Sample Category Title

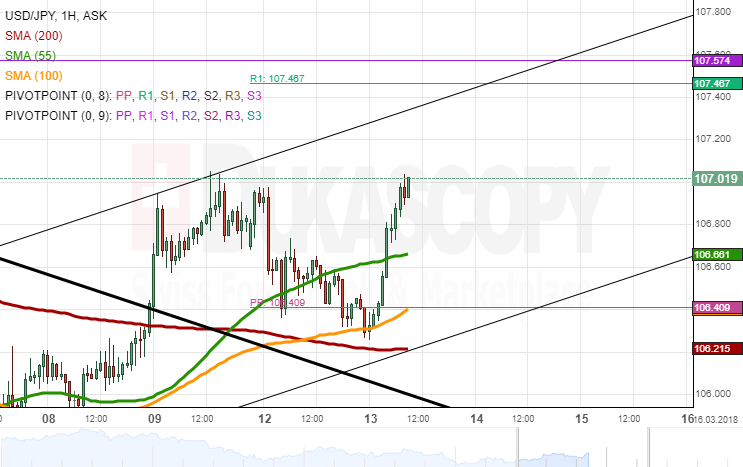

USD/JPY Analysis: Gains Momentum Early On Tuesday

Minor downside risks dominated the USD/JPY exchange rate on Monday, as it closed the session with a 60-pip fall.

The lack of bearish stimulus did not allow the Greenback to breach the combined support of the 100– and 200-hour SMAs circa 106.20. Thus, the Asian session started with a solid surge which erased all losses accumulated during the previous day.

The pair is currently trading in a two-week ascending channel. Given that its lower boundary was not reached yesterday, the pair could reverse significantly its current market sentiment and go for a test of this line, the weekly PP and the 100-hour SMA at 106.40 during the first part of the day. The remaining session is likely to be dominated by the US inflation data released at 1230GMT.

OECD: Global growth to strengthen in 2018, 2019

OECD Interim Economic Outlook: GETTING STRONGER, BUT TENSIONS ARE RISING

The world economy will continue to strengthen in 2018 and 2019, with global GDP growth projected to rise to about 4%, from 3.7% in 2017.

Stronger investment, the rebound in global trade and higher employment are helping to make the recovery increasingly broad-based.

New tax reductions and spending increases in the United States and additional fiscal stimulus in Germany are key factors behind the upward revision to global growth prospects in 2018 and 2019.

Inflation remains low, but is likely to rise modestly.

Still-elevated risk-taking and high debt levels in many countries raise financial vulnerabilities. Monetary policy normalisation could also result in greater volatility of exchange rates and capital flows, particularly in emerging market economies.

Medium-term growth prospects remain much weaker than prior to the financial crisis, reflecting less favourable demographic trends and a decade of sub-par investment and productivity.

Economic policies face several challenges:

- A gradual normalisation of monetary policy is needed, but to a varying degree across the major economies. Continued clear communication about the path to normalisation is essential to minimise the risk of financial market disruptions.

- Fiscal policy choices should avoid being excessively pro-cyclical and be clearly focused on measures that strengthen the prospects for sustainable and more inclusive medium-term growth.

- Structural reform efforts should be revived, seizing the opportunity of the stronger economy to help secure a more robust recovery of productivity, investment and living standards.

Safeguarding the rules-based international trading system will help to support growth and jobs. Governments should avoid escalation and rely on global solutions to resolve excess capacity in the global steel industry.

