Sample Category Title

Equities Drop, Bonds and Yen Gain on Trade War Fears

Wednesday February 7: Five things the markets are talking about

The fear of heightened protectionism continues to have a massive impact on capital markets.

President Trump's former economic adviser Gary Cohn's resignation late yesterday has hit global equities and the currencies of U.S trade partners, as investors consider the news means that Trump is pushing forward with his planned steel and aluminum tariffs.

Sovereign bonds have rallied while the yen rose to its strongest level in almost 16-months. Oil is under pressure as the trade-war fears sap most commodities ahead of today's EIA data that's expected to show U.S stockpiles expanded (10:30 am EST).

On tap: U.S ADP Non-Farm Employment Change at 08:15 am EST and Bank of Canada (BoC) rate announcement at 10:00 am EST.

1. Stocks see red

In Japan, the Nikkei share average dropped overnight after free-trade advocate Gary Cohn resigned as Trump's top economic adviser. The fear that Trump will proceed with tariffs pushed the steelmaker index to an eight-month low. The Nikkei fell -0.8%, not far from its five-month low. The broader Topix Iron and Steel index lost -2.1%.

Down-under, the Aussie commodity-heavy S&P/ASX 200 fell -1%, while in S. Korea, the Kospi declined -0.4% as optimism about N. Korea being open to talking about giving up its nuclear weapons was offset by worries about global trade.

In Hong Kong, stocks followed global markets lower amid renewed trade war fears. The Hang Seng index fell -1.0%, while the China Enterprises Index lost -1.1%.

In China, stocks reversed earlier gains to end the overnight session under pressure. At the close, the Shanghai Composite index was down -0.5%, while the blue-chip CSI300 index was -0.75% lower.

In Europe, regional indices trade mostly lower, tracking sharp declines in the U.S futures on Gary Cohn's announced resignation.

U.S stocks are set to open deep in the "red" (-1%).

Indices: Stoxx600 -0.3% at 370.1, FTSE flat at 7146, DAX -0.3% at 12077, CAC-40 -0.5% at 5146, IBEX-35 -0.2% at 9569, FTSE MIB -0.2% at 22156, SMI -0.3% at 8739, S&P 500 Futures -1.0%

2. Oil under pressure as concern grows over U.S trade, gold lower

2. Oil under pressure as concern grows over U.S trade, gold lower

Oil prices fell overnight, in line with other asset classes, after Gary Cohn's resignation renewed concerns that Washington will go ahead with import tariffs and risk a trade war.

Ahead of the U.S open, Brent futures are down -85c at +$64.94 a barrel, while U.S crude futures (WTI) are down -69c at +$61.91 a barrel.

A rise in U.S crude inventories has also dented market sentiment. API data yesterday showed that U.S crude inventories rose by +5.661m barrels last week to +426.8m barrels.

Official data by the U.S Energy Information Administration (EIA) is due later this morning (10:30 am EST).

Yesterday, the EIA upwardly revised its predictions for U.S crude oil production – it now expects to rise by more than +120k bpd to +11.17m bpd by Q4 2018.

Gold prices have retreated from their one-week high as trade war fears weigh on the dollar and equities. Spot gold is down -0.1% at +$1,333.15 per ounce, after touching +$1,340.42, its highest since Feb. 26, earlier in the session.

3. Yield focus shifts to central bank announcements

Later this morning, the Bank of Canada (BoC) will publish its monetary statement at 10:00 am EST. The central bank is not expected to make changes to the benchmark interest rate, keeping it at +1.25%.

The growing uncertainty over Canada's trade ties with the U.S is keeping the loonie under pressure (C$1.2933). Investors will be looking for clues that the BoC is still expected to raise rates three more times this year to keep up with the U.S Fed pace of rate hikes.

Earlier this morning, the Turkish central bank (CBRT) kept interest rates unchanged. The communiqué stated that the committee decided to maintain the tight monetary policy stance given that "core inflation remains elevated." It added that a tight monetary policy stance "will be maintained decisively until inflation outlook displays a significant improvement."

Elsewhere, the yield on U.S 10's fell -3 bps to +2.86%. In Germany, the 10-year Bund yield declined -1 bps to +0.67%, while in the U.K the 10-year Gilt yield fell -2 bps to +1.521%.

