Sample Category Title

Uncertainty Lingers

Uncertainty Lingers

Asset markets continue to wobble to and fro as uncertainty lingers over Trump’s tariff, while investors are left absorbing the aftershocks from Cohn’s resignation.

Also, New York is dealing with the deadly snowstorm that is tearing through the North Eastern United States which is likely weighing on market participation.

A worse-than-expected US trade deficit report didn’t help the free trade camp as the deficit moved to a nine-year high, further stoking the protectionist fires. The sharp widening of the trade shortfall with China is a significant point of contention, and ultimately eclipsed a firm ADP print which beat estimates at 234k (185k forecasted).

The trade numbers could not have come at a worse time for the market as the President took to Twitter, his favourite medium to express policy views, suggesting he’s setting sights on China demanding a one billion dollar reduction in $375.2 billion imbalance. Peanuts really, but more significantly in his follow up tweet he implied the U.S. is acting swiftly on Intellectual Property theft which is by far the most significant risk to the market. Following through on 301 of the US trade act could result in a swift and potential market destabilising response from China. Certainly, one road the market doesn’t want to go down.

Trump is reported to be planning a tariff announcement on Thursday at 12:00 EST. And while Trump continues his sabre rattle, investors are hoping for a more efficient tariff approach directed at more obvious trade infringements. Where there is hope, there is is still life in the markets.

Fedspeak remained on a hawkish bias nudging the US yields a touch higher but with the market singularly focused on tariff talks, subtly shifting market narratives seem to matter little to traders.

Oil Markets

Investors angst over a possible trade war escalation is sucking most asset classes into an ever-expanding tariff sinkhole. The negative economic implications are weighing on global growth sentiment and in turn denting oil market sentiment. Not helping matters, the Department of Energy showed weekly US crude production hit a record high last week of almost 10.4 million barrels per day. Probably not the most bullish of oil price signals.

Gold Markets

A strong ADP jobs report and the hawkish Fed bias have temporarily dented gold sentiment. And with the USD going through it usual pre ECB and NFP position adjustment and other such machinations we should expect Gold prices to be at the mercy of USD position adjustments over the next 24 hours. Although we could be in for a chop feast it’s unlikely we will threaten the edges of near-term ranges ahead of critical macro risk events.

Currency Markets

The Euro

EURUSD position adjustment take paramount to extending risk ahead of the ECB decision so markets should remain in confined ranges ahead of the ECB

The Japanese Yen

The USDJPY is hanging firm after running into solid support at 10.5.50 level after yesterday Cohn wobble. The currency markets are trying to find a balance between the hawkish fed narrative and the tariff fall out. But with the all-important NFP and specifically the wages component due later in the week, traders don’t want to be caught too short USDJPY in fear of an uptick in wages inflation.

Japan Q4 GDP has come at 0.4% versus 0.2% expected. The annualised SA QoQ is now at 1.6% versus 1% expected. But currency traders are waiting to take their cues from the open of cash equity markets in Japanese as the Yen remains an extremely risk-sensitive trade over the short term to medium term.

The Malaysian Ringgit

MPC stayed on hold at 3.25% as widely expected; global growth outlook remained positive and struck all the right decisive domestic external chords to keep investors happy. While their inflation assessment was even more dovish than January all but suggesting, it will take an inflationary surprise to move the rate hike dial on more time in 2018. But they certainly left the door open further policy normalisation by signalling they will continue to assess the balance of growth and inflation.

BNM appetite for a stronger MYR is seen mitigating the inflationary impact from higher prices at the pump and providing them with more wiggle room on monetary policy.

While the MPC was a bit more dovish than expected their rosy assessment of domestic and international economic conditions should ultimately remain supportive of the Ringitt

Gold Volatility Continues Over Trump Tariff Threat

Gold has posted sharp losses in the Wednesday session, erasing much of the gains seen on Tuesday. In North American trade, the spot price for an ounce of gold is $1324.71, down 0.75% on the day. In economic news, there was positive news on the labor front, as ADP Nonfarm Payrolls report ticked higher to 235 thousand, easily beating the estimate of 199 thousand. On Thursday, the US releases unemployment claims.

Gold prices continue to show strong fluctuation, as the markets remain focused on President Trump's threat to impose heavy tariffs on imported steel. The announcement has infuriated US trading partners, as well as sharp criticism from senior Republican lawmakers. There was further drama on Tuesday, as Gary Cohen, Trump's economic adviser, resigned. Cohen was a strong advocate of free trade, so his resignation could weaken opposition in the White House to the tariffs. Gold posted strong gains on Tuesday, but has given up much of these gains on Wednesday. Will Trump make good on his threat or back off? Until the situation is resolved, traders should be prepared for continuing volatility from gold.

