Sample Category Title

Daily Wave Analysis: EUR/USD Prepares For ABC Zigzag In Bearish Wave 2

Currency pair EUR/USD

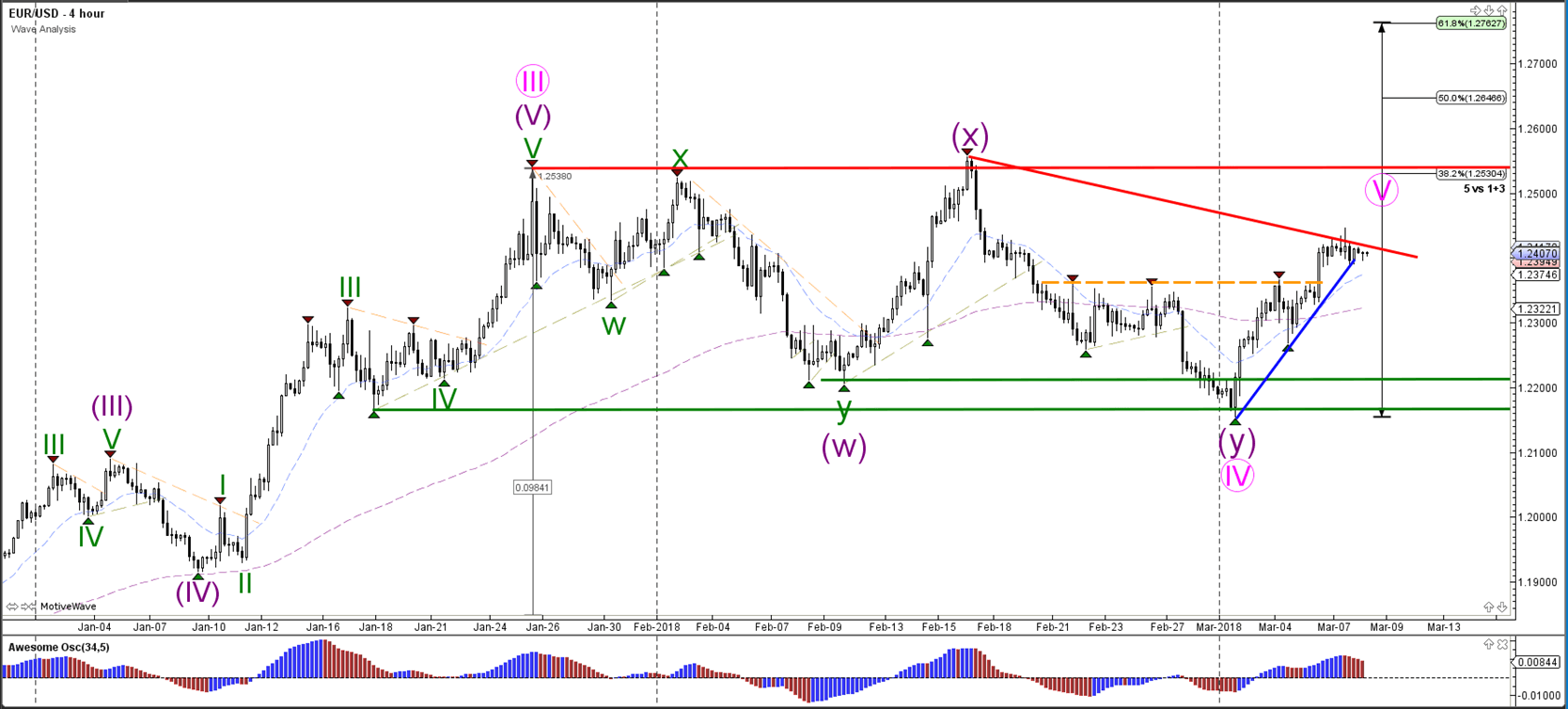

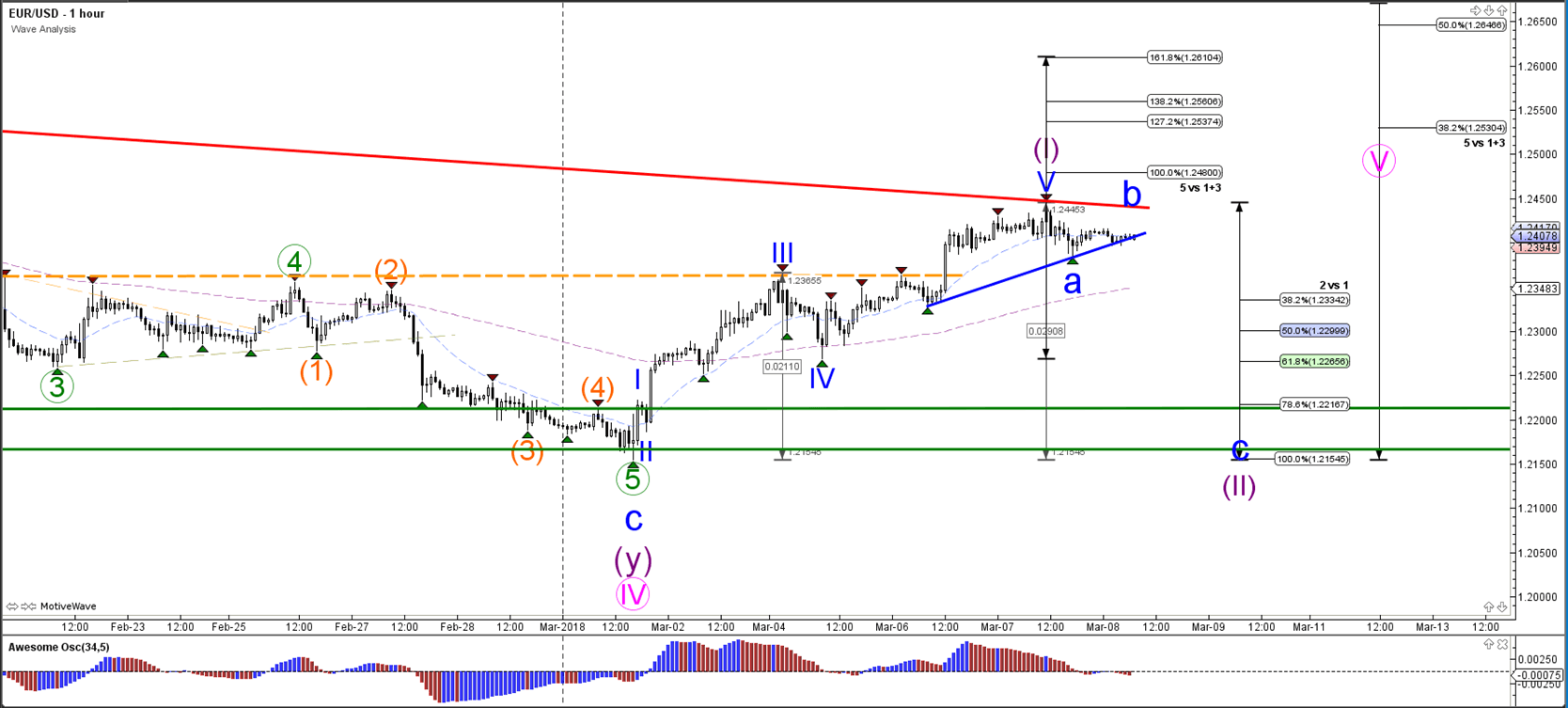

The EUR/USD has probably started with the wave 5 (pink) pattern but a break above the previous top (red) and trend line (red) is needed before price can potentially reach the 61.8% Fibonacci target.

