Sample Category Title

Chinese Trade & Inflation Data Coming Up With Aussie also in Focus

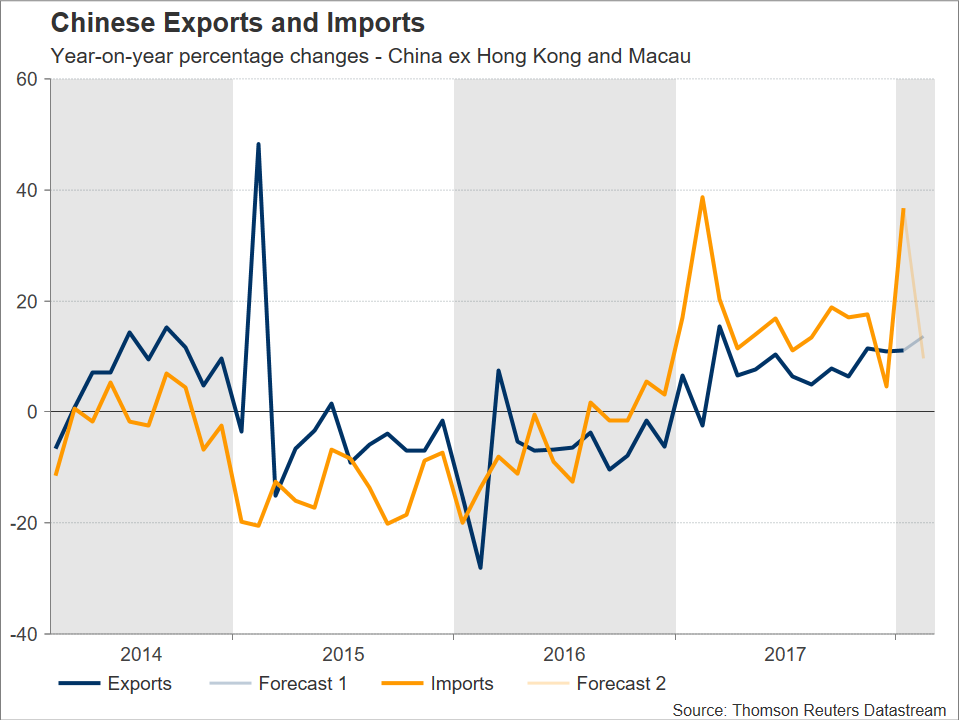

Chinese trade data for the month of February are due on Thursday – the figures lack a fixed time of release – with both exports and imports projected to grow solidly. The readings on producer and consumer prices for the month of February scheduled for release on Friday at 0130 GMT will also be in focus out of the nation. On an annual basis, PPI growth is expected to ease, while CPI expansion is anticipated to accelerate.

Year-on-year, exports and imports are expected to have grown by 13.6% and 9.7% respectively during the second month of the year. These compare to January’s respective increases of 11.1% and 36.9%. Should exports come in line with projections, they would expand at their highest pace since March 2017. February’s trade surplus is anticipated to stand at $0.6 billion from around $20.4bn in January. It deserves mention though, that comparisons are not as useful is this instance as the data were distorted by seasonal factors relating to the timing of Lunar New Year celebrations which took place in mid-February this year. For example, January’s surge in imports was attributed to an inventory buildup ahead of New Year festivities, with higher commodity prices also playing a role. A better approach to gauge the robustness of the figures might be to look at overall first quarter data.

Thursday’s figures are perhaps coming into more prominence on the face of the latest trade developments that have rattled markets and relate to US President Trump’s decision to impose tariffs on imported steel and aluminum. Earlier in the year, the Trump administration also levied tariffs on solar panels and washing machines, with China retaliating by probing sorghum imports from the US.

Thursday’s figures are perhaps coming into more prominence on the face of the latest trade developments that have rattled markets and relate to US President Trump’s decision to impose tariffs on imported steel and aluminum. Earlier in the year, the Trump administration also levied tariffs on solar panels and washing machines, with China retaliating by probing sorghum imports from the US.

Following Trump’s recent actions, China said it will host US officials for a new round of talks on trade issues. However, reports suggest that the White House is also considering clamping down on Chinese investments in the US and instituting tariffs on a wide range of its imports from the country. Should tensions escalate out of control, with the two countries merely engaging in tit-for-tat retaliatory actions, then the outlook for Chinese exports would look much grimmer than at present.

