Sample Category Title

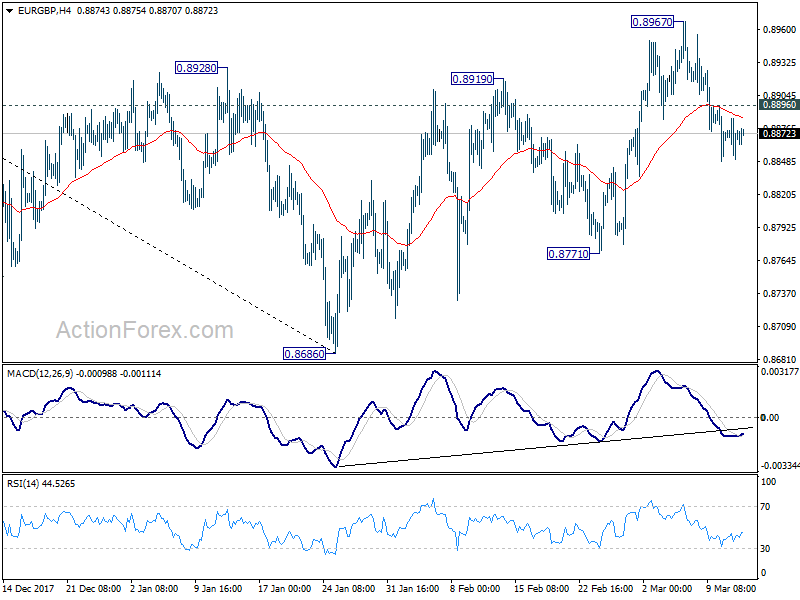

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8855; (P) 0.8870; (R1) 0.8890; More...

With 0.8896 minor resistance intact, intraday bias in EUR/GBP remains on the downside. Fall from 0.8967 should target 0.8871 support first. Break there will confirm completion of rebound from 0.8686 and target a retest of this low. On the upside, above 0.8896 minor resistance will turn bias neutral first. Further break of 0.8967 will resume the rebound from 0.8686 to 61.8% retracement of 0.9305 to 0.8686 at 0.9069.

