Sample Category Title

XAUUSD Intraday Analysis

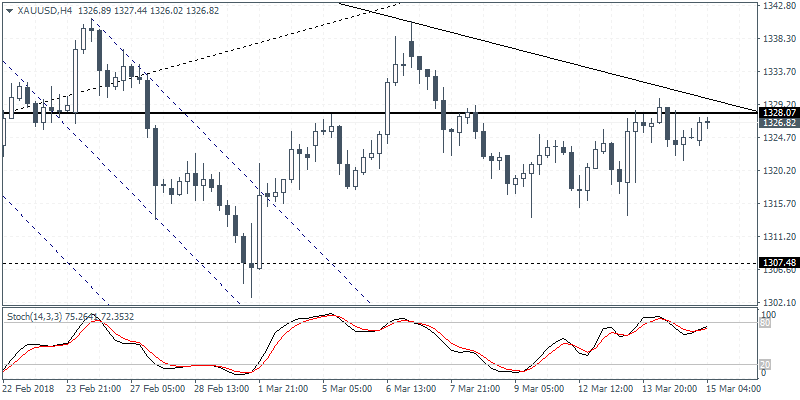

XAUUSD (1326.82): Gold prices were seen posting a consolidation just below the 1328 level. Price action has been flat for nearly four days trading around the major resistance level. To the upside, a break above 1328 could see gold prices testing the falling trend line which could act as dynamic resistance. Further gains can be expected only on a close above the trend line. Alternately, a reversal around the 1328 region could signal gold prices slipping back to the 1307 level of support.

GBPUSD Intraday Analysis

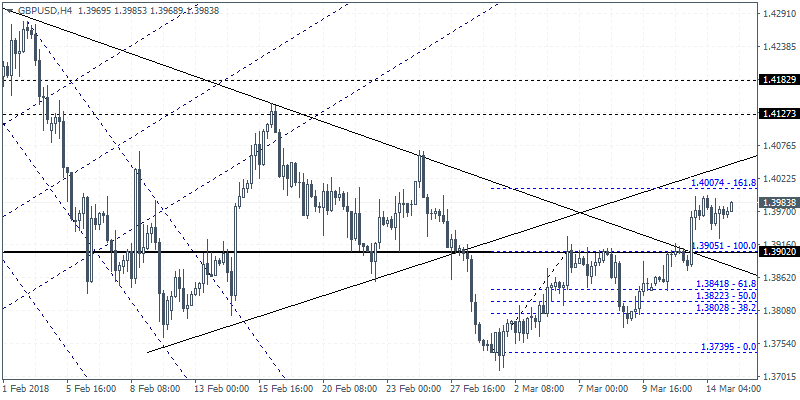

GBPUSD (1.3938): The British pound continued to edge higher on the day but price action was seen giving up the intraday gains to close with a doji. With price supported above 1.3902 we expect to see some consolidation taking place at this level. On the 4-hour chart, GBPUSD is yet to test the initial ascending triangle target at 1.4007 region. Any near-term corrections could see GBPUSD dipping back to 1.3905 level to establish support.

EURUSD Intraday Analysis

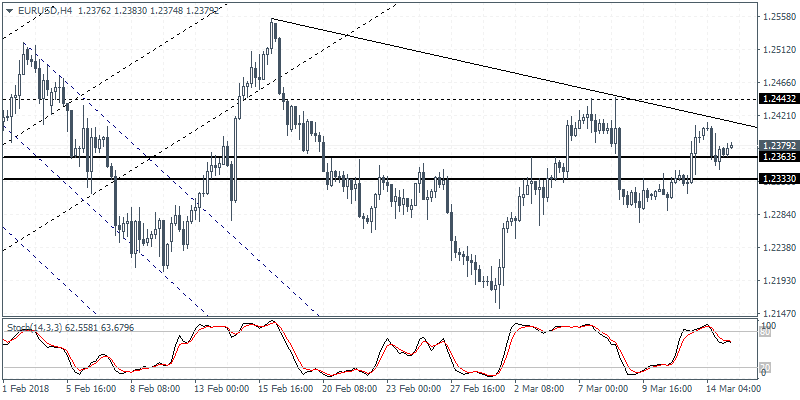

EURUSD (1.2379): The EURUSD was seen trading weaker yesterday following Tuesday's strong gains. Price action remains range bound however but with the euro finding support at 1.2363 level of support, we expect to see price action trading above this price in the near term. The breakout from the falling trend line could potentially keep EURUSD biased to the upside with the potential for the currency pair to target the previous highs at 1.2443. To the downside, a strong close below 1.2330 is required in order to shift the bias to the downside.

SNB And Norges Bank Meetings

The uncertainty in the USD continued to linger as the first quarter GDP projections were revised lower following a weak retail sales report. Headline retail sales fell 0.1% in February marking a third month of decline and missed expectations of a 0.3% increase.

