Sample Category Title

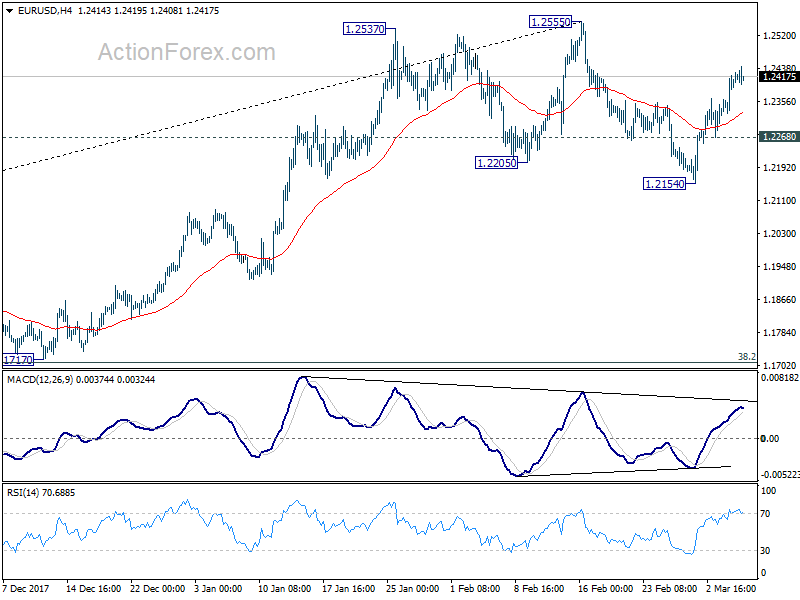

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2347; (P) 1.2384 (R1) 1.2440; More....

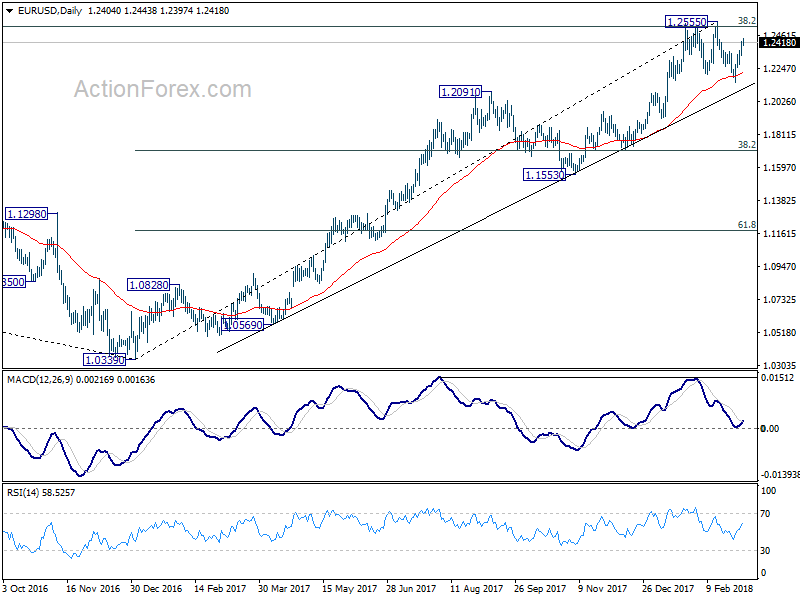

Intraday bias in EUR/USD remains on the upside at this point. Rebound from 1.2154 is in progress to retest 1.2555 high. The corrective structure of the fall from 1.2555 to 1.2154 argues that larger rally is not finished. More importantly, firm break of 1.2555 and 1.2516 long term fibonacci level will carry larger bullish implications. On the downside, below 1.2268 minor support will turn bias back to the downside for 1.2154 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