The EUR/USD is in a break or bounce spot. A break above the 78.6% Fib target could price extend the wave 5 to higher Fib levels whereas a bearish break could see price retest the Fib levels of wave 2.

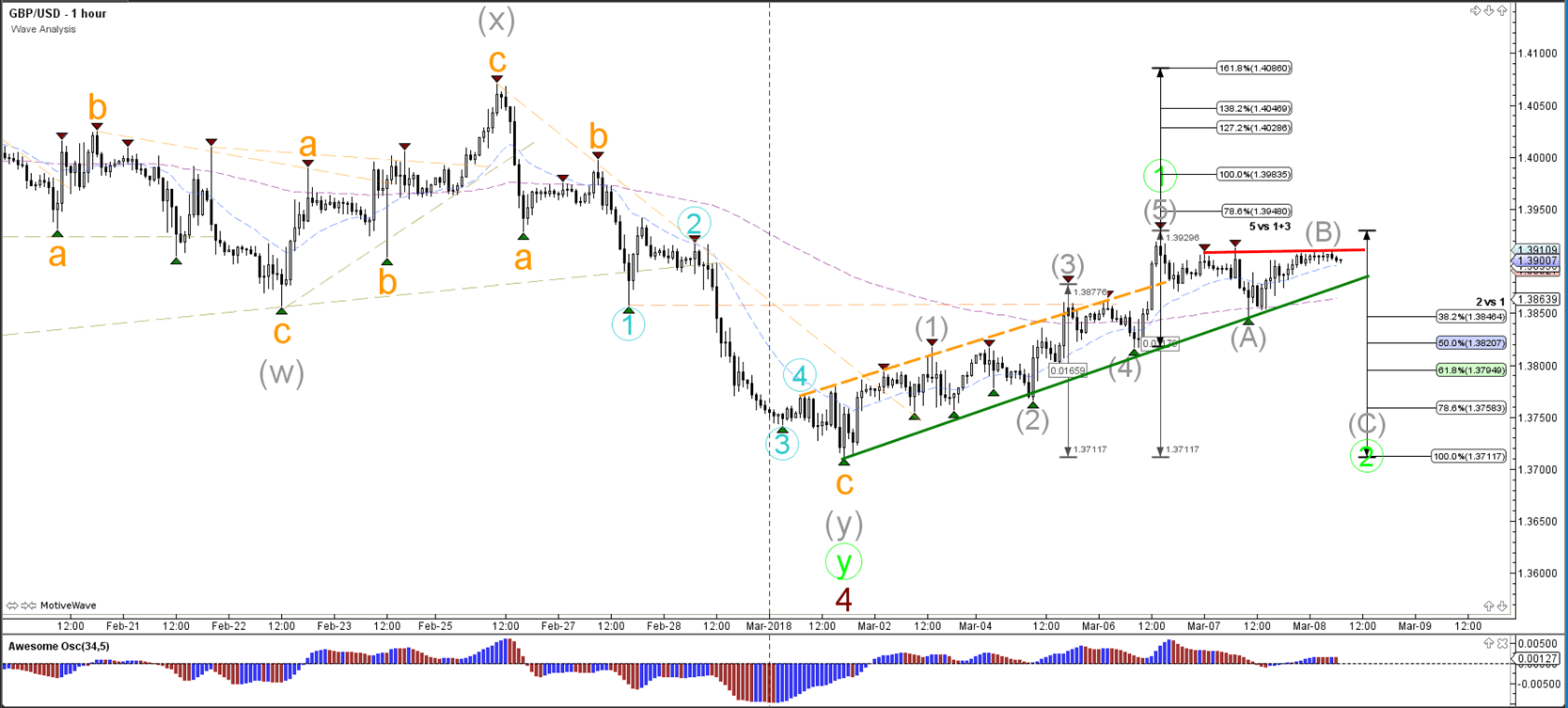

Currency pair GBP/USD

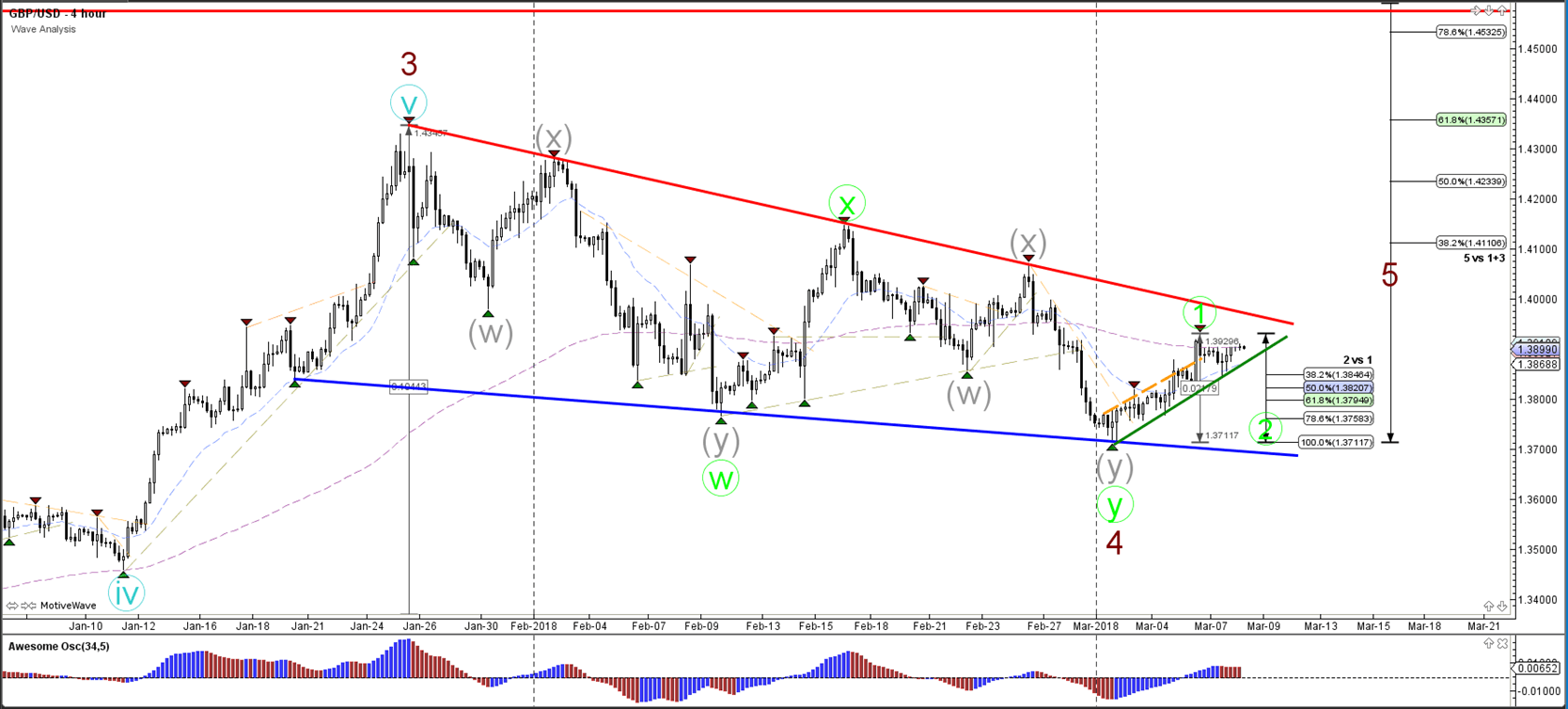

The GBP/USD bullish momentum is probably creating a wave 1 (green). A bullish break above resistance (red) could confirm wave 5 (brown).

The GBP/USD seems to have completed a 5th wave (grey) and could correct lower when it breaks support. Alternatively, it could break for one more higher high and complete wave 5 at the Fib targets.

