Sample Category Title

AUD/USD Decreasing

AUD/USD's momentum momentarily stops, heading for the 0.7850 range. Hourly support and resistance are given at 0.7704 (24/12/2017 low) and 0.7979 (15/01/2018 high). Further resistance is given at 0.8134 (26/01/2018 high). The technical structure suggests short-term upward decrease.

In the long-term, the upward trend slows down after failing to reach key resistance at 0.8164 (14/05/2015 low). Key support stands at 0.6009 (31/10/2008 low). A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Pausing Before Another Leg Higher

USD/CAD has bounced off 1.2805 low, currently trading along the 1.2950 range and heading for hourly resistance at 1.2998 (05/03/2018). Hourly support remains at 1.2805 (12/03/2018 low). The short-term technical structure suggests further short-term sideway moves.

In the longer term, the pair is trading between resistance point at 1.3805 (05/05/2017 high) and support at 1.2128 (18/06/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head lower. The pairs is trading above its 200 DMA.

USD/CHF Trading Sideways

USD/CHF is trading sideway following recent hike at 0.9480. The pair currently trades between hourly support and resistance at 0.9296 (05/02/2018 low) and 0.9668 (17/01/2018 high). Expected to show short-term decrease.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support lies at 0.9072 (07/05/2015 low) while resistance at 1.0344 (15/12/2016 high) is distanced. The technical structure favours a long term bullish bias since the unpeg in January 2015

USD/JPY Bouncing Off

USD/JPY is rising back following recent decline at 105.79, heading higher along the 106.30 range. Hourly support and resistance are given at 105.29 (02/03/2018 low) and 107.90 (14/02/2018 high). The bearish pattern started in January 2018 is maintained. The short-term technical structure suggests short-term rising moves.

We favor a long-term bearish bias. Support remains at 101.20 (09/11/2016 low). A gradual rise toward the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 101.20 (09/11/2016 low). The pair trades largely below its 200 DMA.

GBP/USD Slight Increase

GBP/USD momentum continues, approaching 1.40. The pair is currently contained between hourly support and resistance at 1.3765 (09/02/2018 low) and 1.4151 (05/02/2018 high). The technical structure suggests short-term increase.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Stabilizing

EUR/USD is trading sideway along the 1.2370 range. Hourly support and resistance are given at 1.2112 (12/01/2018 low) and 1.2537 (31/01/2018 high). The technical structure suggests further short-term sideway moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

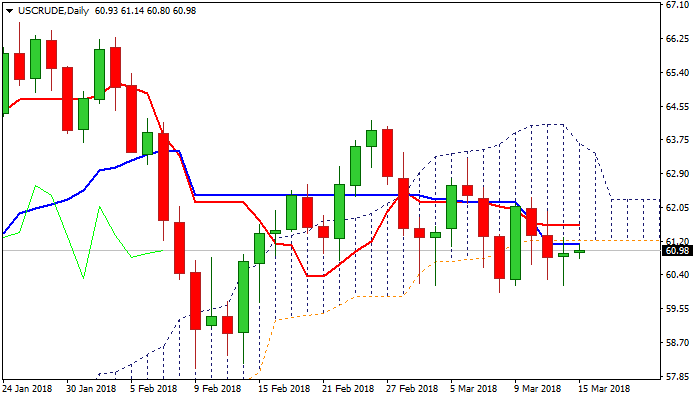

Technical Outlook: WTI Oil – Strong $60 Support Zone Holds For Now But Daily Cloud Top Caps And Maintains...

WTI oil moved higher and holds in $61 zone on Thursday after dipping to $60.11 low on downbeat US crude stocks data on Wednesday. EIA report showed much stronger than expected build in crude inventories last week (5.02 million barrels vs forecasted build of 2.02 million barrels) which raised concerns about global oil demand. Increasing US oil production also keeps oil price pressured. Strong $60 support zone (psychological support, reinforced by rising 100SMA) so far contained repeated attacks, but remains under pressure and risks eventual break lower. Thick daily cloud continues to weigh, as cloud base ($61.23) caps near-term action, maintaining bearish bias. Weakening momentum studies support the notion, with renewed attacks at $60 zone to be expected while the price remains below cloud base. Eventual break through the base forming at $60 zone would signal continuation of bear-leg from $64.22 (26 Feb high). Penetration of daily cloud would sideline immediate downside risk, but plethora of daily MA barriers above, would signal limited upside.

Res: 61.23, 61.42, 61.84, 62.53

Sup: 60.80, 60.49, 60.11, 59.94

Thursday March 15: Five Things The Markets Are Talking About

Euro stocks are better bid despite an uncertain Asian session as the market assesses the implications of the latest personnel changes at the White House.

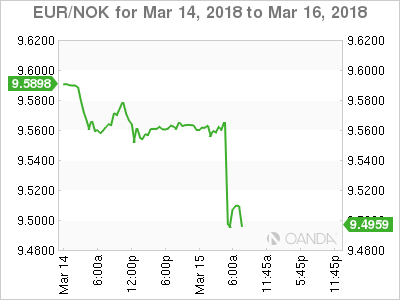

In currencies, the NOK (€9.4980) rallies +0.7% outright to a four-month high after Norges Bank’s interest rate decision, at which officials said there are chances of a “somewhat earlier” rate increase than seen in the previous report.

