Sample Category Title

DOW extending triangle pattern; EURJPY, EURGBP, USDCAD on the move

Dow trading up over 1% at the time of writing, back above 25000 handle. It looks like price actions from 25800 are forming a triangle pattern. More upside would be in favor as long as 24217.76 support holds, for retesting 26616.71 record high.  Yen remains the strongest one today even though it's paring some gains in the current 4 hour period. It's followed by the resilient Sterling. Commodity currencies are generally weak.

Yen remains the strongest one today even though it's paring some gains in the current 4 hour period. It's followed by the resilient Sterling. Commodity currencies are generally weak.

A few technical development to note:-

A few technical development to note:-

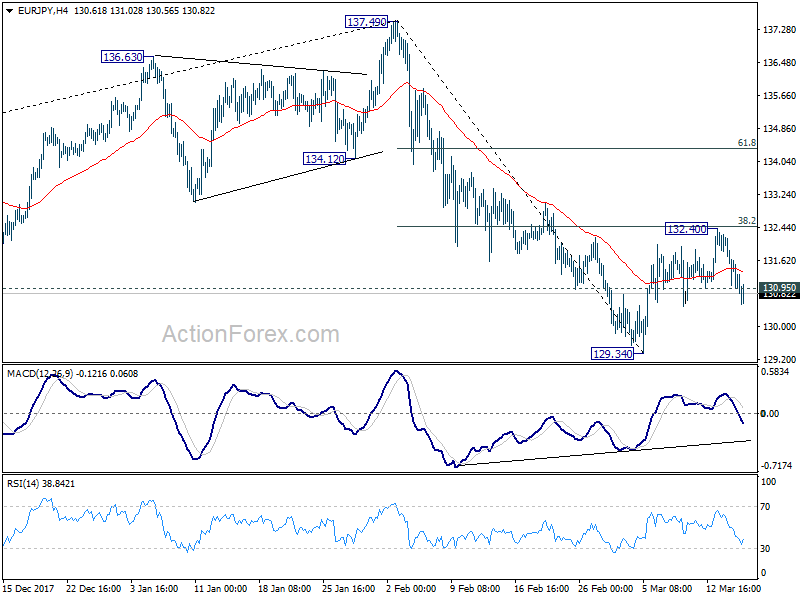

EUR/JPY's rebound from 129.34 could have completed at 132.40, heading back to 129.34.

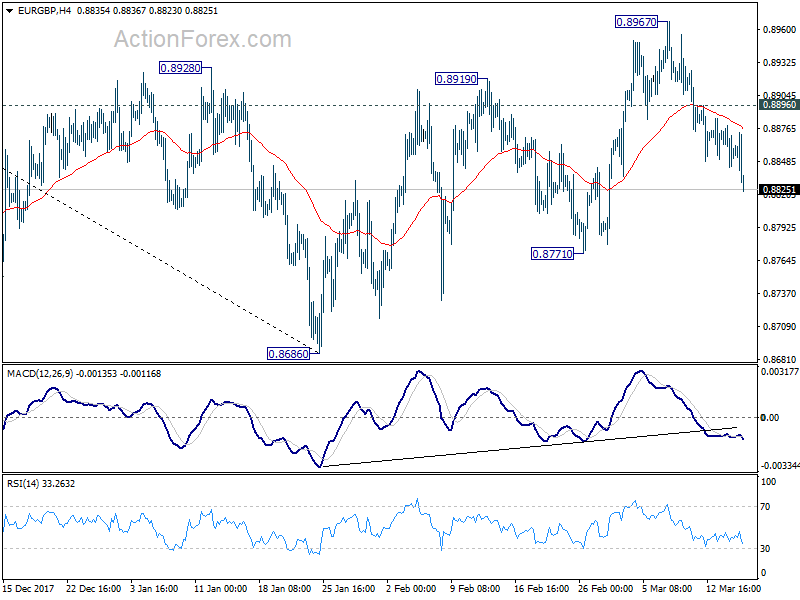

EUR/GBP extending the fall from 0.8976 to 0.8771 support.

