Sample Category Title

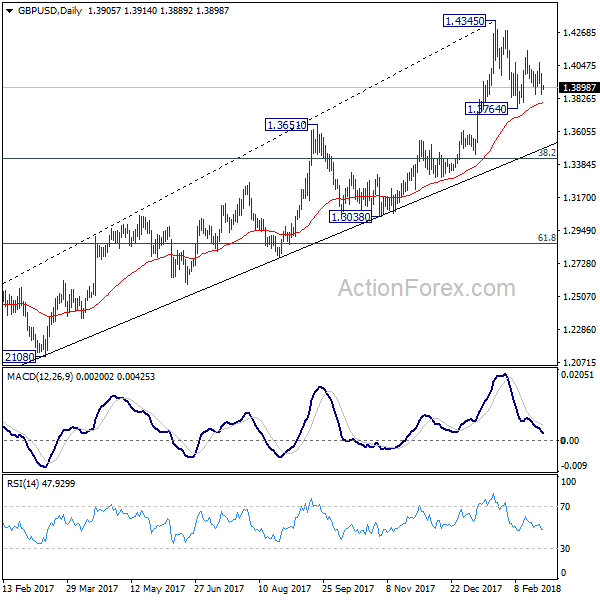

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3845; (P) 1.3921; (R1) 1.3984; More....

Intraday bias in GBP/USD remains neutral as it's bounded in range of 1.3764/4144. On the upside, break of 1.4144 will extend the rise from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5056). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

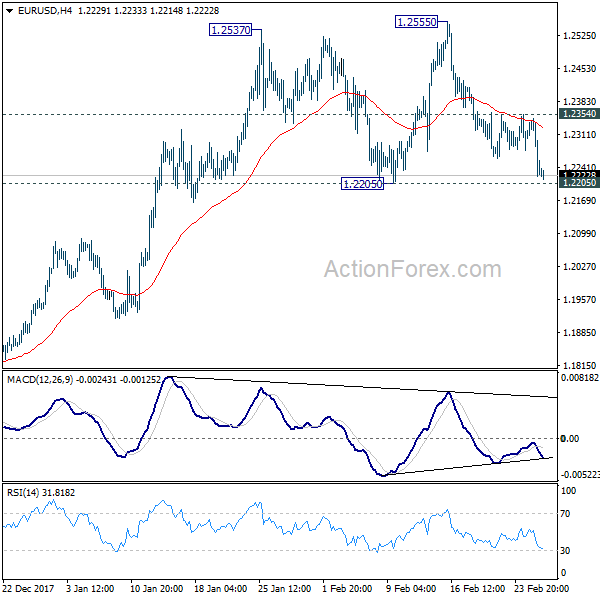

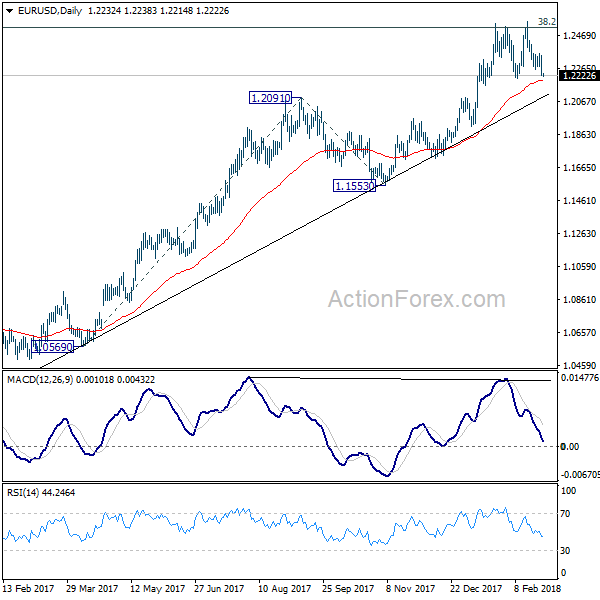

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2187; (P) 1.2266 (R1) 1.2312; More....