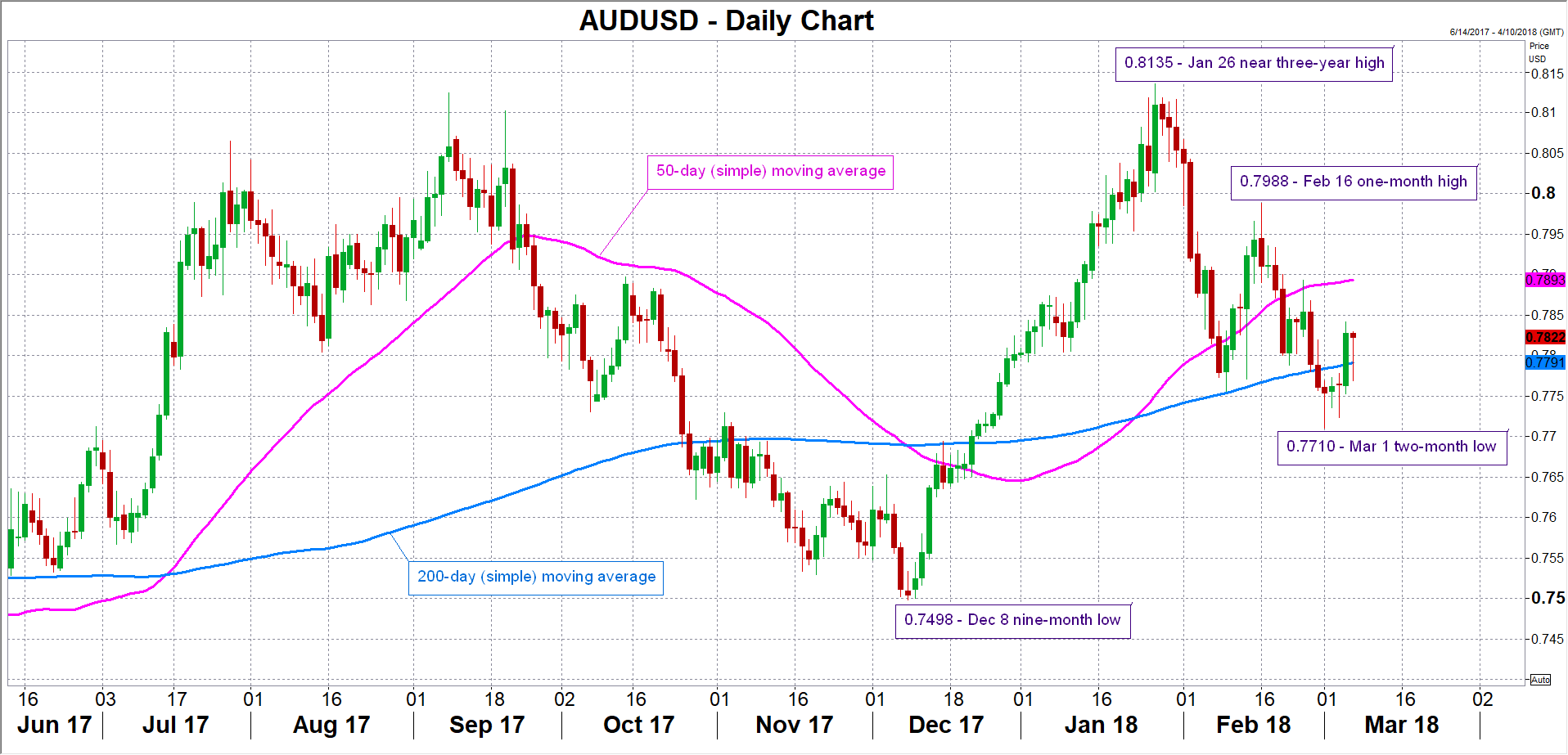

Dollar/yuan is down by around 3% year-to-date, but beyond the Chinese currency, the Australian currency will also be in focus as trade numbers go public. The aussie is viewed as a liquid proxy for China’s economy due to the two nations’ close economic ties, as China is Australia’s largest export and import partner.

Upbeat data could lead to long aussie/dollar positions, with price advances potentially meeting resistance around the current level of the 50-day moving average at 0.7893. The area around this level was subject to congestion in the past and also encapsulates the 0.79 handle that may hold psychological significance. Stronger bullish movement would turn the attention to the one-month high of 0.7988 that was recorded on February 16.

If the figures disappoint though, aussie/dollar might post losses. Should this scenario materialize, support could come around the 200-day MA at 0.7791. Notice that this includes the 0.78 level that could also be of psychological importance. Further below, the two-month low of 0.7710 from March 1 would be eyed next.

