Sample Category Title

Elliott Wave View: USDJPY Rally Should Fail Below 107.9

Short Term USDJPY Elliott Wave view suggests that the rally to 107.9 ended Minor wave X. Pair is expected to resume lower while bounces stay below this level. Down from Minor wave X at 107.91, Minor wave Y is in progress as a double three Elliott Wave Structure. Minute wave ((w)) of Y ended at 105.23 as a zigzag Elliott Wave pattern. Above from there, Minute wave ((x)) is currently in progress to correct cycle from February 21 peak as a double three Elliott Wave structure in 3, 7, or 11 swing.

Internal of Minute wave ((w)) of Y unfolded as a zigzag Elliott Wave pattern where Minutte wave (a) ended at 106.35, Minutte wave (b) ended at 107.67, and Minutte wave (c) of ((w)) ended at 105.23. Up from there, internal of Minute wave ((x)) is unfolding as a double three Elliott Wave Structure where Minutte wave (w) ended at 106.46 and Minutte wave (x) ended at 105.43. Near term, expect pair to extend higher towards 106.66 – 106.95 area to end Minutte wave (y) of ((x)), then as far as pivot at 2/21 peak (107.9) stays intact, expect pair to extend lower. We don’t like buying the pair.

USDJPY 1 Hour Elliott Wave Chart

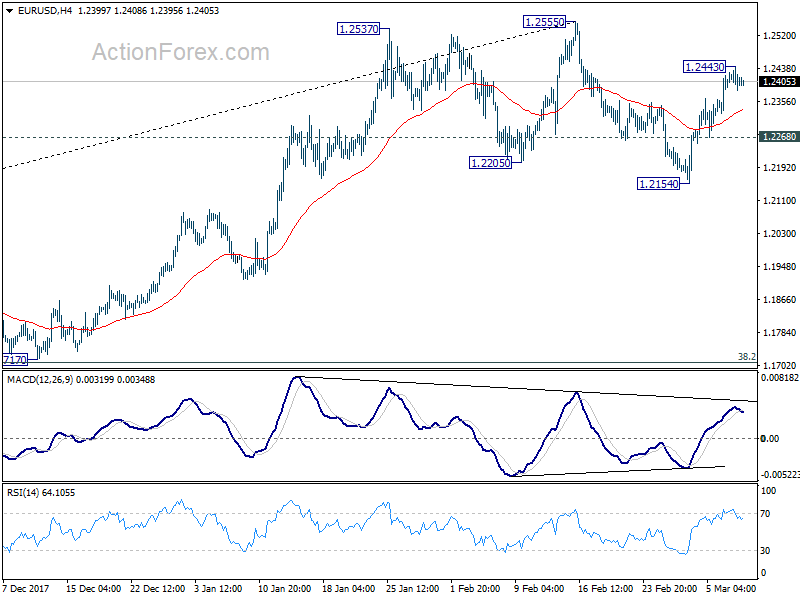

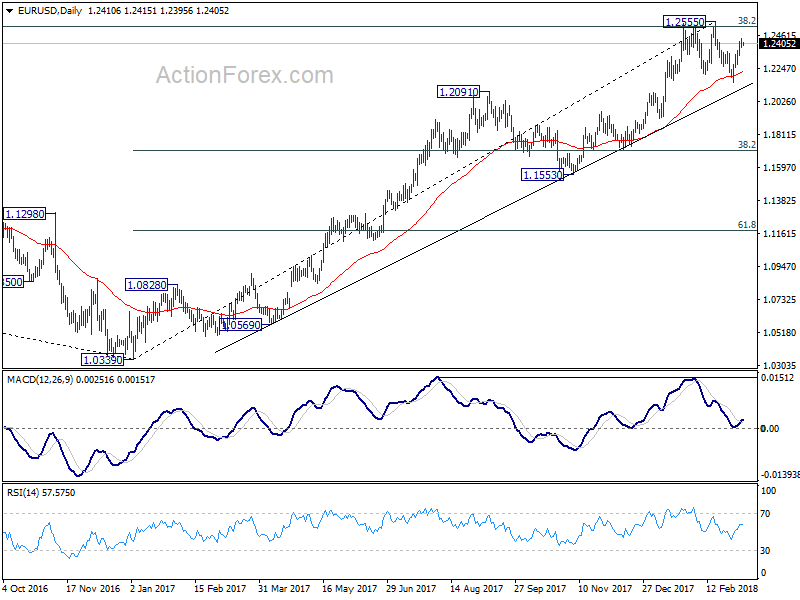

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2381; (P) 1.2413 (R1) 1.2441; More....

