Sample Category Title

Market Morning Briefing: Gold Continues To Remain Stable

STOCKS

Looking at the daily candles, Dow (24758.12, -1.00%) looks bearish for the coming sessions and is likely to break below 24500. The resistance on the 3-day chart seems to be holding well and the index may come off towards 24000 in the next few sessions.

Dax (12237.74, +0.14%) looks bearish towards 12000 or even lower in the near term. It would be difficult for the index to move up sharply while below 12500

The daily chart shows some scope of re-testing 21000 on the downside for Nikkei (21674.48, -0.47%) but there is support near 21400 on the 3-day chart which if holds, could initiate medium term bullishness for the index. Watch price action near 21400.

Shanghai (3286.22, -0.16%) is gradually coming down from 3350 levels. It could be stuck in the 3350-3200 region in the near term.

Nifty (10410.90, -0.15%) is stuck in the 10500-10100 region since the last couple of weeks. A fall below 10200-10100 would trigger further downside for the index; else if it moves up above 10500-10600 levels, the focus would turn to the upside.

Sensex (33835.74, -0.06%) needs to move above 34000 in order to initiate medium term bullishness. While below 34000, there is scope of re-testing levels near 33500-33000. While below 34000, near to medium term looks bearish.

COMMODITIES

Brent (64.99) and Nymex WTI (61.12) are stable without any major movement just now. The prices are likely to remain stable in the 66-64 and 59.50-60.0 zone respectively.

Gold (1326.60) continues to remain stable and could trade above 1315-1320 levels for the next 1-2 sessions without any major movement.

Copper (3.1570) almost tested 3.20 on the upside before falling off from there. Overall the price is stuck in the broad 3.2250-3.0750 region and is likely to continue so for the coming week too.

FOREX

The Dollar Index (89.665), is sustaining its break of support on daily candles near 89.75 and over the course of the next week, it might move further down towards support near 89.2-89.0 on weekly line chart. As mentioned yesterday as well, this is a crucial support level seen on a trendline coming from Mar'14, a break of which could lead to medium term bearishness.

Euro (1.2378): As predicted yesterday, the Euro seems to have found some resistance near 1.24, provided by earlier support (now resistance) trendline on the daily line chart. However, in case of a breach of the same, the Euro should test resistance near 1.25-1.255 on 3 day and daily candles over the course of the coming week. The EU CPI data release on Friday would be vital – a higher than expected figure would be bullish for Euro.

Dollar-Yen (106.06) is seeing a resumption of the downmove towards crucial support near 105.5-105.0 on the daily candles -a break of the same would confirm medium term bearishness.

The Euro-Yen (131.25) has moved down from yesterday's levels near 132 as there has been a pause in Euro strength while the Yen has continued to strengthen against the Dollar. It could move further down towards support near 130 on the weekly candles by next week. A testing of 130 however implies 105 on the Dollar Yen (if Euro stays near 1.24) – if this happens, Dollar Yen might drop further, taking Euro Yen below 130-129.

Pound (1.3977) exactly as per expectation, tested resistance near 1.4 on daily candles yesterday and has dipped from there. Immediate support is now seen near 1.39 on 3 day candles.

Dollar Rupee (64.82) may test 64.75 before again trying to move up towards 65. Overall sideways range in 64.75-65.15 expected in this week.

INTEREST RATES

After US inflation data disappointed yesterday, US retail sales fell for the third consecutive month bringing down sentiments around the US economy's growth. Some impact of both these data releases are being seen with US yields dropping further.

US 10 Year Yield (2.81), US 30 year Yield (3.05), US 5 year yield (2.60), US 2 year yield (2.25) : US yields continue to see a dip as the Fed meeting comes closer. A week of decline prior to the meeting and an eventual rate hike in the meeting might just push yields up immediately after the meeting.

Lets wait and watch how further US data releases- US Housing Starts data (Friday) and US Industrial Prodn data (Friday) impact yields. We should prepare for some volatility in US yields in the week ahead. (Long term resistance levels for the 4 yields have been as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively)

Can Gold Price Gain Upside Momentum?

