Sample Category Title

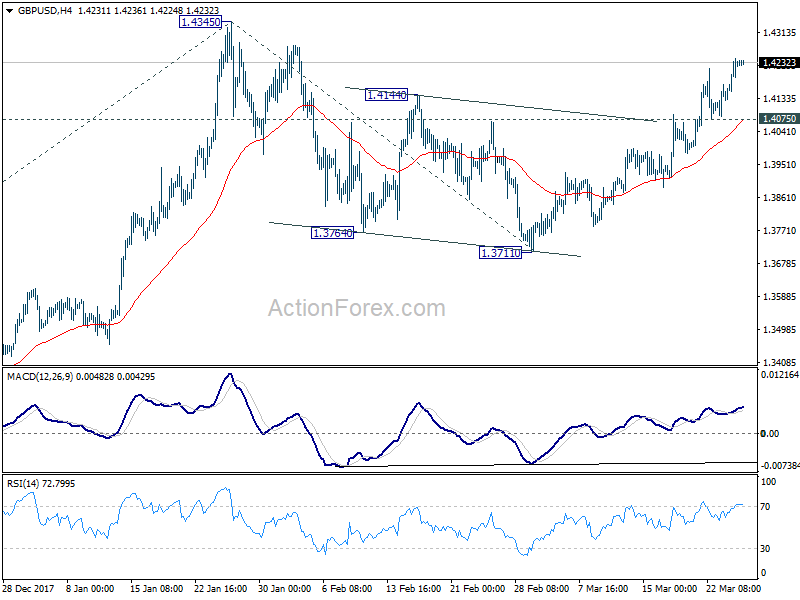

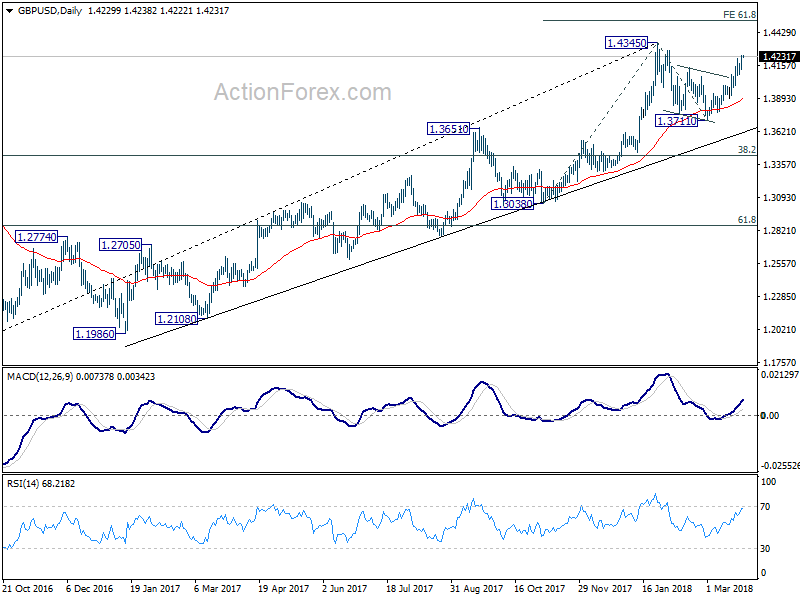

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4156; (P) 1.4200; (R1) 1.4273; More....

Intraday bias in GBP/USD remains on the upside. Rise from 1.3711 is in progress to retest 1.4345 high first. Decisive break there will resume larger up trend and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, break of 1.4075 support is needed to indicate completion of the rebound from 1.3711. Otherwise, outlook will stay cautiously bullish even in case of retreat.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

