Sample Category Title

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8736; (P) 0.8766; (R1) 0.8789; More...

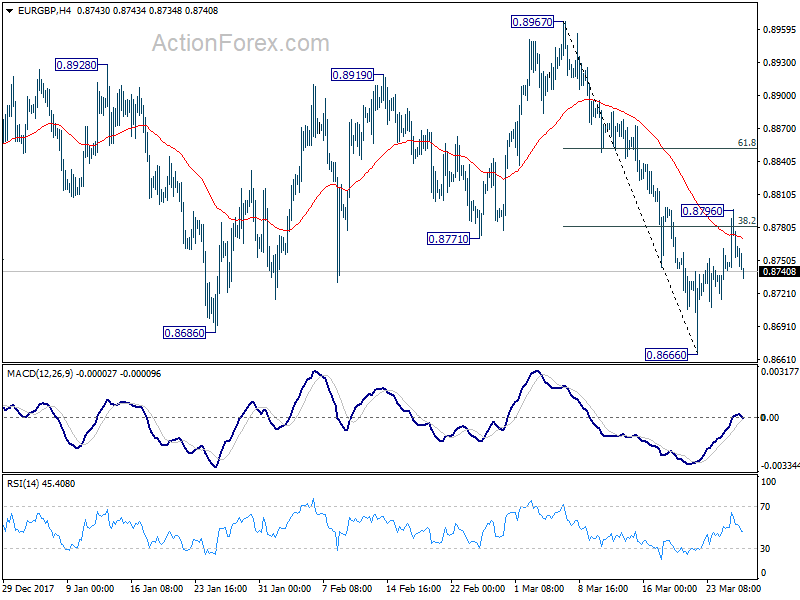

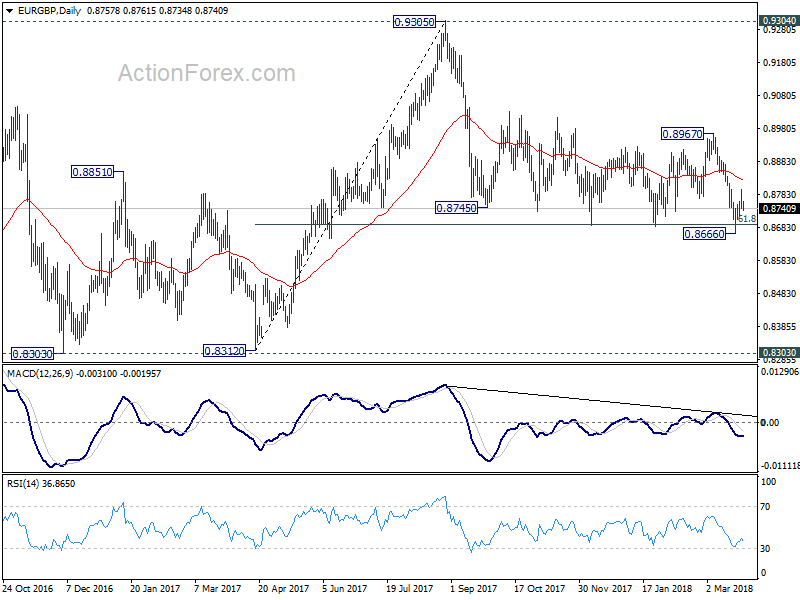

EUR/GBP rebounded to 0.8796 but failed to sustain above 38.2% retracement of 0.8967 to 0.8666 at 0.8781 and retreated. Intraday bias is turned neutral first. As EUR/GBP was supported by 0.8686 key support level, we'd slightly favoring the case for further rebound. On the upside, above 0.8796 will target 61.8% retracement at 0.8852 and above. Nonetheless, on the downside, firm break of 0.8666 will resume the decline from 0.9305 and pave the way to 0.8303 key support zone next.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

US- China Trade Tensions: Trump’s Soap Opera to Get Better Deal

Over the past months, US trade policy has been a major cause of the wax and wane of the financial markets. The White House has triggered a number of investigations under the rarely used 1972 US trade law since Trump took office. All investigations have resulted in tariff imposition, claiming to be targeting China. While Trump's tariff vow is indeed consistent with his brinkmanship foreign policy practice (pushing everything to an extreme in order to gain bargaining power), we notice that the tariffs announced are merely threats and do not intend to pose actually impact on Chinese economy.

