Sample Category Title

U.S. Chamber of Commerce: USD 60b tariffs on Chinese goods is devastating to American families

U.S. Chamber of Commerce President and CEO Thomas Donohue criticized that unilateral tarrifs on Chinese goods by Trump's government would be destructive to the economy. He warned that the USD 30b a year tariffs on Chinese good would w"ipe out over a third of the savings American families received from the doubling of the standard deduction in tax reform." Further, with Trump's request of USD 60b a year tariff, "the impact would be even more devastating."In addition, Donohue said "tariffs could lead to a destructive trade war with serious consequences for U.S. economic growth and job creation,"

UK-EU planning instensive talk on Irish border, after completing the transition deal

UK Brexit Secretary David Davis is targeting to complete the legal text of the transition deal at the two-day summit from March 22. Most of the differences would likely be bridged on the following days. But the criteria of avoiding a hard Irish border remains a key showstopper. EU proposed a fall back option in its own draft published earlier this month. That is, should there be no compromisable solution, Norther Ireland would stay in the customs union along side Republic of Ireland. But UK Prime Minister Theresa May has instantly and bluntly rejected that idea. Intensive talk is now planned between March 26 and April 18 on the issue. There is some optimism on completing the transition agreement among UK officials. But businesses in UK would definite request a deal with full clarity. Any conditions in the deal attached to the outcome of Irish border issue would dissatisfy UK businesses and markets.

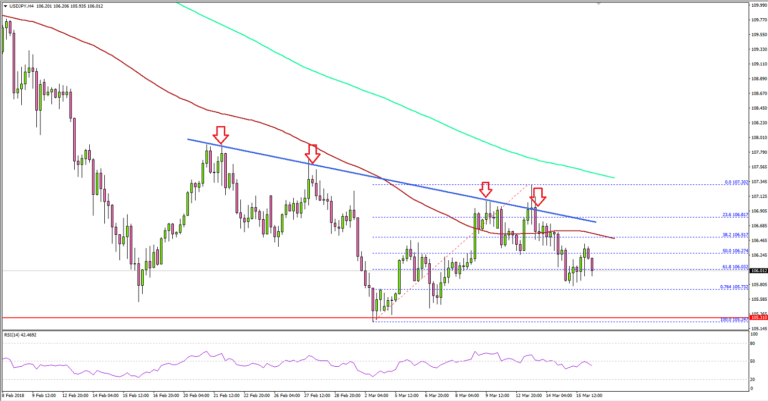

USD/JPY Remains In Bearish Trend Below 107.00

Key Highlights

- The US Dollar failed to move higher above 107.00 and declined against the Japanese Yen.

- There is a crucial bearish trend line forming with current resistance at 106.80 on the 4-hours chart of USD/JPY.

- The US initial jobless claims for the week ending March 10, 2018 declined from the last revised reading of 230K to 226K.

- Today, the US Industrial Production figure for Feb 2018 will be released, which is forecasted to increase by 0.3% (MoM).

USDJPY Technical Analysis

The US Dollar struggle to move higher above 107.00 continues against the Japanese Yen. The USD/JPY pair is currently trading in a bearish zone with a key support at 105.30.

Looking at the 4-hours chart of USD/JPY, the pair failed to gain upside momentum above 107.00. There was a false break above 107.00 and the 100 simple moving average (red, 4-hour).

Buyers failed and the pair declined back below 107.00 and the 100 SMA. There was also a move below the 50% Fib retracement level of the last wave from the 105.24 low to 107.30 high.

It seems like the pair is under pressure and it may continue to struggle to move above 107.00. Moreover, there is a crucial bearish trend line forming with current resistance at 106.80 on the same chart.

A successful close above 107.00 could push the pair back in the bullish zone towards 108.50. On the downside, the last swing low of 105.30 is a major support. A push below 105.30 could expose a move towards 104.00.

Recently, the US initial jobless claims report for the week ending March 10, 2018 was released by the US Department of Labor. The market was looking for a decline to 226K, and the outcome was similar.

Moreover, the last reading was revised down from 231K to 230K. The report added that:

The 4-week moving average was 221,500, a decrease of 750 from the previous week’s revised average. The previous week’s average was revised down by 250 from 222,500 to 222,250.