A temporary top is in place at 1.2443 in EUR/USD with 4 hour MACD crossed below signal line. Intraday bias is turned neutral first. For the moment, further rise will remain mildly in favor as long as 1.2268 minor support holds. Firm break of of 1.2555 and 1.2516 long term fibonacci level will carry larger bullish implications. On the downside, below 1.2268 minor support will turn bias back to the downside for 1.2154 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Euro Pares Gains ahead of ECB, Canadian Dollar Rebounds on Tariff Exclusion

The financial markets show that investors are well prepared for the steel and aluminum tariff by the US. Dow closed down just -0.33% overnight, at 24801.36. 10 year yield gained 0.006 to 2.883, staying in near term sideway consolidation. Nikkei is trading up 0.5% at the time of writing while HSI is up 1.4%. In the currency markets, Yen is paring some gains as risk aversion recedes and commodity currencies recover today. In particular, Canadian Dollar responded rather positively to the news that the country will be temporarily excluded from the tariffs. Meanwhile, Euro is broadly softer today, digesting recent gains and as traders are preparing for ECB.

Trump to sign tariff order today, exclude Canada and Mexico temporarily

US President Donald Trump is set to ignore all the oppositions from Republicans and business leaders and sign the order for steel and aluminum tariffs on Thursday afternoon at the White House. It's being planned to hold at 3:30pm ET in the Roosevelt Room. A top White House trade advisor Peter Navarro said "the proclamation will have a clause that does not impose these tariffs immediately on Canada and Mexico". But whether there will be permanent exclusion will depend on NAFTA negotiations. Press secretary also gave similar comments as "there are potential carve-outs for Canada and Mexico based on national security, and possibly other countries as well".

EU responded formally yesterday on the counter measures in a statement. Commissioner for Trade Cecilia Malmström said after the meeting of the College of Commissioners that "we have made clear that if a move like this is taken, it will hurt the European Union. It will put thousands of European jobs in jeopardy and it has to be met by firm and proportionate response. And she pointed to "the root cause of the problem in the steel and aluminium sector is global overcapacity" and, " a lot of steel and aluminium production takes place under massive state subsidies, and under non-market conditions."

Fed Bostic: No certainty to what products would be pulled into trade wars

Atlanta Fed President Raphael Bostic offered some direct comments on monetary policies. He said the tax cuts "were forcing us to more aggressive policy" But, "the trade stuff is uncertainty in the other direction" referring to Trump's initiative to impose steel and aluminum tariffs. He added that "the U.S. in this latest round has identified aluminum and steel as issues. Europe has signaled they would hit a whole host of other products that are not aluminum or steel. There is just not certainty as to which products are going to get pulled into this." And, "anyone who is engaged in any kind of international trade space has got to be concerned."

BOC Left Rates On Hold, More Concerned About US Trade Policy

As widely anticipated, BOC left the policy rate unchanged at 1.25% yesterday. The accompanying statement was more cautious than the previous one, over the trade outlook. Policymakers suggested that 'trade policy developments are an important and growing source of uncertainty for the global and Canadian outlooks', in addition to reiteration of the need for remaining 'cautious in considering future policy adjustments'. Expectations of another rate hike in April diminished after the announcement.

More on BoC: BOC Left Rates On Hold, More Concerned About US Trade Policy

Australia recorded massive AUD 1.06b trade surplus in January

Australia recorded massive trade surplus of AUD 1.06b in January, a turnaround from December's AUD -1.15b trade deficit. Exports jumped 4% mom to AUD 33.9b, with 4% rise in non-rural goods, 54% rise in non-monetary gold. Much more than offsetting -8% fall in rural goods. Imports, on the other hand, dropped -2% to AUD 32.9b. Consumption goods dropped -7%, non-monetary gold dropped -19%, capital goods dropped 1%.