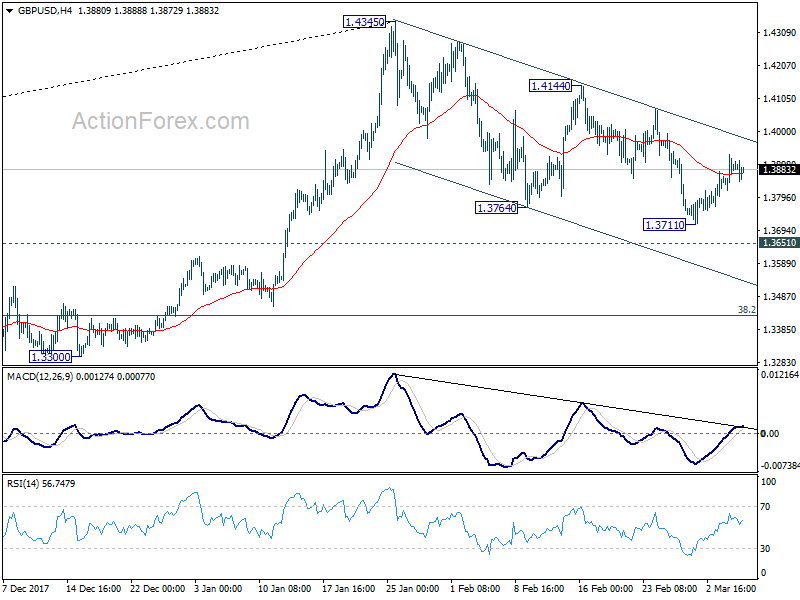

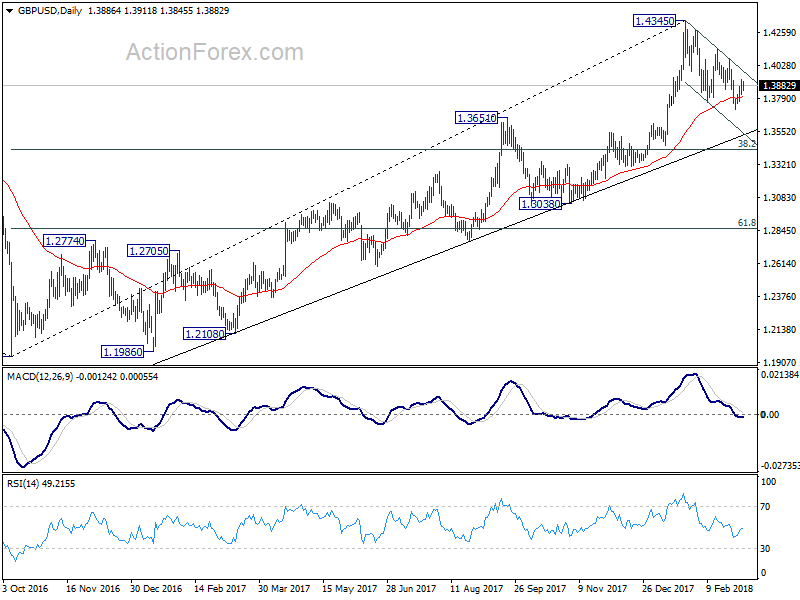

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3826; (P) 1.3877; (R1) 1.3939; More....

Intraday bias in GBP/USD remains neutral at this point. Decline from 1.4345 is in favor to extend. Below 1.3711 will resume the fall from 1.4345 through 1.3651 resistance turned support. We'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound. This will be the preferred case as long as 1.4144 resistance holds.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