Also of significance in the world’s second largest economy, the annual National People’s Congress meetings – these being parliamentary meetings – are currently taking place in Beijing and are set to continue through March 20. Planning for the year ahead is taking place at this event. On Monday, Premier Li Keqiang kicked off the gathering by announcing that the nation’s growth target for 2018 will be around 6.5%. This is the same as last year, when the economy actually grew by 6.9%. The Chinese premier also stressed the need to step up efforts relating to curbing financial risks. In this regard, data on bank lending for February will be made public sometime next week; the release is tentative, lacking a specific day of release.

Also of significance in the world’s second largest economy, the annual National People’s Congress meetings – these being parliamentary meetings – are currently taking place in Beijing and are set to continue through March 20. Planning for the year ahead is taking place at this event. On Monday, Premier Li Keqiang kicked off the gathering by announcing that the nation’s growth target for 2018 will be around 6.5%. This is the same as last year, when the economy actually grew by 6.9%. The Chinese premier also stressed the need to step up efforts relating to curbing financial risks. In this regard, data on bank lending for February will be made public sometime next week; the release is tentative, lacking a specific day of release.

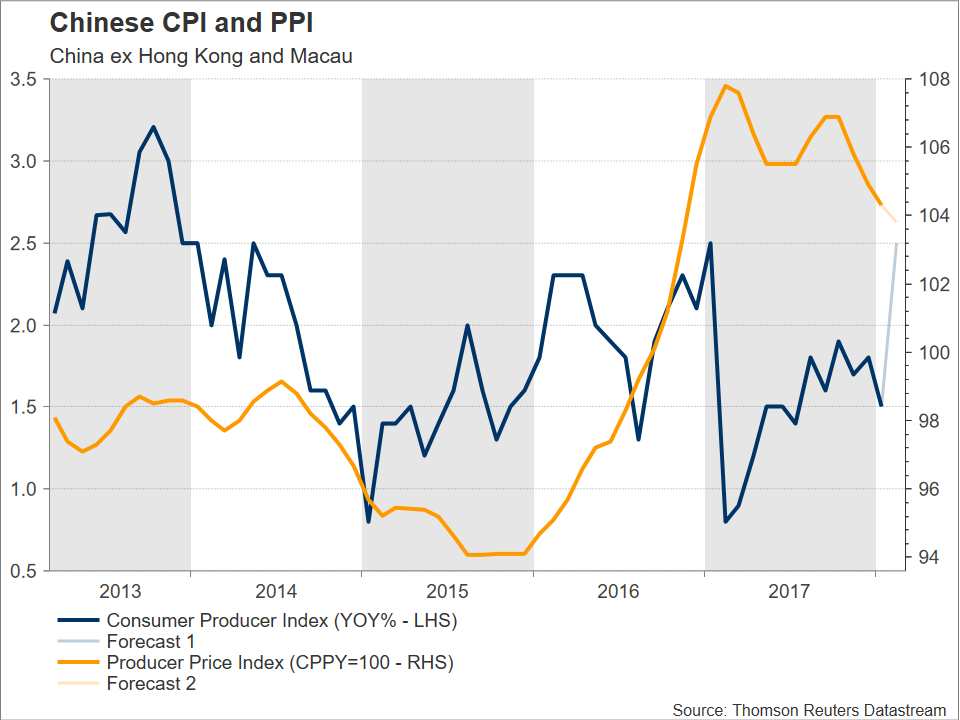

Other important data out of China will pertain to February’s producer and consumer price inflation, both due out on Friday at 1330 GMT. PPI growth is projected to decline to 3.8% y/y (versus 4.3% in January), easing for the fourth straight month. If it comes as expected, its rate of growth would be at its lowest since November 2016, with government efforts to reduce environmental pollution and curb risks in the financial system likely weighing on factory prices. CPI growth, on the other hand, is forecast to increase to 2.5% y/y (versus 1.5% in January), at a pace last seen in January 2017.

Lastly, and given that mention was made on aussie/dollar, Australia will see the release of January trade balance figures on Thursday at 0030 GMT. These could also spur movements in the pair.

Lastly, and given that mention was made on aussie/dollar, Australia will see the release of January trade balance figures on Thursday at 0030 GMT. These could also spur movements in the pair.

ECB Will Probably Need More Time to Change Forward Guidance

The European Central Bank concludes its two-day policy meeting on Thursday, but no major policy shift is expected once again. February did not add much to the Eurozone’s economic recovery but instead indicated that the bloc’s positive momentum has slowed down. March did not have a great start either, with political uncertainties lingering on, while threats of a trade war arose out of the blue.

