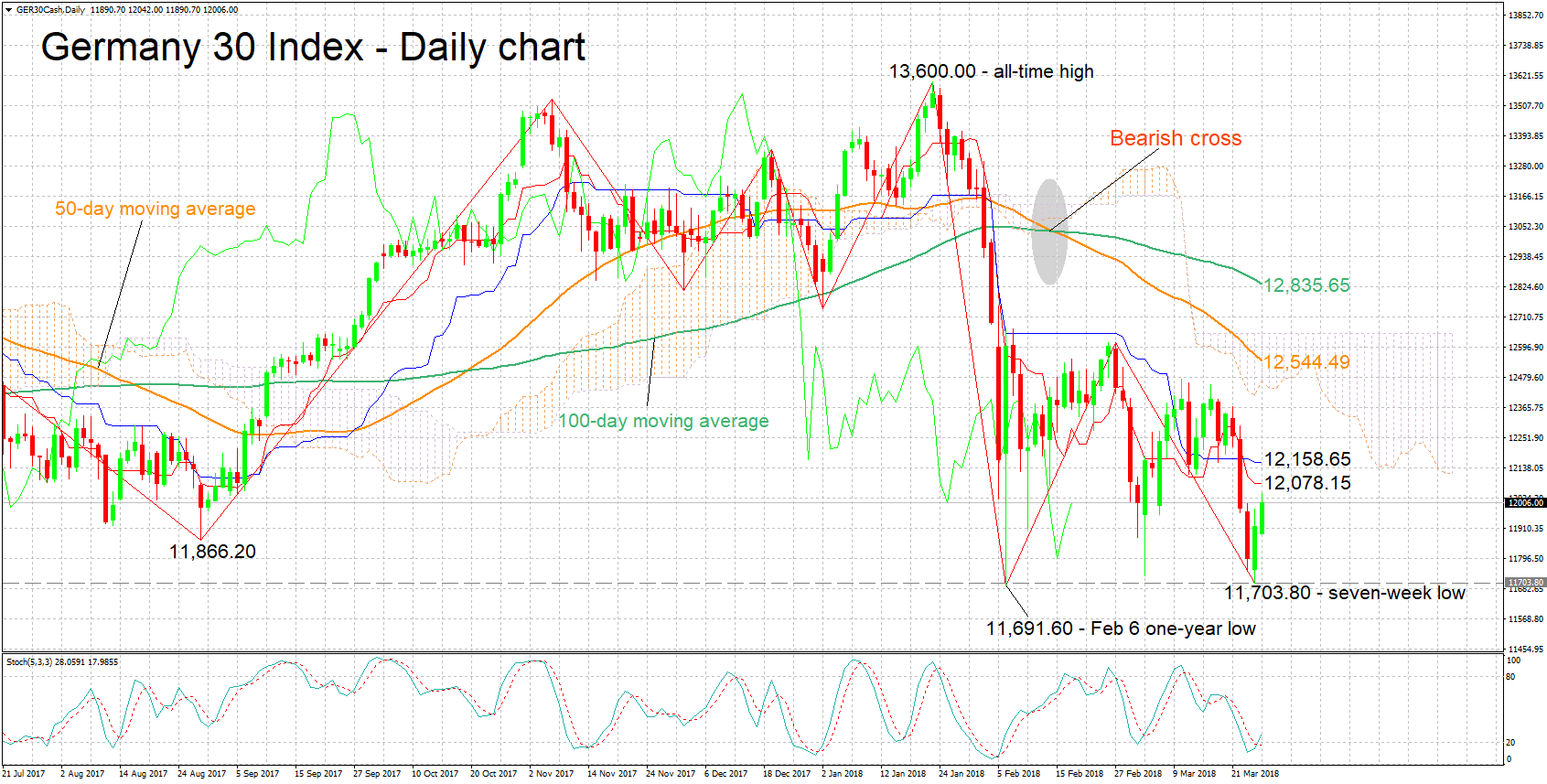

GER 30 Recovers from 7-Week Low to Exceed 12,000 Mark; Bullish Signal by Stochastics in Very Short-Term

The Germany 30 index has rebounded after hitting a seven-week low of 11,703.80 during Monday’s trading. The index ended up gaining 1.0% during yesterday’s trading, while on Tuesday – at the time of writing – it is up by around 0.8%.