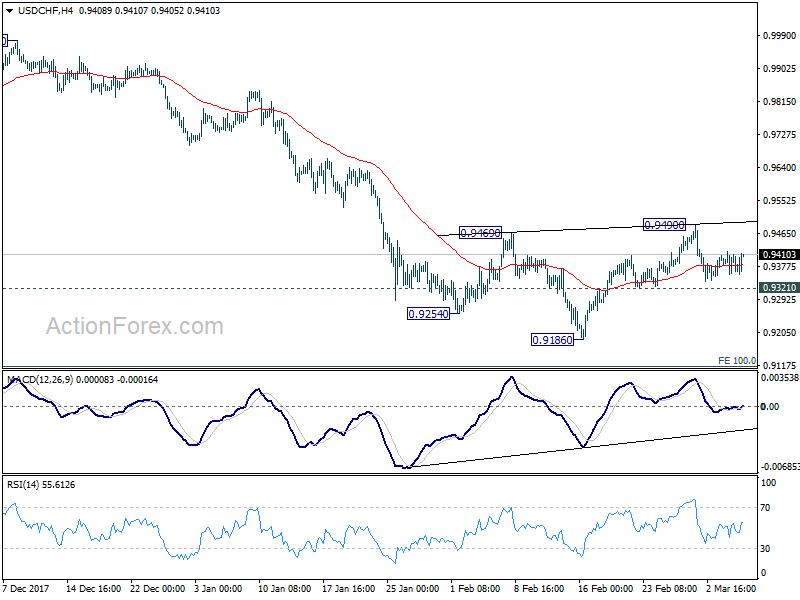

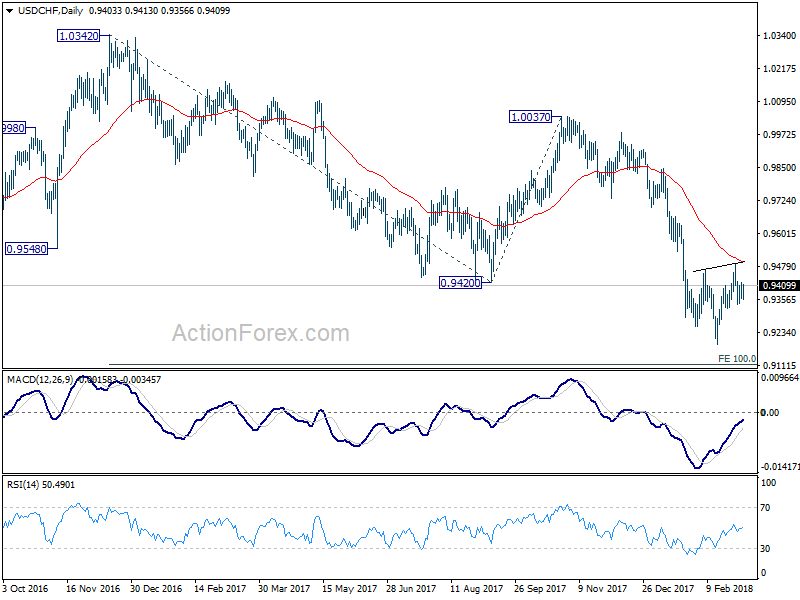

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9369; (P) 0.9394; (R1) 0.9429; More...

Intraday bias in USD/CHF remains neutral at this point. On the downside, break of 0.9321 will indicate completion of the rebound from 0.9186. Intraday bias will be turned back to the downside for 0.9186 first. Break will resume larger down trend to 0.9115 projection level. On the upside, break of 0.9490 will revive the case of near term reversal, on bullish convergence condition in 4 hour MACD. In that case, outlook will be turned bullish.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