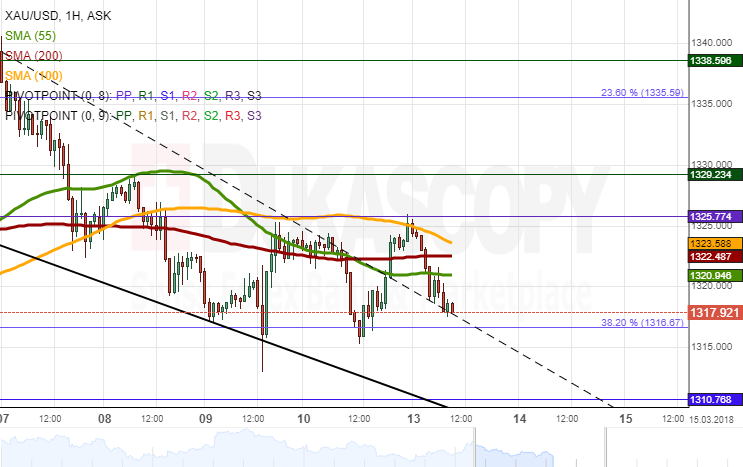

XAU/USD Analysis: Fails To Overcome 1,325.00

Following two sessions of decline, the yellow metal has allayed its bearish sentiment. The first part of Monday's session was very calm, as the bounds of the 55-, 100– and 200-our SMAs limited more extensive movements. Additional volatility was introduced later in the day; however, the aforementioned SMAs still remained the main limiting factor for the pair.

Technical indicators are strongly bearish, thus pointing to a possible decline in this session. The nearest southern barrier is 1,305.00 where the senior channel and a breached trend-line are located. In terms of resistance, Gold is restricted by the monthly PP and the 23.60% Fibo at 1,330.00 and 1,335.60, respectively.

Traders should be attentive when the US inflation data come out at 1230GMT.

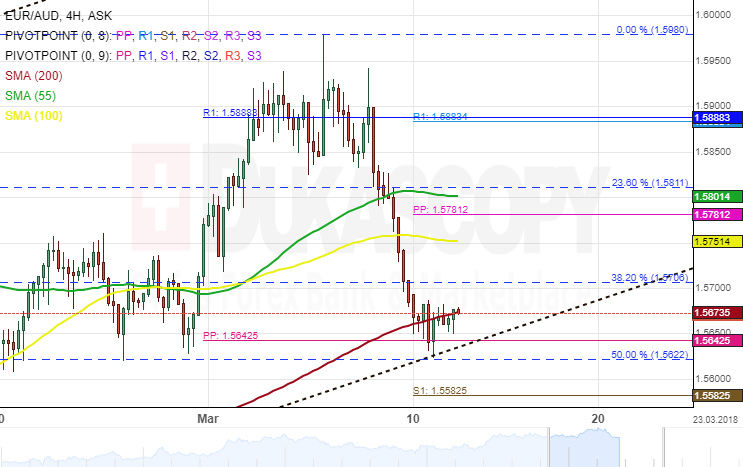

EUR/AUD 4H Chart: Restricted By SMA

The common European currency has been trading in an eight-month ascending channel against the Australian Dollar after it hit the lower boundary of a dominant channel.

After reaching the 50.00% Fibonacci retracement level, the Euro began to surge, however, the 200-hour simple moving average was pressuring the currency pair further south. This retracement can be measured by connecting the January low at 1.5264 and the March 7 high at 1.5980.

Everything being equal, the currency exchange rate is likely to decline further as technical indicators favour bears to continue their dominance.

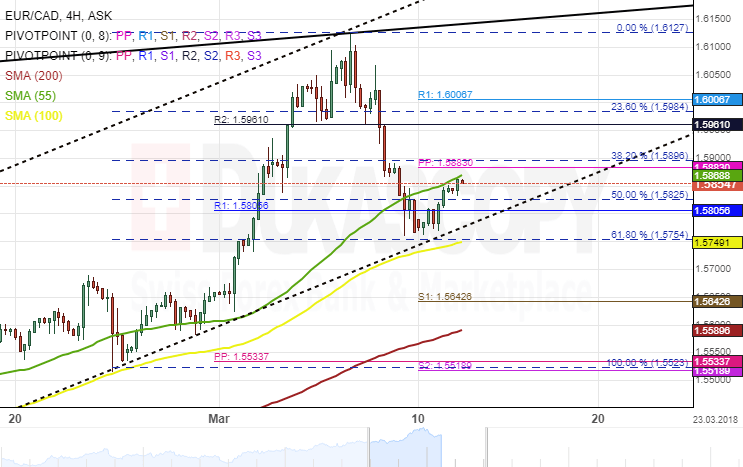

EUR/CAD 4H Chart: Reaches 61.80% Fibo

The Euro has been guided by a long and short-term ascending channel against the Canadian Dollar. The exchange rate bounced off the lower boundary of a dominant channel on September 22 and has since remained bullish.

