Sample Category Title

EURUSD Intraday Analysis

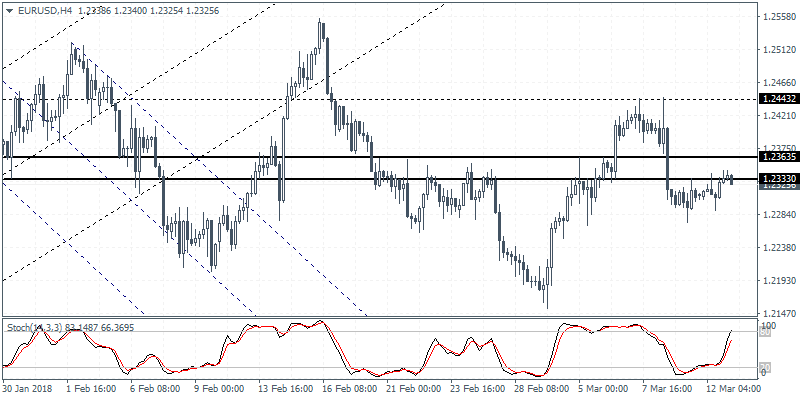

EURUSD (1.2325): The EURUSD was see trading with Friday's range with price action forming an inside bar. The breakout from the inside bar could potentially indicate the near term bias. We expect to see EURUSD continuing to push lower following the consolidation at the resistance level at 1.2333 - 1.2635. The downside target towards 1.2090 remains in play as long as the resistance level holds the gains in the near term. A convincing close above the resistance level could shift the bias to the upside with the common currency likely to target 1.2443.

USD Trades Flat With Inflation Data In Focus

Lack of fundamentals on a quiet trading day left the U.S. dollar to trade flat following Friday's decline. However, the USD was seen trading mixed across the board especially with the commodities turning weaker on the day.

Looking ahead, the inflation data coming out today will be a major event to watch with both headline and core inflation rate expected to rise at a slower pace compared to January's solid gains. On an annual basis, headline CPI is expected to rise slightly while core CPI is expected to remain flat at a pace of 1.8%.

Elsewhere, the BoC Governor Poloz is expected to speak later in the afternoon followed by second tier data from Japan.

GBPUSD Strongly Bullish Above 1.3920 Level

The British pound has continued to push higher against the U.S dollar, although price-action has so far struggled to make gains above the 1.3900 resistance area. The GBPUSD pair is currently trading around the 1.3890 support level, with buyers now looking for a major technical breakout above the 1.3920 level. Traders look to the release of the UK Budget, where the UK Treasury Chancellor presents the economic forecast for next year, containing details about GDP growth estimates, spending and borrowing forecasts as well as fiscal stimulus.

The GBPUSD pair remains intraday bullish above 1.3890 level, further upside towards 1.3920 and 1.3974 seems possible.

A sustained move below the 1.3890 level may lead to a GBPUSD price-correction back towards the 1.3833 support level.

EURUSD Bulls Still In Control Above 1.2305 Level

The euro continues to post fresh intraday trading highs against the greenback, with price-action reaching an overnight high of 1.2345, as the U.S dollar index comes under slight selling pressure. The EURUSD is now trading around the 1.2320 level, after falling back below the 1.2334 level, with the pair still retaining a bullish bias whilst price-action holds above the 1.2305 support level. Traders also remain cautious, ahead of the release of today’s key CPI inflation report from the United States economy.

The EURUSD pair retains a bullish bias whilst trading above the 1.2305 level, with further gains towards the 1.2367 and 1.2400 levels seems possible.

Should the EURUSD pair move below the 1.2305 level, sellers will likely target the 1.2278 and 1.2239 support levels.

US CPI Data In Focus On Tuesday

Economic data takes the spotlight once again on Tuesday, with US inflation figures likely to generate most of the chatter.

Like on Monday, the European release schedule is relatively light on Tuesday. The French government will report on nonfarm payrolls at 06:00 GMT. The report is expected to show employment growth of 0.3% in the fourth quarter.

Two hours later, the Spanish government will report on consumer inflation for the month of February. This includes the monthly consumer price index (CPI) as well as the harmonized index of consumer prices (HICP). The HICP reading is expected to come in at 1.2% annually.

Shifting gears to North America, the US Department of Labor will release its February CPI report at 12:30 GMT. Annual CPI is forecast to strengthen to 2.2%, compared with 2.1% the previous month. So-called core inflation, which strips away volatile goods such as food and energy, is expected to come in at 1.8% year-over-year.

