Sample Category Title

EU Juncker: Increasing urgency on Brexit negotiation

European Commission President Jean-Claude Juncker in European Parliament on Brexit:-

- "There is increasing urgency to negotiate this orderly withdrawal."

- "As the clock counts down, with one year to go, it is now time to translate speeches into treaties, to turn commitments into agreements."

- "It is obvious that we need further clarity from the UK if we are to reach an understanding on our future relationship."

Currencies: Soft ECB Speak Caps EUR/USD Topside

- Rates: US CPI won't shift thinking about next week's FOMC

Focus turns to US CPI today. We don't think that the outcome, even in case of a disappointment, will dramatically shift expectations about next week's Fed meeting. Greek bonds could outperform after yesterday's Eurogroup meeting, while SLOVGB's might underperform on the developing political crisis. BTP auctions are a good test for appetite. - Currencies: Soft ECB speak caps EUR/USD topside

The dollar was still looking for a clear direction yesterday. Soft ECB comments prevented a sustained rise in EUR/USD. The US CPI takes center stage today. A positive surprise might support the dollar, but it is not sure that this surprise will already come this month. Sterling is trading off recent lows as Brexit is (temporary) off the radar.

The Sunrise Headlines

US stock markets parted ways yesterday with only Nasdaq ending with gains. Risk sentiment on Asian stock markets is mixed overnight with China underperforming (-0.5%).

President Trump blocked Broadcom's $117 bn hostile bid for Qualcomm, capping moves by the Trump administration reflecting concerns about an intensifying arms race between the US and China over advanced technologies.

Slovakia's government edged towards break-up after one of the junior parties in the ruling coalition of PM Fico called for early elections to stem the furore over the murder of an investigative journalist. (FT)

China is merging its banking and insurance regulators and creating a slew of ministries including a new agricultural and rural affairs ministry as part of the biggest government shake-up in years

EMU creditors will disburse new loans to Greece this month and are working on debt relief measures, the head of the Eurogroup Centeno said. Those moves should help strengthen the Greek recovery.

Japan's FM Aso is considering skipping a G-20 finance leaders' gathering in Buenos Aires next week, Japanese media reported, as a suspected cover-up of a cronyism scandal paralyses parliament and puts his job on the line.

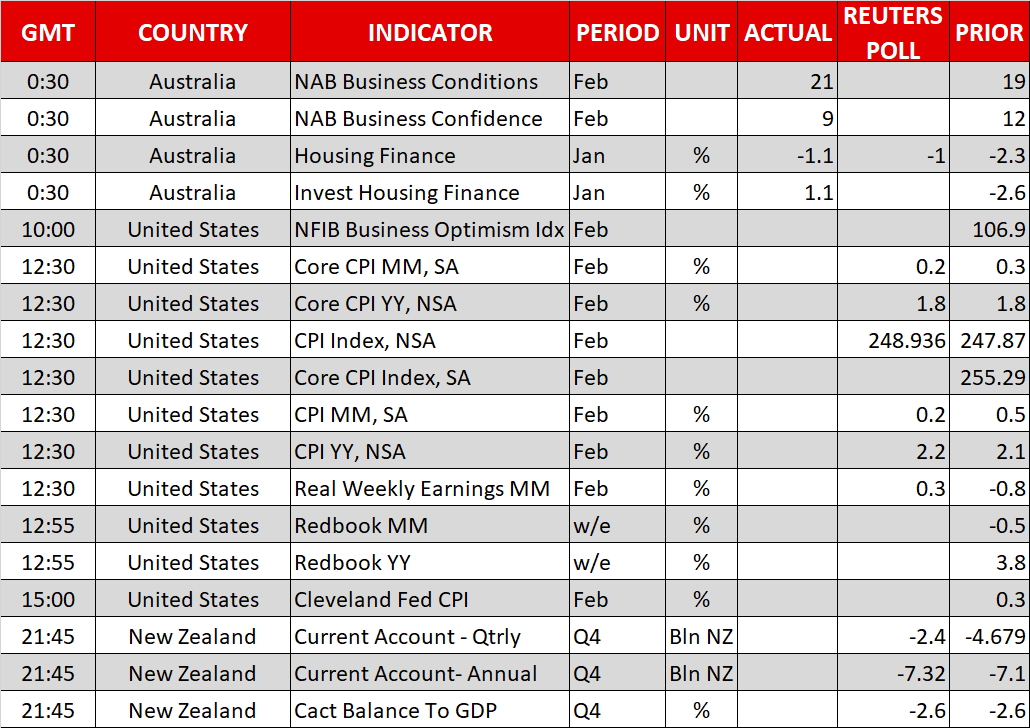

Today's eco calendar contains US NFIB small business optimism and US CPI data. The Netherlands, Italy and the US tap the bond market

Currencies: Soft ECB Speak Caps EUR/USD Topside

Soft ECB speak caps EUR/USD topside

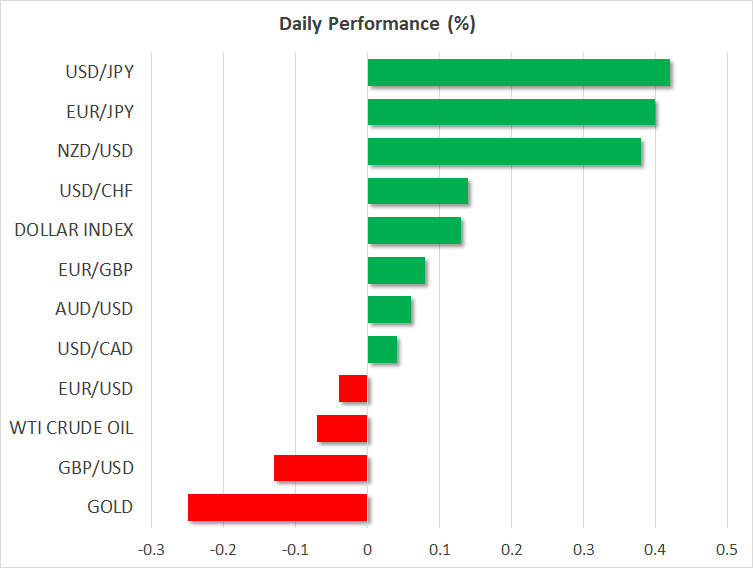

Risk sentiment stayed constructive yesterday after Friday's almost perfect payrolls. Still, the dollar didn't find a clear direction. EUR/USD hovered in the lower half of the 1.23 big figure. The topside in EUR/USD is apparently rather well protected as the market assumes that any ECB normalization will develop in a very gradual way. This was confirmed by soft comments from ECB Smets and Coeuré. EUR/USD closed the day at 1.2334. USD/JPY held in the mid 106 area. Overnight, Asian equities are trading mixed. Changes in the major indices are modest. Markets don't give too much weight to the political tensions in Japan. The Nikkei regained initial losses and this ‘propelled' USD/JPY. The dollar also regains a few ticks against the euro. The Aussie dollar is holding near it ST top (0.7875 area) on constructive eco data.