China pledges "justified and necessary response" to trade wars"

China Foreign Minister Wang Yi pledged to have "justified and necessary response" to trade wars. He said that "A trade war has never been the right way to solve the problem, especially under globalization." And, these conflicts "will only harm everyone and China will surely make a justified and necessary response."

At the same time China's trade surplus widened to USD 33.7b in January, or CNY 225b. Both were way better than expectation of USD -8.5b or CNY -71b deficit. Exports rose 44.5% yoy. Imports rose 6.3% yoy.

ECB as the main focus ahead

ECB is widely expected to keep interest rate and asset purchase program unchanged today. The main question to the markets is when the central bank will start tweaking its forward guidance to pave the way for ending QE. This topic will certainly be discussed during the meeting. But it's uncertain whether ECB will take this meeting to do it. In particular, there could be some concerns over resurgence of Euro sceptics shown in Italian election. And, the intensification of risks of trade war with the US could also concerns policymakers much. But it should be noted that, the reactions in Euro could be huge even if ECB apply a "small dose" of chance in the language.

In addition, Swiss will release unemployment rate. Germany will release factory orders. Canada will release housing starts, new housing price index and building permits. US will release jobless claims as usual on a Thursday.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2381; (P) 1.2413 (R1) 1.2441; More....

A temporary top is in place at 1.2443 in EUR/USD with 4 hour MACD crossed below signal line. Intraday bias is turned neutral first. For the moment, further rise will remain mildly in favor as long as 1.2268 minor support holds. Firm break of of 1.2555 and 1.2516 long term fibonacci level will carry larger bullish implications. On the downside, below 1.2268 minor support will turn bias back to the downside for 1.2154 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity Q4 | 2.80% | 0.50% | ||

| 23:50 | JPY | Current Account (JPY) Jan | 2.02T | 1.76T | 1.48T | 1.68T |

| 23:50 | JPY | GDP Q/Q Q4 F | 0.40% | 0.20% | 0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | 0.10% | 0.00% | 0.00% | |

| 0:01 | GBP | RICS House Price Balance Feb | 0% | 7% | 8% | |

| 0:30 | AUD | Trade Balance Jan | 1.06B | 0.22B | -1.36B | -1.15B |

| 2:00 | CNY | Trade Balance (USD) Feb | 33.7B | -8.5B | 20.3B | |

| 2:00 | CNY | Trade Balance (CNY) Feb | 225B | -71B | 136B | |

| 6:45 | CHF | Unemployment Rate Feb | 2.90% | 3.00% | ||

| 7:00 | EUR | German Factory Orders M/M Jan | -1.60% | 3.80% | ||

| 12:30 | USD | Challenger Job Cuts Y/Y Feb | -2.80% | |||

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 13:15 | CAD | Housing Starts Feb | 220K | 216K | ||