4. Dollar under pressure

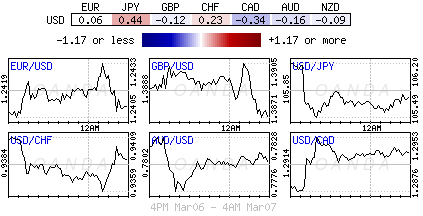

The USD is a tad lower against G10 currency pairs in quiet trading. Gary Cohn departure, Trump's most senior economic adviser, is considered a massive blow to pro-business and free trade.

EUR/USD is a tad higher by +0.2% at €1.2425 and seems poised to retest the upper-end of its 2018 range with €1.25 in the cross hairs.

GBP/USD is the outlier, trading under pressure, down -0.25% at £1.3855. Data this morning showed that the U.K Feb Halifax House Prices beat expectations, but still registered its lowest level in five-years.

USD/JPY continues to trade atop of the ¥105.60 level and within striking distance of 16-month lows.

5. Eurozone Q4 GDP

5. Eurozone Q4 GDP

Euro data this morning showed that the third estimate of euro-zone GDP in Q4 showed that expansion was driven mainly by net exports.

As expected, Q4 euro-zone growth was left unrevised at +0.6%, slightly slower than Q3's +0.7%.

Digging deeper, both the German and French economies were confirmed to have grown by +0.6%, while Italy lagged behind with a +0.3% expansion. In 2017 as a whole, the euro-zone economy grew by +2.5%.

Next up will be tomorrows European Central Bank (ECB) monetary policy announcement. Many individuals expects the ECB to remove the easing bias at its meeting, making it the first step in its "gradual" change of language.

The easing bias refers to the possibility that the ECB's QE could be increased again if need be.

DAX Ticks Higher as Eurozone GDP Stays Steady

European stock markets are seeing green on Tuesday, and the DAX and CAC have both posted strong gains. Currently, the DAX is trading at 12,097.08, up 0.10% since the Tuesday close. On the release front, Eurozone Revised GDP posted a gain of 0.6% for a fourth straight quarter. This matched the forecast. On Thursday, the ECB sets its benchmark rate, and the US will publish unemployment claims.

The ECB will be in focus on Thursday, as policymakers set the monthly benchmark rate. This will be followed by a press conference with Mario Draghi. The interest rate has been pegged at a flat 0.0% for the past two years, and no change is expected. The markets will be keeping a close eye on the language of the rate statement; in particular, whether the easing bias stance will be removed. If so, this would likely be interpreted as a plan to eventually tighten policy and would be bullish for the euro. Inflation remains weak, so there is little pressure on the ECB to tighten policy anytime soon. Recent indicators show that inflation in the eurozone is steady, but remains well below the ECB target of around 2 percent.

European stock markets have been turbulent since US President Trump stunned investors last week when he proposed stiff tariffs on steel imports, much to the consternation of the European Union and other US trading partners. Fears of a trade war sent the DAX sharply lower last week, with losses of 5.2%. The DAX has clawed back some of the losses this week, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. This has raised hopes that Trump will back down. However, the unpredictable president could barrel ahead and impose the tariffs, which would likely send global stock markets lower.

USD/JPY W Bullish Pattern at Daily Support

The USD/JPY dropped heavily to its session lows after Trump cancelled Thursday’s Tariff meeting. Now we can see that the price is exactly at the POC zone and it is either “make it or break it”. The price might spike from 105.75-60 zone to the upside. In that case targets are 105.94 and 106.25. Only above 106.25 targets are 106.44 and 106.72. H1 momentum or 4h close above 106.75 aims for 107.05. A drop below 105.45 should target 105.04. If we see a daily close below 105.00 then 104.38 is next target.

- W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- M H4 - Monthly Camarilla Pivot (Very Strong Monthly Resistance)

- M L3 – Monthly Camarilla Pivot (Monthly Support)

- M L4 – Monthly H4 Camarilla (Monthly Strong Daily Support)

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Euro Edges Higher As Eurozone GDP Matches Estimate

The euro has edged higher in the Wednesday session. Currently, EUR/USD is trading at 1.2452, up 0.17% on the day. On the release front, Eurozone Revised GDP posted a gain of 0.6% for a fourth straight quarter. This matched the estimate. In the US, today’s key indicator is ADP nonfarm payrolls, which is expected to drop sharply to 199 thousand. On Thursday, the ECB sets its benchmark rate, and the US will publish unemployment claims.