Today, the US NFIB small business confidence is interesting, but the focus will be on the February US CPI data. The consensus expects 0.2% M/M and 2.2% Y/Y (from 2.1%) for headline CPI. The core reading is expected unchanged at 1.8% Y/Y. We don't see much reason for a big positive surprise for the February data. This evening, the US treasury sells 30-yr bonds. Yesterday's sale of 10-y Treasuries was OK. For now, US data don't provide much new guidance for the dollar (and for interest rates) going into the March 21 Fed meeting. We also monitor comments from ECB members. In the wake of last week's ECB meeting (Draghi's comments were perceived soft), comments of ECB's Smets and Coeuré pointed in the same direction. So, ST a further decline in EUR/USD maybe has to come from the euro side of the story, rather than from the USD. Especially as the market is probably still positioned a bit euro long. The US tariffs/trade debate remains a wildcard.

The post ECB price action suggests that the EUR/USD topside is rather well protected. Constructive US eco data might cause a renewed EUR/USD test of the 1.2155 area.

Sterling traded with a cautiously positive bias yesterday. There are again no UK eco data today. Markets keep an eye at Fin Min Hammond's half year public finance update. Less focus on austerity might be a slightly positive for sterling, but it won't be a game-changer. For now there is no trigger for a clear directional move in EUR/GBP. Some further range trading near current levels might be in the cards.

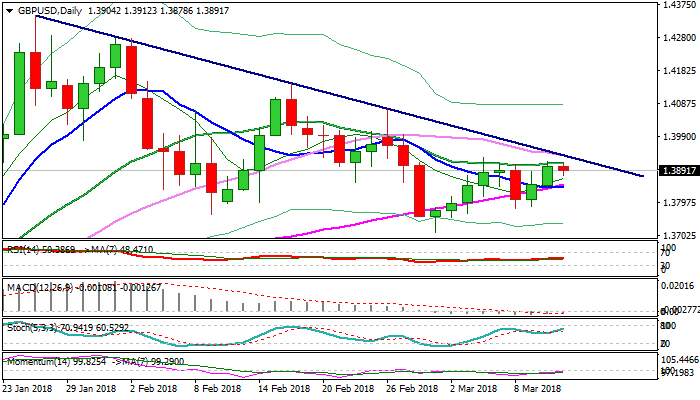

Technical Outlook: GBPUSD – 20 SMA Continues To Cap And Keep N/T Risk Skewed Lower

Cable ticked lower in early European trading after holding with narrow range in Asia and remains capped by 20SMA (1.3910) for the fifth straight day.

Bear-trendline off 1.4345 high lies just above (1.3934) and produces additional pressure.

Momentum studies are bullishly aligned but MA’s are mixed and RSI in neutral mode, lacking clearer direction signal.

Strong offers at 1.3910/30 zone keep the downside vulnerable and repeated failure to break higher could spark fresh weakness towards strong support at 1.3782 (daily cloud base).

Bullish scenario requires close above trendline resistance (also Fibo 61.8% of 1.4069/1.3711 bear-leg) to generate bullish signal for extension towards 1.40 zone (daily cloud top / psychological barrier.

UK’s Spring statement is key event for the pound today, as UK Finance Minister Hammond is expected to give more details about economic growth outlook for the Brexit-bound economy.

Also, release of US CPI data, due later today, would give fresh signals.|

Res: 1.3910, 1.3934, 1.3985, 1.4000

Sup: 1.3878, 1.3849, 1.3820, 1.3782

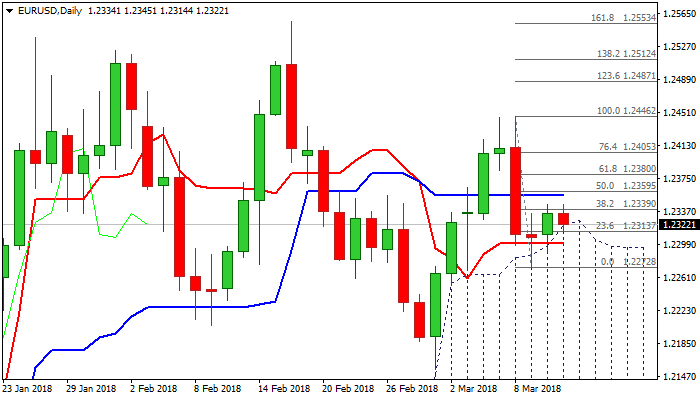

Technical Outlook: EURUSD Holds In Tight Range And Looks For Fresh Direction Signal

The Euro traded within tight range in Asia on Tuesday with the downside being held by rising 10SMA/top of thick daily cloud (1.2320) and the upside remaining capped for the third straight day by 20SMA (1.2340). Near-term action shows no clear direction as daily studies send mixed signals. Fresh momentum is conflicting mixed MA's and neutral RSI, suggesting the pair needs the catalyst for fresh direction signal. Rising daily cloud continues to underpin the action since the beginning of the month, but fresh upside attempts from 1.2272 (09 Mar low) face strong headwinds from 20SMA and sideways-moving daily Kijun-sen (1.2355). Bulls need firm break here to generate direction signal and spark further recovery of last week's strong fall from 1.2446. Initial negative signals could be expected on close below cloud top/10SMA, to expose 1.2300 support (sideways-moving daily Tenkan-sen) and 1.2272/53 (09 Mar low/rising 55SMA). With thin calendar for the European session, focus turns towards key event of the day, release of US inflation data. Forecasts signal that the CPI would fall in February which could be further blow for expectations of US Fed's more aggressive approach towards interest rates in 2018 and could further depress the greenback.

Res: 1.2340, 1.2355, 1.2380, 1.2400

Sup: 1.2320, 1.2300, 1.2272, 1.2253

Yen Weakens On Politics, All Eyes On US Inflation

Here are the latest developments in global markets:

FOREX: The dollar was trading higher versus a basket of currencies on Tuesday, posting notable gains against the yen in the midst of a political scandal in Japan that raises questions about the government’s ability to deliver moving forward.