| 13:30 | CAD | New Housing Price Index M/M Jan | 0.00% | |||

| 13:30 | CAD | Building Permits M/M Jan | 4.80% | |||

| 13:30 | USD | Initial Jobless Claims (MAR 3) | 216K | 210K | ||

| 15:30 | USD | Natural Gas Storage | -78B |

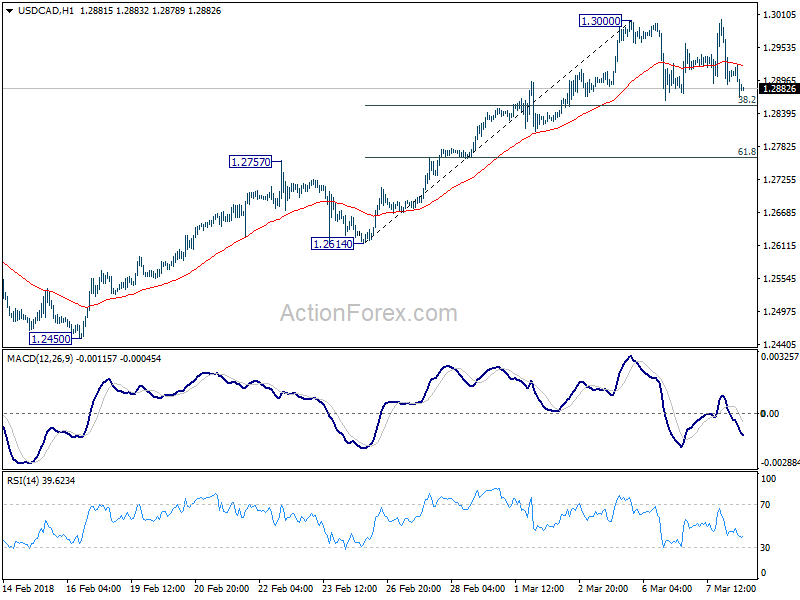

Canada and Mexico to be temporarily excluded from steel and aluminum tarrifs, CAD rebounds

Trumps is set to ignore all the oppositions from Republicans and business leaders and sign the order for steel and aluminum tariffs on Thursday afternoon at the White House. It's being planned to hold at 3:30pm ET in the Roosevelt Room. A top White House trade advisor Peter Navarro said "the proclamation will have a clause that does not impose these tariffs immediately on Canada and Mexico". But whether there will be permanent exclusion will depend on NAFTA negotiations. Press secretary also gave similar comments as "there are potential carve-outs for Canada and Mexico based on national security, and possibly other countries as well".

Canadian dollar responded quite positively to the news with USD/CAD dipping sharply after failing to take out 1.3000.

China Foreign Minister Wang Yi warned “justified and necessary response” to trade wars

China Foreign Minister Wang Yi pledged to have "justified and necessary response" to trade wars. He said that "A trade war has never been the right way to solve the problem, especially under globalization." And, these conflicts "will only harm everyone and China will surely make a justified and necessary response."

At the same time, released today, China's trade surplus widened to USD 33.7b in January, or CNY 225b. Both were way better than expectation of USD -8.5b or CNY -71b deficit.

Exports rose 44.5% yoy. Imports rose 6.3% yoy.

Australia Jan trade balance: Massive AUD 1.06b surplus

Australia recorded massive trade surplus of AUD 1.06b in January, a turnaround from December's AUD -1.15b trade deficit.

Exports jumped 4% mom to AUD 33.9b, with 4% rise in non-rural goods, 54% rise in non-monetary gold. Much more than offsetting -8% fall in rural goods.

Imports, on the other hand, dropped -2% to AUD 32.9b. Consumption goods dropped -7%, non-monetary gold dropped -19%, capital goods dropped 1%.

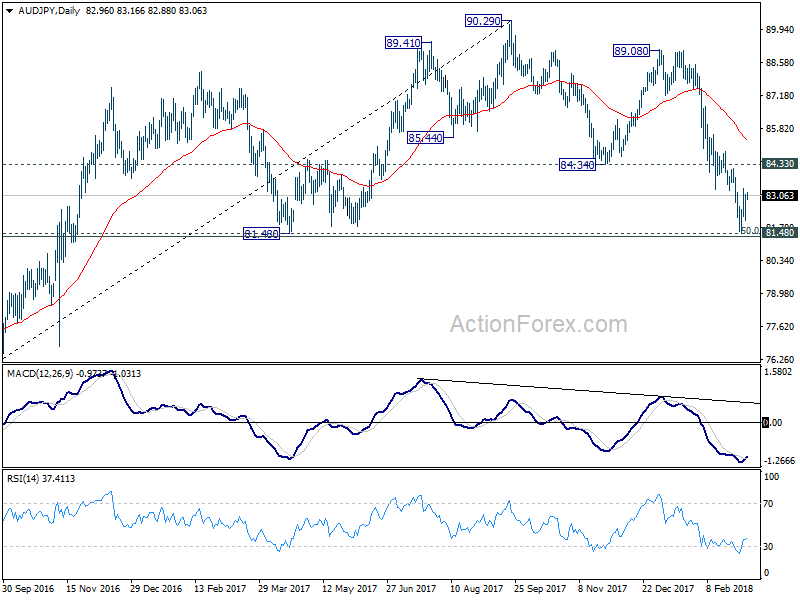

AUD/JPY is tentatively drawing strong support from key medium term cluster at 81.48, 50% retracement of of 72.39 (2016) low to 90.29 (2017 high) at 81.34. But the bigger hurdle is on 84.34 support turned resistance for confirming short term bottoming. Otherwise, risk will remain on the downside.