Key Highlights

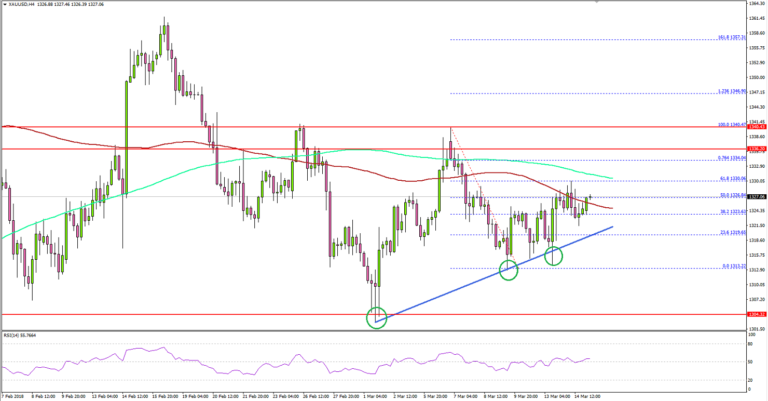

- Gold price started an upside move after forming a support above $1,300 against the US Dollar.

- There is a key bullish trend line forming with support at $1,320 on the 4-hours chart of XAU/USD.

- The US Retail Sales figure for Feb 2018 posted a decline of 0.1%, compared with the forecast of a 0.3% rise.

- The US Jobless Claims for the week ending March 10, 2018 will be released today, which is forecasted to decline from 231K to 226K.

Gold Price Technical Analysis

After a major decline, gold price formed a decent support above $1,300 and recovered against the US Dollar. The price traded higher and succeeded in moving above the $1,315 resistance area.

It traded towards $1,340 before correcting lower. Recently, an intermediate low was formed at $1,313.22. At the moment, the price is moving higher and is trading above the 23.6% Fib retracement level of the last decline from the $1,340.47 high to $1,313.22 low.

However, buyers need to break the 200 simple moving average (green, 4-hour) to gain upside momentum.

On the downside, there is a key bullish trend line forming with support at $1,321 on the 4-hours chart. As long as the price is above the trend line and $1,320, it could move higher.

US Retail Sales

The US Retail Sales figure for Feb 2018 was released by the US Census Bureau. The market was looking for a rise of 0.3% in sales compared with the previous month.

The actual result was lower than the forecast since there was a decline in sales by 0.1% instead of a rise. Looking at the US Retail Sales ex Autos figure, there was a rise of 0.2%, less than the forecast of +0.4%.

The report added:

Retail trade sales were down 0.1 percent (±0.5 percent)* from January 2018, but 4.2 percent (±0.7 percent) above last year. Nonstore Retailers were up 10.1 percent (±1.4 percent) from February 2017, while Gasoline Stations were up 7.9 percent (±1.6 percent) from last year.

Overall, the result was slightly negative, but the US Dollar was not impacted much. Having said that, EUR/USD and GBP/USD were seen trading in a positive zone.

Economic Releases to Watch Today

- SNB Interest Rate Decision – Forecast -0.75% versus -0.75% previous.

- US Initial Jobless Claims – Forecast 226K, versus 231K previous.

- US Import Price Index for Feb 2018 (MoM) – Forecast +0.2%, versus +1.0% previous.

- US Export Price Index for Feb 2018 (MoM) – Forecast +0.3%, versus +0.8% previous.

China’s February Economic Data Beat Expectations

China's economic data beat expectations in February. Headline CPI improved to +29% y/y, beating expectations of +2.5%, from January's +1.5%. On the economic activity barometers, industrial production grew +7.2% y/y in February, exceeding expectations of +6.3% and January's +6.2%. Urban fixed asset investments expanded +7.9% y/y in the first two months of the year, compared with consensus of +7% and previous reading of +7.2%. Retail sales rose +9.7% y/y last month. While the reading has missed consensus of +10%, it came in better than January's growth of +9.4%. Undoubtedly, these data were distorted by Lunar New Year. As such, March's data would be in focus.

The surge in headline inflation was mainly driven by the rally in food price. Food price inflation jumped +4.4% ,after contracting -0.5% in January, due to a +17.7% jump vegetable picce and a +22.5% jump in egg price. These offset the decline in pork price. Non-food inflation also improved to +2.5% in February from +2 a month ago, led by an increase in transportation and recreation. The underlying condition also improved with the core inflation rebounding to +2.5% from +1.9% in January. Removing the Lunar New Year effect, the combined January-February CPI data came in at +2.2%, up from +1.8% last December.

The biggest growth contributors to economic activities were industrial production and fixed asset investment. Colder-than-expected weather in February probably lifted IP growth due to higher heating demand. Meanwhile, the fact that Lunar New Year occurred in the second half of February suggests that IP growth would be better than if it had occurred in the first half. Manufacturers have a tendency to extend their holiday and shut down factories for a longer period of time than the official public holidays. Therefore, it might have some negative effects on March's figure.

Urban FAI growth has been in downtrend in the second half of 2017 as the government tightened the monetary policy targeting real estates. The rebound in February was a pleasant surprise. However, caution is advised as FAI is subject to a number of reporting issue. Yet, the strength last month might be attributed to the government's shantytown redevelopment project.

