Sample Category Title

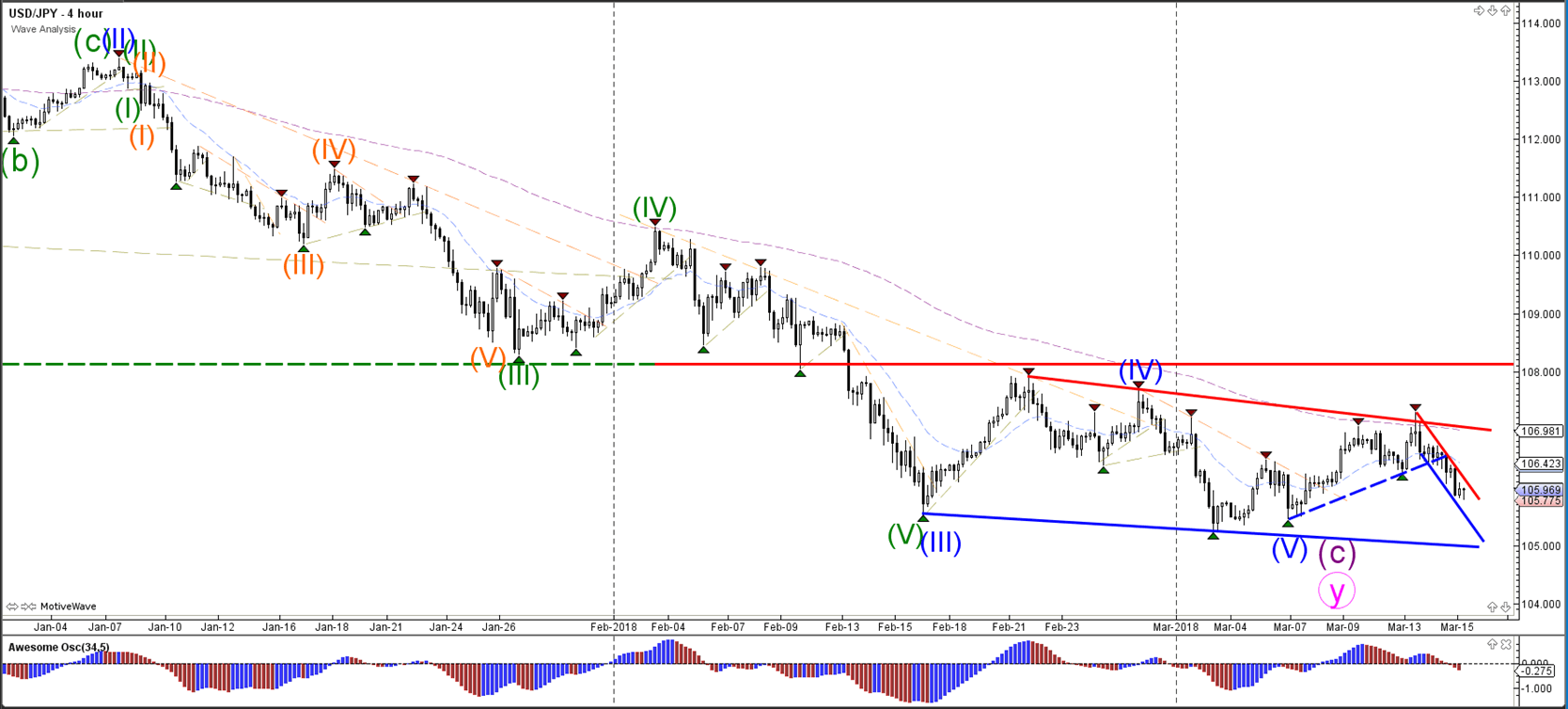

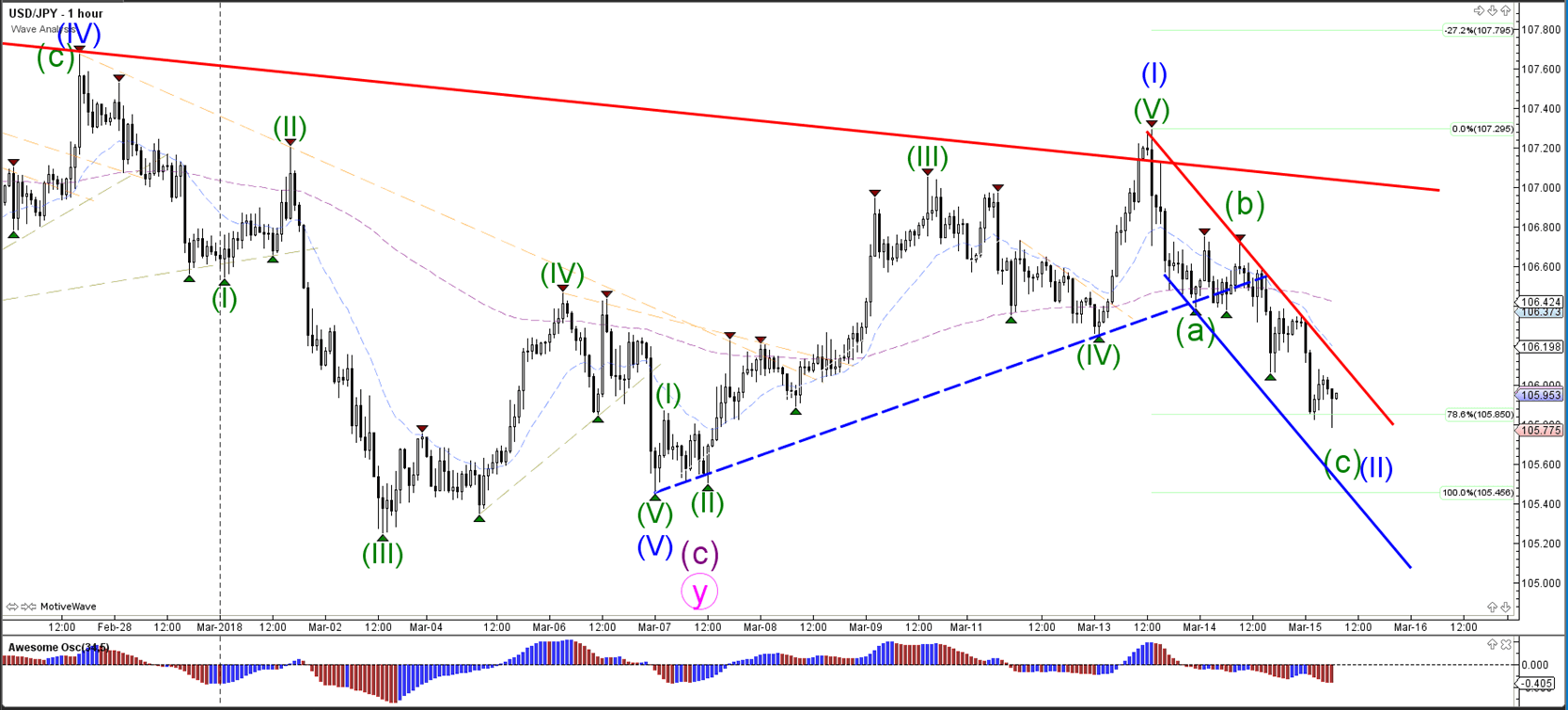

USDJPY Remains In Bearish Phase, Unable To Break Below 16-Month Low

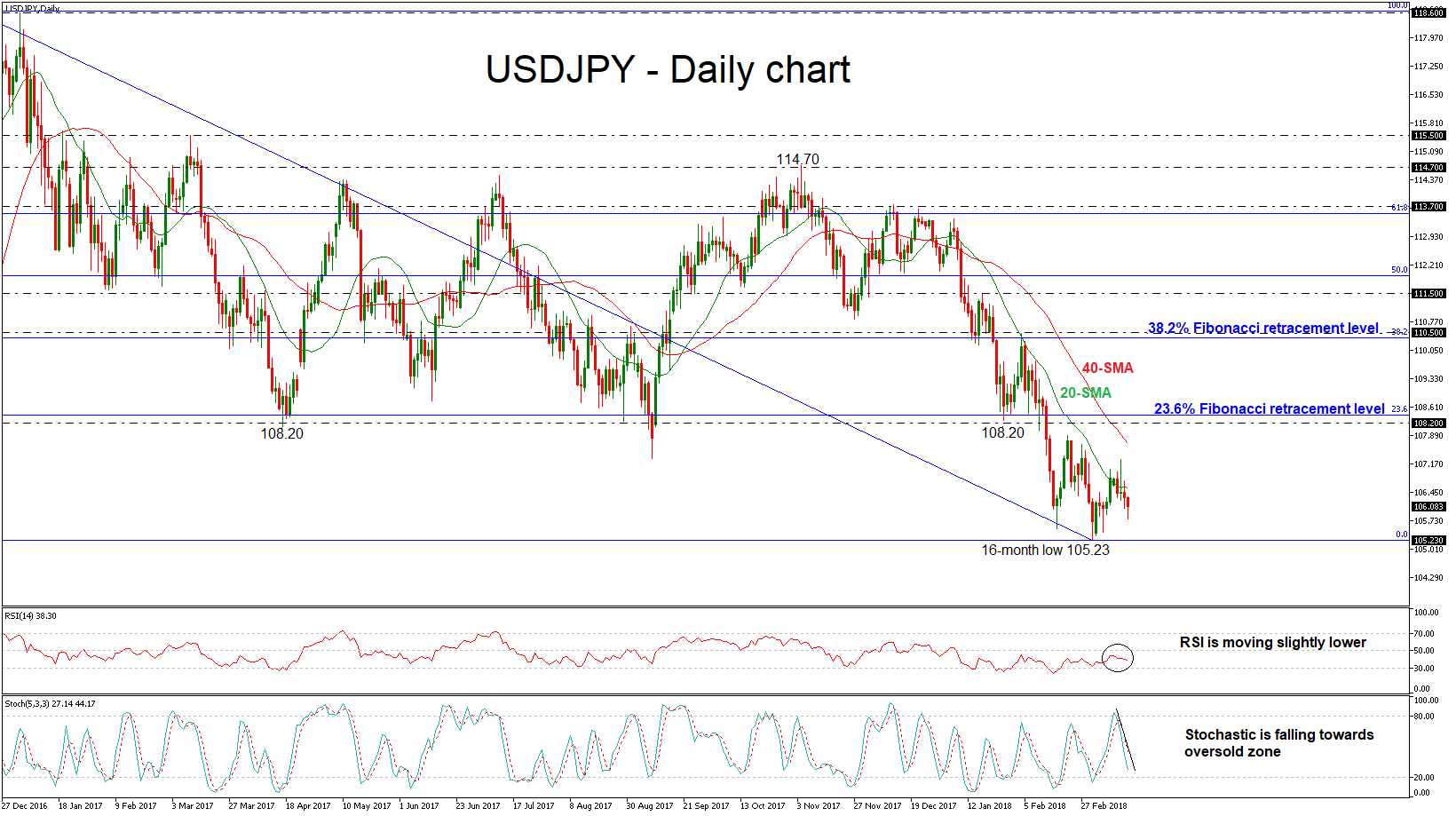

USDJPY fell as low as 105.77 during today’s European session and is recording another negative day. The drop below the 108.20 strong resistance level has pushed the price further lower, creating a 16-month low of 105.23. When looking at the bigger picture, in the weekly timeframe, the price has been trying to break the aforementioned level over the last three weeks.

The negative bias in the near term is supported by the deterioration in the momentum indicators. The %K and %D lines of the stochastic oscillator are falling sharply towards the oversold area, while the RSI indicator is moving lower in the negative zone with weak momentum.

For the time being, 106.00 holds as support for USD/JPY, but a move above 107.00 would be needed to ease the negative flows. However, if prices continue to head lower below the 105.23 support barrier, this could open the way towards the next significant psychological level of 101.00 taken from the low of November 2016.

On the flip side, should an upside reversal take form, the next pause could be on the 40-day simple moving average near 107.70 before a run until the 23.6% Fibonacci retracement level at 108.40 of the downleg from 118.60 to 105.23. A break above this area could shift the bias back to a bullish one, with the next resistance coming from the 38.2% Fibonacci level near 110.50.

Swiss Franc mixed ahead of SNB rate decision.

The SNB meeting today would bring no change in the monetary policy. Policymakers would reiterate the pledge to intervene the currency market in defense of excessive appreciation of Swiss franc. However, the is less urgency for the central bank to act given the strength in the euro.

CHF is trading up again most currency except Sterling for the week. It's supported by risk aversion, just like JPY. But for today, there is no follow through buying. Indeed, in the current 4 hour period, there is some selling seen ahead of SNB.