EUR/GBP extending the fall from 0.8976 to 0.8771 support.

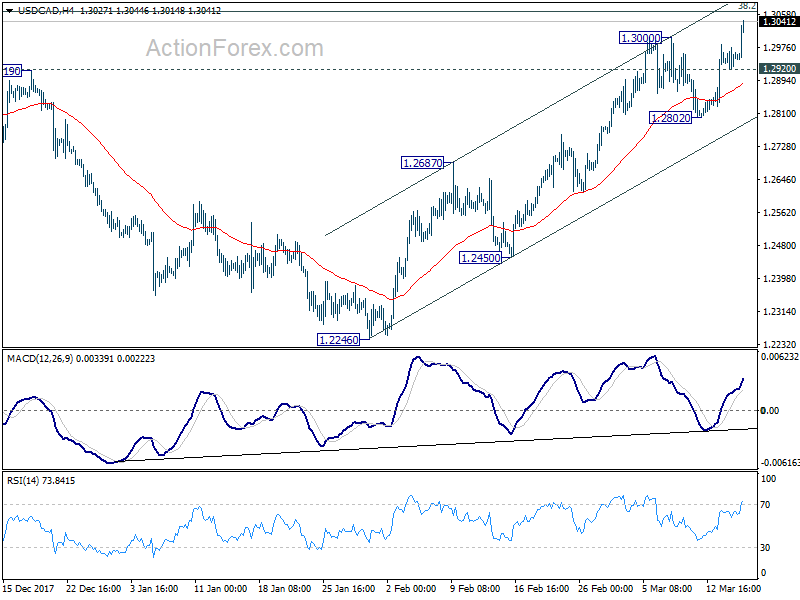

USD/CAD broken 1.3000 for rally resumption to 1.3065 fibonacci level.

USD/CAD broken 1.3000 for rally resumption to 1.3065 fibonacci level.

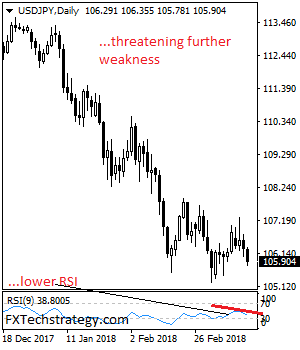

USDJPY: Weakens, Threatens Price Extension

USDJPY: The pair looks to weaken further as more decline is expected in the days ahead. On the downside, support lies at the 105.50 level where a break if seen will aim at the 105.00 level. A cut through here will turn focus to the 104.50 level and possibly lower towards the 104.00 level. On the upside, resistance resides at the 106.50 level. Further out, we envisage a possible move towards the 107.00 level. Further out, resistance resides at the 107.50 level with a turn above here aiming at the 108.00 level. On the whole, USDJPY faces further downside pressure.

Sunset Market Commentary

Markets:

Core bonds stay well bid as uncertainty on global trade kept investor interest for safe haven assets alive. Bunds again outperform Treasuries. Recent soft ECB comments cause EMU bond bears to reduce exposure. The German 10-y yield broke below the 0.62% floor, adding to positive sentiment. There were few important eco data in Europe. US data including the Empire Manufacturing survey, jobless claims, import prices and the Philly Fed business outlook were ok/mostly slightly above consensus (except for the Philly Fed). However, they didn’t change markets’ assessment ahead of next week’s Fed policy decision. At the time of writing, the US 2-y yield rises 1.2bps. Yields for other maturities decline less than 1bp. The German yield curve bull flattens with the 2-yr German yield declining 0.5 bps and the 30-yr easing 2.7 bps. Intra-EMU spread vs Germany are little changed expect for Greece (+9bps).