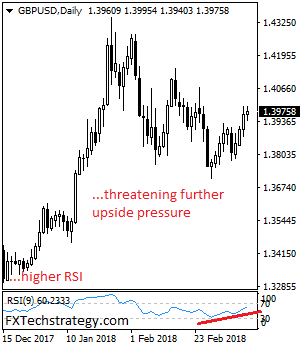

GBPUSD – Bullish, Remains Biased To The Upside

GBPUSD - The pair continues to retain its upside pressure closing higher on Tuesday and looking to extend that gain. Support lies at the 1.3900 level where a break will turn attention to the 1.3850 level. Further down, support lies at the 1.3800 level. Below here will set the stage for more weakness towards the 1.3750 level. Its daily RSI is bullish and pointing higher. Conversely, resistance stands at the 1.4000 levels with a turn above here allowing more strength to build up towards the 1.4050 level. Further out, resistance resides at the 1.4100 level followed by the 1.4150 level. On the whole, GBPUSD looks to follow through higher.

Risk – Off Continues To Seep

Risk -Off continues to seep.

Risk off continues to seep through markets as traders scramble to revise both inflation and US growth forecast in the wake of a tepid CPI and PPI prints while February’s dreary US retail sales deliver more disappointment to the markets.

The sagging USD and the fear of an escalating trade war with China have global markets on edge with investors taking a defensive posture moving from buying on dips to the more careful preservation of cash strategy. According to Investment Company Institute (ICI), U.S. fund investors withdrew billions from domestic stocks during the equity market’s tariff tantrum.

The “Rexit” to Pompeo transition continues to cast a dark cloud over the markets as investors are preparing for more market-alarming, protectionist headlines. The US is determined to reduce China’s bilateral trade surplus by 100 billion, but things are about to get very messy as reports continue to circulate that the Trump administration is ready to levy US tariffs on China imports targeting intellectual property which could come as early as this week.

All the usual go-to haven trades have been on the move, JPY is eyeing 106, EUR has found a bid while gold remains firmly supported on dips.

However, adding to the US dollar downdrafts, US yields are looking very tired approaching the significant support around. 2.80 in 10 Year US Treasuries. If the level gives it could spring a trap door type of reaction on the USD.

Despite yesterday’s robust Chinese data as industrial production and fixed asset investment surged, concern about the tariffs plagued mainland and Hong Kong equity sentiment which is unlikely to abate short term given trade war escalation is looking more likely than ever.

Reports are circulating that You’re Fired Episode #36 The Sessions Saga is about to air. However, this should not surprise as the air is rife with stories of more high profile departures are yet to come.Topping the betting boards are Ivanka & Jared Kushner, and White House Chief of Staff John Kelly.

Oil Markets

A bit of a topsy-turvy overnight session as prices initially plummeted after The U.S. Energy Information Administration reported that crude supplies rose by 5 million barrels for the week ended March 9 doubling analysts’ expectations. Nevertheless, after taking a standing eight count, prices recovered thanks to the gasoline-thirsty US consumer as Gas warehouses dropped 6.3 million barrels, and diesel inventories declined by 4.4 million barrels well more than market forecasts.

However, the Shale Oil machine is showing little signs of slowing, and with OPEC now conceding that non -OPEC oil supply, spearheaded by US shale producers, will outpace global oil demand growth in 2018, it would suggest that the path of least resistance remains lower despite this afternoon short covering rally.

Gold Markets

Gold markets have taken a break during the NY session as price action has turned a very neutral and not surprisingly so with traders in wait and see mode during this Fed blackout period ahead of the March FOMC. During these lulls in price action, the market tends to be more driven by technical rather than fundamentals.After moving to the critical trend line resistance level of $1,330 and failing to push through, the short term fast money traders were quick to take profit.

With the US dollar still holding within near-term ranges and USDJPY appearing extremely sticky above 106.00, Gold bulls will need some help from a more defined USD negative bias to break above trendline resistance. Nevertheless, when considering the negative overtones in global equity markets, drops in gold prices should prove short-lived.

Currency Markets

The Euro

Topside momentum was chilled thanks to ECB President Draghi who sounded the caution alarm at the ECB and Its Watchers Conference. Again emphasising that inflation was the most critical factor and that there was no rush to remove stimulus while Euro strength is driven by exogenous factors not supported by economic expansion.

The Australian Dollar

The Aussie outperformance comes down to China data. Specifically, Industrial production increased by 7.2%YoY in February vs 6.2% consensus expectations that lit a fire under the industrial metals complex underpinning the AUD despite risk aversion creeping into the pictures.

