Sample Category Title

USD/JPY – Dollar Drops Below 106, US Jobless Claims Steady

The Japanese yen continues to post gains. In North American trade, USD/JPY is trading at 105.96, down 0.34% on the day. In the US, unemployment claims dropped to 226 thousand, just below the estimate of 226 thousand. Manufacturing reports were mixed. The Philly Fed Manufacturing Index dropped to 22.3, missing the forecast of 23.1 points. There was better news from the Empire State Manufacturing Index, which jumped to 22.5, crushing the estimate of 14.9 points. This marked a 5-month high. Japan will release Revised Industrial Production, with the markets braced for a sharp decline of 6.6%. On Friday, the US releases three key events – Building Permits, Housing Starts and Preliminary UoM Consumer Sentiment.

With the Japanese economy continuing to show improvement, investors are carefully following the Bank of Japan, looking for hints regarding any change in monetary policy. Earlier in the week, the BoJ released the minutes of its January policy meeting, but the markets were more interested in what Bank of Japan Governor Haruhiko Kuroda had to say. The minutes indicated that some policymakers expressed concern about the drawbacks of the Bank’s massive monetary stimulus program, such as hurting the profits of financial institutions. However, most members were of the view that the Bank should continue its radical easing stance. Speaking after the release of the minutes, Kuroda said he was confident that the BoJ would exit its ultra accommodative monetary policy, but qualified his remarks by adding that it was too early to get into specifics, given that inflation remained well below the Bank’s target. Kuroda is playing his cards very cautiously, using the E- word (exit), while at the same time saying that it is much to early to discuss any change in policy until inflation moves closer to the target of around 2 percent.

The Federal Reserve is widely expected to raise interest rates next week, which would mark the first hike of 2018. According to the CME Group, the odds of a quarter-point raise stand at 89 percent. What can we expect from the Fed during the year? The pressing question is how many rate hikes will we see in 2018. The current Fed projection remains at three hikes, but the superb nonfarm payrolls report last week has raised speculation that the Fed could accelerate the pace to four hikes, which would be good news for the US dollar. Investors will be keeping a close eye on key US data, especially inflation indicators. If these numbers improve, we’re likely to see four rate hikes in 2018.

Yen Holds Strong amid Trade Concerns; European Stocks Open Higher

Here are the latest developments in global markets:

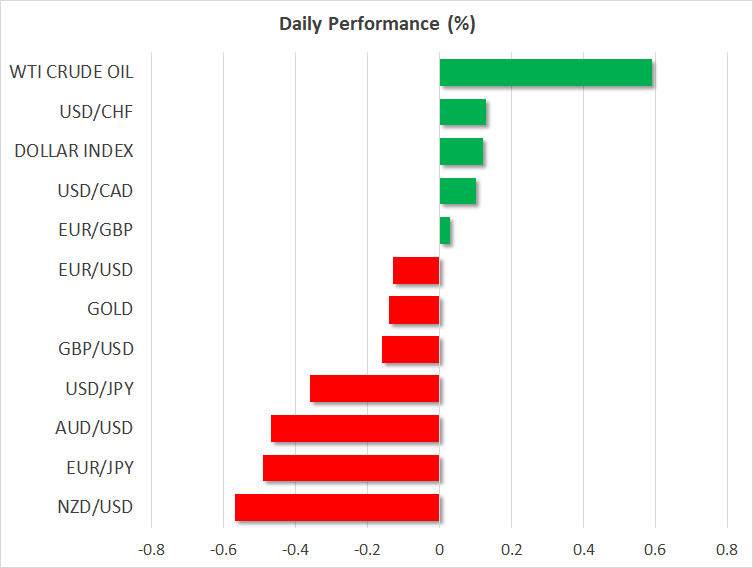

FOREX: Dollar/yen hovered near one-week lows, last trading at 105.90 (-0.35%) as investors continued to look for safer assets amid worries that the incoming US economic adviser, Larry Kudlow, who previously criticized US-China trade relations could back Trump’s plans to impose further import tariffs to China. This comes ahead of a crucial G20 meeting next week where world leaders are expected to denounce unfair trade practices. Pound/dollar extended losses towards 1.3928 (-0.14%) as the UK Brexit Minister, David Davis, said he would accept EU’s offer of a 21 months transition period rather than two years. Note that Brexit negotiating teams will meet during the weekend, with markets being optimistic that a deal on the transition period will likely happen. Euro/dollar inched down to 1.2352 (-0.12%), weighed by concerns on the future of the US-EU trade partnership although today’s remarks by officials out of the bloc were supporting that a tit-for-tat retaliation is not the answer to US protectionism, including the German Chancellor. Meanwhile in Norway, the Norges Bank kept interest rates steady but announced unexpectedly that a rate hike would probably come “after summer”, somewhat earlier than previously thought. Dollar/Krone dived to 7.6862 (-0.66%) and euro/krone retreated to 9.49 (-0.62%). The Swiss National Bank, also left interest rates unchanged today, reporting that it will maintain an accommodative monetary policy and remain active in foreign exchange markets given the appreciation of the local currency in the face of a weaker dollar. Dollar/swissie inched up to 0.9462 (+0.13%) following the decision.

STOCKS: Positive corporate results continued to support European stocks on Thursday, despite worries about Trump’s trade policy implications. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.17% and 0.30% respectively, with the majority of the sectors being in the green. The German DAX 30 climbed by 0.22%, with the German carmaker Volkswagen and the largest world reinsurer Munich Re being the best performers. The former saw significant gains during the week due to its plans to broaden production to electric cars, while the latter saw its shares jumping by 2.0% after it upgraded its 2018 profit forecasts. On the other hand, the shares of the French Bank Societe Generale tumbled by 3.0% after the unexpected resignation of the deputy CEO. Still, gains in healthcare and industrials were enough to send the French CAC 40 higher by 0.28%. The UK’s FTSE 100 managed to rise by 0.17% despite sharp losses in technology sectors, while the US stock futures were mixed.

COMMODITIES: Oil prices headed higher after the Energy International Administration said that global demand is expected to rise this year, but oil supply is increasing at a faster pace, reporting that inventories could pick up in the first half of 2018. WTI crude and Brent were last seen at $61.32 (+0.59%) and $65.19 (+0.46%) per barrel correspondingly. In precious metals, gold extended declines towards $1322.66 (-0.13%) per ounce.

Day ahead: US initial jobless claims & business indices attract attention

Day ahead: US initial jobless claims & business indices attract attention

The US will release another bunch of economic data today, though, positions on the dollar might be on the defensive as investors continue to price risks stemming from Trump’s protectionist appetite which could drive global trade on edge.

At 1230 GMT, the New York Fed will publish readings on manufacturing conditions in the New York state, with the index expected to improve in March after four months of falling. The Philadelphia Fed will also report on regional business conditions at the same time, however, in this case, projections are for the business index to weaken.

US initial jobless claims for the week ending March 9 and March import prices will be published along with the above data as well. A few hours later at 1400 GMT, the National Association of House Builders will issue its Housing Market Index which tracks the relative level of current and future single-family home sales. A print above 50 is considered a positive sign for the housing market.

Trump’s politics will remain in the center stage during the day after the resignation of the chief economic adviser, Gary Cohn, last week and the firing of the Secretary of State, Rex Tillerson on Tuesday which increased speculations that the president is serious about his punitive legislative plans. Early today news confirming Larry Kudlow to be the new economic adviser, pushed the dollar lower as the CNBC’s economic analyst is known for his tough stance against US-China trade relations. On the other hand, he has been critical of Trump’s tariff approach.

