Sample Category Title

Yen Lower as Trade War Fears Recede, Euro and Sterling Surge

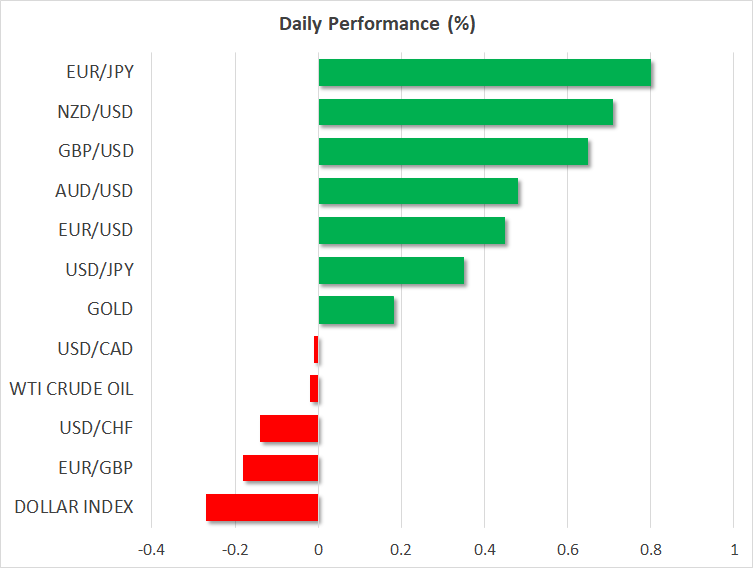

Risk sentiments stabilized as markets reacted positively to the possibility of a trade deal between US and China. Major European indices are trading higher even though gains are only at 0.35-0.55% in FTSE, CAC and DAX only, at the time of writing. US futures also point to triple digit gains in DOW at open. In the currency markets, Yen trades broadly lower, paring much of last week's gain as sentiments stabilized. For the momentum New Zealand Dollar is trading as the strongest one for today so far. But Sterling and Euro and catching up entering into US session.

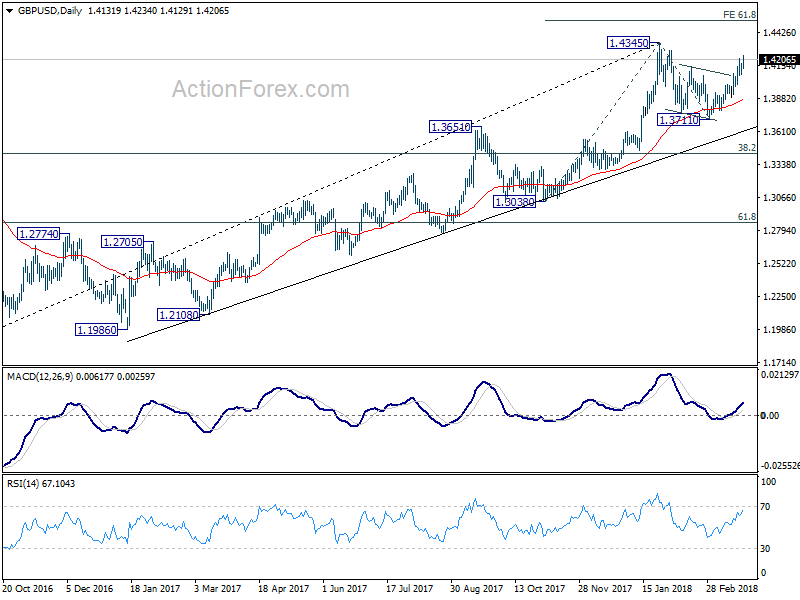

Technically, GBP/USD's rally from 1.3711 extends today and is on course to test 1.4345 near term resistance. Break will resume medium term up trend. EUR/USD's rise also affirms that case that rebound from 1.2154 is in progress. We're now waiting for 1.2445 resistance to break to confirm. Also, while Yen is trading broadly lower, the retreat against Dollar is shallow. USD/JPY is staying in very tight range above 104.63. There is not sign of short term bottoming in USD/JPY yet.

Moody's updates view on Brexit: Uncertainty prevails before conclusive final agreement

Moody's, the credit rating agency, acknowledge the positive impact of the Brexit transition deal announced last week. However, it remained cautious that risks will prevail until a final agreement is made. It said in a report today that the transition agreement reinforces the view that Brexit's impact will be "manageable" for UK corporate issuers, despite increased bureaucracy costs under an FTA. And it was "mildly positive" to UK banks as it "reduces downside risks to growth and revenues." Also, risk of disorder Brexit is "somewhat mitigated", it reinforces the central scenario of "gradually moderating growth" in the UK. However, Moody's warned that uncertainty regarding the future relationship between UK and EU prevails until a " conclusive final agreement" is reached.