Let's have a review of the White House's recent trade investigations and measures:

1. Section 232 investigations on steel, aluminum, and uranium – Reports on two investigations done on steel and aluminum imports last year were submitted to the president in January. Trump eventually signed orders to impose 25% tariff on steel imports and 10% on aluminum imports. Interestingly, despite the claim to target its biggest trading partner, China is only the 10th largest source of US steel imports, accounting for just 2% total US steel imports last year. The White House knows more than anyone else that China has reduced its steel exports to the US by a third after the then-president Barack Obama's 500% steel tariff imposed in 2016. Chinese steel producers have shifted its focus from the US to Asia markets since then. China ranks number 3 as US aluminum imports. Yet, the impost amount has also been down -11% from last year.

In response, China last week announced plans to impose tariffs on 128 US products that include pork, wine, fruit and steel. It has revealed that tariff on US soy exports would be the last resort and the biggest bullet as about one-third of Chinese soy imports comes from the US. However, this would be an internecine scenario as tariff on US soy exports would raise the cost of some Chinese producers.

The biggest losers of the tariff plan would be Canada, Mexico and certain Eurozone members. However, US plan to exempt these countries has alleviated the concerns of producers from these countries. The exemptions have also reduced the tariff to something symbolic. Undoubtedly, shares of US steel and aluminum companies slumped after Trump's announcement of a light version of the tariff plan earlier this month.

2. Section 201 investigations on solar panels and washing machines – the investigations resulted in tariffs on washing machines and solar panels announced on January 22. Imported washing machines would be subject to a 20% tariff for the first 1.2M units/ year, and 50% for units above that level (for 3 years). Imported solar panels would be subject to a tariff of 30% for the next 4 years, with an exemption for the first 2.5 gigawatts of imports per year. The measures are claimed to target China and South Korea, shipments from both sectors contribute less than 5% to the overall exports from either country to the US.

3. Section 301 investigations on China's intellectual property and technology transfer – US last week announced tariffs on Chinese imports, worth about US $60B, in response to China's of US technology and intellectual property. The measures target goods including clothing, shoes, and electronics and restrict some Chinese investment in the US.

US announcement of the latest tariff plan was shortly followed by China's retaliatory policy (mentioned above). This dramatically led to negotiations between the two parties with US Commerce Secretary Wilbur Ross affirming the market that the country and China were "ending up with negotiated deals, not trade wars". Ross, however, added that there would be limitations on foreign investment" and President Donald Trump would take "other action" on foreign takeovers. Indeed, there have been reports suggesting that the US was looking to protect the domestic tech sector by curbing investment from China, by using an emergency law.

There are practical reasons the US to show a tougher stance on trade policy recently. The mid-term election in November is approaching with all House seats and 34 senate seats re-elected. Given a number of failure, including Republican's loss of the Alabama seat for the first time in 25 years, since he took office, Trump is obliged to impose measures that are appealing to his supporters. Indeed, various US industries have been complaining about China's business practices, which are deemed to be unfair for foreign companies. For instance, pharmaceutical companies have complained that it takes over two years to get drug license in China. Meanwhile testing procedures are no compliant with international standards. For decades, credit card business in China remains monopolized by Union Pay which is sole provider of renminbi clearing services for bankcard transactions. This has prohibited Master/ Visa from tapping the Chinese market.

We would not feel surprise to see more announcements on trade barriers in the months ahead. While the trade news might cause market volatility, we do not believe the measures are intended to hurt the trade relations between the US and China.

