Sample Category Title

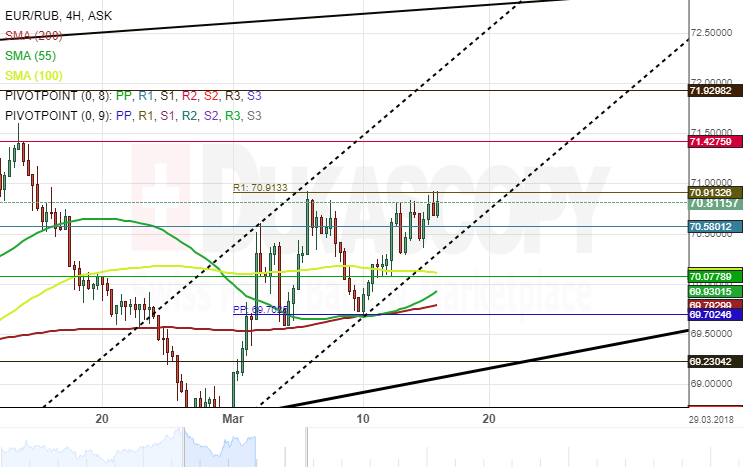

EUR/RUB 4H Chart: Continues To Surge

The common European currency has been trading in a long-term ascending channel against the Russian Ruble. The pair bounced off the lower boundary of a dominant channel on April 19, 2017, and has since reached a new high.

A strong support cluster set by the weekly pivot point with the combination of the 55– and the 200-hour SMAs was providing support near 69.70 as it can be observed on the chart.

As for near future, the EUR/RUB currency exchange rate is likely to continue moving upwards for a test of the upper boundary of a junior pattern where the monthly PP is located.

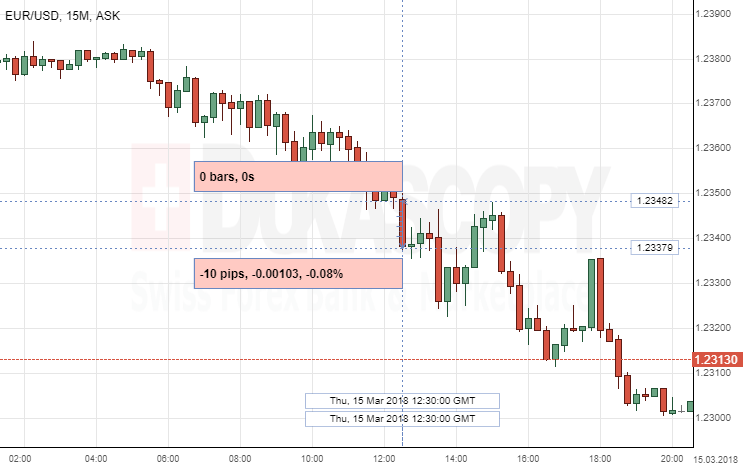

EUR/USD: US Unemployment Claims

The Greenback fluctuated based on the releases of the controversial reports from the Federal Reserve Bank of New York and Philadelphia and the US Department of Labour on Thursday. The EUR/USD currency pair lost 10 pips, or 0.08%, reaching the 1.2337 level.

The three simultaneously released reports created small increase in volatility in the financial currency market. The US unemployment claims data came out slightly better than expected, and with a help of the positive Empire State manufacturing index data, pushed EUR/USD pair lower. However, the Philly Fed manufacturing index data came out a bit short of expectations, as the divergence did not surprise the markets enough for a correction.

