Sample Category Title

Return Of The Jedi, Er, SNB

Return of the Jedi, er, SNB

'There is no simmering trade war,' 'international trade remained dynamic' – so spoke the Swiss National Bank today as it held monetary policy unchanged. Maybe this Jedi Mind Trick of saying something and so making it true will work, but we wonder. It overlooks risks that could strengthen the CHF and move Swiss inflation. The SNB is likely to continue guiding the market by highlighting conditions that support its objective. Or perhaps they are just seeing through the short-term hype.

The SNB still views the CHF as highly valued (despite EUR/CHF nearing 1.20) and reiterated its participation in foreign exchange markets as necessary. Speculation that the SNB would lead the European Central Bank on policy tightening continues to be off the mark: the inflation forecast shifted downwards for 2018 from 0.7% to 0.6%, hardly enough to move interest rates. The SNB expects economic growth of 2.4%, driven by manufacturing. Mortgage lending is down, but house prices are starting to rise, warning of a potential correction. Overall, the SNB is content with the current policy and in no rush to adjust. We suspect that the first hike will occur in 2019, a solid 6 month after the ECB’s.

Indian approaches price stability

As inflation slows and the Indian economy grows (7.10% in December 2017), we remain confident that market risk is being distanced. The Reserve Bank of India will therefore maintain its current interest rate at 6% at its next monetary policy meeting on 5 April. USD/INR is currently at 64.86 (+1.86% this year) and expected to remain in this range near term.

India is showing openness, holding recent talks with the Philippines President Rodrigo Duterte, Iranian Prime Minister Hassan Rouhani and French President Emmanuel Macron about topics such as industrial developments, security and education. February’s Wholesale Price Index came out yesterday at 2.48% annually, confirming our view of moderate expansion for Manufactured Goods, Primary Articles and Fuel & Power. The recently published February Consumer Price Index shows a similar pattern at 4.44% following January’s 5.07%. This supports moderate inflation, giving further relief to the Reserve Bank of India.

SNB Warned Of Franc Appreciation Against US Dollar, Kept Commitment To Intervene

As widely anticipated, the SNB kept the sight deposit rate unchanged at -0.75%, while the target range for the three-month Libor stayed at between –1.25% and –0.25%. Again, the SNB maintained the commitment to intervene the FX market when needed, reiterating that it would 'remain active in the foreign exchange market as necessary', while 'taking the overall currency situation into consideration'. Policymakers appeared more concerned about the value of Swiss franc, referring to franc’s strength against the greenback. On the economic outlook, the central bank downgraded inflation expectations while leaving the growth estimates unchanged.

On the reference to the exchange rate, SNB acknowledged that the franc has 'appreciated slightly overall on the back of the weaker US dollar' and remains 'highly valued'. Policymakers warned that the exchange rate condition remains 'fragile' and 'monetary conditions may change rapidly'. They reiterated that 'the negative interest rate' policy and SNB’s 'willingness to intervene in the foreign exchange market' would keep the 'attractiveness of Swiss franc investments low and eases pressure on the currency'.

On the inflation outlook, SNB revised lower the forecast to +0.6% for this year, down from +0.7% projected in the previous quarter. It also revised lower the inflation forecast to +0.9% for 2019, down from +1.1% projected previously. The central bank introduced its inflation forecast for 2020 which is expected to reach +1.9%. On GDP growth, SNB attributed the country’s 4Q17 growth, at +2.4% annualized, to strong manufacturing activities. It maintained the GDP growth forecast for 2018 at +2%