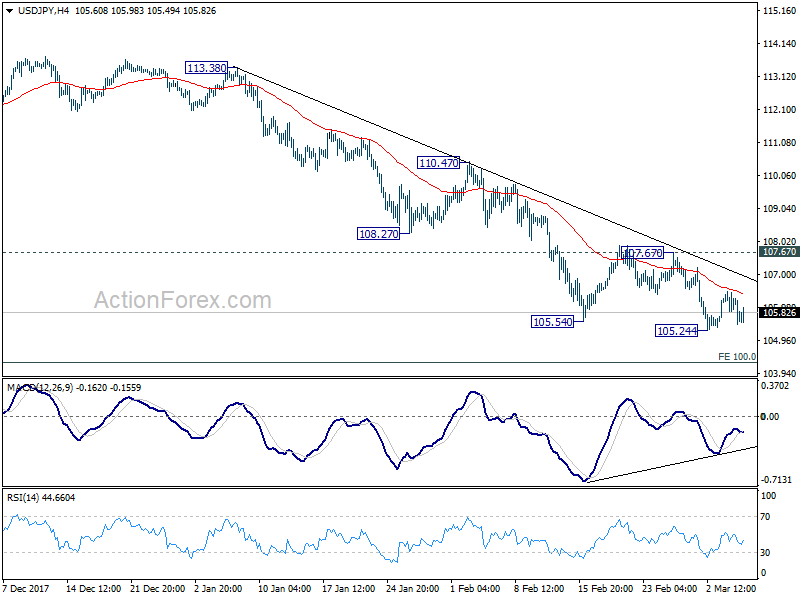

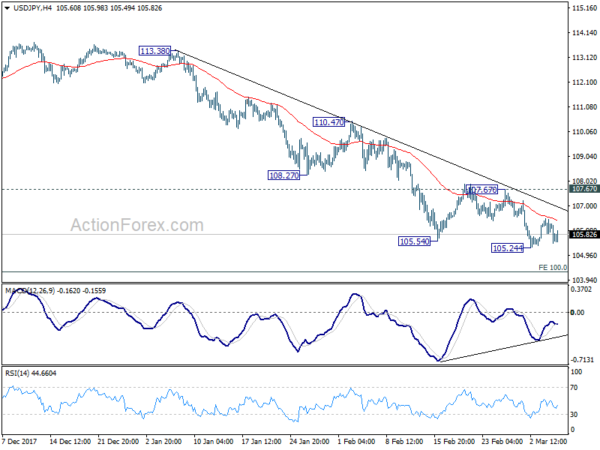

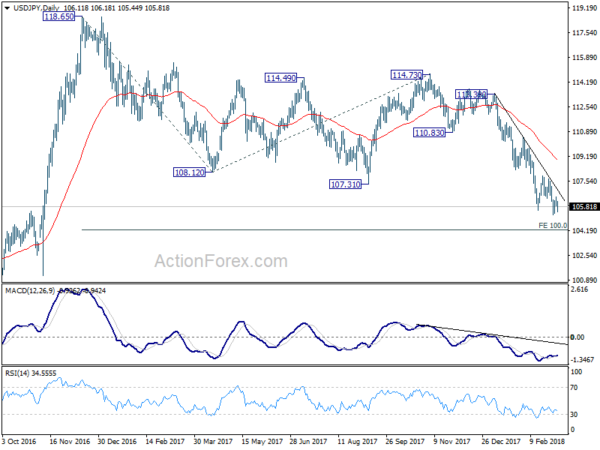

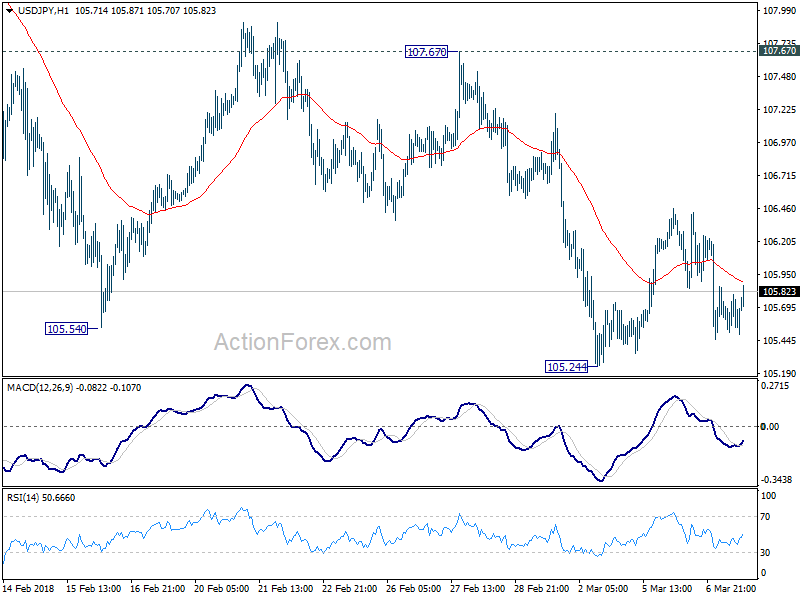

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.82; (P) 106.14; (R1) 106.43; More...

USD/JPY recovers mildly in early US session but momentum has been week. It's also kept comfortably below falling 4 hour 55 EMA. Nonetheless, as it's staying above 105.24 temporary low, intraday bias remains neutral first. Again, as long as 107.67 resistance holds, near term outlook will remain bearish. Break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will pave the way to 98.97 key support level and below. However, break of 107.67 will indicate short term bottoming, on bullish convergence condition in 4 hour MACD. In such case, stronger rebound would be seen back to 55 day EMA (now at 108.92) first.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Dollar Attempting to Rebound as ADP Job Beat Expectation, But Momentum Weak

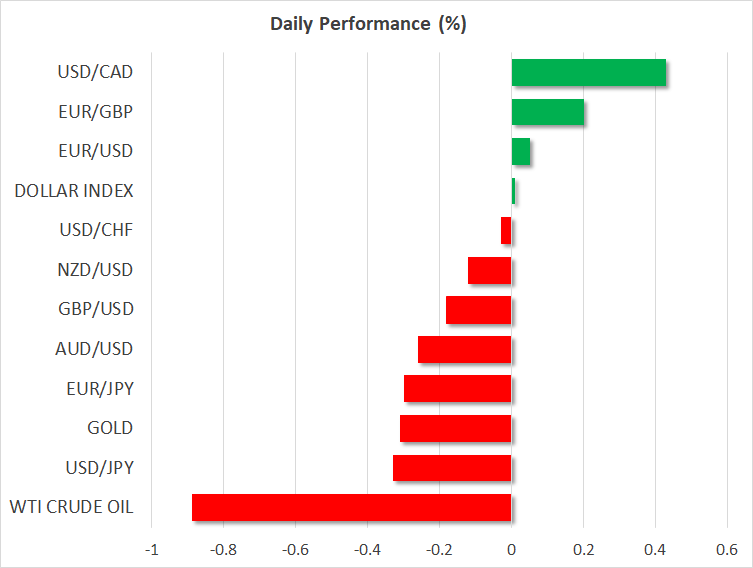

Dollar is trying to regain some ground in early US session after better than expected job data. But momentum of the greenback is so far very week. Dollar suffered some selling on news of White House top economic advisor Gary Cohn's resignation, due to his opposition to President Donald Trump's steel and aluminum tariff initiative. Global stocks are mixed today, with FTSE trading up 0.2% and DAX up 0.6%, following -0.77% decline in Nikkei. But DOW futures point to sharply lower open. Canadian Dollar continues to trade as the weakest one as markets await BoC rate decision.