German inflation report for February showed no change while the industrial production figures for the Eurozone also came out weaker than expected. ECB President Mario Draghi spoke at the ECB Watchers conference yesterday where he said that officials will remain patient and accommodative as inflationary pressures are yet to build. Later in the evening, New Zealand GDP data showed that the economy expanded at a pace of 0.6% in the quarter ending December. This was below forecasts with the annual GDP rate for 2017 rising at a slower pace.

Looking ahead, the Swiss national bank will be holding its quarterly monetary policy meeting today. No changes are expected from the central bank at today's meeting. The Norges bank will also be holding its monetary policy meeting today. Interest rates are expected to remain steady at 0.5%.

Dovish SNB stands pat, lowers inflation forecasts

SNB left sight deposit rates unchanged at -0.75%, three-month Libor range at -1.25% to -0.25%, as widely expected. Inflation forecasts for 2018 and 2019 are lowered due to Swiss Franc's appreciation to Dollar. SNB maintained that negative rate and intervention are essential

Latest forecasts:-

- 2018 inflation forecast: 0.6% (prior 0.7%)

- 2019 inflation forecast: 0.9% (prior 1.1%)

- 2020 inflation forecast: 1.9%

- 2018 GDP forecast: around 2%

Key quotes from the release:-

- Since the last monetary policy assessment in December, the Swiss franc has appreciated slightly overall on the back of the weaker US dollar.

- The Swiss franc remains highly valued.

- The negative interest rate and the SNB's willingness to intervene in the foreign exchange market as necessary therefore remain essential.

- The SNB continues to expect GDP growth of around 2% for 2018 and a further gradual decrease in unemployment.