Another month of rising inflation will almost assuredly compel the Federal Reserve to continue raising interest rates sooner rather than later. The Fed is scheduled to hold its next policy meeting on 20-21 March, where officials are widely expected to raise rates for the first time since December. The March policy statement will be delivered alongside quarterly economic projections covering GDP, unemployment and inflation.

North of the border, the Bank of Canada’s Stephen Poloz will deliver a speech at 14:30 GMT. Last week, the BOC kept interest rates on hold amid growing trade risks involving the United States.

Energy traders will also keep tabs on weekly inventory data courtesy of the American Petroleum Institute (API). The API report will be released at 20:30 GMT.

USD/CAD

The US dollar rose against its northern counterpart on Monday, although gains were limited by ongoing geopolitical risks involving the Trump administration. The USD/CAD touched a session high of 1.2844 on Monday and has since backtracked slightly. The pair is now trading at 1.2836, where it is coming up against a firm resistance. On the opposite side of the ledger, immediate support is likely found at 1.2800.

EUR/USD

Europe’s common currency traded sideways on Monday, as investors continued to assess dovish comments from ECB President Mario Draghi. The pair is currently trading around 1.2340. Immediate resistance is located at 1.2380. On the flipside, support is located near 1.2270, the 50-day SMA.

AUD/USD

The Australian dollar edged slightly higher on Tuesday following stronger than expected business data. However, gains remain capped ahead of headline CPI data out of Washington. At the time of writing, the AUD/USD exchange rate was up 0.1% at 0.7882. Immediate support is located around the 0.7820 level. Prices are coming up on an important resistance band near the psychological 0.7900 level.

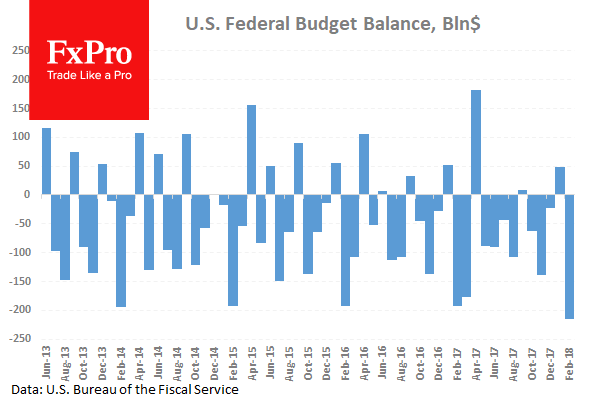

Forex Analysis: US Monthly Budget Experiences Biggest Decline Since February’14

The US Monthly Budget Statement (Feb) was $-215B v an expected $-216B, against a reading of $49.0B in the prior month. This data represents the balance of the federal government’s income and spending. The February number was the biggest decline in the budget since February of 2014. Seasonally, the February data is lower than other months due to variations that occur at this time of year and events that settle during the month. Receipts are at their lowest in this reading each year, while, for outlays, it is one of the highest, leading to a disparity. USDJPY sold off from 106.538 to 106.310 because of this data release.

New Zealand RBNZ Governor Grant Spencer gave a speech titled “Getting the best out of macro-prudential policy” at the Reserve Bank of New Zealand. He made the following comments: The RBNZ is to review macro-prudential policies with the Treasury. He is keen to see macro-prudential develop as a credible and sustainable policy.

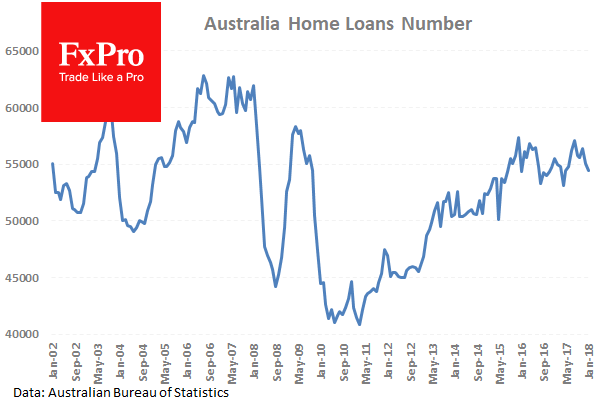

Australian Home Loans (Jan) came in at -1.1% v an expected -0.1%, against a previous -2.3%. This is a volatile data point, with recent extremes between +5 and -6. This result shows a contraction in the number of loans for home purchases. Also released at this time was Investment Lending for Homes (Jan) data, coming in at 1.1% against a previous -2.6%. AUDUSD fell from 0.78743 to a low of 0.78661 after this data.