Yen Gains As US Political Uncertainty Intensifies

Here are the latest developments in global markets:

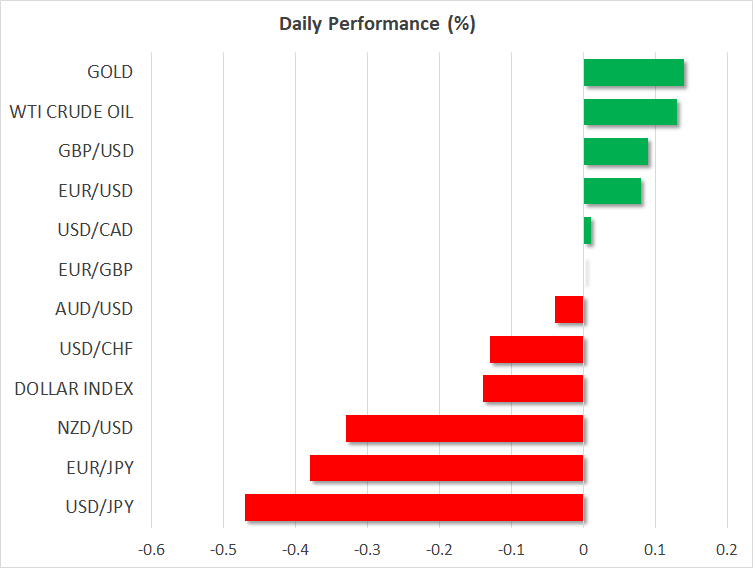

FOREX: The dollar traded lower against a basket of currencies on Wednesday on the back of reports suggesting that the White House personnel shakeup would continue. The safe-haven perceived yen was the biggest beneficiary from these reports.

STOCKS: US markets ended mixed yesterday, as political uncertainty and protectionist concerns continued to suppress risk appetite. Reportedly, Special Counsel Robert Mueller ordered the Trump organization to hand over documents related to the Russian investigation, while separate reports suggest the President is set to sack his national security advisor next. The Dow Jones climbed by 0.5%, while the S&P 500 and the Nasdaq Composite fell by 0.1% and 0.2% respectively. Moreover, futures tracking the Dow, S&P and Nasdaq 100 are all currently flashing red. The risk aversion rolled into Asian trading, with Japan's Nikkei 225 and Topix tumbling by 0.6% and 0.4% correspondingly, while Hong Kong's Hang Seng index was down by 0.3%. In Europe, futures tracking all major benchmarks are in negative territory, pointing to a slightly lower open.

COMMODITIES: In energy markets, both WTI crude and Brent are higher by 0.1% today, ahead of the Baker Hughes oil rig count data at 1700 GMT. Rigs fell in the previous week, and it will be interesting to see if the pattern continues. If so, it would enhance the narrative that US production may have peaked for now, easing some of the downward pressure on oil prices. In precious metals, gold is up by 0.15% today, recovering some of the notable losses it posted yesterday on the back of a stronger US dollar. The yellow metal has remained largely indifferent to the recent risk aversion, in contrast to other safe-haven assets such as the Japanese yen or US Treasuries, which have experienced a notable surge in demand.

Major movers: Yen on the rise on seeming lack of stability in the White House

Reports that US President Donald Trump plans to oust his national security adviser H.R. McMaster weighed on the dollar. Those reports were later refuted by the White House, but still, given they add to the narrative that things are not working smoothly in the administration, they continued to act to the detriment of the US currency. The dollar index was down by 0.1% at 0730 GMT. Falling long-term Treasury yields were also seen as contributing to the decline in the dollar.

The yen, which tends to benefit at times of uncertainty, was on the rise on the back of US political developments. Dollar/yen traded 0.45% lower at 105.85. A political scandal has been hitting headlines earlier in the week in Japan, mounting pressure on the country's Finance Minister to resign. Japanese press is currently reporting the Finance Minister will not be attending the highly-anticipated G20 meeting next week, which serves as a testament to the seriousness of the situation. Weekend poll results on the approval rating of Prime Minister Shinzo Abe – who has been promoting a weak yen policy – will be attracting interest in this respect. Euro/yen was also facing pressure, being down by 0.4% at 130.35.