Action bias also reveal that CHF is generally neutral.

Action bias also reveal that CHF is generally neutral.

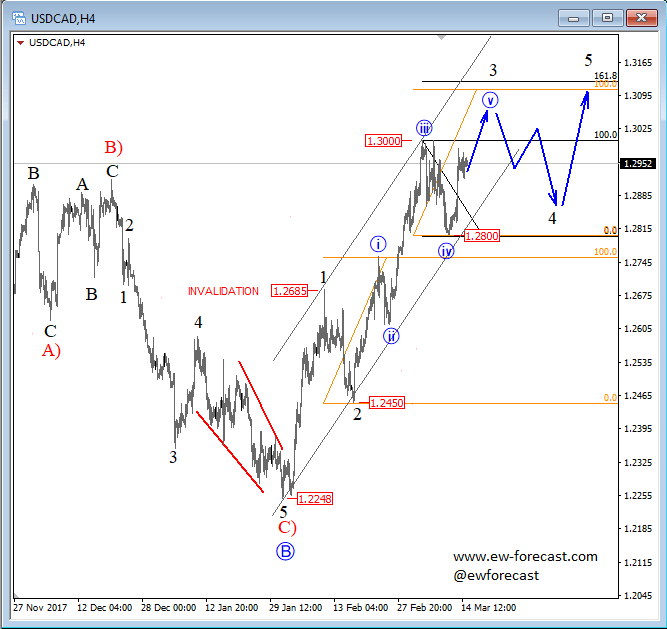

USDCAD Can See Resistance Around 1.3071/1.3140 Zone

USDCAD made a strong and sharp reaction recently, which we now see it as part of sub-wave v of 3. As such base for the past sub-wave iv was found at the 1.2800 level. All being said, current rally can now target 1.3071/1.3140 region, where various Fibonacci ratios of 100.0 and 161.8 project end of wave 3. At the same region bulls can slow down, and corrective wave 4 may start to show up.