Intensive talks of Irish Border in Brexit negotiation starts

The UK and EU start intensive talks on the most troublesome topic in Brexit negotiation today, the Irish Border. Both sides agreed, back in December, on the principle of avoiding a hard border between Ireland and Northern Ireland. However, there are key differences on the way to fulfil this principle. And there seems to be no agreeable solution yet. The negotiation team will try to address areas like customs, food safety, animal health and regulations of goods and come up with something for next EU summit in June.

Last month, EU proposed a backstop option if there will be no solution on Irish border. And that is, Northern Ireland will remain in the customs union. But that was bluntly objected by UK Prime Minister Theresa May.

Brexit Secretary David Davis reiterated that position on Sunday. Davis said that while UK agreed to a "backstop", it will not be the one as proposed by the EU. He remained optimistic and said it's "overwhelmingly likely" to solve the problem in the context of a trade and customs agreement. And he added, "there are ways of dealing with this. You can't just say 'we haven't done it anywhere else' – we haven't attempted to do it anywhere else."

Bundesbank Weidmann: It's important to start to end QE soon

Bundesbank President, Jens Weidmann, a known ECB hawk, called for ending stimulus again today. He painted an upbeat picture of Eurozone economic outlook and hailed that "the upswing is now everywhere on broad feet; the growth rates of the Member States are now scattering noticeably less. The unemployment rate has fallen to 8.6 percent, its lowest level since the end of 2008. The sentiment indicators continue to move at very high levels. This indicates that the favorable economic development continues for the time being.

ECB economists projected 2.4% GDP growth in 2018, 1.9% in 2019 and 1.7% in 2020. Also, They forecast inflation to be at 1.4% in 2018 and 2019, and then rise to 1.7% in 2020. And to Weidmann, that is "a level that is broadly consistent with our medium-term definition of price stability." With this background, "it is not surprising that the financial markets have been expecting net bond purchases to end in 2018." He also emphasized that "the end of net purchases is only the beginning of a multi-year process of monetary normalization. That's why it's so important to actually start soon."

Regarding interest rates, Weidmann said that "the markets see a first rate hike around the middle of the year 2019, which is probably not entirely unrealistic."

IMF Lagarde proposes "rainy-day fund" to Eurozone as "temporary cushion"

In a speech titled, "A Compass to Prosperity: The Next Steps of Euro Area Economic Integration", IMF managing director Christine Lagarde outlined her recommendations. She focused on three of the reform areas for Eurozone officials to consider in the review in the coming months. The ares include a modernized capital markets union, an improved banking union, and a move toward greater fiscal integration, starting with the creation of a central fiscal capacity.

In particular, she mentioned IMF's proposal of a "rainy-day fund" for building up assets in good times. During a downturn, countries could receive funding to help offset budget shortfalls. And, in extreme cases, " the fund would be allowed to borrow, however any borrowing would be repaid by members' future contributions." Though, she emphasized that " it will be a temporary cushion and not a permanent pillow."

China's WTO embassador Zhang Xiangchen: "Lock this beast back into the cage"

Zhang Xiangchen, China's Deputy International Trade Representative and WTO embassador urged the organization complained about US unilateral tariffs at a WTO meeting today. He criticized that "US is setting a very bad precedent by bluntly breaching its commitment made to the world" as it has agreed not to apply such tariffs without TWO approval. And he urged WTO members to jointly "lock this beast back into the cage of the WTO rules".

He added that "unilateralism is fundamentally incompatible with the WTO, like fire and water. In the open sea, if the boat capsizes, no one is safe from drowning." And, "we shouldn't stay put watching someone wrecking the boat. The WTO is under siege and all of us should lock arms to defend it."

Mnuchin in "very productive conversations" with China on trade agreement to avert Section 301 tariffs

US Treasury Secretary Steven Mnuchin said in a Fox News Sunday interview that the US is having "very productive conversations" with China. And he's "cautiously hopeful we can reach an agreement" to avert the tariffs on USD 50-60b announced last week. Mnuchin noted that both countries agreed on reducing the US trade deficit to China. And, they were trying "to see if we can reach an agreement as to what fair trade is for them to open up their markets, reduce their tariffs, stop forced technology transfer."

But Mnuchin emphasized that the US is still on track to impose the Section 301 tariffs unless there is an "acceptable agreement" for Trump to sign off on. He also noted that "we're not afraid of a trade war, but that's not our objective." And, "in a negotiation you have to be prepared to take action."

Separately, the WSJ reported that Mnuchin and US Trade Representative Robert Lighthizer sent a letter to Chinese Vice Premier Liu He last week, detailing the list of specific request for China. And the list is reported to include reduction of Chinese tariffs on US vehicles, purchases of semiconductor products and larger access to China's financial markets.

RBNZ added employment to its mandate. But won't change Governor Orr's policy bias

RBNZ jointly announced the policy target agreements with Ministry of Finance today. Employment is now formally added to its mandate. The statement retained price stability as a target. RBNZ should target to keep annual CPI inflation between 1-3% over medium term. And focus is to keep inflation near to the 2% mid-point. Additionally, the with stable general price level maintained, the monetary would "contribute to supporting maximum sustainable employment within the economy." Overall, the announce is widely expected as a result of the new government's RBNZ review. And, there wouldn't be any change to the neutral to slightly dovish bias of RBNZ as Adrian Orr just take over as the governor.