Euro/dollar traded higher by 0.1% at 1.2319 after shedding 0.5% on Thursday. Dovish-perceived comments by ECB chief Mario Draghi didn't allow the currency to advance versus the dollar this week. It is notable that euro/pound recorded a more than two-week low of 0.8821 on Thursday. Today the pair is flat, trading not far above the aforementioned low.

Pound/dollar was 0.1% up at 1.3950, with developments on Brexit expected to offer direction to the pair moving forward.

In commodity-linked currencies, dollar/loonie was roughly flat after surging 0.8% on Thursday. Soft housing data out of Canada led market participants to revise their tightening expectations for the Bank of Canada, pushing additional rate hikes back in time, while some comments by President Trump spurred trade worries and also hurt the Canadian dollar. Despite currently being flat, dollar/loonie recorded a near nine-month high of 1.3071 earlier on Friday. The aussie and the kiwi were down by 0.05% and 0.3% versus their US counterpart on falling risk sentiment. Aussie/dollar and kiwi/dollar touched 0.7768 and 0.7239 earlier on Friday, their lowest since March 6.

Day ahead: Eurozone & US data due with political uncertainties in the spotlight

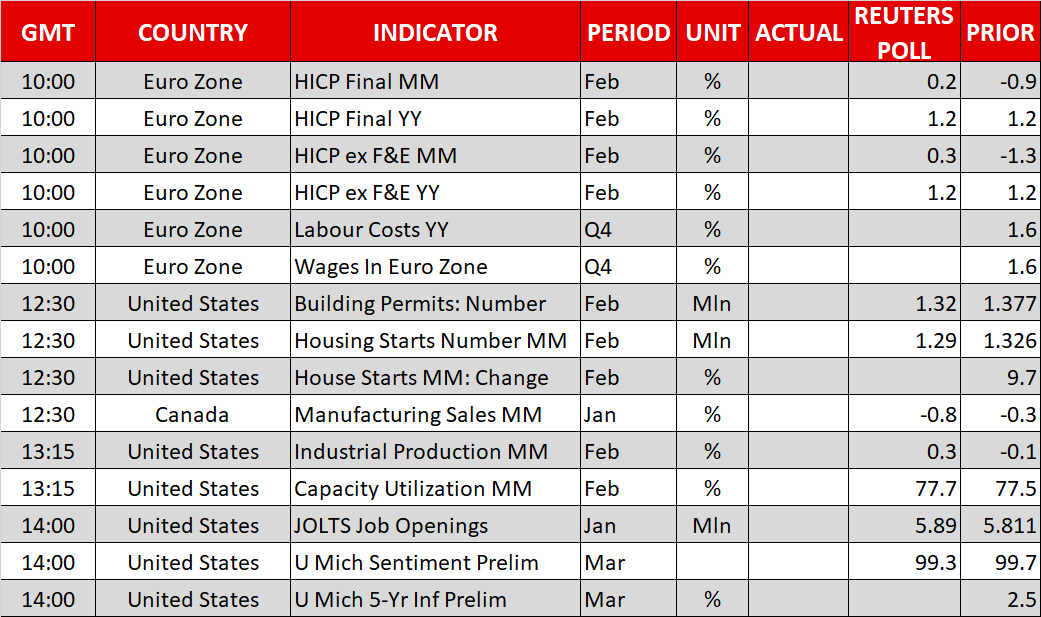

In the eurozone, the most noteworthy release will be wage growth figures for Q4 at 1000 GMT, though no forecast is available. Faster wages are critical for inflation to move higher and thus, these prints will be watched closely by ECB policymakers and investors alike. A potential acceleration in wages could spark speculation that inflation may pick up soon and that the ECB could adopt a more hawkish stance at its upcoming meetings, thereby helping the euro to recover some of its latest losses. Conversely, if wages grow at the same pace as previously or slow down, the common currency may continue to correct lower. Eurozone's final CPI data for February are also due out at 1000 GMT, but the final figures are usually not a major market mover.

