Sample Category Title

FOMC Preview Sticking To Three Rate Hikes Signal For 2018

- We expect the Fed to raise the target range by 25bp to 1.50-1.75%.

- We expect the Fed to maintain the hiking signal at 3 hikes this year but lift the median dot for next year from 2.25 to (close to) 3 hikes. We also expect the Fed to raise rates three times both this year and next year.

- The hike is unlikely to steer a new direction for USD. We think Trump policies are more important for USD at present. Near term, EUR/USD is set to stay in the 1.21- 1.26 range.

- 5y point on the US curve could see upward pressure. We expect the US curve to continue to flatten both 2y10 and 5y10y after the FOMC meeting.

Fed to maintain three hikes signal for 2018

In line with market pricing and consensus, we expect the Fed to raise its target range by 25bp to 1.50-1.75% at next week's meeting. We expect the Fed to maintain the three hikes signal for this year but showing more confidence in the signal, as more of the dovish members now seem to support this. If we are right, this would likely be interpreted dovishly, as markets are speculating whether the Fed is about to hike four times this year. Markets have already priced in three hikes this year, which is quite a lot at this point. We think the recent average hourly earnings and CPI data support this. However, we note that some of the most outspoken doves do not vote this year (Bullard, Evans, Kashkari) meaning that the median dot among the voting FOMC members is likely higher than the median dot among all members. In this sense, we agree with markets that the balance of risk is skewed towards a fourth hike although three remains our base case. New Fed Chair Jerome Powell also sounded slightly more hawkish at his hearing before Congress (at least on day 1, as he downplayed it on day 2), as he said his ‘personal outlook has strengthened', see Flash Comment US: Powell says ‘personal outlook has strengthened;, 27 February. We do not expect big changes to the statement. The Fed will likely repeat that risks are ‘roughly balanced', that it still monitors inflation ‘closely' and that it expects ‘further gradual increases'.

We think the Fed will signal it is time actually to hit the brakes by raising the Fed funds rate above the longer-run dot of 2.75% (the Fed's view on the nominal level of the natural rate of interest when the economy has normalised) in coming years, as we expect the Fed to raise the dot signal for 2019 from slightly more than 2 hikes to (close to) 3 hikes. This implies a Fed funds rate at 3.0% by the end of 2019. Markets have only priced in slightly more than four hikes from now until year-end 2019, against our expectation of six hikes.

Although we expect the Fed to signal that more hikes are needed than projected in December on the back of a more expansionary fiscal policy, we do not think the Fed will offset it one-to-one, implying the total policy mix is becoming more expansionary. That is also why we argue that there are upside risks to our US inflation forecast, especially next year.

Powell to stick to current policy strategy near term

It is Jerome Powell’s first meeting as a Fed chair so his interaction with the press during the Q&A is also going to be interesting to follow. Based on his hearing before US Congress, it seems that he has a more direct approach than Yellen. One important thing, which Powell confirmed during his Q&A, is that he relies more on policy rule guidance going into Fed meetings (looking at a range of rules, not just one). In the Fed’s Monetary Policy Report - February 2018 (released Friday 23 February) the Fed describes a few rules - see our tweet, 27 February.

Powell is sticking to the Fed’s existing tightening strategy by continuing the gradual hiking cycle (and shrinking the balance sheet). What will be more interesting will be how Powell reacts should the economy or financial markets be hit by a shock in either direction. Powell is less qualified than Yellen (in terms of academic credentials) and the Fed will be less experienced (many new members). We wrote more about this topic here FX Edge – inexperienced Fed to be a drag on USD, 30 November).

We expect the US yield curve to flatten further

The confirmation from the Fed that they still ‘only’ plan to hike three times this year should make the market scale back slightly the 75bp priced for 2018, as only two hikes in 2018 again is a viable option. However, the lift in the 2019 ‘dots’ works in the other direction. It will be a strong signal from the FOMC. It will be a surprise to the market that a majority of the members are actually now ready to lift the Fed Funds above the 2.75% longer-run dot. The latter points to a repricing of the single hike priced in 2019 and the 5y point on the US curve in particular could see upward pressure. All in all, we expect the US curve to continue to flatten both 2y10 and 5y10y after the FOMC meeting.