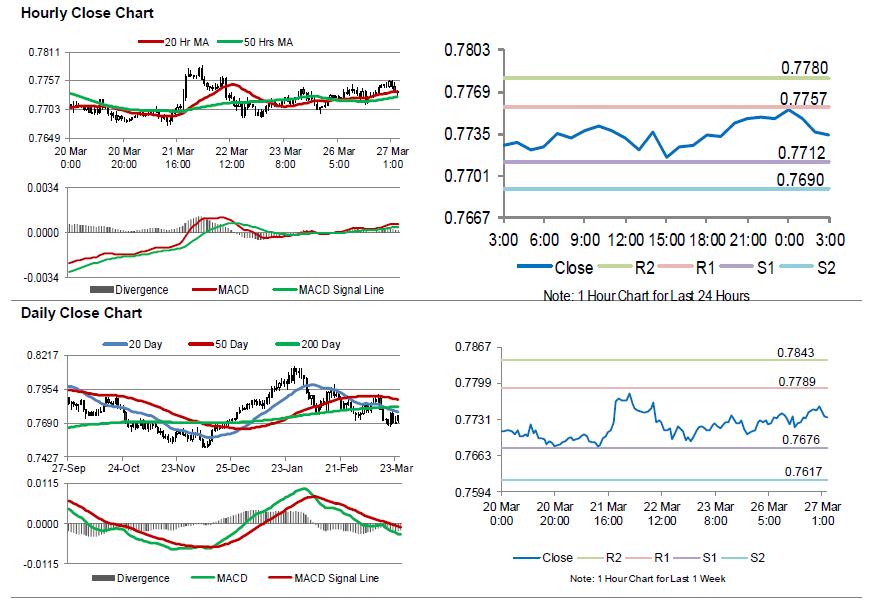

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.23% against the USD and closed at 0.7747.

LME Copper prices declined 2.4% or $158.0/MT to $6500.0/MT. Aluminium prices declined 1.3% or $27.0/MT to $2022.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7734, with the AUD trading 0.17% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7712, and a fall through could take it to the next support level of 0.7690. The pair is expected to find its first resistance at 0.7757, and a rise through could take it to the next resistance level of 0.7780.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average

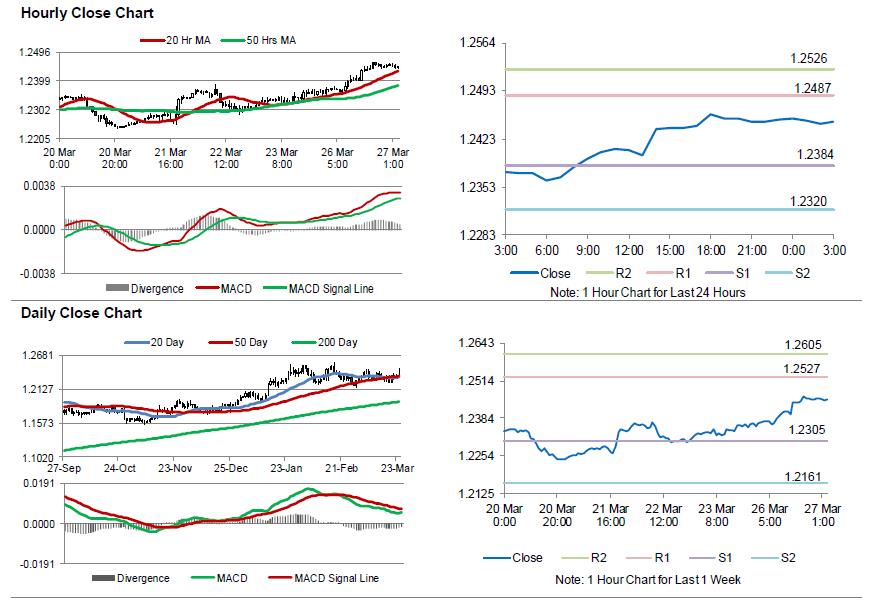

Euro Trading A Tad Lower This Morning

For the 24 hours to 23:00 GMT, the EUR rose 0.65% against the USD and closed at 1.2451.

In economic news, the final gross domestic product (GDP) in France rose more than initially estimated by 0.7% QoQ in the final three months of 2017, while the preliminary figures had indicated an advance of 0.6%. The nation's GDP had recorded a revised rise of 0.5% in the previous quarter.

In the US, data indicated that the Dallas Fed manufacturing business index fell more-than-estimated to a level of 21.4 in March, compared to market expectations for a drop to a level of 33.5. In the prior month, the index had registered a level of 37.2. Moreover, the nation's Chicago Fed national activity index advanced to a level of 0.88 in February, beating market consensus for a rise to a level of 0.15. In the prior month, the index had registered a revised level of 0.02.

In the Asian session, at GMT0300, the pair is trading at 1.2448, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.2384, and a fall through could take it to the next support level of 1.2320. The pair is expected to find its first resistance at 1.2487, and a rise through could take it to the next resistance level of 1.2526.