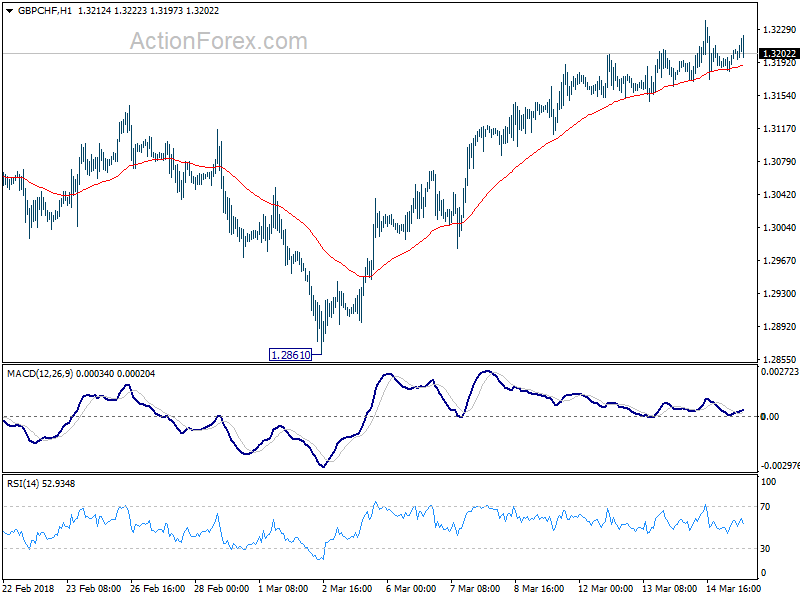

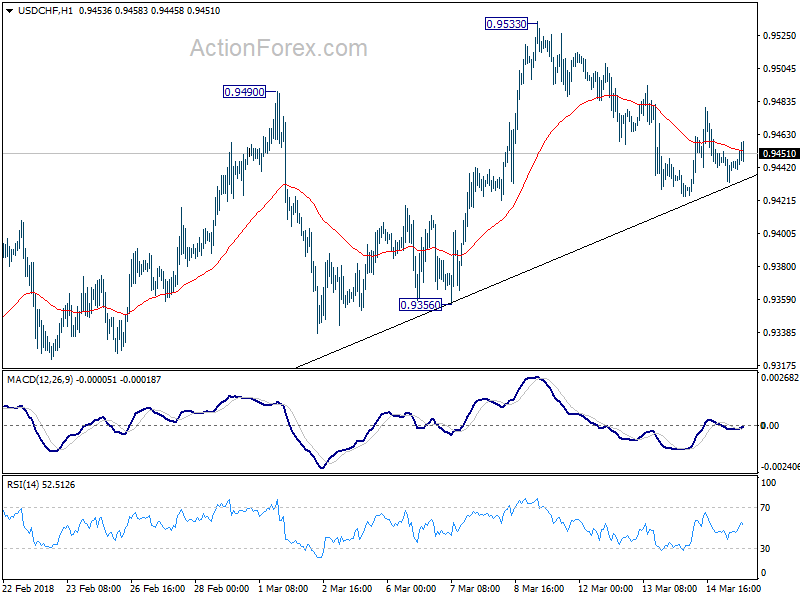

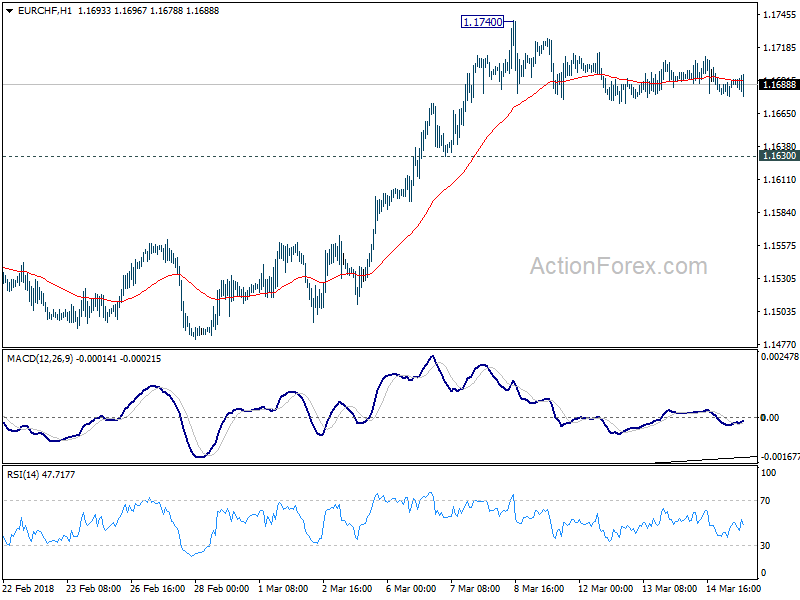

Market reactions to the release is muted as seen from EUR/CHF, USD/CHF and GBP/CHF below.

Dollar Falls Versus Yen With Trade Worries Back In The Forefront, SNB & Norges Bank Decisions Eyed

Here are the latest developments in global markets:

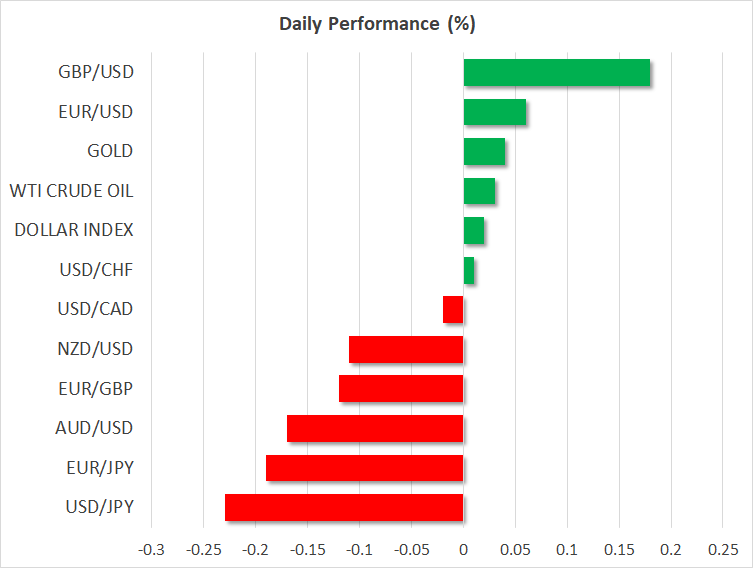

FOREX: The dollar was roughly flat versus a basket of currencies on Thursday, though it was losing ground versus the safe-haven perceived yen as risk sentiment was dented on worries over rising trade tensions. Elsewhere, the kiwi came under pressure after New Zealand's growth numbers fell short of forecasts.

STOCKS: US markets closed lower yesterday, as concerns over the possibility of a trade war with China continued to undermine risk appetite. The Dow Jones tumbled by 1.0%, the S&P 500 fell 0.6%, while the Nasdaq Composite declined by 0.2%. That said, futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a positive open today. Asian markets were mostly higher, albeit not significantly so. In Japan, the Nikkei 225 gained 0.1%, while the Topix barely closed in the green. In Hong Kong, the Hang Seng climbed by 0.3%. Europe was a more optimistic story, with futures tracking all the major indices being safely in positive territory, signaling that these benchmarks may open higher.

COMMODITIES: In energy markets, oil prices experienced another volatile session yesterday. They initially fell after the weekly EIA data revealed a larger-than-anticipated build in crude inventories, but managed to recover almost all of their losses in the following hours. Both WTI and Brent crude are trading practically unchanged today. In the near-term, prices will likely continue to be driven by any updates around the surge in US production, as well as risk sentiment in general. In precious metals, gold prices are also more or less flat today, last trading near the $1325 per ounce mark. It's worth noting that the reduction in investors' risk appetite has done little to support gold in recent days, with traders seemingly favoring the Japanese yen instead as a safe-haven play.