The Tenkan-sen line remains below the Kijun-sen line in support of a negative short-term bias, though the Kijun-sen has flatlined, an indication that downside short-term momentum is running out of steam. Moreover, the stochastics are giving a bullish signal in the very short-term as the %K line has crossed above the slow %D one and is heading higher.

Further advances might meet resistance around the current levels of the Tenkan- and Kijun-sen lines at 12,078.15 and 12,158.65 respectively, with the area around the Ichimoku cloud bottom at 12,466.52 next coming into view as an additional barrier to the upside – this area was a rather congested one recently.

In case of declines, the range around a previous bottom at 11,866.20, that also encapsulates the 11,900 round figure, might provide support. Further below, the attention would shift to the range around yesterday’s seven-week low of 11,703.80 for additional support, with the one-year low of 11,691.60 from February 6 also being part of this area.

The medium-term picture is looking negative, with price action taking place below the 50- and 100-day moving average lines, as well as below the Ichimoku cloud. A bearish cross was also recorded around mid-February when the 50-day MA moved below the 100-day one.

Overall, the short-term bias is looking partially bearish – though a bullish signal is in place in the very short-term – with the medium-term outlook looking negative at the moment.

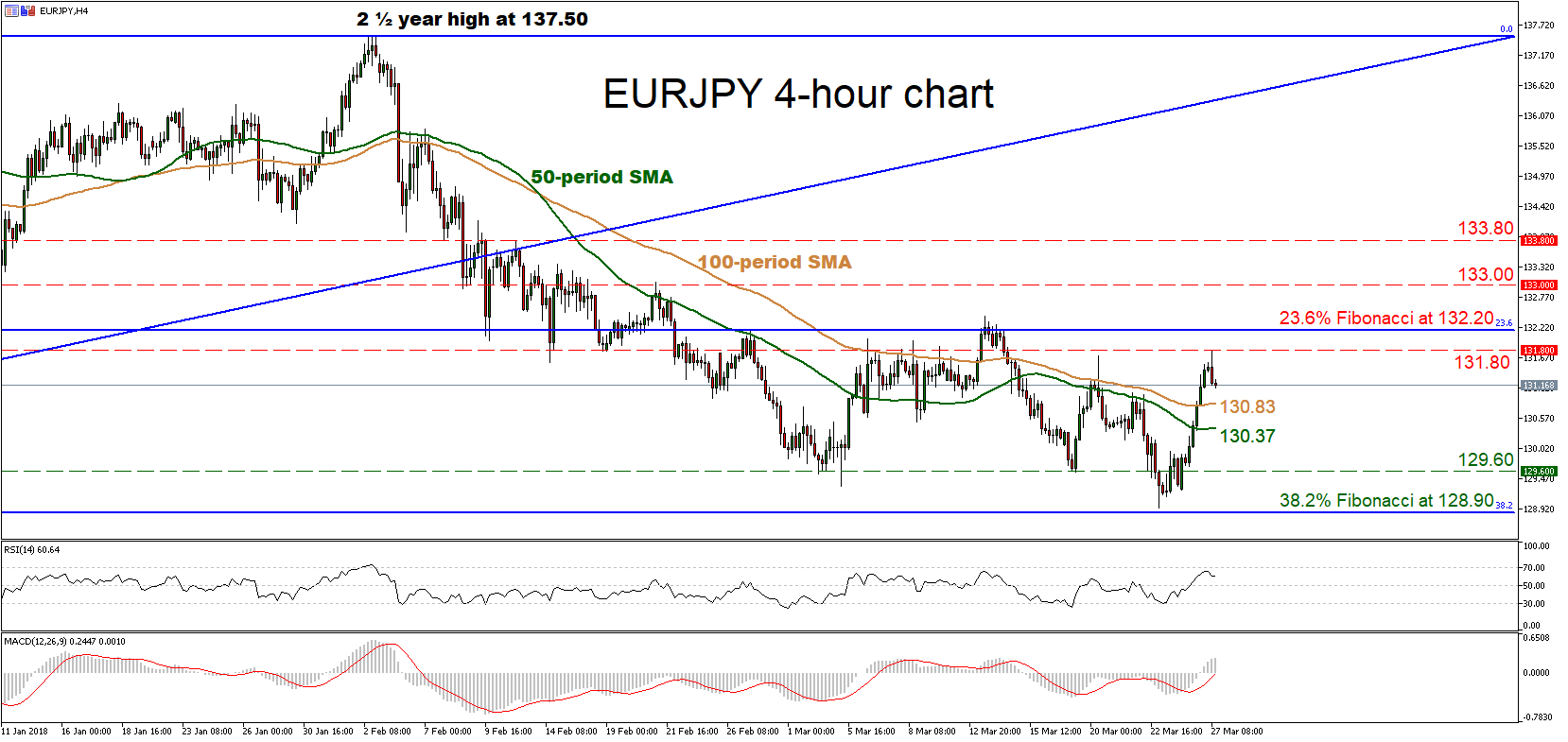

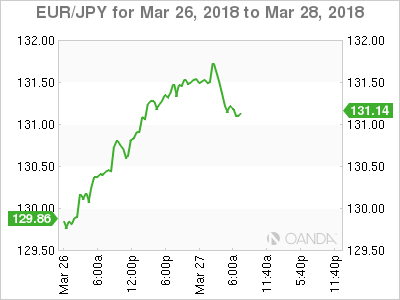

EURJPY Bounces from Recent Lows, Attempts to Break Higher

EURJPY rebounded on Friday, after touching a 7-month low of 128.90. The pair surged to encounter resistance at the 131.80 barrier earlier today and has since pulled back somewhat, currently trading near 131.20. Despite the latest bounce though, EURJPY is still 4.5% lower from its 2 ½ – year high of 137.50 reached in early February.