USDCAD, 4H

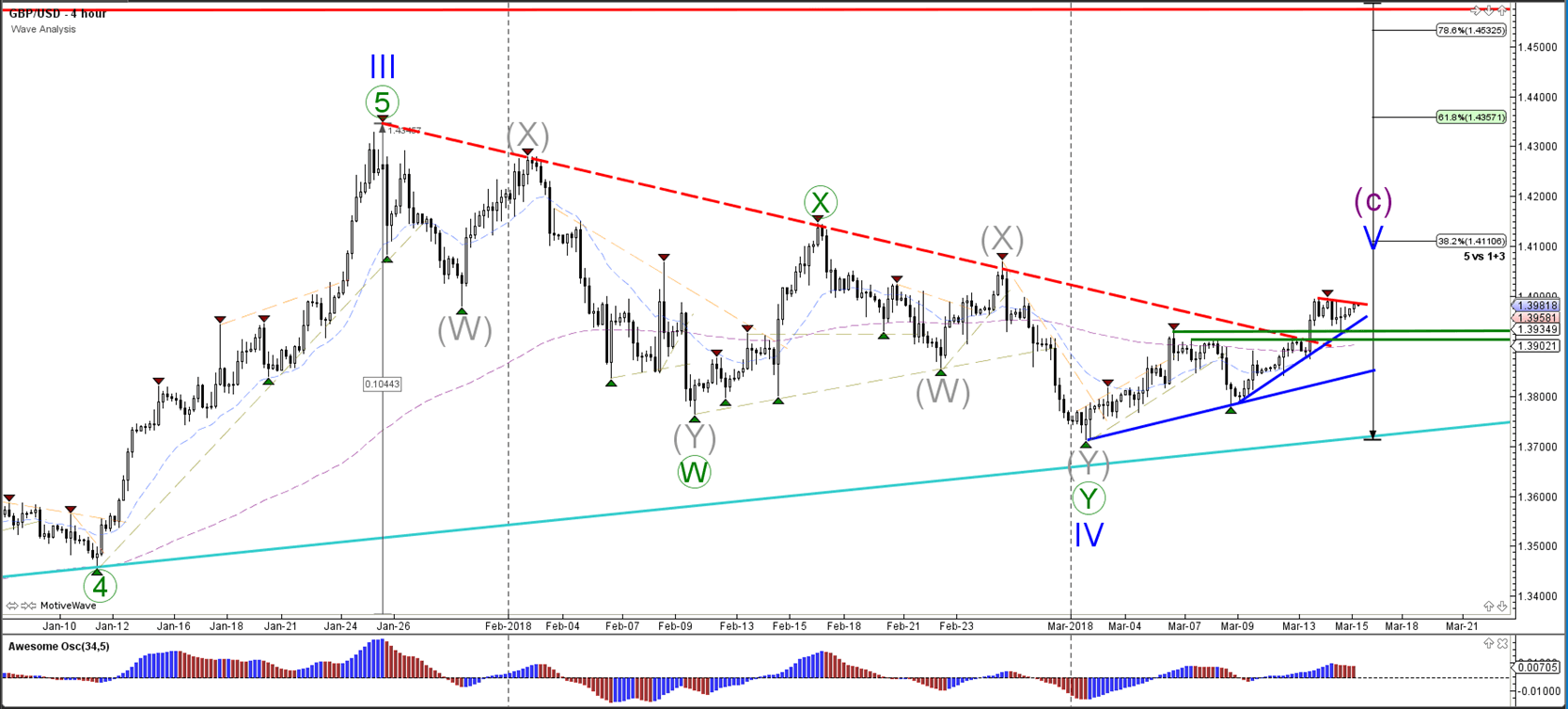

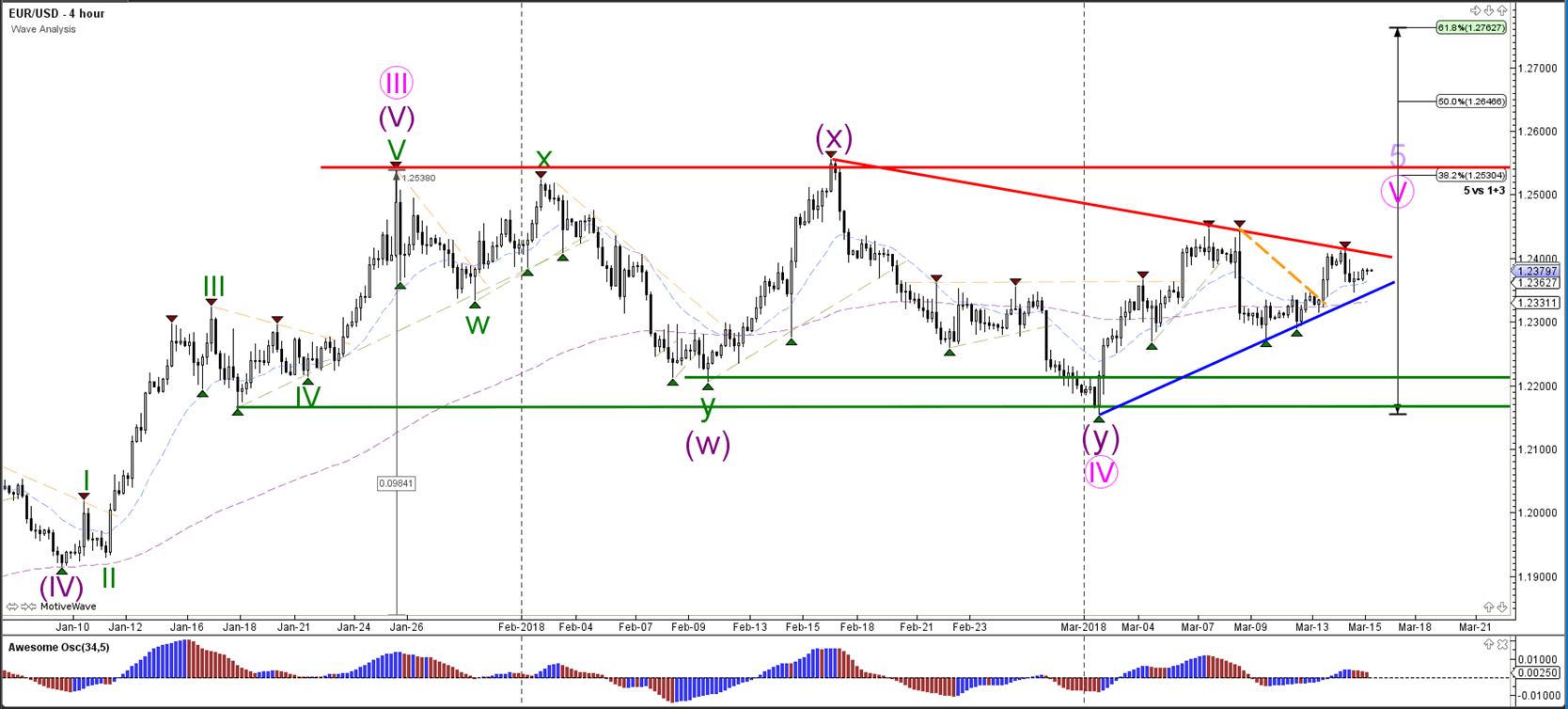

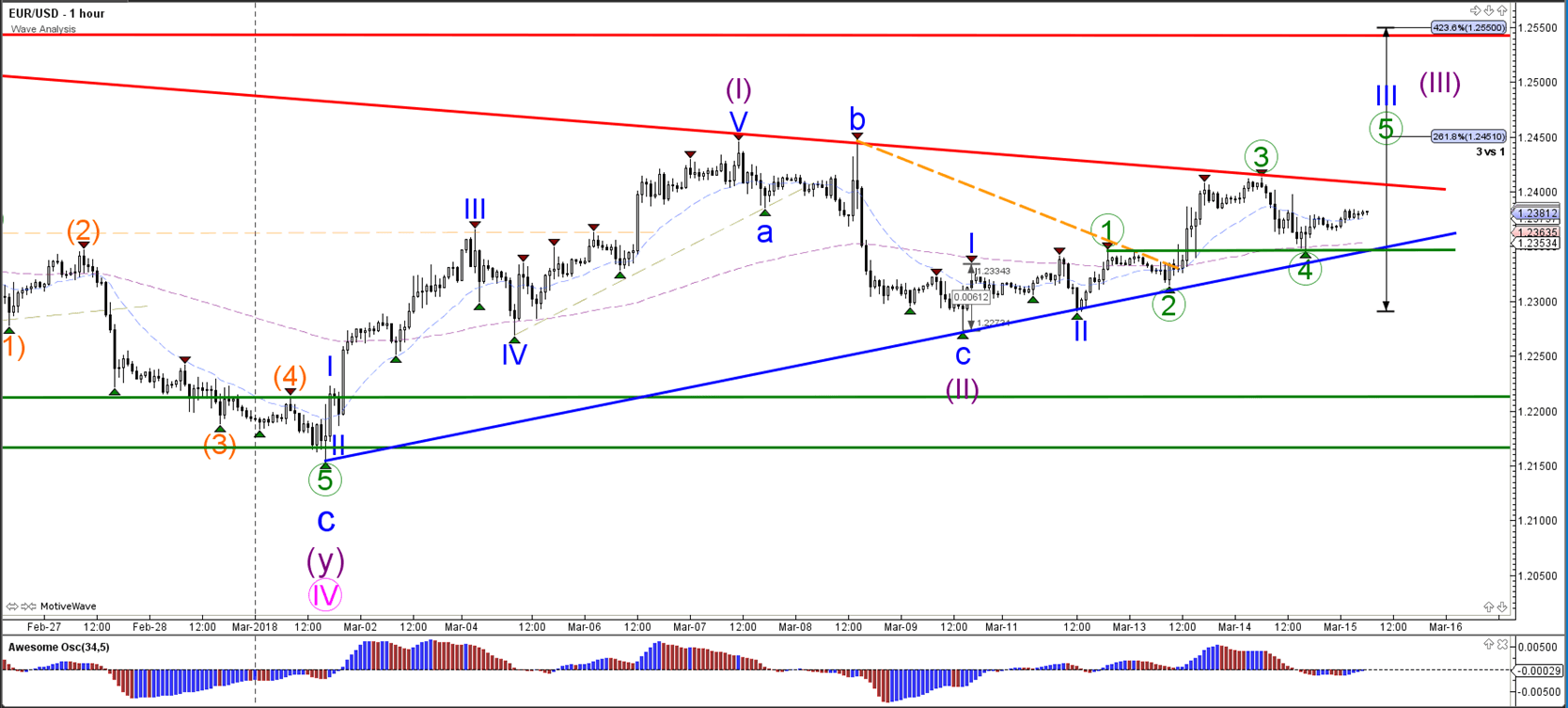

Daily Wave Analysis: EUR/USD, GBP/USD Bounce At Previous Tops Within Wave 4 Patterns