New Zealand trade surplus at NZD 217m in Feb, import hits Feb record high

NZD trades generally higher in Asian session after trade balance data. Accord to Stats NZ Tatauranga Aotearoa, for February 2018 compared with February 2017, goods exports rose NZD 446 million or 11% yoy to NZD 4.5 billion. Goods imports rose NZD 187 million or 4.6% to NZD 4.2 billion. Import was a new high a new high for total imports in a February month. The previous high was NZD 4.1 billion, in February 2017. The monthly trade balance was a surplus of NZD 217 million. That equals to 4.9% of exports.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4085; (P) 1.4128; (R1) 1.4173; More....

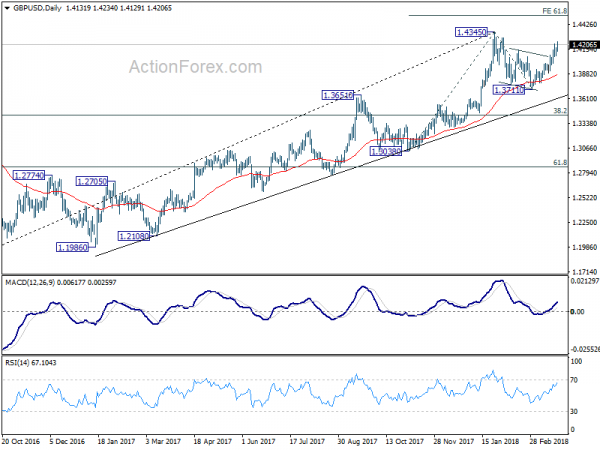

GBP/USD's rally continues today and reaches as high as 1.4234 so far. Intraday bias remains on the upside for 1.4345 high. Decisive break there will resume larger up trend and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, break of 1.3982 support is needed to indicate completion of the rebound from 1.3711. Otherwise, outlook will stay cautiously bullish even in case of retreat.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance Feb | 217M | -100M | -566M | -655M |

| 08:30 | GBP | BBA Loans for House Purchase Feb | 38.1K | 39.2K | 40.1K | 40.0K |

Moody’s updates view on Brexit: Uncertainty prevails before conclusive final agreement

Moody's, the credit rating agency, acknowledge the positive impact of the Brexit transition deal announced last week. However, it remained cautious that risks will prevail until a final agreement is made.

Here are some highlights of the report:

- The agreement reinforces Moody's view that the impact of Brexit will be manageable for rated UK corporate issuers, despite increased bureaucracy costs under an FTA.

- For UK banks the agreement is mildly positive to the extent that it reduces downside risks to growth and revenues.

- As far as the risk of a disorderly withdrawal is somewhat mitigated, the agreement reinforces Moody's central scenario of gradually moderating growth in the UK.

- Uncertainty concerning the terms of UK's future long-term relationship with the EU will prevail until a conclusive final agreement is reached.

Major Currencies Gain Ground as Trade Fears Recede; European Equities Move Higher

Here are the latest developments in global markets:

FOREX: Trump’s decision to exempt several countries from his import tariffs on Thursday and today’s headlines that China is stepping up efforts to start trade negotiations with the US, gave a lift to dollar/yen during early European trading hours, sending the pair to 105.83 (+0.37%) from a 16-month low of 104.55 touched earlier today. The dollar index, though, which tracks the dollar’s strength versus six major currencies was unable to bounce up, falling to 89.21 (-0.21%), as the euro and the pound were strengthening as well. Euro/dollar jumped to a 2 ½ -week high of 1.2416 (+0.52%), while pound/dollar surged to near a two-month high of 1.4225 (+0.60%) after the UK Prime Minister confirmed on Monday that the British parliament will have a clear vote on the final Brexit deal following the opposition Labour party’s demand on Friday for the parliament to have the final say on the deal. In the antipodean currencies, aussie/dollar and kiwi/dollar were in an uptrend as well, with the former trading at 0.7733 (+0.48%) and the latter at 0.7284 (+0.72%).

STOCKS: European stocks opened higher on Monday as concerns over a potential global trade war seemed to ease. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.34% and 0.50% respectively at 1150 GMT, with all sectors being in the green except consumer non-cyclicals. The German DAX 30 rose by 0.50%, the French CAC 40 increased by 0.23% and the UK FTSE 100 climbed by 0.24%. In contrast, the Italian FTSE MIB failed to gain ground, retreating by 0.34% instead, after news that the Italian anti-establishment Five Star Movement and the anti-immigrant League might find common ground to form a coalition government. The Italian president is said to start formal negotiations on forming the new government on April 3 but the proceedings could probably be postponed into the end of April when regional elections take place.