Looking at momentum oscillators, in the 4-hour chart, the Relative Strength Index (RSI) is above its neutral-perceived 50 level detecting positive momentum, though it met resistance near its 70 line and has turned down somewhat. Meanwhile, the MACD lies in positive territory and is also above its trigger line. Combined, these paint a cautiously positive picture for the pair in the near-term, something supported by the price action being above both the 50 and the 100-period moving averages.

In case of further advances in the pair, immediate resistance may be found near the latest top, at 131.80. Further bullish extensions could stall near the 132.20 area, which is the 23.6% Fibonacci retracement of the April 2017 – February 2018 upleg, from 114.80 to 137.50. A decisive break above that zone would mark a higher high on the 4-hour chart, which could set the stage for further gains, initially towards the 133.00 barrier, marked by the highs of February 21.

On the flip side, if the bears retake control, support can come near the 50 and 100 period moving averages, at 130.83 and 130.37 respectively. More declines would open the way for the 129.60 hurdle, identified by the lows of March 19, and subsequently for the pair’s recent bottom at 128.90, which is also the 38.2% of the aforementioned Fibonacci retracement. A downside violation of 128.90 would mark a fresh lower low, increasing the likelihood for more bearish extensions. In such case, buy orders may be found near 127.55, the August 2017 low.

Euro, Pound Erase Gains; European Equities Cheer on Trade Hopes

Here are the latest developments in global markets:

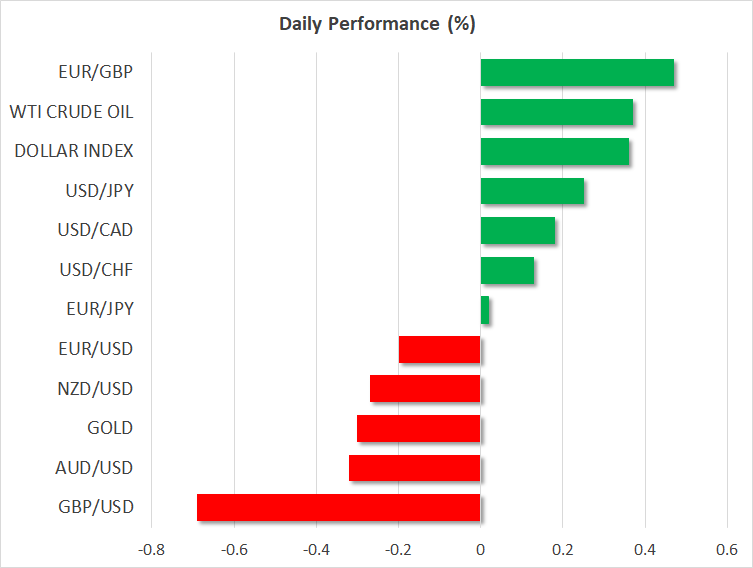

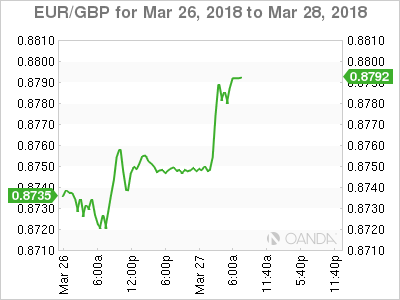

FOREX: Dollar/yen held strong at 105.63, trading at five-day highs during the early European afternoon, underpinned by hopes that a trade war between the US and China could be averted based on encouraging comments made by US and Chinese authorities in recent days. Not so hawkish remarks delivered by the Atlanta’s Fed President, Raphael Bostic (a centrist voting member) pressured the pair temporarily after Bostic said in an interview with the Wall Street Journal published today that tax cuts might boost growth but not inflation. The dollar index, which tracks the greenback’s strength against a basket of six major currencies, rebounded sharply from a more than a five-week low of 88.94 to an intra-day high of 89.35 as the euro and the pound erased today’s gains and were on track to finish the day in the red. The weakness in euro/dollar appeared after ECB member Erkii Liikanen took a cautious stance over an early monetary tightening, while disappointing data on the Eurozone’s economic sentiment in March added further losses to the currency. Meanwhile in the UK, the BOE Financial Committee policy meeting minutes showed that policymakers were considering to raise the amount of capital banks must put aside to mitigate unexpected shocks, arguing that risks have increased since the committee set the countercyclical buffer at 1.0% in Q1 2016. Euro/dollar and pound/dollar dropped to 1.2400 (-0.33%) and 1.4108 (-0.86%) respectively, while euro/pound extended upwards to 0.8791 (+0.55%). Against the yen, the pound lost the most compared to the euro, falling by 0.55%, while the euro was flat. Aussie/dollar and kiwi/dollar gave up gains as well, slipping to 0.7708 (-0.48%) and 0.7268 (-0.41%) respectively.

STOCKS: European equities opened substantially higher on Tuesday, following their Asian counterparts as investors felt more confident to put some money on riskier investments. The pan-European STOXX 600 was set to post its best day in seven weeks, surging by 1.34% at 1030 GMT, while the blue-chip Euro STOXX 50 was rising faster by 1.63% with all sectors being in the green. The German DAX 30 was up by almost 2.0%, the French CAC 40 jumped by 1.48% and the Italian FTSE MIB increased by 1.45% despite political uncertainties weighing in the background. The UK’s FTSE bounced off one-year lows, recouping losses made in the past four sessions. Asian equities maintained upside momentum, while US stock index futures were pointing to another upbeat trading on Tuesday.

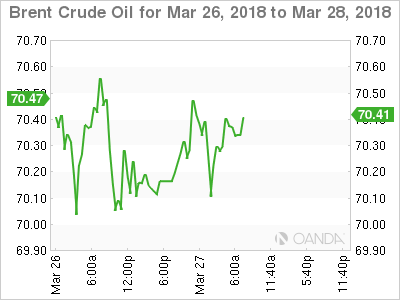

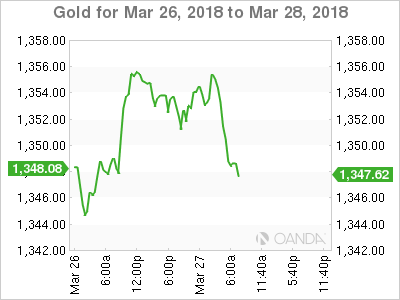

COMMODITIES: Geopolitical risks in Middle-East and Venezuela, Libya and more importantly in Iran, as well as compliance by OPEC/non-OPEC members on the deal to reduce supply, continued to support oil prices. WTI crude was last seen at $65.76/barrel (+0.35%) after hitting a session high of $65.99 earlier in the day, while the London-based Brent peaked at $70.47/barrel (+0.33%). In precious metals, gold dived from a five-week high of $1,365.66/ounce touched during the Asian session to trade at $1,348.90/ounce.