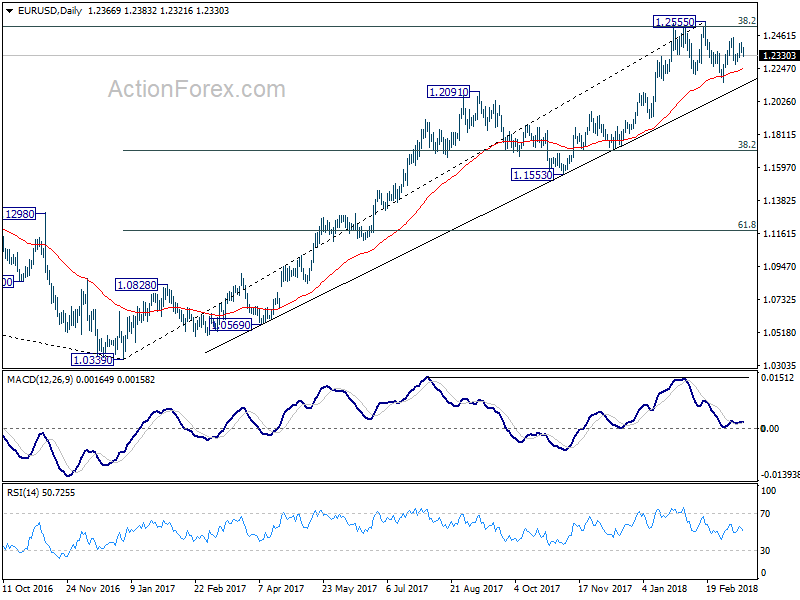

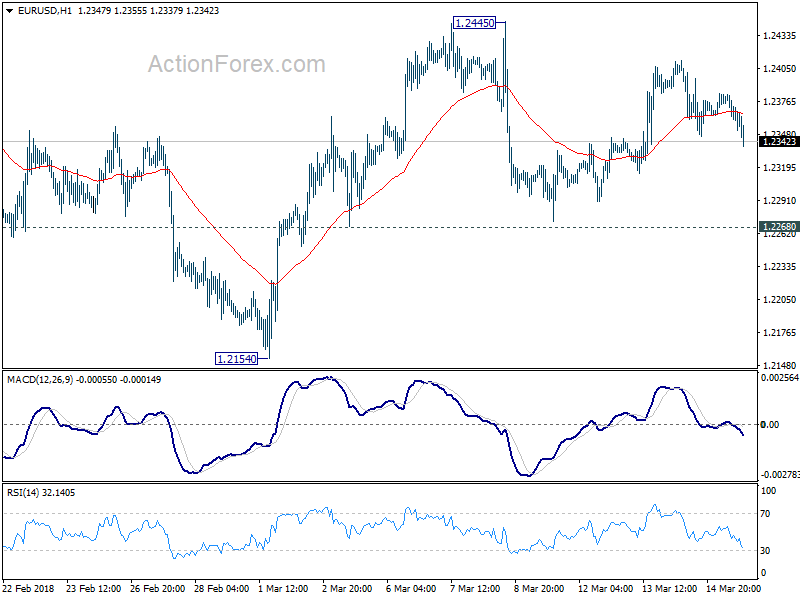

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2338; (P) 1.2375 (R1) 1.2404; More....