COMMODITIES: Oil prices were weaker during the early European afternoon but rising tensions in the Middle-East continued to support the market. On Sunday, Saudi Arabian air-forces destroyed seven ballistic missiles fired by Yemen’s Iran-aligned Houthi militia, while worries that the US could abandon the Iran deal were also supportive. In other news, China launched its first crude futures today at Shanghai’s exchange market denominated in yen – its first commodity derivative offered to foreign investors-, with markets expecting it to become the third largest benchmark along WTI and Brent. WTI crude and Brent were last seen at $65.77 (-0.17%) and $70.44 (-0.01%) per barrel respectively. In precious metals, gold rebounded to $1,348.30 (+0.11%) per ounce after touching a session low of $1,344.11 per ounce earlier in the day.

Day ahead: Trade risks loom in the background

Day ahead: Trade risks loom in the background

After a noisy week with a trade warn drama that spurred risk-off activities again into the markets, Monday is expected to be relatively quiet with few economic releases. However, the spotlight will remain on trade developments and investors will be eager to hear how the trade story will wrap up from here on following Trump’s decision on Thursday to implement new import tariffs on China and exclude a number of allies from the mental tariffs. Topics on monetary policy will also be in focus as several central bankers prepare to deliver speeches later today.

In the UK, a speech by the Bank of England Chief Economist Andy Haldane held in Scotland will be in focus for any clues that could signal that the central bank is ready to proceed with further monetary tightening at its next policy meeting in May. Note that last week, policymakers decided to leave interest rates unchanged but an unexpected split in the voting structure, with Ian McCafferty and Michael Saunders, calling for a rate hike, spurred speculation that borrowing costs could increase in May for the second time since the financial crisis. If Haldane holds a hawkish tone today, signaling that the next move in rates is up, then the pound could pick up speed.

In the US, business surveys conducted by the Chicago and the Dallas Fed will be released at 1330 GMT and 1530 GMT respectively, but the measures are less likely to move the dollar. Instead, comments by Fed voting members later today, including New York Fed President William Dudley (1630 GMT), Cleveland Fed President Loretta Mester (2030 GMT) and Fed Board Governor Randal Quarles (2310 GMT), could be of greater importance to the currency.

Still, any moves in the markets could be limited by the risk-off sentiment heightened last week after Trump put his warnings against China on the table, signing new import tariffs against the world’s largest exporter which stretched into other product areas other than steel and aluminum. China threatened to retaliate accordingly last week, but today China’s foreign minister said that the country is willing to start negotiations with the US to dissolve their trade differences, hinting that a trade war between them could be averted. Earlier, the US agreed to revise a free-trade agreement with South Korea (KORUS) which Trump called a “horrible deal” back in April. Particularly, Seoul said today that US automakers will have a better access to the economy, while South Korean steelmakers will avoid import tariffs but face quotas in the US market. While these developments seem to provide some relief to the markets and hopes that the US and China could end up to a less painful agreement for the moment, it remains to see whether Trump is willing to adjust his attitude in a positive way.

USD/CAD – Canadian Dollar Pauses After Strong Week

The Canadian dollar is trading sideways in the Monday session. Currently, USD/CAD is trading at 1.2891, down 0.04% on the day. On the release front, there are no data releases in Canada or the US. We’ll hear from three FOMC members – William Dudley, Loretta Mester, Randal Quarles. On Tuesday, the key event of the day is US CB Consumer Confidence.

Canadian consumer data was positive on Friday, helping propel the Canadian dollar to gains of 1.6% last week. CPI, ticked lower to 0.6% but beat the estimate of 0.4%. Retail Sales rebounded with a gain of 0.9%, after a sharp loss of 1.8% in the previous release. This reading matched the estimate. There was good news south of the border, as Core Durable Goods Orders rebounded with a strong gain of 1.2%, crushing the estimate of 0.5%. This marked the strongest gain since July 2016. Durable Goods Orders jumped to an 8-month high, with a gain of 3.1%. The reading easily beat the forecast of 1.6%. The US manufacturing sector continues to expand at an impressive clip, a result of stronger global growth and a cheaper US dollar, which makes US goods less expensive for foreign buyers.

Canada is heavily dependent on exports, so the specter of a global trade war could be disastrous for the Canadian economy. There is considerable worry in Ottawa, as US President Trump seems intent on “righting wrongs” in US trade balances by applying the hedge hammer of tariffs. On Thursday, US President Trump slapped 25% tariffs on up to $60 billion worth of Chinese imports on Thursday. For its part, China wasted no time in threatening to retaliate, saying it was planning to impose tariffs on 128 US products, which amounted to $3 billion in imports. The tariffs directed against China come on the heels of tariffs on steel imports coming into the US, although the US has exempted Canada and some other countries. There is serious concern that these moves could lead to a downturn in the Chinese economy and cause a global recession, a nightmarish scenario for Canadian policymakers.