Major movers: Dollar retreats versus yen on trade worries, retail sales also weigh on currency; kiwi records losses as growth numbers disappoint

The dollar index was little changed at 89.73 after adding 0.1% the previous day. The greenback was losing ground versus the yen though, which was attracting safe-haven flows on the back of investors' angst over a possible escalation of global trade tensions. Dollar/yen was 0.25% down, having fallen to an eight-day low of 105.77 earlier in the day.

US equities came under pressure on Wednesday following weaker-than-expected retail sales data, but also the Trump administration's intention to impose fresh tariffs on China which weighed on risk appetite. Markets seem to fear tit-for-tat retaliatory actions by China that might push the situation out of control. The aforementioned disappointing retail sales figures also acted to the US currency's detriment.

Following the narrative that US officials will seek a weak-dollar policy, especially after some comments made earlier in the year by US Treasury Secretary Steven Mnuchin, it is interesting that Larry Kudlow, the incoming director of the White House National Economic Council, supported a strong dollar yesterday, adding that it is important for the health of the US economy. Still, the country's stance on trade seems to have much greater capacity to drive the currency at the moment than such comments on dollar strength.

Euro/dollar traded higher by less than 0.1% at 1.2371, after being hurt yesterday following some dovish-perceived comments by ECB President Mario Draghi. Meanwhile, pound/dollar traded higher by around 0.2% at 1.3982, not far below yesterday's two-week high of 1.3996.

The kiwi came under selling pressure earlier in the day as New Zealand Q4 GDP figures surprised to the downside. It is notable though that the currency managed to recover a significant part of earlier losses, with kiwi/dollar trading lower by 0.1% at around 0.7320 at 0731 GMT. Aussie/dollar was 0.15% down at 0.7865. Both the aussie and the kiwi posted three-week highs versus their US counterpart during Wednesday's trading.

Day ahead: SNB & Norges Bank policy decisions in the spotlight

During the early European session, both the Swiss National Bank (SNB) and Norway's Norges Bank will announce their rate decisions, at 0830 GMT and 0900 GMT respectively. With regards to the SNB, the forecast is for no change in policy, so investors will likely be looking for signals on whether the Bank is contemplating an eventual exit from its negative interest rates policy. That said, with Swiss inflation still subdued, the Bank is unlikely to provide any such signals, especially since doing so would risk a sharp appreciation in the exchange rate that could make it even harder for inflation to reach its target. A broadly dovish tone on policy and a reiteration that the Swiss franc remains “highly valued”, could bring the currency under renewed selling interest on the news, particularly versus the strong euro.

As for the Norges Bank, it is expected to keep its policy unchanged as well and thus, focus will be on any signals regarding the timing of the first planned rate hike in Norway. The latest projections the Bank provided back in December suggested that the first hike could come in December 2018 and markets will concentrate on whether that timing is brought forward, or pushed backwards. Taking a look at economic data, they suggest that a hawkish revision in the rate path may be more likely, as the unemployment rate has stayed very low, GDP growth is solid, and core inflation surprised to the upside in February. Should the Bank indeed signal that a September rate hike has now become more likely for instance, the NOK could gain on the decision.