U.S Treasury yields continue to hover atop of last months low yields on market bets that the Fed will not signal quicker rate hikes when policy makers meet next week (March 20-21).

Elsewhere, crude oil is holding its gains as signs of stronger U.S fuel consumption is been balanced by OPEC’s forecasting. Bitcoin (BTC – $8,196) has touched its lowest level in four weeks.

On tap: E.U – 27 government officials discuss the E.U’s Brexit position.

1. Stocks mixed bag

In Japan, the Nikkei share average eked out small gains overnight with the Bank of Japan (BoJ) buying up ETF’s, offsetting weakness in machinery makers. The Nikkei ended +0.1% higher, while the broader Topix was little changed.

Down-under, a -1% drop for Aussie banks helped keep the country’s stock benchmark in the red for a third session. The S&P/ASX 200 fell -0.2% even as the materials sector rose +0.6%. In S. Korea, the Kospi closed out advancing +0.25%.

In Hong Kong, stocks rallied on Thursday, led by property and IT shares, as investors shrugged off concerns that growing trade tensions will hurt the global economy. The Hang Seng index rose +0.3%, while the China Enterprises Index gained +0.2%.

In China, stocks traded relatively flat, with any gains offset by investors dumping new listings. At the close, the Shanghai Composite index was unchanged, while the blue-chip CSI300 index gained +0.6%.

In Europe, regional indices trade mostly higher across the board with notable strength in the DAX, which leads the gainers after declines yesterday.

U.S stocks are set to open in the ‘black’ (+0.2%)

Indices: Stoxx600 +0.3% at 376.2, FTSE +0.4% at 7158, DAX +0.6% at 12313, CAC-40 +0.5% at 5261, IBEX-35 -0.1% at 9682, FTSE MIB +0.6% at 22576, SMI -0.2% at 8853, S&P 500 Futures +0.2%

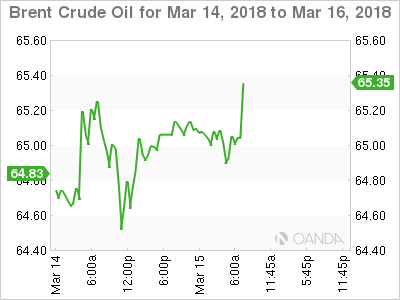

2. Oil prices stable on healthy demand, but oversupply worries loom

Oil prices are little changed, supported by healthy global demand, but at the same time, held back by a relentless rise in U.S production that is undermining OPEC’s efforts.

Brent crude futures are at +$64.91 per barrel, near yesterday’s close, while U.S West Texas Intermediate (WTI) crude futures CLc1 are up by +9c to +$61.05 a barrel.

Prices continue to receive support from healthy demand. OPEC said yesterday that oil consumption was expected to grow by +1.62m bps in 2018.

But looming over markets has been a relentless climb in U.S crude output. EIA data this week hit another record last week by rising to +10.38m bpd, up by more than +23% since mid-2016. Commercial crude inventories were up by +5m barrels, at +430.93m barrels.

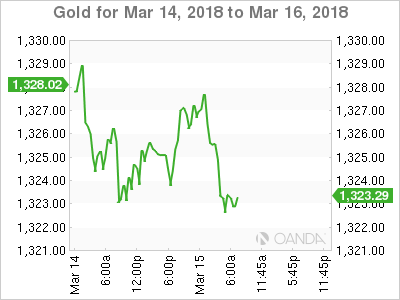

Ahead of the U.S open, gold prices are steady atop of their one-week high print in yesterday’s session amid political tensions between Britain and Russia, and renewed worries about a global trade war. Spot gold is nearly flat at +$1,325.06 per ounce.

3. Sovereign yields little changed

Earlier this morning, Norway’s central bank (Norges) left its key policy rate unchanged, but said that rates are likely to rise “after summer 2018,” slightly earlier than previously indicated. The vote was unanimously in favour of leaving the sight deposit rate at a record low of +0.5%, where it has been since March 2016. But the board indicated it is ready to follow the Fed and the BoE and raise rates this year.

“The outlook for the Norwegian economy suggests that it will soon be appropriate to raise the key policy rate,” it said.

Note: If the Norges Bank were to raise its key rate this summer, it would likely do so ahead of the ECB, since the market does not expect the ECB to lift its key policy rate before 2019.

Also this morning, the Swiss National Bank (SNB) kept its key policy rate at -0.75% despite recent signs of a pickup in the Swiss economy, as officials continued to warn about fragile conditions in currency markets and the “highly valued” Swiss franc.

In its policy statement, the SNB said it expects Swiss GDP to expand around +2% this year amid a broader pickup in the global economy. Unemployment should decline gradually, it said. The SNB’s deposit rate has been at its current level since January 2015.