In the US, industrial production data for February will be released at 1315 GMT and expectations are for production to have risen by 0.3%, a rebound following a 0.1% tumble previously. Besides this, there's a raft of second-tier indicators due out. Building permits and housing starts for February will be made public a little earlier, at 1230 GMT. A few hours later, at 1400 GMT, the preliminary University of Michigan consumer sentiment index for March and the Job Openings and Labor Turnover Survey (JOLTS) for January will be in focus.

In equity markets, the spotlight remains on political developments, particularly those surrounding protectionism. Note that yesterday, White House trade adviser Peter Navarro said that in the coming weeks, President Trump will get recommendations on how to address China's “theft” of American intellectual property. He added that this will be only one of many steps that the administration will take to tackle unfair trade practices, intensifying speculation that the situation could quickly escalate into a tit-for-tat trade war.

In the oil market, the Baker Hughes oil rig count is due for release at 1700 GMT. The number of active US rigs fell last week, providing an indication that US production may have peaked for the time being, or is slowing down at least. Another decline in rigs today could add credibility to that argument and thereby, ease some of the downward pressure on oil prices in the near-term. Even if that is the case though, it's worth noting that agencies like the EIA anticipate US production to surge much further by the end of the year, so any slowdown in US supply may prove to be only a temporary phenomenon.

In politics, attention is likely to remain on the chaos in US politics, and specifically on whether President Trump will indeed fire his national security advisor H.R. McMaster. If he does, this would mark the third departure of a key figure from the administration in the span of a few days, something widely seen as increasing the probability for more protectionism, as the more moderate voices are “leaving the building”.