Investors are keeping a close eye on the ECB, which will set the benchmark rate on Thursday. This will be followed by a press conference with Mario Draghi. The interest rate has been pegged at a flat 0.0% for the past two years, and no change is expected. The markets will be keeping a close eye on the language of the rate statement; in particular, whether the easing bias stance will be removed. If so, this would likely be interpreted as a plan to eventually tighten policy and would be bullish for the euro. Inflation remains weak, so there is little pressure on the ECB to tighten policy anytime soon. Recent indicators show that inflation in the eurozone is steady, but remains well below the ECB target of around 2 percent.

In the US, tensions over proposed tariffs on steel imports continue to hurt the US dollar, and the euro has gained closed to 1% in the past week. President Trump appears set on applying stiff tariffs of 25% on steel, much to the consternation of the European Union and other US trading partners. However, there is plenty of domestic opposition to Trump’s plan, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. If Trump doesn’t back down, the Republicans could even resort to legislation to limit Trump’s authority on tariffs. The announcement of the tariffs last week sent the dollar broadly lower, and if the tariffs are introduced, negative investor sentiment could continue to weigh on the dollar.

Market Update – European Session: Cohn’s Exit From White House Gives Conservatives And Protectionists More Influence Over Policy

Notes/Observations

China Feb FX Reserves fall for the 1st time in over a year

UK Feb Halifax House Prices beat expectations but registers its lowest level in 5 years

Trade war concerns escalate

Gary Cohn departure gives conservatives and protectionists much more influence over White House policy

Asia:

Australia Q4 GDP misses expectations with quarterly growth at slowest pace since Q1 of 2017 (/Q: 0.4% v 0.5%e; Y/Y: 2.4% v 2.5%e)

RBA Gov Lowe reiterated there was no strong case for a near-term policy adjustment; likely that next RBA rate move would be up

China PBoC conducts 1-year MLF facility at unchanged rate of 3.25%; skips daily OMO for third straight session

BoJ Dep Gov Nominee Wakatabe: Won't automatically propose more easing, but did not exclude proposing extra easing

BoJ Dep Gov Nominee Amamiya ('Mr BoJ') reiterated Japan economy making progress toward CPI goal

Europe:

EU internal report argued that UK PM May was 'double cherry-picking' on Brexit and called her model unworkable; Report dismissed May’s Brexit speech as "being more about Conservative Party management than putting forward sensible solutions on trade"

Americas:

White House economic adviser Gary Cohn to resign; Expected to leave Administration in coming weeks

Fed Kaplan (non-voter, dove) reiterated base case was approx 3 interest rate hikes in 2018

Fed Brainard (voter, dove): Had greater confidence Fed to achieve 2% inflation target; tailwinds could speed up pace of rate hikes

Energy:

Weekly API Oil Inventories: Crude: +5.7M v 0.9M prior

Economic Data:

(ZA) South Africa Feb Gross Reserves: $50.1B v $50.5B prior; Net Reserves: $43.3B v $43.7Be

(RO) Romania Q4 Preliminary GDP (2nd reading) Q/Q: 0.6% v 0.6%e; Y/Y: 6.9% v 6.9%e

(MY) Malaysia Central Bank (BNM) left the Overnight Policy Rate unchanged at 3.25%; as expected

(DK) Denmark Jan Industrial Production M/M: +2.6% v -1.4% prior

(NO) Norway Q4 Current Account (NOK): 35.0B v 21.2B prior

(MY) Malaysia End-Feb Foreign Reserves: $103.7B v $103.6B prior

(FR) France Jan Trade Balance: -$5.6B v -$4.5Be

(FR) France Jan Current Account: -€1.6B v -€0.8B prior

(TW) Taiwan Feb CPI Y/Y: 2.2% v 2.0%e; CPI Core Y/Y: 2.4% v 0.8% prior, WPI Y/Y: -0.3% v -0.7% prior