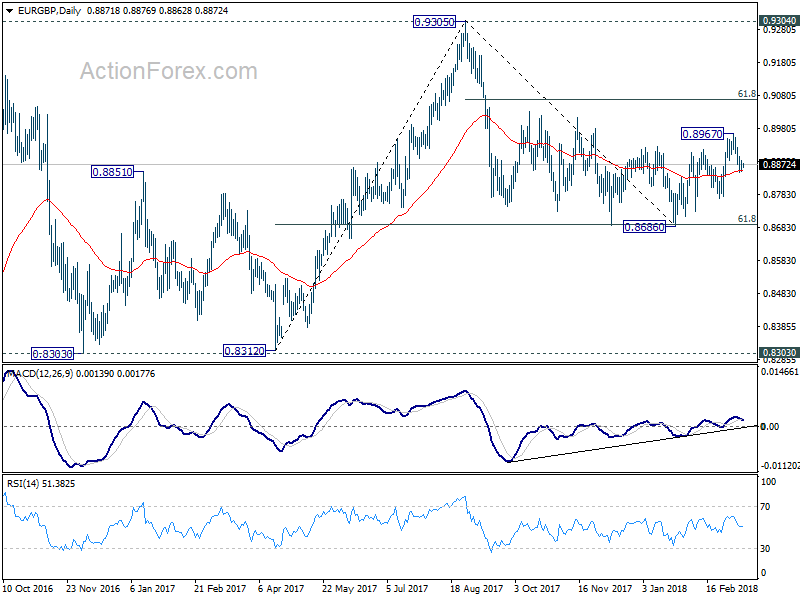

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

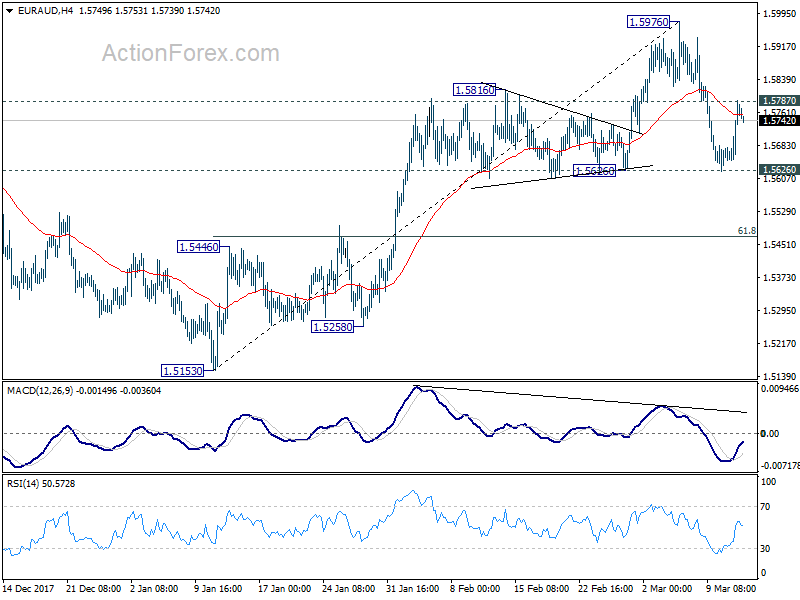

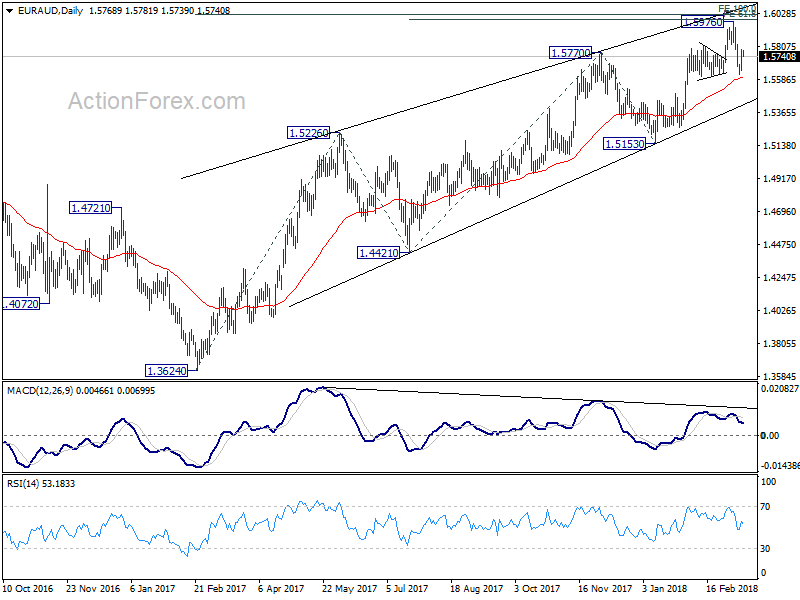

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5676; (P) 1.5733; (R1) 1.5820; More....

EUR/AUD rebounded after drawing support from 1.5626. Intraday bias is turned neutral first. On the upside, break of 1.5787 minor resistance will indicate completion of the pull back from 1.5976. And, intraday bias will be turned back to the upside for retesting 1.5976 high. ON the downside, decisive break of 1.5626 will target 61.8% retracement of 1.5153 to 1.5976 at 1.5467 and below.

In the bigger picture, change of medium term reversal is increasing with EUR/AUD just missing double projection target. They are 61.8% projection of 1.4421 to 1.5770 from 1.5153 at 1.5987, and 100% projection of 1.3624 to 1.5226 from 1.4421at 1.6023. Also, bearish divergence condition remains in daily MACD. Break of 1.5626 support will add to this bearish case and target 1.5153 key support for confirmation. Nonetheless, before that happens, as long as 1.5153 support holds, medium term rise from 1.3624 could still extend to retest 1.6587 high.

Market Update – Asian Session: Equities Remain Lower

Headlines/Economic Data

General Trend: Asian equity markets trade generally lower: Trade concerns being cited according to press reports

Financials decline amid drop in bond yields

Toyota to offer workers total pay increase of 3.3% amid calls for 3% wage hikes by Japan’s government

China issues Jan-Feb Industrial Production, Lunar New Year impact unclear

Yesterday saw the first time 10-yr JGBs failed to trade since June 2017

President Trump fires Sec State Tillerson, replacing him with CIA director Pompeo

Japan

Nikkei 225 opened -0.9%; closed -0.9%

Toyota Motor, 7203.JP Planning to raise pay by 3.3% this year – Asahi

Nikkei-weighted Fast Retailing declines over 2% on below avg volume

(JP) Participants in the QUICK survey see USD/JPY at ¥106.39 at the end of March v ¥109.99 seen in poll taken in late Feb – Nikkei

(JP) Japan Jan Core Machine Orders M/M: 8.2% v +5.2%e (fastest pace in 2-yrs); Y/Y: +2.9% v -0.7%e

(JP) Bank of Japan (BOJ) Jan 22-23rd Policy Meeting Minutes: Markets have become more sensitive to BOJ policy

(JP) Japan PM Abe: Did not order doctoring of Moritomo documents; Want Fin Min Aso to rebuild ministry of finance

