Sample Category Title

Fitch predicts 25bps RBA hike in 2018, 50bps hike in 2019

Fitch rating agency predicts RBA to raise cash rate by 25bps this year. It also predicts another 50bps hike next year in 2019.

What Fitch observed is that RBA appears comfortable lagging behind other central banks in tightening policy, allowing exchange rate flexibility to serve as a buffer". This is in-line with what RBA Governor Stephen Lowe has repeated a couple of times. That is, RBA didn't cut as deep as other global central banks. And therefore, it also doesn't need to reverse that cycle as others like Fed and BoC.

But Fitch expects Australia economy to gain further momentum this year with growth holding steady at 2.7% in 2019. That's thanks to "strong terms of trade on income, broadly accommodative financial conditions and buoyant prospects for investment".

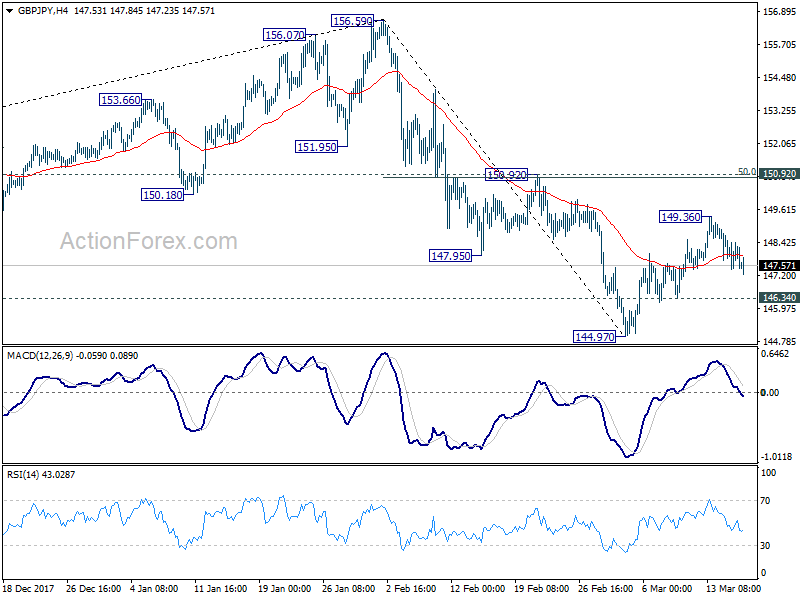

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.58; (P) 148.04; (R1) 148.63; More....

At this point, intraday bias in GBP/JPY remains neutral first. in case corrective rise from 114.97 extends, upside should be limited by 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption eventually. Below 146.34 minor support will suggest that the recovery has completed. Intraday bias will then be turned back to the downside for 144.97 first. Break will extend the decline from 156.59 to 143.51 medium term fibonacci level next.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

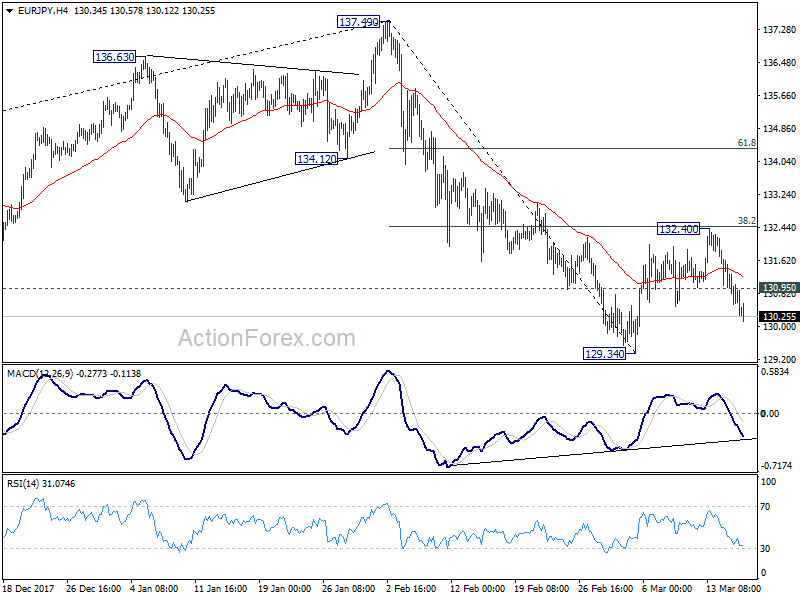

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.42; (P) 130.98; (R1) 131.39; More....

As noted before, the corrective rebound from 129.34 has completed at 132.40 already. That's slightly ahead of 38.2% retracement of 137.49 to 129.34 at 132.45. Intraday bias remains on the downside for retesting 129.34 low first. Break will resume whole fall from 137.49 and target 126.61 medium term fibonacci level. In case of another rise, we'd continue to expect strong resistance from 132.45 to limit upside.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

Eurozone Consumer Price Index And U.S. Housing Starts

At 10:00 GMT, Eurozone Consumer Price Index – Core (YoY) (Feb) will be released. The consensus points to an unchanged value of 1%. Consumer Price Index (MoM) (Feb) is expected to be 0.2% from -0.9% previously. Consumer Price Index (YoY) (Feb) is expected to be unchanged at 1.2%. Consumer Price Index – Core (MoM) (Jan) is expected at 0.4% from -1.7% prior. Inflation rose late in 2016 and early in 2017 to 2.0%, the highest levels in five years, but has stabilized around 1.3% since June (YoY). The ECB is looking for inflation to “approach 2%”. Labour Cost (Q4) is expected to be 1.8% against a previous reading of 1.6%. EUR pairs may see volatility pick up due to this data.

At 12:30 GMT, US Housing Starts (MoM) (Feb) is expected at 1.290M from a previous number of 1.326M. Building Permits (MoM) (Feb) is expected to come in at 1.320M, from the prior reading of 1.377M, which was revised down from 1.396M. This data is expected to show a slight fall in residential construction activity, but these data points have been recovering since hitting lows of 0.46M and 0.49M respectively after the 2009 financial crisis. The readings last month were the highest since those lows for both data points. USD crosses could see increased volatility around this data release.