(TW) Taiwan Feb Trade Balance: $2.9B v $3.7Be; Exports Y/Y: -1.2% v +3.7%e; Imports Y/Y: 0.9% v 4.9%e

(CH) Swiss Feb Foreign Currency Reserves (CHF): 732.8B v 732.0Be

(HU) Hungary Jan Industrial Production M/M: 1.5% v 1.3%e; Y/Y: 6.7% v 5.4%e

(CN) China Feb Foreign Reserves: $3.135T v $3.155Te (1st decline in 13 months)

(UK) Feb Halifax House Prices M/M: 0.4% v 0.4%e; 3M/Y: 1.8% v 1.6%e (lowest annual pace since 2013)

(SE) Sweden Feb Budget Balance (SEK): 49.9B v 0.0B prior

(CZ) Czech Feb International Reserves: $150.9B v $152.1B prior

(SG) Singapore Feb Foreign Reserves: $282.8B v $282.4B prior

(ZA) South Africa Feb Sacci Business Confidence: 98.9 v 99.7 prior

(EU) Euro Zone Q4 Final GDP Q/Q: 0.6% v 0.6%e; Y/Y: 2.7% v 2.7%e

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month, 6-month and 12-month bills

(DK) Denmark sold total DKK2.38B in 2020 and 2027 Bonds

(SE) Sweden sold SEK1.5B vs. SEK1.5B indicated in 0.75% May 2028 Bonds; Avg Yield: 0.8080% v 0.9046% prior; Bid-to-cover: 3.16x v 4.33x prior

(NO) Norway sold NOK2.0B vs. NOK2.0B indicated in 1.75% Feb 2027 Bonds; Avg Yield: 1.93% v 1.81% prior; Bid-to-cover: 3.49x v 2.48x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 370.1, FTSE flat at 7146, DAX -0.3% at 12077, CAC-40 -0.5% at 5146 , IBEX-35 -0.2% at 9569, FTSE MIB -0.2% at 22156 , SMI -0.3% at 8739, S&P 500 Futures -1.0%]

Market Focal Points/Key Themes:

European Indices trade mostly lower tracking sharp declines in US futures as President Trump's White House Economic adviser Gary Cohn announced his resignation, which has hit sentiment.

On the corporate front Rolls Royce reported a beat on the top and bottom line, with shares trading sharply higher, while Legal and General, Esure also trade higher after results. To the downside

Deutsche Post trades lower after earnings, with Paddy Power, Agfa Gevaert and Page Group also trading lower.

Looking ahead looking notable earnings include Dollar Tree and Brown Forman.

Movers

Consumer Discretionary [Paddy Power Betfair [PPB.UK] -3.2% (Earnings), Lookers [LOOK.UK] +1.3% (Earnings), Pagegroup [PAGE.UK] -5.6% (Earnings), Restaurant Group [RTN.UK] +11.6% (Earnings) ]

Industrials [ Rolls Royce [RR.UK] +13.6% (Earnings), Smurfit Kappa [SKG.UK] +3.4% (Follow through following rejected bid from IP), Deutsche Post [DPW.DE] -1.2% (Earnings)]

Financial [ Legal and General [LGEN.UK] +1.1% (Earnings), Esure [ESUR.UK] +1.5% (Earnings) ]

Technology [Agfa Gevaert [AGFB.BE] -1.1% (Earnings)]

Speakers

EU's Dombrovskis: EU ready to discuss banking cooperation with UK

China FX Regulator SAFE stated that falling asset price led to decline in FX reserves but reiterated its view that FX reserves expected to remain stable overall

Currencies

USD was slightly lower against most major pairs in quiet trading on Wed. The headwinds did loom for the greenback as analysts commented on the departure of While House Economic advisor Cohn. Overall view that Cohn was the most important and powerful pragmatic, pro-business member of the President's inner circle with the immediate impact to be on trade policy

EUR/USD was higher by 0.2% at 1.2425 and seemed poised to retest the upper-end of its 2018 range with 1.25 in sight

GBP/USD bucked the trend and was softer in session. The UK Feb Halifax House Prices beat expectations but still registered its lowest level in 5 years. Pair off by 0.2% at 1.3865

USD/JPY was hovering around the 105.60 level and within striking distance of re-testing Nov 2016 lows

Fixed Income

Bund Futures trades 18 ticks higher at 156.68 popping higher after President Trump’s top economic advisor Cohn’s resigned. Upside targets 157.50, while a return lower targets the155.75 level.