Released from US, ADP report showed 235k growth in private sector jobs in February, above expectation of 200k. Prior month's figure was revised up from 234k to 244k. Trade deficit widened to USD -56.6b in January. Nonfarm productivity was finalized at 0.0% in Q4, unit labor costs at 2.5%. From Canada, trade deficit narrowed to CAD -1.91b in January. Labor productivity rose 0.2% qoq in Q4.

EU leaders discussing counter measures to US tariffs

Markets' eyes will stay on when and whether Trump would formally sign the order to impose the 25% tariffs on steel and 10% on aluminum. But for today, focus will turn to EU's plans first. EU leaders are discussing possible counter-measures should the tariffs are imposed. European commission tweeted today that "we have made it clear that a move that hurts the EU and puts thousands of European jobs in jeopardy will be met with a firm and proportionate response".

European Commission Vice President Valdis Dombrovskis said he hoped that the US initiative of steel and aluminum tariffs "will not be followed through." But he also warned that " EU is going to react if these one-sided tariffs are going to be imposed by the U.S." While EU is assessing the options of possible against against US, Dombrovskis emphasized that "we will react in a firm and proportionate way within WTO rules." This is inline with the rhetoric of all other EU officials.

It's reported that EU is considering a 25% tit-for-tat tariff on US goods that worth EU 2.8b, should US imposes the steel and aluminum tariffs.

IMF Lagarde: trade war generally finds losers on both sides

IMF Managing Director Christine Lagarde warned that "in a so-called trade war, driven by reciprocal increases of import tariffs, nobody wins, one generally finds losers on both sides." The macroeconomic impact could be serious especially if other countries were to retaliate. And, notably, she pointed to the most affected by US steel and aluminium tariffs, including Canada, Europe and Germany. She also pointed to China as a case that "some countries in the world that do not necessarily respect the World Trade Organization's agreements".

Released from EU, Euroarea E19 Q4 GDP growth was finalized at 0.6% qoq, 2.7% yoy. EU28 Q4 GDP growth was finalized at 0.6% qoq, 2.6% yoy. In Q4, Estonia ranked top with growth at 2.2%, followed by Slovenia at 2.0% and Lithuania at 1.4%. Greece and Croatia were both at bottom with growth at 0.1%, followed by Italy and Latvia at 0.3%.

Also released in European session, Swiss foreign currency reserves rose to CHF 733b in February, up from CHF 732b.

EU draft Brexit negotiation guidelines reject "mutual recognition

European Council President Donald Tusk is putting forward a draft of Brexit negotiation guidelines. The 6-page document was leaked to Politco. A point to note is that the document rules out UK Prime Minister Theresa May's proposal of "mutual recognition" of standards."

It notes that "trade in services … to an extent consistent with the fact that the U.K. will become a third country and the [European] Union and the U.K. will no longer share a common regulatory, supervisor, enforcement and judiciary framework."

Another point is that financial services is not included in the trade agreement. This certainly disappoints Chancellor Philip Hammond who has been pushing to include it.

Also, the "the European Council has to take into account the repeatedly stated positions of the UK, which limit the depth of such a future partnership. Being outside the customs union and the single market will inevitably lead to frictions.

BoJ deputy nominee Wakatabe: Policy should be date dependent, not date-driven

BoJ deputy governor nominee Masazumi Wakatabe appeared in upper house confirmation hearing today. He said that BoJ has "various things" that can be done under the yield curve control framework. In addition, it can " strengthen its existing tool kit," or even "come up with a new policy". Regarding the 2% inflation target, Wakatable emphasized that the policy is should be data-dependent, not date-driven" and not be bounded by a "set timeframe". He also cautioned that the impact of the sales tax hike in fiscal 2019 should be watched closely. Another deputy nominee Masayoshi Amamiya said there is still a distant to the 2% target and BoJ needs to continue with powerful easing.

Released from Japan, leading indicator dropped to 104.8 in January, down from 107.4.

RBA Low: No strong case for a near term hike

RBA Governor Philip Lowe expressed his optimism on the economy and said it's going to be "stronger" in 2018. He pointed to better business conditions "at any time since before the financial crisis." The economy is "moving in the right direction" and it's likely that the next move in interest rates is "up, no down". However, the board does not see a strong case for a near-term adjustment of monetary policy", thanks to slow progress in unemployment and inflation.

Regarding the steel and aluminum tariffs of the US, Lowe slammed it as "highly regrettable and bad policy". He added that "history is very clear here. Protectionism is costly." If it's confined to steel and aluminum tariffs, Lowe believed "it's manageable for the world economy." However, he warned that "this could turn very badly, though, if it escalates."

Australia GDP grew 0.4% qoq in Q4, below expectation of 0.5% qoq and slowed from prior 0.7% qoq. RBA is generally expected to keep rates on hold throughout 2018, except that NAB predicts one hike. Slowing growth figure in Q4 and risk of trade wars would add to the case for RBA to stand pat.