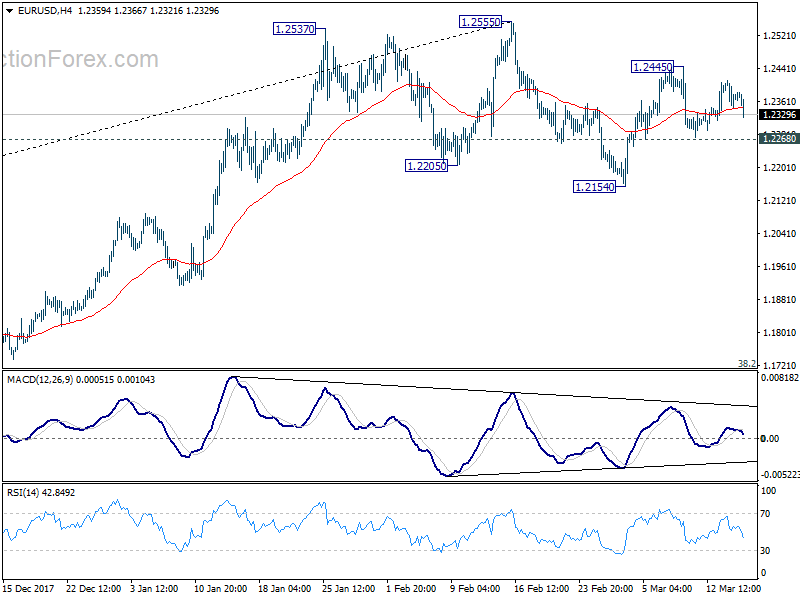

NO change in EUR/USD's outlook and intraday bias stays neutral despite the dip in early US session. On the upside, break of 1.2445 will target a test on 1.2555 high. Decisive break there will resume medium term rally and carry larger bullish implication. But again, break of 1.2268 will argue that fall from 1.2555 is resuming. And intraday bias will be turned back to the downside for 1.2154 support and below.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.01; (P) 106.37; (R1) 106.69; More...

USD/JPY is still bounded in range above 105.24 and intraday bias stays neutral for the moment. The consolidative trading from 105.24 is still in progress and could extend. But after all, near term outlook remains bearish with 107.67 resistance intact. And deeper decline is in favor. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, firm break of 107.67 resistance will indicate near term reversal, on bullish convergence condition in 4 hour MACD. In such case, outlook will be turned bullish for 110.47 resistance next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

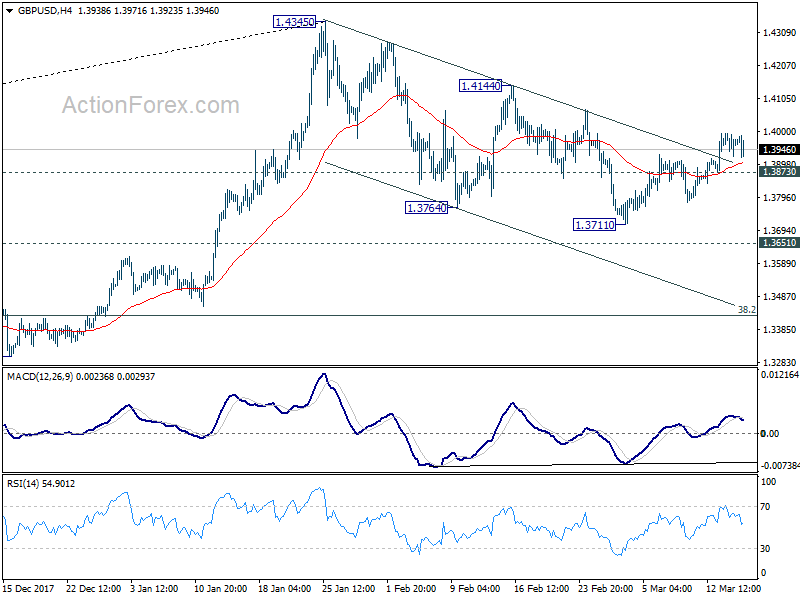

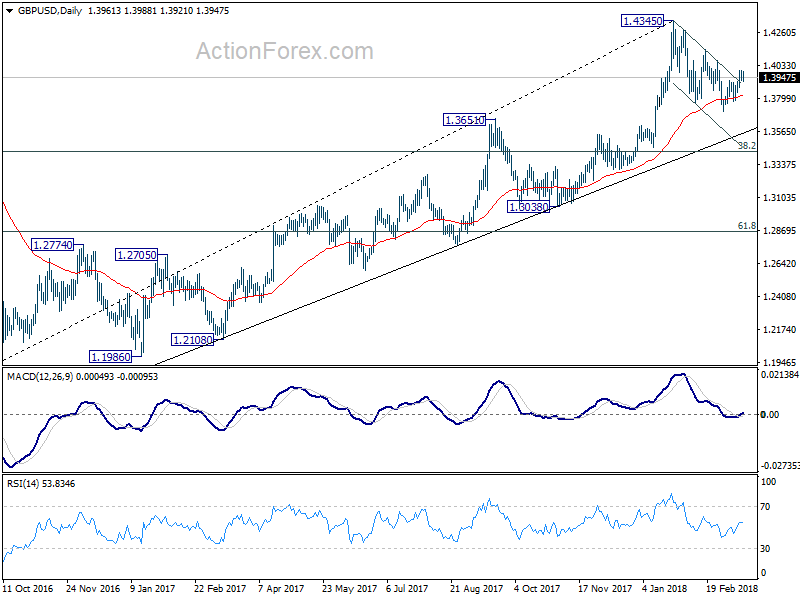

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3926; (P) 1.3961; (R1) 1.3996; More....