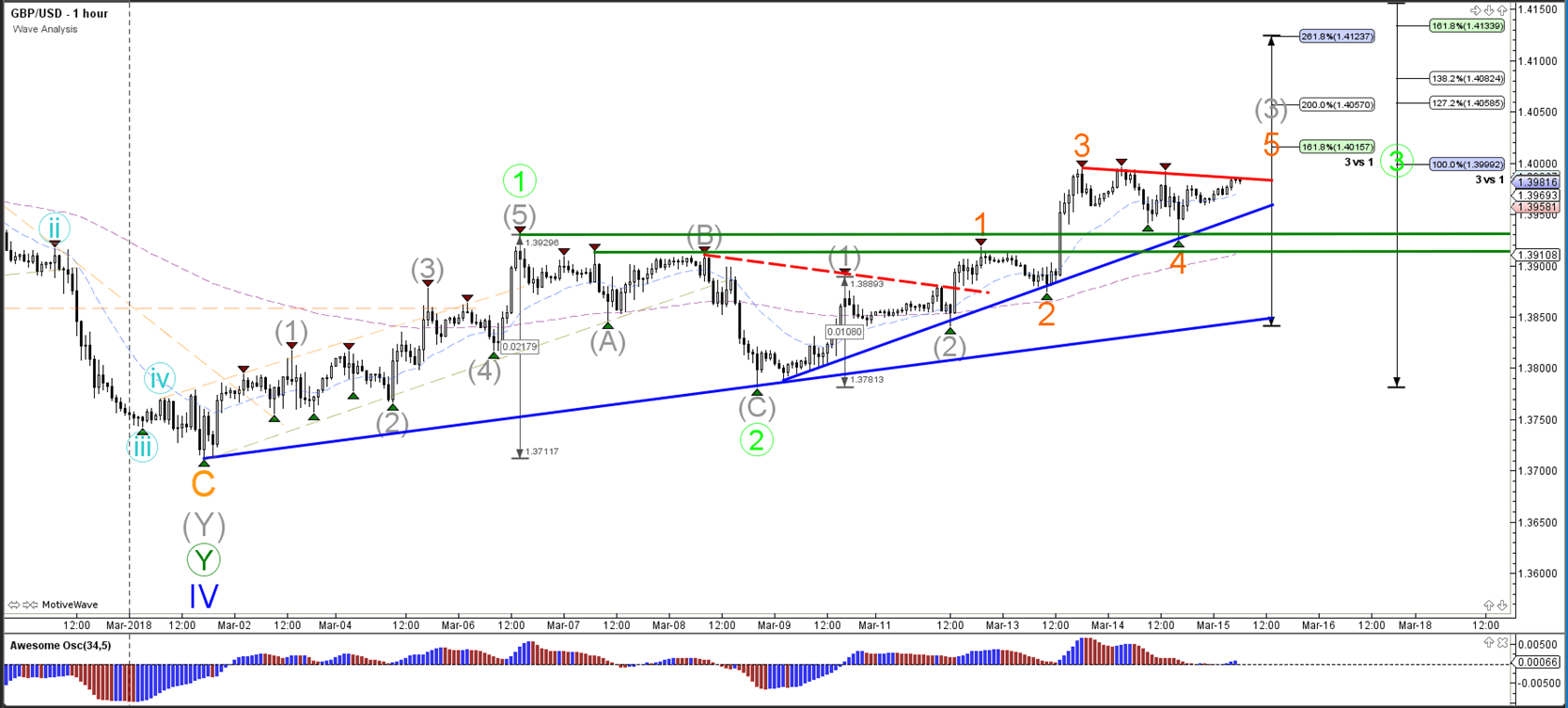

Currency pair GBP/USD

The GBP/USD made a break and pullback above the long-term resistance trend line (dotted red) and is now testing a lower time frame resistance level. The next break could be a bullish continuation within wave 5 (blue). Price will need to stay above the support trend lines (green) otherwise the uptrend is in danger.

The GBP/USD bounced at the previous tops (green lines), which could be explained by a potential wave 4 (orange) pattern. A bullish breakout could confirm the continuation of the wave 3 (grey).

Currency pair EUR/USD

The EUR/USD is still in a triangle pattern and will need to break above the resistance trend line before more momentum can be expected.

The EUR/USD bearish retracement did not break below the top of wave 1 (green line) which makes a wave 4 (green) still possible. A break of below it invalidates the wave pattern and a bullish breakout confirms it.

Currency pair USD/JPY

The USD/JPY broke below the support trend line (dotted blue) and is starting a new bearish channel.

The USD/JPY could be building a potential bearish ABC (green) within wave 2 (blue) but price will need to bounce at or above the 100% Fib level, otherwise the wave 1-2 (blue) pattern is invalidated

French CPI, SNB Interest Rate And US Initial Jobless Claims

At 07:45 GMT, French Consumer Price Index (EU norm) (YoY) (Feb) will be released. The consensus is for 1.3% from 1.4% previously. This data is expected to contract, after the monthly reading slipped under 0%, and is expected to remain there again on this occasion. However, this year’s seasonal drop has been much less than previously, giving some hope for future readings. EUR pairs could move due to this data.

At 08:30 GMT, the Swiss National Bank Interest Rate Decision and SNB Quarterly Bulletin will be released. The Interest Rate is expected to be left on hold at -0.75%. Close attention will be paid to the Quarterly Bulletin for insights on future policy. CHF crosses may see volatility pick up as a result of this event.

At 12:30 GMT, US Initial Jobless Claims (Mar 9) is expected to be 226K from 231K previously. Continuing Jobless Claims (Mar 2) is expected to be 1.90M from 1.87M previously. Philadelphia FED Manufacturing Survey (Mar) is expected to be 23.0 against 25.8 previously. USD crosses may be moved by this data. Jobless Claims had been holding steady above the 200 mark for much of 2017, with extremes at 300 above and 130 below over the course of the year. The data has remained above 100 since November of 2011, showing that the US jobs market is robust and performing steadily. Philly Fed Survey has been declining since its high in February 2017 but has remained above 20.0 over the last six months.

At 15:45 GMT, the ECB’s Lautenschlager is due to make a scheduled speech and, as a member of the ECB’s executive board, her comments could affect EUR crosses.