Moving ahead, investors would look forward to the Euro-zone's final consumer confidence index for March, slated to release in a few hours. Later in the day, the US consumer confidence index for March, will be eyed by market participants.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

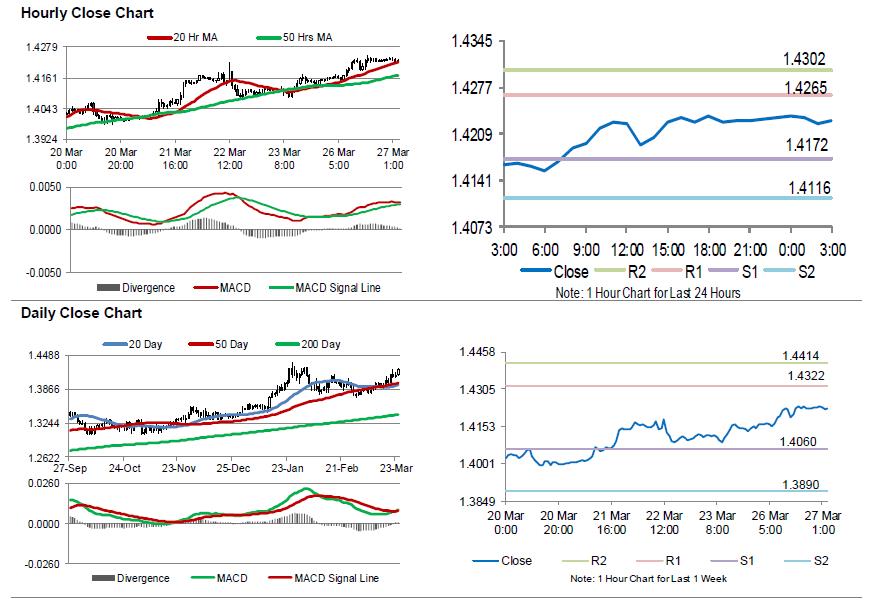

UK’s BBA Mortgage Approvals Declined In February

For the 24 hours to 23:00 GMT, the GBP rose 0.49% against the USD and closed at 1.4233.

Macroeconomic data revealed that UK's BBA mortgage approvals eased more-than-anticipated to a level of 38.1K in February, compared to market expectations for a fall to a level of 39.0K. BBA mortgage approvals had recorded a revised reading of 40.0K in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.4229, with the GBP trading a tad lower against the USD from yesterday's close.

The pair is expected to find support at 1.4172, and a fall through could take it to the next support level of 1.4116. The pair is expected to find its first resistance at 1.4265, and a rise through could take it to the next resistance level of 1.4302.

With no macroeconomic releases in Britain today, investors would focus on global macroeconomic events for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average

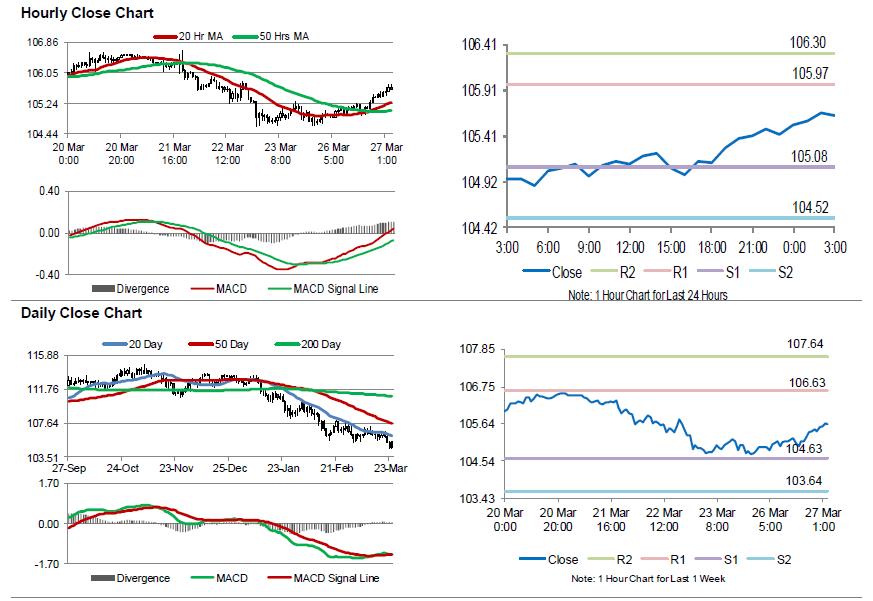

Japanese Yen Extends Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.47% against the JPY and closed at 105.43.