At 13:15 GMT, US Industrial Production (MoM) (Feb) will be released. The consensus is for 0.3% from -0.1% previously. After four months of positive data, this measure slipped below the zero line in the last reading but is expected to rebound back to the positive today. Capacity Utilization (Feb) will also be released at this time, with an expectation for 77.7% v 77.5% prior. This data point fell last month after reaching a two year high in December. USD crosses may be impacted.

At 14:00 GMT, US Michigan Consumer Sentiment Index (Mar) is expected at 99.3 from a previous number of 99.7. This measure of consumer confidence is at levels not seen since 2003, with the highest level since the financial crisis being achieved in October with a reading of 101.1. USD crosses could move in reaction to this data.

At 17:00 GMT, Baker Hughes US Oil Rig Counts will be released with a headline number from last week of 796. WTI Oil could become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

Currencies: Euro Eases, but USD isn’t in great shape either

Rates: Bund outperforms with important technical break

The German 10-yr yield lost 0.62% support. The break suggests a return to 0.46%/0.48% support (gap open/62% retracement). US politics continue to play first fiddle, filling the eco/event void between now and next week's FOMC meeting. At this moment, it generates more safe haven flows into German Bunds instead of US Treasuries.

Currencies: Euro eases, but USD isn't in great shape either

EUR/USD drifted south yesterday as the ECB indicated that there is still a lot work to do to reach the inflation target. Today's eco data probably won't change the dynamics on the FX markets. We expect EUR/USD to hold the recent consolidation pattern going into the Fed meeting. USD/JPY looks more vulnerable

The Sunrise Headlines

- US stock markets ended mixed yesterday with the Dow Jones outperforming (+0.5%). Asian risk sentiment is mixed overnight with Japan underperforming (-0.5%) on a stronger yen.

- Nato closed ranks against Russian President Putin as the US unveiled new sanctions and joined France and Germany to back Britain's accusations against the Kremlin for the poisoning of a former Russian spy on UK soil. (FT)

- Sources say special Counsel Mueller has subpoenaed the Trump Organization for documents related into his investigation into whether Trump's associates colluded with Russia's efforts to interfere in the 2016 presidential election.

- US President Trump has decided to replace his national security adviser, H.R. McMaster, but the move is not expected to be made immediately, the Washington Post reported. The White House denied the report.

- The head of the US Chamber of Commerce warned the Trump administration that unilateral tariffs on Chinese goods could lead to a destructive trade war that will hurt American consumers and US economic growth.

- Investors are underpricing the risk of higher interest rates globally and need to seek adequate compensation for that risk, Deputy Governor of the RBA, Debelle, said.

- Today's eco calendar contains US housing starts, building permits, industrial production and Michigan consumer confidence. Final EMU inflation will also be published.

Currencies: Euro Eases, but USD isn't in great shape either

Euro declines, but dollar isn't in good shape either

Earlier this week, USD softness prevailed due to US political uncertainty. The USD still wasn't in great shape, but euro softness became more dominant yesterday. EUR/USD declined in the 1.23 big figure. Of late, interest rate differentials were often ignored, but 2-yr German/US spreads reached a new cycle peak. Finally, this provided some downside protection for the dollar against the euro. EUR/USD closed the session at 1.2305. From a technical point of view, the established ranges remain intact. The picture of USD/JPY remained fragile. Despite a late session rebound, the pair still closed the session at 106.34.

Overnight, BOJ governor Kuroda was reapproved for another term of five year. However, the focus in Japan is currently on the land scandal, questioning the political future of PM Abe and even more of Fin Min Aso. For now, the political noise, both in the US and Japan, is weighing on USD/JPY and on Japanese equities. USD/JPY dropped again below the 106 level. The loss of the dollar against the euro stays very modest (EUR/USD near 1.2315).

The final EMU CPI is expected at a low 1.2% Y/Y today. US housing starts building permits, production, and Michigan consumer confidence will also be published. These reports probably won't change investor expectations for next week's Fed meeting. This week, the euro came under modest pressure as a gradual ECB approach questions the timing of a first rate hike in 2019. At the same time, USD political uncertainty remains a factor, too. The EUR/USD decline might ease. A break below the 1.2273 correction low probably won't be that easy. At the same time, rising interest rate differentials make holding USD shorts quite costly. For now, we assume more consolidation in the 1.2155/1.2450 range going into next week's Fed meeting. Downside pressure in USD/JPY and EUR/JPY might also help to cap the topside in EUR/USD, even in case off broader USD weakness.

Technical considerations continued to dominate sterling trading. Cable was blocked ahead of the 1.40 resistance. EUR/GBP drifted south in line with EUR/USD. There are no UK eco data today. Tensions between Russia and the UK have little impact on sterling. Technically inspired trading for EUR/GBP around current levels might be in the cards.

EUR/USD eases slightly on reduced rate hike expectations, but stays within established range