Nissan, 7201.JP Approves 2.4% wage raise, ¥3,000/month base pay raise - Japan press

(JP) According to analysts international investors are worried about "Abexit" with $2.1B in funds flowing out of 70 Japan focused funds so far this month – Nikkei

Honda, 7267.JP Said to tell union that it plans to raise base pay by ¥1,700/month

(JP) BoJ Gov Kuroda: Reiterates BoJ should not discuss timing and details of stimulus exit at the moment

Korea

Kospi opened -0.7%

(KR) According to OECD South Korea likely to maintain 3% GDP through 2018 and 2019 - Korean press

(KR) South Korea Feb Export Price Index M/M: +1.0% v -0.4% prior; Y/Y: -1.3% v -3.5% prior; Import Price Index M/M: +0.7% v +0.7% prior; Y/Y: +0.4% v -2.4% prior

(KR) South Korea President Moon: Urges govt to quickly come up with measures to help small and medium-sized enterprises, as well as people and businesses in Gunsan, the region hit by the planned shutdown of the GM Korea plant

(KR) Pres Trump: something positive will come out of Korea situation

(KR) South Korea President Moon and North Korea leader Kim may discuss declaring an end to Korean war - Korean press

China/Hong Kong

Hang Seng opened %, Shanghai Composite %

Hang Seng Financials Index -1.5%, Information Technology -1.3%

(CN) Trump admin reportedly considering imposing $60B in tariffs on Chinese goods - press (earlier reports said Trump wanted over $30B in tariffs)

(CN) China monetary policy must serve high quality economy - China Daily

(CN) Shanghai plans to encourage state-owned enterprises (SOEs) to list shares - Chinese Press

(CN) China PBoC Open Market Operation (OMO): Injects CNY50B v CNY60B prior in 7 and 28-day reverse repos; Net injection CNY50B v CNY60B prior

(CN) PBOC sets yuan reference rate at 6.3205 v 6.3218 prior

(HK) Hong Kong Finance Sec Chan: Hong Kong will subsidize cost of bond issues up to HK$2.5M

(CN) China Feb Fixed Assets Ex Rural YTD Y/Y: 7.9% v 7.0%e

(CN) CHINA FEB INDUSTRIAL PRODUCTION YTD Y/Y: 7.2% V 6.2%E

(CN) CHINA FEB RETAIL SALES YTD: 9.7% V 10.0%E

(CN) China NBS: External and domestic demand remains solid; have the conditions to reach 6.5% GDP target

(CN) China to announce PBOC Gov Zhou replacement Monday March 19th; front runners include Politburo member Liu He or economist Xie Fuzhan - SCMP

Cathay Pacific, 293.HK Reports FY17 (HK$) Net loss 1.3B v loss 2.3Be; Rev 97.3B v 94Be (2nd consecutive yearly loss, 1st time in history of company)

Australia/New Zealand

ASX 200 opened -0.1%; closed -0.6%

ASX 200 Telecom Index -2.4%, REIT -1%, Financials -0.8%

National Australia Bank, NAB.AU Staff were approving loans they knew that were fake in order to meet sales targets and trigger incentive payments - AFR

(NZ) New Zealand Q4 Current Account (NZ$): -2.77B v -2.5Be; Current Account GDP Ratio YTD: -2.7% v -2.6%e

(AU) Reserve Bank of Australia (RBA) Kent: Mortgage bond issuance has stayed at post crisis high; Accommodative monetary policies and generally low levels of inflation are contributing to easy financial conditions for issuers. No reason RBA moves have to be in 25bps increments

Looking Ahead: New Zealand Q4 GDP data due for release on Thursday

Other Asia

(ID) Indonesia Central Bank (BI): Rupiah has been stable since last week; we have consistently maintained rupiah level

(SG) Singapore Monetary Authority (MAS) Survey: 2018 GDP growth seen at 3.2% v 3.0% estimated in Dec

North America

US equity markets ended lower: Dow -0.7%, S&P500 -0.6%, Nasdaq -1.0%, Russell 2000 -0.6%

S&P500 Technology -1.2%, Financials -1.1%

(US) Pres Trump has removed US Secretary of State Rex Tillerson; nominates current CIA Director Mike Pompeo to be new Secretary of State

(US) Trump says he and Tillerson disagreed on the Iran deal; Pompeo agrees with him that Iran nuclear deal is terrible

(US) Reportedly Tillerson wanted to remain in the job; Trump wanted to reshuffle his foreign relations team ahead of potential talks with North Korea – press(US) Weekly API Oil Inventories: Crude: +1.2M v +5.7M prior