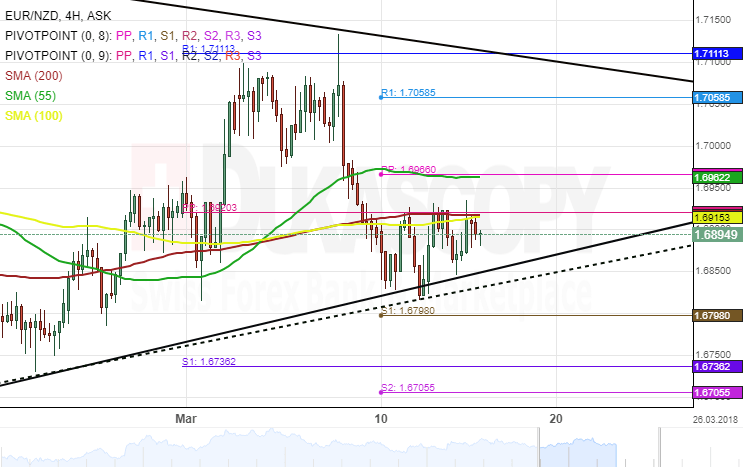

EUR/NZD 4H Chart: Trading Sideways

The common European currency has appreciated substantially against the New Zealand Dollar since February. This bullish movement has been constrained by a nine-month ascending channel. During the past few days, however, this bullish sentiment has not been so idiosyncratic, as the rate was trading sideways.

A strong resistance cluster set by the monthly pivot point with the combination of the 100– and 200– hour SMAs near 1.6914 was restricting the EUR/NZD pair from making any upwards moves.

Given that the currency exchange rate has moved closer to the lower boundary of a medium-scale triangle, a breakout is likely to occur during the following trading sessions.

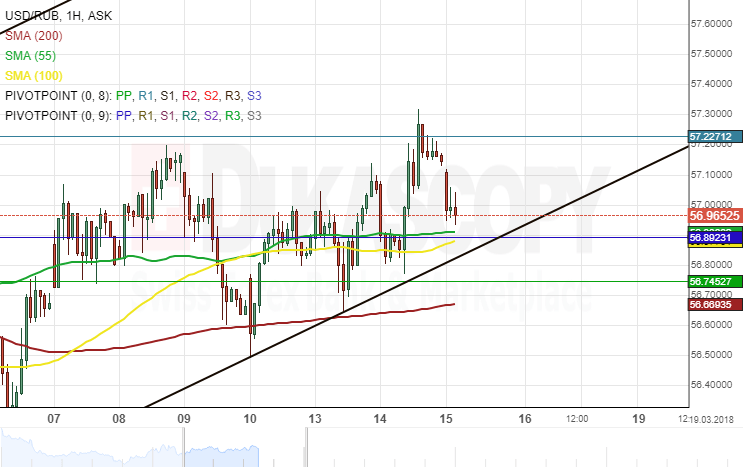

USD/RUB 1H Chart: Potential Surge

The US Dollar has been appreciating gradually against the Russian Ruble since late February. The currency pair bounced off the lower boundary of a junior channel on February 28 and has since remained stable and slowly moving north.

Technical indicators suggest that bulls should take a greater hand in the market once again and thus sending the US Dollar higher. In the meantime, the exchange has tested the weekly R1 and made a retracement south.

Everything being equal, the aforementioned scenario should occur if the combined support of the 55– hour simple moving average and the monthly pivot point near 56.89 holds.

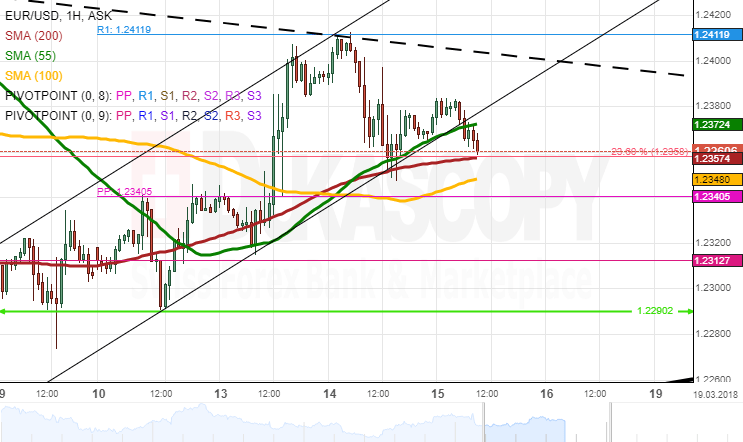

EUR/USD Analysis: Likely To Be Pressured North

The Euro managed to remain near 1.24 during the Asian session early on Wednesday, thus trying to gain enough strength to surpass the weekly R1 at 1.2412.

Bears saw an opportunity to push the rate lower—a move which was strengthened by rather dovish comments from the ECB President Draghi during the first part of the day. The subsequent fall, however, failed to match support set by the 55– and 200-hour SMAs and the 23.60% Fibo at 1.2360.