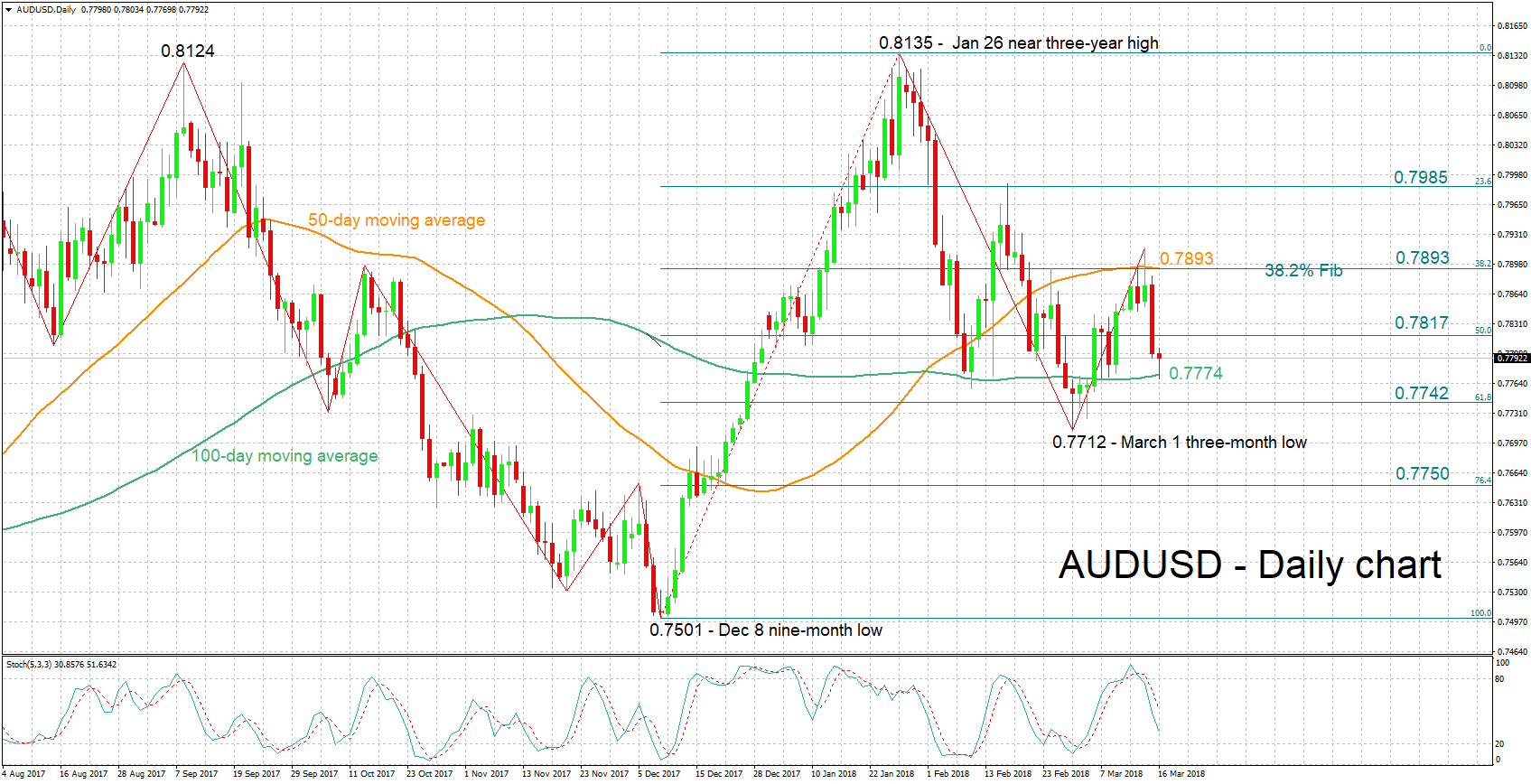

Technical Analysis: AUDUSD posts 12-day low; bearish signal by stochastics in very short-term

AUDUSD has recorded a 12-day low of 0.7768 earlier on Friday after losing roughly 1.0% on the day that preceded. The stochastics are giving a bearish picture in the very short-term for the pair: the %K line has crossed below the low %D one – while both lines were above 80 – and the two lines are currently heading lower. Australia is a major commodity exporter and its currency tends to benefit on upbeat views on the global economy.

Escalating trade tensions weighing on the outlook for global growth could hurt the pair. At the moment, support could be occurring around the 100-day moving average at 0.7774 which was briefly violated earlier on Friday. A downside violation would bring into view the 61.8% Fibonacci retracement level of the December 8 to January 26 upleg at 0.7742 for additional support.

Receding fears for a trade war on the other hand are expected to boost risk appetite and likely support AUDUSD. Resistance in this case could come around the 50% Fibonacci level at 0.7817 and further above – in case of stronger bullish movement – at the 38.2% Fibonacci mark and the 50-day MA which coincide at 0.7893.

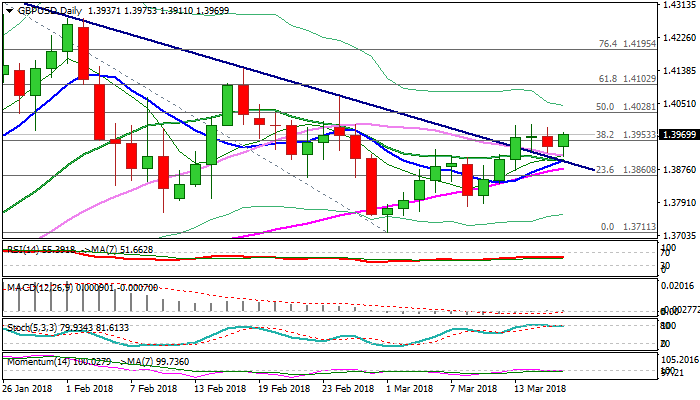

Technical Outlook: GBPUSD – Fresh Bulls Attack Again Key 1.40 Zone

Cable is in fresh bullish acceleration after dips in Asia were contained by 30SMA, which marked strong support in past couple of sessions.