No change in GBP/USD's outlook. Even though upside momentum is diminishing as seen in 4 hour MACD, further rise is still in favor with 1.3873 minor support intact. Rebound from 1.3711 would extend to 1.4144 resistance. Break there will confirm completion of correction from 1.4345 and target retest of this high. On the downside, below 1.3873 minor support will turn bias to the downside to extend the corrective fall from 1.4345 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

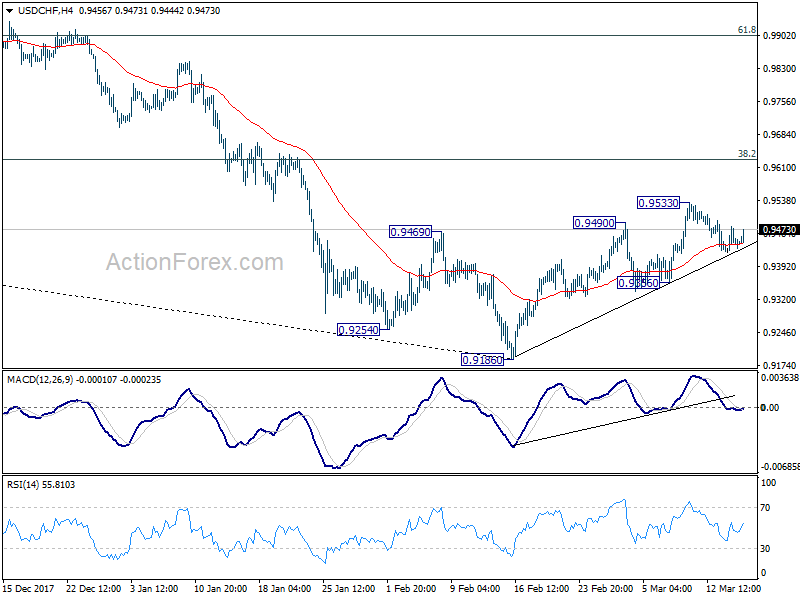

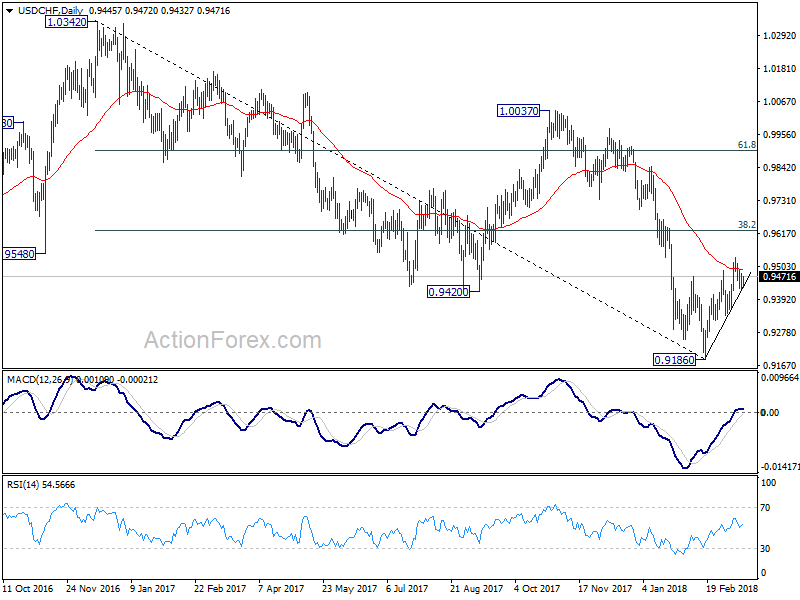

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9421; (P) 0.9451; (R1) 0.9477; More...