It is likely that this barrier pressures the rate higher during this session, especially when a strong support cluster near 1.2355 is apparent on the four-hour chart, as well.

Gains are likely to be capped near the one-month high of 1.2440. The prevalence of this scenario would push the Euro closer to a medium-term channel circa 1.2450.

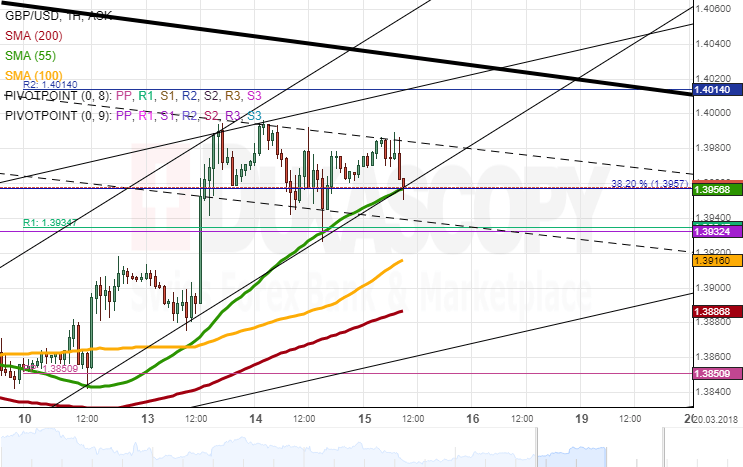

GBP/USD Analysis: Consolidates Below 1.40

Even though the general tendency for the pair was southwards on Wednesday, GBP/USD failed to make a notable advance in this direction. From the upside, the Sterling was restricted by a two-week high of 1.40, while support was provided by the 38.20% Fibo at 1.3957.

As apparent on the chart, the pair is currently trading in several channels that flash opposing signals. However, technical indicators demonstrate that some upside potential still exists in the market, thus favouring a rate increase up to the 1.4015 territory where the weekly R2 and the senior channel are located.

This appreciation is unlikely to be as steep as the drawn one-week channel, thus pointing to a more gradual increase today. Meanwhile, a possible fall should not exceed the weekly R1 and the monthly PP at 1.3830.

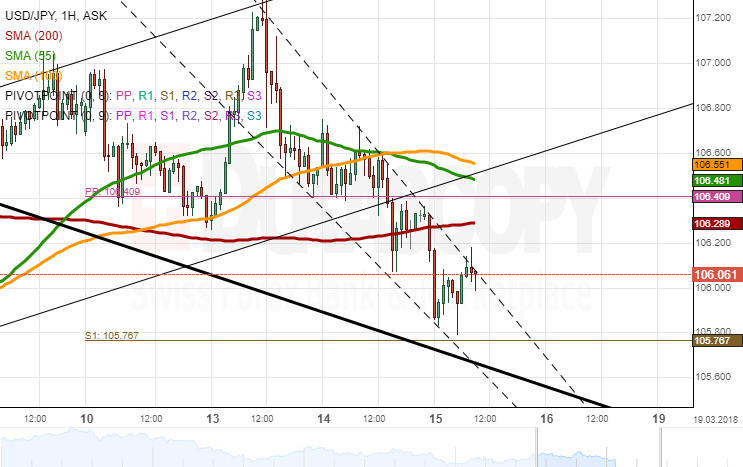

USD/JPY Analysis: Breaches SMAs

The USD/JPY exchange rate has been guided by bearish sentiment for the second consecutive session. The pair has fallen 135 pips during this time, thus dashing through various support levels along the way.

By Thursday morning, the pair was located near the 105.75 mark where the weekly S1 and the upper boundary of a three-month channel is located. Technical indicators are located in the strongly bearish area, suggesting that some upward correction should occur soon.

It is likely that the Greenback forms a retracement form the senior channel circa 105.50 and pushes for the weekly PP and the 55– and 100-hour SMAs near 106.40.

In case no fundamental events shake the market in this session, the pair is unlikely to breach this area, thus remaining in the 105.50/106.40 range.