QCOM Following opposition from the US government Broadcom is expected to abandon bid - US financial press

(US) Pennsylvania Special Election Results: Conor Lamb (D) leads by 95 votes with 109,945 vote v Rick Saccone (R) with 109,850 votes; 99% of votes counted

(US) Weekly API Oil Inventories: Crude: +1.2M v +5.7M prior

Looking Ahead: US Feb Retail Sales to be released, along with the weekly DOE Crude Oil Inventories

Europe

(UK) UK PM May Brexit Committee said to agree to open borders until 2021 - UK Press

(EU) EU Commission draft proposal: banks to be required to have higher prudential backstops for new loans originating after March 14th that go bad – press

G20 Leaders March 20th draft communique: plan to reiterate summit conclusions on trade from July 2017; To say they are working to strengthen trade contribution to their economies; Will refrain from competitive devaluations and not target exchange rates for competitive purposes; to say flexible exchange rates where feasible can serve as a shock absorber - press

Looking Ahead: OPEC monthly report due to be released

Levels as of 01:00ET

Hang Seng -1.4%; Shanghai Composite -0.4%; Kospi -0.5%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.3%, Dax 0.0%; FTSE100 -0.1%

EUR 1.2412-1.2389; JPY 106.75-106.39; AUD 0.7878-0.7852;NZD 0.7354-0.7322

Apr Gold +0.3% at $1,330/oz; Apr Crude Oil +0.1%at $60.77/brl; May Copper +0.9% at $3.16/lb

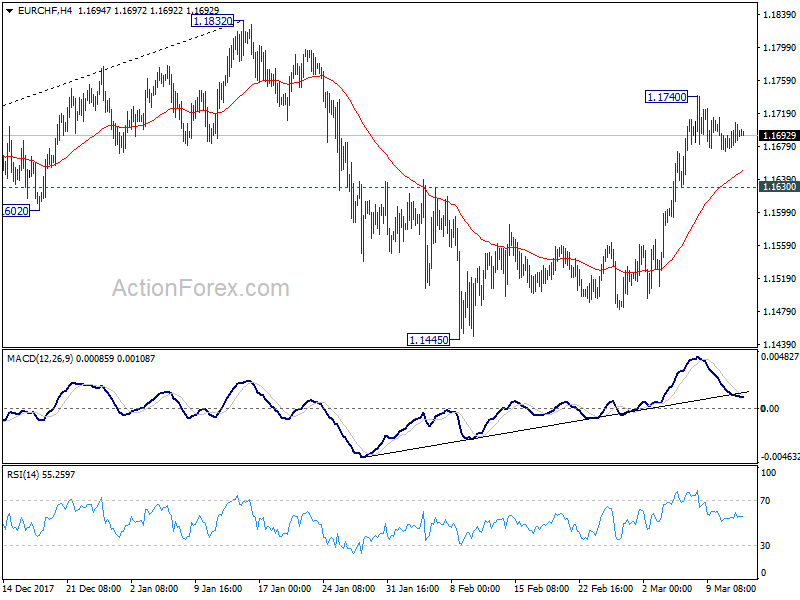

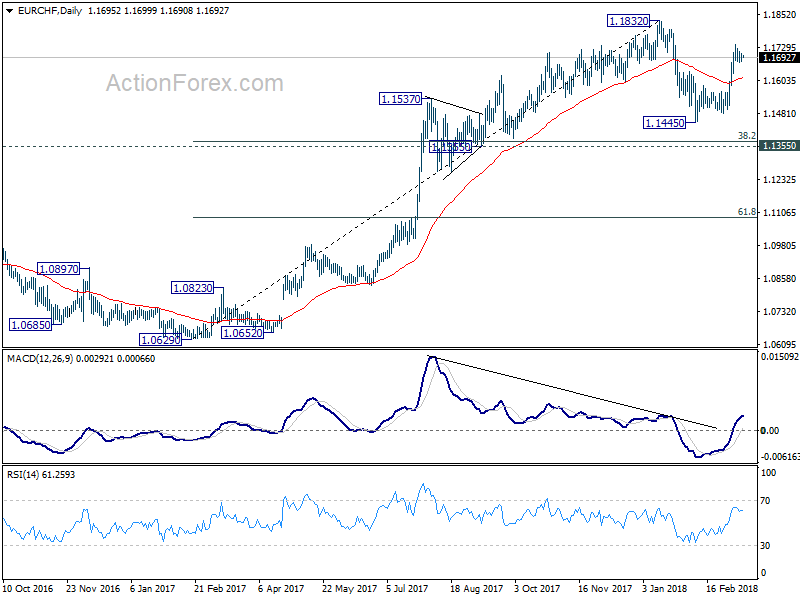

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1677; (P) 1.1692; (R1) 1.1712; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 1.1740 temporary top extends. Further rise is expected as long as 1.1630 minor support holds. Above 1.1740 will target a test on 1.1832 high. We'll stay cautious strong resistance from there to bring another fall. Corrective pattern from 1.1832 might still have an attempt on 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372) before completion. On the downside, below 1.1630 minor support will target 1.1445 low again.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