Fresh attempts higher are pressuring daily cloud top (1.3979) and looking for renewed attack at psychological 1.40 barrier, after repeated rejections in the zone in past few days.

Bullishly aligned daily MA’s remain supportive, but lack of stronger momentum might be an obstacle.

Sustained break above 1.40 zone (top of congestion which extends into fourth straight day) is needed to signal continuation of recovery leg from 1.3711 (01 Mar) towards 1.4070/ 1.4103 (01 Mar high / Fibo 61.8% of 1.4345/1.3711 descend).

Repeated failure at 1.40 zone would signal extended range trading, while key supports at 1.3913/02 (30SMA / broken bear-trendline off 1.4345 peak) hold.

Firm break below 1.39 handle would mark lower platform and generate bearish signal fresh weakness.

Res: 1.3979, 1.4000, 1.4028, 1.4070

Sup: 1.3913, 1.3902, 1.3888, 1.3853

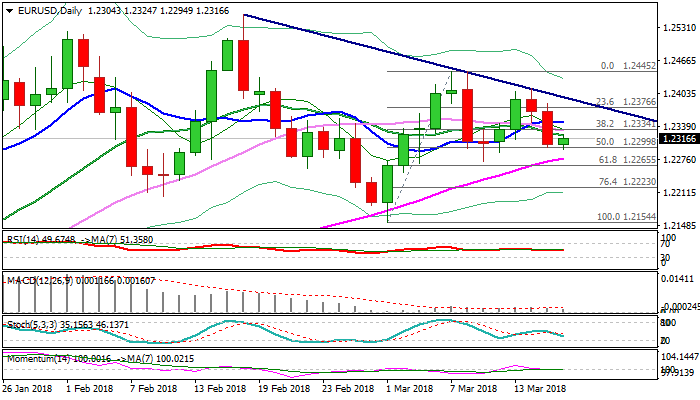

Technical Outlook: EURUSD – Bears Take A Breather Ahead Of Key Support Zone As Dollar Weakens On Fresh Political...

The Euro ticked higher in early Friday after strong fall in past two days found footstep at daily cloud top which provides solid support, currently at 1.2296. Near-term structure weakened after bulls were capped by bear-trendline off 1.2555 peak at 1.2412 on Wednesday and Thursday’s strong bearish acceleration resulted in close below a cluster of daily MA’s (10,20,30SMA) in 1.2322/47 zone, which now turned to resistances.

Momentum is moving into negative territory and adding to existing pressure, signaled by MA’s bearish setup.

Today’s brief bounce was triggered by weaker dollar on fresh political uncertainty in the US and could be seen as a breather before bears continue.

Strong support zone between 1.2296 and 1.2265, consisting of daily cloud top, 55SMA and Fibo 61.8% of 1.2154/1.2445 upleg needs to be cleared to complete failure swing pattern on daily chart and signal bearish continuation.

EU inflation data are key event of European session, with a batch of data expected in the American session (US housing data, IP, Michigan consumer sentiment) which could provide fresh direction signals.

Res: 1.2332, 1.2348, 1.2399, 1.2412

Sup: 1.2296, 1.2278, 1.2265, 1.2223

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

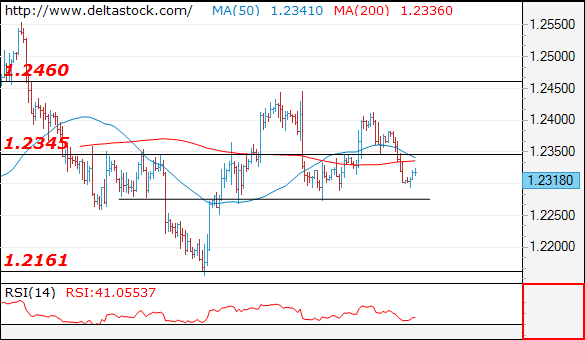

EUR/USD

Current level - 1.2318

My outlook here is counter-trend, for a reversal of the slide form 1.2410, towards 1.2460 resistance. Initial intraday support is projected around 1.2270.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2460 | 1.2460 | 1.2350 | 1.2160 |