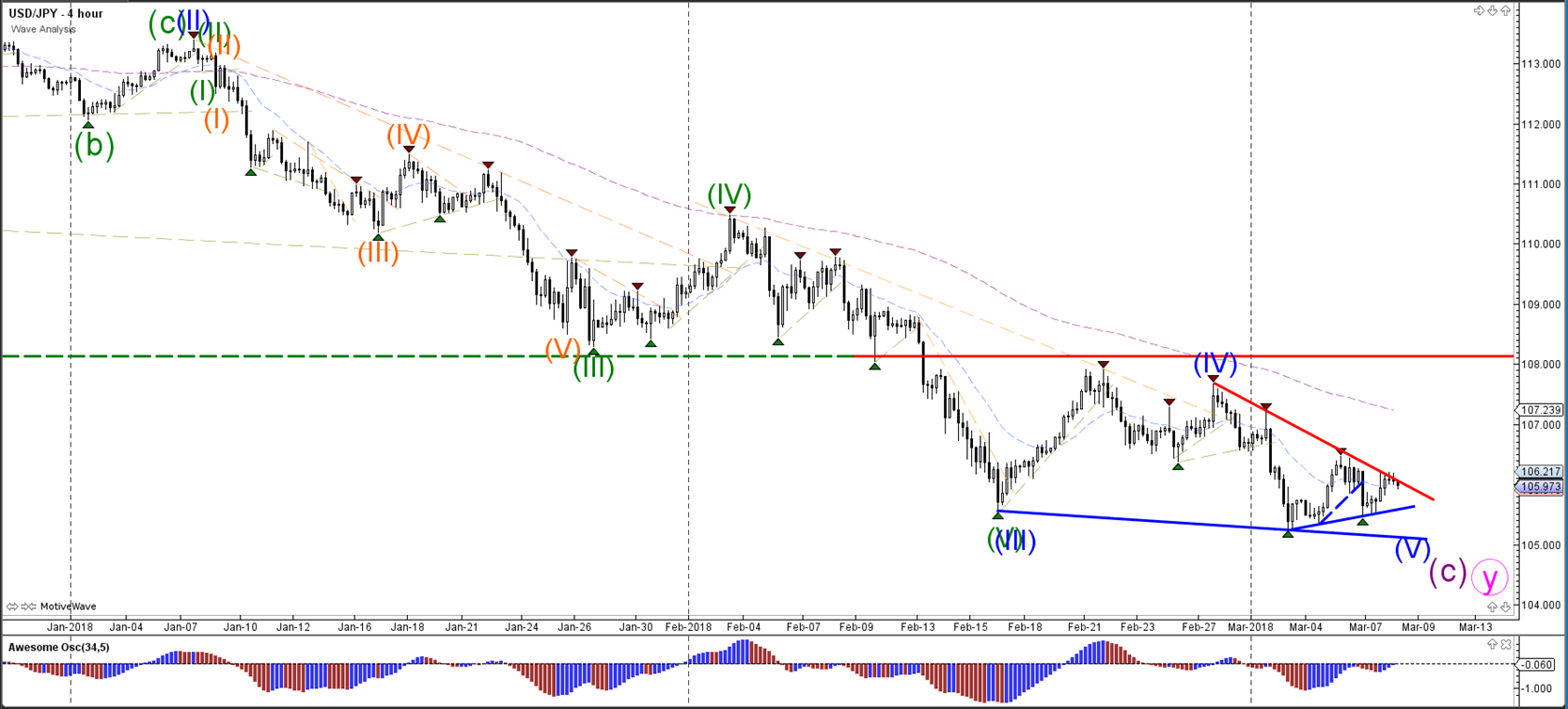

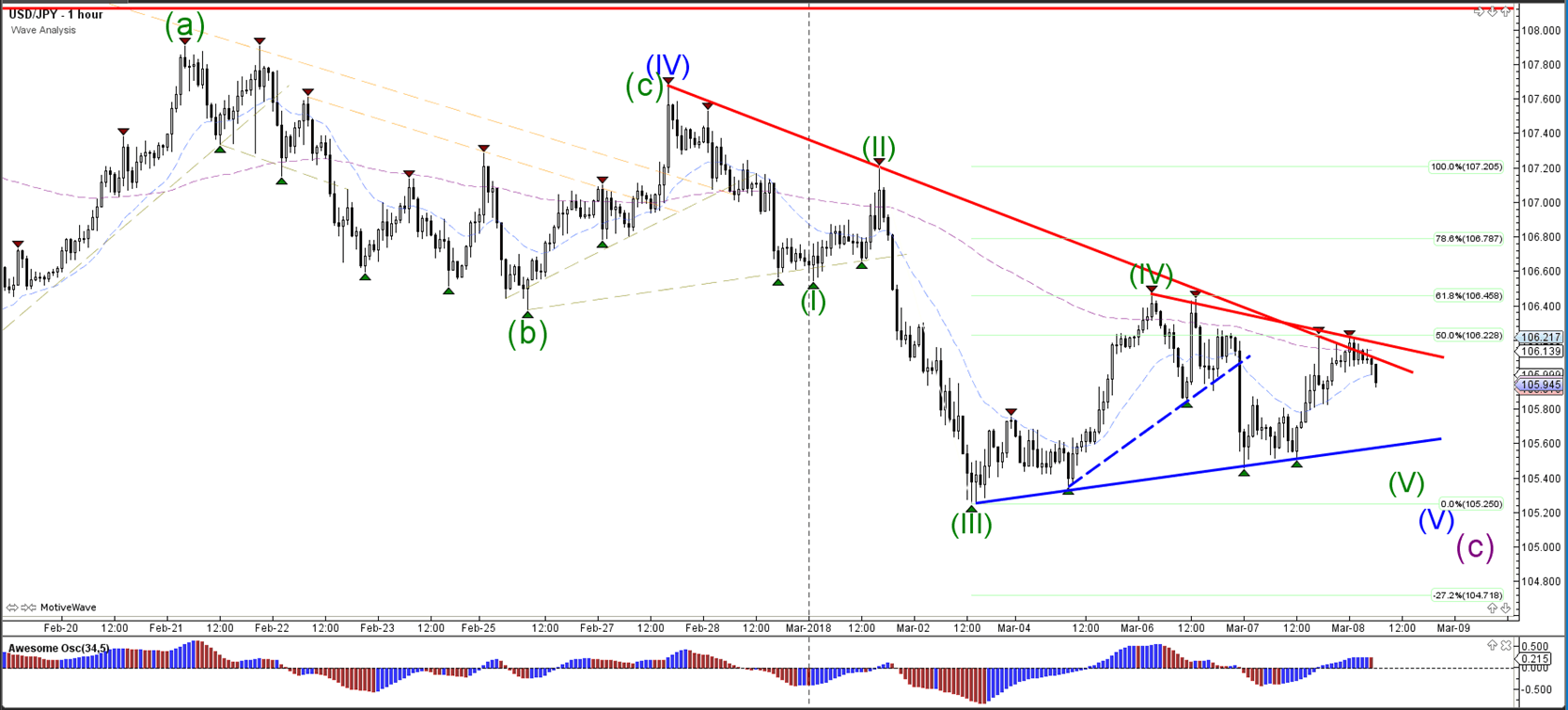

Currency pair USD/JPY

The USD/JPY did not manage to break above the resistance trend line (red) and therefore could still be in a wave 5 (blue).

The USD/JPY is building a triangle pattern.

Market Update – Asian Session: China Reports Unexpected Trade Surplus In Feb

Headlines/Economic Data

Asian equity markets trade generally higher

Wynn Macau rises after release of Jan-Feb results

China reports unexpected Feb trade surplus amid higher than expected exports and lower imports

China Jan-Feb steel products exports -27.1% y/y

Japan Jan Trade deficit beats expectations

In Feb, Japanese sold a net of ¥2.73T in foreign bonds.

Australia/New Zealand

ASX 200 opened +0.3%; closed: +0.7%%

ASX 200 Utilities Index +1.9%, Consumer Discretionary +1.3%, Telecom +1.1%, Financials +0.8%; Resources -0.5%

(AU) AUSTRALIA JAN TRADE BALANCE: A$1.06B V A$160ME

(AU) Australia Feb Port Hedland Iron Ore Shipments to China: 31.3M tons v 34.7M m/m

(NZ) New Zealand Q4 Manufacturing Activity Volume Q/Q: 1.0% v 0.3% prior; Manufacturing Activity Q/Q: 2.8% v 0.5% prior

China/Hong Kong

Shanghai Composite opened -0.1%, Hang Seng +1.1%

Hang Seng Services Index +2.3% (gaming companies rise), Consumer Goods +1.9%, Info Tech +1.7%, Telecom +1.5%, Energy +1.4%, Financials +1.3%, Property/Construction +1.2%

Wynn Macau [1128.HK]: Rises over 5% after reporting Jan-Feb Rev +19%

(CN) CHINA FEB TRADE BALANCE (USD): +$33.7B V -$5.7BE; Exports Y/Y: 44.5% v 11.0%e; Imports Y/Y: 6.3% v 8.0%e

(CN) CHINA FEB FOREIGN RESERVES: $3.135T V $3.155TE (1st MoM decline in 13 months; released on March 7th)

(CN) China PBoC Open Market Operations (OMO): Skips OMO (4th straight session): Net: CNY100B drain

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3239 V 6.3294 PRIOR

Japan

Nikkei 225 opened +1.1%; closed +0.5%