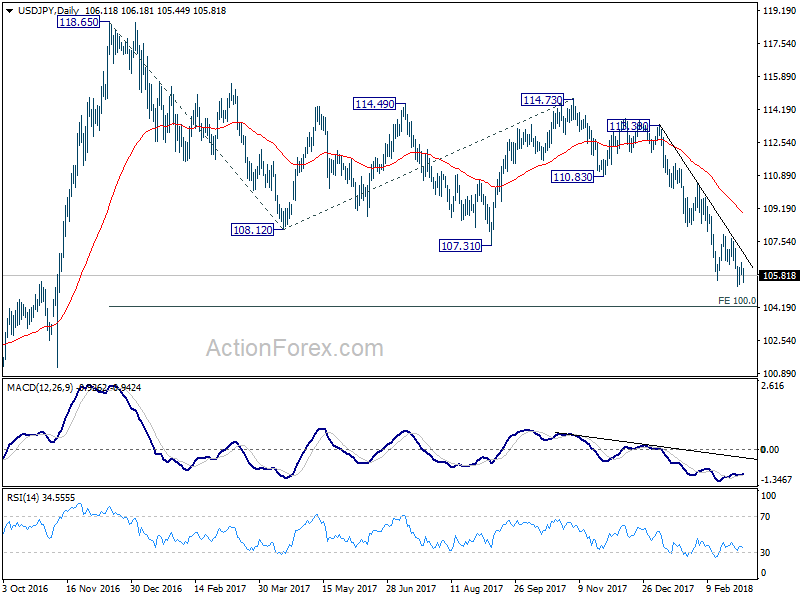

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.82; (P) 106.14; (R1) 106.43; More...

USD/JPY recovers mildly in early US session but momentum has been week. It's also kept comfortably below falling 4 hour 55 EMA. Nonetheless, as it's staying above 105.24 temporary low, intraday bias remains neutral first. Again, as long as 107.67 resistance holds, near term outlook will remain bearish. Break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will pave the way to 98.97 key support level and below. However, break of 107.67 will indicate short term bottoming, on bullish convergence condition in 4 hour MACD. In such case, stronger rebound would be seen back to 55 day EMA (now at 108.92) first.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

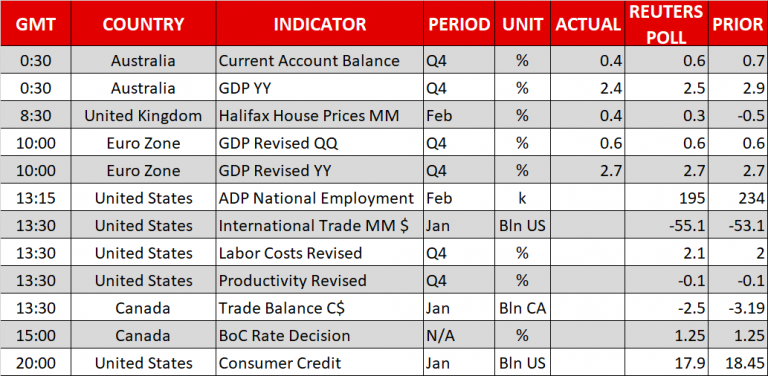

Economic Indicators Update

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q4 | 0.40% | 0.50% | 0.60% | 0.70% |

| 05:00 | JPY | Leading Index CI Jan P | 104.8 | 106.1 | 107.4 | |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Feb | 733B | 735B | 731B | 732B |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 F | 0.60% | 0.60% | 0.60% | |

| 13:15 | USD | ADP Employment Change Feb | 235K | 200K | 234K | 244K |

| 13:30 | USD | Nonfarm Productivity Q4 F | 0.00% | -0.10% | -0.10% | |

| 13:30 | USD | Unit Labor Costs Q4 F | 2.50% | 2.10% | 2.00% | |

| 13:30 | USD | Trade Balance Jan | -56.6B | -52.6B | -53.1B | -53.9B |

| 13:30 | CAD | Labor Productivity Q/Q Q4 | 0.20% | 0.30% | -0.60% | -0.50% |

| 13:30 | CAD | International Merchandise Trade (CAD) Jan | -1.91B | -2.50B | -3.2B | -3.05B |

| 15:00 | CAD | BoC Rate Decision | 1.25% | 1.25% | ||

| 15:30 | USD | Crude Oil Inventories | 3.0M | |||

| 19:00 | USD | Federal Reserve Beige Book |

ADP 235k beat expectation 200k, USD/JPY slightly higher

USD/JPY slightly higher as ADP job report beat expectation.

ADP Feb: 235k vs exp 200K vs prior 244k

But it remains to be seen if USD/JPY could sustain gain.