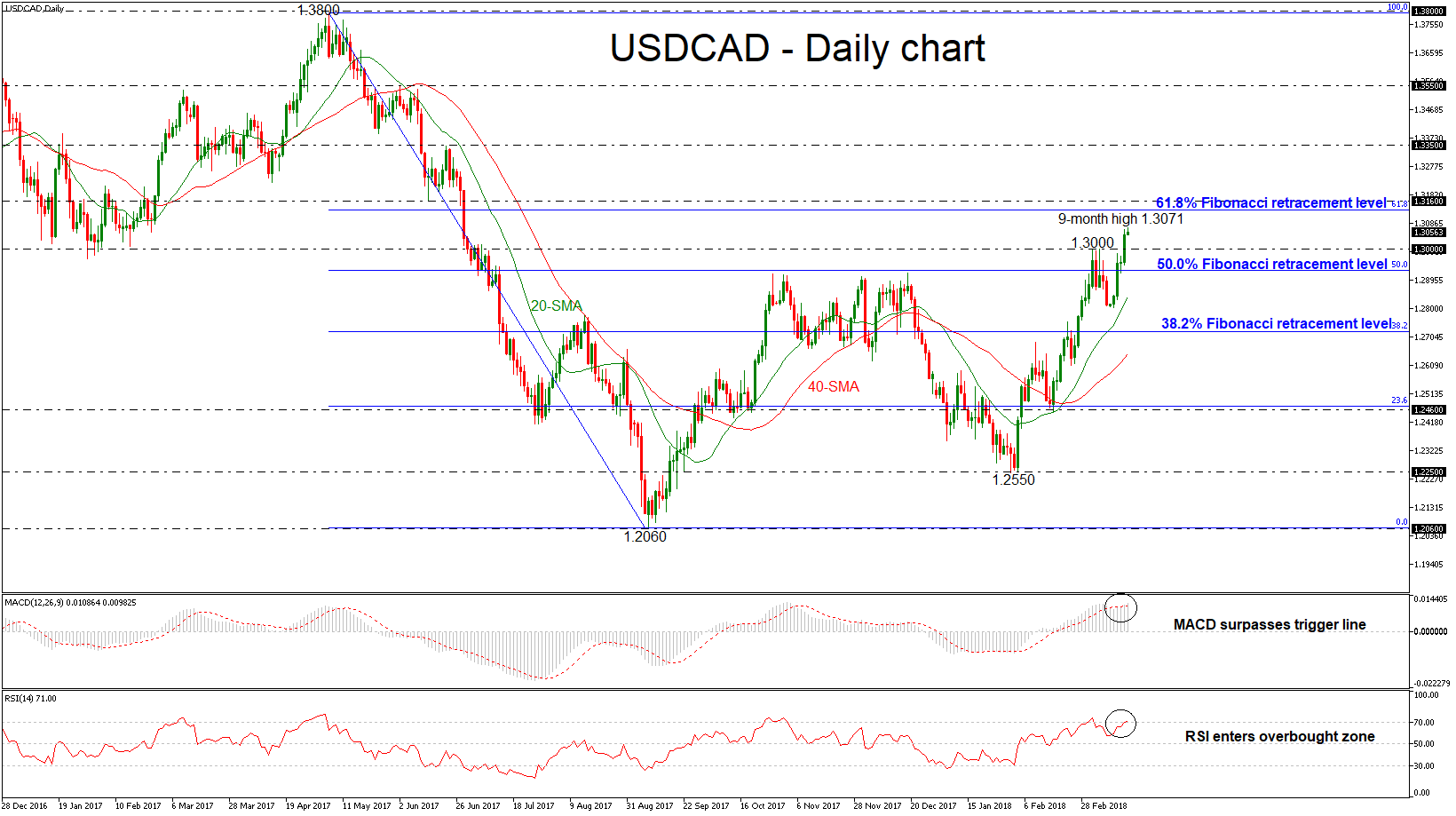

USDCAD Records 9-Month High, Sharp Buying Interest In Short Term

USDCAD has advanced considerably over the last four trading days, hitting an almost 9-month high of 1.3071 during today’s European session. Price action at the moment is taking place not far below this peak, having successfully surpassed the 1.3000 strong psychological level. The technical picture supports that the bullish bias is likely to continue in the short-term.

Having a look in the daily timeframe, the technical indicators are holding in the overbought areas. The RSI indicator is moving slightly above the threshold of 70, suggesting that the market could keep moving higher. The MACD oscillator also supports this view as it jumped above its trigger line, posting a bullish cross.

Upsides moves are likely to find resistance at 1.3130. This is the 61.8% Fibonacci retracement level of the downleg from 1.3800 to 1.2060. Slightly higher, the 1.3160 level could act as strong resistance obstacle taken from the low on June 2017. Breaking this level could see a retest of the 1.3350 high.

In the wake of negative pressures, the market could meet support at 1.3000 before it heads lower at the 50.0% Fibonacci mark near 1.2930. A successful close below this level could drive the price towards the 38.2% Fibonacci of 1.2720, but the pair needs to go through the 20-day simple moving average near 1.2840 at the time of writing.

Turning to the medium-term picture, the market seems to be in bullish mode given that the pair trades above the 1.3000 handle. In addition, as long as the bullish cross between the 20 and 40-week SMAs remains intact, the upside rally holds.

Forex Analysis: Kuroda Approved For Another 5-Year Term As BOJ Governor

Current BOJ Governor Kuroda has been approved for another 5-year term as the banks head, with nominees Wakatabe and Amamiya approved as BOJ deputy governors.

Russia has yet to act in relation to the British government decision to expel 23 Russian diplomats on Wednesday. It is expected that Russia will respond in kind to the British move. The US took action against the country yesterday by increasing sanctions for alleged meddling in the US Presidential Election. In related news, Special Counsel Robert Mueller issued a subpoena for the Trump Organisation to hand over documents, some of which are thought to show Russian links.

With international tensions ratcheting higher, the China holdings of US Treasuries have fallen to a six-month low. In a running battle with the US over trade, Chinese sources have reported that “if the U.S. wants to reduce its trade deficit, it has to make Americans more hard-working and conduct reforms in accordance with international market demand, instead of asking the rest of the world to change”.

French Consumer Price Index (EU norm) (YoY) (Feb) came in as expected at 1.3%, from 1.4% previously, which was revised down to 1.3%. This year’s seasonal drop has been much less than previously, giving some hope for future readings. EURUSD dipped to 1.23623 but recovered back to its starting level at 1.23698 after this data was released.

The Swiss National Bank Interest Rate Decision came in as expected, unchanged at -0.75%. The SNB will remain active in the FX market as necessary while taking the overall currency situation into consideration. The Swiss franc remains highly valued while the situation in the FX market is still fragile and monetary conditions may change rapidly. The SNB expects continued GDP of 2% in 2018 and a further gradual decrease in unemployment. The SNB will continue to monitor the real estate market closely. GBPCHF tested higher to 1.32216 before selling off to 1.31658 as a result of this event.

US Initial Jobless Claims (Mar 9) came in as expected at 226K, from 231K previously, which was revised down to 230K. Continuing Jobless Claims (Mar 2) was 1.879M v an expected 1.90M, from 1.87M previously, which was revised down to 1.875M. These data points show sustained strength in the labour market despite a slight miss on the headline number. Philadelphia FED Manufacturing Survey (Mar) was 22.3 v an expected 23.0, against 25.8 previously. Philly Fed Survey has been declining since its high in February 2017 but has remained above 20.0 over the last six months. This is now the longest run of sustained improvement in manufacturing conditions since 2005. EURUSD moved lower from 1.23495 to 1.23218 as a result of this data.

New Zealand Business NZ PMI (Mar) was 53.4 v 55.6 previously, which was revised lower to 54.4. After a fall in the January reading, this data point recovered in February but is now down again in March. This index has remained above 50 since December 2012. NZDUSD fell from 0.72797 to 0.72504 after this data came out.