At 21:30 GMT, New Zealand Business NZ PMI (Mar) will be released, with a prior reading of 55.6. After a fall in the January read, this data point recovered in February. This index has remained above 50 since December 2012. NZD crosses may be moved by this data.

At 22:45 GMT, RBA Assistant Governor Debelle is due to make a scheduled speech about risk and return in a low rate environment, at the Financial Risk Day event hosted by the Centre for Financial Risk, in Sydney. Audience questions are expected and comments may affect AUD crosses.

Larry Kudlow Confirmed As Chief Economic Advisor As US Retails Dip Again

Yesterday, Larry Kudlow accepted the role of White House Chief Economic Advisor. He immediately targeted China and said that the next step is for the US to deal with the stealing of intellectual property by the Chinese. He also said that China has not played by the rules of trade for a long time and they have earned a tough response. He said that he does not think that the announced trade tariffs will hurt the US economy.

German Harmonised Index of Consumer Prices (YoY) (Feb) was released, coming in as expected, unchanged at 1.2%. In line with expectations, EURUSD fell from 1.23987 to 1.23852 due to this data.

ECB President Mario Draghi spoke at the ECB conference hosted by the Institute for Monetary and Financial Stability, in Frankfurt. His comments were: Monetary policy adjustments will remain predictable. Sustained adjustment in the path of inflation towards the target is the condition for net asset purchases to end. The ECB still needs to see further evidence that inflation dynamics are moving in the right direction. The Euro strength could weigh on inflation down the line. EURUSD moved lower from 1.23889 to 1.23632 as a result of his comments.

US Retail Sales (MoM) (Feb) was released coming in at -0.1% v an expected 0.3%, from -0.3% previously, which was revised up to -0.1%. Retail Sales ex Autos (MoM) (Feb) was 0.2% v an expected 0.4% from 0.0% prior, which was revised up to 0.1%. Retail Sales Control Group (Feb) was 0.1% v an expected 0.4%, from 0.0% prior. As expected, auto sales dragged on the figures, as demand caused by hurricane season dried up. This was seen in the CPI data, which showed a 0.2% fall in auto prices and the second month of declines for sales in auto dealerships, which were down 0.9%. As a result, the expected bounce back from last month’s number was less than expected. Other declining sectors were furniture, electronics and grocers. Building material stores gained 1.9% after a 1.7% decline in sales last month. EURUSD initially moved higher to 1.23964 after opening at 1.23814 but then declined to 1.23487 after this data release.

The ECB’s Coeure made a scheduled speech and his comments were: ECB stimulus will add around one-third of a percentage point to 2018 GDP growth. Monetary policy can do little to life growth rates in Europe.

New Zealand Gross Domestic Product (QoQ) (Q4) was 0.6% v an expected 0.7%, against 0.6% previously. This marks the third time in the last five readings that the number has missed expectations, with the GDP number remaining at 0.6% and appearing to be stable. Gross Domestic Product (YoY) (Q4) was 2.9% v an expected 3.1%, against 2.7% previously. GBPNZD moved higher after the data release from 1.90332 to 1.91101.

Foreign Investment in Japanese Stocks (Mar 9) was released, coming in at ¥-432.5B. The prior reading was ¥-463.4B. Foreign Bond Investment (Mar 9) was ¥-1,090.0B against a previous ¥-1,188.5B. As a result, USDJPY continued its move lower, falling to 105.820.

Australian Consumer Inflation Expectation (Mar) came in at 3.7%, against a prior 3.6%, showing a steadying in the figure which has been at 3.7% since November, barring the slip to 3.6% last month.

EURUSD is unchanged overnight, trading around 1.23652.

USDJPY is down -0.25% in early session trading at around 106.050.

GBPUSD is up 0.08% this morning, trading around 1.39724.

Gold is up 0.05% in early morning trading at around $1,325.30.

WTI is up 0.15% this morning, trading around $61.05.

The Swiss National Bank (SNB) Holds Its Quarterly Policy Meeting

Market movers today

The key event in the Scandi markets will be the Norges Bank (NB) meeting today. Although we do not expect any changes to the key rate, we expect the interest rate path to be revised up a little this year, and slightly more in 2019 and 2020 (for more see next page).

We also get Danish housing market statistics for Q4 17 and Prospera inflation expectations in Sweden.

The Swiss National Bank (SNB) holds its quarterly policy meeting; we expect unchanged rates and few new policy messages, see next page.

Globally, we have a quiet day in terms of the calendar , with few global market movers released. Instead markets will likely continue to watch for political developments in the US and Italy.

Selected market news

It has been a relatively quiet session with equities mixed in the US and Asia alike and minor drops in US Treasury yields . Weighing on sentiment are mounting UK-Russian tensions as UK Prime Minister May expelled a number of Russian diplomats and suggested a freeze of Russian state assets after Russia's alleged poisoning attack on British soil.

Disappointing retail sales out of the US had a clear dampening effect on sentiment yesterday, signalling a weak start for private consumption in Q1 despite very high optimism on the back of the tax reform. That said, we still believe private consumption will remain a key US growth driver this year, as employment continues to rise, real wage growth is stable and confidence is set to remain high.

USD crosses were little moved by comments from US President Trump's new economic advisor, Larry Kudlow , that one should 'buy King dollar and sell gold'. Kudlow is a former investment bank economist and best known for his CNBC appearances - one in which he yesterday confirmed that he is a hardliner on trade and protectionism and offered the above-mentioned 'trading recommendation'. He went further to comment on monetary policy, saying the Fed should not 'overdo' it in terms of raising interest rates. While the US now has a top economic advisor advocating that a 'great country needs a strong currency' and that 'stability is key', speculation that the US Treasury could abandon its 'strong dollar' policy may fade. However, in our view that does not change the fact that the fiscal policies being pursued are USD-negative via the deteriorating effects on the US 'twin deficits'.

A range of Japanese carmakers announced decent wage increases for workers overnight as the reporting season kicked off with notably Toyota saying that averages salaries would rise by 3.3% this year. While better than feared, this will likely still fall short of exerting any pronounced upward pressure on inflation because base wages (ex bonuses and benefits) are set to rise by less. Thus it may still fall short of Abe's call for a 3.0% or more increase and USD/JPY fell back below 106 on the news and extended the decline due to lingering trade war concerns.