TOPIX Electric Appliances Index +0.9%, Real Estate +0.6%

(JP) JAPAN Q4 FINAL GDP SA Q/Q: 0.4% V 0.2%E; ANNUALIZED Q/Q: 1.6% V 1.0%E; Business spending Q/Q: 1.0% v 1.3%e; Deflator Y/Y: +0.1% v 0.0%e

(JP) Japan Jan Trade Balance (BoP Basis): -¥666.6B v -¥695.5Be

(JP) Japan Jan Current Account Balance: ¥607.4B v ¥437.4Be

(JP) Japan FSA: Orders suspension of business at cryptocurrency exchanges including Bit Station and FSHO for 1-month beginning on March 8th

Looking Ahead: BoJ policy statement due for release on Friday

Korea

Kospi opened +0.8%Samsung Electronics

Samsung Electronics [005930.KR]: Could report Q1 operating profit around KRW14T v KRW9.9T y/y; The profit is seen declining q/q (from KRW15.2T) amid declining demand for displays, says the report. – Yonhap

(NK) North Korea govt reportedly has offered a conditional halt to its ICBM program - Korean press

(KR) South Korea Finance Min Kim: Expects South Korea will not be labelled FX manipulator by the US Treasury

Other Asia

Singapore Exchange [SGX.SG]: Reports Feb total securities market turnover value S$32.8B, +12% m/m and +16% y/y (highest since May 2013); Feb total derivatives volume +45% y/y

North America

US equity markets ended mixed: Dow -0.3%, S&P500 -0.1%, Nasdaq +0.3%, Russell 2000 +0.8%

S&P500 Technology +0.6%; Consumer Staples -0.9%

(US) White House spokesperson Sanders: there could be potential carve outs for Canada and Mexico, and could extend to other countries as determined on a national security basis

(US) US steel and aluminum tariffs said to temporarily exempt Canada and Mexico for 30-days with extensions possible depending on NAFTA talks - Washington Post

(US) Separately, White House reportedly could have tariff signing ceremony at noon tomorrow – NYT

(US) CNBC's Javers: there could be more conversations in the White House on Thurs or Fri about further trade actions, including possibly against China