RBA Assistant Governor Debelle made a scheduled speech about risk and return in a low rate environment, at the Financial Risk Day event hosted by the Centre for Financial Risk, in Sydney. He made the following comments: global asset prices depend on rate structure remaining low and he expects to see a re-pricing of assets if rates rise more. Equity prices assume the global economy can grow strongly without a pickup in inflation. He added that global monetary stimulus will unwind as the world recovers, with the lift in short-term yields and the recent spike in equity volatility a “small example” of what could happen as a result.

EURUSD is up 0.10% overnight, trading around 1.23166.

USDJPY is down -0.37% in early session trading at around 105.929.

GBPUSD is up 0.07% this morning, trading around 1.39457.

Gold is up 0.07% in early morning trading at around $1,316.99.

WTI is up 0.13% this morning, trading around $61.27.

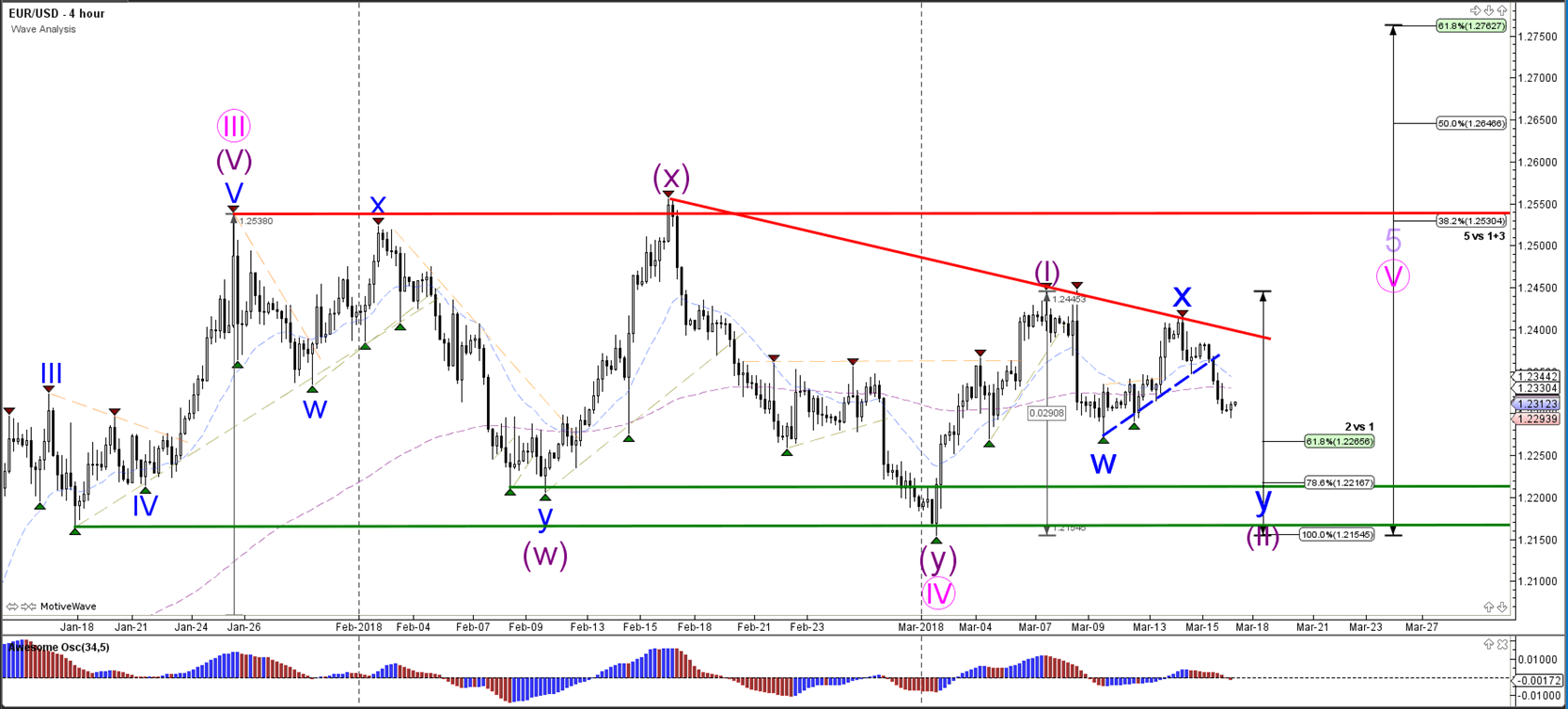

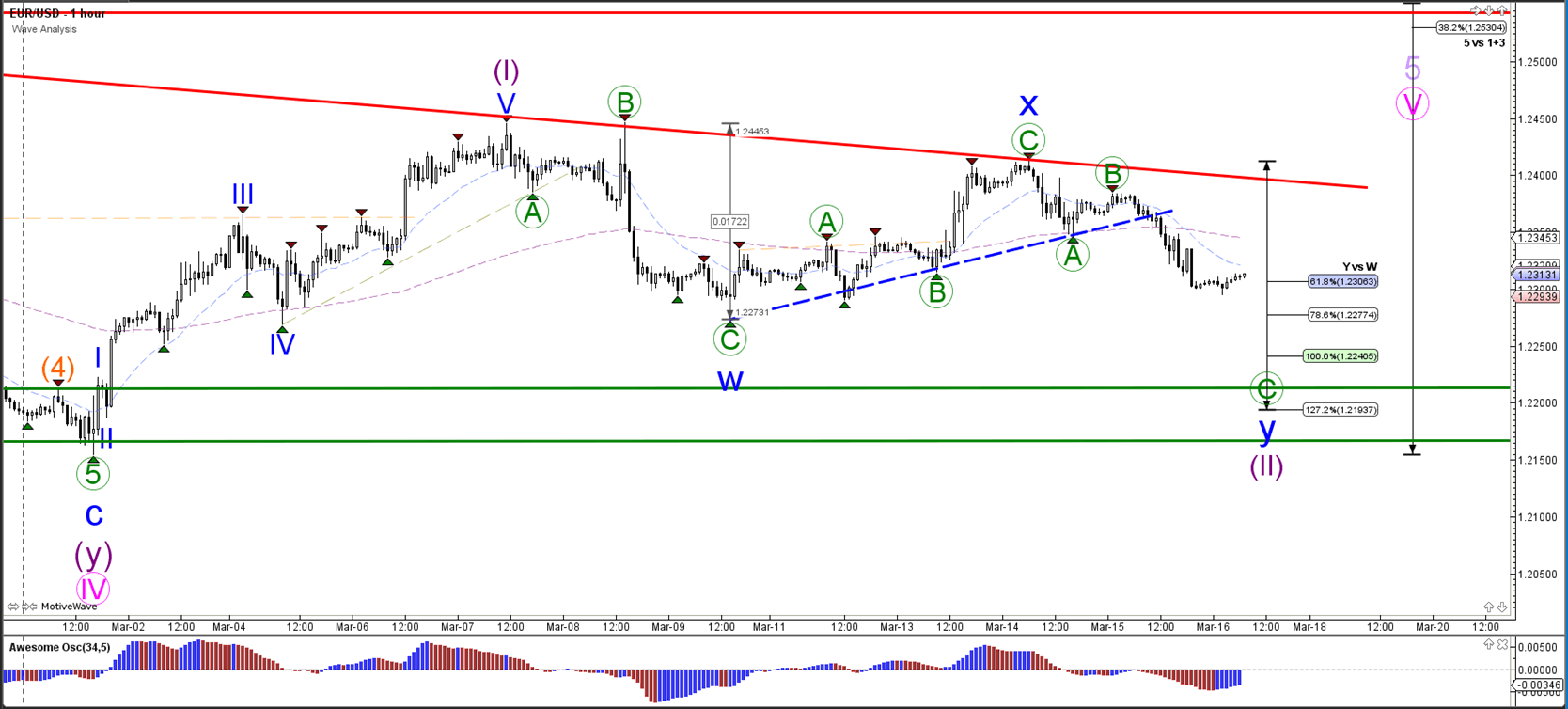

Daily Wave Analysis: EUR/USD Breaks Support Trend Line And Expands Wave 2 Correction

Currency pair EUR/USD

The EUR/USD broke below the support trend line (dotted blue) which makes a larger bearish correction more likely. The correction is probably part of a larger wave 2 (purple) correction, as long as price stays above the 100% Fibonacci level. A bullish break above resistance (red) could start waves 5.

The EUR/USD invalidated the wave 4 (green) pattern and is now probably expanding the wave C (green) within a larger WXY (blue) correction.