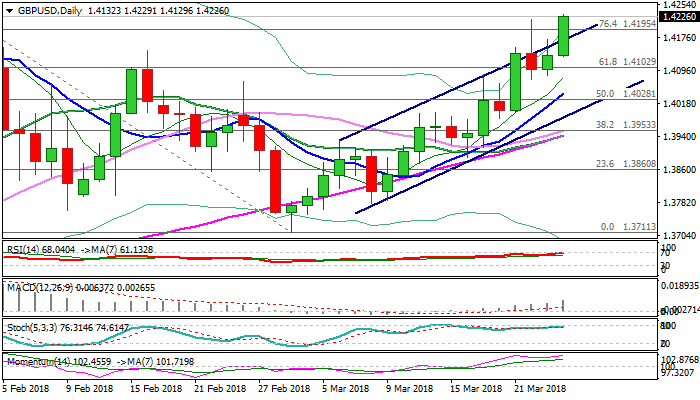

GBPUSD Extends To New Seven-Week High

Cable maintains positive tone on Monday and broke through previous high at 1.4218, hitting new 7-week highs. Firm break above cracked upper boundary of daily bull-channel (after two attempts last week failed) was bullish signal which adds to firm bullish tone from daily techs and overall positive sentiment following last week's announcement of progress in Brexit talks. Fading risk aversion on US-China talks which showed some positive signals, helped bulls to extend higher and open way towards next targets at 1.4277 (01/02 Feb double-top), with stronger acceleration to extend towards key barrier at 1.4345 (the highest of post-Brexit recovery). Close above 1.4218 is needed to generate bullish signal and support further advance. Broken bull-channel upper trendline now acts as strong support (1.4176) which is expected to keep the downside protected.

Res: 1.4277, 1.4300, 1.4345, 1.4400

Sup: 1.4218, 1.4176, 1.4144, 1.4129

Trade War Worries Ease

Notes/Observations

- Easing trade tensions allowed risk appetite to rebound

- US Treasury poised for its largest weekly sale of debt ever (approx. $294B)

Asia:

- Trump Administration said to send letter from Treasury Sec and US Trade Rep to China President Xi's top economic advisor Liu He seeking reduction of China's tariffs on US autos, requested additional purchases by China of US semiconductors and more access to China's financial sector.

- Treasury Sec Mnuchin: Trump administration was pressing ahead with tariffs, but remained hopeful on reaching trade deal with China. President Trump was not afraid of a trade war.

- ,South Korea Trade Min: South Korea and the United States have reached an agreement “in principle” on renegotiation of their free trade agreement; South Korea to be exempted from the 25% steel tariffs

- PBoC Gov Yi Gang inaugural speech noted that China's economic performance in early 2018 had shown 'good' momentum extending from 2017; reiterated prudent and neutral monetary policy (not be too tight or too lose). Expected consumer inflation pressures to be mild in 2018.

- China Vice Premier Han Zheng inaugural speech stated that China pledged to move forward with market opening and reforms; reiterated China would treat domestic and foreign companies equally and protect intellectual property rights. Transition from high-speed growth to high-quality development would not be easy but would ensure that market played a decisive role in economy

Europe:

- Italy's 5-star and League parties said to reach agreement on election of parliamentary speakers. Roberto Fico elected as President of the lower house and Forza Italia member Elisabetta Casellati as president of the Senate

- Italian PM Gentiloni: formally resigned on Saturday, Mar 24th (as expected). President Mattarella said to have asked Gentiloni while country forms new Govt

- Former Catalonia leader Carles Puigdemont was detained by police officials in Germany (acting on an international arrest warrant issued by a judge in Spain)

- Sovereign rating:

- S&P raised Spain sovereign debt rating one notch to A- from BBB+; outlook Positive

- S&P affirmed Belgium sovereign rating at AA; outlook Stable

- S&P and Fitch affirmed Norway sovereign debt rating at AAA; outlook Stable

- Fitch affirmed Switzerland sovereign debt rating at AAA; outlook Stable

- Moody's affirmed South Africa sovereign debt rating at Baa3; outlook revised to Stable

Americas:

- San Francisco Fed President Williams (moderate, voter) thought to be leading candidate to become New York Fed President (Note: Dudley planning to step down this summer)

Energy:

- China launch its yuan denominated oil futures contract, the "petroyuan", effective, Mar 26th after long awaited approval from China State Council (as speculated)

Economic Data:

- (NL) Netherlands Q4 Final GDP Q/Q: 0.8% v 0.8%e; Y/Y: 2.9% v 2.9%e

- (SG) Singapore Feb Industrial Production M/M: -0.5% v -8.4%e; Y/Y: 8.9% v 4.2%e