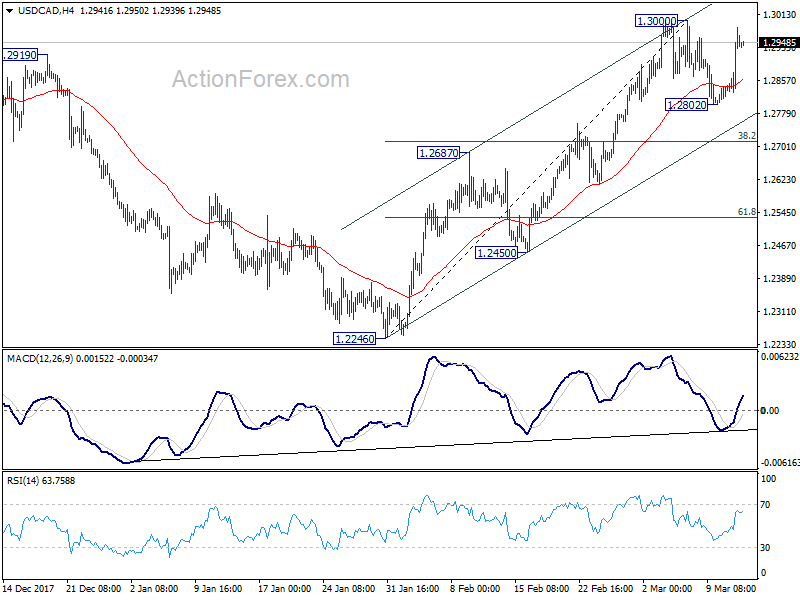

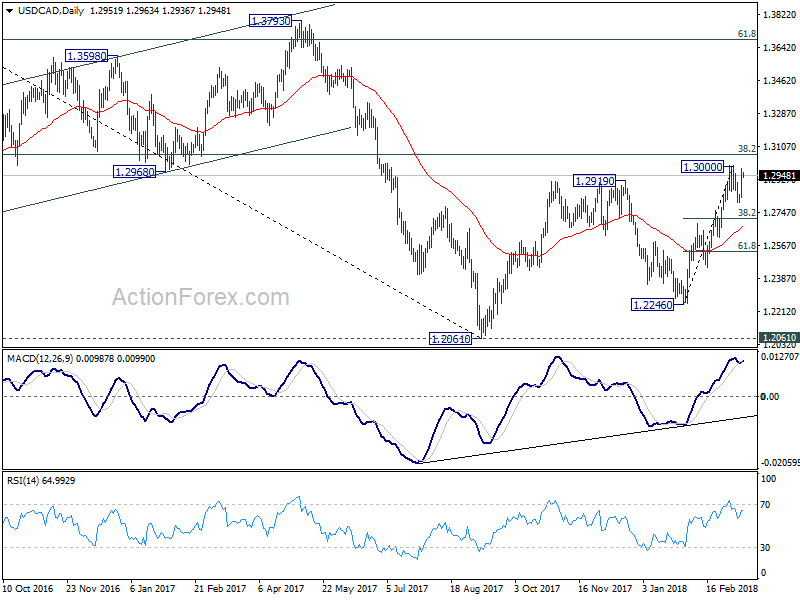

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2869; (P) 1.2926; (R1) 1.3023; More....

While the rebound from 1.2802 was strong, it's limited below 1.3000 resistance. Intraday bias in USD/CAD remains neutral first. On the upside, break of 1.3000 will resume medium term rebound from 1.2061 and target 1.3065 medium term fibonacci level. On the downside, in case of another decline as consolidation from 1.3000 extends, we'd expect strong support from 38.2% retracement of 1.2246 to 1.3000 at 1.2712 to contain downside and bring rise resumption.

In the bigger picture, we're favoring the medium term bullish case. That is larger down trend from 1.4689 has completed at 1.2061, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen back to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 first. Break will target 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2687 support holds.