The ECB Governor, Mario Draghi, is anticipated to say on Thursday that the current loose monetary policy is still needed to accommodate healthy growth in the Eurozone, keeping interest rates at record lows for the second year running (1045 GMT) and signalling that it is not yet time to consider an early exit from the central bank’s quantitative easing program as some in his board desire. Commenting on data, he will probably remind markets about the weak inflation environment. Indeed, the consumer price index – the ECB’s preferred inflation measure – has stuck below the ECB’s target of 2.0%, retreating to 1.3% y/y in January, while initial estimates for February signaled that inflation might have eased further to 1.2%. At this point, he might cite the recent strength in the exchange rate as a headwind to price growth. But as he previously said, he might also argue that the factors that restrict inflation from rising towards the goal will probably fade out as the unemployment rate continues to fall and economic expansion rises.

Besides that, markets believe that the recent political developments in the Eurozone and the Trump’s proposed protectionism measures could persuade Draghi to play safe.

Besides that, markets believe that the recent political developments in the Eurozone and the Trump’s proposed protectionism measures could persuade Draghi to play safe.

Germany’s political gridlock has finally come to an end during the weekend, with Merkel securing another term as chancellor under a grand coalition agreement with her former coalition partners, the SPD. At the same day though, the Italian elections favored Eurosceptic parties more than anticipated, bringing a new headache to the EU. The anti-immigration far-right Five Start Movement party turned to be the largest single party with 32.1% of the votes and has now the right to negotiate a leading position in the new government. Still, Draghi might give little weight on this front as this is a story heard before.

The announcement of new punitive import tariffs on steel and aluminum on Friday caught markets by surprise and will undoubtedly be raised for discussion at Draghi’s press conference at 1330 GMT. While there are still some rumors supporting that the measures are a way to advance Trump’s negotiating position (probably bringing a better NAFTA deal for the US on the table) rather than something that could turn real, Gary Cohn’s resignation – Trump’s chief economic advisor and free-trade advocate – late on Tuesday sparked fears that tariffs are not unlikely to happen. This could spread economic pain to European auto industries, deteriorating the bloc’s terms of trade. Therefore, as long as the issue continues to weigh on business sentiment, the ECB will probably keep its hands in its pockets. Recall that the Sentix index, which gauges investors’ confidence on the bloc’s economic performance for the next six months, retreated near one-year lows in February.

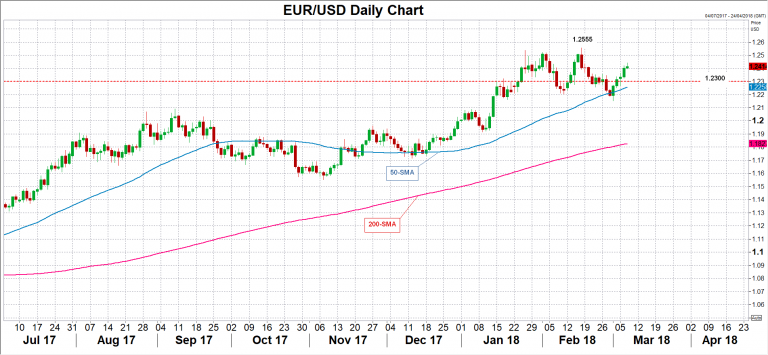

ECB minutes regarding January’s meeting stated that a shift in forward guidance was at that moment premature and that “the language pertaining to the monetary policy stance could be revisited early this year. Policymakers are likely to repeat this wording tomorrow as well, with investors now expecting a change in forward guidance occurring probably in April or June, while they also believe that policymakers could set an end-date for the QE program and reveal plans on interest rates by September. However, if they hold a more cautious stance tomorrow than is already priced in, euro/dollar could easily lose ground to meet again the 1.23 key mark or even worse deep below the 50-day moving average which currently stands at 1.2258. Alternatively, if they feel more confident about the bloc’s economic outlook despite the aforementioned uncertainties, the pair could crawl up towards the three-year high of 1.2555.

U.S. Trade Deficit Hits 9-Year High in January

Oil played a major role in the widening in the trade deficit in January. Although this volatility should subside, net exports likely will exert another significant drag on overall GDP growth in the first quarter.