Fed March hike unlikely to steer a new direction for USD

On average, with the Fed unlikely to signal four hikes this year, but possibly upping rate expectations for 2019, a March hike is unlikely to steer a new direction for USD. Notably we stress that a hike in itself is unlikely to provide much dollar support given that is seen as a ‘done deal’ by the market. More broadly, we stress that actual movements in interest rates are indeed of little use in predicting USD moves at present as the Fed has entered a phase in the policy cycle – notably versus e.g. the ECB – during which the currency historically has not seen a clear direction from central-bank policy (see chart). Rather than the Fed, we think Trump policies are more important for USD at present, i.e. how the president’s ‘America first’ agenda plays out will be key for the medium-term direction for dollar crosses, see FX Strategy: Trump in MEVA space: US isolation puts USD at risk, 14 March 2017. Near term, EUR/USD is set to stay in the 1.21-1.26 range as the ECB is reluctant to allow a more aggressive pricing of its normalisation process.

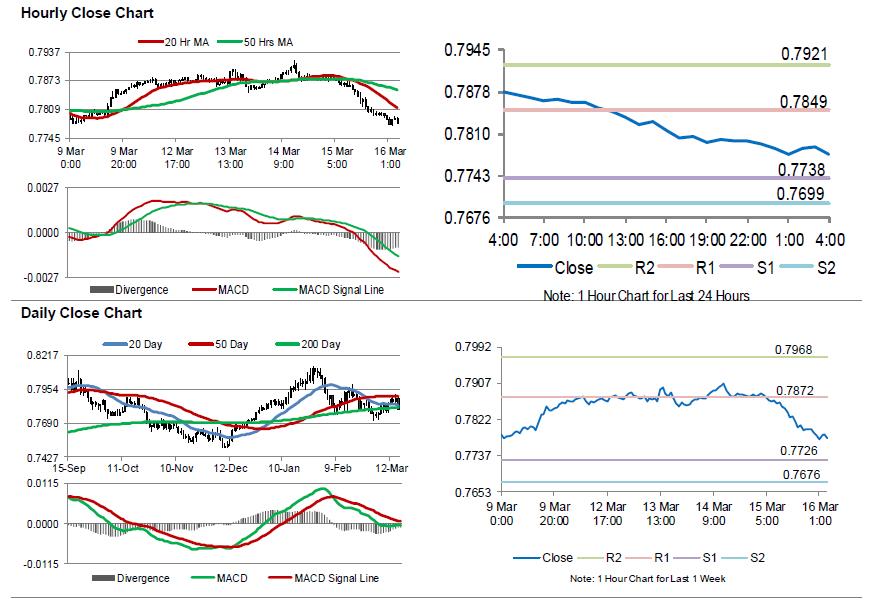

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 1.13% against the USD and closed at 0.7793.

LME Copper prices declined 1.9% or $129.5/MT to $6885.5/MT. Aluminium prices declined 1.6% or $33.5/MT to $2062.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7777, with the AUD trading 0.21% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7738, and a fall through could take it to the next support level of 0.7699. The pair is expected to find its first resistance at 0.7849, and a rise through could take it to the next resistance level of 0.7921.