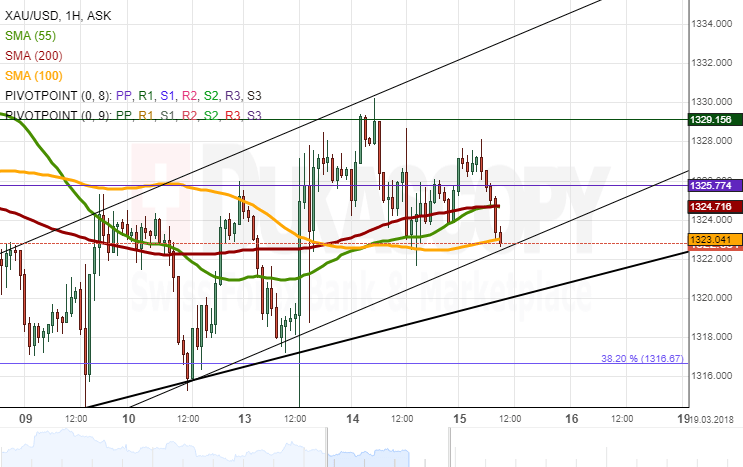

Gold Approaches Trend-Line

The yellow metal has made no significant advances during the previous session, as any attempts to move below the 1,322.90 area was restricted by the strong support of the 55-, 100– and 200-hour SMAs.

The pair has managed to appreciate during the past few sessions following a test of the 1,315.00 level. A notable climb, however, has not yet followed. Thus, it is likely that the pair fails to edge higher this week, especially given the fact that it has approached a downward-sloping trend-line guiding the rate during the previous four weeks.

By and large, the rate might remain stranded between this line and the SMAs for several hours. However, downside risks should eventually prevail, thus sending the pair closer to the 38.20% Fibo at 1,316.65.

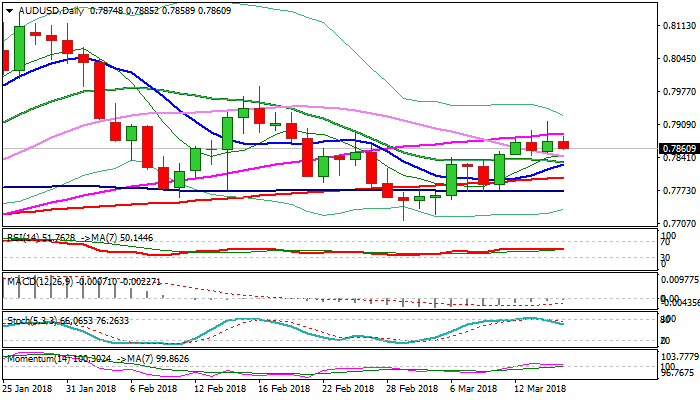

Technical Outlook: AUDUSD – Stronger Reversal Signal On Break Below Daily Kijun-Sen

The Australian dollar moved lower on Thursday after repeated failure on attack at key barriers at 0.7882/90 (Fibo 61.8% of 0.7988/0.7712 / 55SMA). Near-term action so far holds above daily Kijun-sen support (0.7850) which limits downside risk, generating after repeated upside rejections and supported by weakening momentum studies and south-heading slow stochastic which reversed from overbought territory. Bearish scenario requires break below Kijun-sen as initial negative signal, with extension below daily cloud base (0.7817) to confirm top and reversal. Extended consolidation could be expected while Kijun-sen holds, but close above 55SMA is needed to generate bullish signal for continuation of recovery leg from 0.7712 (01 Mar low).

Res: 0.7890, 0.7923, 0.7973, 0.7988

Sup: 0.7850, 0.7830, 0.7817, 0.7772

Market Update – European Session: Norway Tweaks Its Language On Its 1st Potential Rate Hike To Be More Hawkish

Notes/Observations

SNB keeps its rhetoric unchanged; shows it was in no hurry to change rates

Norway Central Bank (Norges) tweaked its view on the 1st potential rate hike to after summer from its prior view of in the autumn (more hawkish)

Sweden Unemployment data handily beats expectations but analyst see several caveats due to design of survey

Poland Feb CPI data miss keeps door open for more potential rate cuts

Asia:

New Zealand Q4 GDP Q/Q: 0.6% v 0.8%e; Y/Y: 2.9% v 3.1%e

Australia Mar Consumer Inflation Expectation Survey: 3.7% v 3.6% prior

-Japan Fin Min Aso reiterated stance that BoJ law had the central bank forbidden from buying foreign bonds for the purpose of influencing FX rates; had to be 'very careful' about buying foreign bonds. BoJ was adopting easing policy to beat deflation, not influence FX moves (**Insight: BoJ was not allowed to buy foreign bonds for the purpose of influencing FX rates, since exchange rate policy was under Japan's Finance Ministry)

Japan ruling party Diet affairs official stated that Fin Min Aso to skip G20 finance chief meeting next week (as speculated). Aso was scheduled to participate in a session of the Budget Committee of the House of Councilors on Monday to answer questions from lawmakers.