Oil Played Outsized Role in Trade Dynamics in January

The U.S. deficit in international trade in goods and services widened to $56.6 billion in January from an upwardly revised figure of $53.9 billion in December (top chart). Not only was the outturn larger than most analysts had expected, but it was also the largest trade deficit that the country has incurred since October 2008. Although the value of overall imports was more or less flat in January relative to the previous month, exports of goods and services fell by $2.7 billion in January. As we will discuss, petroleum products played an outsized role on both sides of the ledger.

The weakness in exports was due, at least in part, to a $1.8 billion drop in aircraft exports, which can be notoriously volatile on a monthly basis. But the value of petroleum exports fell by nearly $600 million in January despite an upward trend in oil prices in recent months. In short, real petroleum exports tanked by 9 percent in January. On the other side of the ledger, the value of petroleum imports shot up by $3.2 billion, which largely cancelled out the $3.6 billion drop in non-oil imports. In that regard, there was widespread weakness in other major categories of imports.

In our view, the volatility in petroleum exports and imports in January is simply a seasonal quirk. As the middle chart makes clear, the value of oil imports has followed a downward trend over the past five years, while petroleum exports have been trending higher. These trends reflect the sharp increase in American oil production that has occurred in recent years. Moreover, the weakness in non-petroleum exports, which fell 2.7 percent on a real basis in January, and in non-petroleum imports—real non-oil imports were off 2.2 percent—were also one-off events. Solid economic growth in the rest of the world in conjunction with the lagged effects of past dollar depreciation should support American export growth in coming months. Likewise, strong growth in U.S. domestic demand should continue to pull in non-petroleum imports going forward.

Trade Likely Will Exert Drag on Real GDP Growth in Q1

These caveats notwithstanding, real exports came into 2018 with weak momentum while real imports started at a high level (bottom chart). If real goods exports in February and March remain unchanged at January's level, then they will fall 3.7 percent on an annualized basis in Q1 relative to the fourth quarter. On the other hand, real imports will have grown modestly. Although we expect some rebound in real exports in February and March, it is evident that export growth in the first quarter will be weak. Real net exports of goods and services sliced 1.1 percentage point from topline real GDP growth in Q4-2017. Although the drag from trade in the first quarter likely will not be as extreme as it was in Q4, the headwinds on real GDP growth from the external sector are set to continue.

Caution Again Rules the Day at the Bank of Canada

As widely anticipated, the Bank of Canada held its key monetary policy interest rate at 1.25% this morning. The accompanying statement struck a dovish tone.

Global growth is seen as solid, and U.S. policy changes are expected to boost U.S. growth this year and next. It was also noted however that trade policy developments are an 'important and growing source of uncertainty'

Turning to Canada, the overall level of output is seen as in line with their expectations despite a softer than anticipated end to last year. The gain in imports was attributed to stronger business investment, adding to economic capacity. Housing is the wildcard, and the Bank sees the strong performance in the fourth quarter as representative of a pull-forward of demand. The impact of policy changes will take time to assess. The statement also noted that household credit growth has decelerated for three consecutive months.

On inflation, the statement noted an overall pace close to 2% and the further gains in the Bank's core measures, pointing to an economy operating near capacity, although temporary factors are having an impact particularly on the headline measure. On wages, the Bank continues to view the current pace as lower than typical for an economy with no labour market slack.

Ultimately, the Governing Council remains of the view that higher rates will be warranted over time, but will continue to assess the economy's sensitivity to interest rates, economic capacity, and wages/inflation.

Key Implications

Given the developments since January, anything that wasn't dovish would have been a surprise. The economic outlook may be positive, but with trade risks mounting and the economy in the middle of an adjustment to yet another round of measures to cool housing markets, a 'wait and see' approach is clearly appropriate. Now is not the time to rock the boat.

As the statement pointed out, ultimately rates are likely to rise further, but with time needed to assess the impacts of both domestic policy changes and external developments, we remain of the view that the July meeting is the most likely to see the next move.

Of note, this decision marks the start of a new communications approach from the Bank of Canada. Deputy Governor Tim Lane will provide an 'economic progress report' tomorrow that should hopefully provide more insight on how the Bank is assessing recent developments.

Sunset Market Commentary

Markets

Global core bonds enjoyed a cautious safe haven bid as markets tried to get some insight in the next turn of the US foreign trade policy. The protectionist declarations of US President Trump remain a sources of global uncertainty and are weighing on risky assets. However, Trump’s plans are facing strong headwinds inside and outside the US. So , markets still see a chance of the US President easing its stance. At least for now, the trade debate doesn’t look like changing the Fed’s intentions to continue policy normalization. Even so, during the day, US Treasuries again slightly outperformed German bunds even as the ECB isn’t expected to announce a substantial change in policy /communication at tomorrow’s policy meeting. At the time of writing, US yields decline between 0.5 and 1.5 bp, the 5y/10 y sector outperforming. German yields are marginally lower on a daily perspective with the 30-y outperforming (-2.6bp). Despite a cautious risk-off sentiment, 10-y intra-EMU spreads versus Germany mostly narrow, Greece and Portugal outperforming (-5 bp).