STOCKS: US markets were mixed yesterday. The Nasdaq Composite closed 0.4% higher, reaching another record high, but the S&P 500 and the Dow Jones fell by 0.1% and 0.6% respectively. Futures tracking the Nasdaq 100, S&P and Dow are flashing green, pointing to a higher open, but the broader direction of these indices today will likely depend on the upcoming US CPI data. Asian benchmarks were mixed as well. Japan’s Nikkei 225 and Topix closed higher by 0.7% and 0.6% correspondingly, but the Hang Seng in Hong Kong was down by 0.3%. In Europe, futures tracking most of the major indices were in negative territory, but only marginally so.

COMMODITIES: Oil prices fell on Tuesday, with WTI and Brent crude declining by 0.1% and 0.2% respectively, both benchmarks extending losses from yesterday. The losses are being attributed to a report by the Energy Information Administration (EIA) which projected an increase in crude production from major US shale firms, reigniting concerns of an oversupplied market. Today, the weekly private API inventory data will be in focus, ahead of the official EIA figures tomorrow. In precious metals, gold prices declined by 0.25%, last seen around the $1318 per ounce handle. Today, the yellow metal will probably get its directional cue from any movement in the dollar, after the US CPI data.

Major movers: Yen declines as political scandal threatens government’s policies; antipodeans record fresh 2-week highs

The dollar index was 0.1% higher on Monday after shedding 0.2% the day that preceded. February’s CPI reading out of the US due at 1230 GMT, despite not being the Fed’s preferred measure of inflation, is still keenly awaited ahead of the central bank’s meeting next week and is likely to give short-term direction to the US currency.

Dollar/yen was up by 0.4% at 106.85, more than making up for yesterday’s decline. A scandal involving Japanese Finance Minister Taro Aso, a key individual in PM Abe’s government, is casting doubts over the government’s ability to deliver on its economic policy agenda moving forward; the incident is seen as threatening Shinzo Abe from securing a third term as leader of his party when a leadership vote takes place in September. The euro was also up by 0.4% against the Japanese currency, with euro/yen trading at 131.79.

Euro/dollar was little changed at 1.2324. The pair has been unable to make up for the losses incurred after ECB chief Mario Draghi struck a cautious tone on inflation in the euro area last Thursday, saying “victory can’t be declared yet on inflation.”

Sterling lost 0.1% versus the greenback, trading at $1.3887. The pair posted gains yesterday after junior Brexit minister Robin Walker said that the UK is very close to agreeing the details of an implementation period with the EU for its transition out of the bloc. Euro/pound was mostly unchanged after recording losses on Monday.

Aussie/dollar traded higher, though only marginally so, and kiwi/dollar was up by 0.4%. Both pairs posted fresh 2-week highs of 0.7884 and 0.7325 respectively. The aussie was lifted after the NAB’s index of business conditions rose to its highest on record in February, boosting optimism on the economy.

Day ahead: US inflation data to drive the dollar; UK Spring statement in focus with politics also in the spotlight

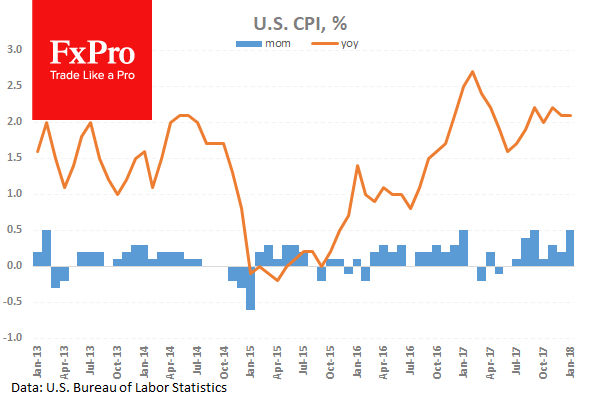

The main event today will be the release of the US CPI data for February at 1230 GMT. The forecast is for the headline CPI rate to tick up to 2.2% in yearly terms from 2.1% previously, while the core rate is projected to hold steady at 1.8%. These figures will be closely tracked ahead of next week’s Fed policy meeting, as they have the capacity to impact market expectations ahead of the gathering.

The latest set of US wage data – released on Friday – showed that wage growth remains subdued, easing pressure on the Fed to raise rates aggressively. Markets will be looking for a confirmation of this narrative today. If the CPI data disappoint as well, for example if the core rate surprisingly ticks down, then investors could scale back their expectations over how many hikes the Fed will deliver this year. Such an outcome would likely weigh on the dollar, but push US stock indices even higher. On the contrary, an upside surprise in the CPI prints could revive some inflation concerns and heighten speculation for a more aggressive rate path by the Fed, thereby helping the dollar to recover and simultaneously weighing on stocks.

In the UK, Chancellor Philip Hammond will address the Parliament at 1230 GMT in order to present the Spring budget statement. While this budget update is typically used to announce new policy measures, this is unlikely to be the case today, as major announcements have recently been reserved for the main budget, the Autumn statement. Instead, markets may look at the updated economic forecasts for the UK economy, while media reports suggest there may also be some details on the effects of the Brexit divorce bill on UK public finances, both of which could impact sterling.

More broadly, Brexit will likely remain a key driver for the pound over the remainder of the month. Junior Brexit minister Robin Walker said yesterday that the UK and the EU are very close to agreeing a transitional divorce deal, something the EU is expected to approve at its March 22-24 summit. Any comments from UK and EU officials ahead of the summit will probably be critical for sterling’s forthcoming direction.

In energy markets, investors will look to the private API inventory data at 2030 GMT, in order to gauge whether US production has really peaked for the time being, something signaled by the decline in the Baker Hughes oil rig count on Friday.

In politics, all eyes will be turned to the US, where a special election will be held in Pennsylvania for an open seat in the House of Representatives. While a single House seat is usually not very important in US politics, this time is different. Back in 2016, Trump and the Republicans won this district by a landslide, but opinion polls now suggest that the Republican and Democratic candidates are running neck and neck. If the Democratic contender wins, or comes close to winning, that would be a clear sign that the Republicans are at risk of losing districts they won easily in 2016. Such an outcome could heighten speculation that the Republicans may lose control of Congress at the mid-term elections later this year.