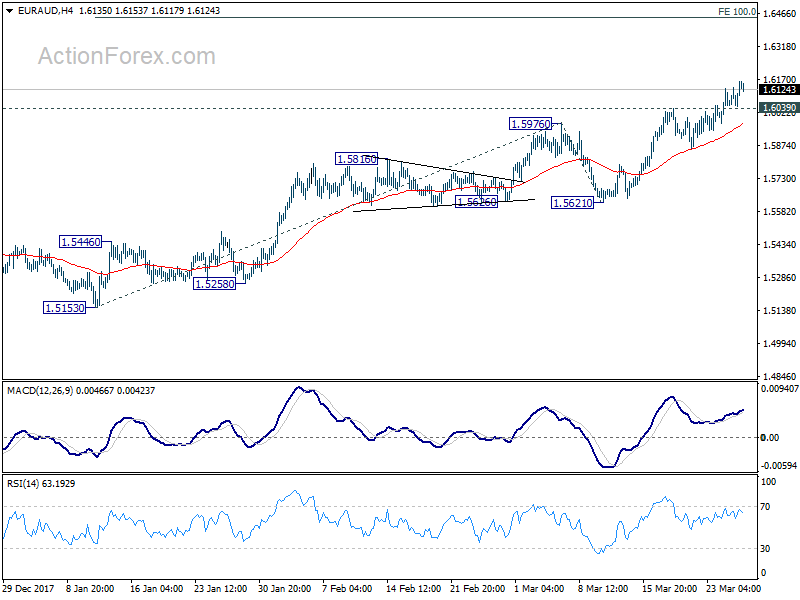

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6081; (P) 1.6121; (R1) 1.6189; More....

EUR/AUD's rally is still in progress and intraday bias remains on the upside. Current rise should target 100% projection of 1.5130 to 1.5976 from 1.5621 at 1.6444 next. On the downside, below 1.6039 minor support will turn intraday bias neutral and bring consolidation first. But retreat should be contained well above 1.5621 support to bring rally resumption.

In the bigger picture, current development suggests that rise from 1.3624 is not completed yet. And it's still in progress for 1.6587 key resistance level. We'd be cautious on strong resistance from there to limit upside, on bearish divergence condition in daily MACD. But for now, break of 1.5621 support is needed to be the first sign of medium term reversal. Otherwise, outlook will stays bullish even in case of deep pull back.

Euro Stays Strong after Volatility in Thin Holiday Markets

There was some volatility seen yesterday in the forex markets. But as dusts settled, Euro is staying as the strongest one for the week, followed by New Zealand Dollar and Sterling. On the other hand, Yen and Dollar are trading as the weakest one, followed not too far away by Australian Dollar. No important levels of dollar pair were broken with yesterday's moves. EUR/USD and GBP/USD retained near term bullishness for further rise. And, USD/JPY is staying bearish. As liquidity continues to drop ahead of holiday, we might see more such volatility ahead.

In the stock markets, DOW initially gained 244 pts to 24446.22 but reversed to closed down -344.89 pts or -1.43% at 23857.71. Considering that it hit as low as 23708.73, that was indeed a massive 737 pts swing. The reversal was mainly because tech stocks were crushed. S&P 500 lost -45.93 pts or -1.73% to 2612.62. NASDAQ suffered most and closed down -211.73 pts or -2.93% at 7008.81.

Facebook was downgraded by Bank of America Merrill Lynch. Its CEO Mark Zuckerberg would testify before the US Congress on the data privacy scandal. Facebook dropped -4.9%. Meanwhile, Twitter slumped 12% after Citron Research said it was short the stock while Nvidia was down -7.8% after the company suspended self-driving tests. While US-China trade friction has shown signs of cooling, it was reported that the US might still restrict technology investment from China.

Selloff continues in Asia with Nikkei down -1.9%, HK HSI down -1.5% at the time of writing.

Kim met Xi ahead of summit with Moon in April and Trump in May

It's confirmed that North Korean leader Kim Jong-un has taken his first know foreign trip as president this week. And he met with Chinese President Xi Jinping and other officials in Beijing. It's seen as a symbolic visit of courtesy ahead of Kim's planned meeting with South Korean President Moon Jae-in in April, and US President Donald Trump in May. Kim should have explained his positions regarding the summits and sought China's position too.

The issue of denuclearization of the Korean Peninsula is something that leaders from the US, South Korea and China would like to resolve in the coming months. White House press secretary Sarah Huckabee Sanders hailed themselves that "we see this development as further evidence that our campaign of maximum pressure is creating the appropriate atmosphere for dialogue with North Korea".