Day ahead: US Conference Board Consumer Confidence index pending

Day ahead: US Conference Board Consumer Confidence index pending

Economic releases will be limited during the rest of the day as a long Easter holiday weekend is approaching, with the US publishing readings on house prices and consumer confidence. Trade headlines during the day, however, could be more important for the markets as investors are eagerly waiting to see how the trade row story will play out, as risk-off sentiment continues to ease after the US and China expressed willingness to push forward negotiation.

At 1400 GMT, the S&P/Case-Shiller house price index will come into view, probably showing that house prices in 20 of the largest US metropolitan areas have slightly weakened in yearly terms in January but inched up month-on-month. An hour later, the Conference Board Consumer Confidence gauge is expected to rise to 131.0 in March compared to 130.8 in the previous month, posting a fresh 17-year high.

In energy markets, the American Petroleum Institute will publish its regular weekly report on US crude oil stocks at 2130 GMT. Oil prices have surged significantly over the last two weeks on the back of a weaker dollar and escalating tensions in the Middle East, touching two-month highs yesterday and any decline in API readings could add further gains to the market (no forecasts exist for the measure). This could somewhat ease concerns that increases in US output could harm efforts from OPEC/non-OPEC countries to curb oil’s supply glut.

Regarding today’s public appearances, Atlanta’s Fed President, Raphael Bostic, will participate in conversation before the HOPE Global Forums 2018 Annual Meeting at 1600 GMT.

Canadian Dollar Dips, Markets Await US Consumer Confidence

The Canadian dollar has posted gains in the Tuesday session. Currently, USD/CAD is trading at 1.2881, up 0.30% on the day. On the release front, there are no Canadian indicators. In the US, CB Consumer Confidence is expected to rise to 131.2 points. On Wednesday, the US releases Final GDP.

Last week was positive for the Canadian dollar, which posted gains of 1.6 percent. The Canadian currency gained ground on Friday, after strong consumer data. CPI, ticked lower to 0.6% but beat the estimate of 0.4%. Retail Sales rebounded with a gain of 0.9%, after a sharp loss of 1.8% in the previous release. This reading matched the estimate. There was positive news in the US as well, as durable good reports beat their estimates. A stronger US economy means a larger demand for Canadian exports, which is good news for the Canadian dollar.

Concerns over a possible global trade war have eased this week, after China filed applications with the World Trade Organization regarding US tariffs on Chinese products. China has objected to the US claim that the tariffs were imposed on national security grounds. Rather, China says that the US simply applied trade restrictions in order to protect domestic steel producers. Last week, President Trump announced that the US would impose tariffs on up to $60 billion worth of Chinese imports, and China has threatened to retaliate. These moves sent the markets lower, as the specter of a downturn in the Chinese economy and the possibility of a global recession weighed on investor risk appetite.

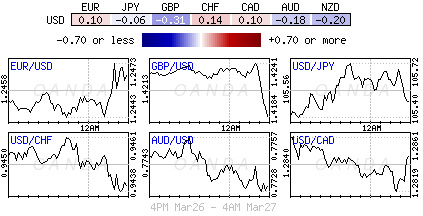

USD in counter trend rebound as buying emerges in European session

Buying emerges for USD in European session as seen in the 4H heatmap. And that also majors USD as the strongest one for the day.  H action bias of dollar also turned all up. (EUR/USD, GBP/USD, AUD/USD, NZD/USD down means USD up, just in case).

H action bias of dollar also turned all up. (EUR/USD, GBP/USD, AUD/USD, NZD/USD down means USD up, just in case).

However, it should be noted that firstly, 6H action bias of USD is all neutral. Indeed, USD is in down action bias against EUR and GBP in daily chart. USD is also in down action bias against JPY, GBP and CAD in weekly chart. Hence, the momentum across time frame is not consistent. That means, the current rebound in dollar in counter trend.

However, it should be noted that firstly, 6H action bias of USD is all neutral. Indeed, USD is in down action bias against EUR and GBP in daily chart. USD is also in down action bias against JPY, GBP and CAD in weekly chart. Hence, the momentum across time frame is not consistent. That means, the current rebound in dollar in counter trend.