Over the previous days, some modest USD softness prevailed as investors pondered next developments in the US trade/tariffs saga. The dollar still isn’t in great shape, but today euro softness was the more dominant factor among the major FX cross rates. EUR/USD gradually drifted further south in the 1.23 big figure. Of late, interest rate differentials were often ignored as a driver for EUR/USD trading. However, some tentative policy divergence between the ECB en the Fed is again coming to the forefront. The ECB recently indicated that there is still a long way to go to reach its inflation target. In this context, an ECB rate hike might still be further away than the market recently discounted. The 2-yr US German interest rate differential widened to a new cycle peak (285 bps). Finally, it looks that this is providing some downside protection for the dollar against the single currency. EUR/USD trades in the 1.2330 area. From a technical point of view, the established ranges remain perfectly intact. The picture of the dollar against the yen looks far less buoyant. The pair still struggles not to fall below the 106 barrier. The 105.25 correction low is again coming with reach.

Technical considerations continued to dominate sterling trading. The Cable 1.40 area still proved a tough resistance. The political tensions between the UK and Russia for now have only modest impact on markets. Even so, they are no help for sterling. Sterling was under pressure early in the session but found a better bid later. The intraday slide of EUR/USD also reinforced the EUR/GBP decline back to recent lows. EUR/GBP tries to sustain below 0.8850. This move is at least as much due to euro softness rather than sterling strength. Cable hovers near 1.3975.

News Headlines:

Norway’s central bank signalled it will move faster in raising interest rates as a change in the inflation target and accelerating growth opens up for the first tightening in seven years. Governor Olsen said that a first rate hike can be expected after this Summer. EUR/NOK dropped (temporary?) below 9.5, breaking technical support.

The Swiss National Bank kept its monetary policy unchanged (deposit rate -0.75%). The SNB remains willing to intervene in the FX market if necessary. Swiss growth is finally accelerating and inflation is expected to hit the 2%-target by the end of the policy horizon (2020).

Euro zone banks may get a reprieve until 2021 to fully implement ECB guidelines on treating new soured loans, an ECB document showed, a retreat from an earlier proposal for a more aggressive treatment of bad debt.

Most US eco data beat expectations. The Empire Manufacturing rose in March from 13.1 to 22.5 (vs 15 expected). Weekly jobless claims continued to hover near historically low levels (226k). Import prices rose more than forecast in February (0.4% M/M) while the opposite was true for export prices (0.2% M/M). The Philly Fed business outlook faced a somewhat larger than forecast setback, declining from 25.8 to 22.3.

Mexican Guajardo : NAFTA will continue, just maybe without US

Mexican Economy Minister Ildefonso Guajardo warned today: -

- "You have to be ready to live with a NAFTA without the U.S."

- "NAFTA at risk of ending? No. NAFTA will continue between Canada and Mexico because at the end of the day, what is important is you send a message that you believe in free trade. The U.S. is the one that will decide to be in or out."

Canadian Prime Minister Justin Trudeau said yesterday:-

- An "eminently achievable win-win-win" result available on NAFTA

British Pound Slightly Higher as US Posts Mixed Data

The British pound has ticked upwards in the Thursday session. In North American trade, GBP/USD is trading at 1.3977 up 0.15% on the day. On the release front, there are no key British releases on the schedule. In the US, unemployment claims dropped to 226 thousand, just below the estimate of 226 thousand. Manufacturing reports were mixed. The Philly Fed Manufacturing Index dropped to 22.3, missing the forecast of 23.1 points. There was better news from the Empire State Manufacturing Index, which jumped to 22.5, crushing the estimate of 14.9 points. On Friday, the US releases three key construction reports and Preliminary UoM Consumer Sentiment.

It’s an unusually quiet week for British releases, with no key economic indicators. The highlight of the week was the annual budget, which was released on Tuesday. Finance Minister Philip Hammond was likely relieved to deliver the budget in parliament and move on, as the economic forecasts were not particularly upbeat. According to the Office of Budget Responsibility, the country’s economic growth is expected to be weak – 1.5 percent in 2018, and just 1.3 percent in 2019 and 2020. The OECD underscored the bleak picture, when it said on Tuesday that Britain’s economy would grow more slowly than all the Group of 20 members in 2018. The economy has slowed since the Brexit vote in June 2016, taking the British pound down as well. With London and Brussels at odds over the relationship between the sides after Brexit takes effect in March 2019, the pound could face strong headwinds during the year.