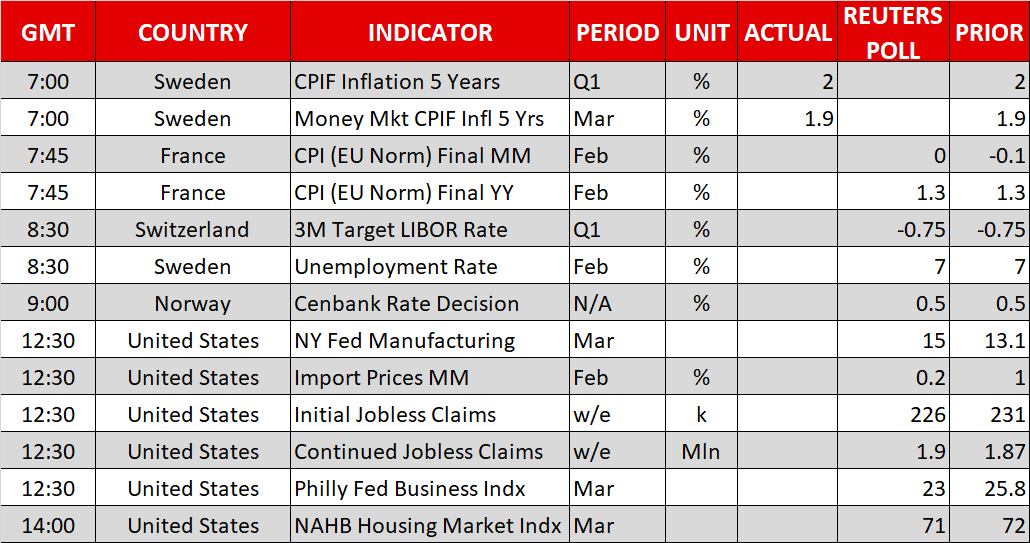

In terms of economic data, the only noteworthy releases will be in the US. Both the New York Fed and the Philly Fed will release their manufacturing surveys for March, at 1230 GMT. While neither of these is usually a major market mover, they could provide some indications of how the manufacturing sector fared in the final month of the first quarter. At the same time, the nation will also release its initial jobless claims for the week ended March 9, while at 1400 GMT, the NAHB housing market index for March is due out.

In equity markets, investors will continue to be on the lookout for updates on the trade front, as they gauge the probability of recent tensions escalating into a full-blown trade war. In particular, any news regarding the tariffs that the US is reportedly preparing against China will be of importance. Note that the newly-appointed director of the National Economic Council, Larry Kudlow, noted yesterday that China has “earned a tough response” on trade.

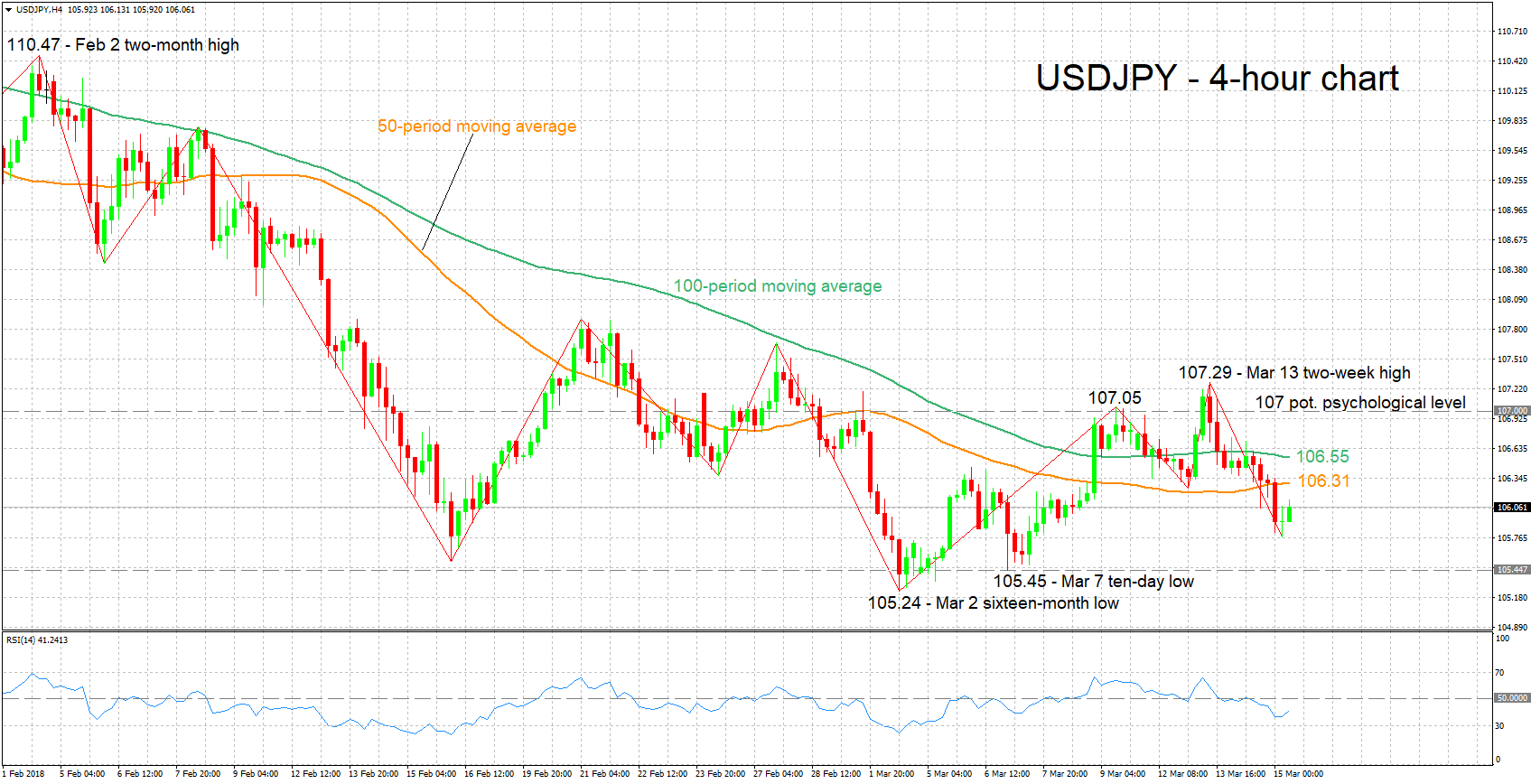

Technical Analysis: USDJPY posts 8-day low; looking bearish in the near-term

USDJPY has declined after reaching a two-week high of 107.29 on March 13. Earlier on Wednesday the pair recorded an eight-day low of 105.77. The RSI has been falling, crossing below the 50 neutral-perceived level and pointing to a bearish short-term picture.