Market Morning Briefing: Dollar-Yen Has Again Bounced From The Crucial 105.45-105.50 Levels

STOCKS

Most of the stock indices are testing immediate resistance as seen on the respective daily candle charts. While they hold, the indices may come off in the near term. Immediate view is bearish to sideways for most indices.

Dow (24801.36, -0.33%) tested a low of 24535 yesterday but moved up to close near 24800. As mentioned yesterday, 24500 is an immediate support which if holds, could produce a bounce back towards 25500 levels in the near term. Failure to bounce back from 24500, would trigger a fall to lower levels of 24000.

Dax (12245.36,+1.09%) made an intra-day high of 12275, attempting to test 12300 on the upside. If 12300 holds as interim resistance, the index may come off towards 1190 again; else a break above 12300 is needed to confirm a near term uptrend targeting 12500-12600 in the coming sessions. Wait to see price action near 12300.

Nikkei (21411.38, +0.75%) is stuck in the 21000-21600 region for the last few sessions and is likely to test 21800 on the upside just now. A break on either side of 21000-21800 zone would indicate further directional movement. Till then some narrow sideways movement may continue.

Shanghai (3283.44, +0.36%) came off a bit from immediate resistance near 3300 as seen on the daily candle chart. If that holds in the near term, the index could come off towards 3250-3200 again in the coming sessions.

Nifty (10154.20, -0.93%) and Sensex (33033.09, -0.85%) are trading lower and look bearish for the week. Nifty could test 10080-10020 on the downside whereas Sensex could come off towards 32500 in the next few sessions.

COMMODITIES

Brent (64.49) has immediate resistance near 66 and while that holds, price may test lower levels of 63-62. WTI (61.30), on the other hand, is likely to trade in the 60-62.50 levels in the coming sessions.

Gold (1328.30) came off sharply contrary to our expectation of moving up towards 1350. The price may be trapped in the 1345-1315 region for the next few sessions.

Copper (3.1370) came off from 3.1750 and could test 3.10-3.07 on the downside in the next few sessions before again moving back towards 3.20.

FOREX

The Dollar Index (89.596), after seeing lows near 89.4 in the last couple of days is currently trading near 89.6. As mentioned yesterday, there is crucial long term support level on the weekly line charts near 89.0-89.5. Whether the index will break this support zone and move down towards lower support on daily candles near 88 would highly depend on the two central bank meetings in the next 2 days – ECB and Bank of Japan. If the ECB makes a slight step forward in the direction of future tightening of its monetary policy, we might see Dollar weaken and the Dollar index come down below 89.0-89.5.

Euro (1.2403) saw a high of 1.2445 yesterday but is currently trading just above 1.24. We might see muted movement in the Euro in the few hours before the ECB meeting. The Euro infact stands at a crucial juncture right now. Looking at the daily candles, we see both a downmove towards support near 1.225-1.23 and an upmove towards resistance near 1.255 possible. The charts suggest slightly greater chances (say 55-60%) of it rising up. However, as mentioned yesterday too, Draghi might have to be as emphatic as his famous "whatever it takes" statement if he wants to talk the Euro down. In that case the Euro dips back to 1.23 and 1.22. Chances are 40-45%.

Dollar-Yen (106.09) has again bounced from the crucial 105.45-105.50 levels . This is the lowest level seen by the Dollar Yen in more than a year. The struggle to break this level might suggest that the markets are waiting for both the ECB and BOJ meetings. We repeat that a downmove towards 105 could imply medium term bearishness and could lead to a quick test of support close to 104.0-104.5, on daily and 3 day candles.

The Euro-Yen (131.570) had tested resistance near 132 on daily and 3 day candles day before yesterday and might see a slow downmove towards 129-130 in the coming sessions.

As mentioned yesterday, Pound (1.3904) is slowly moving up towards 1.395, which is seen as immediate resistance on daily candles. It is likely to dip after testing 1.395.

Dollar-Rupee (64.885): Test of Support at 64.80-75 still possible. Look for a bounce from there to 65.20-25. Else, break below 64.75 raises chances of 64.60-40.