Good news on the employment front translated into losses for gold on Wednesday. The ADP nonfarm payrolls report, which precedes the official nonfarm payrolls report on Friday, ticked upwards to 235 thousand, up from 234 thousand a month earlier. This easily beat expectations, boosting investor risk appetite. The nonfarm payrolls report is also expected to remain steady, and if the indicator can again beat expectations, gold prices would likely head lower.

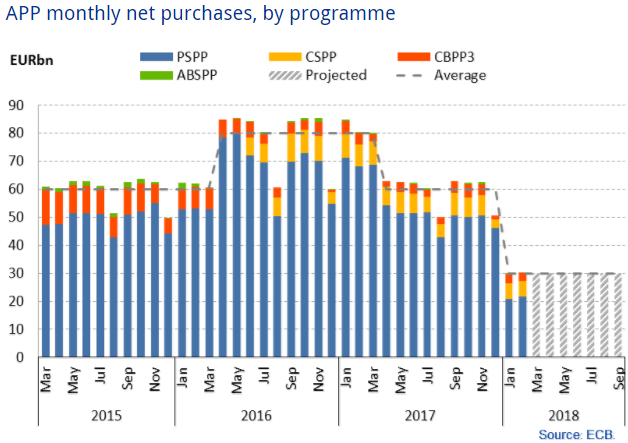

ECB To Prepare Markets For End Of QE

Traders Look For Subtle Clues Ahead of September Expiry

Thursday's European Central Bank meeting may not go down as the most exciting on record but it could contain some very subtle hints that the end of quantitative easing is close.

- ECB Bond Buying Expected to End This Year

- Gradual, Calm Exit Sought By Policy Makers

- Markets May Be Sensitive to Small Changes in Message

The ECB has been gradually and carefully bringing its QE program to an end ever since it announced its first reduction – which is claimed was not a taper out of fear of a repeat of the taper tantrum the Federal Reserve experienced in 2013 – back in December 2016.

Since then, purchases have fallen from €80 billion a month to €60 billion – in April last year – and then to €30 billion from January this year. With the current purchases expiring in September, there has been speculation about whether the ECB will end it at expiry or briefly extend to the end of the year at a slightly reduced pace. The reality is that it doesn't really matter and we're not likely to find out until June, but that doesn't mean we shouldn't pay attention to the meetings until then.

For one, a number of things could change between now and the June meeting that could force the ECB to increase the pace of tightening or further delay the end of QE and clues about such a move will come from the meetings and/or the speeches they give in between them.

The ECB has also made it clear that any policy changes will be communicated very gradually so I would imagine we will see small differences at almost every meeting for the rest of the year so as to well prepare us for the end of QE. That may not be particularly exciting but it could well move markets.

The language that is speculated to be targeted on Thursday is the reference to the central banks readiness to increase the asset purchase program in size or duration if the outlook becomes less favourable. While this was always a pointless line, the ECB has stuck by it and the removal of it is a small acknowledgement that less dovish language in warranted.

The question is how much this tiny gesture is priced in, what impact it will have on the euro and whether they will go any further given the tense environment – trade wars, fragile market sentiment. We may well see some movement in the euro around the release but ultimately, Mario Draghi – the ECB President – will likely determine what markets will do.

I expect he may keep his cards very close to his chest and let the press conference pass without any major talking points. Either way, traders will be sitting and waiting to pounce on any unexpected hawkish or dovish message Draghi decides to divulge.

Pound Unchanged, Tusk Takes PM May To Task

The British pound is unchanged in the Wednesday session. In North American trade, GBP/USD is trading at 1.3886, down 0.01% on the day. In economic news, there are no major indicators in the UK. In the US, ADP Nonfarm Payrolls report ticked higher to 235 thousand, easily beating the estimate of 199 thousand. On Thursday, the US releases unemployment claims.

The game of hardball between Britain and the European Union continues. On Wednesday, Donald Tusk, president of the European Council, advised Prime Minister May to “pink’ her red lines on Brexit, if Britain wants to maintain a close economic relationship with the bloc. May has insisted that there will be no customs union, and the European Court of Justice will have no jurisdiction over the UK. Last week, the EU published draft negotiating guidelines for Brexit, and the guidelines warned of “negative economic consequences” if Britain does not soften its position. Tusk added that he does not want to build a wall with Britain, and the EU could offer Britain a free trade agreement, with zero tariffs. At the same time, Tusk warned that Brexit will make trade between the two sides “complicated and costly” and the EU would not allow Britain to cherry pick in any future trade arrangement. EU members are expected to sign off on the negotiating guidelines at a summit in late March, which is likely to heat up the tense relationship between London and Brussels.