Technical Analysis: EURUSD looking neutral in the short-term

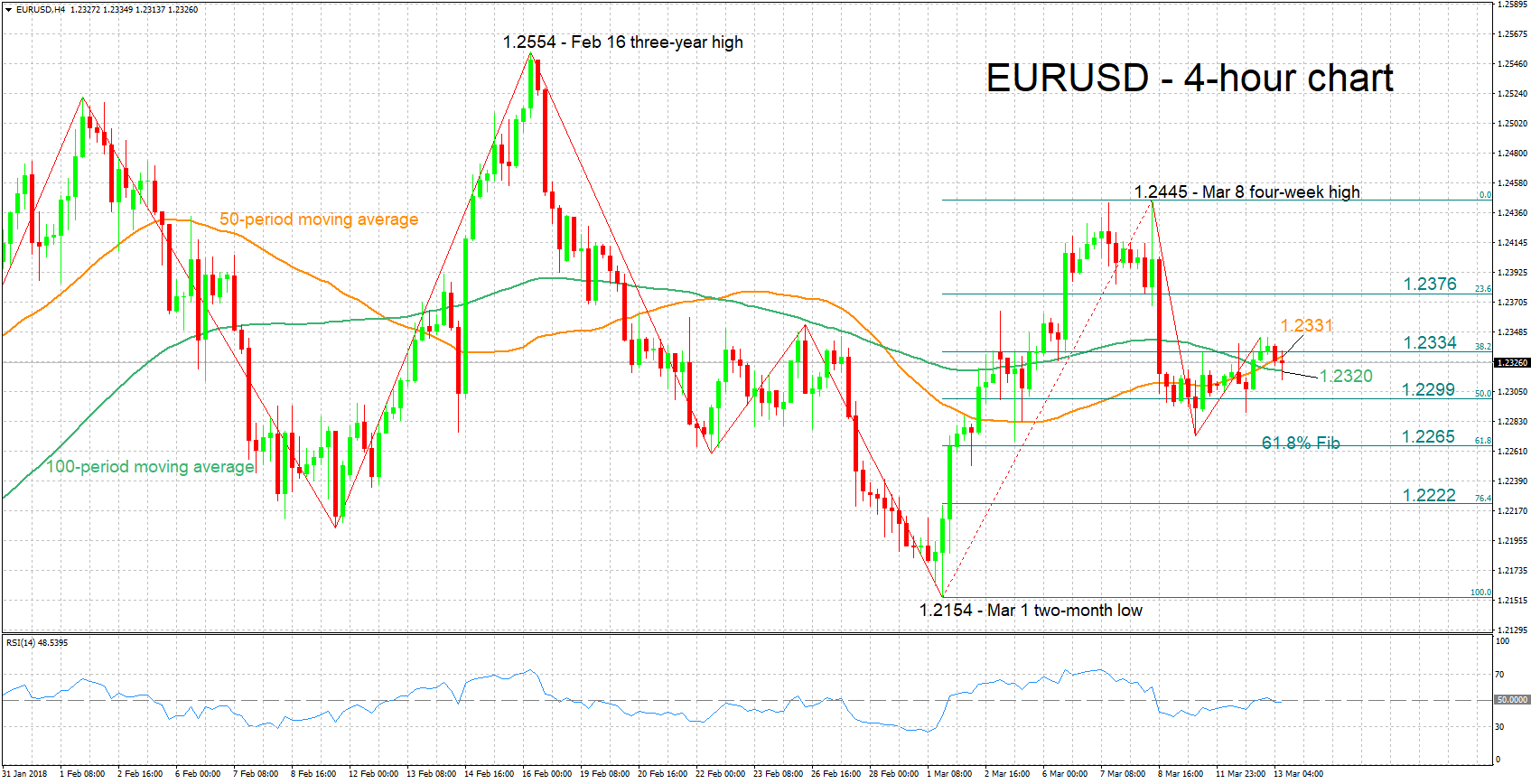

EURUSD has been ranging in recent days, moving within the 38.2% and 50% Fibonacci retracement level of the March 1 to March 8 upleg for the most part. The RSI has been largely moving sideways, pointing to a predominantly neutral picture in the short-term.

Stronger-than-expected CPI figures out of the US today, might lead market participants to price in a more aggressive Fed tightening cycle and thus lead to dollar strength. Euro/dollar might find support around the 100-period moving average at 1.2320 in this case – price action is taking place close to this level at the moment – with steeper declines bringing into view the range around the 50% Fibonacci level at 1.2299, including the 1.23 handle that may be of psychological significance.

If the readings disappoint though, euro/dollar could head higher. Resistance could be taking place at the moment in the area around the 50-day MA and the 38.2% Fibonacci mark, ranging from 1.2331 to 1.2334. A move above would turn the attention to the 23.6% Fibonacci level at 1.2376.

It is notable that despite prospects of more Fed rate hikes being theoretically dollar-positive, there are other currency drivers at play that might act to the detriment of the dollar. Market participants seem to be increasingly wary of these drivers.

GBPUSD Still In Bearish Correction Mode, Maintains Weak Bias In Near Term

GBPUSD has been holding in a short-term valid descending trend line since January 25. The pair struggled below the 20 and 40 simple moving averages near 1.3900 and 1.3960 respectively. The bearish correction seems to still be in progress, however, the technical indicators are holding in a neutral territory.

In the daily timeframe, the MACD oscillator jumped above its trigger line and posted a bullish crossover but is still standing below the zero line. Moreover, the RSI is flattening near the 50 level with no clear signal for further upside or downside move in price action.

In case of a penetration below the 23.6% Fibonacci retracement level of 1.3810, this could open the path back to the 1.3710 support level. Breaking this level, the next immediate barrier is near the 1.3660 level. Further losses could push the pair lower towards the medium-term ascending trend line near 1.3620, which has been holding over the last past year.

Conversely, a climb above the downtrend line and the SMAs could drive GBPUSD towards the 1.4070 resistance level. Jumping above this area could drive the pair to the 1.4150 resistance level taken from the peak on February 16.

US Consumer Price Index Takes Centre Stage

At 11:30 GMT, the UK Budget Report will be released. This is a mini-budget and outlines the government’s updated budget for the fiscal year, including infrastructure and spending projections, public finance forecasts and potential tax reforms. It is likely that the data will reveal an improvement in the public finances. Analysts will look to the assessment of productivity growth, which was cut in November, the state of the public finances and news on tax reform. GBP may be affected by this report.

At 12:30 GMT, US Consumer Price Index (YoY) (Feb) data will be released, with an expected reading of 2.2% against 2.1% previously. Consumer Price Index Ex Food & Energy (YoY) (Feb) data will be released and is expected to be unchanged at 1.8%. Consumer Price Index Ex Food & Energy (MoM) (Feb) data will be released, with an expected reading of 0.2%, against 0.3% previously. Consumer Price Index (MoM) (Feb) data will be released, with an expected reading of 0.2%, against 0.5% previously. These data points will provide an updated measure of the effect of inflation on consumers. Inflation is one of the main drivers of market sentiment in the US currently. The expectation is for an increase in consumer prices year-on-year but for the monthly reading to show a drop. The higher reading shocked the market in January but can be partly explained as an increase in demand for winter items due to the cold weather. If this is the case, the February number should show a correction. USD pairs and US assets could experience a pickup in volatility due to this data.