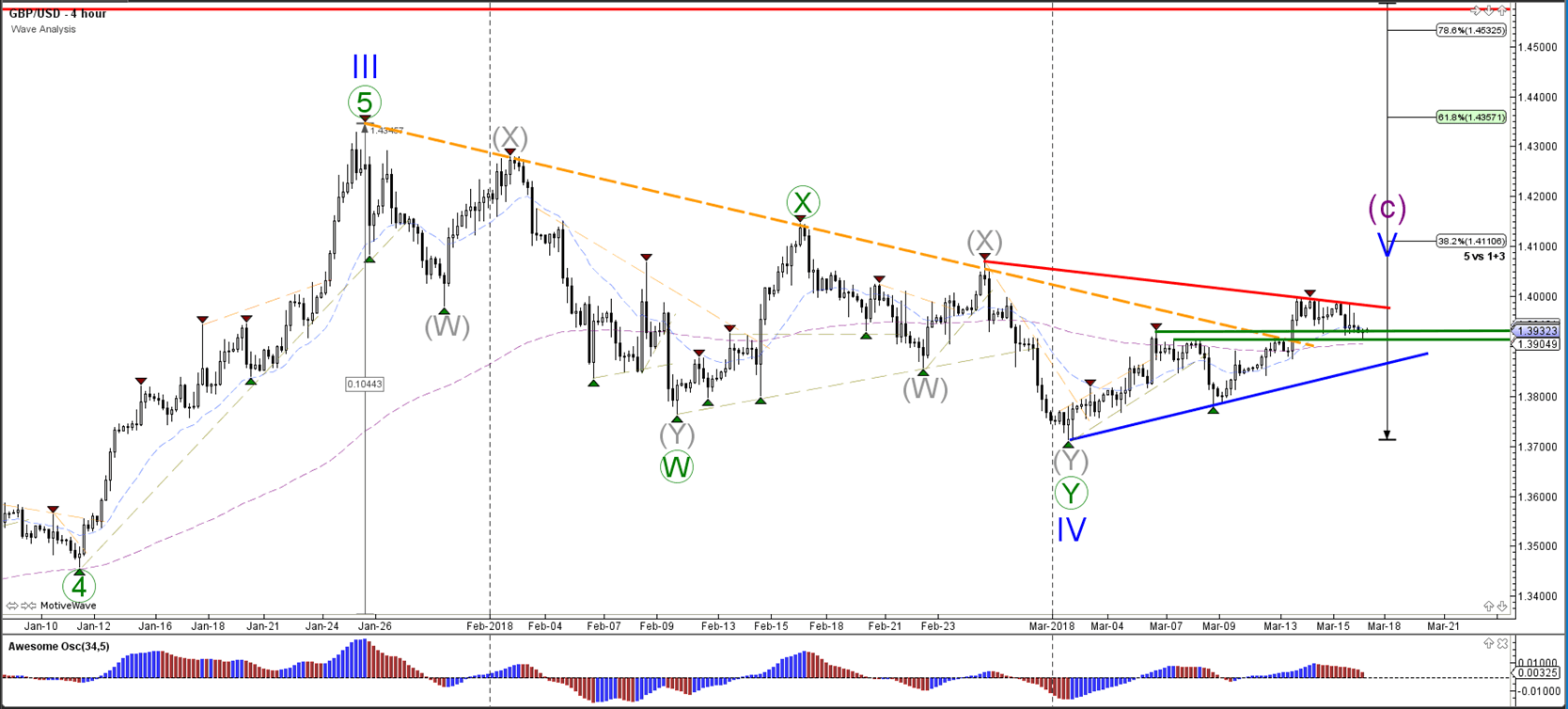

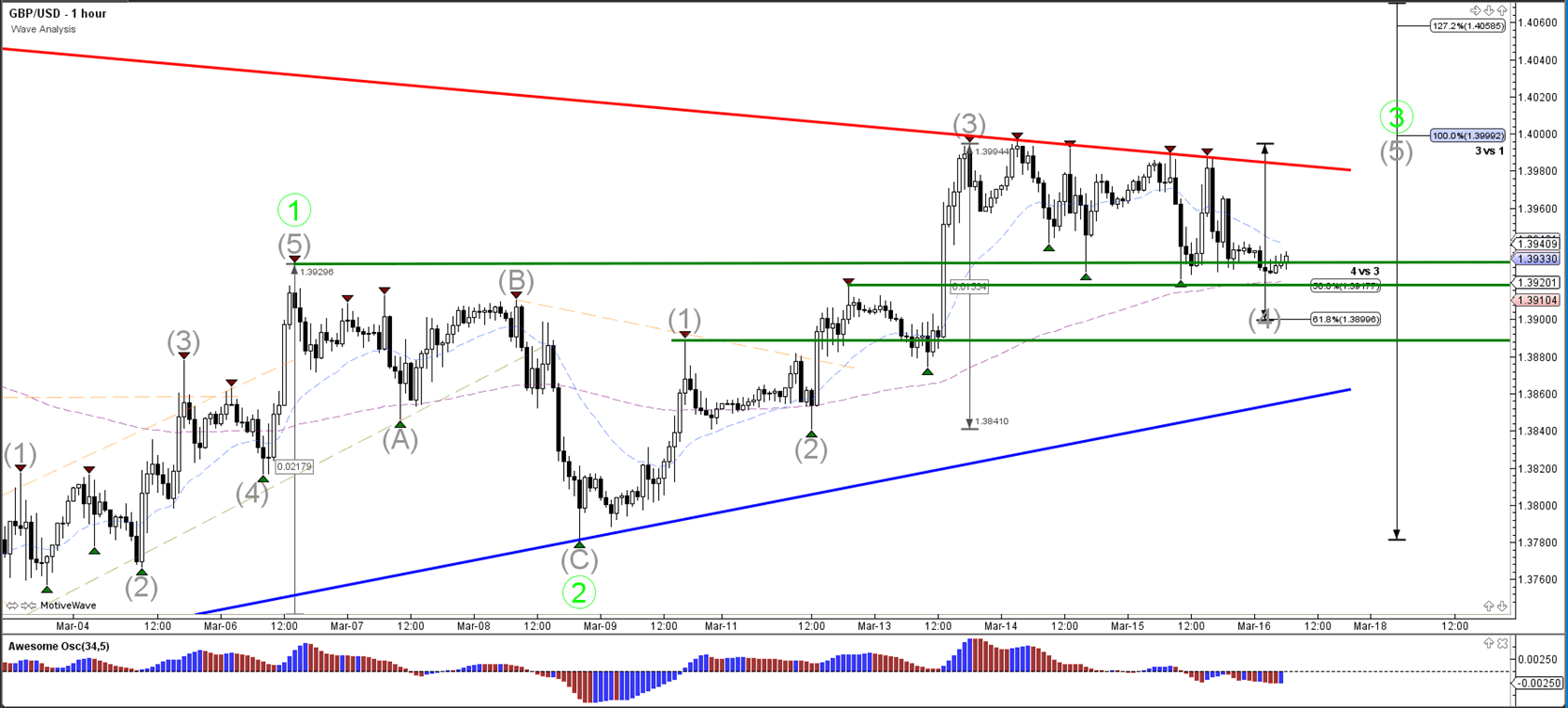

Currency pair GBP/USD

The GBP/USD bullish breakout above the long-term resistance trend line (dotted red) is slowing down substantially and building a sideways correction. Price is now testing a key support zone.

The GBP/USD is building many ups and downs which could be explained by a potential choppy wave 4 (orange) pattern. A bullish breakout could confirm the continuation of the wave 3 (green).