BoJ Gov Kuroda: Japan had been implementing strong QE; inflation had been steadily rising in the last two years. Reiterated to continue with powerful easing and carefully look at impact from policy

Europe:

UK Brexit Sec Davis: Could live with a transition period under 2 years if that helps secure an early deal. The govt main priority was to secure an agreement on implementation period at next week’s EU Leader summit

Forza Italia's Berlusconi stated that would not join a govt with the Five Star Party and sought to convince right-wing ally to try to form government with support from centre-left democratic party

EU said to consider 3% 'digital tax' on the revenues of technology companies and could apply to technology companies that have over 100K users in Europe.

Americas:

White House confirmed Kudlow has accepted the position as NEC chairman (replaced Gary Cohn); Fed's Quarles said to be considered by the Trump administration for Chairman of the Financial Stability Board

Economic Data:

(NL) Netherlands Jan Trade Balance: €3.4B v €4.2B prior

(NL) Netherlands Jan Retail Sales Y/Y: 4.9 v 1.3% prior

(NL) Netherlands Feb Unemployment Rate: 4.1% v 4.2% prior

(DK) Denmark Feb PPI M/M: 0.0% v 0.7% prior; Y/Y: 1.1% v 1.4% prior

(FI) Finland Jan Current Account Balance: €0.3B v €0.4B prior

(TR) Turkey Dec Unemployment Rate: 10.4% v 10.4%e

(EU) EU27 Feb New Car Registrations: 4.3% v 7.1% prior

(SE) Sweden Prospera Inflation Expectations Survey

(FR) France Feb Final CPI M/M: 0.0% v -0.1%e; Y/Y: 1.2% v 1.2%e

(FR) France Feb Final CPI EU Harmonized M/M: 0.0% v 0.0%e; Y/Y: 1.3% v 1.3%e; CPI Ex-Tobacco Index: 101.64 v 101.60e

(CZ) Czech Jan Industrial Output Y/Y: 5.5% v 5.5%e; Construction Output Y/Y: +33.6% v -3.2% prior

(CZ) Czech Jan Retail Sales Y/Y: 5.7% v 6.3%e; Retail Sales (ex- Auto) Y/Y: 8.2% v 6.5%e

(TR) Turkey Feb Central Gov't Budget Balance (TRY): -1.9B v +1.7B prior

(CH) Swiss Feb Producer & Import Prices M/M: 0.3% v 0.3% prior; Y/Y: 2.3% v 1.8% prior

(CH) Swiss National Bank (SNB) Interest Rate Decision: Expected to leave Sight Deposit Interest Rate unchanged at -0.75% and maintain the 3-Month Libor Range between -1.25% to -0.25%

(SE) Sweden Feb Unemployment Rate: 6.3% v 7.0%e; Unemployment Rate (Seasonally Adj): 5.9% v 6.5%e

05:00 (PL) Poland Feb CPI M/M: -0.2% v +0.2%e; Y/Y: 1.4% v 1.8%e

(NO) Norway Central Bank (Norges) left the Deposit Rates unchanged at 0.50% (as expected); brings forward its 1st potential rate hike

(ZA) South Africa Jan Total Mining Production M/M: 1.0% v 0.5%e; Y/Y: 2.4% v 1.3%e; Gold Production Y/Y: -7.7% v -12.5% prior; Platinum Production Y/Y: -13.6% v -1.4% prior

(IT) Italy Jan General Government Debt: €2.280T v €2.256T prior

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €4.95B vs. €4.5-5.5B indicated in 2022, 2028, 2033 and 2040 Bonds

Sold €1.81B in 0.45% Oct 2022 SPGB; Avg yield: 0.294% v 0.358% prior, Bid-to-cover: 1.45x v 1.88x prior