On the other hand, China's Xinhua news agency reported Kim saying that "the issue of denuclearization of the Korean Peninsula can be resolved, if South Korea and the United States respond to our efforts with goodwill, create an atmosphere of peace and stability while taking progressive and synchronous measures for the realization of peace."

US to restrict tech sector investment from China

As the market gauging the developments of US-China trade tensions, US Commerce Secretary Wilbur Ross told Fox News that the country and China were "ending up with negotiated deals, not trade wars". However, there were reports suggesting that the US was looking to protect the domestic tech sector by curbing investment from China, by using an emergency law. Indeed, that the Fox interview, Ross noted that there will be "limitations on foreign investment" and President Donald Trump would take "other action" on foreign takeovers.

New Zealand business confidence suggests 2-3% annual growth

New Zealand ANZ business confidence dropped to -20 in March, down from -19. That means a net 20% of businesses are pessimistic about the year ahead. ANZ noted in the release that "headline business confidence and firms' views of their own activity have trodden water in March, both little changed from the preceding month." Also, "belying the headline measures somewhat, all key activity indicators improved further, albeit while remaining well off their cycle highs." Also, "pricing indicators were broadly steady". ANZ also indicated that the growth indicator, which combines business and consumer confidence, continues to suggest growth around 2-3% y/y.

Looking ahead

German Gfk consumer confidence and UK CBI reported sales will be featured in European session. US will release trade balance, wholesale inventories, pending home sales and Q4 GDP final.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6081; (P) 1.6121; (R1) 1.6189; More....

EUR/AUD's rally is still in progress and intraday bias remains on the upside. Current rise should target 100% projection of 1.5130 to 1.5976 from 1.5621 at 1.6444 next. On the downside, below 1.6039 minor support will turn intraday bias neutral and bring consolidation first. But retreat should be contained well above 1.5621 support to bring rally resumption.

In the bigger picture, current development suggests that rise from 1.3624 is not completed yet. And it's still in progress for 1.6587 key resistance level. We'd be cautious on strong resistance from there to limit upside, on bearish divergence condition in daily MACD. But for now, break of 1.5621 support is needed to be the first sign of medium term reversal. Otherwise, outlook will stays bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | NZD | ANZ Business Confidence Mar | -20 | -19 | ||

| 6:00 | EUR | German GfK Consumer Confidence Apr | 10.7 | 10.8 | ||

| 10:00 | GBP | CBI Reported Sales Mar | 7 | 8 | ||

| 12:30 | USD | Advance Goods Trade Balance Feb | -74.1B | -75.3B | ||

| 12:30 | USD | Wholesale Inventories M/M Feb P | 0.50% | 0.80% | ||

| 12:30 | USD | GDP Annualized Q/Q Q4 T | 2.70% | 2.50% | ||

| 12:30 | USD | GDP Price Index Q4 T | 2.30% | 2.30% | ||

| 14:00 | USD | Pending Home Sales M/M Feb | 2.00% | -4.70% | ||

| 14:30 | USD | Crude Oil Inventories | -2.6M |

Market Morning Briefing: Pound Saw An Unexpected Low Near 1.4066

STOCKS

Dow (23857.71, -1.43%) had attempted a rise from 23500 but could not sustain. The index fell back to 23700 yesterday, re-testing the near term support. Watch price action here as a break or bounce from current levels would decide the further course of direction.

Dax (11970.83, +1.56%) did bounce back from 11700 as expected but does not show signs of bullishness just now. Although there is scope on the upside towards 12200-12300 levels, Dax could see a dip from 12050-12100 levels itself again heading back towards 11800-11700 region. Watch price action near current levels.

Nikkei (20939.59, -1.77%) opened at lower levels today after the sharp rise to 21317 yesterday. Currently trading below 21000, Nikkei could be stuck in the broad 21200-20200 region for the near to medium term.

Shanghai (3147.91, -0.59%) opened with a gap up with an attempt to rise higher yesterday but has come off from there again to levels below 3150. If a rise does not take the index back above 3200, the index could gradually lose its upside momentum leading to a medium term sideways consolidation.