EUR/USD drops to as low as 1.2214 so far but it's still staying above 1.2205 key near term support. Intraday bias remains neutral at this point. As noted before, break of this important 1.2205 support will confirm rejection by 1.2516 key fibonacci level and trend reversal. IN that case, further decline should be seen back to 1.1553 support next. On the upside, above 1.2354 minor resistance will bring retest of 1.2555 high. Break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Dollar Jumped, Yields Surged, Stocks Tumbled after Fed Powell’s Upbeat Q&A

The initial response to Jerome Powell's first Congressional Testimony as Fed Chair was muted as his prepared speech provided nothing new. Nonetheless, stocks tumbled while Dollar surged as Powell offered an upbeat outlook in his Q&A. There are notable increase in chance of continuous rate hikes towards the end of the year as indicated by fed fund futures. DOW ended down -299.24 pts or -1.16% at 25410.03. S&P 500 dropped -35.32 pts or -1.27% to close at 2744.28. 10 year yield regained 2.9 handle by rising 0.049 to 2.908. Dollar index jumped to as high as 90.49 and is heading back towards 91.01 key structural resistance.

In the currency markets, Dollar is now trading as the strongest major currency for the week, followed by Yen and then Swiss Franc. Commodity currencies are the weakest ones. Nonetheless, we'd like to point out that Dollar is still holding below recent resistance against other currencies. The key levels are 1.2205 support in EUR/USD, 1.3764 in GBP/USD, 0.7758 in AUD/USD, 0.9469 resistance in USD/CHF and 108.27 in USD/JPY.

Fed Powell: Economy has strengthened since December

Described by some analysts as direct and forthcoming, Powell offered his optimistic view on the economic outlook. He told the House Financial services Committee that "my personal outlook for the economy has strengthened since December." And, "we've seen some data that will in my case add some confidence to my view that inflation is moving up to target. We've also seen continued strength around the globe, and we've seen fiscal policy become more stimulative."

Powell acknowledged that "fiscal policy changes can have an effect, changes of this size can have an effect, and that can be seen in the path of policy." But he added that "it's very hard to say in advance what that would be."

The key take away from his prepared speech is regarding recent financial market volatility. He said "we do not see these developments as weighing heavily on the outlook for economic activity, the labor market and inflation." This suggested the path is unlikely to be altered by the market volatility.

Let's take a look at fed fund futures pricing. They're now indicating 33.7% chance of a total of four hikes by December to raise the federal funds rate from 1.25-1.50% to 2.25-2.50%. That's notably higher than 26.9% a day ago and 22.6% a month ago.

UK Gfk consumer confidence stayed negative

UK Gfk consumer confidence dropped to -10 in February, down from -9. The series has not be positive since February 2016. Gfk noted that "ongoing concerns about sluggish household income, rising prices paid by consumers in the shops and the prospect of inflation-busting council tax and interest rate hikes has dented confidence after last month's surprising rally". And, "the two-year trend of negative sentiment proves consumers feel pessimistic about the state of household finances and the wider UK economy." "Consumers have good reason to feel jittery and depressed." BRC shop price index dropped -0.8% yoy in February.

NAB forecasts one RBA hike in 2018, instead of two

In Australia, the National Australia Bank lowered its RBA interest rate forecast for the year. NAB now expects only one RBA hike this year, instead of two. The bank said in its report that "weak wages growth and slow progress reducing unemployment means it is now less likely that the RBA will raise rates twice in 2018." It explained that "while total wages did increase a touch 0.55%, there was no acceleration in private wages growth." Nonetheless, "wage increases are overdue" and " tightness in employers' ability to find suitable labour, may finally see private sector wages start to moderately edge up." And, "we now see the RBA raising rates only once in late 2018 with November 2018 as the most likely start date for a gradual RBA rate hiking cycle." However, there is still a change for RBA to stand pat depending on data flow.

New Zealand business confidence stayed pessimistic

New Zealand ANZ business confidence improved to -19.0 in February, up from -37.8. That is, a net 19% of business were pessimistic about the year ahead. ANZ noted in the release that "a slower housing market, a small dip in net migration, difficulty finding credit and already-stretched construction and tourism sectors are making acceleration hard work from here." Meanwhile, "strong terms of trade and a positive outlook for wage growth are providing a push." And, "the rebound in business confidence is consistent with our belief that while no longer at top speed, this business cycle has legs yet. In particular, incomes are set to be supported by the strong terms of trade and higher wage growth."