In the US, tensions over proposed tariffs on steel imports continue to hurt the US dollar. President Trump appears set on applying stiff tariffs of 25% on steel, much to the consternation of the European Union and other US trading partners. However, there is plenty of domestic opposition to Trump’s plan, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. If Trump doesn’t back down, the Republicans could even resort to legislation to limit Trump’s authority on tariffs. The announcement of the tariffs last week sent the dollar broadly lower, and if the tariffs are introduced, negative investor sentiment could continue to weigh on the dollar.

Fed: Beige Book Indicates that Strong Economic Momentum Has Extended into 2018

Today's Beige Book indicated that economic activity across all twelve Federal Reserve Districts expanded at a modest to moderate pace in January and February. Led by strong consumption fundamentals, sentiment remains positive and has further upside potential, owing to tax cuts.

Consumption was reported to be mixed, with non-auto retail sales posting solid activity, in contrast to auto purchases which floundered across districts. This confirms that previous strength related to hurricane vehicle replacement has likely dried up, with an increase in borrowing costs likely to weigh on auto purchases over the remainder of the year. On the other hand, retailers are confident that non-auto purchases will continue to be supported by consumer confidence and tightening labor markets.

Prices increased at a moderate pace, with inputs to construction, including lumber and steel, increasing notably. Transportation costs also ticked up on higher fuel costs that increased freight rates. Some steel producers reported raising selling prices on account of the resolution of pending trade cases and these cost increases were absorbed by manufacturers further down the supply chain. However, their ability to pass these increases on to final consumers was largely unchanged from the previous report. At the same time, retailers cited competition as a reason for holding selling prices steady or decreasing them in some cases.

Extending last year's trend, residential real estate inventories remained thin, leading to steady growth in home prices. Continued labor scarcity and a lack of land proved to limit construction of homes. In turn, this restrained home purchases, due to the lack of options on the market. At the same time, a scarcity of labor also limited construction activity, with contacts reporting little relief in the near future. This is in contrast to the commercial real estate segment, with reports of robust activity in three Districts representing an improvement from the prior report. Favorable business conditions have supported this trend recently and will likely continue to as the effects of the Tax Cuts and Jobs Act (TCJA) continue materializing over the remainder of the year.

Employment grew moderately, with Districts universally reporting labor market tightness and heightened demand for qualified workers. Increasingly, employers are outsourcing hiring to staffing placement services as the search for workers becomes cumbersome. Again, manufacturing and construction workers were in short supply, with information technology workers being added to the list. This led employers to increase wages and expand benefit packages, with a select few Districts reporting compensation increases owing to the TCJA.

Key Implications

This Beige Book confirms that the economy continued to expand at a solid clip at the start of 2018. Employer sentiment remained elevated amid strong household spending, while inflation pressures continued to build, with steady increases in labor and non-labor input costs suggesting that selling prices will rise over the year. Several employers reported increasing compensation as a result of the TCJA, with others raising wages in order to remain competitive and retain workers. Building material prices and transportation costs continued to exhibit some of the most pronounced price pressures amid heightened demand. This could be amplified in the near future with the implementation of tariffs that producers would pass on to consumers. Speculation surrounding the implementation of tariffs adds to pre-existing uncertainty in the manufacturing industry regarding NAFTA negotiations. Moreover, the increase in input costs could further strain housing construction that is already being limited by quickly rising land and building material costs.

Despite supply-side uncertainty, household spending continues to be upheld by labor market tightness, and that has propped up demand in housing markets amid quickly escalating prices. However, some metro housing markets are becoming increasingly unaffordable as housing inventories dwindle. Tax code changes will amplify this in high-priced and high-tax markets, with robust wage gains only partially mitigating these effects. Specifically, the lower cap on the mortgage interest deduction (down from $1M to $750k), combined with the implementation of the $10,000 cap on state and local tax deductions (which includes property taxes), will raise the cost of homeownership notably in high-priced and high-tax markets including those in New York and the District of Columbia, which will slow home price growth. Additionally, these unfavorable tax measures may hinder the ability of these regions to attract workers in the future, exacerbating labor shortage issues.