Gilt futures trade at 122.13 up 26 ticks as Gilts resume their push higher. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

Wednesday's liquidity report showed Tuesday's excess liquidity rose to €1.879T from €1.878T prior. Use of the marginal lending facility fell to €40M from €51M prior.

Corporate issuance saw 2 issuers raise $1.7B in the primary market

Looking Ahead

(EU) EU President Tusk presents Brexit strategy

(IE) Ireland Debt Agency (NTMA) to sell 2022 and 2028 IGB bonds

(IL) Israel Feb Foreign Currency Balance: No est v $117.6B prior

(UR) Ukraine Feb CPI M/M: 0.8%e v 1.5% prior; Y/Y: 14.0%e v 14.1% prior

05:30 (DE) Germany to sell €4.0B in 0% Apr 2023 BOBL; Avg Yield: % v 0.08% pior; Bid-to-cover: x v 1.3x prior (Jan 31st 2018)

06:00 (TR) Turkey Central Bank (CBRT) Interest Rate Decision: Expected to leave Benchmark Repurchase Rate unchanged at 8.00%

06:00 (IE) Ireland Jan Retail Sales Volume M/M: No est v -0.1% prior; Y/Y: No est v 7.2% prior

06:00 (IE) Ireland Jan Industrial Production M/M: No est v 3.0% prior; Y/Y: No est v 3.0% prior

06:00 (PL) Poland Central Bank (NBP) Interest Rate Decision: Expected to leave Base Rate unchanged at 1.50%

06:00 (BR) Brazil Feb FGV Inflation IGP-DI M/M: 0.1%e v 0.6% prior; Y/Y: -0.2%e v -0.3% prior

06:00 (RU) Russia to sell RUB 40B in OFZ Bonds

06:30 (CL) Chile Central Bank Traders Survey

06:30 (CL) Chile Feb Trade Balance: $1.1Be v $1.2B prior; Exports: $6.5Be v $6.7B prior; Imports: $5.4Be v $5.5B prior; Copper Exports: No est v 2.6B prior

06:30 (CL) Chile Feb International Reserves: No est v $38.7B prior

06:45 (US) Daily Libor Fixing

07:00 (US) MBA Mortgage Applications w/e Mar 2nd: No est v 2.7% prior

07:00 (CL) Chile Jan Nominal Wage M/M: No est v 0.5% prior; Y/Y: 4.6%e v 4.6% prior

08:00 (PL) Poland Feb Official Reserves: No est v $117.5B prior

08:00 (RU) Russia Feb Official Reserve Assets: $457.7Be v $447.7B prior

08:00 (RU) Russia Gold and Forex Reserves w/e Mar 2nd: No est v $450.9B prior

08:00 (US) Fed's Dudley (dove, FOMC voter) speaks in Puerto Rico

08:00(US) Fed's Bostic (2018 voter, dove) speaks on the Economic Outlook

08:05 (UK) Baltic Dry Bulk Index

08:15 (US) Feb ADP Employment Change: +200Ke v +234K prior

08:30 (US) Q4 Final Nonfarm Productivity: -0.1%e v -0.1% prelim; Unit Labor Costs: 2.1%e v 2.0% prelim

08:30 (US) Jan Trade Balance: -$55.0Be v -$53.1B prior

08:30 (CA) Canada Q4 Labor Productivity Q/Q: +0.1%e v -0.6% prior

08:30 (CA) Canada Jan Int'l Merchandise Trade (CAD): -2.5Be v -3.2B prior

09:30 (TR) Turkey Feb Cash Budget Balance (TRY): No est v -1.6B prior

10:00 (CA) Bank of Canada (BOC) Interest Rate Decision: Expected to leave Interest Rate unchanged at 1.25%

10:00 (PL) Poland Central Bank Gov Glapinski to hold post rate decision press conference