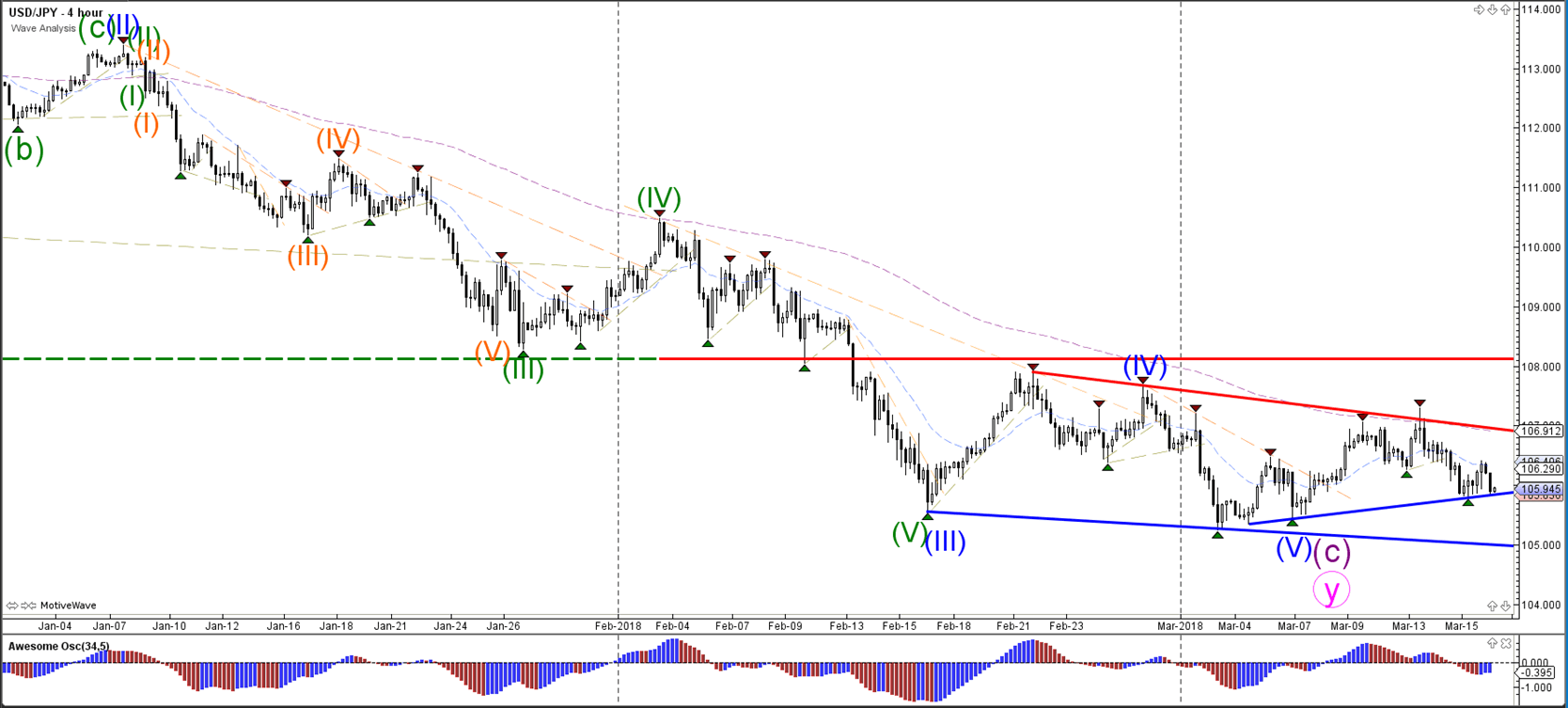

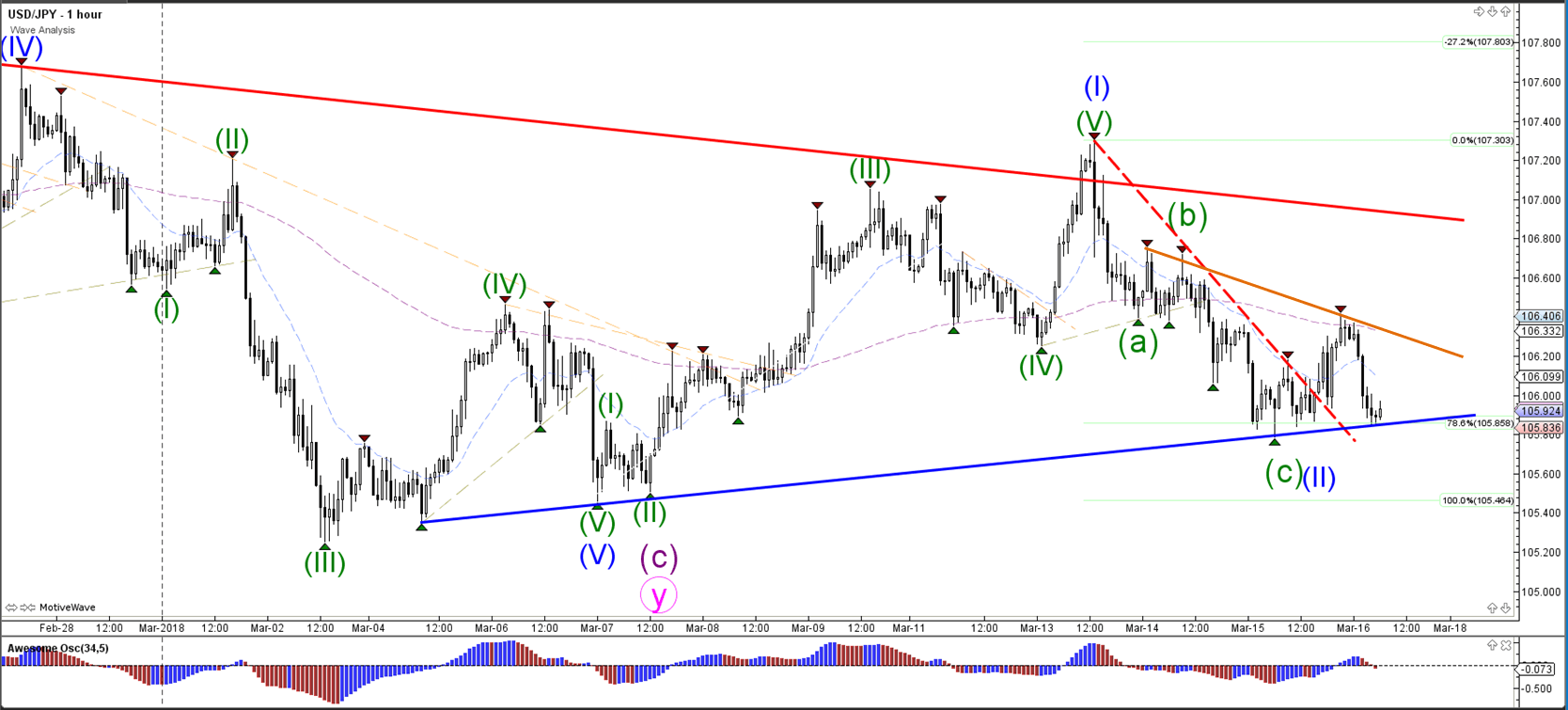

Currency pair USD/JPY

The USD/JPY is building a lengthy consolidation zone. The price action between the support (blue) and resistance (red) trend lines is showing indecision and requires a breakout before a new trend can emerge.

The USD/JPY needs to break the trend lines before the next direction becomes clear.

Asian Market Update: Asian Equity Markets Trade Mixed

Headlines/Economic Data

General Trend:

In weekly period, US-based Japan equity funds had $500M in outflows (largest outflow since July), says Lipper; Uncertainty related to government’s Moritomo scandal lingers

AUD/JPY tracks declines in Japanese equities

BoJ Gov Kuroda may become longest serving Governor in history of BoJ, according to Japanese press

PBoC conducts second 1-year medium-term lending facility in March as quarter end approaches; skips daily open market operation (OMO)

Singapore Feb Non-oil exports sees largest y/y decline in almost 1.5 years; Exports to China -23.6% y/y

Next week’s US Fed meeting and rate projections in focus (Tuesday March 20 to Wednesday 21st)

G20 Meeting due to be held In Argentina on Monday-Tuesday (March 19-20th)

Australia/New Zealand

ASX 200 opened +0.4%; closed: +0.5%

ASX 200 Telecom Index +1%, Utilities +0.9%, REIT +0.9%, Resources +0.8%, Consumer Discretionary +0.7%; Financials -0.5%

Wesfarmers [WES.AU]: Gains over 5% after announcing planned spin-off of supermarket chain

(AU) RBA Assist Gov Debelle: Expects to see repricing of assets if rates continue to rise'; No initial comments on monetary policy