However, the US Dollar failed to gain bids versus the Japanese Yen. On the other hand, there was a slight bearish pressure on EUR/USD and GBP/USD.

Economic Releases to Watch Today

- Euro Zone CPI for Feb 2018 (YoY) – Forecast +1.2%, versus +1.2% previous.

- Euro Zone CPI for Feb 2018 (MoM) – Forecast +0.2%, versus -0.9% previous.

- US Housing Starts for Feb 2018 (MoM) – Forecast 1.280M, versus 1.326M previous.

- US Building Permits for Feb 2018 (MoM) – Forecast 1.320M, versus 1.377M previous.

- US Industrial Production for Feb 2018 (MoM) – Forecast +0.3%, versus -0.1% previous.

RBA Debelle: Markets underpriced risks of global tightening

RBA Deputy Governor Guy Debelle:-

- "Equity prices embody a view of the future that robust growth can continue without generating a material increase in inflation."

- "There is little priced in for the risk that this may not turn out to be true."

- Market volatility in February, was just "a small example of what could happen following a larger and more sustained shift upwards in the rate structure."

- He admitted before wrong in predicting higher volatility before, but added "I think there is a higher probability of being proven correct this time."

February 25 imagery suggests North Korea testing nuclear reactors at Yongbyon

Defence & security intelligence analysts Jane's reported that North Korea likely had preliminary testing it's nuclear reactors at the Yongbyon research facility. That came weeks ahead of the planned meeting between North Korean Leader Kim Jong-un and South Korean President Moon Jae-in next month. There will also be a planned meeting between Kim and US President Donald Trump in May.

But it should be noted that the analysis was based on an imagery from February 25. Jane's noted:-

- Satellite imagery suggests that preliminary testing of North Korea's experimental light water reactor (ELWR) at Yongbyon may have begun.

- Signatures of testing in late February follow logically from numerous indicators of increased activity at the ELWR that were visible throughout 2017, although reactor criticality is only likely to occur later in 2018 or in 2019.

- The ELWR was built and optimized for electricity production, but has 'dual-use' potential and can be modified to produce fissile material for nuclear weapons.

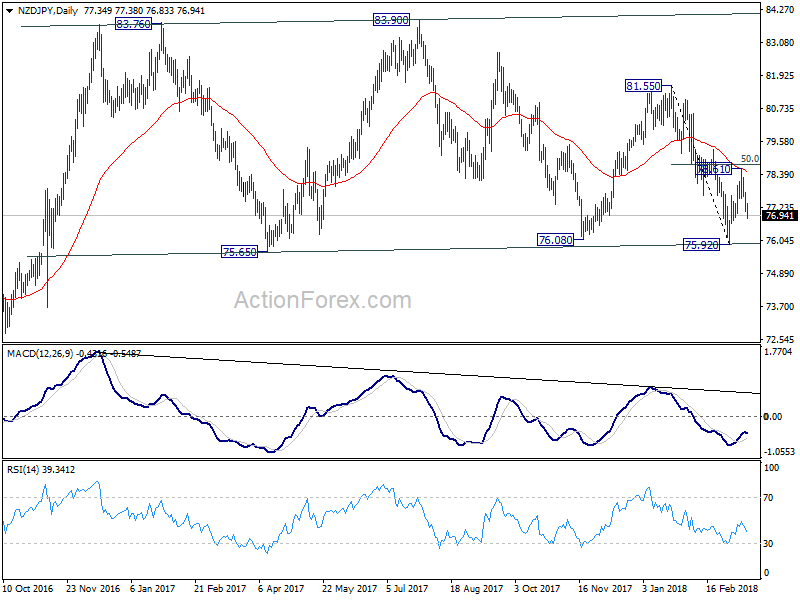

BusinessNZ manufacturing PMI dropped to 53.4, NZD/JPY extending dive

New Zealand Business NZ manufacturing PMI dropped to 53.4 in February, down from 54.4.