In the Asian session, at GMT0300, the pair is trading at 105.63, with the USD trading 0.19% higher against the JPY from yesterday’s close, amid receding tensions over a potential trade war between the US and China.

The pair is expected to find support at 105.08, and a fall through could take it to the next support level of 104.52. The pair is expected to find its first resistance at 105.97, and a rise through could take it to the next resistance level of 106.30.

Amid no key macroeconomic releases in Japan today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

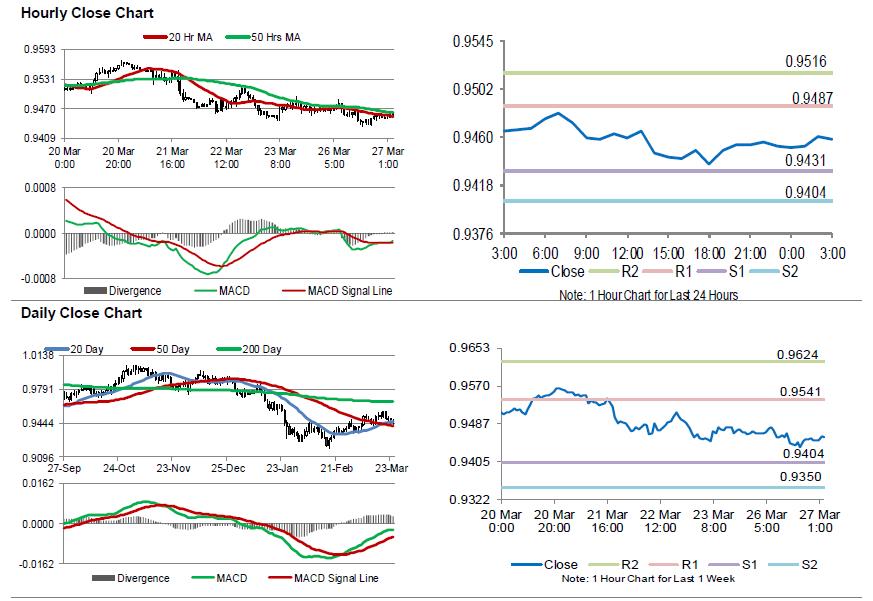

Swiss Franc Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.16% against the CHF and closed at 0.9452.

In economic news, Switzerland’s total sight deposits rose to a level of CHF576.0 billion in the week ended 23 March, compared to a level of CHF575.9 billion reported in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9458, with the USD trading 0.06% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9431, and a fall through could take it to the next support level of 0.9404. The pair is expected to find its first resistance at 0.9487, and a rise through could take it to the next resistance level of 0.9516.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

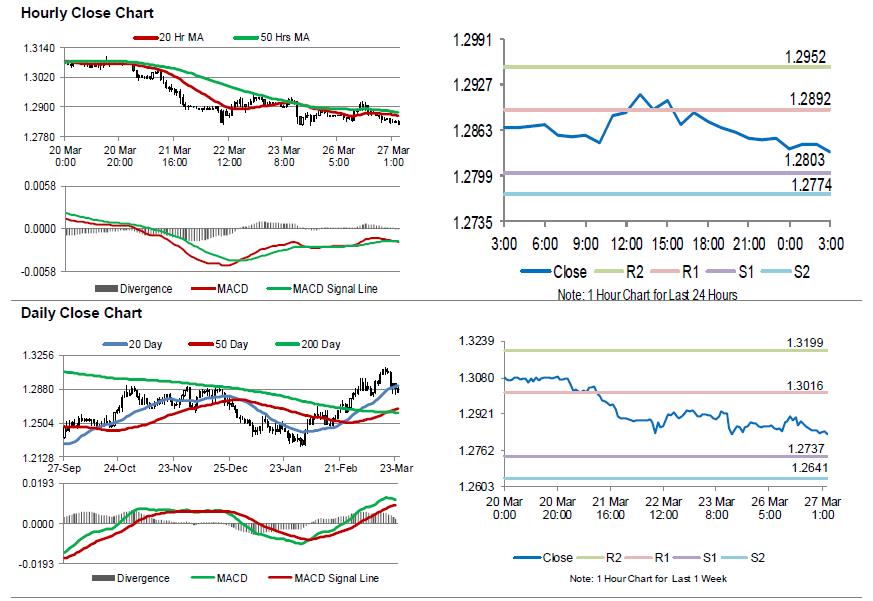

Loonie Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.08% against the CAD and closed at 1.2852.