Japanese Tertiary Industry Index (MoM) (Feb) came in at -0.6% against an expected -0.2%, from 0.0% previously, which was revised up from -0.2%. A lower than expected result is a slight worry for future economic health but inside recent ranges for this data point. USDJPY moved higher from 106.593 to 106.838 after this data was published.

EURUSD is down -0.04% overnight, trading around 1.23290.

USDJPY is up 0.42% in early session trading at around 106.856.

GBPUSD is down -0.13% this morning, trading around 1.38860.

Gold is down -0.28% in early morning trading at around $1,319.28.

WTI is down -0.19% this morning, trading around $61.15.

Market Update – Asian Session: Markets Muted Ahead Of US CPI

Headlines/Economic Data

General Trend:

Asian equities trade directionless after mixed US session

Japanese equities pare losses

China shakes up structure of its ministries and government departments: Move seen as attempt to limit bureaucracy and strengthen the leadership of Communist Party

National Australia Bank (NAB) suggests Feb Australia business confidence weighed down by financial market turbulence

South Korea Finance Ministry puts size on planned 50-year bond sale

Volatility in currency market subdued ahead of US Feb CPI data

China Feb Fixed Asset Investment, Industrial Production and Retail Sales due on Wednesday

Japan

Nikkei 225 opened -0.4%; closed +0.7%

TOPIX Iron & Steel Index -0.7%; Electric Appliances

(JP) Japan Fin Min Aso may skip G20 finance minister meeting in Buenos Aires this month – press

(JP) Japan Fin Min Aso: Documents seem to be falsified to fit Sagawa's testimony; will depend on Parliament situation if I will attend G20

(JP) Japan Feb PPI (CGPI) M/M: 0.0% v 0.2%e; Y/Y: 2.5% v 2.5%e

(JP) According to NHK poll PM Abe cabinet approval rating fell to 44% v 46% in Feb

(JP) Japan MoF sells ¥2.2T v ¥2.2T indicated in 0.10% (prior 0.1%) 5-yr bonds; avg yield -0.108% v -0.093% prior; bid to cover 4.18x v 4.67x prior

Looking Ahead: Bank of Japan Jan Policy Meeting Minutes due for release on Wednesday

Korea

Kospi opened flat

(KR) North Korea leader Kim Jung-un would like to sign peace treaty with US and establish diplomatic relations including a US embassy in Pyongyang - financial press

(KR) South Korea Deputy PM Kim: Concerning the US tariffs on steel imports, the Govt will devote all its energy through every available channel in order to get them lifted - Korean press

(KR) South Korea to offer KRW300B in 50-yr bonds on March 15th

China/Hong Kong

Hang Seng opened -0.1%, Shanghai Composite -0.1%

Hang Seng Telecom Index -1.4%, Energy -1.4%, Property/Construction -0.5%; Financials +0.2%

(CN) China proposes to give PBOC some functions currently held by CBRC and CIRC and merge the insurance and banking regulators

(CN) China PBoC Open Market Operation (OMO): Injects CNY60B v CNY90B prior in 7 and 28-day reverse repos; Net injection CNY60B v CNY90B prior

(CN) PBOC sets yuan reference rate at 6.3218 v 6.3333 prior

(HK) Hong Kong new home supply expected to reach 20K units (15-yr high) - HK press

(CN) Shanghai and Shenzhen stock exchanges considering delisting companies for serious law violations – Xinhua

(CN) China Banking Regulatory Commission (CBRC) and four other regulators planning to expand capital tools for commercial banks to replenish their capital in order to boost their support for the real economy – Xinhua

(CN) China National Development and Reform Commission (NDRC) approves 3 coal projects: Approves CNY3.4B coal mine project in Inner Mongolia, capacity of 6Mt/yr

(CN) China State Assets Supervision and Administration Commission (SASAC) official Xiao: China seeks to ensure and increase value of state assets

Looking Ahead: China Feb Fixed Asset Investment, Industrial Production and Retail Sales due for release on Wednesday

Australia/New Zealand

ASX 200 opened +0.5%; closed -0.5%

ASX 200 Resources Index -1.2%, Telecom -1%, Energy -0.7%, Financials -0.4%

(NZ) RBNZ Acting Gov Spencer: Macro-prudential policy ultimately can't control the housing cycle

(NZ) New Zealand sells NZ$2.0B in 3.0% April 2029 bonds, avg yield 3.135%

(AU) Australia sells A$150M in 2027 indexed bonds, avg yield 0.8208%, bid to cover 3.07x

(AU) AUSTRALIA JAN HOME LOANS M/M: -1.1% V -0.2%E; INVESTMENT LENDING: +1.1% V -2.6% PRIOR; Owner occupier home loan value m/m: +1.1% v -1.0% prior