Next week, the Reserve Bank of Australia’s March meeting minutes and Australia’s unemployment rate data, will keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

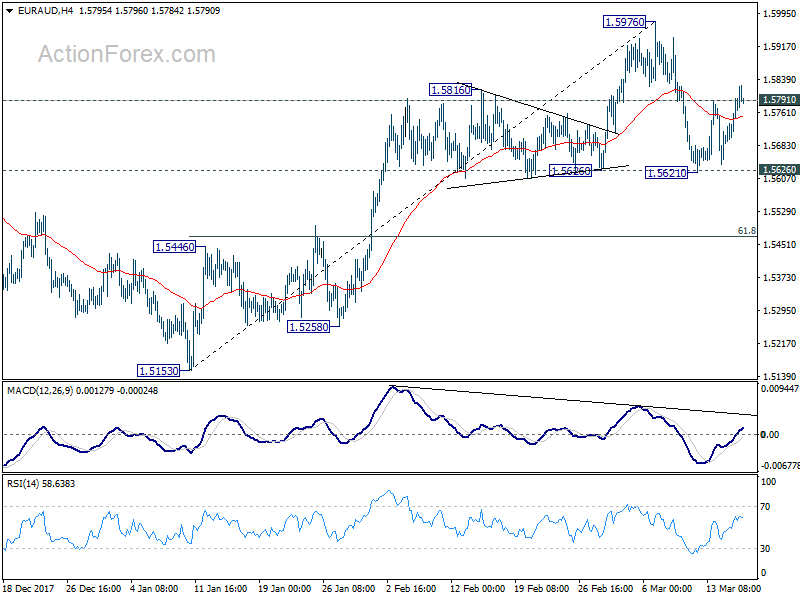

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5715; (P) 1.5755; (R1) 1.5816; More....

EUR/AUD's strong rebound and break of 1.5791 minor resistance suggests that pull back fro 1.5976 has completed at 1.5621, after drawing support from 1.5626 support. Intraday bias is turned back to the upside for retest 1.5976 first. Break will resume larger up rise from 1.3624. On the downside, decisive break of 1.5626 near term support will firstly resume the fall from 1.5976. Secondly, that will also raise the odds of larger reversal. Deeper fall should then be seen to 61.8% retracement of 1.5153 to 1.5976 at 1.5467 and below.

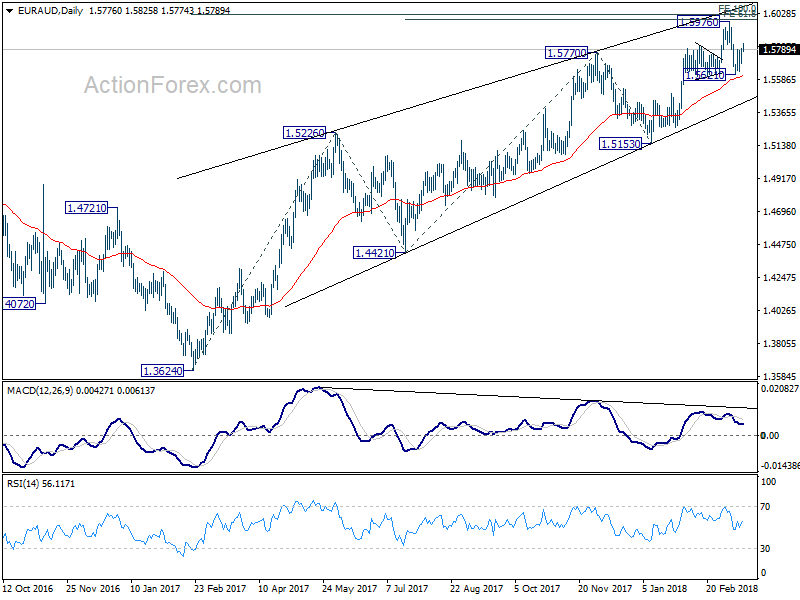

In the bigger picture, change of medium term reversal is increasing with EUR/AUD just missing double projection target. They are 61.8% projection of 1.4421 to 1.5770 from 1.5153 at 1.5987, and 100% projection of 1.3624 to 1.5226 from 1.4421at 1.6023. Also, bearish divergence condition remains in daily MACD. Break of 1.5626 support will add to this bearish case and target 1.5153 key support for confirmation. Nonetheless, before that happens, as long as 1.5153 support holds, medium term rise from 1.3624 could still extend to retest 1.6587 high.