10:30 (US) Weekly DOE Crude Oil Inventories

14:00 (US) Federal Reserve Beige Book

15:00 (US) Jan Consumer Credit: $17.7Be v $18.4B prior

18:50 (JP) Japan Q4 Final GDP Q/Q: 0.2%e v 0.1% prelim; Annualized GDP Q/Q: 1.0%e v 0.5% prelim; Nominal GDP Q/Q: 0.1%e v 0.0% prelim

(JP) Bank of Japan (BOJ) Interest Rate Decision: Expected to leave Interest Rate on Excess Reserves (IOER) Unchanged at -0.10%

EURUSD – Threatens Further Upside Pressure

EURUSD -With the pair continuing to hold on its upside pressure, more strength is envisaged. On the upside, resistance comes in at 1.2450 level with a cut through here opening the door for more upside towards the 1.2500 level. Further up, resistance lies at the 1.2550 level where a break will expose the 1.2600 level. Conversely, support lies at the 1.2350 level where a violation will aim at the 1.2200 level. A break of here will aim at the 1.2150 level. Below here will open the door for more weakness towards the 1.210. All in all, EURUSD faces further bull threats on correction.

USDJPY Now Bearish Below 106.00 Level

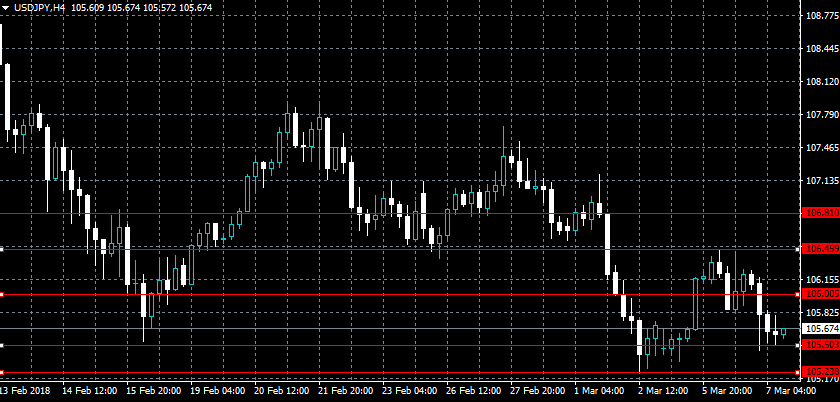

The U.S dollar has erased Tuesday's gains against the Japanese yen as risk-off trading sentiment quickly returns to financial markets, following top U.S economic advisor Gary Cohn's resignation. The USDJPY pair has slumped back towards the key 105.50 support level, with MACD and RSI technical indicators now turning bearish as sellers once again gain control of price-action. Traders now look towards the release of the U.S ADP jobs report and the U.S stock market open, with futures markets pointing to heavy declines.

The USDJPY pair is likely to decline further below the 105.50 level, sellers will likely target the 105.23 and 104.60 support region.

If the USDJPY pair can hold the 105.50 support area, a technical test of the key 106.00 resistance level seems likely.

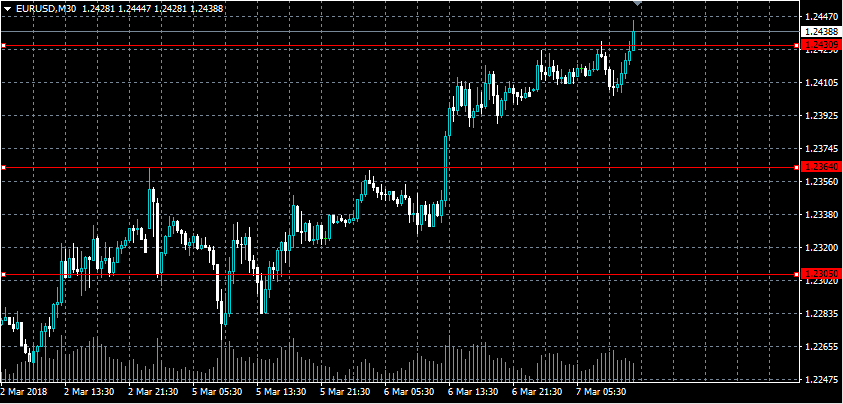

EURUSD Breaks Above Key 1.2430 Resistance Level

The euro has broken above the key 1.2430 resistance level against the greenback during the European trading session, as the U.S dollar index comes under strong selling pressure. The EURUSD pair has so far set a new weekly trading-high of 1.2444, with further intraday gains likely as traders use the 1.2430 level as former key resistance turned critical support. Traders now look towards the release of the U.S ADP jobs report, with economists expecting 185,000 new private sector jobs to be created.