After hitting the 61.80% Fibonacci retracement level, the EUR/CAD made a U-turn north. However, the 55-hour simple moving average was restricting the pair from making a further gain. This retracement can be measured by connecting the low at 1.5523 and the high at 1.6127.

Technical indicators demonstrate that the currency exchange rate could continue to trade upward during the following trading sessions. Nevertheless, traders are advised wait for the pair to breach the aforementioned SMA.

Market Update – European Session: Awaiting US CPI Data

Notes/Observations

Focus on US CPI data but analysts believe it would unlikely alter expectations for Fed policy

Chancellor of Exchequer Hammond (Fin Min): Spring Statement expected to reduce FY issuance for the 1st time since the financial crisis began a decade ago

Asia:

China proposes changes to government departments, ministries and bureaus: to give PBOC some functions currently held by CBRC and CIRC and merge the insurance and banking regulators. Govt giving thr PBoC the power to write the rules for the financial sector (**Note: part of a sweeping overhaul aimed at closing regulatory loopholes and curbing risk in the $43 trillion banking and insurance industries)

RBNZ Acting Gov Spencer: To review macro-prudential policy with Treasury (**Insight: Review could lead to an easing of some restrictions on home loans)

Europe:

Eurogroup Chief Centeno: ESM to approve €5.7B tranche by the end of March for Greece after national approval procedures were completed (as expected); commended Greece for its progress

Euro zone without breakthrough on deposit guarantee despite ECB call. Technical work before the meeting was still under way to agree on a common way of measuring if risks have fallen enough. ECB chief Draghi said to have told EU ministers during the meeting that conditions for the guarantees already existed - Italy Democratic Party Dep Sec Martina said to have ruled out coalition agreements with Five Star and the Centre Right. Would continue to serve citizens, from the opposition, with the role of a parliamentary minority

Americas:

Trump blocks Broadcom takeover of Qualcomm on security risks

CNBC's Larry Kudlow reportedly leading contender to replace White House economic adviser Gary Cohn

Republicans find no evidence of collusion or Russian preference for Trump. The worst the panel uncovered was “perhaps some bad judgment, inappropriate meetings, inappropriate judgment at taking meetings

Economic Data:

(FR) France Q4 Final Private Sector Payrolls Q/Q: 0.4% v 0.3%e; Total Payrolls Q/Q: 0.3% v 0.2%e

(RO) Romania Feb CPI M/M: 0.3% v 0.3%e; Y/Y: 4.7% v 4.7%e

(FI) Finland Jan Final Retail Sales Volume Y/Y: 5.1% v 4.0% prelim

(ES) Spain Feb Final CPI M/M: 0.1% v 0.1%e; Y/Y: 1.1% v 1.1%e

(ES) Spain Feb Final CPI EU Harmonized M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e

(ES) Spain Feb CPI Core M/M: 0.3% v 0.1%e; Y/Y: 1.1% v 0.8%e

(HK) Hong Kong Q4 Industrial Production Y/Y: 0.6% v 0.3% prior

(HK) Hong Kong Q4 PPI Y/Y: 3.5% v 3.7% prior

(IT) Italy Q4 Unemployment Rate: 11.0% v 11.0%e (lowest since 2012)

Fixed Income Issuance:

(ID) Indonesia sold total IDR23.45T vs. IDR17T indicated in 3-month, 12-month bills, 5-year,10-year,20-year and 30-year Bonds