At 14:30 GMT, Bank of Canada Governor Poloz will give a speech titled “Today’s Labour Market and the Future of Work” at Queen’s University, in Ontario. CAD pairs could be moved by comments made during the speech or by answers given to audience questions afterwards.

At 23:50 GMT, BOJ Monetary Policy Meeting Minutes will be released, providing key insights into how the decisions made by the Board were influenced by economic conditions. JPY crosses may experience volatility as a result.

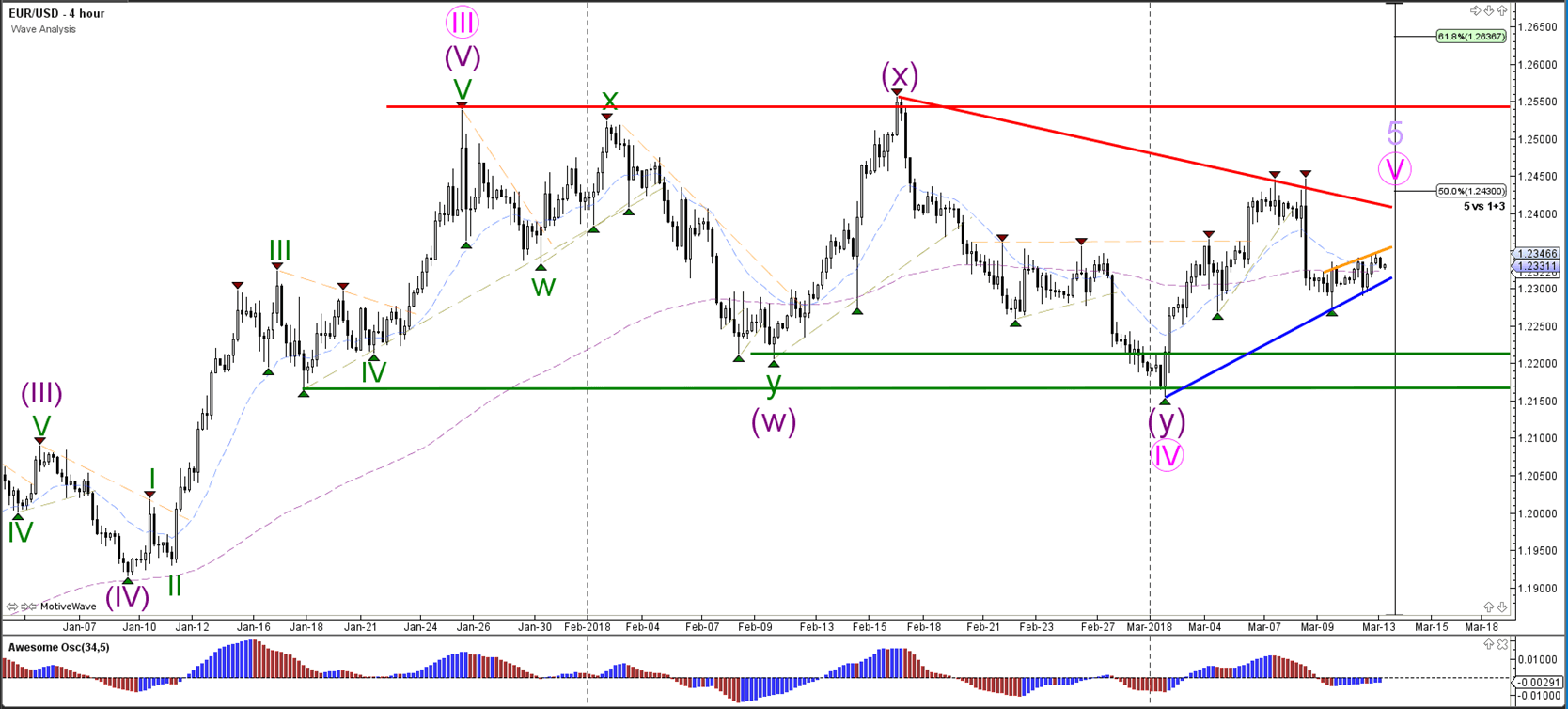

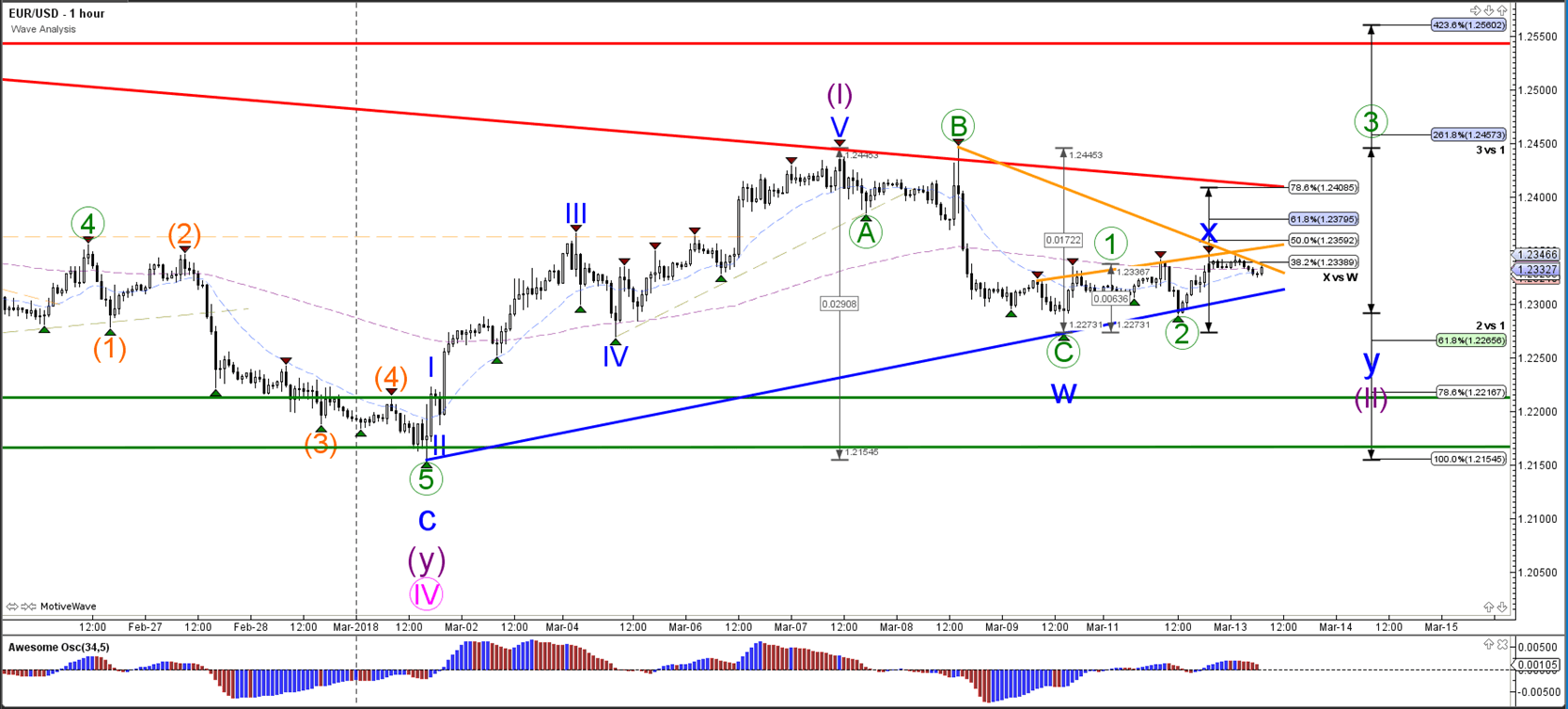

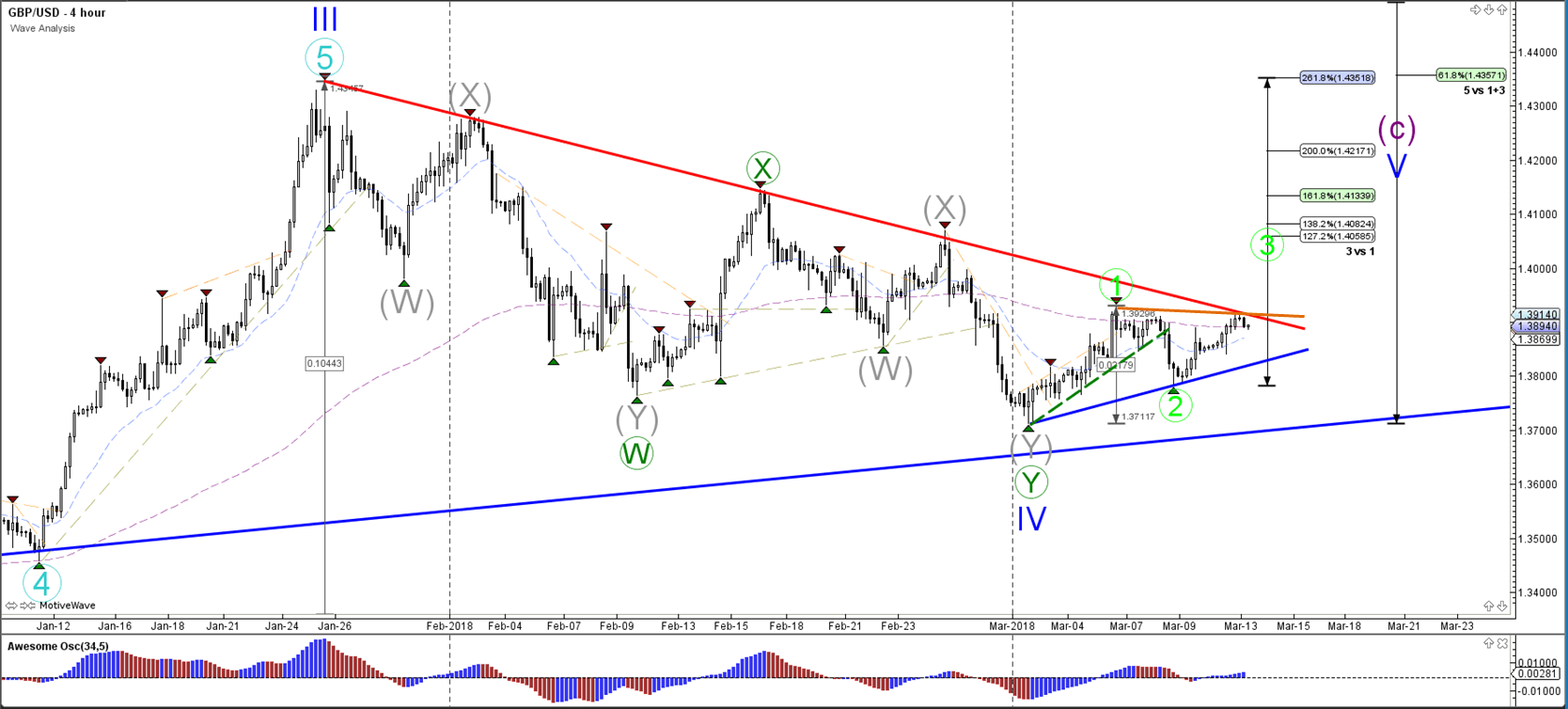

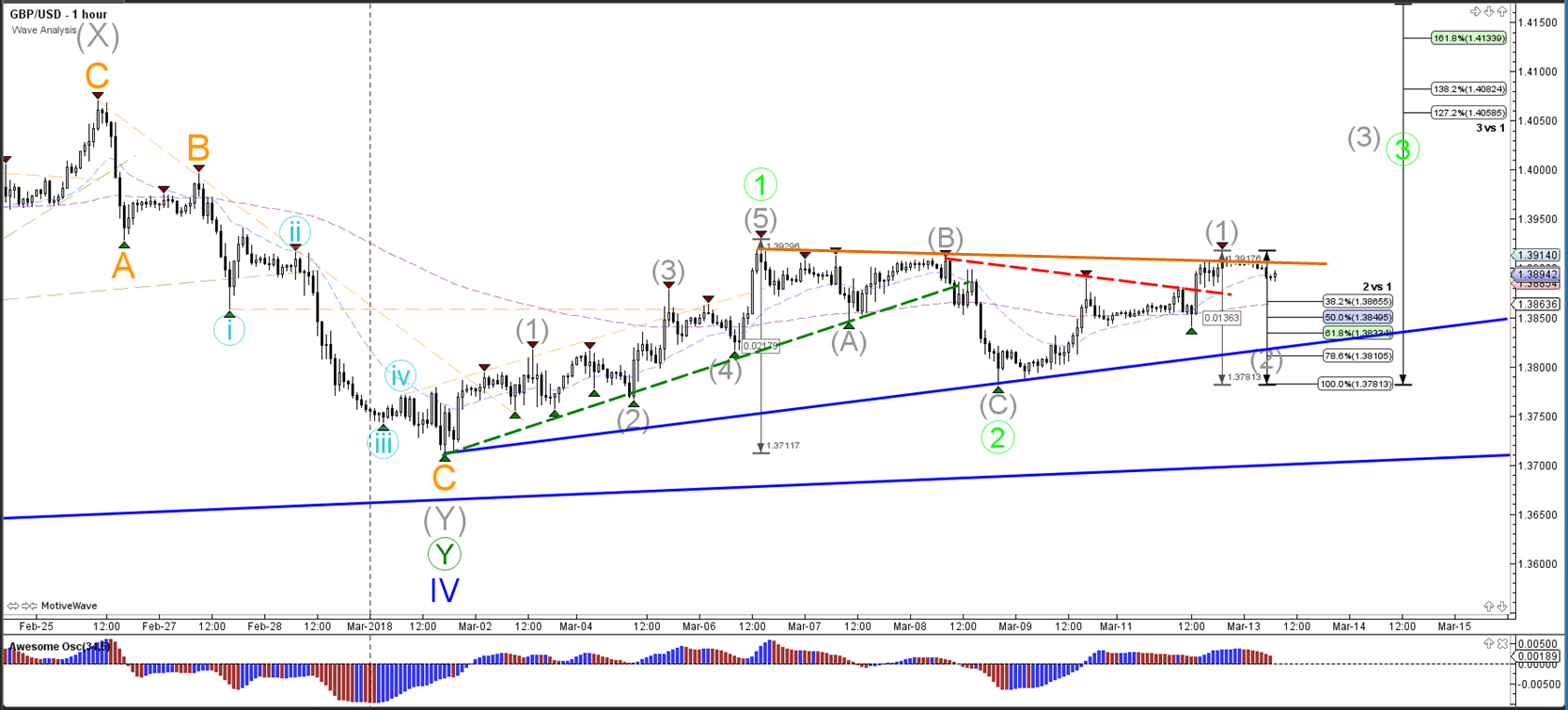

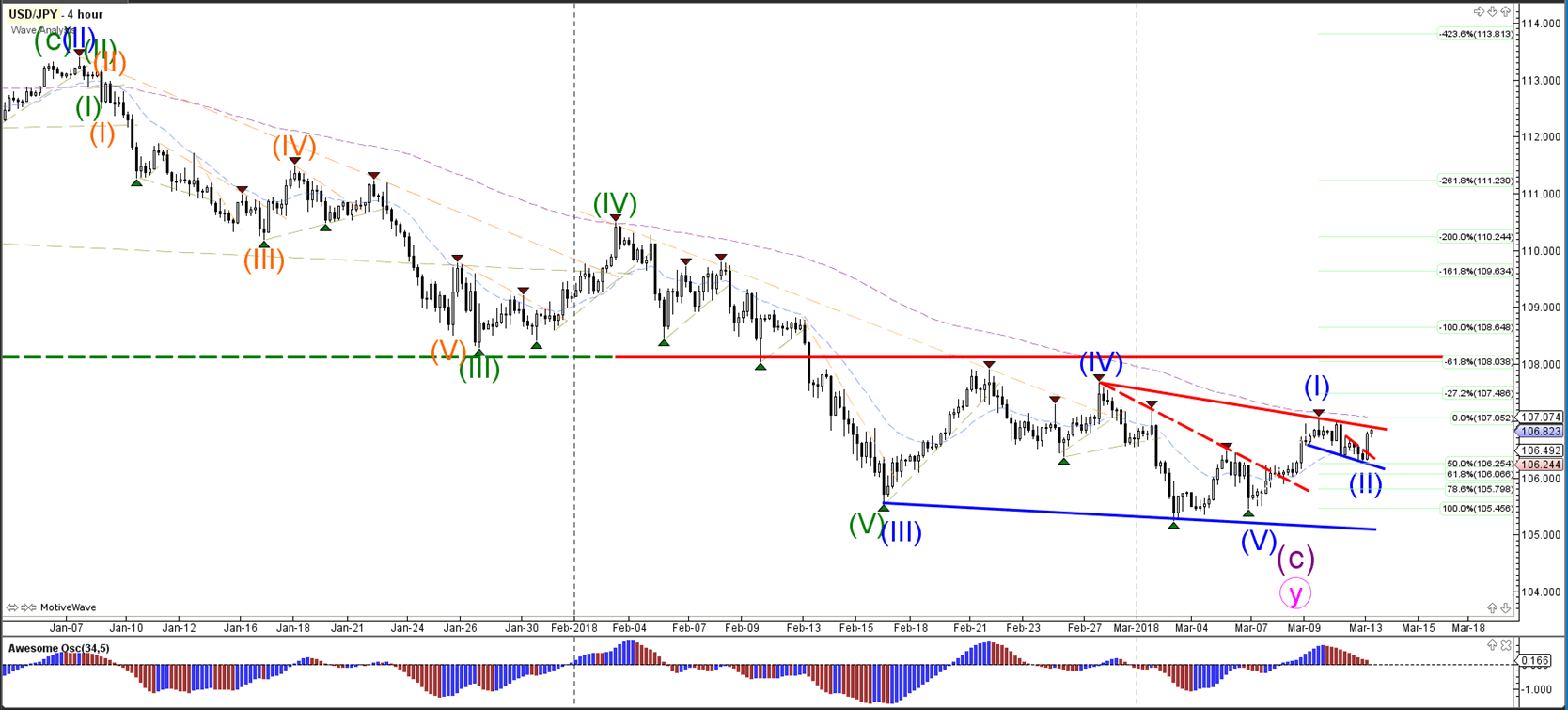