The headlines on a potential trade war between the US and its major trading partners continued to dominate the headlines on the financial newswires after Gary Cohn resigned as economic advisor of US president Trump. For now the losses of the dollar are contained. EUR/USD hovers in a sideways range in the lower half of the 1.24 big figure. USD/JPY found a bottom in the mid 105 area after a one-off decline on the Cohn news overnight. There were no important eco data in EMU. The ADP labor market report showed job growth of 235 000 in the US private sector in February, confirming that the US labour market remains very healthy. The focus of FX traders is currently on the trade story rather than on US data. However, as strong US data make Fed governors ever more considering the option of four rather than three rate hikes this year, they at least help to limit the damage for the dollar. EUR/USD is trading near 1.2420. USD/JPY is again nearing the 106 barrier. This evening, the Fed will publish its Beige Book preparing the March 21 Fed policy meeting. Tomorrow, the focus turns to the ECB policy meeting.

Sterling continued trading with a tentative negative bias today. The EU published a draft proposal for the EU/UK relationship in the post-Brexit era. Meetings between EU and UK politicians over the previous days already indicated that the water between the two parties remains deep. The EU proposes a cooperation that is far less tight than the UK had hoped for, but this wasn’t a surprise. That said, the political stalemate persists and the countdown to the formal separation next year continues. This remains a negative for sterling. In line with recent price action the moves/losses of sterling remained modest. EUR/GBP intraday touched the highest level since end November last year. The pair trades currently in the 0.8940/50 area. EUR/GBP 0.9033 is the next high profile resistance on the charts. Cable trades in the 1.3875 area as sterling softness is counterbalanced by USD weakness.

News Headlines

The EU offered Britain a free trade deal for the post-Brexit era. However, the cooperation will be much more limited than London had called for. The EU says its position “reflects the level of rights and obligations compatible with the positions stated by the U.K.,” but if Britain’s positions shift, the EU “will be prepared to reconsider its offer.” The EU also indicated that Britain would be treated like any other third country in respect of financial services.

ADP research Institute said the US private sector added 235 0000 jobs in February. The January figure was upwardly revised from 234 000 to 244 000. The data suggest ongoing strong US labour market conditions at the start of the year. Investors are now looking forward to the US payrolls to be published on Friday.

The economy in the EMU expanded by 0.6 percent in the final quarter of 2017, Eurostat confirmed today. Euro zone GDP rose 2.3 percent in 2017 as a whole, the fastest growth rate since 2007 (3.0%).

EU’s official response on possible US tariffs for steel and aluminum

Here is the official statement published today.

European Commission outlines EU plan to counter US trade restrictions on steel and aluminium

The College of Commissioners discussed today the EU's response to the possible US import restrictions for steel and aluminium announced on 1 March. The EU stands ready to react proportionately and fully in line with the World Trade Organisation (WTO) rules in case the US measures are formalised and affect EU's economic interests. The College gave its political endorsement to the proposal presented by President Jean-Claude Juncker, Vice-President Jyrki Katainen and Commissioner for Trade Cecilia Malmström. Speaking after the College meeting, Commissioner Malmström said: "We still hope, as a USA security partner, that the EU would be excluded. We also hope to convince the US administration that this is not the right move. As no decision has been taken yet, no formal action has been taken by the European Union. But we have made clear that if a move like this is taken, it will hurt the European Union. It will put thousands of European jobs in jeopardy and it has to be met by firm and proportionate response. Unlike these proposed US duties, our three tracks of work are in line with our obligations in the WTO. They will be carried out by the book. The root cause of the problem in the steel and aluminium sector is global overcapacity. It is rooted in the fact that a lot of steel and aluminium production takes place under massive state subsidies, and under non-market conditions. This can only be addressed by cooperation, getting to the source of the problem and working together. What is clear is that turning inward is not the answer. Protectionism cannot be the answer, it never is."The EU remains available to continue working on this together with the United States.The EU has been and remains a strong supporter of an open and rules-based global trade system. (For more information: Daniel Rosario - Tel.: +32 229 56185; Kinga Malinowska - Tel: +32 229 51383)

BoC stands pat, maintain tightening bias but sounds cautious

Bank of Canada kept overnight rate target unchanged at 1.25% as widely expected.