INTEREST RATES

The German 10 Yr – US 10 Yr yield differential (-2.22%) has again dipped slightly towards long term support level near -2.25% via a dip in the German 10 year yield towards 0.655% and rise in US 10 Yr towards 2.877%. We will have to watch out for the ECB meeting later today and 21st March US Fed meeting as they now become extremely vital to the course of yields and forex rates. Any indication of tightening by the ECB might lead to a rise in the German yields and correspondingly the German – US yield spread.

US 10 Year Yield (2.877), US 30 year Yield (3.148), US 5 year yield (2.64), US 2 year yield (2.246) : US yields have been seeing sideways movement in a very narrow range for the past few days and are likely to see a significant move soon. The sentiment surrounding global politics indicate that a rise in US yields beyond long term resistance levels is imminent.

The first half of March should see muted movement in US yields – however, some volatility due to the ECB meeting on 8th March is possible. As the 21st March Fed meeting comes closer, there could be a rise in yields in anticipation of a rate hike.

(Long term resistance levels for the 4 yields have been as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively – a decisive breach of these levels could happen in March 2nd half.)

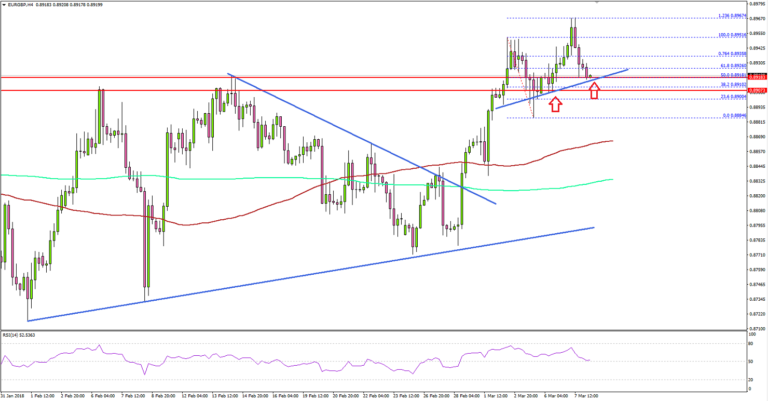

EUR/GBP Remains In Steady Uptrend

Key Highlights

- The Euro made a nice upside move and traded above the 0.8920 resistance against the British Pound.

- There is a connecting bullish trend line forming with support at 0.8920 on the 4-hours chart of EUR/GBP.

- The Euro Zone Gross Domestic Product increased 0.6% in Q4 2017, similar to the market forecast.

- Today, the ECB Interest Rate Decision will be announced, and the central bank is likely to keep rates at 0%.

EURGBP Technical Analysis

The Euro started a fresh upside wave from the 0.8840 level against the British Pound. The EUR/GBP pair traded above 0.8900 and moved into a positive zone.

During the upside move, the pair broke a major bearish trend line with resistance at 0.8830 on the 4-hours chart. Moreover, there was a break above a crucial resistance zone at 0.8910-20.

It opened the doors for more gains and the pair traded toward the 1.236 fib extension of the last decline from the 0.8951 high to 0.8884 low. If the current trend continues, the pair may even test the 1.618 fib extension of the last decline from the 0.8951 high to 0.8884 low.

On the downside, there is a connecting bullish trend line forming with support at 0.8920 on the 4-hours chart. However, the most important support is near 0.8910, which was a resistance earlier.

Recently, the Euro Zone Gross Domestic Product for Q4 2017 was released by the Eurostat. The market was looking for a rise of around 0.6% in the GDP compared with the previous quarter.

The result was similar to the forecast as there was a 0.6% rise. In terms of the yearly change, there was a rise of 2.7%, similar to the forecast and the last reading.

Overall, the Euro may continue to rise versus the British Pound, and the 0.8900-10 support area remains a crucial zone for EUR/GBP.

Economic Releases to Watch Today

- German Factory Order for Jan 2018 (MoM) – Forecast -1.6%, versus +3.8% previous.

- ECB Interest Rate Decision – Forecast 0%, versus 0% previous.

- US Initial Jobless Claims – Forecast 220K, versus 210K previous.

CPTPP: An Antidote to NAFTA Flux?