(US) White House floats possible successors for Gary Cohn's position; Some of the names being floated: Shahira Knight, Jim Donovan, Kevin Hassett, Larry Kudlow, Chris Liddell, Mick Mulvaney, Peter Navarro, Mark Calabria, Bob Steel. - press

(US) White House Trade Adviser Navarro: I'm not on the list to replace economic adviser Gary Cohn

(US) Fed's Bostic (2018 voter, dove): Trade wars are not winnable; Have to see details on the final tariff plan to estimate the economic impact; December I was forecasting two rate hikes; has adjusted that to three now; Everything is on the table in regards to two, three or four rate hikes in 2018 - comments from Florida

(US) DOE CRUDE: +2.4M V +2.5ME;

Express Scripts [ESRX]: Cigna said to be near deal to acquire the company - US financial press

Europe

(EU) ECB Governing Council: ECB has no objections to Spain's de Guindos taking vice presidency

(TR) Moody's cuts Turkey sovereign rating one notch to Ba2 from Ba1; outlook to Stable from Negative

(UK) UK FEB RICS HOUSE PRICE BALANCE: 0% V 7%E (lowest since March 2013)

Looking Ahead: ECB rate decision expected later today

Levels as of 01:00ET

Hang Seng +1.3%; Shanghai Composite +0.3%; Kospi +0.6%

Equity Futures: S&P500 flat; Nasdaq100 flat, Dax flat; FTSE100 +0.2%

EUR 1.2396-1.2416 ; JPY 105.92-106.22; AUD 0.7814-0.7841 ;NZD 0.7272-0.7298

Feb Gold flat at $1,327/oz; Feb Crude Oil flat at $61.17/brl; Copper -0.4% at $3.120/lb

The Key Event Today Will Be The ECB Meeting

Market movers today

The key event today will be the ECB meeting , see preview . We do not expect any changes to the policy rates and find it unlikely that the ECB will outline a decision on extension/termination of the QE programme before June. That said, we are looking for the ECB to remove the easing bias in the forward guidance , meaning it will drop the paragraph about increasing the QE programme in size and/or duration if economic conditions turn less favourable.

US President Donald Trump's protectionist measures will continue to be in focus, as he plans to sign orders for steel and aluminium tariffs today at 21:30 CET. For more on US trade policy and protectionism see our piece Research US: Symbolic protectionism with limited impact on growth and inflation but risks remain .

On the data front, we have German factory orders and US jobless claims.

In Scandi , it is time for industrial production data out of Norway and the Riksbank will hold its Open Forum.

Selected market news

Still a lot of focus on global trade and protectionism. Yesterday evening, a White House official said Trump plans to sign orders for the steel and aluminium tariffs today at 21:30 CET but NAFTA countries (and possibly other allies) will initially be exempt and Republican lawmakers issued a statement yesterday expressing concerns that broad tariffs could cost job and lift inflation, hurting the Republicans chances to win the mid-term elections in November. Instead, they think Trump should target China, see CNBC . With respect to China, we think the administration is waiting for the official ongoing investigation into Chinese stealing of US intellectual property before we see some action. China s foreign minister Wang Yi said yesterday that China would make a 'justified and necessary response' to measures hitting the country. As long as Trump's measures are symbolic, we believe China will be cautious in its response, as the US is its most important export market. For more on this topic see our piece released yesterday Research US: Symbolic protectionism with limited impact on growth and inflation but risks remain .

Yesterday, the EU published its draft guidelines for post-Brexit relationship, which did not contain many surprises. The EU wants tariff-free and quota-free trade but reiterated that there can be no cherry picking by choosing which parts of the EU single market the UK wants to be a part of. The EU still thinks the only likely solution is a free trade agreement like Canada. Services will only be included with restrictions and there will be no special access for banks. The UK Chancellor of the Exchequer Philip Hammond said it is 'hard' to see an agreement not covering services, as the EU has a surplus in goods while the UK has a surplus in services. This is in line with our base case, as we expect a Canada-style FTA but with more services included.

The Fed's blackout period begins next week and Bostic (voter, dovish) said yesterday that he has lifted his personal view on the number of Fed rate hikes from two to three, supporting our case that the Fed may just have become more confident in its three-hike signal.

German factory orders -3.9% mom, Swiss unemployment rate at 2.9%

German factory orders Feb: -3.9% mom vs exp -1.6% mom vs prior 3.0% mom

Swiss unemployment rate Feb: 2.9% vs exp 2.9% vs prior 3.0%

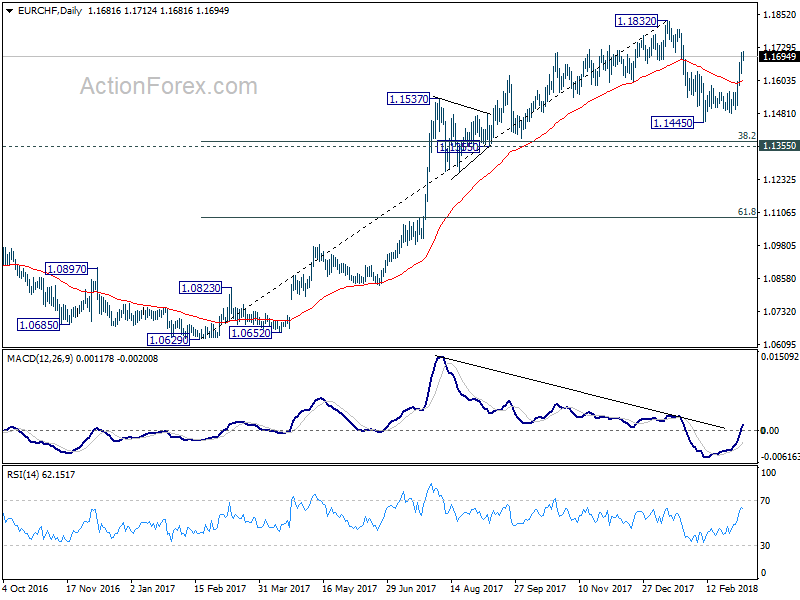

Little reaction to the data as markets await ECB later today. Recent rebound in EUR/CHF suggests pull back from 1.1832 has completed at 1.1445 already. But the corrective pattern from 1.1832 could still extend with another falling leg before completion. Mario Draghi's message will likely decide whether EUR/CHF will target 1.1832 first, or 1.1445 again first.