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2031, 2040, 2044 and 2048 bonds

(ES) Spain Debt Agency (Tesoro) sold total €1.355B vs. €1.0-2.0B indicated range in 3-month and 9-month Bills

(NL) Netherlands Debt Agency ((DSTA) opened book to sell €4.0-6.0B in 0.75% July 2028 DSL Bond vis dutch auction; Guidance seen +16.5-17.5BPS to 0.5% Feb 2028 DSL; order book over €11B

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.1% at 379.6, FTSE flat at 7215, DAX +0.2% at 12437, CAC-40 +0.5% at 5301, IBEX-35 +0.8% at 9800, FTSE MIB +0.4% at 22846 , SMI +0.1% at 8979, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices trade higher across the board following a mixed session in Wallstreet overnight and mixed markets in Asia. On the corporate front, EON trades higher after results and guidance, with other notable risers including Antofagasta, RWE, Aurubis, Geberit, while Illiad, Hannover Re, Telit and Greencore trade lower after results and updates. Veolia trades lower after the Qatari Diar divested its stake; In the states shares of Qualcomm will be in focus after receiving a presidential order prohibiting Broadcom's proposed takeover. Looking ahead notable earners include Dick Sporting Goods, HD Supply and DSW.

Movers

Consumer Discretionary [ Greencore [GNC.UK] -23% (Profit warnings)]

Industrials [Antofagasta [ANTO.UK] +2.6% (Earnings), Aurubis [NDA.DE] +3.6% (Earnings), Geberit [GEBN.CH] +1.2% (Earnings)]

Financials [ Hannover Re [HNR1.DE] -3.5% (Earnings)]

Telecom [Telit Communications [TCM.UK] -3.4% (Business update), Illiad [ILD.FR] -6.6% (Earnings)]

Materials [Wacher Chemie [WCH.DE] -3.4% (Earnings)]

Utilities [Veolia [VIE.FR] -2.3% (Qatari sovereign wealth developer sell entire stake)] -Energy [RWE [RWE.DE] +0.8% (Earnings), EON [EOAN.DE] +5.6% (Earnings)]

Speakers

ECB's Coeure (France): Cryptocurrencies are poor imitations of money

EU's Juncker stated that he saw an increase urgency in Brexit negotiations and reiterated that PM May must give more clarity. Solid draft text of UK withdrawal pact exists and believed the UK will regret its Brexit decision. Brexit must mean no change for citizens in Irelands and reiterates that the EU stood firm and united on the issue

EU Dombrovskis reiterated the view that EU was prepared to react to US tariffs

EU might avoid US tariffs if certain conditions were met. Exemption could come if EU was considered a reliable partner in addressing over capacity and other criteria

Italy Northern League leader Salvini (euro-skeptic) stated that EU policies were crazy and suicidal but did not foresee any unilateral, improvised exit from the Euro

Italy Northern League official Giorgetti: Likely a 50% change of another election this year - Germany BDI Industry Association: Companies needed to prepare for a hard Brexit

South Africa Fin Min Nene: Need to keep debt at sustainable level. Working towards revising higher GDP growth forecasts. Met with senior Moody's sovereign analyst in London; hard to read their body language. Land expropriation will be handled responsibly but can be abused by populists

Taiwan Central Bank: Domestic inflation seen stable; Jan-Feb CPI being mild. Market liquidity had been ample. TWD currency REER lower than China's Yuan, Korean Won and Singapore Dollar. Real interest rates higher than major economies

Iran said to increase its oil production to repay Chinese investors. Believed that OPEC to agree on the production increase

Currencies

USD was little changed against the major European FX pairs with the focus turning to US CPI data. However analysts believed it would unlikely alter expectations for Fed policy for the time being.

GBP/USD was softer ahead of Chancellor of Exchequer Hammond (Fin Min): Spring Statement but dealers noting the commentary seem more likely to help the gilts as less issuance is expected to be announced for the current fiscal year (thanks to higher tax receipts).