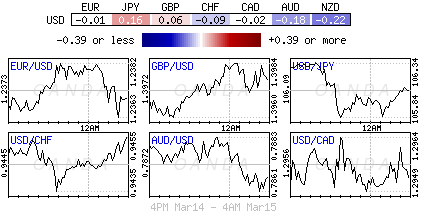

4. Dollar little changed

The USD is again little changed against the major European pairs.

Earlier this morning, the SNB kept its rhetoric unchanged with the CHF currency ($0.9451) seen as ‘highly valued’ thus showing it was in no hurry to change rates any time soon.

The EUR/SEK (€10.0905) has crossed its two-week lows and is firmer after Swedish February unemployment data beat expectations.

The NOK currency has appreciated after the Norwegian Central bank (Norges) tweaked its view on the first potential rate hike to after summer from its prior view of in the autumn. EUR/NOK hit a 4-month low of under €9.50 in the aftermath of the commentary as Norges new rate path suggested 100% chance of a September rate hike.

The yen has strengthened by as much as 6% against the dollar since the start of the year due to a combination of persistent dollar weakness, the BoJ monetary policy outlook and safe-haven demand as a result of political risks. These factors have pulled the ‘big’ dollar down from levels around ¥113 in early January to a 16-month low of ¥105.25 early this month.

5. French CPI was stable on the month and up on the year

Data this morning showed that French consumer prices (CPI) for February was unchanged, following a -0.1% downturn in January.

Digging deeper, food prices barely edged down (-0.1%), in the wake of fresh product prices. Those of “manufactured product” decreased again, but less markedly than in January (-0.3% after -2.2%). Services prices slowed down for the second consecutive month (+0.1% after +0.2%). Lastly, energy prices were stable, the decrease in petroleum product prices being offset by a rise in gas and electricity prices.

Seasonally adjusted, consumer prices dropped by -0.3%, after an acceleration to +0.7% in January.

Year-on-year, the CPI fell on the month to +1.2% from +1.3%. This slight decrease resulted from a lesser rise in prices of services, food and tobacco.

DAX Edges Higher, Investors Await Eurozone CPI

The DAX index has posted considerable gains in the Wednesday session. Currently, the DAX is trading at 12,259, up 0.18% on the day. On the release front, there are no eurozone or German events on the schedule. On Friday, the focus will be on inflation indicators, with the release of the German Wholesale Price Index and the Eurozone Final CPI.

On Wednesday, ECB President Mario Draghi expressed cautious optimism that inflation levels are moving higher, but added that the bank still needed to see further evidence that this was indeed the case. Therefore, Draghi said that monetary policy would “remain patient, persistent and prudent”. With the eurozone economy showing its best numbers in a decade, there has been growing speculation that the ECB will wind up its stimulus program in September. However, inflation remains well below the ECB target of around 2 percent, so Draghi can afford to remain cautious and maintain current monetary policy.

German Chancellor Angela Merkel was elected to a fourth term on Wednesday, as Germany finally has a government in place, after an inconclusive election in September. However, Merkel will have her work cut out for her in what could be her last stint as leader of the eurozone’s largest economy. Merkel’s stature has diminished after a poor election, and she will preside over a fractured coalition. The vote in the German parliament was 364 to 315. Merkel was forced to give the SDP the finance and foreign ministry portfolios, so we can expect the new government to be more supportive of eurozone integration, including assistance for weaker eurozone members.

Euro Unchanged, Investors Eye Jobless Claims

EUR/USD has inched lower in the Thursday session. Currently, the pair is trading at 1.2363, down 0.03% on the day. On the release front, there are no eurozone or German indicators. French Final CPI edged up to 0.0%, beating the estimate of 0.1%. In the US, unemployment claims is expected to drop to 227 thousand, and the Philly Fed Manufacturing Index is forecast to fall to 23.1 points. On Friday, Germany releases the Wholesale Price Index and the eurozone will publish Final CPI. The US will release Building Permits, Housing Starts and Preliminary UoM Consumer Sentiment.

The eurozone economy continues to improve, but manufacturing indicators for January pointed downwards in Germany and the eurozone. Eurozone Industrial Change declined 1.0% in January, its sharpest drop since December 2016. The estimate stood at -0.4%. Last week, German numbers disappointed. Factory Orders in January plunged 3.9%, worse than the estimate of -1.9%. This marked the second decline in the past three months. This was followed by a decline of 0.1% from Industrial Production, marking a second straight decline. The reading was well off the forecast of 0.6%. The latest numbers are somewhat surprising as the German economy remains very strong, and has led the way as eurozone economy continues to expand.

German Chancellor Angela Merkel was elected to a fourth term on Wednesday, as Germany finally has a government in place, after an inconclusive election in September. However, Merkel will have her work cut out for her in what could be her last stint as leader of the eurozone’s largest economy. Merkel’s stature has diminished after a poor election, and she will preside over a fractured coalition. The vote in the German parliament was 364 to 315. Merkel was forced to give the SDP the finance and foreign ministry portfolios, so we can expect the new government to be more supportive of eurozone integration, including assistance for weaker eurozone members.