- (FI) Finland Feb PPI M/M: 0.7% v 0.7% prior; Y/Y: 2.4% v 2.4% prior

- (FI) Finland Feb Preliminary Retail Sales Volume Y/Y: 2.1% v 5.1% prior

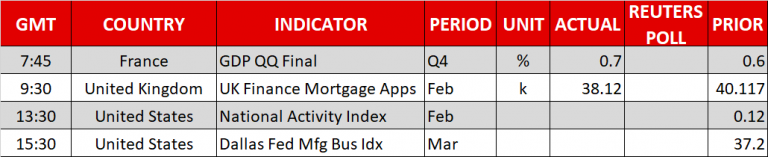

- (FR) France Q4 Final GDP Q/Q: 0.7% v 0.6%e; Y/Y: 2.5% v 2.5%e

- (CZ) Czech Mar Business Confidence: 16.5 v 17.1 prior; Consumer Confidence: 10.3 v 9.5 prior

- (UK) BBA Loans for House Purchases: 38.1K v 39.0Ke

- (IS) Iceland Mar CPI M/M: 0.6% v 0.6% prior; Y/Y: 2.8% v 2.3% prior

Fixed Income Issuance:

- (IT) Italy Debt Agency (Tesoro) sold €2.5B vs. €2.0-2.5B indicated range in 0.1% May 2023 I/L Bonds (BTPei); Avg Yield: -0.43% v -0.41% prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +04% at 367.1, FTSE +0.4% at 6946, DAX +0.6% at 11955, CAC-40 +0.4% at 5113, IBEX-35 +0.1% at 9405, FTSE MIB -0.3% at 22226 , SMI +0.8% at 8634, S&P 500 Futures +1.1%]

Market Focal Points/Key Themes:

- European Indices trade mostly higher across the board recovering from early weakness following a rebound in US Equity futures after a sharp selloff on Friday. The Swiss SMI outperforms as Alpiq trades over 5.5% higher following results and the divestment of its industrial business for CHF850M. Elsewhere in the M&A space, JD Sports announced the acquisition of Finishline for $13.50/shr; Naturex trades over 40% higher after Givaudan took a 40% stake and to launch tender for remaining shares; Smurfit Kappa trades lower after rejecting a second offer from International Paper.

Looking ahead notable earners include Paychex and Athenex.

Movers

- Consumer Discretionary [ JD Sports [JD.UK] +2% (Acquires FInishline for $13.50/shr), Inchcape [INCH.UK] +1.1% (Acquisition) ]

- Materials [Naturex [NRX.FR] +40.6%, Givaudan [GIVN.CH] +1.4% (Givaudan acquires 40.6% stake in Naturex, launches mandatory cash tender for remaining shares)]

- Industrials [ Smurfit Kappa [SKG.UK] -2.8% (Rejects 2nd proposal from IP), Speedy Hire [SDY.UK] +5.2% (Trading update) ]

- Consumer Staples [ Amplifon [AMP.IT] +1.8% (Mid term targets) ]

Speakers

- ECB's Nouy (SSM chief): Greece still needed to reduce the levels of its bad loans (NPLs)

- France Fin Min Le Maire: 2018 GDP growth forecast seen at 1.7%

- IMF chief Lagarde called for a roadmap for reducing vulnerabilities in the Euro Zone banking sector. Needed an agreement for a schedule for a common Euro Zone Bank deposit insurance scheme. Called for a modernized capital markets union and improved banking union.

- Ireland Dep PM Coveney (also foreign Min): Will focus on trying to put in place a backstop position to avoid a hard border by maintaining full alignment with rules of the single market and customs union in Northern Ireland

- Former PM Berlusconi: Northern League leader Salvini (euro-skeptic) may try to form an Italian government

- Euro Working Group chief Vijbrief: Greece will have enhanced monitoring in post bailout period

- France Stats Agency (INSEE): 2017 public deficit to GDP at 2.6% v 3.4% y/y

- Turkey Dep PM Simsek: TRY currency (Lira) depreciation has made the country more competitive

Currencies

- Some of the risk aversion flowed ebbed in the session after dealers noted a de-escalation in the current phase of trade talks. Weekend reports noted that US Treasury Sec Mnuchin was more optimistic in reaching an agreement with China noted that recent conversations with China were "very productive".

- USD/JPY moved off 16-month lows of 104.63 area to retest above the 105 area.

- GBP/USD was retesting the post BOE decision highs around 1.42 while EUR/USD was higher by 0.3% near the 1.24 handle

Fixed Income

- Bund Futures trade 22 ticks higher at 158.78 after Spain was upgraded by Fitch. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 121.57 down 25 ticks after BOE’s Vlieghe hawkish comments that UK data warrant further removal of stimulus. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Monday's liquidity report showed Friday's excess liquidity fell to €1.801T from €1.810T prior. Use of the marginal lending facility increased from €70M to €100M.