Sub-indices:-

- Production up 0.4 to 53.9

- Employment up 3.3 to 54.8

- New orders up 5.1 to 54.8

- Deliveries up 2.9 to 52.7

- Finished stocks down -1 to 51.1

Comments from Bank of New Zealand economist Doug Steel:-

- "The generally slower PMI suggests we shouldn't expect Q1 manufacturing GDP to be much different from the flat result recorded in yesterday's official figures for Q4,"

- "Early livestock culling on account of adverse weather seemed to boost Q4 manufacturing activity but will have the opposite effect through early 2018 given New Year rains."

- "It all suggests primary processing will be a drag on manufacturing activity early in 2018,"

Comments from Business NZ manufacturing executive director Catherine Beard:-

- Pace of expansion had levelled off in recent months

- "noted the sluggish start to the year with a dip in new orders being a common message."

Sharp fall in NZD/JPY this week suggests that rebound from 75.92 has completed at 78.61. The cross was held by 55 day EMA slightly below 50% retracement of 81.55 to 75.92. For the near term, it's going to revisit key support level around 75.65/75.92. It remains to be seen if there is enough selling to push through this key support zone. But outlook is not looking good.

King For A Day

King for a day

The dollar turned king overnight in a market lacking conviction across most asset classes got swept up by a wave of position adjustments as investors turn incredibly indecisive heading into next weeks FOMC. Indeed it’s shaping up to be arguably one of the most critical Centeral Bank policy events in some time as Jay Powell gets set to dictate the course of Fed policy for the remainder of 2018 and beyond. Given the enormity of the risk event, traders are getting remarkably anxious awaiting hints on forwarding guidance, so we should expect interest rate uncertainty to intensify as we near the event horizon.

But the pace of the dollar short covering was heightened by US economic data which showed the number of Americans applying for unemployment benefits fell while import prices rose more than expected, the later buttressing inflation expectations.

And sure the Kudlow interview on CNBC has some market observers anointing him the new Market Oracle of Pennsylvania Avenue after his King Dollar sell Gold remarks; the fact is traders didn’t react to the news at all, and why would they? Indeed, on that narrative alone I wouldn’t rush out to buy tickets for the next USD dollar coronation, which is probably years away given that US investors are quickly running out of reason to be optimistic as the increase in vacuous rhetoric emanating from the Whitehouse continues to dent market sentiment.

Bond Markets

US yields have backed up overnight supporting the USD, but without “risk on” supporting global equity market it has left both commodity bloc and EM Asia currencies prone

Equity Markets

The recent flow of headlines, especially those centring on trade are creating an air of uncertainty, and when it comes to investor sentiment, uncertainty fuels anxiety which causes investors ” Fear Guage “to ratchet higher. Whether its an escalation of a trade war or leeriness after news that US Special Counsel Mueller subpoenaed more documents from the Trump organisation, there’s always some prattle coming out of Washington these days that continues to cast a dark cloud over the markets.

Even in the face robust US economic data, US equity market could not hold onto gains as investors fears about the US administration trade policy trumps all else. This despite thinly veiled efforts to temper markets when Peter Navarro, Director of the White House National Trade Council, suggested the US could put tariffs on foreign goods without sparking a global trade war. Of course, he didn’t quite explain how that was achievable.

Oil Markets

There is no escaping the Oil market yo-yo as sings of growing oil demand are offsetting the bearish overtones from Shale oil output, at least for today. The International Energy Agency( IEA) in the heavily subscribed monthly report suggested global oil demand should grow by 1.5 million barrels a day, to average 99.3 million barrels a day in 2018. The estimate was an upward revision of 90,000 barrels a day compared with last month’s report.

The market positioning remains incredibly frangible to the continually shifting supply and demand narrative as the latest IEA headline implies market rebalancing is working. However topside price action remained well in check given the burgeoning Shale oil output projections for 2018 and beyond.

Gold Markets

Gold prices plunged as the USD gained some swagger overnight as traders get incredibly anxious about the possibility of a 4th interest rate hike this year. When interest rate rhetoric rises, gold plummets although the rise of geopolitical tensions between the UK and Russia likely tempered the sell-off.

Traders remain incredibly indecisive about the course of Fed policy, and all assets markets are enduring position adjustments where the lack of investor participation could exaggerate price action. Trader’s are precisely in position reduction mode as opposed to risk-taking style.

Currency Markets

Currency markets remain in well-defined ranges as traders prepare for the pre FOMC position chop fest.