In the Asian session, at GMT0300, the pair is trading at 1.2833, with the USD trading 0.15% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2803, and a fall through could take it to the next support level of 1.2774. The pair is expected to find its first resistance at 1.2892, and a rise through could take it to the next resistance level of 1.2952.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

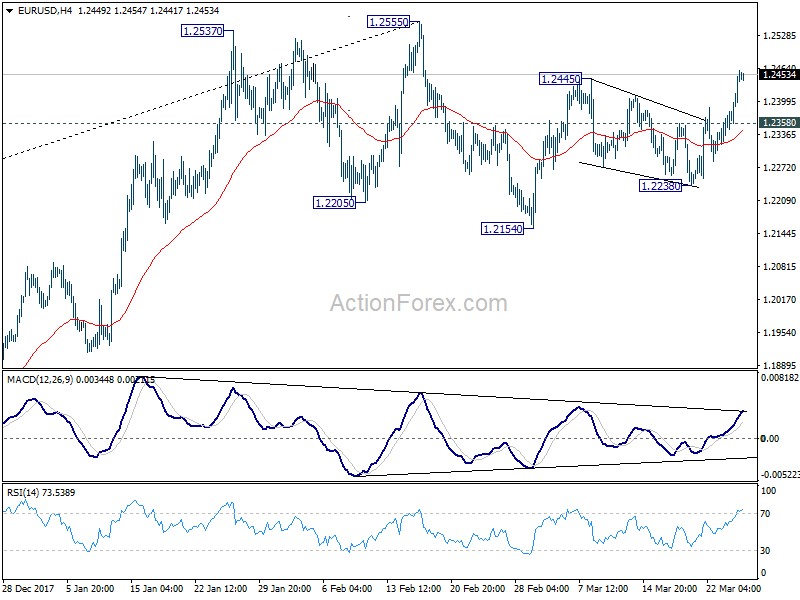

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2376; (P) 1.2419 (R1) 1.2490; More....

The break of 1.2445 resistance confirms resumption of rebound from 1.2154. Intraday bias stays on the upside for further rally to 1.2555 high, which is close to 1.2516 key long term fibonacci level. We'd be cautious on reversal from there. But decisive break will carry larger bullish implications. On the downside, below 1.2358 minor support will turn intraday bias neutral first. And further break of 1.2338 will target 1.2154 and below again.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

EUR/USD to Look into Confidence Indicators for Guidance, as Risk Aversion Eased

The financial markets responded positively to news that US and China are back on the table for trade negotiation. At least for now, the fear of further escalation in tension is eased. DOW ended yesterday up 669.40 pts or 2.84% at 2420.60. S&P 500 gained 70.29 pts or 2.72% to close at 2658.55. NASDAQ also rose 227.87 pts, or 3.26% to 7220.54. Asian markets follow with Nikkei trading up over 1.6% at the time of writing. Hong Kong HSI is up 0.9%.

In the currency markets, Yen is paring much of its recent gains as risk aversion receded, and it's trading as the weakest one for the week so far. Euro and Sterling are the strongest ones thanks to yesterday's rally. But Canadian Dollar is picking up some steam in Asian session too. Trading could start to turn quieter as holidays approach. But Euro traders will look into confidence indicators to be released for the needed fuel for EUR/USD to head to 1.2555 resistance. Also, US consumer confidence will be a feature of the day.

Fed Mester supports gradual rate hike, against a steep path

Cleveland Fed President Loretta Mester she supports gradual rate hike "this year and next year". At the same time, she's "against a steep path" in tightening because "we want to give inflation time to move back to goal". She sounds optimistic saying that "this year is shaping up to be another good year for the economy." And for monetary policymakers, the task is to "calibrate policy to this healthy economy so that the expansion is sustained."

The government's tax cut poses "some upside risk" to the forecast, and Mester expects a better read on household spending "over the next several months". Globally, she noted that "for the first time in many years, economic activity around the world is picking up and forecasts for global growth are being revised up." And, "this should have a positive feedback effect on the U.S. economy via exports."

Meanwhile, she warned that trade developments are a "risk to the forecasts". And the uncertainty "may not be resolved quickly". But it didn't change her outlook for the over economy yet.

Goldman Sachs bullish on gold price

Goldman Sachs published a note that's bullish on gold price yesterday and expected it to outperform over the coming months. It's forecasting four Fed hikes this year, which is one more than FOMC's own projection. And the bank admitted that its upbeat view on gold is "counter-intuitive".