Market Update – Asian Session: NZ GDP Lower Than Expected

Headlines/Economic Data

General Trend:

Asian equity markets generally pare losses

Financials continue to be weighed down by decline in bond yields

Cathay Pacific Airways [293.HK] rises over 9% in the aftermath of FY17 earnings

South Korea sold more than indicated amount of 50-year bonds

New Zealand Q4 GDP misses ests: Stats Bureau notes impact of hot summer on agricultural sector

There are concerns that Moritomo scandal could delay approval of BoJ Deputy Gov candidates (Japan Press)

Foreign investors have continued to sell Japanese equities, according to weekly data

USD/JPY falls below 106, at the same time Nikkei 225 hit fresh low, while S&P futures weakened

Japan

Nikkei 225 opened -0.3%; closed +0.1%

TOPIX Real Estate Index +0.7%; Securities -1%

Mega-banks track weakness in US financials

(JP) BoJ said to start to worry that political scandal could leave two deputy gov seats vacant - Japanese Press

(JP) Nikkei looks at Spring wage increase in Japan, noting most have offered a modest increase, lower than PM Abe's target of 3%

(JP) BoJ may have declined to issue conditions for yield-curve control (YCC) target adjustment in order to give it flexibility in policy decisions – Japanese Press

(JP) Japan Govt will change drug approval regulations to give approvals without human testing if it has enough data to back up efficacy – press

(JP) There is renewed press speculation that Finance Min Aso will not attend G20 - Japanese Press

(JP) Japan MoF sells ¥1.0T v ¥1.0T indicated in 0.50% (prior 0.60%) 20-yr bonds; avg yield 0.5430% v 0.5610% prior; bid to cover 4.47x v 4.44x prior

(JP) BoJ Gov Kuroda: Japan has been implementing strong QE; inflation has been steadily rising in the last 2-yrs

(JP) Japan Fin Min Aso: Have to make use of low interest rate environment

(JP) Japan ruling party Diet affairs official: Fin Min Aso to skip G20 finance chief meeting next week. Aso is scheduled to participate in a session of the Budget Committee of the House of Councillors on Monday to answer questions from lawmakers.

(JP) Japan Parliament Lower House to vote on BOJ nominees tomorrow

Korea

Kospi opened flat

(KR) South Korea and China to hold FTA service and investment talks on March 22-23

(KR) Bank of Korea (BoK) Gov Lee: Reiterates inappropriate to link policy and governor reappointment

(KR) South Korea sells KRW325B v KRW300B indicated in 50-year bonds at 2.64%

China/Hong Kong

Hang Seng opened -0.8%, Shanghai Composite -0.4%

Hang Seng Property/Construction Index +0.4%; Energy -1.1%

(CN) China regulators considering reform of airline fuel surcharge

(CN) PBOC sets yuan reference rate at 6.3141 v 6.3205 prior

(CN) China PBoC Open Market Operation (OMO): Injects CNY40B v CNY50B prior in 7 and 28-day reverse repos; Net injection CNY40B v CNY50B prior

Australia/New Zealand

ASX 200 opened flat; closed -0.2%

ASX 200 Financials Index -0.9%, Energy -0.7%

(NZ) NEW ZEALAND Q4 GDP Q/Q: 0.6% V 0.8%E; Y/Y: 2.9% V 3.1%E

(AU) Australia ACCC released its Interim Report into residential mortgage products: Mortgage pricing in Australia is not strongly competitive

Aurizon, AZJ.AU Australia ACCC raises concerns about Pacific National's proposal to acquire intermodal assets

(AU) Australia Mar consumer Inflation Expectation: 3.7% v 3.6% prior

(AU) Australia Feb RBA Govt FX Transactions (A$): -438M v -634M prior

Looking Ahead: RBA Assistant Gov Debelle due to speak on Friday

Other Asia

(ID) Indonesia reported 3rd consecutive trade deficit in Feb; exports missed expectations

(TW) Taiwan Central Bank Gov Yang Chin-Long: No need to set inflation target; FX market less predictable since US President Trump

North America

US equities ended lower, Dow and S&P closed down for 3rd straight session: Dow -1%, S&P500 -0.6%, Nasdaq -0.2%, Russell 2000 -0.5%

S&P500 Materials -1.2%, Financials -1.1%, Industrials -1.1%; Utilities +1%

(US) White House confirms Larry Kudlow has accepted the position of NEC chairman

(US) Incoming White House economic advisor Kudlow: would like to see the dollar "a wee bit stronger"; No one has ever devalued their currency into prosperity - CNBC interview

(US) Commerce Sec Ross: Will soon publish rules on tariff exemptions

(US) Sources say Pres Trump has discussed a plan to fire Attorney General Jeff Sessions - Vanity Fair

(US) DOE CRUDE: +5.0M V +2.5ME

Europe

(EU) EU said to consider 3% tax on the revenues of technology companies - US financial press

(EU) ECB's Coeure (France): Euro area growth relies too much on monetary support; ECB stimulus will add one third of a percentage point to 2018 GDP growth this year

(UK) CEOs from some of UK's leading corporations to meet with UK PM May on Thurs to discuss concerns about Brexit - Sky News

Looking Ahead: Swiss National Bank (SNB) due to hold rate decision, IEA expected to release monthly report

Levels as of 01:00ET

Hang Seng -0.1%; Shanghai Composite -0.5%; Kospi +0.3%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.2%; FTSE100 +0.1%

EUR 1.2383-1.2365; JPY 106.36-105.78; AUD 0.7885-0.7863;NZD 0.73-0.73

Apr Gold +0.1% at $1,326/oz; Apr Crude Oil 0.0% at $60.97/brl; May Copper -0.2% at $3.14/lb