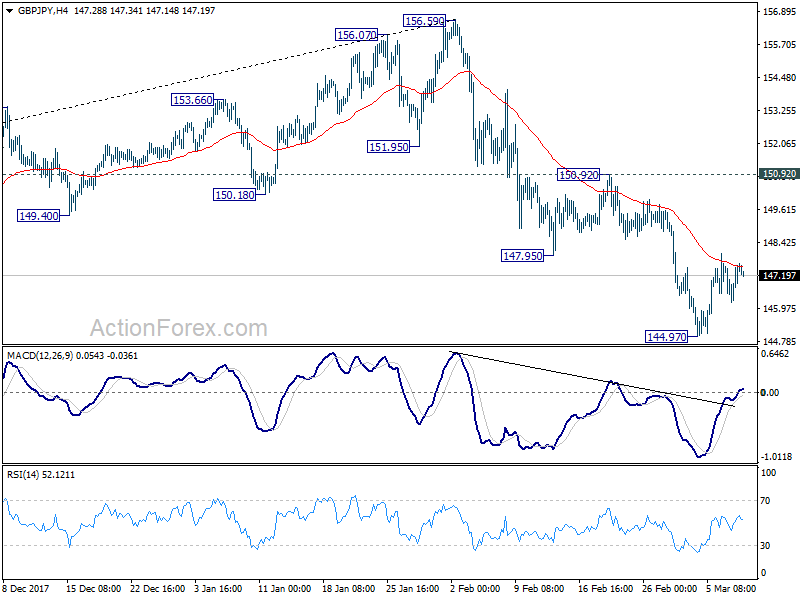

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.60; (P) 147.08; (R1) 147.94; More...

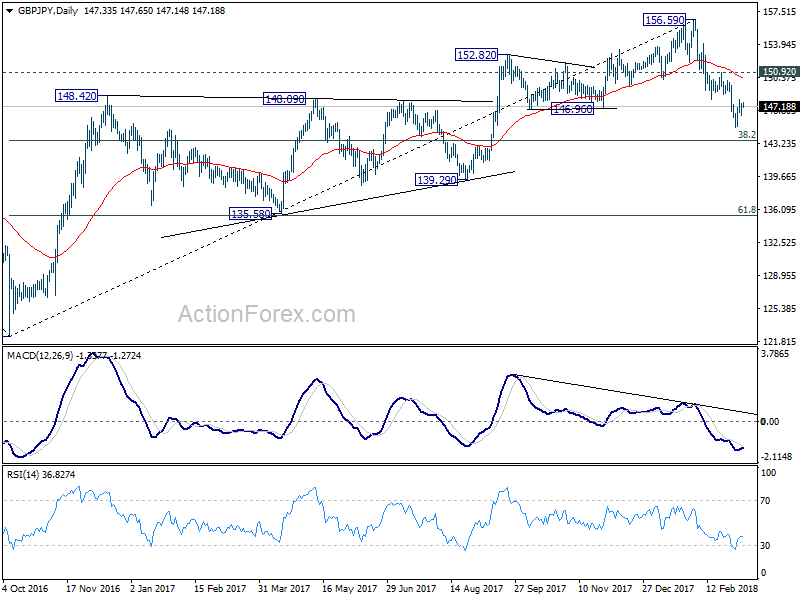

Intraday bias in GBP/JPY remains neutral as recovery from 144.97 temporary low is in progress. While further rise cannot be ruled out, upside should be limited below 150.92 resistance to bring another decline. Break of 144.97 will extend the fall from 156.69 to 143.51 medium term fibonacci level next. We'll look for bottoming signal there. But firm break will target 139.29 support.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

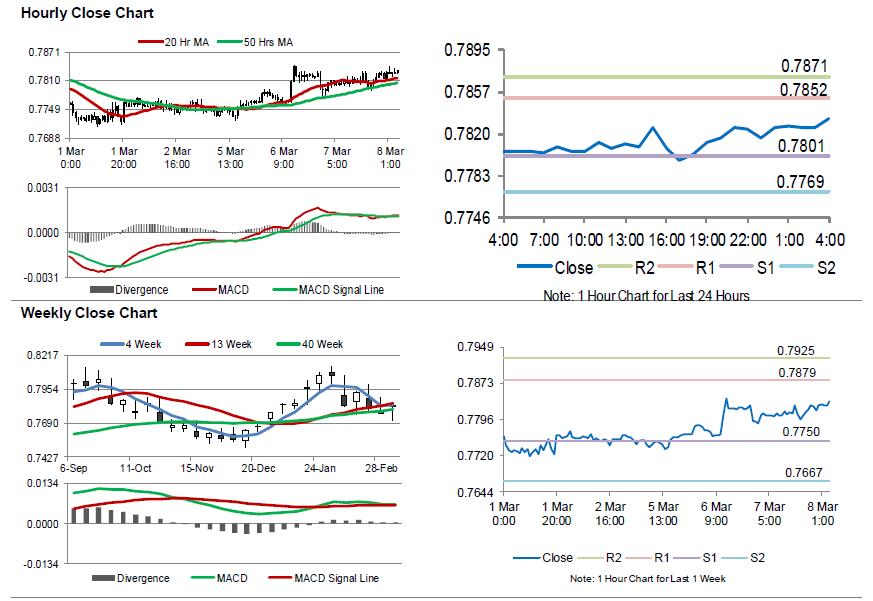

Australia Posted A More-Than-Expected Trade Surplus In January

For the 24 hours to 23:00 GMT, the AUD rose 0.09% against the USD and closed at 0.7816.

LME Copper prices declined 1.4% or $95.5/MT to $6873.0/MT. Aluminium prices declined 1.1% or $23.5/MT to $2112.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7833, with the AUD trading 0.22% higher against the USD from yesterday’s close, after latest data revealed that Australia’s trade balance returned to surplus in January.

Overnight data indicated that, Australia reported a seasonally adjusted trade surplus of A$1055.0 million in January, beating market expectations for a surplus of A$160.0 million, amid a sharp fall in imports. The nation had registered a revised trade deficit of A$1146.0 million in the prior month.

Elsewhere, in China, Australia’s largest trading partner, trade surplus climbed more-than-estimated to $33.74 billion in February, after registering a revised surplus of $20.35 billion in the previous month. Markets were expecting the country’s trade deficit to stand at $5.70 billion.

Moreover, the nation’s exports surged more-than-estimated by 44.5% on an annual basis in February, accelerating at its fastest pace in 3 years. Exports had recorded a rise of 11.1% in the prior month, while investors had envisaged for a gain of 11.0%. Further, the nation’s imports registered a rise of 6.3% YoY in February, falling short of market expectations for an advance of 8.0%. Imports had risen by a revised 36.8% in the prior month.