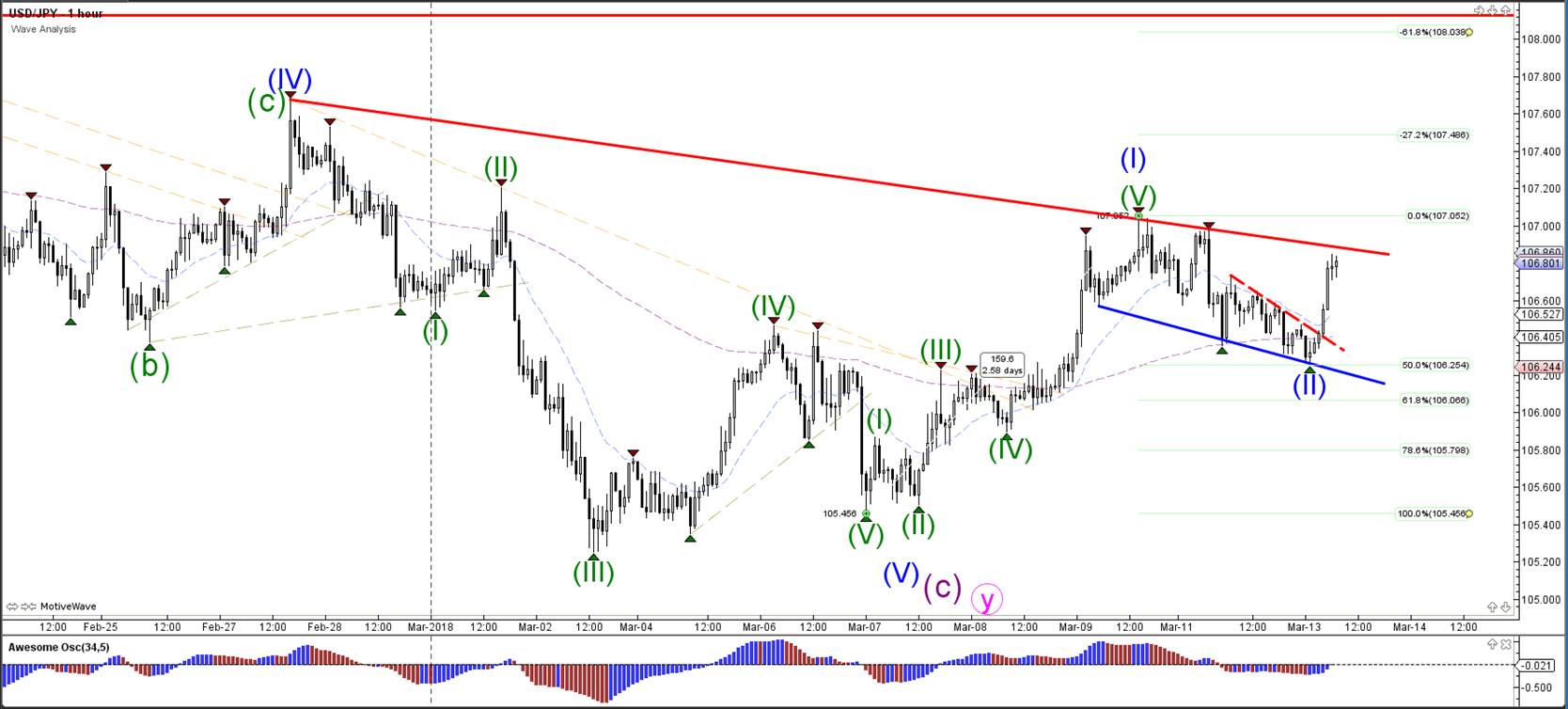

Daily Wave Analysis: Major Currency Pairs Close To Breaking Trend Lines

Currency pair EUR/USD

The EUR/USDis in a large consolidation zone and the new direction will depend whether price breaks above resistance (red) or below support (green). A bullish breakout would confirm the expected wave 5 pattern

The EUR/USD is building a channel which could indicate a larger WXY (blue) correction within wave 2 (purple) if price breaks below support (blue). A bullish breakout above resistance (orange/red) could start a potential wave 3 (blue).

Currency pair GBP/USD

The GBP/USD is probably ina wave 1-2 (green)within wave 5 (brown) unless price breaks below the bottom of wave 4 (brown). A bullish break above resistance (red) could confirm wave 5 (blue).