The signing of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership comes at a pivotal time for Canada, when the U.S. is asserting a more protectionist trade policy. President Donald Trump's recent tariff move on steel and aluminum only drives the point home. Will the CPTPP provide any offsetting benefits? Our view: not an immediate, across-the-board economic boost, but some wins. They include a limited hedge at a time of NAFTA uncertainty, the elimination of behind-the-border hurdles that are especially difficult for smaller firms to overcome, and a voice at the table as new global trade relationships develop.

Casting a wider net for Canadian goods and services

The CPTPP comprises a $13.4 trillion (US$10.5 trillion) economy of 500 million consumers—representing 13% of global GDP in 2017, or more than the Eurozone's five largest economies combined. Yet Canada's new CPTPP trade partners currently absorb a mere 5% of our goods exports. Also, 80% of this market—the pact's seven Asian economies—do not have free trade agreements with Canada. Notwithstanding some competition in sectors such as food, chemicals and transportation manufacturing, Canada's trade with those countries is fairly complementary. Its top-three goods exports and imports to and from the group do not overlap. More such trade should be welcome.

In addition to casting a wider net for Canadian exports, what does the CPTPP offer? We have identified four benefits.

1. A limited hedge at a time of U.S. trade uncertainty

The CPTPP forms the basis for more Canadian export growth in the direction of Japan and other markets. It doesn't lessen our export dependence on our southern neighbour, but it does offer growth at the margins. Ottawa estimates that Canadian exports to CPTPP partners could increase by 4.2% or $2.7 billion, and provide a very minor boost to Canada's GDP of $4.2 billion by 2040.

Together with the Comprehensive Economic and Trade Agreement (CETA) with the European Union, the CPTPP provides a limited hedge for some export sectors at a time of rising protectionism in the U.S.

Such a hedge may appeal to sectors that would face higher Most Favoured Nation duties at the U.S. border relative to the NAFTA schedule, such as vegetables, oils and fats. It may also appeal to sectors that already export across the Pacific and have been stung by U.S. trade action in the past. Those include beef and pork production and more recently, steel and aluminum. However, some of these sectors would also face significant competition from CPTPP members (e.g. Australian beef and mineral fuels). CPTPP markets would also need to demonstrate their viability as export alternatives for Canada when factoring in transportation costs relative to expected market share gains.

Whatever hedge value the CPTPP provides shouldn't be exaggerated.

Major export sectors such as automotive and machinery remain somewhat locked into existing North American trade patterns due to decades of capital-intensive supply chain integration. If anything, they may see more competition, given CPTPP rules of origin could benefit Japanese automotive exporters to Canada by allowing them more liberal access to components sourced from Chinese and other East Asian suppliers.

The short-term benefit to small and medium-sized firms could also be limited. Some 88% and 96% of small and medium exporters, respectively, sell to the U.S., whereas only 15% and 24% do so to Asia ex-China. Given the time and resources involved in exploring new and unfamiliar markets, the CPTPP hedge may only be of longer-term value to such firms.

2. Tackling those thorny "21st century" trade barriers

The CPTPP tackles many so-called 21st century trade issues that limit effective market access to exporters through nontariff barriers and other deterrents. These issues include digital commerce, liberalization of trade in services and investment, customs and trade facilitation, technical barriers to trade, and more. Addressing these issues should be of particular benefit to smaller and medium-sized exporters, for which maneuvering such trade issues can pose a formidable hurdle to expanding their markets.

North American exporters often cite Japan in particular as a challenging market, not on account of its duties on nonagricultural goods (its simple average applied Most Favoured Nation rate is 4%), but because of its widespread use of country-specific criteria that diverge from international practice. Its non-tariff barriers include labelling requirements, direct and indirect subsidies for domestic grain production, safety requirements for construction materials, differing regulatory standards for domestic and foreign financial institutions, and much more.

3. Keeping up with the Joneses—or getting ahead of them

The CPTPP is partly a defensive play for Canada. The "Joneses" to keep up with are economies which compete with key Canadian exports in CPTPP markets and that recently concluded their own free trade deals with CPTPP countries. Take the EU, which concluded a trade deal with Japan in 2017, and looms large as a competitor to Canada across a range of exports, including beef, pork and other processed food, wood products, and financial services. Without the CPTPP, Canadian exporters of such goods and services risked seeing their competitiveness further erode in favour of EU exporters. For example, Canada's relative share of Japanese meat imports has decreased since 2010, whereas the EU's has grown.