The Euro

The Euro continues to consolidate with the near term top side firmly in check ahead of the FOMC meeting on the back of overtly dovish Draghi and growing uncertainty over Fed forward guidance

Japanese Yen

The ever so slight moderation in negative risk sentiment has seen USDJPY try to follow the broader dollar sentiment higher. However, the Abe political scandal continues to haunt investors and the potential threat to Abenomics should curb top side momentum

The Australian Dollar

While the Aussie initially became a bit of a passenger with the stronger USD in the driver’s seat, however, the Aussie is getting hammered mercilessly as trade war rhetoric with China is likely to escalate. Given Australia precarious position in the China supply chain, the potential escalation of regional trade war is not sitting well with the G-10 trading community this morning who have set their sight’s on the toppling Aussie

Falling Iron ore and copper prices aren’t helping sentiment either.

The Malaysian Ringgit

The Ringgit was underperforming this week due to quarter end repatriation flows, but now the USDMYR is caught up in the broader USD dollar strength and rising US bond yields. But with risk sentiment waning regional equity market will struggle, and the threat of additional regional outflows as trade war rhetoric increases could dent all regional currency sentiment dragging the MYR lower by proximity.

Eco Data 3/16/18

[php_everywhere instance="1"]

USD/CAD – How Significant is a Break Above 1.30?

Is Bullish Momentum Gathering?

USDCAD has been climbing quite aggressively over the last couple of months, rising around 6.5% since the end of January and hitting levels last seen in June.

After running into resistance around 1.30 last week – a notable psychological level and important support late 2016 and early 2017 – the pair fell back to 1.28 where it found support from a combination of the 38.2% fib level and the 233-day simple moving average.

A shallow correction like this could be a sign of a very bullish market and with the pair having recently breached the 200 and 233-day SMAs, it joins a growing list of bullish indicators.

Should the pair hold onto today’s gains and close above 1.30, the next key technical levels above will be around 1.32, with it having found support around here last time it traded above between March and June last year. It’s worth noting though that 1.32 is not a precise level, the pair found support during these months roughly between 1.3165 and 1.3265.

One interesting thing about the recent rally has been the momentum indicators which aren’t fully supportive of price action. The MACD moving averages are making new highs, while the MACD histogram is making lower highs and the Stochastic is relatively neutral. This in itself isn’t really a bearish signal but it will be very interesting to see how these look should we reach the 1.32 zone.

Gold Dips as Jobless Claims Drop, Markets Eye Consumer Confidence

Gold has posted considerable losses in the Thursday session. In North American trade, the spot price for an ounce of gold is $1317.95, down 0.54% on the day. On the release front, unemployment claims dropped to 226 thousand, just below the estimate of 226 thousand. Manufacturing reports were mixed. The Philly Fed Manufacturing Index dropped to 22.3, missing the forecast of 23.1 points. There was better news from the Empire State Manufacturing Index, which jumped to 22.5, crushing the estimate of 14.9 points. On Friday, the US releases two key construction reports and Preliminary UoM Consumer Sentiment.

After an uneventful week, gold prices have dropped on Thursday, after a strong unemployment claims release. Still, there are expectations that gold could quickly recover, as the markets nervously follow the aftermath of a toxic attack in London in early March. Relations between the UK and Russia have nosedived after a toxic attack in London aimed against a former Russian intelligence officer was poisoned, and the UK has laid the blame on the Kremlin. The May government has ordered the expulsion of 23 Russian diplomats, and Russia is sure to retaliate. As well, President Trump has slapped tariffs on steel, and this could trigger a response from the EU and China. These hotspots have dampened risk appetite on the part of investors, and if these crises continue, safe-haven gold could be a big winner.

The Federal Reserve is widely expected to raise interest rates next week. According to the CME Group, the odds of a quarter-point raise stand at 89 percent. What can we expect from the Fed during the year? The pressing question is how many rate hikes will we see in 2018. The current Fed projection remains at three hikes, but the superb nonfarm payrolls report last week has raised speculation that the Fed could accelerate the pace to four hikes, which would be good news for the US dollar. Investors will be keeping a close eye on key US data, especially inflation indicators. If these numbers improve, we're likely to see four rate hikes in 2018.