For example, for GBP/USD's we'd prefer to see a break of 1.4075 before weighing the chance of a near term reversal. Otherwise, GBP/USD is seen as in a correction only.

What Trade War Fears?

Risk appetite is finding traction thanks to diplomatic tones as U.S officials indicated efforts to diffuse rising trade tensions between the world’s two largest economies.

This week, U.S stocks have rallied aggressively from their biggest weekly rout in 24-months, with major benchmarks climbing more than +3% on signs that an escalation of global trade tensions was beginning to ease.

Stateside, financials and technologies led gains yesterday as the S&P 500 index tested its biggest one-day rally since the summer of 2015. Monday’s rally erased Friday’s drop, though the gauge still had a ways to go to make up all of last week’s losses.

Elsewhere, the U.S 10-year Treasury yield has climbed ahead of this week’s major debt sales, while the ‘big’ dollar has dropped to a five-week low.

U.S President Trump’s administration is urging China to lower tariffs on cars and to open its market to U.S financial services as part of talks to resolve a rise in trade tensions that has shaken global markets.

Note: U.S Treasury Secretary Mnuchin and Liu He, China’s vice premier in charge of economic policy are committed to finding a mutually agreeable way to reduce the trade deficit.

1. Stocks in the ‘black’

In Japan, equities have rallied sharply overnight as immediate concerns about trade frictions between the U.S and China abated. The Nikkei ended +2.7% higher, while the broader Topix advanced +2.6%.

Down-under, Aussie shares climbed on Tuesday on a surge in base metal and oil prices, as trade war fears eased on reports and indications that the U.S and China are willing to renegotiate tariffs and trade imbalances. The S&P/ASX 200 index was up +0.7% at the close of trade. In S. Korea, the Kospi was up +0.6%.

In Hong Kong, stocks join global market rebound as trade war fears ease. The Hang Seng index rallied +0.8%, while the China Enterprises Index gained +0.9%.

In China, stocks snapped a four-session losing streak to end higher overnight, powered by robust gains in tech firms, and as trade war fears eased on reports of behind-the-scenes talks between the U.S and China. At the close, the Shanghai Composite index was up +1%, while the blue-chip CSI300 index was up +0.86%.

In Europe, regional indices trade sharply higher overnight, mirroring Wall Street and Asian gains on easing fears of an U.S/China trade war.

U.S stocks are set to open in the black (+0.6%).

Indices: Stoxx600 1.3% at 367.7, FTSE +1.6% at 6999, DAX +1.4% at 11976, CAC-40 +1.3% at 5133, IBEX-35 +1.0% at 9473, FTSE MIB 1.4% at 22307, SMI +1.5% at 8639, S&P 500 Futures +0.6%

2. Oil holds above $70 as geopolitics eclipses supply outlook, gold higher

Oil rallied overnight, holding above +$70 a barrel for a third consecutive day, supported by concerns that tensions in the Middle East could lead to supply disruptions.

Brent crude futures are up +28c on the day at +$70.40 a barrel, while West Texas Intermediate (WTI) crude futures are up +19c at +$65.74 a barrel.

Note: The oil price has risen by more than +7% so far this month and by +5.3% in Q1, 2018, putting it on track for a third consecutive quarterly gain, something the market has not witnessed since late 2010.

Geopolitics and expectations of the world’s largest exporters controlling supply have helped push Brent above +$70 this year for the second time since late 2014, but analysts said this strength may not persist for long.

Price strength of the last couple of weeks is down to two factors; the first one is a stable OPEC output level and the second one is supply-side geopolitical developments in Venezuela, Libya and Iran.

Note: Capping prices is U.S production; shale oil drilling has already grown by nearly +25% in under 24-months to above +10m bpd.

Ahead of the U.S open, gold prices have rallied for a third consecutive session overnight as the dollar sank to a new five-week low, as capital markets eyed rising tensions between Russia and the West even as a U.S/China trade spat appeared to ease. Spot gold is up +0.16% percent at +$1,355.19 per ounce, after touching +$1,356.66 earlier in the session.

3. Sovereign yields trade in narrow range

Narrow ranges across Bunds and most Euro and U.S spreads amid lower volumes suggest that the fixed income market has already entered Easter mode.