Upbeat data on initial and continued jobless claims due later in the day could see USDJPY heading higher. Resistance in this case could come around the 50- and 100-period moving averages at 106.31 and 106.55 respectively. An additional barrier in case of an upside break might come around the 107 handle, a potential psychological level with the area around it being congested as well as encapsulating a couple of peaks from the recent past.

A data miss might see the pair posting losses. The area around March 7's ten-day low of 105.45 might offer support, with the sixteen-month low of 105.24 from earlier in the month coming next into view in case of steeper declines.

Risk sentiment – increasingly driven by developments on trade lately – also has the capacity to spur movements in the pair.

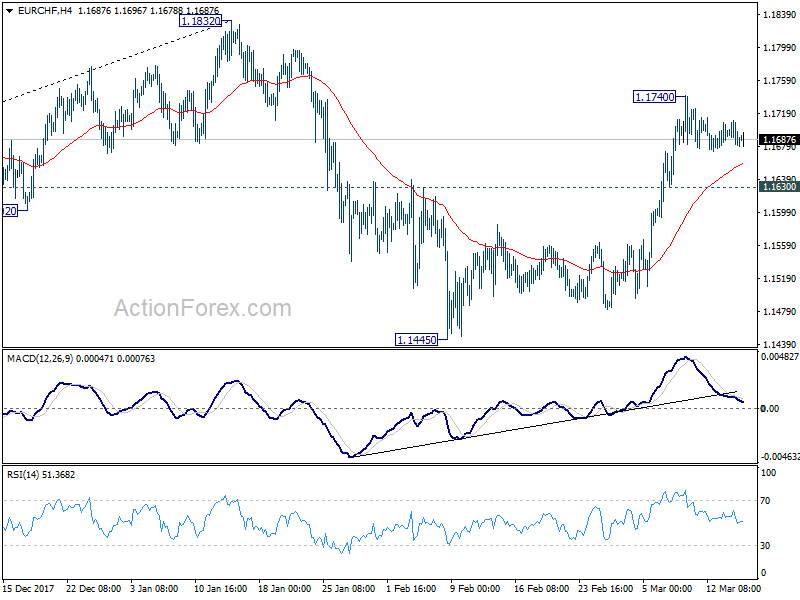

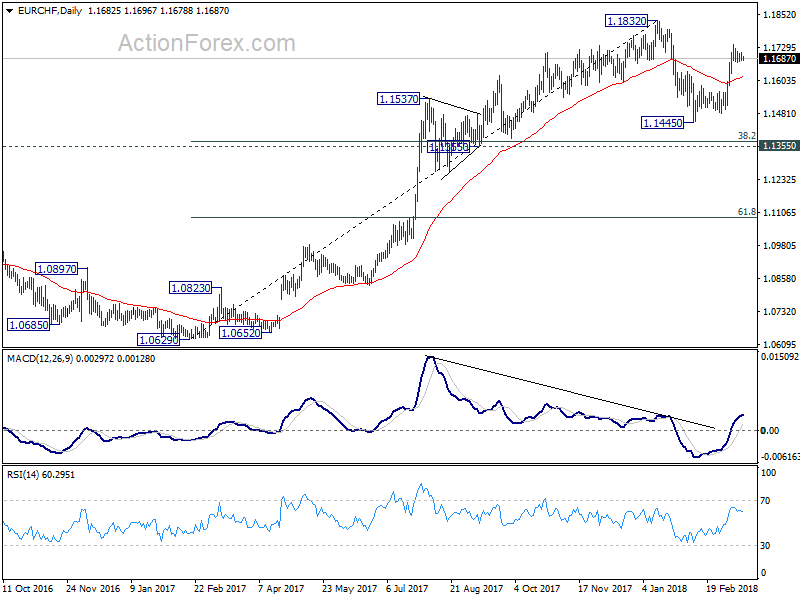

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1674; (P) 1.1692; (R1) 1.1703; More...