Canadian Dollar Dips, Markets Eye Bank of Canada

USD/CAD has posted gains in Wednesday session, erasing much of the losses seen on Tuesday. Currently, USD/CAD is trading at 1.2927, up 0.40% on the day. On the release front, today’s key event is ADP nonfarm payrolls, which is expected to drop sharply to 199 thousand. In Canada, the trade deficit is expected to narrow to C$2.5 billion. As well, the Bank of Canada will set the benchmark rate, which is expected to remain pegged at 1.25%.

The Federal Reserve is widely expected to raise rate four times in 2018, but the Bank of Canada will likely be unable to compete with that kind of pace. The BoC is concerned with economic growth, which slowed in the fourth quarter, as well as uncertainty over NAFTA, which could fall apart if the Trump administration makes good on its threat to withdraw if its demands for more favorable treatment for US goods is not met. The Bank is not expected to raise rates before May, and if the Fed outpaces the BoC on the rate front, the Canadian dollar could lose ground to a more attractive US currency.

The Canadian government is seeing red after President Trump has threatened to impose stiff tariffs on Canadian steel imports. Canada is the top exporter of steel to the US, accounting for some 16% of US steel imports. The “tariff tussle” could prove to be a major irritant in US-Canada relations, and has weakened the Canadian dollar, as USD/CAD broke above the 1.30 line on Monday, for the first time since late June. Trump is facing strong opposition to the move from Republican lawmakers, and has held out a carrot to Mexico and Canada – if a new NAFTA deal is reached, both countries would be exempted from the tariffs. Canada’s steel industry is a crucial backbone of the economy, and if the US does slap on the tariffs, it could ignite a trade war with Canada and other US trading partners.

Dollar Resumes Slide and Risk Appetite is Weakened, Following Cohn Shock

The unexpected nature of sudden announcements from the Whitehouse never fails to surprise.

Investors across the globe have been taken by surprise following the sudden news that top economic advisor to President Trump, Gary Cohn, resigned overnight. The breaking development encouraged an acceleration in selling momentum for the Dollar, with the Dollar Index touching its lowest level in two weeks. The resignation appears to have played a role in weakening risk appetite towards the stock markets. High-yielding currencies, like the South African Rand, suffered against the USD during trading on Wednesday. Other emerging market currencies, like the Russian Ruble and Turkish Lira, have also declined against the Dollar.

Gary Cohn was previously viewed as a leading candidate to replace past Federal Reserve Chair Janet Yellen, therefore his resignation has not been something that investors are prepared to overlook. Cohn was also seen as an advocate for global trade, therefore there is speculation that President Trump’s trade war rhetoric, is being considered as a catalyst behind his sudden resignation.

I think that investors will be inclined to take the news of Cohn’s resignation as another reason to sell the Dollar. It shouldn’t have a long-lasting impact on the stock markets and risk appetite, unless Trump does step up the trade war narrative.

The broad weakness in the Dollar during trading so far on Wednesday has been behind the Euro trading at its highest level in nearly three weeks, while the Japanese Yen appears to be close to achieving a new milestone high, after reaching its strongest level against the USD since November 2016 late last week. The Swiss Franc also gained against the Dollar.

Gold appears to be at risk for profit-taking after originally trending higher in the early hours of trading today. As long as Gold remains above the psychological $1300 level, I remain bullish on the precious metal over the medium and longer-term.

The British Pound is surprisingly one of the currencies that has been unable to capitalize on Dollar weakness. The Pound is currently trading lower against the Dollar. This could be linked to the GBPUSD facing what is seen as quite tough resistance around the 1.40 handle, although Sterling sensitivity to Brexit developments could also be encouraging pressure on the Pound.

EU Warns of Retaliation to US Tariffs, BoC Rate Decision Pending

Here are the latest developments in global markets:

FOREX: The resignation of Trump’s economic adviser and free-trade advocate, Gary Cohn, late yesterday, spurred speculations that the President’s plans to impose hefty import tariffs on aluminum and steel were more likely than analysts previously thought. The dollar index touched a fresh two-week low at 89.40 (-0.14%) and dollar/yen continued to trade near 16-month lows reached yesterday, last seen at 105.46 (-0.46%). Pound/dollar extended losses to reach 1.3858 (-0.17%) after the EU’s Brexit guidelines stated that a future trade deal should address an “appropriate” customs cooperation, preserving any regulatory autonomy. Moreover, the document acknowledged that Britain’s departure from the EU will lead to frictions in trade, though it also revealed the EU’s willingness to maintain a close partnership with the UK. Euro/dollar inched up to a fresh three-week high of 1.2443 (+0.14%) shrugging off US trade threats as the EU reiterated its warnings to react accordingly if the US punitive tariffs materialize. Speaking in Brussels, the EU trade Commissioner argued that US protectionism would damage transatlantic relations, hoping for the EU to be excluded from the tariffs. Dollar/loonie changed hands higher at 1.2932 (+0.43%) ahead of the BoC rate announcement, aussie/dollar edged back up to 0.7800 (-0.24%) but remained down on the day, while kiwi/dollar was weak at 0.7279 (-0.14%).