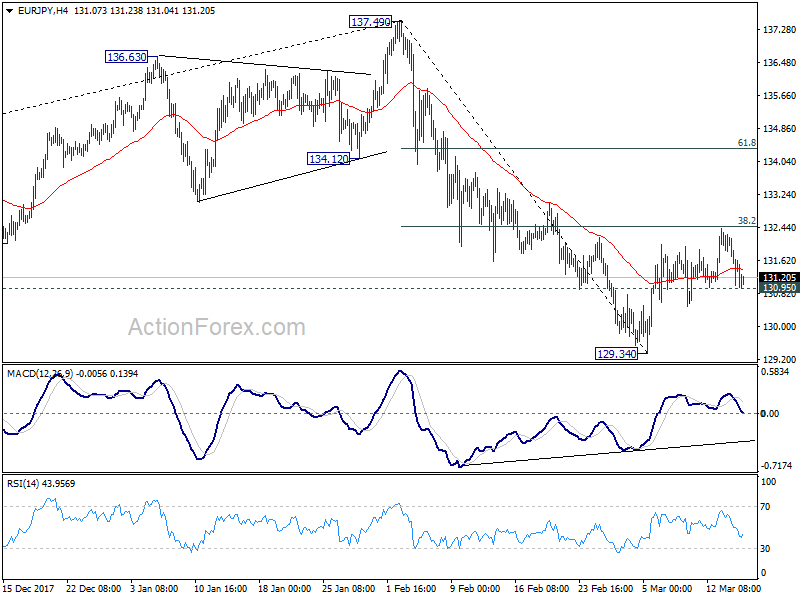

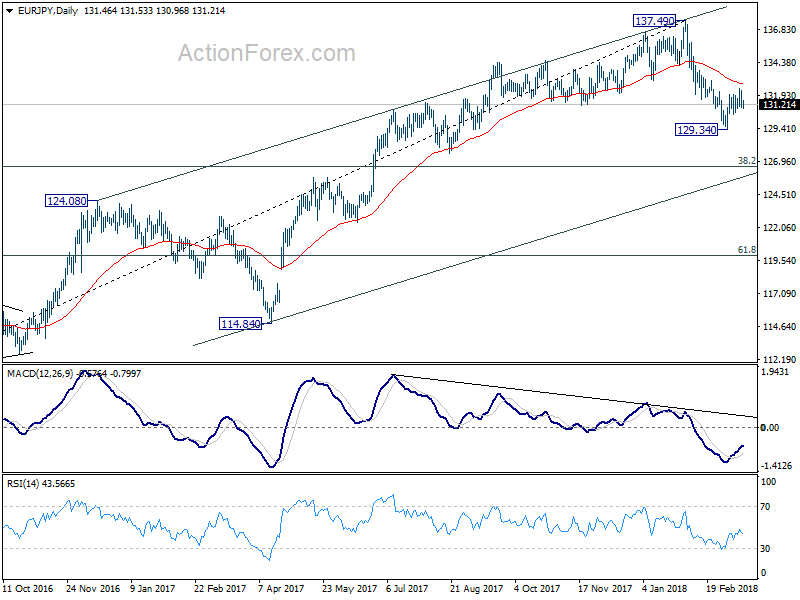

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.91; (P) 131.60; (R1) 132.17; More....

Intraday bias in EUR/JPY remains neutral at this point. In case of another rise, we'll stay cautious on strong resistance from 38.2% retracement of 137.49 to 129.34 at 132.45 to finish the corrective rise from 129.34. Below 130.95 minor support will turn bias to the downside for retesting 129.34. Break of 129.34 will resume the whole decline from 137.49 to 126.61 medium term fibonacci level. Nonetheless, sustained break of 132.45 will target 61.8% retracement at 134.37 first, before resuming the fall from 137.49.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

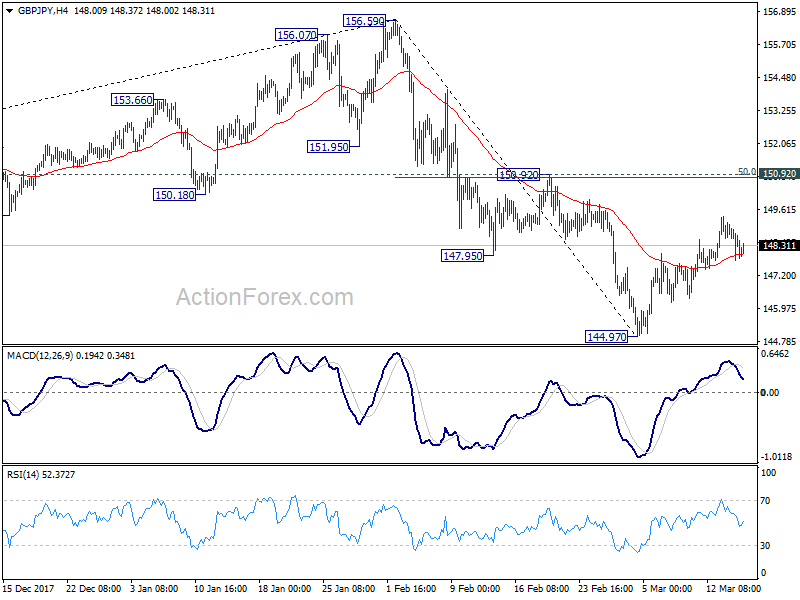

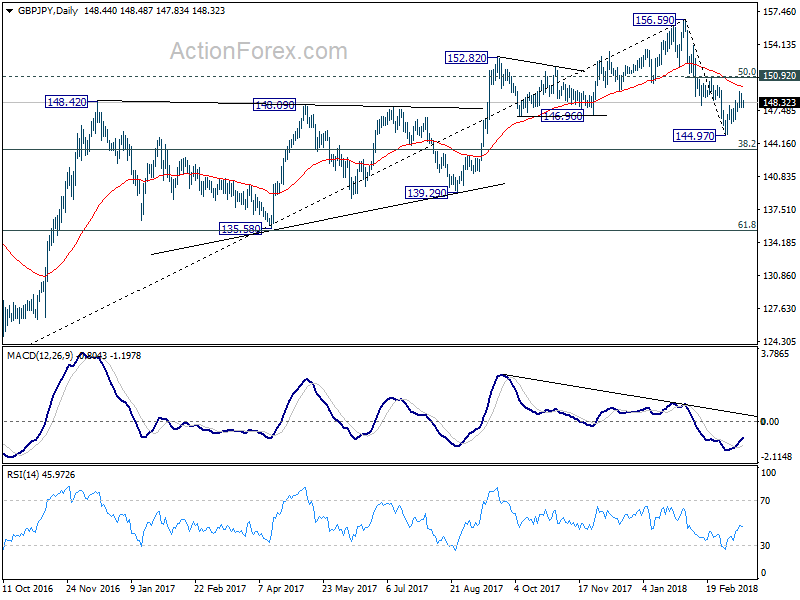

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.74; (P) 148.44; (R1) 149.15; More....

No change in GBP/JPY's outlook. The corrective rise from 144.97 is still in progress and could extend higher. But, upside should be limited by 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption. Break of 144.97 will extend the decline from 156.59 to 143.51 medium term fibonacci level next.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.