The Federal Reserve is widely expected to raise interest rates next week. According to the CME Group, the odds of a quarter-point raise stand at 89 percent. What can we expect from the Fed during the year? The pressing question is how many rate hikes lie ahead in 2018. The current Fed projection remains at three hikes, but the superb nonfarm payrolls report last week has raised speculation that the Fed could accelerate the pace to four hikes, which would be good news for the US dollar. Investors will be keeping a close eye on key US data, especially inflation indicators. If these numbers improve, we’re likely to see four rate hikes in 2018.

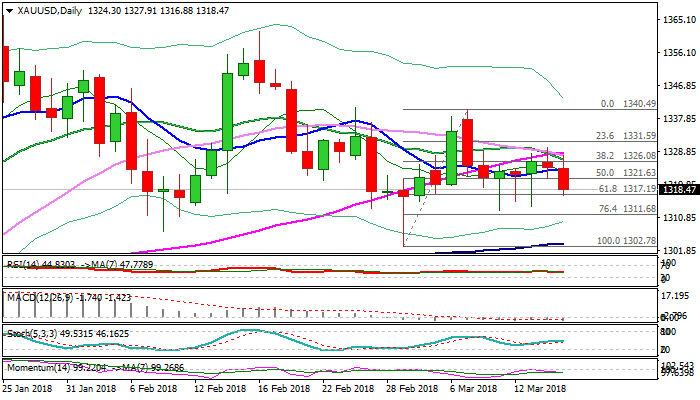

GOLD Price Moves Lower as Dollar Firms, But Still Within 4-Day Range

Spot Gold moved lower and holds in red on Thursday, turning focus towards key near-term supports at $1313 zone (base of four-day congestion).

Stronger dollar on better than expected US jobless claims and import data, pushed yellow metal’s price into lower side of four-day $1313/$1330 range.

Fresh easing weakened structure of daily techs as MA’s turned into bearish configuration and formed multiple bear-crosses (20/55 and 30/55), 14-d momentum moved to negative territory, while RSI turned south moved lower from neutrality zone, generating negative signal.

However, fresh bears need eventual close below cracked Fibo support at $1317 (Fibo 61.8% of $1302/$1340 upleg) and firm break below n/t congestion floor at $1313, to confirm an end of directionless phase and turn focus towards key supports at $1302 zone (01 Mar spike low/100SMA/daily cloud base).

Caution on repeated failure at $1313 which could signal further extension of recent range-trading, as concerns about trade war keep greenback vulnerable.

FOMC policy meeting next week is in focus as key event which could generate fresh direction signal.

The Fed is expected to hike rates three times this year, with likely scenario of first hike occurring in March’s meeting, but traders will be looking for fresh signals about the pace of Fed’s action this year, as recent positive releases from the US signal the central bank could be more aggressive.

More hawkish tone for Fed would likely send gold price further down.