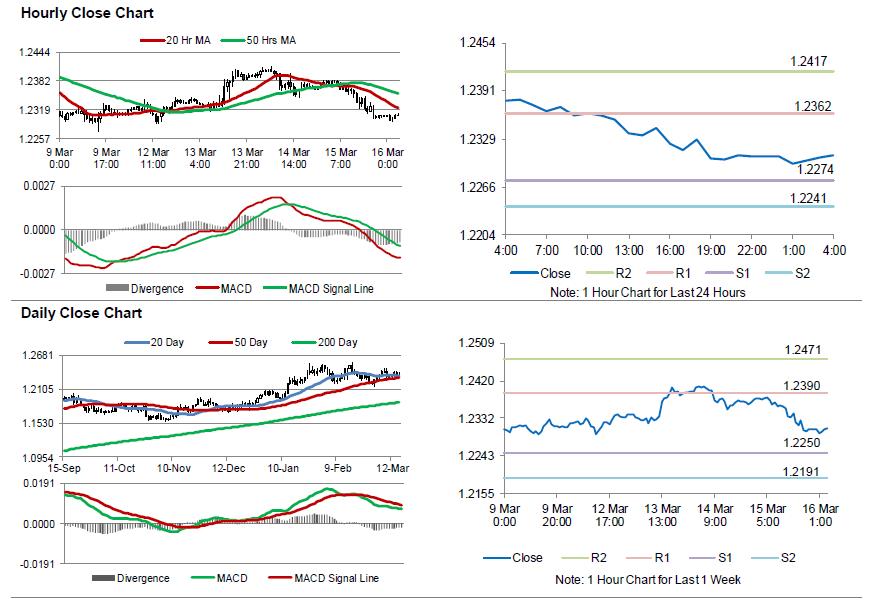

Euro Trading A Tad Higher, Ahead Of Euro-Zone’s Final Consumer Price Inflation Data

For the 24 hours to 23:00 GMT, the EUR declined 0.57% against the USD and closed at 1.2306.

The US Dollar advanced against a basket of major currencies, on upbeat US economic reports. Data revealed that the number of Americans filing for fresh jobless claims dropped more-than-expected to a level of 226.0K in the week ended 10 March, thus pointing to continued strength in the nation's labour market. Initial jobless claims had recorded a revised reading of 230.0K in the previous week, while investors had anticipated for a fall to a level of 228.0K.

Other data revealed that the US import price index rose 0.4% on a monthly basis in February, exceeding market expectations for a rise of 0.2%. The index had registered a revised rise of 0.8% in the prior month. Moreover, the nation's export price index advanced less-than-anticipated by 0.2% MoM in February, while investors had envisaged for a gain of 0.3%. The index had recorded a rise of 0.8% in the previous month. Furthermore, the nation's New York Empire State manufacturing index registered a rise to a level of 22.5 in March, beating market consensus for an advance to a level of 15.0. The index had registered a level of 13.1 in the prior month.

On the contrary, the nation's NAHB housing market index unexpectedly eased to a level of 70.0 in March, dipping for the third straight month and defying market consensus for a rise to a level of 72.0. In the prior month, the index had registered a revised level of 71.0. Moreover, the nation's Philadelphia Fed manufacturing index declined to a level of 22.3 in March, more than market anticipation for a fall to a level of 23.0 and compared to a level of 25.8 in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.2308, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.2274, and a fall through could take it to the next support level of 1.2241. The pair is expected to find its first resistance at 1.2362, and a rise through could take it to the next resistance level of 1.2417.