The EURUSD pair is strongly bullish while trading above the 1.2430 level, further gains towards the 1.2474 and 1.2550 levels appears likely.

If the EURUSD pair now falls below the 1.2430 level, price-action may correct back towards the 1.2400 and 1.2364 support levels.

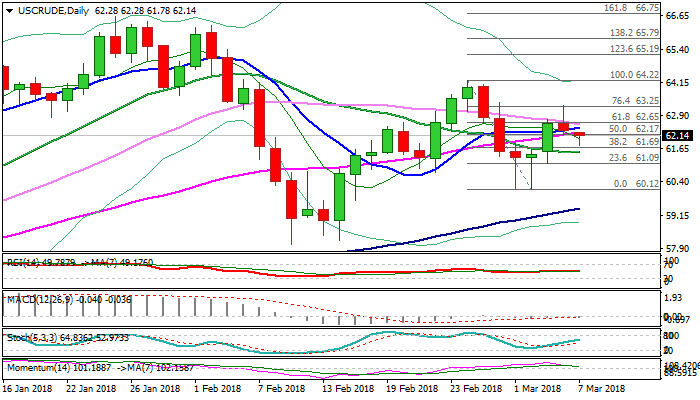

WTI Oil Weakens On Strong Oil Stocks Build, Risks Further Downside

WTI oil stands in red on Wednesday on fresh negative sentiment, sparked by stronger than expected build of crude stocks and rising fears about potential global trade war. Oil price closed in red on Tuesday after attempts to extend strong rally from Monday were strongly rejected at $63.26, leaving daily candle with long upper shadow, which was initial bearish signal. API weekly crude stock report, released late Tuesday, showed unexpectedly strong build in crude inventories by 5.66 million barrels, more than double of forecast for build of 2.7 million barrels. Oil price extended weakness to $61.78 on Wednesday, driven by negative sentiment, but dips were so far short-lived as the price bounced back above cracked Fibo support at $62.06 (38.2% of $60.12/$63.26 recovery). Fresh easing weakened near-term structure as daily MA's (10/30/55) turned to bearish setup and momentum dipped to the border of negative territory, threatening of further weakness, which could be triggered by stronger than forecasted build of weekly crude stocks from EIA report (due later today) and close below cracked Fibo support at $62.06. Bearish scenario would look for Fibo levels at $61.69 (50%) and $61.32 (61.8% of $60.12/$63.26) which guard the base of thick daily cloud at $60.91. Bullish scenario sees minimum requirement on bounce above 30SMA ($62.56) to ease immediate downside risk, however, extension above Tuesday's high at $63.25 is needed for attack at daily cloud top at $63.49, which marks upper pivot.