EUR/CHF is saying in consolidation from 1.1740 temporary top and intraday bias remains neutral. As long as 1.1630 minor support holds, further rally is expected. On the upside, above 1.1740 will target a test on 1.1832 high. We'll stay cautious strong resistance from there to bring another fall. Corrective pattern from 1.1832 might still have an attempt on 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372) before completion. On the downside, below 1.1630 minor support will target 1.1445 low again.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Swiss National Bank Leaves Expansionary Monetary Policy Unchanged

The Swiss National Bank (SNB) is maintaining its expansionary monetary policy, with the aim of stabilising price developments and supporting economic activity. Interest on sight deposits at the SNB is to remain at –0.75% and the target range for the three-month Libor is unchanged at between –1.25% and –0.25%. The SNB will remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration.

Since the last monetary policy assessment in December, the Swiss franc has appreciated slightly overall on the back of the weaker US dollar. The Swiss franc remains highly valued. The situation in the foreign exchange market is still fragile and monetary conditions may change rapidly. The negative interest rate and the SNB's willingness to intervene in the foreign exchange market as necessary therefore remain essential. This keeps the attractiveness of Swiss franc investments low and eases pressure on the currency.

The SNB's conditional inflation forecast has shifted slightly downwards as a result of the somewhat stronger Swiss franc. The forecast for the current year has decreased marginally to 0.6%, from 0.7% in the previous quarter. For 2019, the SNB now expects inflation of 0.9%, compared to 1.1% last quarter. For 2020, it anticipates an inflation rate of 1.9%. The conditional inflation forecast is based on the assumption that the three-month Libor remains at –0.75% over the entire forecast horizon.

The international economic environment is currently favourable. In the fourth quarter of 2017, the global economy continued to exhibit solid, broad-based growth. International trade remained dynamic. Employment registered a further increase in the advanced economies, which is also bolstering domestic demand.

The SNB expects global economic growth to remain above potential in the coming quarters. Given the robust economic situation, the US Federal Reserve plans to continue its gradual normalisation of monetary policy. In the euro area and Japan, by contrast, monetary policy is likely to remain highly expansionary.

In Switzerland, GDP grew in the fourth quarter at an annualised 2.4%. This growth was again primarily driven by manufacturing, but most other industries also made a positive contribution. In the wake of this development, capacity utilisation in the economy as a whole improved further. The unemployment rate declined again slightly through to February. The SNB continues to expect GDP growth of around 2% for 2018 and a further gradual decrease in unemployment.

Imbalances on the mortgage and real estate markets persist. While growth in mortgage lending remained relatively low in 2017, prices for single-family houses and owner-occupied apartments began to rise more rapidly again. Residential investment property prices also rose, albeit at a somewhat slower pace. Owing to the strong growth in recent years, this segment in particular is subject to the risk of a price correction over the medium term. The SNB will continue to monitor developments on the mortgage and real estate markets closely, and will regularly reassess the need for an adjustment of the countercyclical capital buffer.

Investors On Edge As Fears Of Trade War Mount

Global equity bears marched into Thursday's trading session with a mission to sow chaos across stock markets, as fears mount over a potential global trade war.

Asian stocks were mostly depressed during early trading thanks to risk aversion, and this caution could trickle down into the European markets. With Wall Street pummelled by rising fears of U.S protectionism on Wednesday, U.S stocks are at risk of extending losses this afternoon if the negative sentiment prevails. Risk aversion could become a dominant market theme moving forward, as concerns intensify over escalating trade tensions negatively impacting global growth.

Sterling supported by Dollar weakness…

The story around Sterling's appreciation this week continues to revolve around a weakening U.S Dollar.

With investor appetite for the British Pound limited amid Brexit uncertainty, bulls are finding it increasingly difficult to keep prices buoyed. While Dollar weakness has the ability to support the GBPUSD in the near term, price action suggests some fatigue is already starting to take place, with bears lingering in the vicinity. Taking a look at the technical picture, Sterling's appreciation has been halted on two occasions this week by the stubborn gatekeeper known as 1.4000. Sustained weakness below this resistance level could invite a decline back towards 1.3850. Alternatively, a breakout above 1.4000 could trigger an incline towards 1.4050 and 1.4120, respectively.

Commodity spotlight – WTI Oil

WTI Crude held steady on Thursday morning, after the Energy Information Administration (EIA) reported on Wednesday that gasoline supply dropped thanks to demand jumping to a seven-month high.

While recent reports of rising demand could offer the oil price some support in the short term, soaring production from U.S Shale is likely to present many headwinds down the road. With OPEC warning that Trump’s trade policies could negatively impact oil demand, the outlook for WTI Crude remains tilted to the downside. The unsavoury combination of surging U.S Shale oil production and the threat of demand softening amid a potential trade war could spell trouble for OPEC.

From a technical standpoint, WTI Crude remains under pressure on the daily charts below $62.00. Repeated weakness below the $62.00 resistance level could open a path back towards $60.00.

Bitcoin sinks below $8,000

Bitcoin simply failed to shield itself against an onslaught of negativity during Wednesday’s trading session, with prices eventually sinking below $8,000 on Thursday morning.