Sold €1.61B in 1.40% Apr 2028 SPGB; Avg yield: 1.363% v 1.580% prior, Bid-to-cover: 1.28x v 2.47x prior

Sold €719M in 2.35% July 2033 SPGB; Avg Yield:1.875% v 2.110% prior; Bid-to-cover: 1.65x v 1.87x prior

Sold €940M in 4.9% July 2040 SPGB; Avg yield: 2.167% v 2.462% prior, bid-to-cover 1.26x v 1.57x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.3% at 376.2, FTSE +0.4% at 7158, DAX +0.6% at 12313, CAC-40 +0.5% at 5261, IBEX-35 -0.1% at 9682, FTSE MIB +0.6% at 22576 , SMI -0.2% at 8853, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: Trades mostly higher across the board with notable strength in the Dax which leads the gainers, following US futures, which look to rebound after declines yesterday. Lufthansa, K+S, Munich Re, Sixt SE trade higher in Germnay following earnings and guidance. In the UK gainers include Old Mutual, Cineworld following reuslts, while PZ Cussons trades sharply lower after cutting its outlook. Unilever shares trade slightly lower after announcing a new corporate structure; Swedish retail giant H&M trades over 4% lower after missing Revenue forecasts. Looking ahead notable earners include Dollar General and Genesco.

Movers

Consumer Discretionary [Lufthansa [LHA.DE] +2.1% (Earnings), H&M [HMB.SE] -4.7% (Earnings), Sixt SE [SIX2.DE] +2.1% (Earnings), Cineworld [CINE.UK] +2.7% (Earnings), Pz Cussons [PZC.UK] -18% (Outlook)]

Industrials [Leonardo [LDO.IT] +1.8% (Earnings), Kier [KIE.UK] -4.0 (Earnings) ]

Financials [ Generali [G.IT] +1.0% (Earnings), Munich Re [MUV2.DE] +1.4% (Guidance), Old Mutual [OML.UK] +1.2% (Earnings)]

Energy [Bourbon [GB.FR] -8.3% (Earnings)]

Speakers

Swiss National Bank Policy Statement reiterated its view that CHF currency (franc) remained highly valued while FX market remained fragile. Reiterated that negative interest rates and FX intervention pledge remained essential. Reiterated that imbalances in property market persisted and would watch it closely

Norway Central Bank (Norges) Policy Statement: noted that it now saw economic conditions as stronger than expected back in Dec and now forecasted a somewhat earlier increase in interest rates to after summer 2018 compared to its Dec view of one in autumn. Housing market correction had reduced the risk of an abrupt and more pronounced decline further out

Norway Central Bank (Norges) Gov Olsen post rate decision press conference stated that interest rates would most likely to be raised after summer. Remained to be seen if August was a summer month. International growth seen higher than forecast but risk of protectionism could dampen outlook

Bank of France updated its economic outlook which raised 2018 and 2019 GDP forecasts. Raised 2018 GDP growth forecast from 1.7% to 1.9% and 2019 GDP growth forecast from 1.7% to 1.8%

UK Brexit Min Davis reiterated view that no deal is better than a bad deal. Transition period based upon existing arrangements

Italy 5-star leader Di Maio: Spoke with Northern League leader Salvini on options

Japan Fin Min Aso reiterated stance that BoJ law has the central bank forbidden from buying foreign bonds for the purpose of influencing FX rates; hade to be 'very careful' about buying foreign bonds

Thailand Central Bank Gov Veerathai: THB currency (Baht) aprreciating due to weaker USD and inflows of foreign funds. Could not resist the FX trend but could address excessive swings in price action

India Trade Ministry official Dwivedi: Draft gold policy could be finalized by end of month or in early April (**Note: Had been speculation that the tax could be cut by 2% by 2019)

IEA Monthly Report raised its 2018 global oil demand growth forecast from 1.4M bpd to 1.5M bpd with global demand seen at 99.3M vs. 99.2M bpd prior. OPEC Feb oil production at 32.1M (prior was 32.3M bpd) and maintained its Non-OPEC 2018 Oil supply at 59.9M bpd (compared to 58.2M in 2017)

Currencies

USD was again little changed against the major European pairs

SNB kept its rhetoric unchanged with the CHF currency seen as ‘highly valued’ thus showing it was in no hurry to change rates

The SEK currency (Krona) was firmer after Swedish Feb unemployment data handily beat expectations. EUR/SEK cross at 2-week lows to test under 10.0850 level

The NOK currency was former after the Norway Central bank tweaked its view on the 1st potential rate hike to after summer from its prior view of in the autumn. EUR/NOK hit a 4-month low of under 9.50 in the aftermath of the commentary as Norges new rate path suggested 100% chance of a Sept rate hike

Fixed Income

Bund Futures trade 4 ticks higher at 157.89 erasing earlier losses. Upside targets 157.75, while a return lower targets the155.50 level.