The GBP/USD could be building a bearish retracement. A bullish breakout could start a wave 3.

Currency pair USD/JPY

The USD/JPY is in a correction and a bullish breakout above the resistance trend lines (red) is needed before an uptrend could start.

The USD/JPY needs to break above resistance (red) before a larger uptrend could start.

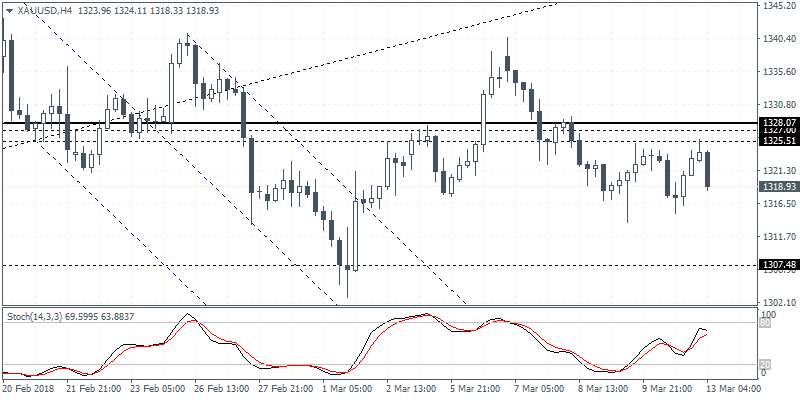

XAUUSD Intraday Analysis

XAUUSD (1318.93): Gold prices once again closed with a doji pattern on Monday but price action was confined to last Friday's range. We expect a downside breakout in price which could see gold prices testing the previous lows around 1307 - 1303 