The Japanese Yen

If it were not for the Yen’s propensity to move on shifting risk sentiment, I do not think the pair would have any momentum. The USDJPY remains very sticky in the 106 handle, but if this latest test of the 106.00 level ends in more disappointment for Yen bulls out of frustration alone traders will start reducing long JPY positions, and on that narrative alone we could test above 107 again.

The Malaysian Ringgit

The market opened supportive yesterday as bond market flow looked strong but USDMYR traded bid as regional equity market risk-off momentum gathered steam after news of Tillerson’s departure. However, with USDMYR remaining well bid overnight despite the USD sagging suggests suspected foreign repatriation of funds for quarter-end /year-end were driving spot higher overnight.

Gold Remains Listless As US Records Mixed Numbers

Gold has ticked lower in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1324.62, down 0.14% on the day. On the release front, consumer spending was a disappointment, as Retail Sales declined 0.1%, missing the estimate of 0.3%. On the inflation front, PPI dipped to 0.2%, but still beat the estimate of 0.1%. On Thursday, the US will publish employment claims and the Philly Fed Manufacturing Index.

Gold has been drifting for most of the week, continuing the trend which marked the base metal last week. One reason for the lack of movement is that investors are trying to get a handle on what the Federal Reserve has planned under new chair Jerome Powell. The Fed is expected to continue to raise rates gradually, but a strong economy and the massive tax cuts could mean that the hikes will of greater size and frequency in the past. Any hints about rate policy will likely impact on gold, which moves inversely to interest rate levels.

The Federal Reserve is widely expected to raise interest rates next week. According to the CME Group, the odds of a quarter-point raise stand at 89 percent. What can we expect from the Fed during the year? The pressing question is how many rate hikes will we see in 2018. The current Fed projection remains at three hikes, but the superb nonfarm payrolls report last week has raised speculation that the Fed could accelerate the pace to four hikes, which would be good news for the US dollar. Investors will be keeping a close eye on key US data, especially inflation indicators. If these numbers improve, we’re likely to see four rate hikes in 2018.

Retail Signs Ignored

A third consecutive contraction in US retail sales threatens the enthusiasm about the US economy this year. Ashraf's chart below shows the other two occasions when retail sales fell for for 3 straight months. The yen was the top performer while the euro lagged.

Economists began lowering their Q1 US growth estimates below 2% Wednesday after a soft reading on retail sales. The consensus was for a 0.3% m/m rise but spending was down 0.1%. It was the first time sales had contracted for three straight months since 2012. The details were also weak with the control group up 0.1% compared to +0.4% expected.

A sign of trouble?

That's doubtful. The dip in sales comes after several strong months late last year and numerous data points have been strong, including jobs and sentiment data. The tax cut may also surely provide a tailwind to growth in the months ahead. That sentiment was reflected in the market reaction to the report. The US dollar dipped on the headlines but recovered shortly afterwards.

What's more pressing is the path of inflation. On that front, US PPI was a touch on the hot side Tuesday at 0.2%. Politics is also an endless soap opera but the main focus right now should remain the steel and aluminum targets due in two weeks and how affected countries respond.

Also note that equities and USD/JPY have lately struggled to hold intraday gains. Ten-year Treasury yields are also near the lows of the month. Those might be early-warning signs about trouble in broader markets.

Traders are increasingly concerned about protectionist rhetoric and so far Trump's talk far exceeds the actions but a few more steps towards a trade war could spark a quick rush to the exits.

Finally, now Bitcoin falling below the March lows on Wednesday, partly caused by Google's decision to stop advertizing from ICOs. The February low of 5,920 marked the bottom of the Head & Shoulders formation. Bears looking for a retest.

Eco Data 3/15/18

[php_everywhere instance="1"]

USD Falls On Washington Politics. CPI Rises At A Slower Pace

The U.S. dollar was seen declining as the day unfolded with President Trump removing Rex Tillerson and appointing CIA director Pompeo as the secretary of state. The changes sparked speculation of the increasing number of officials who are more favorable towards protectionist policies.

On the economic front, consumer prices in the U.S. matched expectations rising 0.2% on the month in February, but the increase was slower compared to January's gain of 0.5%. The annual CPI was seen rising to 2.2% from 2.1% as expected while core inflation rate was steady at 1.8%.

Developments on Brexit also dominated the news wires as the EU President Jean-Claude Junker and the chief negotiator Barnier were seen turning up the heat on the negotiations just a week before the EU conference. They asked UK to come up with solutions on the Irish border. The UK also released the Spring statement with Chancellor Hammond giving an upbeat view. He also said that the cost of Brexit to the UK's economy was estimated to be 38 billion GBP.