USD/JPY was higher by 0.6% above the 107 area for its best session in 5 months with the USD aided by the US Treasury auction results on Monday that showed the highest 3-year bond yield since 2007. Dealers noted that the Japan’s political situation warranted a close watch as historically the JPY currency tended to trive on political turmoil. Japan Fin Min Aso mighty skip G20 finance minister meeting in Buenos Aires later this month with calls for his resignation following the recent firestorm surrounding the cover-up of the govt land sale

Fixed Income

Bund Futures trade 17 ticks higher at 157.46 ahead of the DMO update on Gilts issuance. Upside targets 157.75, while a return lower targets the155.50 level.

Gilt futures trade at 122.38 up 12 ticks with little reaction to UK Trade and production data. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.896T from €1.898T prior. Use of the marginal lending facility stayed steady €0M.

Looking Ahead

(AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave the 7-Day Repo Reference Rate unchnaged at 27.25%

06:00 (US) Feb NFIB Small Business Optimism: 107.1e v 106.9 prior

06:00 (EU) Daily Euribor Fixing - 06:00 (SI) Slovenia to sell bills

06:00 (IT) Italy Debt Agency (Tesoro) to sell combined €7.25-8.75B in 2020, 2025, 2033 and 2047 BTP Bonds

06:15 (CH) Switzerland to sell 3-month Bills

06:30 (EU) ECB allotment in 7-Day Main Refinancing Tender (MRO)

06.30 (UK) Weekly John Lewis LFL sales data

06:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills; Avg Yield: % v 0.00%prior; Bid-to-cover: x v 1.71x prior (Mar 6th 2018)

07:00 (TR) Turkey to sell 12.2% Fixed Rate 2023 Bonds; Yield: % v 12.47% prior

07:00 (IE) Ireland Jan Industrial Production M/M: No est v 3.0% prior; Y/Y: No est v 3.0% prior

07:00 (IL) Israel Feb Trade Balance: No est v -$1.4B prior

07:00 (ZA) South Africa Jan Manufacturing Production M/M: 0.2%e v 1.1% prior; Y/Y: 2.5%e v 2.0% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

07:45 (US) Daily Libor Fixing - 08:00 (IS) Iceland Feb Unemployment Rate: No est v 2.4% prior

08:00 (BR) Brazil Jan Retail Sales M/M: +0.5%e v -1.5% prior; Y/Y: 3.5%e v 3.3% prior

08:00 (BR) Brazil Jan Broad Retail Sales M/M: +0.2%e v -0.8% prior; Y/Y: 6.2%e v 6.4% prior

08:00 (RU) Russia announces weekly OFZ bond auction

08:30 (US) Feb CPI M/M: 0.2%e v 0.5% prior; Y/Y: 2.2%e v 2.1% prior

08:30 (US) Feb CPI Ex Food and Energy M/M: 0.2%e v 0.3% prior; Y/Y: 1.8%e v 1.8% prior

08:30 (US) Feb CPI Index NSA: 248.929e v 247.867 prior; CPI Core Index : 255.749e v 255.287 prior

08:30 (US) Feb Real Avg Weekly Earnings Y/Y: No est v 0.4% prior; Real Avg Hourly Earning Y/Y: No est v 0.8% prior

08:30 (UK) Chancellor of Exchequer Hammond (Fin Min): Spring Statement; to provide govt's half-yearly update of Britain's public finance figures (Debt Management Office expect to cut FY18/19 issuance from £118.7B to £98.2B)

08:55 (US) Weekly Redbook Sales

09:05 (UK) Baltic Dry Bulk Index

10:00 (EU) Weekly ECB Forex Reserves

10:00 (MX) Mexico Jan Industrial Production M/M: 0.4%e v 0.9% prior; Y/Y: 0.4%e v -0.7% prior, Manufacturing Production Y/Y: 2.1%e v -0.1% prior