Going ahead, investors would keep a close watch on Euro-zone's final inflation figures for February, slated to release in a few hours. Additionally, the US flash Michigan consumer sentiment index for March as well as housing starts, building permits, industrial and manufacturing production data, all for February, scheduled to release later in the day, will garner significant amount of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

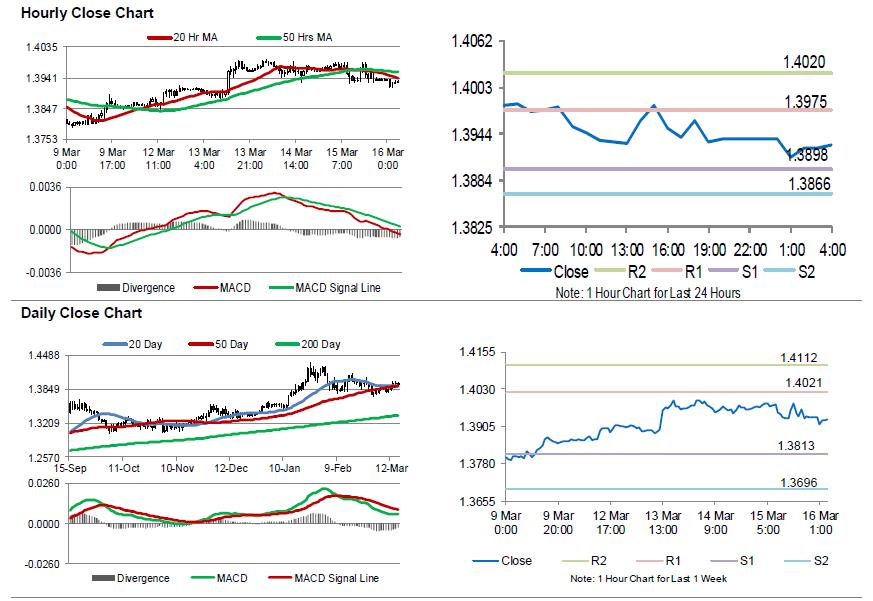

Pound Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the GBP declined 0.28% against the USD and closed at 1.3937.

In the Asian session, at GMT0400, the pair is trading at 1.3929, with the GBP trading 0.06% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3898, and a fall through could take it to the next support level of 1.3866. The pair is expected to find its first resistance at 1.3975, and a rise through could take it to the next resistance level of 1.4020.

Amid no macroeconomic releases in UK today, investors would look forward to the Bank of England’s interest rate decision, due next week. Moreover, UK’s consumer price inflation, retail sales and the ILO unemployment rate, will be on investors’ radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

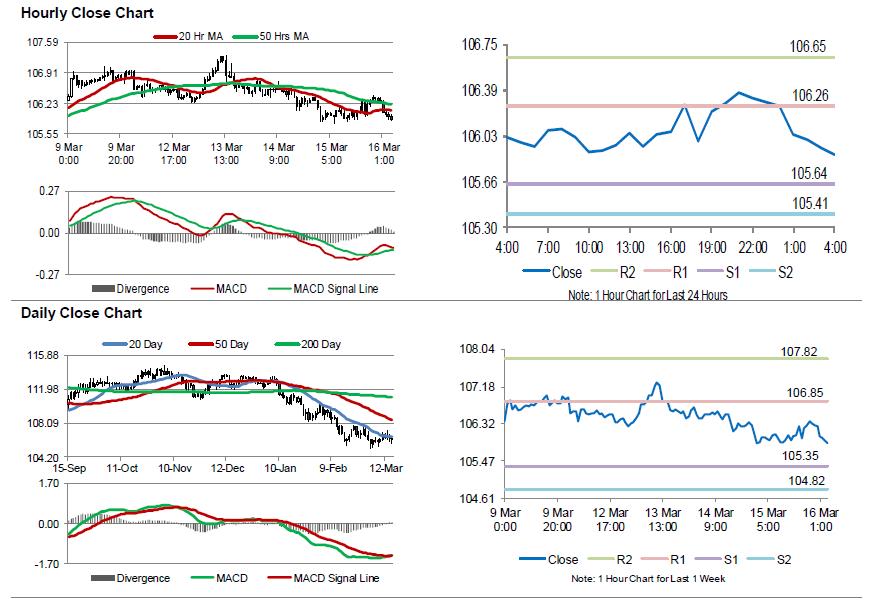

Japan’s Industrial Production Revised Lower In January

For the 24 hours to 23:00 GMT, the USD rose 0.27% against the JPY and closed at 106.30.