10220-10260 could be a decent resistance zone just now which could push Nifty (10184.15, +0.53%) to lower levels. Some stability is possible today likely to end the month below 10260.

Sensex (33174.39, +0.33%) is also likely to come off from 33500, the immediate channel resistance as seen on the daily candles. While that holds, April could possible begin with a dip in the index.

COMMODITIES

Brent (69.68) and Nymex WTI (64.77) are down as expected. WTI could head towards 64 before rising past 66.50 while Brent could come off to 69-68 levels.

Gold (1346) tested 1357 on the upside and came off from there in line with our expectation. A fall to 1340/1330 is possible before trying to move up again in the medium term.

Copper (2.9955) has come off from levels below 3.04 and while it trades lower, there could be chances of coming down to 3.95/90. Some consolidation is possible below 3.04 today.

FOREX

Dollar index (89.27) hasn't yet decisively broken the crucial long term support on weekly line chart near 89.2-89.4. If this support is broken the Dollar Index could turn bearish in the medium term after having ranged in the 88.5-91.0 region for the past 10 weeks. The next downside target would be horizontal support near 88.5 on daily candles. The US GDP data release today could be important – a favorable GDP growth figure could be positive for Dollar strength.

Euro (1.2417) – As mentioned yesterday, there is crucial long term resistance near 1.245 on the weekly line chart which might be pushing the Euro down. A breach of this level would be bullish for the Euro and it could then target 1.255-1.26, seen as horizontal resistance on 3 day candles.

Dollar Yen (105.57) , as predicted yesterday, was pushed down by immediate resistance near 106 on the daily candles and could move down towards 104.5 again by end of this week / early next week.

Euro Yen (131.05) – could slowly move downwards on daily candles towards 130 by the end of this week / early next week, after having tested resistance near 131.75-131.80 yesterday.

Pound (1.4187) saw an unexpected low near 1.4066 yesterday but has stayed within the upward channel on daily candles. As we wrote yesterday, there could be a dip to 1.415-1.41 in the next couple of days (seen as support on daily candles), after which it could again rise, targeting 1.43 by early next week.

Dollar Rupee (64.98) - can test 65.25 and then come off from there.

INTEREST RATES

US yields fell below crucial levels yesterday as investors seem to be shifting away from volatile equity markets into safer debt. This is in line with our expectation of a slow decline in yields, which might continue through Apr-May.

Almost 300 billion $ worth of Treasury debt auctions are underway this week, which could possibly raise yields – we need to watch out for this.

US 10 Yr Yield (2.78%), 30 Yr (3.035%), 5 Yr (2.58%), 2 Yr (2.27%) :

The 10 Year yield instead of rising towards channel resistance near 2.88%-2.90, has dipped slightly below support (near 2.8%). Yesterday we wrote that there is a possibility for 2.75% to be tested in Apr '18 – this could possibly happen in early April if the treasury auctions this week do not raise yields.

The 30 yr yield has dropped to support near 3.04%. We wrote yesterday that a dip from 3.1% could create a downward channel for the 30 Yr yield – we need to see till the end of the week if the same gets confirmed.

The 5 year yield has broken below crucial support near 2.6%. Let's see if the auctions can raise it back up into the horizontal channel.

GBP/USD Remains Supported Ahead Of US GDP

Key Highlights

- The British Pound formed a short-term top at 1.4244 and declined against the US Dollar.

- There is a crucial bullish trend line forming with support at 1.4020 on the 4-hours chart of GBP/USD.

- The S&P/Case-Shiller Home Price Indices in Jan 2018 increased 6.4%, more than the forecast of +6.2% .

- Today, the US GDP report for Q4 2017 will be released, which is forecasted to post a growth of 2.7% (Annualized).

GBP/USD Technical Analysis

This past week, there was a nice upside move in the British Pound above 1.4000 against the US Dollar. The GBP/USD pair recently traded as high as 1.4244 before starting a downside correction.

It seems like a short-term top in place since the pair tested the 50% Fib retracement level of the last wave from the 1.3889 low to 1.4244 high. However, there are many supports on the downside above the 1.4000 level.