- Corporate issuance, primary markets expect $29.5B sold this week

Looking Ahead

- (IT) Italy Debt Agency (Tesoro) to sell €2.5-3.0B in Zero Coupon Mar 2020 CTZ

- 05:30 (DE) ECB's Weidmann (Germany) gives speech in Austrian Central Bank

- 06:00 (SE) Sweden Central Bank (Riksbank) Dep Gov Skingsley gives Speech

- 06:00 (RO Romania to sell 2.3% 2020 Bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Mar FGV Construction Costs M/M: 0.2%e v 0.1% prior

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 08:05 (UK) Baltic Dry Bulk Index

- 08:00 (ES) Spain Debt Agency(Tesoro) announces size of upcoming auctions

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:30 (US) Feb Chicago Fed National Activity Index: 0.15e v 0.12 prior

- 08:55 (FR) France Debt Agency (AFT) to sell combined €4.7-5.9B in 3-month, 6-month and 12-month BTF Bills

- 09:00 (BR) Brazil Feb Federal Debt Total (BRL): No est v 3.528T prior

- 09:30 (BR) Brazil Feb Total Outstanding Loans (BRL): No est v 3.066T prior; M/M: No est v -0.8% prior

- 10:00 (MX) Mexico Jan Retail Sales M/M: -0.3%e v -0.5% prior; Y/Y: -0.2%e v -2.0% prior

- 10:30 (US) Mar Dallas Fed Manufacturing Activity: 33.5e v 37.2 prior

- 11:30 (US) Treasury to sell 3-Month and 6-Month Bills

- 12:30 (US) Fed Dudley (dove, FOMC voter)

- 13:00 (US) Treasury to sell $30.0B in 2-Year Notes

- 16:30 (US) Fed's Mester Speaks on Monetary Policy

EUR and GBP builds upside momentum, Yen retreats on stablizing market sentiments

Yen clearly weakens broadly today with stabilizing market sentiments. Fear of trade war seems to fade mildly on report that the US and China are now in dialogue. At the time of writing, FTSE is trading up 0.3%, DAX up 0.5% and CAC up 0.3%. US futures also point to triple digit gain at open, as markets digest Friday's steep loss.

Euro and Sterling both showing extra strength entering into US session. Both EUR/USD and GBP/USD surges through last week's high.

Euro and Sterling both showing extra strength entering into US session. Both EUR/USD and GBP/USD surges through last week's high.

Meanwhile, for now, both NZD/JPY and GBP/JPY are having more than 1% gain for today.

Meanwhile, for now, both NZD/JPY and GBP/JPY are having more than 1% gain for today.

EURO Targering Key 1.2430 Level

The euro has broken above the 1.2400 level against the U.S dollar during the European trading session, after euro bulls pushed above past the 1.2382 resistance area. The EURUSD pair currently trades around the 1.2410 level, with buyers now moving price-action toward the pivotal 1.2430 level. Moving into the U.S trading session, the key 89.00 level on the U.S dollar is coming into focus as the greenback weakens across the board.

The EURUSD pair is strongly bullish above the 1.2430 level, further upside towards the 1.2500 and 1.2555 levels seems possible.

If the EURUSD pair falls back below the 1.2382 support level, price-action will likely correct back toward the 1.2334 and 1.2305 levels.

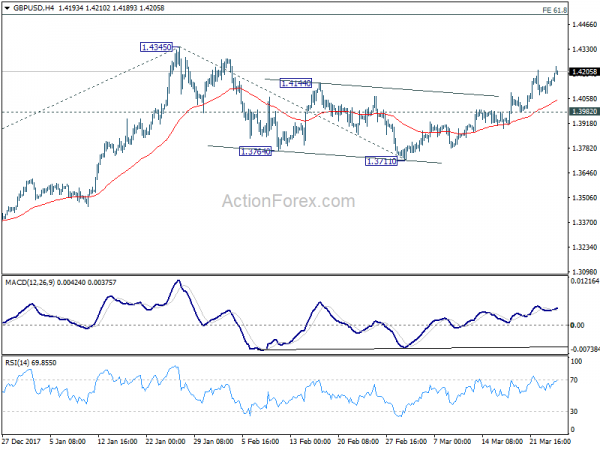

GBPUSD Strongly Bullish Above 1.4220 Level

The British pound has moved above the 1.4200 level against the greenback, as expectations of a May rate hike from the Bank of England, and a weaker U.S dollar index drive the pair higher. The GBPUSD is currently holding price-action above the 1.4200 level, with the former weekly price-high, at 1.4220, the next key upside hurdle. Once clearly above the 1.4220 level, sterling buyers will meet strong technical resistance from the pairs key 200-week moving average, located at the 1.4255 level.

The GBPUSD pair is strongly bullish whilst trading above the 1.4220 level, key technical resistance is found at the 1.4255 and 1.4279 levels.

Should GBPUSD buyers fail to gain traction above the 1.4200 level, key intraday support is located at the 1.4146 and 1.4087 levels.