Some highlights of the statement:

- Trade policy developments are an important and growing source of uncertainty for the global and Canadian outlooks.

- The Bank continues to monitor the economy's sensitivity to higher interest rates.

- Inflation is running close to the 2 per cent target and the Bank's core measures of inflation have edged up, consistent with an economy operating near capacity.

- Wage growth has firmed, but remains lower than would be typical in an economy with no labour market slack.

- While the economic outlook is expected to warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed to keep the economy operating close to potential and inflation on target.

- Governing Council will remain cautious in considering future policy adjustments, guided by incoming data in assessing the economy's sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation.

- Full statement here

There was no elaboration on NAFTA negotiations nor risk of trade war. BoC maintained tightening bias but sounds very cautious.

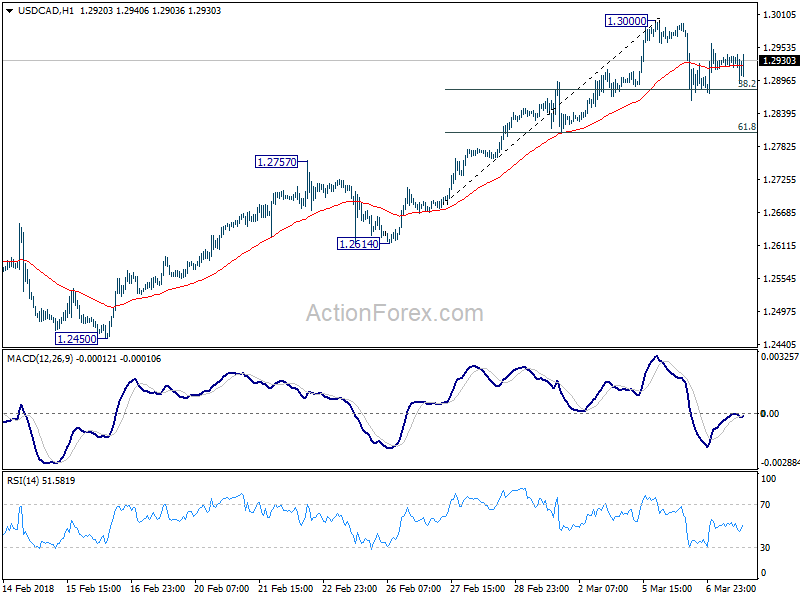

USD/CAD is steadily in consolidation from 1.3000 temporary top.

Canada’s Rrade Deficit Narrowed in January – But With Disappointing Details

Highlights:

- Canada’s nominal merchandise trade deficit narrowed to $1.9 billion in January from $3.1 billion in December -but controlling for the impact of prices, the volume balance was unchanged.

- Export and import volumes both declined 4%.

- About half the drop in export volumes came from lower energy shipments but non-energy exports also remained soft.

Our Take:

The headline trade deficit narrowed to $1.9 billion in January from the $3.1 billion shortfall in December but only because of a big 4.3% drop in imports and a big increase in the price of Canadian energy exports. Nominal exports declined 2.1% but controlling for the impact of prices, volume shipments fell 4.0% — exactly matching the drop in import volumes and implying no change in the ‘real’ trade balance. About half of the drop in export volumes overall came from a 12% plunge in energy shipments. Non-energy exports also declined about 2%, though, and were down 4% from a year ago. Some weakness in imports was expected — particularly in machinery imports which were reportedly boosted in earlier months as companies rushed to import some machinery ahead of new environmental regulations that kicked in in January. The drop in in January was nonetheless larger than we previously assumed.

The monthly trade data is notoriously volatile and revision prone but weakness in non-energy export volumes is also not really new. There is little evidence that Canadian exporters are really tapping significantly into improving global trade flows to-date. That won’t provide much in the way of encouragement to the Bank of Canada which has been counting on growth in external demand as the global economy improves to offset an expected pullback in household spending growth as interest rates rise. To be sure, the data hasn’t all been bad. The overall economy still looks to be operating pretty close to capacity — with separately released productivity accounts data this morning showing maybe a bit more upward wage pressure in Q4 of last year than the Bank of Canada has been expecting. Nonetheless, mixed economic reports recently leave little urgency for the central bank to hike interest rates later this morning after the 25 basis point hike at the last meeting in January.