Gilt futures trade at 122.44 up 4 ticks approaching the January 17th high. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

Thursday's liquidity report showed Wednesday's excess liquidity rose to €1.901T from €1.900T prior. Use of the marginal lending facility stayed rose from €5M to €85M.

Looking Ahead

(CO) Colombia Feb Consumer Confidence Index: No est v -5.4 prior

(CO) Colombia Q4 Current Account Balance: No est v -$2.6B prior

06:00 (GR) Greece Q4 Unemployment Rate: No est v 20.2% prior

05:50 (FR) France Debt Agency (AFT) to sell €6.5-7.5B in 2021, 2023 and 2025 Oats

06:00 (EU) Daily Euribor Fixing

06:00 (SE) Sweden to sell I/L Bonds

06:30 (UK) DMO to sell £2.5B in new 1.625% Oct 2028 Gilts

06:30 (PL) Poland to sell Bonds

06:30 (IE) Ireland Debt Agency (NTMA)to sell€500M in 12-month bills

06:50 France Debt Agency (AFT) to sell €1.25-1.75B in Inflation-Linked 2023, 2028 and 2040 bonds (Oatei)

07:00 (IE) Ireland Q4 GDP Q/Q: 1.7%e v 4.2% prior; Y/Y: 6.0%e v 10.5% prior

07:00 (IE) Ireland Q4 Current Account Balance: No est v €14.5B prior

07:00 (IE) Ireland Feb CPI M/M: No est v -0.7% prior; Y/Y: No est v 0.2% prior

07:00 (IE) Ireland Feb CPI EU Harmonized M/M: No est v -0.7% prior; Y/Y: No est v 0.3% prior

07:00 (BR) Brazil Mar FGV Inflation IGP-10 M/M: 0.4%e v 0.2% prior

07:00 (HU) Hungary Central Bank Holds Interest Rate Swap (IRS) Tender

07:30 (TR) Turkey Central Bank TCMB Survey of Expectations; Next 12 Month: No est v 9.3% prior

07:30 (CL) Chile Central bank Traders Survey - 07:45 (US) Daily Libor Fixing

08:30 (US) Initial Jobless Claims: 227e v 231K prior; Continuing Claims: 1.903Me v 1.870M prior

08:30 (US) Mar Empire Manufacturing: 15.0e v 13.1 prior

08:30 (US) Feb Import Price Index M/M: 0.2%e v 1.0% prior; Y/Y: 3.5%e v 3.6% prior; Import Price Index (ex-Petroleum) M/M: 0.3%e v 0.5% prior

08:30 (US) Feb Export Price Index M/M: 0.3%e v 0.8% prior; Y/Y: No est v 3.4% prior

08:30 (CA) Canada Feb ADP Payrolls Report

08:30 (US) Weekly USDA Net Export Sales

09:00 (RU) Russia Gold and Forex Reserve w/e Mar 9th: No est v $450.9B prior

09:00 (CA) Canada Feb Existing Home Sales M/M: No est v -14.5% prior

09:05 (UK) Baltic Dry Bulk Index

-10:00 (BE) Belgium Jan Trade Balance: No est v -€1.9B prior

10:00 (US) Mar NAHB Housing Market Index: 72e v 72 prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (PT) Portugal PM Costa in Parliament

11:00 (US) Treasury to announcement for upcoming 10-year TIPS auction schedule for Mar 22nd

11:45 (DE) ECB’s Lautenschaelger (Germany, SSM member)

12:30 (IL) Israel Feb CPI M/M: 0.0%e v -0.5% prior; Y/Y: 0.1%e v 0.1% prior

16:00 (US) Jan Total Net TIC Flows: No est v -$119.3B prior; Net Long-term TIC Flows: No est v $27.3B prior