10:00 (IT) Italy Five Star Part Ledaer Di Maio

10:30 (CA) Bank of Canada (BOC) Gov Poloz

10:45 (UK) BOE APF Gilt purchase operation

13:00 (US) Treasury to sell $13B in 30-Year Bonds Reopening

16:30 (US) Weekly API Oil Inventories

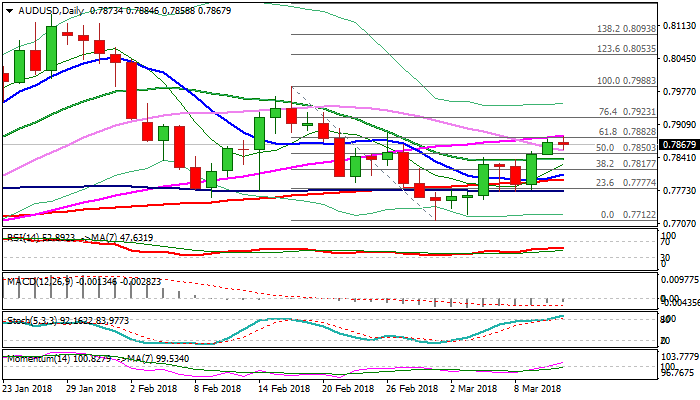

Technical Outlook: AUDUSD – Consolidation Under 55SMA Is Expected Before Bulls Resume

The Australian dollar holds in narrow consolidation under new two-week recovery high at 0.7884, posted after rally of past two days.

The action was capped by 55SMA / Fibo 61.8% of 0.7988/0.7712 descend, with signals that bulls may take a breather here. Strongly overbought slow stochastic supports the notion, but without firmer bearish signal so far.

Strong momentum studies and daily MA’s in bullish configuration, favor further advance. Close above 55SMA / Fibo barrier will be bullish signal for extension towards 0.7923 (Fibo 76.4%).

Meanwhile, the price may hold in consolidation with strong support at 0.7837 (sideways-moving 20SMA) expected to contain and keep bulls intact intact.

Conversely, close below 20SMA would weaken near-term structure and risk return to key support at 0.7817 (daily cloud base).

US CPI data are eyed for fresh signals.

Res: 0.7884, 0.7923, 0.7935, 0.7983

Sup: 0.7856, 0.7837, 0.7817, 0.7798

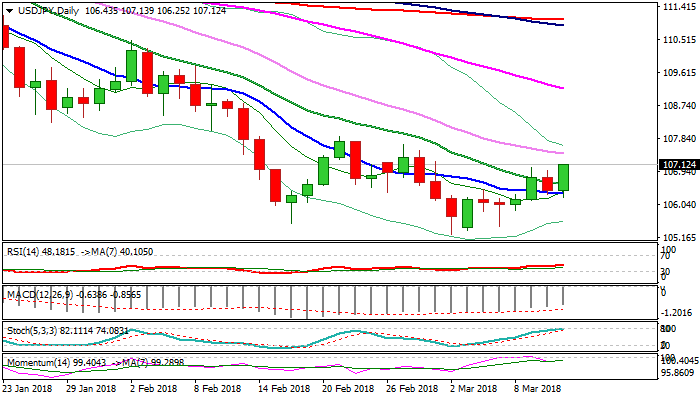

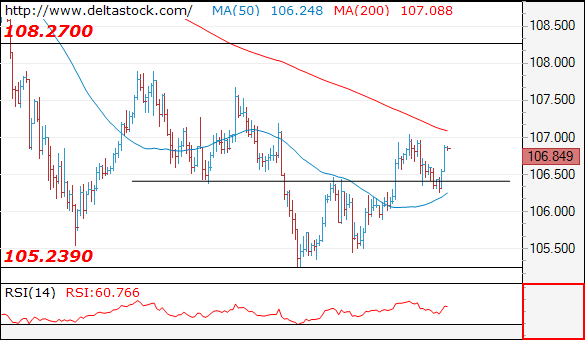

Technical Outlook: USDJPY – Firm Break Above 107 To Generate Bullish Signal

The pair is up on Tuesday, lifted by higher Nikkei and pressuring again 107 resistance zone, which capped upside attempts in past two days.