| 1.2460 | 1.2560 | 1.2280 | 1.2090 |

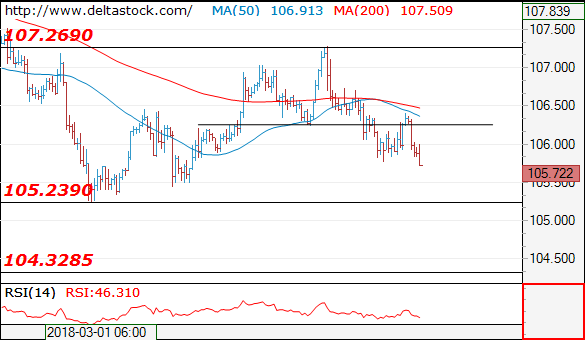

USD/JPY

Current level - 105.72

The minor rebound to 106.40 confirms the negative outlook, for a test and break through 105.20 low, en route to 104.30 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 106.40 | 108.30 | 105.20 | 105.20 |

| 108.00 | 110.40 | 105.20 | 102.40 |

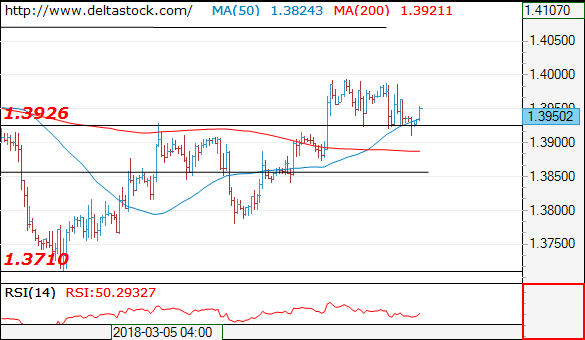

GBP/USD

GBP/USD

Current level - 1.3950

The structure below 1.4000 is still corrective and the outlook remains positive, for a rise towards 1.4150. Initial support lies at 1.3920-30.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4000 | 1.4150 | 1.3930 | 1.3710 |

| 1.4150 | 1.4280 | 1.3870 | 1.3620 |

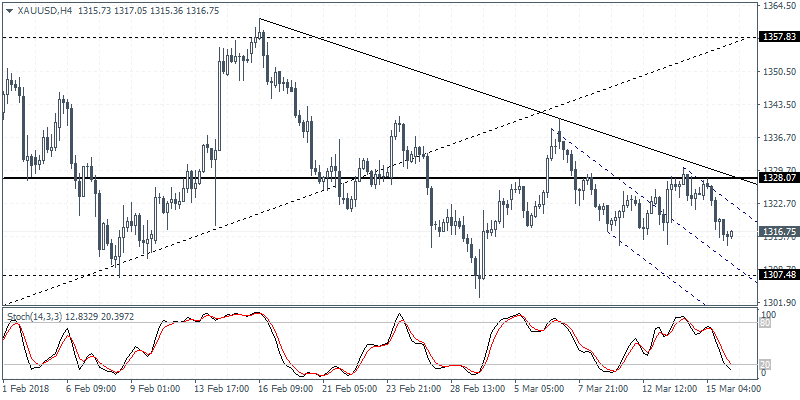

XAUUSD Intraday Analysis

XAUUSD (1316.75): Gold prices were seen retreating off the 1328 level with price action currently biased to the downside. Support at 1307 could be tested in the near term if the downside momentum continues. We expect to see gold prices potentially holding the declines at this support level and could move into a sideways range into next week's FOMC meeting. A break below 1307 could extend the declines towards the round number support at 1300.00.