On offense, Canada may gain some advantage over the U.S. by being in the CPTPP. Canadian beef, pork and wood products producers, but also financial services, could gain market share in economies such as Japan's at the expense of U.S. competitors. Again, while the U.S. share of Japanese meat imports has grown relative to Canada's since 2010, the CPTPP may confer Canadian meat producers and processors an advantage.

4. The long game: a voice at the table

The U.S. and China remain the elephants in the room. The CPTPP was concluded so as to allow Washington to eventually join the rebranded trade pact under a future administration. President Trump even apocryphally suggested in Davos that his country may do so under his own administration, provided it was "in the interests of all." Hence the retention of virtually the entire TPP text originally negotiated with the U.S., and the "suspension" of some of the more controversial clauses on IP and dispute settlement that the Obama administration had secured, but which could resume if the U.S. reentered the agreement.

Ultimately, the CPTPP remains as much about long-term geopolitics as about trade benefits. The Obama administration envisioned the TPP as the economic prong of its Asia pivot strategy, to ensure the U.S. and its closest partners in the Asia-Pacific region would take the lead in defining regional trade rules for the current century. Some observers even suggested the TPP would eventually mutate into global trade norms for the new century. Beijing's own regional trade push, including the One Belt One Road initiative championed by President Xi Jinping, is ostensibly an alternative model.

Being a member of the CPTPP will secure a Canadian voice in influencing regional trade rules. It also could give Canada some leverage in exacting concessions from potential new entrants, and allow it to pool its negotiating weight with like-minded partners on some issues. Indonesia, the Philippines, South Korea, and even China have at one point expressed interest in eventually joining the TPP. As a trading nation, it's in Canada's interest to help set the rules for trade and investment within the Asia-Pacific region.

Competing frameworks for regional trade and investment

BOC Left Rates On Hold, More Concerned About US Trade Policy

As widely anticipated, BOC left the policy rate unchanged at 1.25% in March. The accompanying statement was more cautious than the previous one, over the trade outlook. Policymakers suggested that 'trade policy developments are an important and growing source of uncertainty for the global and Canadian outlooks', in addition to reiteration of the need for remaining 'cautious in considering future policy adjustments'. Expectations of another rate hike in April diminished after the announcement.

On economic developments, the central bank acknowledged slower than expected GDP growth in 4Q17, attributing it to 'higher imports, while exports made only a partial recovery from their third-quarter decline'. It noted that 'the gain in imports mainly reflected stronger business investment, which adds to the economy's capacity. It, however, downplayed the fact that consumption growth weakened during the period. BOC also suggested that housing data in late-2017 signaled 'some pulling forward of demand' and pledged to continue monitoring the 'economy's sensitivity to higher interest rates'.

On the job market, BOC noted that 'wage growth has firmed, but remains lower than would be typical in an economy with no labour market slack'. In Janaury, the central bank acknowledged that wages have 'picked up but are rising by less than would be typical in the absence of labour market slack'. The apparent more upbeat wage growth outlook was accompanied with a modest upgrade on the inflation assessment on which the central bank indicated that the increase in both the headline and core readings have been 'consistent with an economy operating near capacity'. In January, it noted that inflation was moving 'consistent with diminishing slack in the economy'. This implied that most of the slack in the economy has been absorbed and the effect would gradually reflect on growth of wage and price levels.

However, BOC was obviously more cautious over the foreign trade outlook. As noted in the statement, 'trade policy developments are an important and growing source of uncertainty for the global and Canadian outlooks'. The concern has been increased, compared with the prior reference that that 'uncertainty surrounding the future of the North American Free Trade Agreement is clouding the economic outlook'.

In the concluding paragraph, the central bank repeated its monetary stance, suggesting that it 'will remain cautious in considering future policy adjustments, guided by incoming data in assessing the economy's sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation'. Indeed, whether a rate hike would be adopted in April depends on incoming data, NAFTA negotiations as well as the likelihood of and US-induced trade war.