Sustained break above 107 (top of congestion that extends into third day) would generate fresh bullish signal for extension of recovery from 105.24 towards tops at 107.67 (27 Feb) and 107.90 (21 Feb) which mark the upper breakpoints.

Lift above 20SMA (106.61) today was bullish signal as broken 10SMA (106.34) holds the downside for the second day.

Momentum RSI turned north and underpin, but overbought slow stochastic could be an obstacle for fresh bulls.

Dips should remain above broken 20SMA to keep bullish near-term bias.

Return below 20SMA would weaken the structure while break and close below 10SMA would generate stronger bearish signal.

Res: 107.43, 107.67, 107.90, 108.48

Sup: 107.00, 106.61, 106.34, 106.15

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

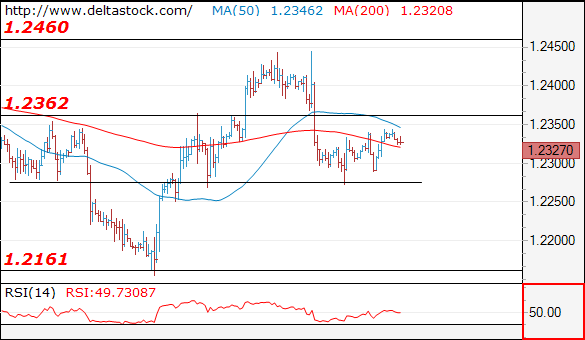

EUR/USD

Current level - 1.2327

The resistance at 1.2360 should provoke a slide towards 1.2160 lows.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2360 | 1.2460 | 1.2280 | 1.2160 |

| 1.2460 | 1.2560 | 1.2160 | 1.2090 |

USD/JPY

USD/JPY

Current level - 106.84

The intraday bias is positive after the failure at 106.30, for a rise towards 107.60.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.60 | 108.30 | 106.30 | 105.20 |

| 108.00 | 110.40 | 105.85 | 102.40 |

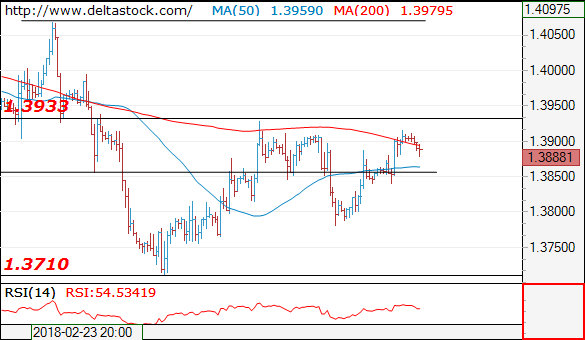

GBP/USD

Current level - 1.3881

My outlook is counter-trend against 1.3930 resistance, for a break through 1.3840 crucial low, towards 1.3710.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3930 | 1.4060 | 1.3840 | 1.3710 |