The most important one is a crucial bullish trend line with support at 1.4020 on the 4-hours chart. The same trend line is close to the 61.8% Fib retracement level of the last wave from the 1.3889 low to 1.4244 high.

Therefore, if the pair corrects further lower, it is likely to find support near 1.4000-20 in the near term. On the upside, an initial resistance is at 1.4200. A push above the mentioned 1.4200 level may perhaps take the pair towards 1.4220 and 1.4240.

Recently, the US saw the release of the S&P/Case-Shiller Home Price Indices for Jan 2018 by the Standard & Poor’s. The market was looking for a rise of 6.2% in indices compared with the same month a year ago.

However, the actual result was positive since there was a rise of 6.4% in the S&P/Case-Shiller Home Price Indices.

Overall, the US Dollar is showing a few positive signs versus the Euro and the British Pound. Having said that, today’s Gross Domestic Product Q4 2017 release may change the market sentiment in the short term.

Economic Releases to Watch Today

- US Gross Domestic Product Q4 2017 – Forecast 2.7% versus previous 2.5%.

- US Personal Consumption Expenditures Prices for Q4 2017 (QoQ) – Forecast +2.7%, versus +2.7% previous.

- US Core Personal Consumption Expenditures for Q4 2017 (QoQ) – Forecast +1.9%, versus +1.9% previous.

New Zealand business confidence: Economy is certainly not crawling, but it’s hardly gliding along

New Zealand ANZ business confidence dropped to -20 in March, down from -19. That means a net 20% of businesses are pessimistic about the year ahead.

Highlights from the release:

- Headline business confidence and firms' views of their own activity have trodden water in March, both little changed from the preceding month.

- Belying the headline measures somewhat, all key activity indicators improved further, albeit while remaining well off their cycle highs.

- Pricing indicators were broadly steady

ANZ also added:

- The economy is certainly not crawling, but it's hardly gliding along.

- Activity indicators increased pretty much across the board but remain below the levels of six months ago.

- Our composite growth indicator, which combines business and consumer confidence, continues to suggest growth around 2-3% y/y.

- Inflation expectations and pricing intentions were little changed.

Full release here.

Euro stays strongest after jitters, EURAUD with solid upside bias

After some jitters yesterday, EUR remains the strongest major currency for the week as seen in W heatmap. Strength is apparent against USD, GBP and AUD. Meanwhile, JPY is trading as the weakest, followed closely by USD, CHF and AUD.

Looking at EURAUD action bias table, the biases are consistent across time frame.

Looking at EURAUD action bias table, the biases are consistent across time frame.

And EURAUD is seen as in up trend in 6H, D and W charts. So, the current H neutral could present an opportunity to long EUR/AUD.

And EURAUD is seen as in up trend in 6H, D and W charts. So, the current H neutral could present an opportunity to long EUR/AUD.

An intraday strategy could be buying at PP at 1.6120 with a stop below S1 at 1.6081.

DOW closed down -1.43% after 737 pts swing, rejected by 24453 resistance

DOW initially gained 244 pts to 24446.22 but reversed to closed down -344.89 pts or -1.43% at 23857.71. Considering that it hit as low as 23708.73, that was indeed a massive 737 pts swing. The reversal was mainly because tech stocks were crushed. S&P 500 lost -45.93 pts or -1.73% to 2612.62. NASDAQ suffered most and closed down -211.73 pts or -2.93% at 7008.81. Selloff continues in Asia with Nikkei down -1.8%, HK HSI down -0.9% at the time of writing.

Technically, we've mentioned before (here) that there will be no change in near term direction before a break of 24453.14 resistance. That is, DOW is expected extend recent decline to 23360.29 and below. The development is no far in line with our near term bearish view.

Complicatedly Confounding Currency Moves

Complicatedly Confounding Currency Moves

One of the best Easter egg hunts shaping up is trying to find the elusive US dollar narrative. Outside of the dollar-yen, the market was distinctly bearish to open the week but then the likely combination of month-end/quarter-end and Easter holidays whetted into context, and the dollar tore through g-10 currency markets like a runaway train overnight.