German Bund yields continue to trade in a narrow range and this is expected to remain slow in the short week ahead of Easter. The 10-year Bund yield is trading at +0.53%, up about +1 bps.

Note: Bunds will not get any input from supply, as there is not a scheduled bond sale in the eurozone today.

Stateside, product is plentiful. There is another +$89B of U.S bills for sale today and +$35B of five-year notes.

Note: The U.S Treasury is expected to auction about +$294B of bills and notes this week, its largest slate of supply ever.

Yesterday’s U.S Treasury +$51B 3-month sale drew a yield of +1.76%, with a bid-to-cover ratio of 2.98. A +$45B 6-month bills drew +1.895%, bid-to-cover yield of +3.06%. Re-the 3-month auction, +60.3% allotted at the high, while the 6-month, +90.7% allotted at the high-

Elsewhere, the yield on U.S 10-year Treasuries declined -1 bps to +2.84%. In the U.K, the 10-year Gilt yield dipped -1 bps to +1.449%, the lowest in two-months. In Germany, the 10-year Bund yield decreased -1 bps to +0.52%, the lowest in 11-weeks.

4. Dollar finds some traction

Risk appetite is on the rise.

Ahead of the open stateside, the USD tentatively probed its recent weekly lows against its Euro pairs, but saw its fortunes do a U-turn as the session wore on. The ‘mighty’ buck remains well well contained within its 2018 trading range.

The EUR/USD (€1.2414) initial probed the upper end of its Q1 price range, but has since drifted from its intraday highs after the ECB’s Liikanen cautioned about “tightening policy too soon” and reiterated that the Council’s view that “patience and persistence” was needed. The single currency also came under pressure from softer data in this morning’s session.

Spain’s March preliminary CPI data came in below expectations – y/y +1.2% vs. +1.4%e, while the Eurozone’s M3 Money Supply missed – +4.2% vs. +4.6%e. European confidence data was also retreating from recent cycle highs (see below).

GBP/USD (£1.4115) has been unable to sustain holding above the psychological £1.42 level as cross-related selling in EUR/GBP weighed down the pound sterling.

5. Eurozone economic sentiment weakens

Earlier today, the European Commission said its economic sentiment indicator fell to 112.6 from 114.2 in February, hitting its lowest level since September 2017.

The market was expecting a drop to 113.4.

Digging deeper, businesses across the eurozone were less upbeat about their prospects in March, while bank lending to companies slowed in February, which could suggest that E.C economic growth may have passed its peak.

Note: The survey was undertaken when the E.U was threatened by new U.S tariffs on steel and aluminum.

The weakening of sentiment during March was spread across the manufacturing, services and retail sectors, while construction companies became more upbeat.

The ECB said bank lending to businesses grew +3.1% on the year in February, following +3.4% growth in January, when lending expanded at the fastest rate since May 2009. The slowdown may reflect a weakening of business confidence related to trade worries, and prove temporary.

Euro Dips, US Consumer Confidence Next

EUR/USD has posted slight losses in the Tuesday session. Currently, the pair is trading at 1.2412, down 0.30% on the day. On the release front, German Import Prices declined 0.6%, weaker than the estimate of -0.3%. This marked the first decline since July. In the US, CB Consumer Confidence is expected to rise to 131.2 points. On Wednesday, Germany GfK Consumer Climate and the US publishes Final GDP.

The ECB will stay the course with regard to its stimulus program, according to a senior ECB policymaker. Governing Council member Erkki Liikanen said on Tuesday that if eurozone growth remains robust, inflation could remain lower than expected. With the current bond purchase program set to expire in September, there is speculation that the ECB will wind up the program, after years of pursuing an accommodative policy. If inflation does move closer to the ECB’s target of around 2 percent, there is a greater likelihood that the bank will not extend stimulus, and could entertain raising interest rates in 2018.

The business sector continues to have strong confidence in the German economy, but there is concern about possible headwinds due to recent tariffs imposed by the Trump administration. The German Ifo Business Climate report dipped to 114.7 in March, which matched the forecast. However, this marked a second straight drop, and was the lowest reading in 11 months. The report attributed lower business morale to concerns that tariffs could hurt transatlantic trade, as well as the negative impact of a stronger euro. On the bright side, tax reform in the US and the economic rebound in the eurozone have increased the demand for German goods and services.