Res: 1321; 1328; 1330; 1338

Sup: 1313; 1311; 1307; 1302

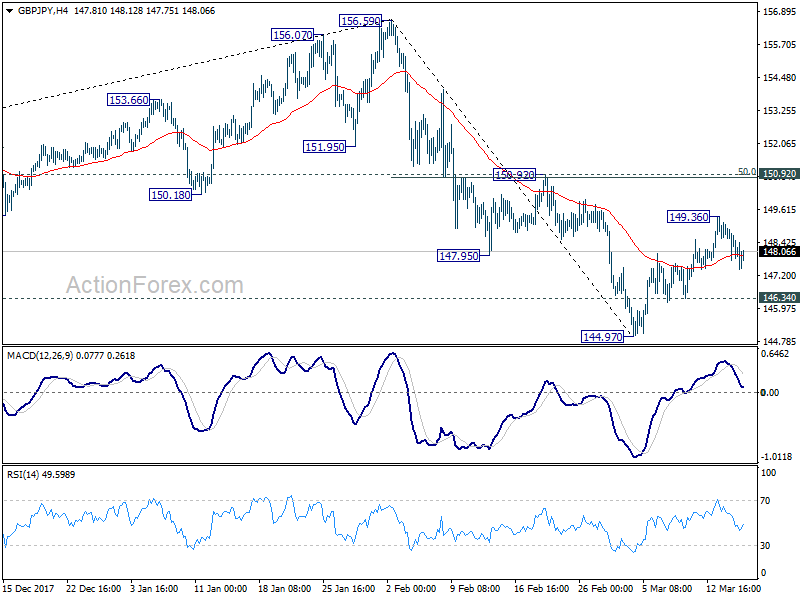

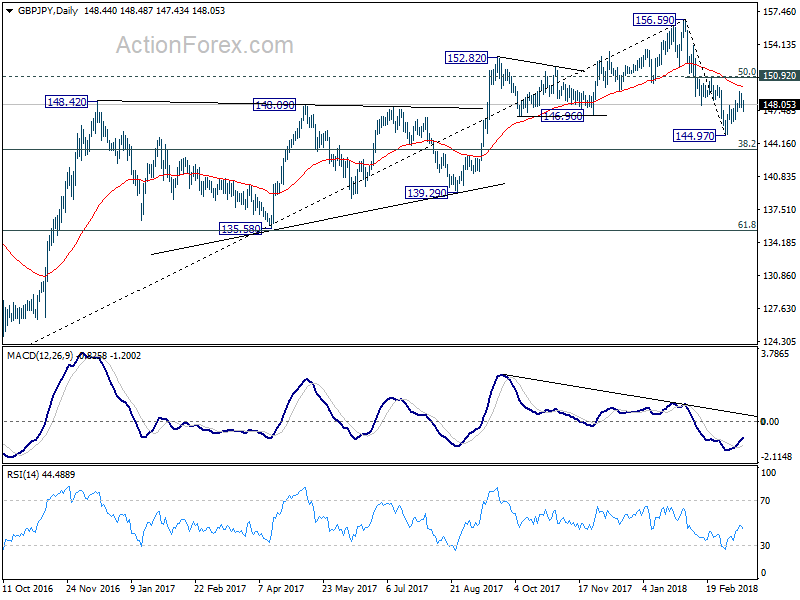

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.74; (P) 148.44; (R1) 149.15; More....

While GBP/JPY's corrective rise from 144.97 might extend, upside should be limited by 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption eventually. Below 146.34 minor support will suggest that the recovery has completed. Intraday bias will then be turned back to the downside for 144.97 first. Break will extend the decline from 156.59 to 143.51 medium term fibonacci level next.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