USD/CHF recovers mildly as it's trying to draw support from 4 hour 55 EMA. But it's limited well below 0.9533 temporary top so far. Intraday bias remains neutral. Again, further rise is in favor as long as 0.9356 support holds. Break of 0.9533 will resume the rebound from 0.9186 and target 0.9626 fibonacci level. However, on the downside, break of 0.9356 will indicate that the rebound has completed. In such case, intraday bias will be turned back to the downside for retesting 0.9186 low.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Dollar Mildly Higher after Solid Data but Upside Limited, Franc Shrugs off SNB

Dollar strengthens mildly in early US session after some solid economic data. But gain for the greenback is so far limited. While Dollar follow Yen as the second strongest major currency for today, it's still down again all but Aussie and Loonie for the week. US President Donald Trump confirmed the appointment of Larry Kudlow as top White House economic adviser, replacing Gary Cohn who left last week. But there is generally expected and priced in. The Swiss Franc also showed little reaction to the dovish rate announcement of SNB. Markets eyes are staying on how the theme of trade war develops.

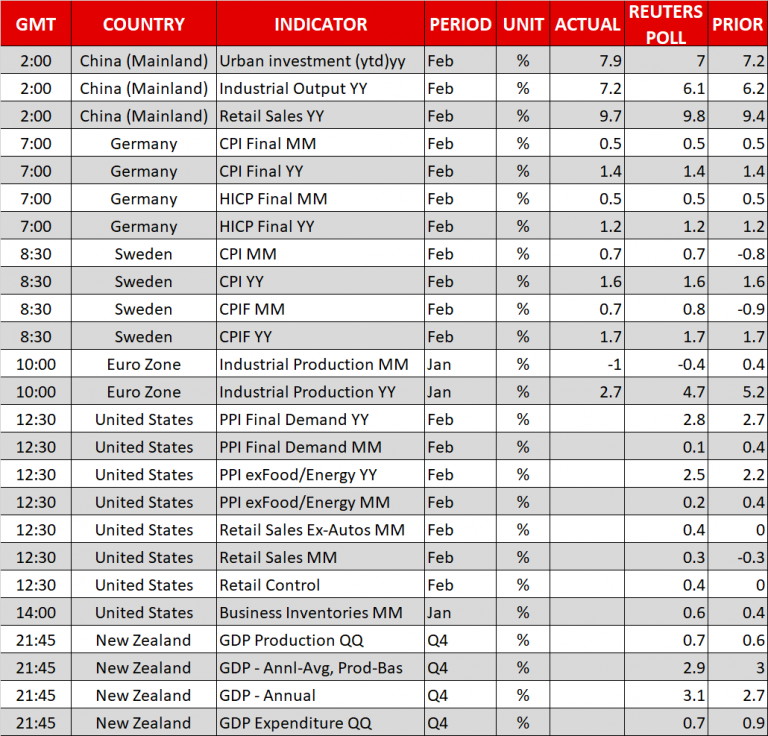

From US, initial jobless claims dropped -4k to 22k in the week ended March 9, in line with expectation. Continuing claims rose a mere 4k to 1.879m in the week ended March 2. Import price index rose 0.4% mom versus expectation of 0.2% mom. Empire state manufacturing index rose sharply to 22.5, up from 13.1, and beat expectation of 15.0. However, Philly Fed manufacturing survey dropped to 22.3, down from 25.8 and missed expectation of 23.0.