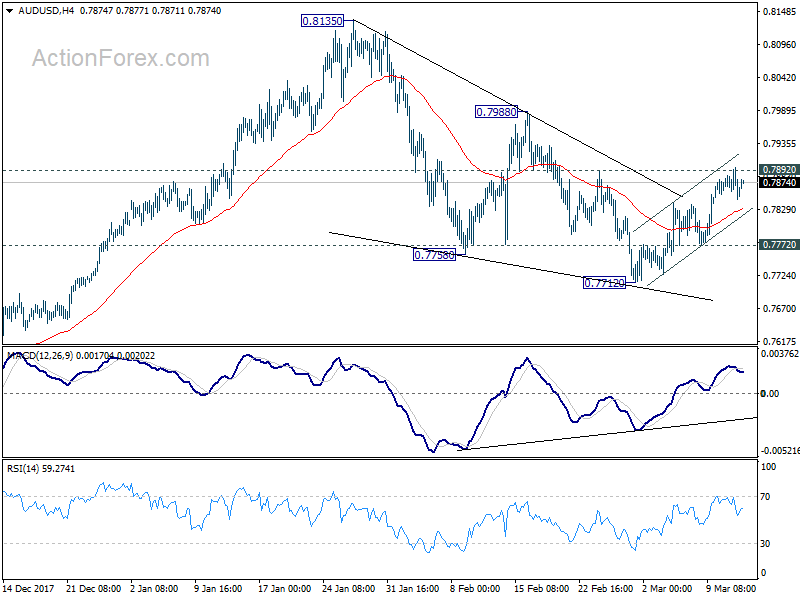

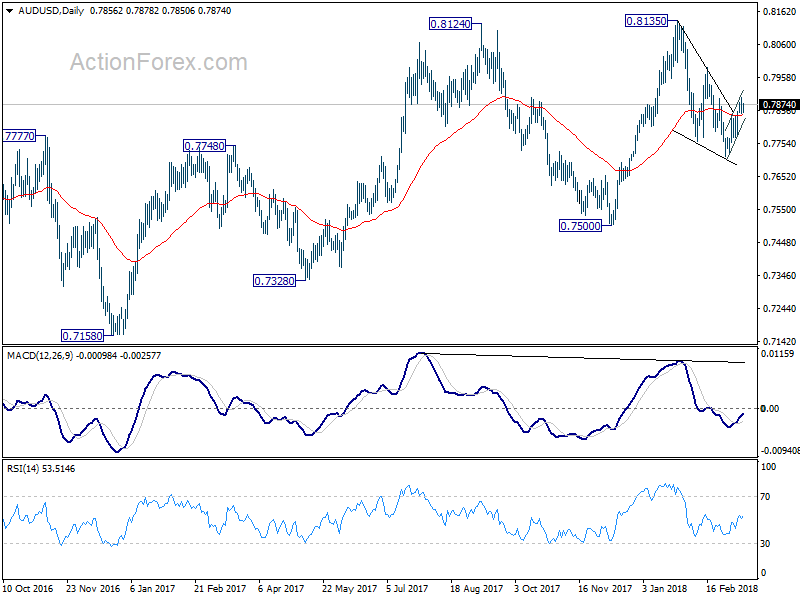

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7836; (P) 0.7867; (R1) 0.7888; More...

AUD/USD lost momentum after failing to stay above 0.7892 resistance. Intraday bias is turned neutral first. We're slightly favoring the case that corrective pull back from 0.8135 has completed with three waves down to 0.7712. Further rise is expected as long as 0.7772 minor support holds. Above 0.7892 again will target 0.7988 resistance. Decisive break there will bring larger rally resumption. Nonetheless, on the downside. On the downside, below 0.7772 will turn bias to the downside for 0.7712. Break there will resume whole fall from 0.8135.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.12; (P) 106.70; (R1) 107.16; More...

USD/JPY's corrective trading from 105.24 continues and retreated after losing momentum ahead of 107.67 resistance. Intraday bias remains neutral as consolidation from 105.24 might extend. Also, another decline will remain in favor as long as 107.67 holds. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, firm break of 107.67 resistance will indicate near term reversal, on bullish convergence condition in 4 hour MACD. In such case, outlook will be turned bullish for 110.47 resistance next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