(AU) Australia Feb NAB Business Confidence: 9 v 11 prior; Conditions: 21 v 18 prior

Other Asia

(ID) Indonesia Energy Ministry: Revises effective date for new coal price to March 12th (prior Jan 1st)

(ID) S&P: Reiterates sees no sovereign ratings upgrade for Indonesia in the next 12-24 months, reminder May of 2017 S&P raised the rating to B from BBB-, Outlook stable

North America

US equity markets ended mixed: Dow -0.6%, S&P500 -0.1%, Nasdaq +0.4%, Russell 2000 +0.3%

S&P500 Industrials -1.2%; Real Estate +0.5%

(US) House Intel member Conaway: House panel finds no Russia collusion with Trump

QCOM, [-4.2% after hours], White House announces President Trump will not allow Broadcom takeover of Qualcomm - press

Looking Ahead: US Feb CPI data due for release, along with Weekly API Crude Oil Inventories

Europe

(US) Sec of State Tillerson: Extremely concerned about Russia, UK poisoning an egregious act and will trigger a response, not sure if Russia was involved

Looking Ahead: UK OBR expected to issue Spring Forecasts, while Chancellor Hammond is expected to issue the Spring Statement

Levels as of 01:00ET

Hang Seng -0.0%; Shanghai Composite -0.2%; Kospi +0.1%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.0%, Dax +0.1%; FTSE100 +0.1%

EUR 1.2345-1.2325; JPY 106.85-106.26; AUD 0.7884-0.7866;NZD 0.7323-0.7292

Apr Gold -0.04% at $1,320/oz; Apr Crude Oil -0.2% at $61.27/brl; May Copper -0.1% at $3.12/lb

Today All Eyes Are On Inflation

Market movers today

Market focus today is on the US CPI core inflation numbers for February, which we expect to come in at 0.2% m/m (1.8% y/y, down from 1.9% y/y in January). We do not think one should read too much into a few releases that came out more strongly than expected, as there is usually some noise in the data.

We recently published a thematic five part series of papers on the theme ‘is inflation finally coming and implications for markets?'. Concerning today's CPI print, we argued in Part 1: Global Inflation: US stimulus and closing output gaps pose upside risk, 26 February, that there are upside risks for US core inflation due to more expansionary fiscal policy but that it will take time for this to materialise.

Luigi Di Maio, leader of Five Star Movement , is due to hold a news conference today at 15:00, which could give some more insight into Five St ar's plans following the inconclusive elect ion result .

Selected market news

This week started quietly. There were only slight developments in the protectionist narrative emanating from Washington. Today all eyes are on inflation.

The European Union is making an at tempt to exempt itself from US steel and aluminium tariffs, while maintaining that it will not cave into bullying.

As the EU deliberates, US President Donald Trump does not . He retorted that his Secretary of Commerce Wilbur Ross will talk to the EU concerning its ‘large tariffs and barriers', which are ‘not fair to our farmers and manufacturers'. The US has come a long way from President Theodore Roosevelt , who prescribed US foreign policy as ‘talk softy and carry a big stick'.

Wilbur Ross and Peter Navarro are two of the architects of current US mercantilist trade policy that is predicated on trade being a zero-sum game. As in checkers (draughts), your loss is my gain. In such a game, current account surpluses serve the national interest. In addition, Navarro and Ross hold that a strong manufacturing sector is a quest ion of national security. We do not expectsanctions to escalate into a full blown trade war. We dive into US tariffs in Research US – Symbolic protectionism with limited impact on growth and inflation but risks remain , 7 March.

JPY broad downside bias, NZD broad upside bias in hourly chart

Yen is building up broad biased downside bias in hourly chart.

NZD is building up broad based upside bias in hourly chart.

Net effect is: NZD/JPY jumping sharply to as high as 78.26 so far. 38.2% retracement of 81.55 to 75.92 is finally firmly taken out. 78.07. We'd now looking at 61.8% retracement at 79.39.

RBA Key Economic Indicators Snapshot

RBA Key Economic Indicators Snapshot

As at March 12, 2018

- Cash rate: 1.5%

- Economic growth: 2.4%

- Inflation: 1.9%

- Unemployment rate: 5.5%

- Employment growth: 3.3%

- Wage growth 2.1%

- Average weekly earnings: AUD 1192

- Household saving ratio: 2.7%

- Net foreign liabilities: 55% of GDP

- AUD 1 = USD 0.79

- China GDP growth: 6.8%

- G7 GDP growth: 2.3%