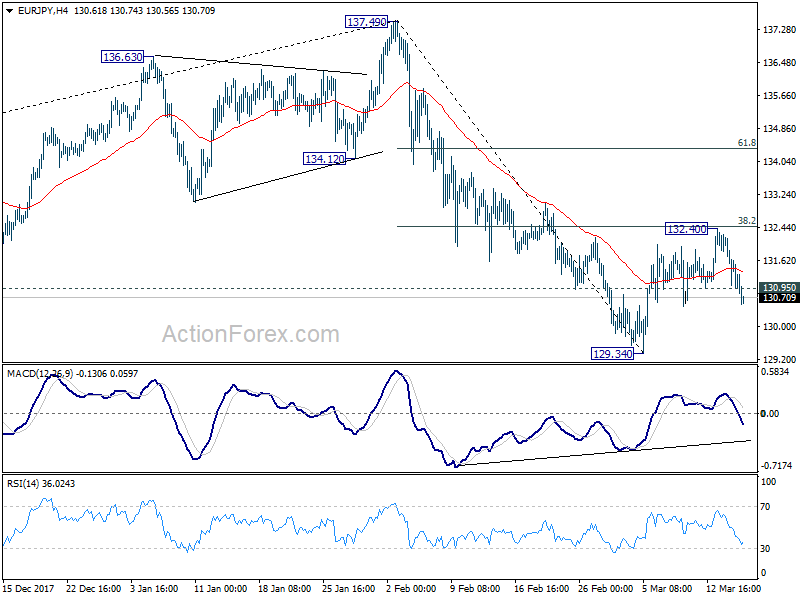

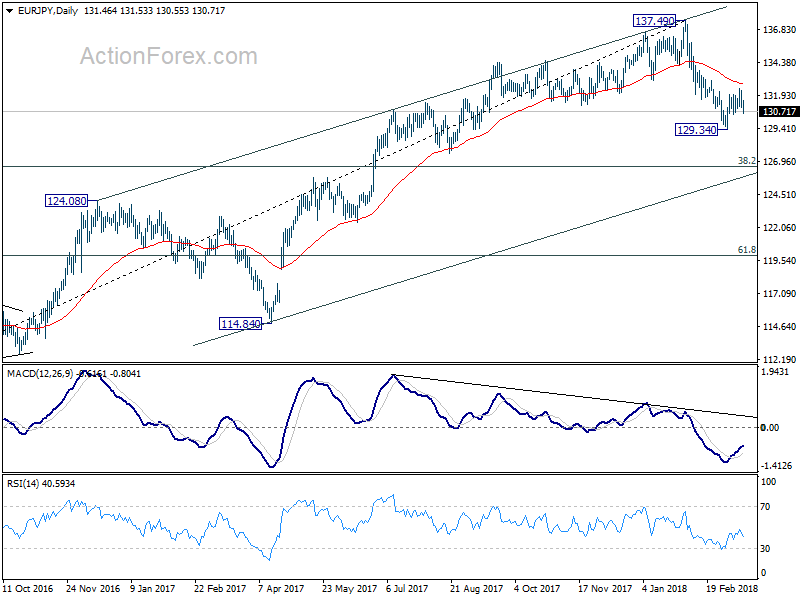

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 130.91; (P) 131.60; (R1) 132.17; More....

EUR/JPY's break of 130.95 minor support suggests that corrective recovery from 129.34 has completed at 132.40 already. That's slightly ahead of 38.2% retracement of 137.49 to 129.34 at 132.45. Intraday bias is back on the downside for retesting 129.34 low first. Break will resume whole fall from 137.49 and target 126.61 medium term fibonacci level. In case of another rise, we'd continue to expect strong resistance from 132.45 to limit upside.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