This report suggested that businesses remain optimistic and are increasingly passing on increases in input prices. As such, these should show up in headline inflation figures in the near future. That will enable the Fed to proceed with three hikes this year, with the first of these likely to take place later this month. Further upside potential comes from the budget deal that should foster additional growth and inflationary pressures.

Bank of Canada Holds Rates Steady Amid Growing Trade Uncertainty

Highlights:

- The overnight rate was held steady at 1.25% today after the bank raised rates in January.

- The statement noted “trade policy developments are an important and growing source of uncertainty,” a clear nod to the Trump administration’s proposed tariffs on steel and aluminum.

- Inflation developments have been consistent with the economy running at full capacity, but wage growth was once again seen as indicating a bit of labour market slack.

- The bank is keeping an eye on how regulatory changes impact the housing market, and how credit growth is responding to higher interest rates.

- Deputy Governor Lane will present an economic progress report tomorrow that should elaborate on the BoC’s latest thinking. The speech will be a regular feature following non-MPR meetings going forward.

Our Take:

Today’s statement suggests the Bank of Canada has added ‘trade policy dependent’ to their ‘data dependent’ mantra. A rate increase at today’s meeting was already a long shot, coming just seven weeks after the central bank’s last move. But any odds of a hike, or even a slightly hawkish tilt, went out the window last week with the Trump administration’s proposal to slap tariffs on steel and aluminum imports. That threat was certainly on the minds of the Governing Council when, front and center in today’s statement, they noted trade policy is “an important and growing source of uncertainty.” The BoC has been worried about the impact of Nafta uncertainty for some time and the latest rhetoric from our largest trading partner has clearly increased the odds of a negative outcome. Metals tariffs on their own won’t drastically change the central bank’s thinking. But if tit-for-tat measures escalate into a full-blown trade war—and to be clear, we aren’t nearly there yet—the BoC would have to rethink their tightening bias. The rapidly-evolving trade backdrop will be a major factor in whether the central bank raises rates in April. How businesses are responding to growing uncertainty—the bank’s next Business Outlook Survey will be released April 9—will also hold sway.

As for their data dependence, developments since January’s meeting provided little reason for the bank to deviate from their current course. We’ve seen further signs that wages and inflation are picking up. And while Q4/17 GDP fell short of their forecast, domestic demand was strong and growth remained slightly above-trend—hardly disappointing when the economy is already at capacity. Financial conditions have been mixed, with bond yields rising and equities falling since mid-January, though a weaker Canadian dollar has provided some offset. On balance, the bank’s tightening bias remains appropriate but so is a healthy dose of caution given tough talk on trade from south of the border

Eco Data 3/8/18

[php_everywhere instance="1"]

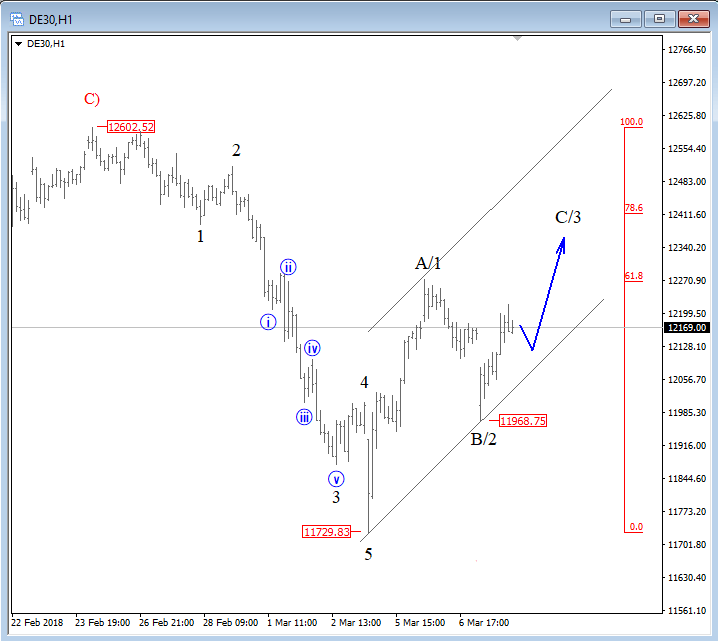

Elliott Wave Analysis: German DAX and USD Index

German DAX made a sharp rally in the past few days, which we see it as first leg A/1 of a minimum three-wave reversal, followed by wave B/2 which so support at 11968 level. Price can now continue towards the 12411 level, where we will see either some resistance and a new drop lower, or a continuation towards higher levels.