However, the report pointed to empirical data for the past six tightening cycles of Fed, and found gold has "outperformed post rate hikes four times". And according to their analysts, "the dislocation between the gold prices and US rates is here to stay". It added that the bullish view was also driven by higher inflation, rising EM wealth and increased risk of equity correction. Also, it's a likely a function of investors "waiting on the sidelines" and the becoming interested in Gold again once the tightening "catalyst" has passed.

Here is our quick technical view on gold

On the data front

Japan corporate service price rose 0.6% yoy in February, below expectation of 0.7% yoy.

German import price and Eurozone M3 money supply will be released in European session. But the focuses would be on confidence indicators including business claims, economic confidence, services confidence and industrial confidence.

Later in the day, US will release S&P Case-Shiller house price as well as Conference Board consumer confidence.

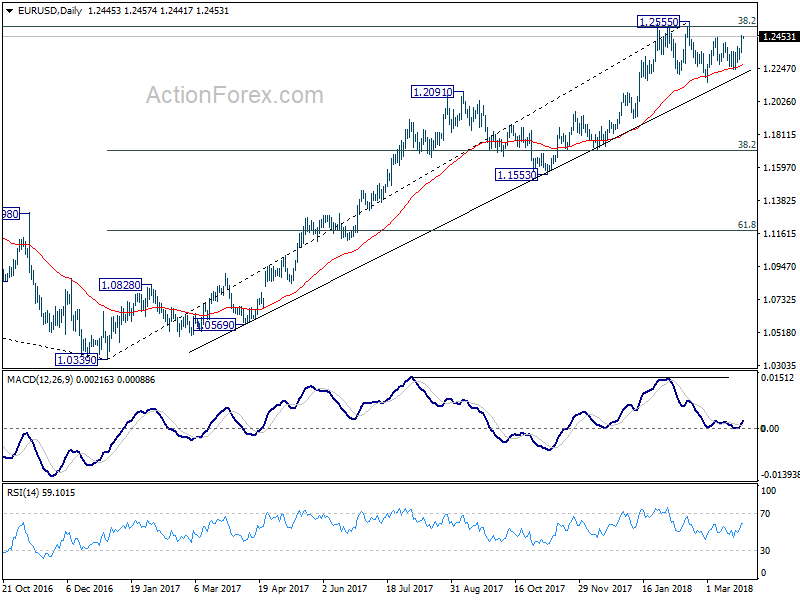

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2376; (P) 1.2419 (R1) 1.2490; More....

The break of 1.2445 resistance confirms resumption of rebound from 1.2154. Intraday bias stays on the upside for further rally to 1.2555 high, which is close to 1.2516 key long term fibonacci level. We'd be cautious on reversal from there. But decisive break will carry larger bullish implications. On the downside, below 1.2358 minor support will turn intraday bias neutral first. And further break of 1.2338 will target 1.2154 and below again.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Y/Y Feb | 0.60% | 0.70% | 0.70% | |

| 06:00 | EUR | German Import Price Index M/M Feb | -0.30% | 0.50% | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | 4.60% | 4.60% | ||

| 09:00 | EUR | Eurozone Economic Confidence Mar | 113.3 | 114.1 | ||

| 09:00 | EUR | Eurozone Business Climate Indicator Mar | 1.36 | 1.48 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Mar | 6.9 | 8 | ||

| 09:00 | EUR | Eurozone Services Confidence Mar | 16.5 | 17.5 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Mar F | 0.1 | 0.1 | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Jan | 6.10% | 6.30% | ||

| 14:00 | USD | Consumer Confidence Mar | 131 | 130.8 |

Market Morning Briefing: Brent Is Almost Stable Above 70

STOCKS

Almost all major indices are in a recovery mode just now, trying to bounce back after a sharp fall last week.

Dow (24202.60, 2.84%) moved up a bit yesterday and could test 25000 on the upside in the next few sessions if the rise sustains. A fall back to levels below 23500 if seen would make it vulnerable to a sharper fall in the medium term. 25000-24000 could be the trade region for the coming sessions.

Dax (11787.26, -0.83%) dipped more and is testing support near 11700. This if holds, could produce an immediate bounce to levels near 12100-12300 in the near term (more preferred); else a fall towards 11600 could be seen.