In the Asian session, at GMT0400, the pair is trading at 105.88, with the USD trading 0.4% lower against the JPY from yesterday's close.

Overnight data revealed that Japan's final industrial production fell more than initially estimated by 6.8% on a monthly basis in January, while the preliminary figures had indicated a fall of 6.6%. Industrial production had recorded a rise of 2.9% in the prior month.

The pair is expected to find support at 105.64, and a fall through could take it to the next support level of 105.41. The pair is expected to find its first resistance at 106.26, and a rise through could take it to the next resistance level of 106.65.

Going ahead, market participants would eye Japan's flash Nikkei manufacturing PMI, all industry activity index and trade balance data, all slated to release next week, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

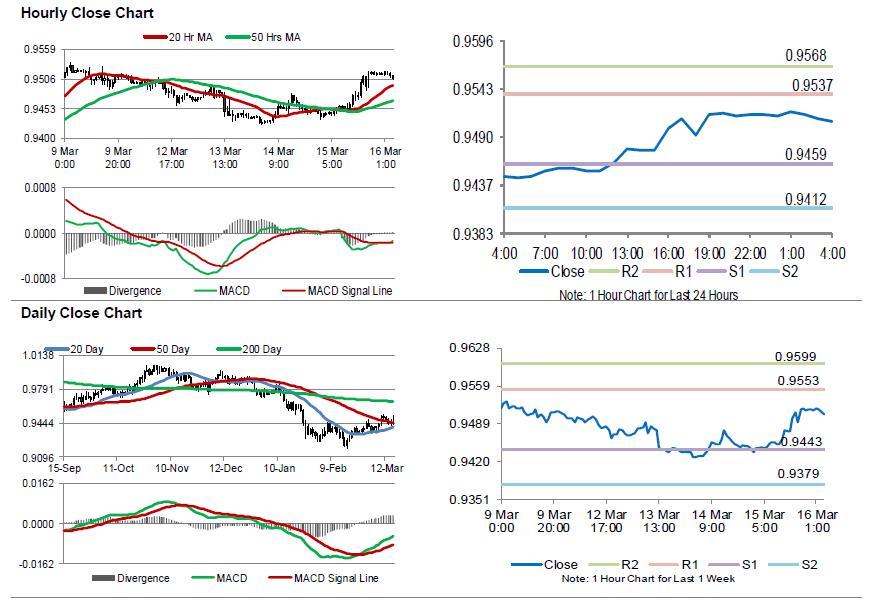

SNB Maintained The Benchmark Interest Rate Unchanged At -0.75%

For the 24 hours to 23:00 GMT, the USD rose 0.74% against the CHF and closed at 0.9515.

Yesterday, the Swiss National Bank (SNB), at its March monetary policy meeting, opted to keep the benchmark deposit rate steady at -0.75%, in line with market expectations. In its policy statement, the central bank reiterated its willingness to intervene in the currency markets as the Swiss Franc is still overvalued. Further, the SNB expects the Swiss economy to expand around 2.0% this year, citing a broader pickup in the global economy.

On the macro front, Switzerland’s producer and import price index grew 0.3% on a monthly basis in February. In the prior month, the index had registered a similar rise.

In the Asian session, at GMT0400, the pair is trading at 0.9507, with the USD trading 0.08% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9459, and a fall through could take it to the next support level of 0.9412. The pair is expected to find its first resistance at 0.9537, and a rise through could take it to the next resistance level of 0.9568.