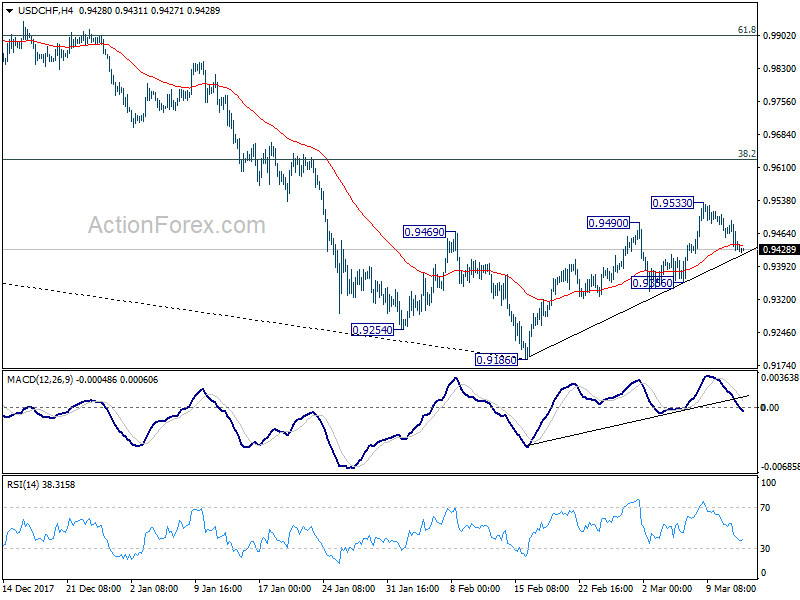

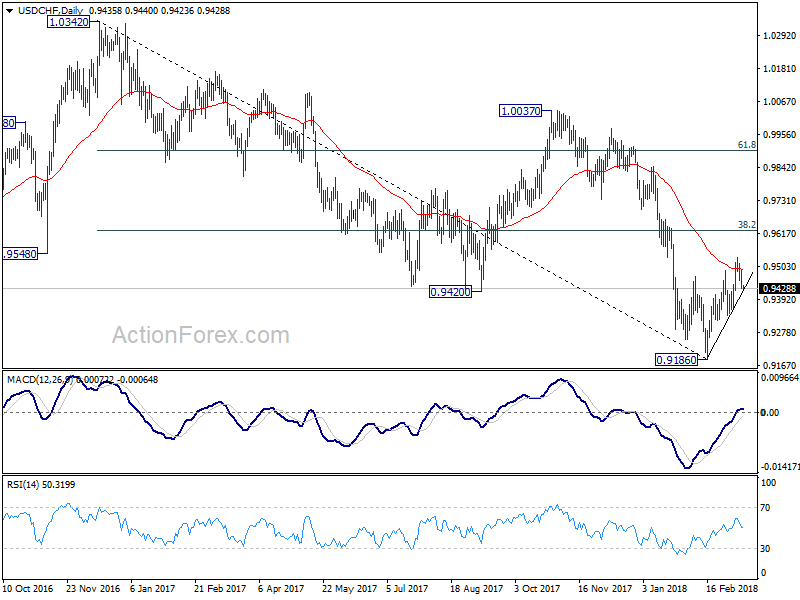

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9414; (P) 0.9454; (R1) 0.9478; More...

Intraday bias in USD/CHF remains neutral for the moment. At this point, further rise is still expected with 0.9356 support intact. Above 0.9533 will target 0.9626 fibonacci level. However, break of 0.9356 will indicate that the rebound has completed. In such case, intraday bias will be turned back to the downside for retesting 0.9186 low.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

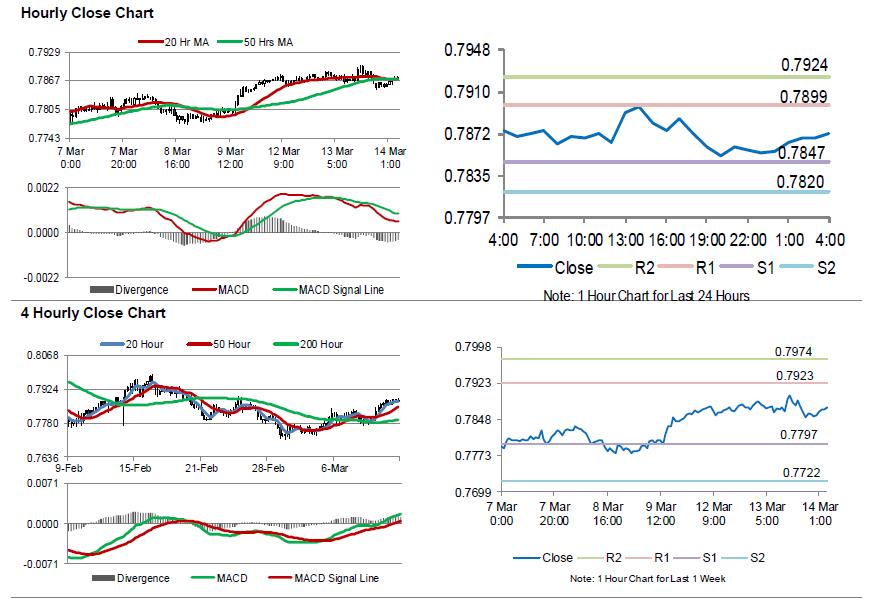

Australia’s Westpac Consumer Confidence Improved In March

For the 24 hours to 23:00 GMT, the AUD declined 0.29% against the USD and closed at 0.7855.