The pair is expected to find support at 0.7801, and a fall through could take it to the next support level of 0.7769. The pair is expected to find its first resistance at 0.7852, and a rise through could take it to the next resistance level of 0.7871.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

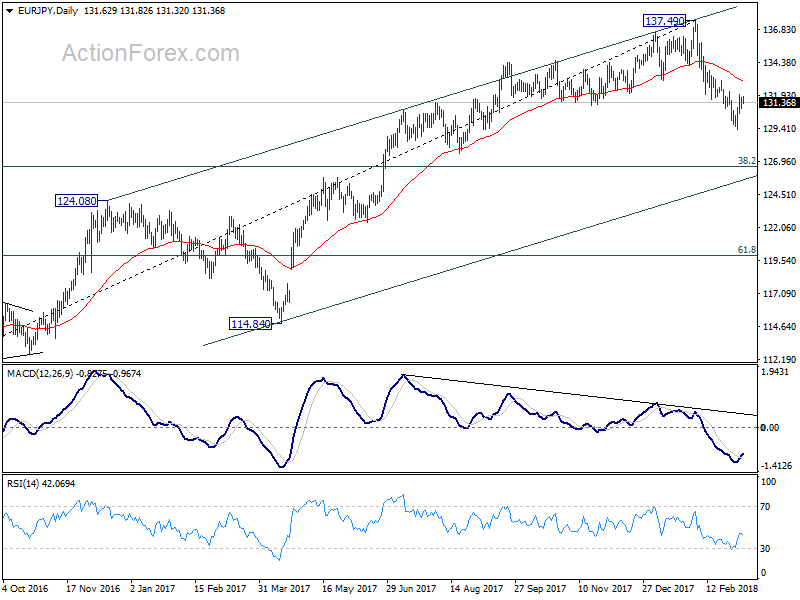

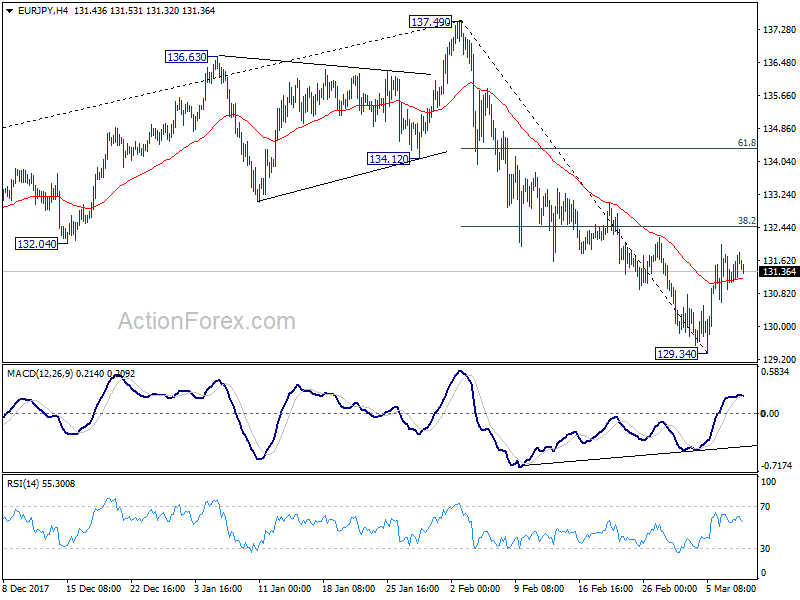

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.12; (P) 131.43; (R1) 131.94; More....

No change in EUR/JPY's outlook. A short term bottom should be in place at 129.34, on bullish convergence condition in 4 hour MACD. Further rise is expected to 38.2% retracement of 137.49 to 129.34 at 132.45. Break will target 61.8% retracement at 134.37. However, decline 137.49 shouldn't be finished yet. We'd still expect another fall at a later stage. And break of 129.34 will pave the way to 126.61 medium term fibonacci level

In the bigger picture, current development argues that rise from 109.03 has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

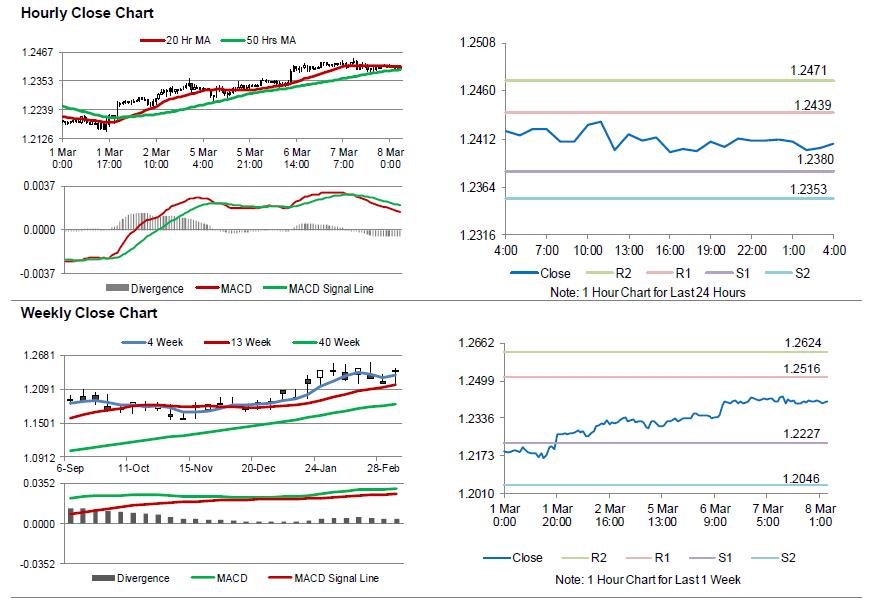

Euro-Zone’s Economic Growth Slowed As Initially Estimated In 4Q 2017

For the 24 hours to 23:00 GMT, the EUR declined 0.06% against the USD and closed at 1.2411.

On the macro front, the Euro-zone's seasonally adjusted final gross domestic product (GDP) climbed 0.6% on a quarterly basis in the October-December 2017 period, confirming the preliminary print. The region's GDP had risen by a revised 0.7% in the previous quarter.

In the US, data indicated that ADP private sector employment increased more-than-anticipated by 235.0K in February, reinforcing the view of underlying strength in the nation's labour market. The private sector employment had registered a revised gain of 244.0K in the previous month, while investors had expected for an advance of 200.0K.

On the contrary, the nation's trade deficit widened to a more than 9-year high level of $56.6 billion in January, suggesting that trade would act as a drag on the nation's economic growth. The nation had posted a revised trade deficit of $53.9 billion in the previous month, while investors had envisaged it to widen to $55.0 billion.

Another set of data revealed that consumer credit in the US grew $13.91 billion in January, undershooting market consensus for an advance of $17.65 billion. In the previous month, consumer credit had climbed by a revised $19.21 billion. Meanwhile, the nation's MBA mortgage applications recorded a rise of 0.3% in the week ended 02 March, after recording an increase of 2.7% in the previous week.