Res: 62.28, 62.56, 62.77, 63.25

Sup: 62.06, 61.78, 61.69, 61.32

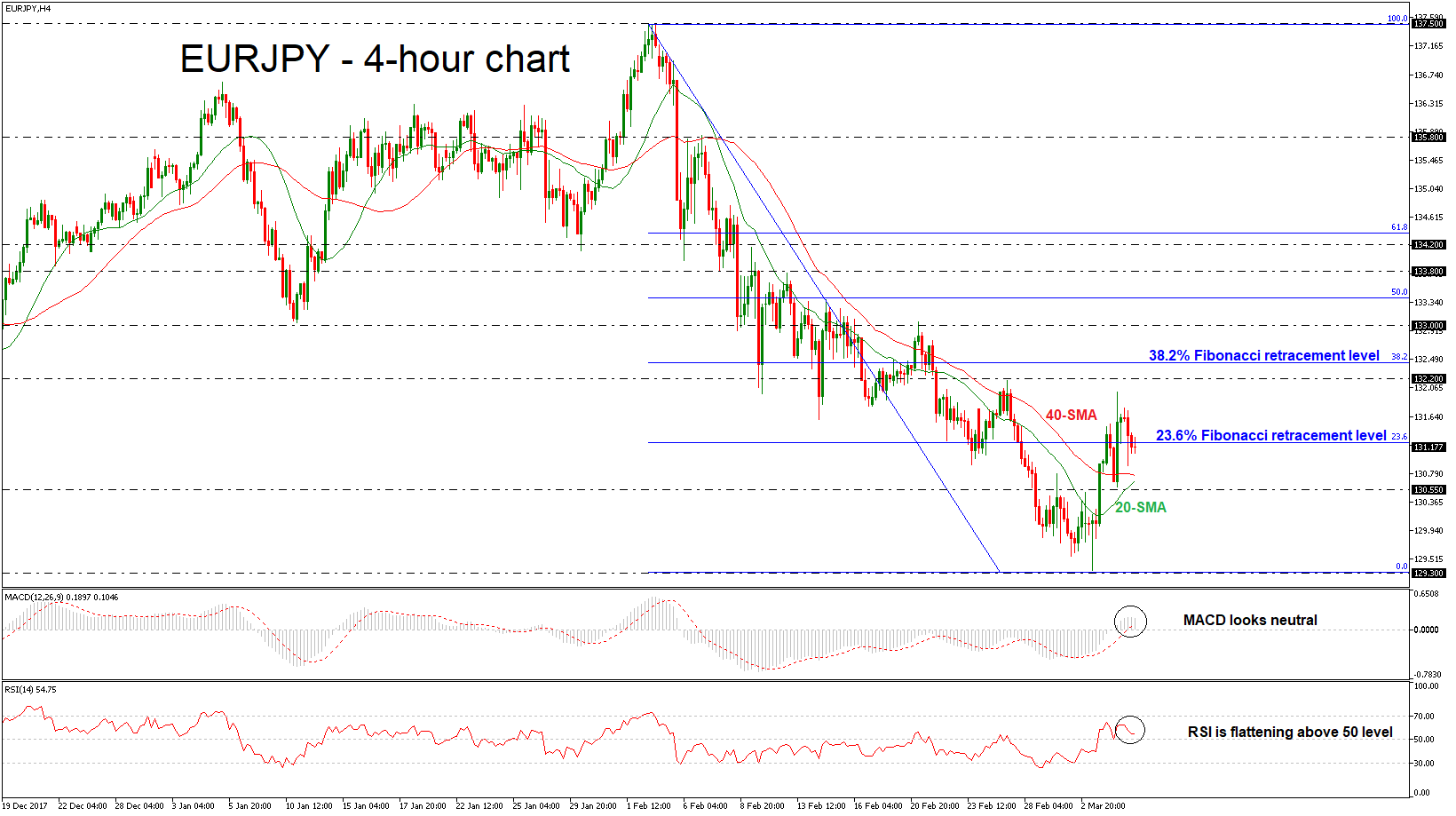

EURJPY Fails To Strengthen Bullish Run, Negative Movement In Progress

EURJPY remains under strong pressure as it has started an aggressive bearish correction since February 2. The price lost more than 30% of its gains since April 2017 as it tried to challenge the 38.2% Fibonacci retracement level at 128.80 of the upleg from 114.90 to 137.50.

During today's European session the pair completed two consecutive bearish sessions in the 4-hour chart and slipped below the 23.6% Fibonacci level of the downleg from 137.50 to 129.30.

From the technical point of view, in the short-term, the MACD oscillator holds in the positive area with weak momentum, while the RSI indicator is flattening above the 50 level, suggesting neutral to negative movement in price action. Despite that, the 20 and 40 simple moving averages are turning to the upside.

In case of further losses, the pair could hit the 130.55 support barrier but needs to fall below the 20 and 40 SMAs. A dip below the aforementioned obstacle could lead the way towards the 129.30 low.

On the flip side, to the upside, the next level to watch is the 132.20 resistance if there is a jump above the 23.6% Fibonacci mark. Rising above this barrier could hit the 38.2% Fibonacci level of 132.45.