LME Copper prices rose 0.4% or $26.0/MT to $6883.0/MT. Aluminium prices declined 0.8% or $17.0/MT to $2080.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7873, with the AUD trading 0.23% higher against the USD from yesterday's close.

Overnight data revealed that Australia's Westpac consumer confidence index rose 0.2% MoM to a level of 103.0 in March, compared to a reading of 102.7 in the prior month.

The pair is expected to find support at 0.7847, and a fall through could take it to the next support level of 0.7820. The pair is expected to find its first resistance at 0.7899, and a rise through could take it to the next resistance level of 0.7924.

Looking ahead, Australia's consumer inflation expectation data for March, set to release overnight, will be eyed by traders.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

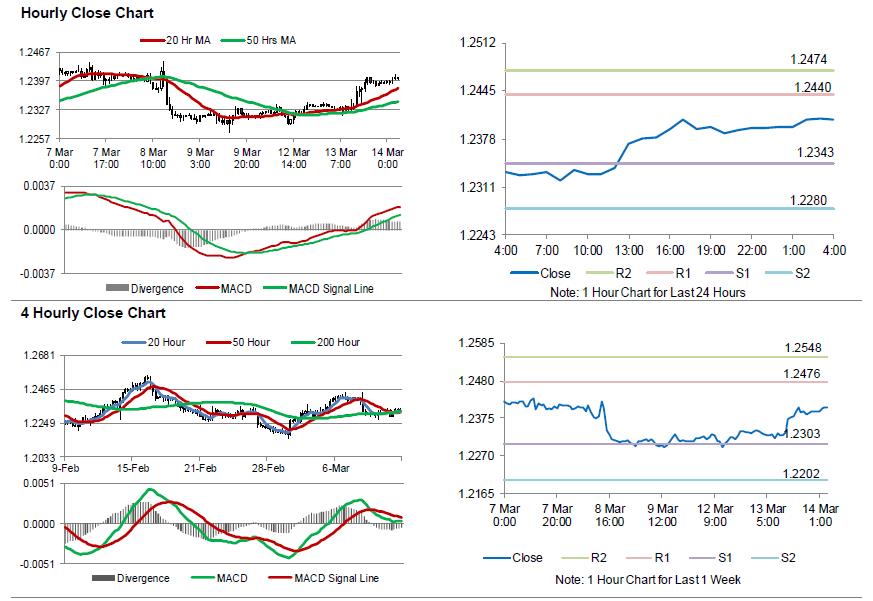

Euro Trading Higher In The Asian Session, Ahead Of Mario Draghi’s Speech

For the 24 hours to 23:00 GMT, the EUR rose 0.48% against the USD and closed at 1.2393, as the Organisation for Economic Co-operation and Development (OECD) raised its growth forecast for Euro-zone to 2.3% in 2018 and 2.1% in 2019.

The US Dollar declined against its key counterparts, amid fresh political tensions in the US after the US President, Donald Trump, unexpectedly ousted the Secretary of State, Rex Tillerson following a series of public rifts.

The greenback extended its losses, after the latest inflation report suggested that the Federal Reserve (Fed) would hike interest rates only gradually this year.

Data indicated that the US consumer price index (CPI) advanced 0.2% on a monthly basis in February, meeting market expectations and compared to a rise of 0.5% in the previous month.

Other data showed that the nation's NFIB small business optimism index climbed more-than-estimated to a level of 107.6 in February, compared to a reading of 106.9 in the prior month, while markets were expecting for an increase to a level of 107.1.

Separately, the OECD boosted its global growth forecast to 3.9% for both 2018 and 2019, up from a previous estimate of 3.6% for both years, citing a rebound in global trade and investments. Moreover, the organisation expects the US economy to grow 2.9% this year and 2.8% in 2019, due to recent enacted tax cuts, up from 2.5% and 2.1% estimated previously.

In the Asian session, at GMT0400, the pair is trading at 1.2405, with the EUR trading 0.10% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2343, and a fall through could take it to the next support level of 1.2280. The pair is expected to find its first resistance at 1.2440, and a rise through could take it to the next resistance level of 1.2474.

Moving ahead, traders would eye a speech by the European Central Bank's (ECB) Chief, Mario Draghi, due in a few hours. Additionally, the Euro-zone's industrial production data for January as well as Germany's final inflation figures for February, would be on investors' radar. Later today, the US advance retail sales for February and business inventories data for January, will keep investors on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.