Separately, the Federal Reserve's (Fed) Beige Book report indicated that the US economy continued to grow at a “modest to moderate” pace in January and February. In addition, it showed that firms across the 12 districts observed widespread labour market tightness that contributed to “moderate inflation”, while many regions noted a pick-up in wage growth since the beginning of the year.

In the Asian session, at GMT0400, the pair is trading at 1.2407, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.2380, and a fall through could take it to the next support level of 1.2353. The pair is expected to find its first resistance at 1.2439, and a rise through could take it to the next resistance level of 1.2471.

Moving ahead, the European Central Bank's (ECB) monetary policy meeting, due later in the day, will be closely watched for further hints on monetary policy as the central bank is widely expected to keep interest rates unchanged. Moreover, the US initial jobless claims data, set to release later today, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

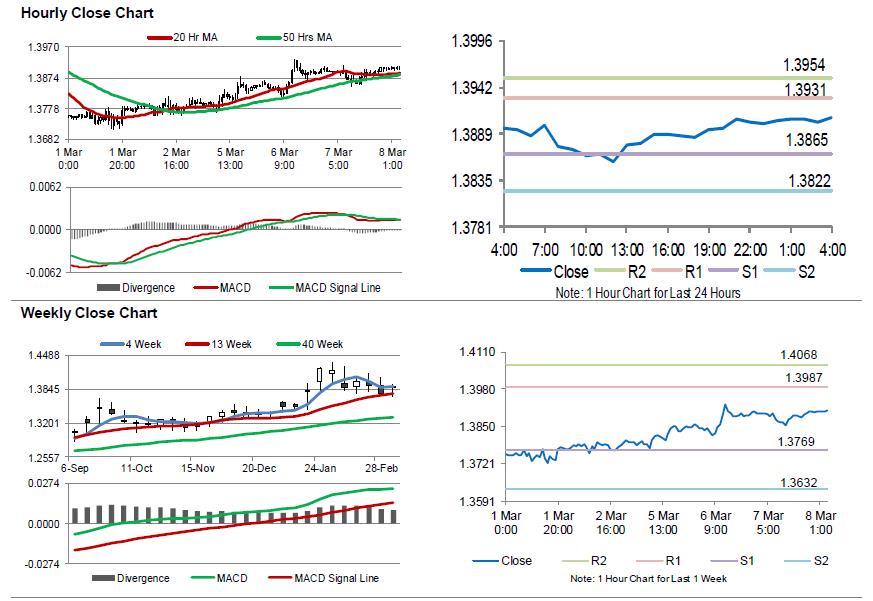

UK’s Halifax House Prices Rose For The First Time Since November 2017 In February

For the 24 hours to 23:00 GMT, the GBP marginally rose against the USD and closed at 1.3901.

On the macro front, Britain's Halifax house price index rebounded 0.4% on a monthly basis in February, at par with market expectations and rising for the first time in 3 months, highlighting that the nation's housing market may be regaining momentum. In the prior month, the index had registered a revised drop of 0.5%.

In the Asian session, at GMT0400, the pair is trading at 1.3907, with the GBP trading slightly higher against the USD from yesterday's close.

Overnight data indicated that the nation's RICS house price balance unexpectedly fell to a level of 0.0 in February, whereas market participants had anticipated it to remain steady at 7.0.

The pair is expected to find support at 1.3865, and a fall through could take it to the next support level of 1.3822. The pair is expected to find its first resistance at 1.3931, and a rise through could take it to the next resistance level of 1.3954.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

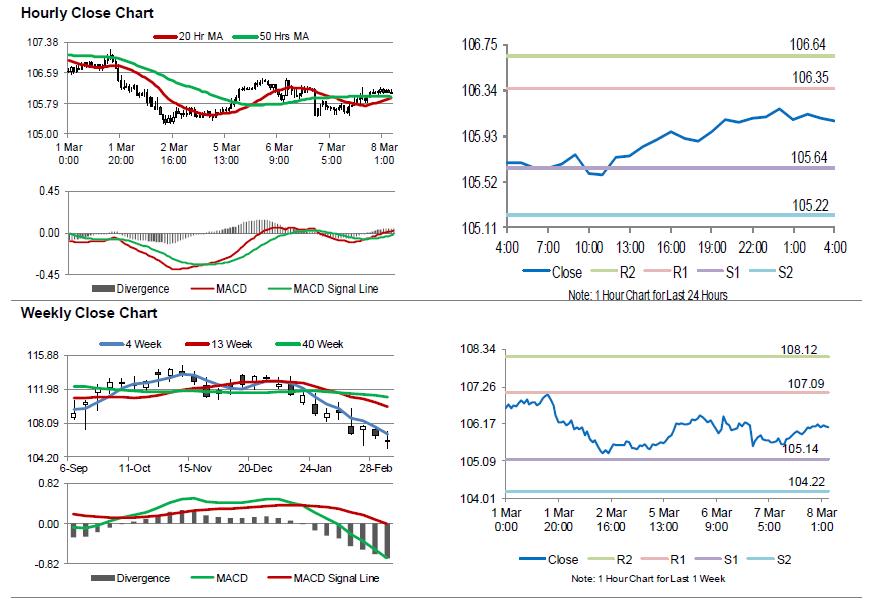

Japan’s Economic Growth Revised Sharply Higher In 4Q 2017

For the 24 hours to 23:00 GMT, the USD rose 0.35% against the JPY and closed at 106.10.

In the Asian session, at GMT0400, the pair is trading at 106.06, with the USD trading slightly lower against the JPY from yesterday's close.

Overnight data showed that final reading on Japan's GDP expanded more than initially estimated by 0.4% on a quarterly basis in the final three months of 2017, while the preliminary figures had indicated an advance of 0.1%. The nation's GDP had advanced 0.6% in the prior quarter.

Other data indicated that the nation posted a less-than-expected (BOP basis) trade deficit of ¥666.6 billion in January, following a surplus of ¥538.9 billion in the previous month. Markets were anticipating the nation to register a (BOP basis) trade deficit of ¥695.5 billion.

Earlier in the session, data revealed that Japan's Eco Watchers Survey for the current situation recorded an unexpected drop to a level of 48.6 in February, confounding market expectations for a rise to a level of 50.5. The index had registered a reading of 49.9 in the prior month. Furthermore, the nation's Eco Watchers Survey for the future outlook declined more-than-anticipated to a level of 51.4 in February, against market consensus for a fall to a level of 51.7. In the prior month, the index had registered a reading of 52.4.

The pair is expected to find support at 105.64, and a fall through could take it to the next support level of 105.22. The pair is expected to find its first resistance at 106.35, and a rise through could take it to the next resistance level of 106.64.

Moving ahead, the Bank of Japan's interest rate decision, due tomorrow, will keep investors on their toes. The central bank is anticipated to stand pat on monetary policy.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.