While liquidity is a bit thin this week, but confusing the landscape is that the intersection of month end /quarter end and Japanese Year end flows which have triggered some complicatedly confounding currency moves. Most quant models were indicating a propensity to buy dollar during this rebalancing act period; unquestionably the movement tripped a few stops on the way to the accounting ledger contributing to the unusually messy price action even by usual quarter end standards. However, given the uncertain timing of month end/quarter end flows, position squaring to place a bit earlier than usual due to Friday’s holiday.

Wall Street’s rebound fizzled as investors are still trying to figure what the US administration is doing on the protectionist front.On the one hand, we get a relief rally on the perception that the trade war was over before it even began. And now the administration is looking to clamp down on Chinese takeovers, while Commerce Secretary Wilbur Ross indicated Trump is planning “other action” on trade

The uncertainty over US protectionism isn’t going to fade anytime soon, and while investors should enjoy the small win on the tariff front, they’ll be best served to prepare for a long drawn out and perhaps more rancorous dialogue between US and China when it comes to intellectual property rights. Best get used to the new normal especially around the S&P post with the President considering passing emergency law to restrict China takeovers of tech sectors companies.

Oil Markets

The market position remains exceptionally long Oil on the rising geopolitical premium, as there remains a growing concern that crude inventories look tight heading into summer months and the potential for Iran and Latin America supply disruption could support that evolving narrative. But with very stretched Hedge Fund long/short positioning and the omnipresent geopolitical hours of the decision, that seems to occur with increasing regularity; the markets will remain very choppy as it continues to climb the peak.

As with most cross-asset price action overnight, there was a higher propensity to reduce risk and given that oil prices were pressing significant resistance levels, as expected prices slipped on profit-taking in this holiday-shortened week despite the continually evolving bullish narrative.

Gold Markets

Gold markets continue to embrace the growing geopolitical risk premium with an anticipated frenzy of potentially geopolitical flashpoints occurring in May; markets will remain firm on dips. As far as overnight price action, it makes perfect sense for a rapid move higher to consolidated for a bit, and this movement will seclude and cement the long gold position and set the stage for further gains. Inventories remain skewed long gold, looking for more topside gains on the return of the weaker US dollar narrative.

Currency Markets

For every swing higher there is an unhappy buyer, and at every swing lower, an unhappy seller. So therein lies the problem trading in baffling market conditions. However, it’s probably not worth reading to much into the overnight moves as strangeness in the currency markets is all around.

Japanese Yen

Amid all the noise, USDJPY traded well on a softer trade war drumbeat but not to unexpectedly ran into the sell some resistance zone between 105.60-80. However, the downside continues to beckon on geopolitical uncertainty while the market continues to weave a cautionary tale regarding Abexit. Japanese exporter remains well underhedged the with every move lower the propensity for Japanese life insurers to increase USD selling hedges grow closer and closer

The Euro

The Euro was prone to month-end rebalancing, and it didn’t take much other than a cooling on EU consumer confidence to send the Euro bulls out to pasture in a day where flows dominated price action and positioning in the absence of any significant data.

The Pound

Cable was crushed all the way down to 1.4066 providing some opportunistic buying opportunities before rebounding sharply. The Pound is particularly vulnerable to month end flow but last night was a bit of overkill.

The Malaysian Ringgit

Yesterday positivity has given way to the reality that the Trade war drums while beating a little softer, are not about to leave the picture anytime soon. While we remain in this muddled landscape, the 3.87 level should hold firm until the broader US dollar negative bias takes hold.

However, the stars are beginning to align again with the Ringgits fortunes especially with the market under-positioned MYR With the break of 3.87 it could open the door to further gains, at a minimum, it brings topside resistance back to 3.90

With US Bond yields remaining low and moving through the critical 2.79 % level the will be growing interest in the MYR carry, and with the Long MYR positions undersubscribed it provided an early morning boost to the Ringgit. With the trade, war drums beating softer and the US Bond yields dropping, this is providing a positive background for the local Bond markets. Renewed USD dollar weakness should see the MYR trade to 3.85