STOCKS: European stocks corrected lower following their Asian counterparts as Cohn’s resignation revived fears of a potential trade war between the US and the rest of the world. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.26% and 0.23% respectively at 1050 GMT. The German DAX 30 retreated by 0.19%, with automaker shares including mainly those of Volkswagen and Daimler being the worst performers in the index. Still, losses could have been larger if not offset by gains in telecommunications. The French CAC 40 fell by 0.37% and the British FTSE 100 managed to erase earlier losses after the British plane engine maker, Rolls Royce stated that it was on track to meet its 2020 goals, lifting its shares by 12.30%. US futures were in the red, pointing to a negative open.

COMMODITIES: Heightened trade risks weighed on oil prices as well, with WTI crude and Brent remaining pressured at $62.14 (-0.79%) and $65.27 (-0.73%) per barrel respectively. Yesterday, the API oil report added to concerns that US oil production could hamper OPEC’s efforts to curb supply as the numbers indicated a larger increase in US stockpiles than analysts thought. In precious metals, gold was slightly down at $1332.64 (-0.11%) per ounce.

Day ahead: Bank of Canada to announce interest rate decision; US ADP nonfarm employment report in focus

Day ahead: Bank of Canada to announce interest rate decision; US ADP nonfarm employment report in focus

The Bank of Canada (BoC) will announce its rate decision at 1500 GMT and expectations are for the central bankers to keep interest rates steady at 1.25% after raising borrowing costs three times since July, when rates stood at 0.75%. In the recent weeks, investors have been paring back the odds of a potential rate hike since the economy seemed to lose momentum in times when the government was struggling to reach an agreement on the NAFTA front. GDP growth slowed down surprisingly to 1.7% y/y in the final quarter of 2017, following a downward revision in the Q3 measure, while it was a big surprise to see employment declining sharply in January. Trump’s punitive import tariffs on steel could be another reason for the BoC to leave monetary policy unchanged today as Canada owns the largest share of steel imports to the US and any implementation of the measures could exaggerate trade conflicts between the countries and make NAFTA negotiations much more difficult. While markets are already waiting for the BoC to hold a cautious tone given the above risks, a larger degree of pessimism in the central bank’s outlook could push the loonie lower.

Canadian trade statistics for the month of January will be also available today prior the rate decision at 1330 GMT.

Meanwhile in the US, investors will keep a close eye on the ADP nonfarm employment report due at 1315 GMT before they prepare their positions ahead of the famous nonfarm payrolls on Friday. According to analysts, the ADP readings which regard the US private sector are expected to show an employment increase of 195,000 in February compared to 234,000 seen in the previous month. Government’s nonfarm payrolls which track changes in both the private and public labor sectors are anticipated to stand flat at 200,000.

In other data out of the US, the Fed’s Beige Book will give an overview of the current economic conditions in each of the 12 Federal districts at 1900 GMT, while the Energy Information Administration will publish its weekly report on US oil inventories earlier at 1530 GMT.

Elsewhere, Japan will see the release of the GDP growth figures for the final quarter of 2017 at 2350 GMT. However, these will be the second estimates and are likely to have a moderate impact on the yen. Forecasts continue to support a growth rate of 0.9% y/y, although first GDP growth estimates came in lower at 0.5%. Data on private consumption and capital expenditure will also attract some attention.

As for today’s speakers, we will hear from Atlanta Fed President Raphael Bostic (voter), as well as New York Fed President William Dudley (voter), at 1300 GMT and 1320 GMT respectively.

EU draft Brexit negotiation guidelines reject “mutual recognition”

European Council President Donald Tusk is putting forward a draft of Brexit negotiation guidelines. The 6-page document was leaked to Politco. A point to note is that the document rules out UK Prime Minister Theresa May's proposal of "mutual recognition" of standards.

It notes that "trade in services … to an extent consistent with the fact that the U.K. will become a third country and the [European] Union and the U.K. will no longer share a common regulatory, supervisor, enforcement and judiciary framework."

Another point is that financial services is not included in the trade agreement. This certainly disappoints Chancellor Philip Hammond who has been pushing to include it.

Also, the "the European Council has to take into account the repeatedly stated positions of the UK, which limit the depth of such a future partnership. Being outside the customs union and the single market will inevitably lead to frictions.