Nikkei (21110.68, +1.66%) has moved up well from 20400 levels and could test daily channel resistance near 21400. Only on a break above 21400 would initiate further chances of an upmove; else a fall back towards 20600-20400 or even lower could be considered for the medium term.

Shanghai (3159.64, +0.83%) opened with a gap up as support near 3100 seems to be holding for now. While the support holds, te index could gradually move up towards 3200-3250 in the coming sessions.

Nifty (10130.65, +1.33%) and Sensex (33066.41, +1.44%) rose yesterday as expected. Nifty could test 10260 again on the upside while Sensex has scope of rise towards 33500.

COMMODITIES

Brent (70.23) is almost stable above 70. While the long term chart may look bullish just now, there could be some dip towards 68 in the coming sessions. A straight rise from here could trigger some more of upside momentum taking it to 72.50. Nymex WTI (65.70) could also see a pause just now. A test of 64 on the downside looks possible before another attempt to rise past 66.50.

Gold (1353) has moved up and is trading just at the resistance level. A break above 1354 if seen and sustained could lead to a sharp rise towards 1360-1380 in the near term before another corrective dip takes place.

Copper (3.0149) has bounced back a little but needs to move up beyond 3.04 to get back the upward momentum and start rising back to higher levels. While below 3.04, there could be chances of seeing a further fall in the coming sessions. Bearishness to be negated only above 3.04.

FOREX

Dollar index (89.10) as mentioned yesterday, has weakened more and has broken below support near 89.4 on daily candles. It has also dipped below crucial long term support on weekly line chart near 89.2-89.4 (earlier mentioned as 89.3-89.4). If this break on the weekly line chart sustains, the Dollar Index could turn bearish in the medium term after having ranged in the 88.5-91.0 region for the past 10 weeks. The next downside target would be horizontal support near 88.5 on daily candles.

Euro (1.2449) – after breaking resistance on daily candles near 1.235 yesterday, the Euro is moving towards higher resistance level on 3 day candles near 1.255-1.260. However, on the weekly line chart, it is testing crucial long term resistance near 1.245, which would have to be breached for a medium term rally to be confirmed. We prefer the breach of this level and a move towards 1.255-1.260 in the next couple of weeks.

Dollar Yen (105.63) , as per our expectation yesterday, didn’t see a break of immediate support near 104.6 on daily candles. It has bounced from there towards immediate resistance near 106 on the daily candles. This is a strong resistance level and should again push the Dollar Yen down towards 104.5. We could see some ranging in the broad 104-106 region in this week.

Euro Yen (131.49), as we had expected, did move up after testing 129 on Friday, but also went on to breach resistance near 131 in the downward channel on daily candles. The crucial downside target of 127.5-128.0 (last seen in Aug ’17) which was mentioned yesterday might well take some time to be tested if Euro continues its rise towards 1.255-1.26 as mentioned above and if the Dollar Yen simultaneously ranges between 106-104.

As per expectation, Pound (1.4231) is continuing to move up in a channel on daily candles towards higher (horizontal) resistance near 1.43. There could be some dip from channel resistance in the next 1-2 sessions towards 1.415-1.420 after which it could again rise, targeting 1.42 by early next week.

Dollar Rupee (64.87) may bounce back from levels near 64.75.

INTEREST RATES

US yields are seeing some ranging after the Fed rate hike last week, but we also believe that this ranging might be part of a broader (slow) decline in yields which might just continue through Apr-May.

US 10 Yr Yield (2.852%), 30 Yr (3.086%), 5 Yr (2.6435%), 2 Yr (2.31%) :

As per our expectation yesterday, the 10 Yr yield did rise from channel support (near 2.8%) on short term chart and might now test channel resistance near 2.88%-2.90% in the next couple of sessions. There could be a possibility for 2.75% to be tested in Apr ’18 if it continues ranging in this channel.

The 30 yr yield should has also moved up from support near 3.04%-3.05%. If it dips from 3.1%, a downward channel for the 30 Yr yield would also be confirmed.

The 5 year yield is has as per expectation bounced from support near 2.6% and could see a rise to 2.7% by end of the week.

The 2 Year yield is near crucial medium term resistance level of 2.3% from where it should see a dip in the coming sessions.

Japan 10 year yield (0.065) exactly as per our expectation is bouncing from horizontal support near 0.03%. Ranging between the broad 0.03%-0.1%, which has been happening since Sep ’17, might continue as long as the Japanese Central Bank sticks to its 0% target for Japanese bond yields.