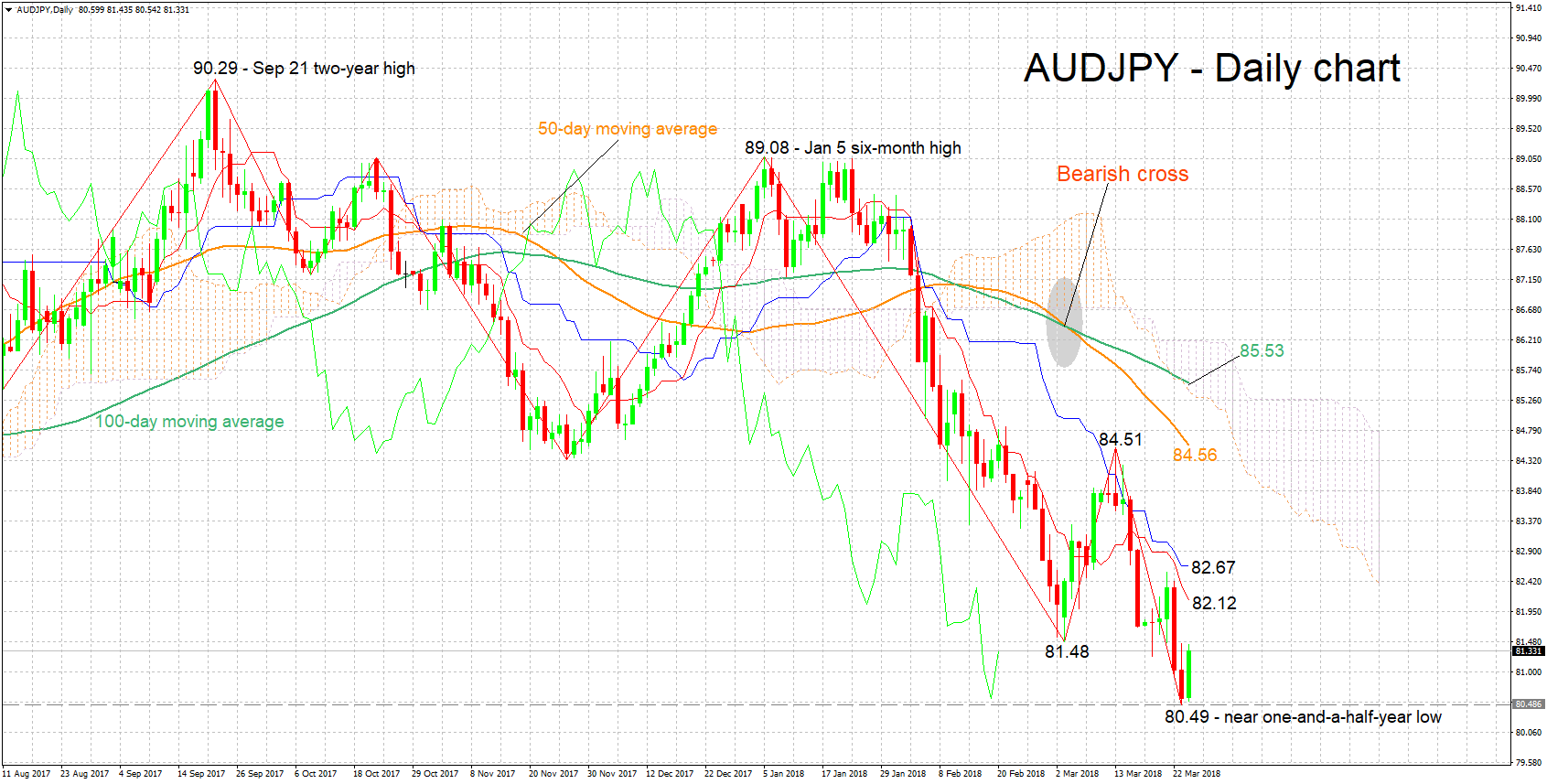

AUDJPY Looking Bearish In The Short-Term Despite Move Off 1½-Year Low

AUDJPY has shed 7.5% year-to-date and is currently trading around 80 pips above the near one-and-a-half-year low of 80.49 hit last Friday.

Despite today’s rebound, the negatively aligned Tenkan- and Kijun-sen lines continue to project a bearish short-term picture for the pair. It is of note that the Chikou Span might be hinting to a somewhat oversold market, rendering today’s recovery “justifiable”.

The pair might be meeting resistance around 81.48 – a previous bottom – at the moment, with an upside break shifting the focus to the area around the current level of the Tenkan-sen at 82.12 as an additional barrier to the upside. The range around the Tenkan-sen also includes the 82 round figure that may hold psychological significance.

Should the pair resume its declines, support could come around last week’s near one-and-a-half-year low of 80.49. Steeper losses would next turn the attention to the 80 handle that may also be of psychological importance.

The medium-term picture is clearly negative: trading is taking place well below the Ichimoku cloud as well as below the 50- and 100-day moving average lines, with both lines maintaining a negative slope. In addition, a bearish cross was recorded in early March when the 50-day MA moved below the 100-day one.

Overall, both the short- and medium-term outlooks are looking bearish at the moment.