Elsewhere

Japan retail sales rose 1.6% yoy in January versus expectation of 2.5% yoy. Japan industrial production dropped -6.6% mom in January versus expectation of -4.2% mom. China manufacturing PMI dropped to 50.3 in February, down from 51.3, missed expectation of 51.2. China non-manufacturing PMI dropped to 54.4, down from 55.3, missed expectation of 55.0.

Looking ahead

Eurozone CPI flash will be a major focus in European session. Germany will release unemployment and Gfk consumer sentiment. Swiss will release KOF leading indicator. Laster in the day, US will release GDP revision, Chicago PMI, pending home sales. Canada will release IPPI and RMPI.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2187; (P) 1.2266 (R1) 1.2312; More....

EUR/USD drops to as low as 1.2214 so far but it's still staying above 1.2205 key near term support. Intraday bias remains neutral at this point. As noted before, break of this important 1.2205 support will confirm rejection by 1.2516 key fibonacci level and trend reversal. IN that case, further decline should be seen back to 1.1553 support next. On the upside, above 1.2354 minor resistance will bring retest of 1.2555 high. Break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Jan | 1.60% | 2.50% | 3.60% | |

| 23:50 | JPY | Industrial Production M/M Jan P | -6.60% | -4.20% | 2.90% | |

| 0:00 | NZD | ANZ Business Confidence Feb | -19.0 | -37.8 | ||

| 0:01 | GBP | GfK Consumer Confidence Feb | -10 | -10 | -9 | |

| 0:01 | GBP | BRC Shop Price Index Y/Y Feb | -0.80% | -0.60% | -0.50% | |

| 1:00 | CNY | Manufacturing PMI Feb | 50.3 | 51.2 | 51.3 | |

| 1:00 | CNY | Non-manufacturing PMI Feb | 54.4 | 55 | 55.3 | |

| 5:00 | JPY | Housing Starts Y/Y Jan | -4.70% | -2.10% | ||

| 7:00 | EUR | German GfK Consumer Confidence Mar | 10.9 | 11 | ||

| 7:45 | EUR | French GDP Q/Q Q4 P | 0.60% | 0.60% | ||

| 7:45 | EUR | French GDP Y/Y Q4 P | 2.40% | 2.40% | ||

| 8:00 | CHF | KOF Leading Indicator Feb | 106 | 106.9 | ||

| 8:55 | EUR | German Unemployment Change Feb | -17K | -25K | ||

| 8:55 | EUR | German Unemployment Rate Feb | 5.40% | 5.40% | ||

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Feb | 1.20% | 1.30% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb A | 1.00% | 1.00% | ||

| 13:30 | CAD | Industrial Product Price M/M Jan | -0.10% | |||

| 13:30 | CAD | Raw Materials Price Index M/M Jan | -0.90% | |||

| 13:30 | USD | GDP Annualized Q/Q Q4 S | 2.50% | 2.60% | ||

| 13:30 | USD | GDP Price Index Q4 S | 2.40% | 2.40% | ||

| 14:45 | USD | Chicago PMI Feb | 64.6 | 65.7 | ||

| 15:00 | USD | Pending Home Sales M/M Jan | 0.50% | 0.50% | ||

| 15:30 | USD | Crude Oil Inventories | -1.6M |

GBP/USD At Continued Risk Of Weakness

Key Highlights

- The British Pound failed to move above the 1.4065 resistance and declined versus the US Dollar.

- There is a significant bearish trend line forming with resistance at 1.4030 on the 4-hours chart of GBP/USD.

- The US Durable Goods Orders in Jan 2018 declined 3.7%, more than the -2.0% forecast.

- Today, the US Gross Domestic Product Q4 2017 (Preliminary) will be released (Forecast 2.5% versus previous 2.6%).

GBPUSD Technical Analysis

The British Pound failed to move above a breakout resistance level near 1.4060-70 against the US Dollar. The GBP/USD pair is currently under pressure and it could trade further lower.

On the upside, there is a major resistance forming near 1.4030, and on the downside, there is a key support at 1.3900. A break on the either side could trigger the next move in GBP/USD.

Looking at the 4-hours chart, the pair was recently rejected from a significant bearish trend line with current resistance at 1.4030. The pair traded lower and broke the 50% Fib retracement level of the last wave from the 1.3856 low to 1.4069 high.