Dovish SNB left interest rates unchanged, downgraded inflation forecasts

SNB left sight deposit rates unchanged at -0.75%, three-month Libor range at -1.25% to -0.25%, as widely expected. Inflation forecasts for 2018 and 2019 are lowered due to Swiss Franc's appreciation to Dollar. SNB maintained that negative rate and intervention are essential . On the inflation outlook, SNB revised lower the forecast to 0.6% for this year, down from 0.7% projected in the previous quarter. It also revised lower the inflation forecast to 0.9% for 2019, down from 1.1% projected previously. The central bank introduced its inflation forecast for 2020 which is expected to reach 1.9%. On GDP growth, SNB attributed the country's 4Q17 growth, at 2.4% annualized, to strong manufacturing activities. It maintained the GDP growth forecast for 2018 at 2%

More in SNB Warned Of Franc Appreciation Against US Dollar, Kept Commitment To Intervene

SNB chairman Thomas Jordan warned of US protectionism in a radio interview today. He said "the risks have not materialized yet, but if international trade doesn't function well, that is damaging for everyone." And, "safe havens are sought when there are political uncertainties or big changes in the financial markets. This can be triggered by protectionism,"

Also released from Swiss, producer and import prices rose 0.3% mom, 2.3% yoy in February, above expectation of 0.4% mom, 0.9% yoy.

Macquarie pushed back expectation of RBA 2018 hike

More economists are paring back their expectation of an RBA hike this year. Macquarie Bank now no longer sees RBA hiking within 2018. it noted in a report that "the primary reason for pushing back our RBA call is that the Bank can err on the side of growing the economy faster for longer to erode spare capacity and have confidence that inflation is firmly moving back into the 2-3% target." .

It referred to other advanced economies for the pattern of falling unemployment rates without wage growth. At this same time, "Australia's unemployment rate remains at 5.5% and noticeably above 'full employment'." Also, "after two years of below-target inflation, and at least another one to come, there seems little danger of generating a meaningful pick-up in inflation expectations from keeping interest rates low for longer."

Besides, "housing has settled", and "investor activity in the housing market has subsided significantly and housing prices have broadly flattened out. There is "little danger" or "reacceleration in housing price or credit growth." And therefore, "the source of much angst for the RBA - fast growth in housing prices in Sydney and Melbourne - has eased."

NAB recently pushed back their RBA rate expectation too and predicted only one hike this year, not two. Westpac continued to expect no hike until 2019.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9421; (P) 0.9451; (R1) 0.9477; More...

USD/CHF recovers mildly as it's trying to draw support from 4 hour 55 EMA. But it's limited well below 0.9533 temporary top so far. Intraday bias remains neutral. Again, further rise is in favor as long as 0.9356 support holds. Break of 0.9533 will resume the rebound from 0.9186 and target 0.9626 fibonacci level. However, on the downside, break of 0.9356 will indicate that the rebound has completed. In such case, intraday bias will be turned back to the downside for retesting 0.9186 low.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q4 | 0.6% | 0.80% | 0.60% | |

| 00:00 | AUD | Consumer Inflation Expectation Mar | 3.7% | 3.60% | ||

| 08:15 | CHF | Producer & Import Prices M/M Feb | 0.3% | 0.20% | 0.30% | |

| 08:15 | CHF | Producer & Import Prices Y/Y Feb | 2.3% | 0.90% | 1.80% | |

| 08:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | -0.75% | |

| 08:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | -1.25% | |

| 08:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | -0.25% | |

| 12:30 | USD | Empire State Manufacturing Mar | 22.5 | 15 | 13.1 | |

| 12:30 | USD | Import Price Index M/M Feb | 0.4% | 0.30% | 1.00% | 0.80% |

| 12:30 | USD | Initial Jobless Claims (Mar 10) | 226K | 228K | 231K | 230k |

| 12:30 | USD | Philadelphia Fed Business Outlook Mar | 22.3 | 23 | 25.8 | |

| 14:00 | USD | NAHB Housing Market Index Mar | 72 | 72 | ||

| 14:30 | USD | Natural Gas Storage | -57B |

Dollar mildly higher after data. Jobless claims drop 4k to 226k

First batch of US data release:-

- Initial jobless claims Mar 9: 226k vs exp 226k vs prior 230k

- Continuing claims Mar 2: 1.88m vs exp 1.90m vs prior 1.88m

- Empire state manufacturing Mar: 22.5 vs exp 15.0 vs prior 13.1

- Philly Fed manufacturing Mar: 22.3 vs exp 23.0 vs prior 25.8

- Import price index Feb: 0.4% mom vs exp 0.2% mom vs prior 0.8% mom

Dollar strengthens mildly after the release.