(AU) Australia sells A$500M v A$500M indicated in 2.75% Nov 2028 bonds, avg yield 2.7124% v 2.9052% prior, bid to cover: 4.50x v 4.50x prior

(NZ) New Zealand Feb Non-Resident Bond Holdings: 59.7% v 60.0% prior

(NZ) New Zealand Feb Business Manufacturing PMI: 53.4 v 54.4 prior

China/Hong Kong

Hang Seng opened -0.6%, Shanghai flat

Hang Seng Materials Index -1.2%, Energy -1.1%, Financials -0.3%; Utilities +0.7%

China Unicom [0762.HK] rises over 1% after reporting FY17 results

(CN) PBOC CONDUCTS 1-YEAR CNY327B MEDIUM TERM LENDING FACILITY (MLF) AT UNCHANGED INTEREST RATE OF 3.25%

(CN) China PBoC Open Market Operation (OMO): Skips OMO v CNY40B injected prior in 7 and 28-day reverse repos: Net injection: v CNY40B injection prior; For the week, the PBoC injected a net of CNY377.5B

(CN) PBOC sets yuan reference rate at 6.3340 v 6.3141 prior

(CN) China sells 30-year bonds: avg yield 4.22% v 4.26%e; bid to cover 2.56x

(HK) Hong Fin Sec Chan: Considering tax on vacant homes

(CN) China PBoC Q1 Survey: Entrepreneurs Confidence Index: 74.3% v 71.8% q/q

(CN) US Chamber of Commerce spokesperson: urges Trump administration to not impose tariffs against China; will hurt Americans and could lead to trade war

Alibaba [BABA]: Reportedly said to explore plan to list shares in China - press

Japan

Nikkei 225 opened +0.3%; closed -0.6%

TOPIX Electric Appliances Index -0.9%; Securities +0.3%

(JP) Japan Lower and Upper Houses of Diet approve BoJ Gov Kuroda to additional 5-year term; also approve Amamiya and Wakatabe as Dep Governors

(JP) Japan Jan Final Industrial Production M/M: -6.8% v -6.6% prelim; Y/Y: 2.5% v 2.7% prelim

Korea

Kospi opened +0.1%

(CN) China President Xi could send delegation to North Korea in late March - South Korean Press [**Reminder: North and South Korea are expected to hold their 3rd summit in late April at the border]

(KR) South Korea and US said to plan to announce military drill plans next week - South Korea Press

North America

US equity markets ended mixed, S&P 500 declined for 4th straight session (longest losing streak of 2018): Dow +0.5%, S&P500 -0.1%, Nasdaq -0.2%, Russell 2000 -0.5%

S&P500 Materials -1.3%

(US) Special Counsel Mueller subpoenas Trump Organization demanding documents about Russia - NYT

(US) JAN TOTAL NET TIC FLOWS: +$119.7B V -$122.5B PRIOR; NET LONG-TERM TIC FLOWS: $62.1B V $23.3B PRIOR; China Total holding of US Treasuries: $1.17T v $1.18T prior (six month low)

Monsanto [MON]: Bayer reportedly hits US regulatory hurdles on Monsanto antitrust approval; US regulators reportedly still have concerns that the merger would harm competition and are not satisfied with the proposed asset sales - press

Qualcomm [QCOM]: Rises over 4% in the afterhours. Former Qualcomm Chairman Jacobs said to seek funding for buyout of the company, says the FT

Europe

(UK) UK and EU officials agree to take part in 'intensive talks' to resolve Irish border issue - press

(EU) EU said to see 'little chances' for WTO suit versus steel tariffs announced by the US - German Press

NEX Group [NXG.UK]: Confirms deal talks with CME are at an early stage and there can be no certainty that an offer for NEX will be made

Levels as of 01:00ET

Hang Seng flat; Shanghai Composite flat; Kospi -0.2%

Equity Futures: S&P500 flat; Nasdaq100 flat, Dax -0.1%; FTSE100 flat

EUR 1.2295-1.2314 ; JPY 105.83-106.39; AUD 0.7770-0.7804 ;NZD 0.7241-0.7282

Feb Gold -0.1% at $1,316/oz; Feb Crude Oil flat at $61.17/brl; Mar Copper -0.1% at $3.122/lb

The Wage Growth Figure For Q4 17 Is Due For Release

Market movers today

In the US, industrial production data for February is due out. PMIs for February indicate that US manufacturing expansion continues. Still, numbers concerning industrial production are usually quite volatile on a monthly basis.

In the euro area, the wage growth figure for Q4 17 is due for release. Wage growth pressure is key to pushing core inflation upwards and thus key for the ECB's monetary policy decisions. Although we have seen gradually rising wage pressures since H2 16, we expect wage growth to remain around its current level in the short term. Note that revised HICP figures for February are also due for release today but we do not expect any major revision.

No market movers are due to be released in the Scandi region today.

Selected market news

Market focus remains on political uncertainty as US-Russia issues were thrown on to the agenda yesterday. Equities generally drifted lower in both the US and Asian sessions, Treasury yields edged a few basis points higher in the short end of the US curve and the US dollar generally strengthened.

Notably, tensions between Russia and a range of NATO countries flared up yesterday after Germany, France and the US called upon the Kremlin to explain its role in the recent UK spy poisoning attack. Further, the US separately went on to sanction a range of Russian individuals and groups for election meddling and cyberattacks. Also, adding to the sense of continued political uncertainty is that US president Donald Trump supposedly plans to sack his national security advisor Herbert McMaster. Finally, US special counsel Robert S. Mueller has reportedly subpoenaed the Trump Organization for documents with ties to the case of Russia meddling in relation to the 2016 election.

US TICS data for January released last night shows that Chinese holdings of US Treasuries fell in the first month of the year ; this takes the exposure down from a local peak in mid-2017. Albeit overall not a significant fall from the 2013 highs, it still hints at changing dynamics, partly as CNY now leads a life 'somewhat separate' from the USD. However, it is also a cue to current China-US tensions. Indeed, this comes after reports in mid-January that China may scale down its Treasury exposure as a form of retaliation to Trump's protectionist rhetoric, which has in the interim been followed up by concrete measures such as tariffs and the ongoing inquiry into China's theft of US intellectual property rights. Watch out for Chinese trade retaliation measures against the US (see more in Research - 10 areas where China could retaliate vs US measures , 15 March.