Next week, investors would closely monitor Switzerland’s trade balance and the SECO economic forecasts report.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

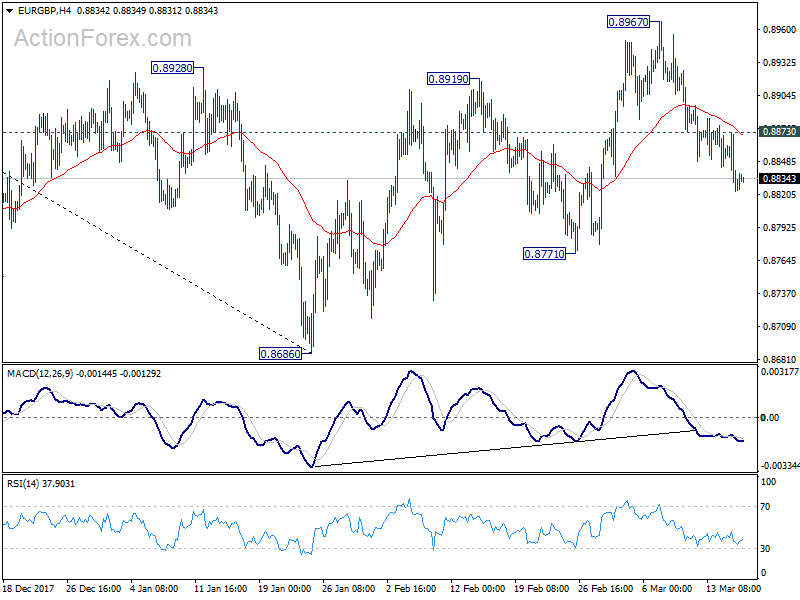

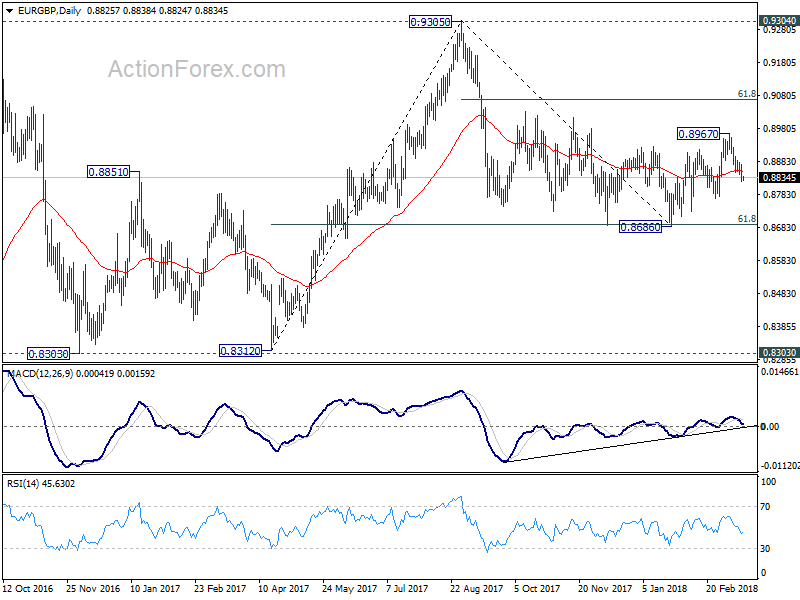

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8810; (P) 0.8842; (R1) 0.8860; More...

Intraday bias in EUR/GBP remains on the downside as fall from 0.89678 extends. Break of 0.8771 support will confirm completion of rebound from 0.8686 and target a retest of this low. On the upside, above 0.8896 minor resistance will turn bias neutral first. Further break of 0.8967 will resume the rebound from 0.8686 to 61.8% retracement of 0.9305 to 0.8686 at 0.9069.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Canada’s Existing Home Sales Sharply Deteriorated In February

For the 24 hours to 23:00 GMT, the USD rose 0.8% against the CAD and closed at 1.3057.

The Canadian Dollar declined against the USD, after Canada's existing home sales slid 6.5% on a monthly basis in February, intensifying concerns over the health of the nation's housing sector. In the previous month, existing home sales had registered a drop of 14.5%.