(BOC) Bank of Canada Maintains Overnight Rate Target at 1 1/4 Per cent

The Bank of Canada today maintained its target for the overnight rate at 1 1/4 per cent. The Bank Rate is correspondingly 1 1/2 per cent and the deposit rate is 1 per cent.

Global growth remains solid and broad-based. In the United States, new government spending and previously-announced tax cuts are anticipated to boost growth in 2018 and 2019. However, trade policy developments are an important and growing source of uncertainty for the global and Canadian outlooks.

In Canada, the national accounts data show that the economy grew by 3 per cent in 2017, bringing the level of real GDP in line with the projection in the Bank’s January Monetary Policy Report (MPR). In the fourth quarter, GDP growth was slower than expected, largely due to higher imports, while exports made only a partial recovery from their third-quarter decline. The gain in imports mainly reflected stronger business investment, which adds to the economy’s capacity.

Strong housing data in late 2017, and softer data at the beginning of this year, indicate some pulling forward of demand ahead of new mortgage guidelines and other policy measures. It will take some time to fully assess the impact of these, as well as recently announced provincial measures, on housing demand and prices. More broadly, the Bank continues to monitor the economy’s sensitivity to higher interest rates. Notably, household credit growth has decelerated for three consecutive months. The implications of the recent federal budget for the outlook for growth and inflation will be incorporated in the Bank’s April projection.

Inflation is running close to the 2 per cent target and the Bank’s core measures of inflation have edged up, consistent with an economy operating near capacity. Wage growth has firmed, but remains lower than would be typical in an economy with no labour market slack. Inflation is fluctuating because of temporary factors related to gasoline, electricity, and minimum wages.

In this context, Governing Council maintained the target for the overnight rate at 1 1/4 per cent. While the economic outlook is expected to warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed to keep the economy operating close to potential and inflation on target. Governing Council will remain cautious in considering future policy adjustments, guided by incoming data in assessing the economy’s sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation.

Information note

The next scheduled date for announcing the overnight rate target is April 18, 2018. The next full update of the Bank’s outlook for the economy and inflation, including risks to the projection, will be published in the MPR at the same time.

Canada’s Trade Deficit Narrowed in January

Canada's trade deficit narrowed to $1.9B in January (previously $3.1B). Imports broadly fell 4.3%, largely driven lower by declines in industrial machinery, equipment, and parts, while exports declined 2.1%, due to declines in the export of passenger cars and light trucks. In real or volume terms, exports declined 3.6% while imports fell 3.9%.

Following two consecutive months of strong increases, imports of industrial machinery, equipment and parts fell 11.3% in January. In addition, the import of logging, mining, and construction machinery and equipment fell 40%. According to Statistics Canada, part of the January decline in imports was likely related to new regulations on off-road diesel engine and machine emissions that took effect at the start of January, which likely limited imports to machinery that met the new standards.

After three consecutive monthly gains, exports fell back in January. Despite a sixth consecutive, price-driven advance in exports of energy products (+2.9% m/m), declines in passenger cars and light trucks (-13.1%) and forestry products and building and packaging materials (-6.6%) helped drag down the headline figure. Statistics Canada notes that atypical plant closures in January were responsible for the decline in imports of motor vehicle engines and parts, while the resumption of the collection of import duties by the U.S. Department of Commerce likely contributed to the decline in export of forestry related products.

Canada's merchandise trade surplus with the U.S. narrowed to $3.1B in January (previously $3.6B), owing to exports falling more than imports. Canada's trade deficit with the rest of the world narrowed to $5.0B (previously $6.6B), as imports fell 8.5% while exports rose a touch (+0.4%).

Key Implications

The January trade data was disappointing, with both export and import volumes declining. While the decline in import volumes was expected after a strong performance in prior months, the trend of weak export numbers pours cold water on the notion that the Canadian economy is rotating away from consumption and housing toward investment and trade. Having said that, some of the weakness in exports is due to temporary factors that should reverse in coming months, and given the volatility in the month-to-month trade data, exports could very well strengthen through the first quarter.

Looking ahead, stronger demand from the U.S. and a sub-80 US cent loonie should provide some support for Canadian exports. But, NAFTA renegotiations pose some risk, and new protectionist rhetoric from the U.S. administration concerning steel and aluminum tariffs only serves to further elevate trade uncertainty.

Later this morning the Bank of Canada is scheduled to announce its decision on interest rates. Given the elevated level of policy uncertainty emanating from the U.S. administration and slowing economic momentum in Canada, the Bank is likely to leave its policy rate unchanged.