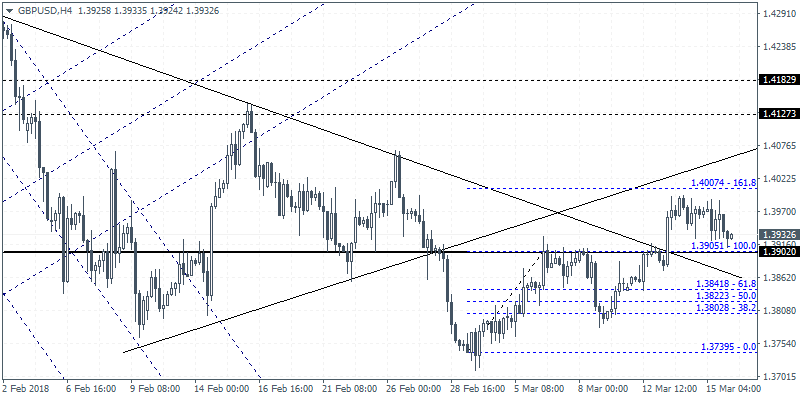

GBPUSD Intraday Analysis

GBPUSD (1.3922): The British pound was seen trading soft above 1.3902. Following the doji session two days ago, price action was seen closing on a bearish note yesterday. A close below 1.3902 is required for the currency pair to post further declines. The near-term declines could stall near the 1.3905 level where support could be established. GBPUSD is yet to test the 1.4007 level which marks the nearterm target for the bullish ascending triangle formed on the 4-hour chart. However, if price closes below 1.3902, we can expect dynamic support coming in from the falling trend line.

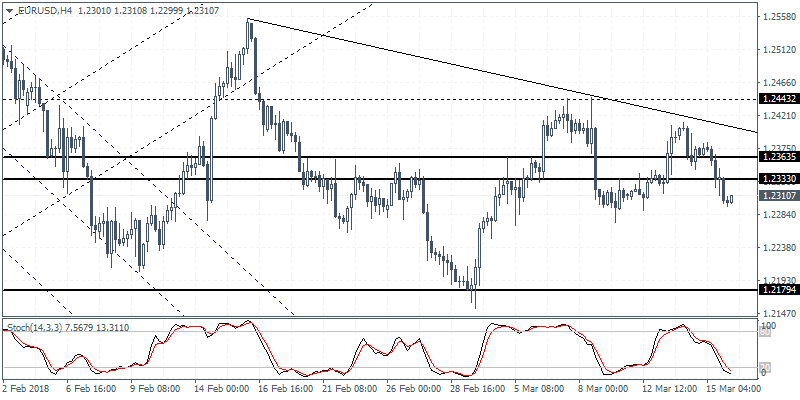

EURUSD Intraday Analysis

EURUSD (1.2310): The EURUSD was bearish yesterday with price action extending the declines for the second day. However, the declines pushed the common currency back below the 1.2333 level of support. The sideways range is expected to continue into next week's FOMC meeting. Uncertainty surrounding Trump's policies on trade along with the changes in Washington continue to keep the U.S. dollar subdued. The EURUSD is expected to be trading near the 1.2333 level with the declines like to stall near the previously established lower support at 1.2179.

USD Strengthens As Focus Turns To Next Week’s Fed Meeting

The U.S. dollar was seen posting some modest gains yesterday with investors positioning themselves ahead of the FOMC meeting next week. Expectations of an interest rate hike stands close to 90% for next week's Fed meeting.

On the economic front, the Swiss National Bank held its monetary policy meeting yesterday. The central bank maintained the three-month LIBOR rate at -0.75% and did not offer any new signals for the market as far as the Swiss monetary policy was concerned. The Norges Bank also held its meeting yesterday with interest rates left unchanged. However, the Norwegian central bank signaled that interest rates could rise by September this year.

Looking ahead, the Eurozone final inflation estimates will be coming out later today. Economists' forecasts point to subdued pace of increase in consumer prices. In the U.S. the building permits and housing starts data will be coming out followed by the industrial production figures.