German DAX, 1H

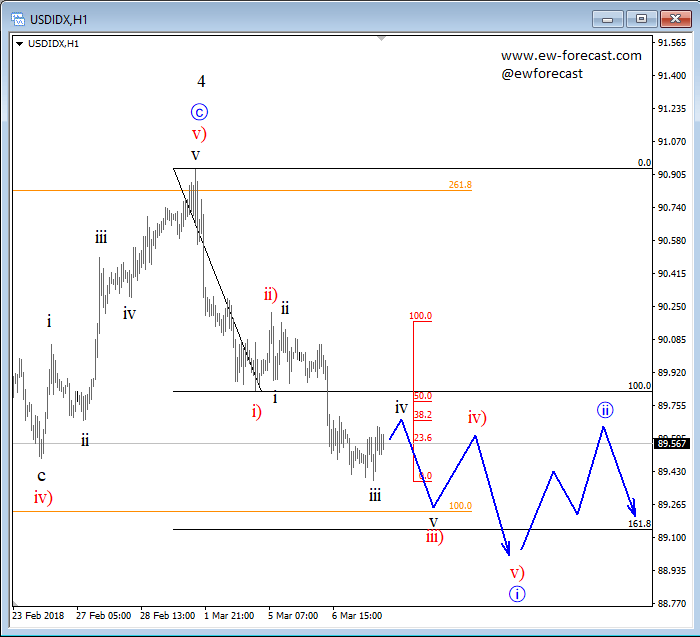

USD Index is trading in a new bearish cycle, with sub-wave iv of three in action. This minor pullback can see resistance around the 23.6/50.0 Fibonacci ratio, from where a new fall into final wave v may follow. Once five waves are visible within red wave iii), that is when a bigger pullback as red wave iv) will follow.

USD Index is trading in a new bearish cycle, with sub-wave iv of three in action. This minor pullback can see resistance around the 23.6/50.0 Fibonacci ratio, from where a new fall into final wave v may follow. Once five waves are visible within red wave iii), that is when a bigger pullback as red wave iv) will follow.

USD Index, 1H

Japanese Yen Ticks Higher, GDP Next

The Japanese yen has posted small gains in the Wednesday session. In North American trade, USD/JPY is trading at 105.98, down 0.13% on the day. On the release front, the US ADP Nonfarm Payrolls report ticked higher to 235 thousand, easily beating the estimate of 199 thousand. Later in the day, Japan Final GDP for the fourth quarter, which is expected to slip to 0.2%. On Thursday, the US releases unemployment claims. Japan will publish Household Spending and the Bank of Japan will release a rate statement.

Will the Bank of Japan drop any hints about exiting it massive stimulus program? On Friday, BoJ Governor bolstered the yen when he said that the BoJ would consider exiting from its ultra-accommodative monetary policy if its inflation target of around 2020 was reached in early 2020. Kuroda’s remarks were unusual in that they mentioned a possible “exit” from its stimulus program, and this caught the markets off guard. The BoJ has been lagging behind the Fed and other central banks in winding up stimulus, but Kuroda added that the Bank would normalize policy if “economic conditions become favorable and our price target is achieved”. Any additional hints from Kuroda or his colleagues about normalization could strengthen the yen, which has run roughshod over the dollar in 2018, with gains of 6.3%.

In the US, tensions over proposed tariffs on steel imports continue to hurt the US dollar. President Trump appears set on applying stiff tariffs of 25% on steel, much to the consternation of the European Union and other US trading partners. However, there is plenty of domestic opposition to Trump’s plan, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. If Trump doesn’t back down, the Republicans could even resort to legislation to limit Trump’s authority on tariffs. The announcement of the tariffs last week sent the dollar broadly lower, and if the tariffs are introduced, negative investor sentiment could continue to weigh on the dollar.

CAD staying the weakest after BoC, DOW shows resilience

The US session is so far rather dull. Canadian Dollar remains the weakest one for the day and the week. Cautious BoC statement gave the Loonie no support. Fresh selling is seen, together with rebound in US stocks.  Talking about stocks, they're rather resilient so far. There are rumors that Trump is going to sign presidential proclamation tomorrow regarding the steel and aluminum tariffs.

Talking about stocks, they're rather resilient so far. There are rumors that Trump is going to sign presidential proclamation tomorrow regarding the steel and aluminum tariffs.

DOW dipped to as low as 24571.50 but recovered. Risk stays on the downside. As we pointed out before, 25000 seems to be tough hurdle. But stocks' reaction to the Gary Cohn resignation news is rather muted.