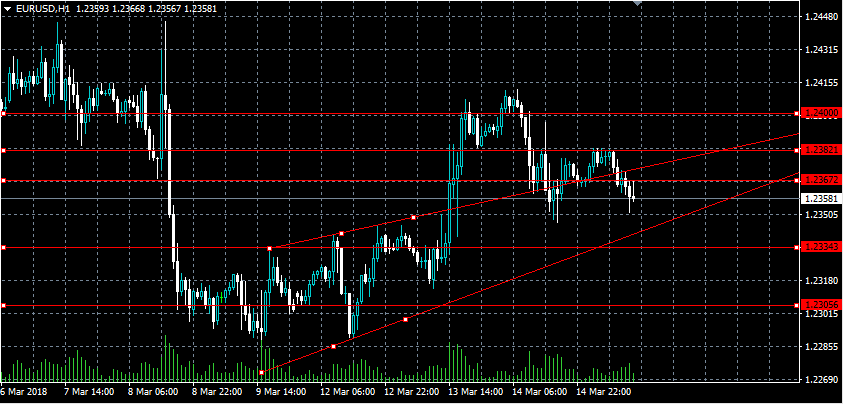

Euro Weakness Expected Below 1.2382 Level

The euro is turning lower in early Thursday trading against the U.S dollar, as buyers repeatedly failed to overcome the key 1.2382 resistance level. The EURUSD pair is currently trading around the 1.2360 region, with short-term RSI and Momentum indicators starting to turn lower. Fundamental factors are also weighing on the euro currency today, with the German finance minister earlier warning investors about the implications of the stronger euro and U.S trade tariffs.

The EURUSD pair is intraday bearish whilst trading below the 1.2382 level, further declines towards the 1.2334 and 1.2305 level remain possible.

Should the EURUSD pair move above the 1.2382 level for a sustained period, price-action will likely turn bullish and test towards the 1.2400 and 1.2400 levels.

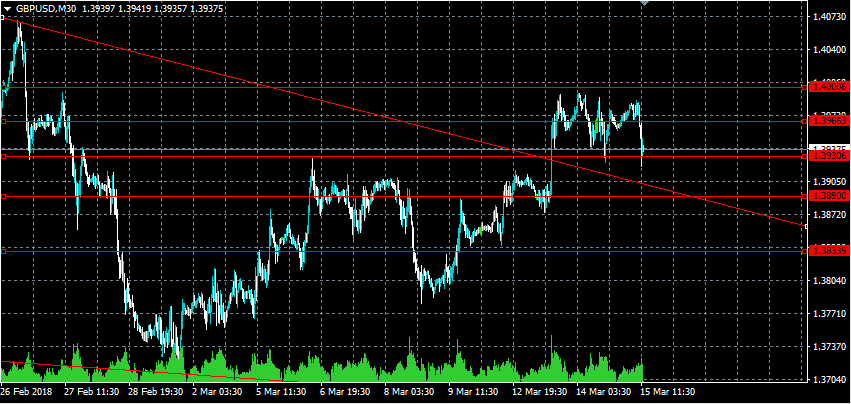

Russian Tensions Now Weighing On GBPUSD

The British pound has turned lower against the greenback during the European trading session, as ongoing tensions between the United Kingdom and Russian governments worsens. The GBPUSD pair has quickly weakened back towards the 1.3930 level after the Russian foreign minister said he will soon expel the United Kingdom’s diplomats from Russia. Intraday pound sentiment is now turning bearish on the news, with sellers pressing towards the key 1.3920 level, which represents the pairs monthly pivot point.

The GBPUSD pair is intraday bearish whilst trading below the 1.3920 level, key support is then found at the 1.3889 and 1.3833 levels.

Should the GBPUSD pair manage to hold price-action above the 1.3920 level, buyers may test towards the 1.3966 and 1.4000 levels.