Looking ahead, the ECB President Mario Draghi will be speaking at the ECB Watchers conference which could be a key event risk for the euro currency. Retail sales from the U.S. will be released later in the day and is expected to rise 0.3% on the month, reversing the declines from January.

Currencies: US Political Noise Weighs On The Dollar

- Rates: US political uncertainty takes the upper hand

The bar to beat today's US eco data isn't that high. However, we don't think that investors are willing to set up big new short positions in core bonds ahead of the Fed meeting given increased US political risk. The latter took the upper hand yesterday. ECB heavyweights Draghi, Constancio and Praet are scheduled to speak. Will they give more details on the end of APP? - Currencies: US political noise weighs on the dollar

US president Trump firing Secretary of State Tillerson blocked any further USD gains. Today's eco calendar contains US PPI and retail sales. Several ECB members speak in Frankfurt. The eco data and the ECB message might be USD supportive/euro negative. However, it uncertain whether this will be enough to counterbalance the US political news flow.

The Sunrise Headlines

- US stock markets ended 0.65% to 1% (Nasdaq) lower after President Trump fired Secretary of State Tillerson. Asian stock markets lose around 0.5% overnight.

- Democrat Lamb and Republican Saccone were locked in a virtual dead heat with nearly all of the votes counted in Pennsylvania's special election for a US House seat. Mr. Lamb carried a lead yet the margin was so tight the race won't be decided until local officials finish counting absentee ballots

- US President Trump is seeking to impose tariffs on up to $60bn of Chinese imports and will target the technology and telecommunications sectors, two people who had discussed the issue with the Trump administration said.

- China's factory output (7.2% Y/Y) and investment growth (7.9% Y/Y) unexpectedly accelerated in the first two months of the year amid robust global demand. Retail sales (9.7% Y/Y YTD) were near consensus.

- G20 financial leaders will pledge to fight unfair trade practices and stress the role of global trade rules when they meet on March 20, as the US raises the threat of a global trade war by imposing import tariffs on steel and aluminium.

- Most BoJ policymakers shared the view that the central bank should "persistently" pursue powerful monetary easing, though some called for the need to scrutinise the potential drawbacks of massive stimulus.

- Today's eco calendar contains EMU industrial production, US retail sales and US PPI data. Several ECB members speak. Germany and Portugal tap the market.

Currencies: US Political Noise Weighs On The Dollar

US political noise weighs on the dollar

Dollar sentiment was neutral (USD/EUR) to modestly positive yesterday in the run-up to the US CPI release. CPI was exactly as expected. However, the market reaction was disturbed by President Trump firing Secretary of State Tillerson. Markets hesitated, but sentiment turned risk-off. US yields, equities and the dollar all declined. This was both due to a soft interpretation of the CPI and as a reaction to US political tensions. EUR/USD closed the session at 1.2390. USD/JPY reversed a big part of the intraday rebound and finished at 106.58.

Chinese eco data (retail sales, production, Fixed assets investments) were OK overnight, but insufficient to balance the negative spill-over effects from the US. Core yields are holding near yesterday's lows. The dollar remains in the defensive. EUR/USD hovers in the 1.24 area. USD/JPY is changing hands in the 106.50 area. For now, the moves both in equities and on the FX market still develop in an orderly way.

US retail sales and PPI take center stage today. Markets will also keep a close eye on a conference in Frankfurt. Several ECB board members, including President Draghi, are scheduled to speak. US retail sales are expected to rebound after a poor January reading. Base effects might also be supportive for the PPI data. We see a good chance for both series to meet or even exceed the consensus. Question is whether this will be enough to counterbalance the US political noise. In Frankfurt, we expect the ECB to confirm a gradual approach on policy normalization. If Draghi and Co back the scenario of a gradual scaling back of APP beyond September, it should in theory be a euro negative. Yesterday, US political risk was the dominant factor for USD trading. Eco data and ECB talk might be EUR/USD negative, but it is far from sure that it will change fortunes for the dollar. We expect more nervous EUR/USD trading near current levels. A break beyond intermediate resistance at 1.2450 would open the way for a retest of the 1.2550/1.26 area. A break of the 1.2155 support looks difficult shortterm.

Yesterday, sterling initially traded with a cautious upward bias as the half year budget update contained some cautiously positive news. However, in the end EUR/GBP closed little changed. There are again no UK eco data today. A global risk-off sentiment is no help for sterling. So EUR/GBP might hold close to or even return north of 0.89.

EUR/USD: US political uncertainty blocks USD gains. Will US data be strong enough to change fortunes for the dollar