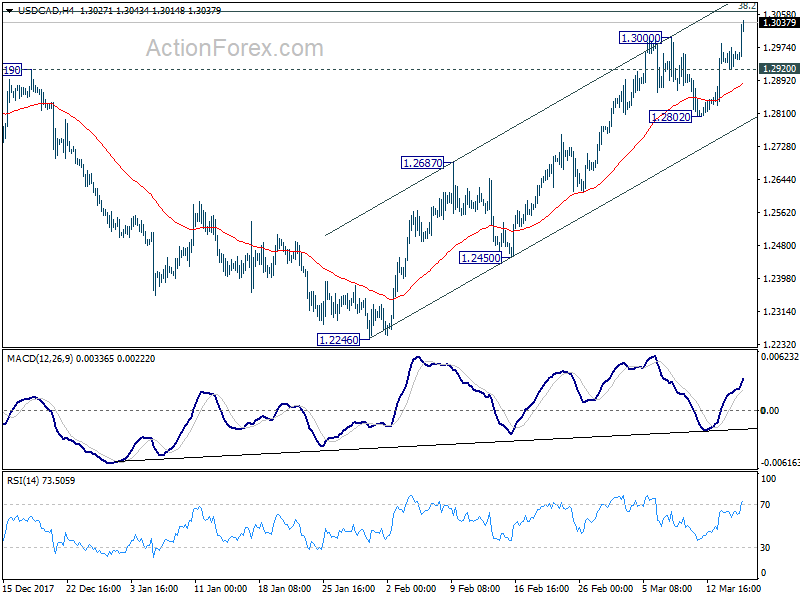

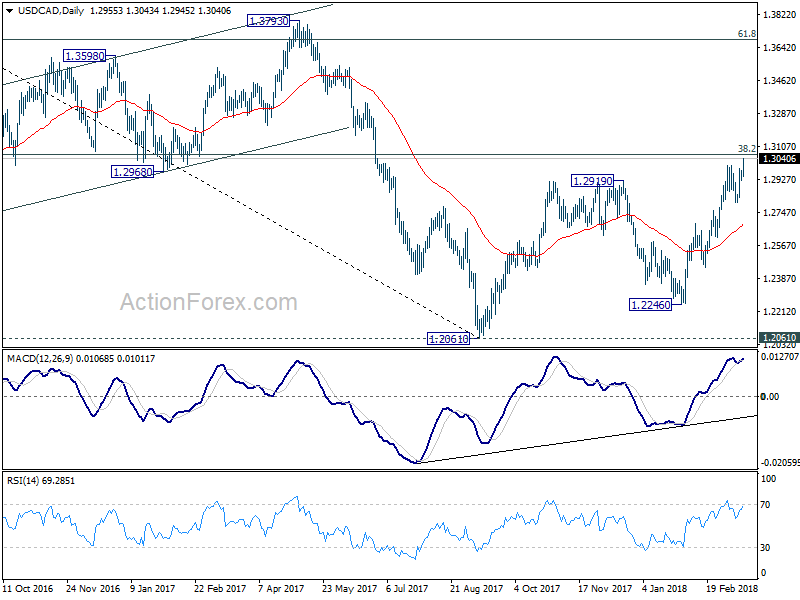

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2924; (P) 1.2950; (R1) 1.2979; More....

USD/CAD rises to as high as 1.3034 so far. Break of 1.3000 confirms rally resumption. Intraday bias is back on the upside for 1.3065 medium term fibonacci level. Sustained break there will pave the way to next fibonacci level at 1.3685. On the downside, below 1.2920 minor support will turn bias neutral first. But near term outlook will stay bullish as long as 1.2802 support holds.

In the bigger picture, we're favoring the medium term bullish case. That is larger down trend from 1.4689 has completed at 1.2061, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen back to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 first. Break will target 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2687 support holds.

Canadian Households’ High Debt Levels Will Shape the 2018 Outlook

Highlights:

- Aggregate household balance sheets improved in Q4/17 with net worth rising 2.1%.

- Household assets rose by 1.9% quarter-over-quarter thanks to strong equity market performance. Nonfinancial assets continued to rise at a more moderate pace as home prices came off the boil.

- Credit market debt rose 1.1% as both mortgage and non-mortgage debt increased at a similar pace.

- Credit market debt-to-assets and debt-to-net worth ratios retraced the previous quarter’s increases, edging down to 16.3% and 19.6%, respectively. Both are just slightly above longer run averages.

- The household debt-to-disposable income ratio was little changed at 170.4%. The previous quarter’s reading was revised down to 170.5% though that was still a record high.

- A previous release showed the household debt service ratio was little changed at 13.8% though the interest portion of payments rose by 0.1 percentage point of disposable income.

Our Take:

In broad strokes, 2017 painted a familiar picture of household finances: rising asset values, more borrowing and fairly steady debt payments relative to consumers’ incomes. 2018 should be more interesting. For one, it looks like debt growth is turning a corner. As the Bank of Canada pointed out last week, household credit growth has slowed in recent months. With interest rates expected to rise further and housing regulations tightening at the federal and provincial level, the peak in debt growth could very well be behind us. That should be viewed as a positive development by the BoC, though progress on reducing the ‘key vulnerability’ of elevated household debt will likely be very slow.

While more moderate debt growth is a welcome development, policymakers will want to be sure they aren’t hitting the brakes too hard. We got the slightest taste of what rising interest rates mean for household debt service costs in Q4/17 and think a trend of gradually rising interest payments will become entrenched this year. Households shelling out a bit more to cover debt costs—and less attractive interest rates for big ticket purchases—will be a headwind for consumer spending this year. How highly indebted consumers react to rising borrowing costs remains a key uncertainty facing the BoC and one that will likely keep them cautious in raising rates.