In a move that eroded investor appetite towards Bitcoin, Google announced that it will ban online advertisements promoting cryptocurrencies. The downside was fuelled by the International Monetary Fund who called for a global crackdown on cryptocurrencies. With members of Congress delivering the knockout blow on Wednesday amid scepticism around digital currency, the outlook for Bitcoin is looking increasingly gloomy.

Focusing purely on the technical picture, Bitcoin is bearish on the daily charts with $10,000 acting a solid psychological resistance level. Sustained weakness below $8,000 could open a path back towards $7,000 and $6,000, respectively.

Currencies: EUR/USD Locked In Indecisive Trading Pattern

Rates: Risk aversion puts support levels in yield at risk

US politics-related risk aversion fills the eco/event void ahead of next week’s FOMC meeting. Core bonds profit with the German 10-yr yield at key and the US 10-yr yield at intermediate support. A break lower would especially be important in Germany, suggesting a technical move towards 0.46%/0.48%. Dovish signals by the ECB could increase Bund momentum.

Currencies: EUR/USD locked in indecisive trading pattern

The dollar remains in the defensive as trade tensions, in particular between the US and China, weigh on the US currency. The picture for EUR/USD is more balanced as the ECB continues to talk very soft on inflation. New economic advisor to US president Trump, Larry Kudlow backs a US strong dollar policy

The Sunrise Headlines

- Concerns over the prospect of a trade war with China weighed on WS yesterday, with industrials leading the way lower (Dow -1%). Asian stock markets trade mixed with China underperforming.

- Lawrence Kudlow, a conservative economic commentator who backs a stronger dollar and would take a tougher line on trade with China, will be the new director of President Trump’s National Economic Council.

- The Trump administration is pressing China to cut its trade surplus with the United States by $100 bn, a White House spokeswoman said, clarifying a tweet last week from President Donald Trump.

- The leader of Italy's eurosceptic League said a government deal with the anti-system 5-Star Movement was possible after an inconclusive election, raising the prospect of two radical groups running the country.

- Slovak PM Fico offered to resign if his party is allowed to remain in charge of the government, a last ditch effort to avoid early elections in the face of the biggest protests since the fall of communism.

- Slovenian PM Cerar resigned, hours after a key investment project hit a legal obstacle, saying he had also had enough of obstruction from his coalition partners and pressure from trade unions.

- Today’s eco calendar contains US empire manufacturing, weekly jobless claims and Philly Fed business outlook. The Swiss and Norwegian central banks decide on monetary policy. Spain & France tap the bond market

Currencies: EUR/USD Locked In Indecisive Trading Pattern

EUR/USD locked in indecisive trading pattern

The dollar remained in the defensive yesterday after US President Trump fired Rex Tillerson as Secreatry of State. USD/JPY initially hovered in the mid 106 area, but ceded further ground later. US data (PPI, retail sales) were mixed, at best, and the dollar lost interest rate support. The picture for EUR/USD was a bit different. Soft comments from ECB’s Draghi and Praet on inflation capped further euro gains. Later in the session, the new economic advisor of President Trump, Larry Kudlow, advocated a strong dollar but he spoke tough on China. USD/JPY closed the session at 106.32. EUR/USD finished at 1.2368.

Asian equities trade modestly lower overnight. Trade tensions between the US and China remain a source of investor caution. US yields are drifting further south. USD/JPY slipped below the 106 big figure. EUR/USD is changing hands in the 1.2375 area.

There are no important data in Europe today. The US calendar contains the Empire manufacturing survey, import prices, jobless claims and the Philly Fed business outlook. The data probably won’t change markets’ thinking on the Fed’s policy assessment for next week. ST market momentum on interest rates is turning softer, with both US and German yields under downward pressure. LT interest rate differentials might widen in favour of the dollar if the German 10-y yield breaks below the key 0.62% support (see FI part of this report ). Question is whether this will be a big help for the greenback. Trade tensions between the US and China will remain a wildcard for USD trading (and for equity sentiment). We expect the current indecisive EUR/USD trading pattern to persist going into next week’s Fed meeting. An escalation in the US-China trade war would probably be USD negative. Especially USD/JPY is vulnerable. For EUR/USD, a break beyond intermediate resistance at 1.2450 would open the way for a retest of the 1.2550/1.26 area. A break of 1.2155 support looks difficult short-term.

The rebound of cable (partially due to US softness) ran into resistance yesterday ahead of the 1.40 mark. At the same time, the intraday decline of the euro (EUR/USD) weighed slightly on EUR/GBP. The pair drifted back to the 0.8850 area. There are no important UK eco data today. For now, the tensions between the UK and Russia have little impact on sterling. More technically inspired trading for EUR/GBP around current levels might be in the cards.

EUR/USD develops indecisive trading pattern as markets are counting down to next week’s Fed decision