region to establish support at this level. In the event that gold prices post further declines, a retest of the lower support at 1282 - 1274 could be in play

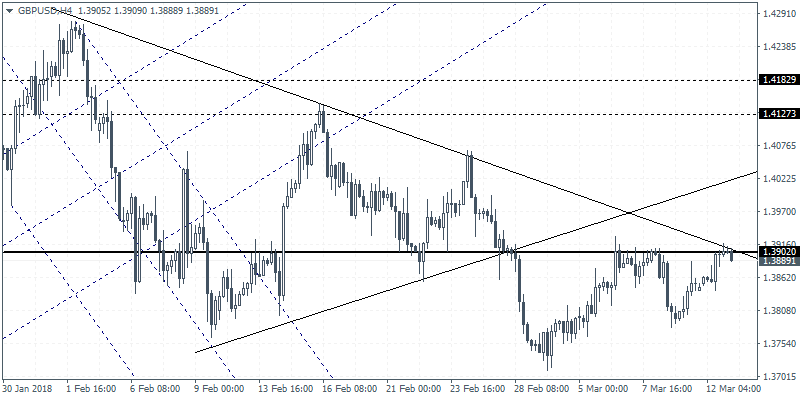

GBPUSD Intraday Analysis

GBPUSD (1.3889): The British pound was seen closing near the resistance level of 1.3902 on Monday and a bearish close today could see price action resuming the decline toward 1.3530. On the 4-hour chart we however see that the price action has consolidated into an ascending triangle pattern. Therefore, a potential breakout above the resistance level at 1.3902 could push the GBPUSD targeting 1.4070 level which would mark the previous high that was formed in the symmetrical triangle pattern.