In the Asian session, at GMT0400, the pair is trading at 1.3060, with the USD trading slightly higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2980, and a fall through could take it to the next support level of 1.2900. The pair is expected to find its first resistance at 1.3106, and a rise through could take it to the next resistance level of 1.3152.

Ahead in the day, investors would keep a close watch on Canada's manufacturing sales data for January.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

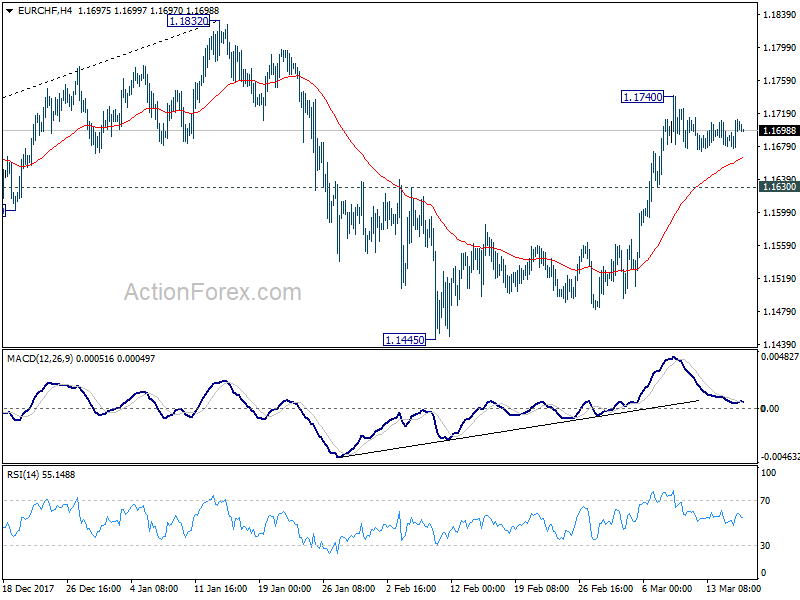

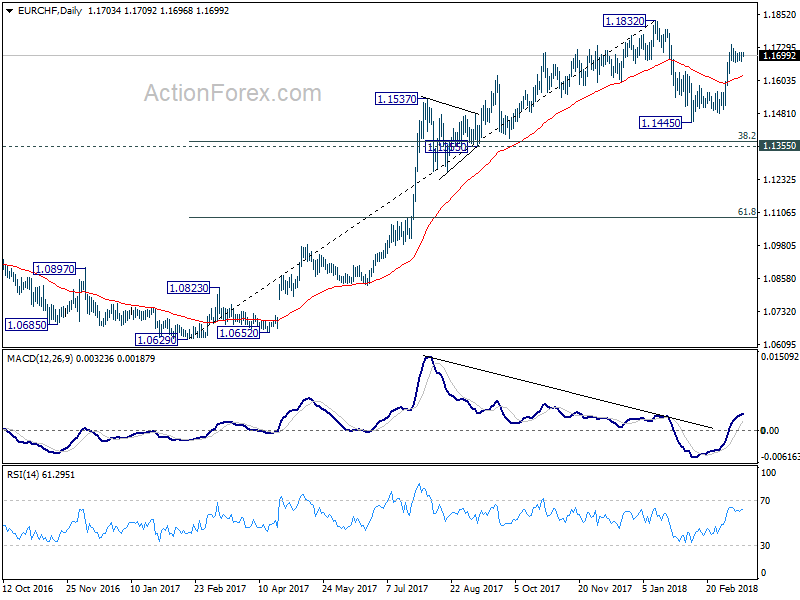

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1684; (P) 1.1698; (R1) 1.1720; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 1.1740 temporary top is extending. With 1.1630 minor support intact, further rise is expected in the cross. On the upside, above 1.1740 will target a test on 1.1832 high. We'll stay cautious strong resistance from there to bring another fall. Corrective pattern from 1.1832 might still have an attempt on 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372) before completion. On the downside, below 1.1630 minor support will target 1.1445 low again.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.