| 1.3930 | 1.4280 | 1.3780 | 1.3620 |

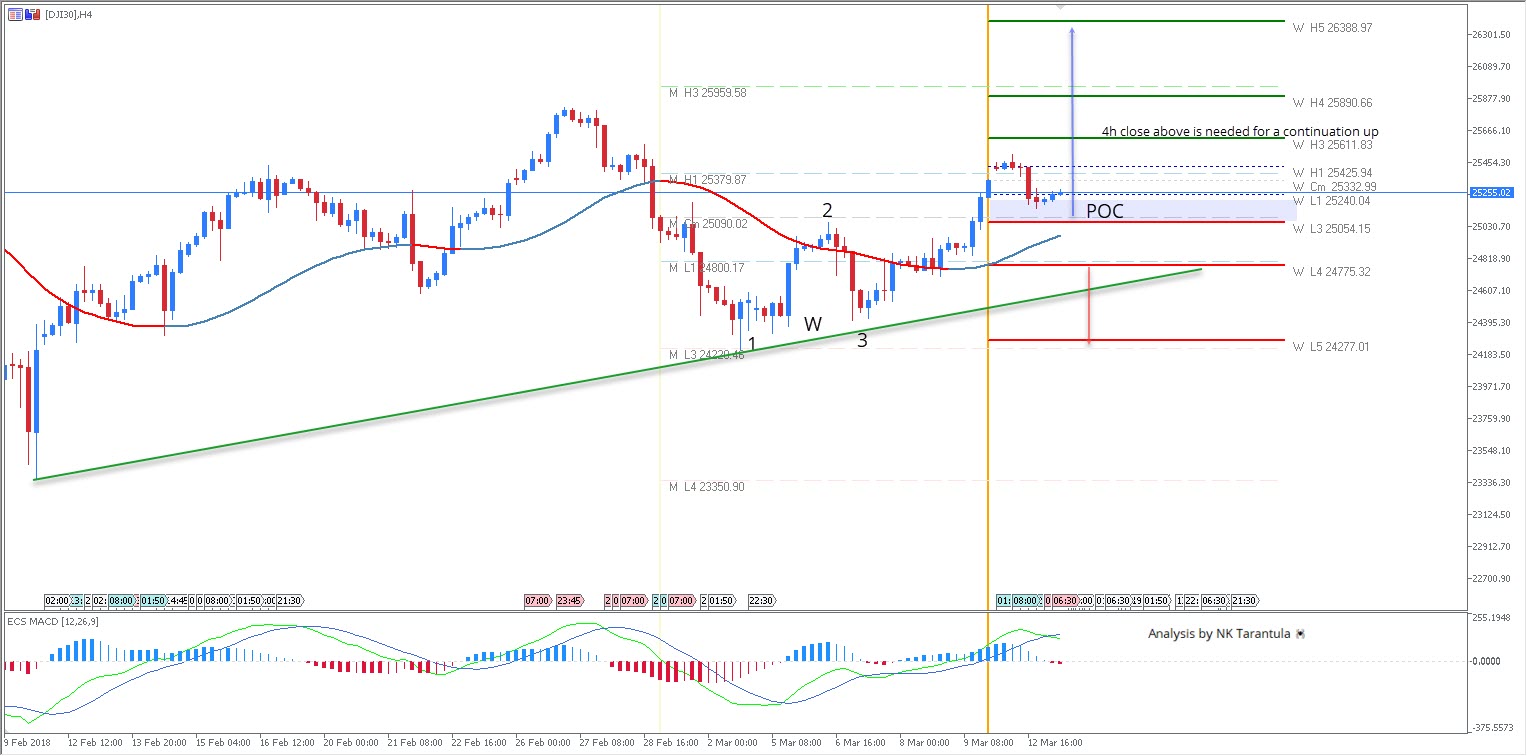

DJI30 Technical W Bullish Pattern Formed In 4h Time Frame

Even though income data was lower than expected in the US, the high NFP number suggests wage pressure may be imminent on company earnings in the USA – one of the reasons why the DJI30 was sold yesterday. The price might reject from the POC zone 25054-25240 as we see a strong confluence of technical levels and W 1-2-3 bullish pattern. Point 2 of W pattern sits precisely at M Cm (monthly camarilla level) and should keep the pair supported. However the index needs to make a 4h close above W H3 – 25611 to proceed further up towards 25890-959. Initially, the price might reject from the level. Above 25960, the target is 26388.

A drop below W L4 -24775 and the price might go further down towards the trend line and 24277

W H3 -Weekly Camarilla Pivot (Weekly Interim Resistance)

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

M H4 - Monthly Camarilla Pivot (Very Strong Monthly Resistance)

M L3 – Monthly Camarilla Pivot (Monthly Support)

M L4 – Monthly H4 Camarilla (Very Strong Monthly Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)