It is a negative sign and it seems like the pair may continue to decline towards the 1.3900 support. Should there be a break below the 1.3900 support, the pair may retest the last low of 1.3856. Any further declines could increase bearish pressures for a move towards 1.3750.

On the upside, the pair must break the trend line resistance near 1.4030 to recover. Above 1.4030, the pair may rise towards the 1.4100 level.

Recently in the US, the Durable Goods Orders figure for Jan 2018 was released by the US Census Bureau. The market was looking for a decline of 2% in orders.

The actual result was disappointing as there was a decline of 3.7% in orders in Jan 2018. Moreover, the Durable Goods Orders ex transportation posted a decline of 0.3%, whereas the market forecast was +0.4%.

The market sentiment still favored the US Dollar, and pairs such as EUR/USD and AUD/USD were under pressure. More importantly, the USD/JPY pair was seen trading higher with a positive tone.

Economic Releases to Watch Today

- Germany's Unemployment Change for Feb 2018 – Forecast -15K, versus -25K previous.

- Germany's Unemployment Rate for Feb 2018 – Forecast 5.4%, versus 5.4% previous.

- Euro Zone CPI for Feb 2018 (YoY) – Forecast +1.2%, versus +1.3% previous.

- US Gross Domestic Product Q4 2017 (Preliminary) – Forecast 2.5% versus previous 2.6%.

Market Morning Briefing: Pound Has Dipped Below Support Near 1.39

STOCKS

Dow (25410.03, -1.16%) and Dax (12490.73, -0.29%) have both dipped yesterday contrary to our expectation of further rise. Dax could test 12400 while below 12600 as mentioned yesterday while Dow could re-test 25000 in the near term.

Nikkei (22309.05, -0.36%) has come off from levels below 22600 and while that holds some dip towards 22200 or lower is possible in the coming sessions before it again attempts to move up. Near term looks bearish just now.

Shanghai (3252.80, -1.19%) also dipped as the resistance on the 3-day seemed to have held well. The index could come off towards 3250 in the near term. View is bearish for the coming sessions.

Nifty (10554.30, -0.27%) and Sensex (34346.39, -0.29%) are almost stable while a slight dip was seen yesterday. A sideways consolidation is possible in the coming sessions within 10620-10380 on Nifty and 34500-33750 on the Sensex.

COMMODITIES

Brent (66.32) has dipped, contrary to our expectation of a rise towards 68-69. This raises chances of a break below 66, which can then target 65 in the near term. Immediate rise towards 68-69 may be negated while below 67.

WTI (62.67) fell from levels near 64 instead of rising towards our mentioned 65 levels. It may possibly come down to test 62.

Brent-WTI Spread (3.65) may test interim resistance near 3.70/75 levels from where another dip looks likely in the next few sessions.

Gold (1317.43) also moved down contrary to our bullish expectation towards 1360/70 levels. Note immediate support near 1310 which if holds may gain push the index back towards 1340-1350 in the near term.

Copper (3.1785) is also down against our expectation to test 3.30. Near term dip is possible towards 3.15 before trying to move up again.

FOREX

The new US Fed Chairman (Jerome Powell) yesterday re affirmed the Fed’s plans of gradual rate hikes in 2018 due to strong confidence in rising US growth and inflation. These words from him have injected some temporary strength for the Dollar.

The Dollar Index (90.412) is close to resistance on the weekly candles (near 90.5) and we expect the same to hold in the near term. If it breaches 90.5, there are 2 strong resistances at 91 (3 day line chart and weekly line chart) and at 91.5 (weekly candle chart), which should produce a dip for the index.

Euro (1.2217) is holding above Support at 1.22 on the 3 day line chart. But, earlier bullishness is dented and will have to be re-examined. It has a good long-term Support at 1.2150 as seen on daily line chart, which can still produce a sharp rise, perhaps even up to 1.26 before the ECB meeting on 8th March.

Dollar-Yen (107.24) rose to a high near 107.70 last night, well above the intra-day bullish target of 107.25 we mentioned yesterday morning. Importantly, though, it has remained below the crucial long-term Resistance at 107.90-108.00, suggesting chances of long-term bearishness.

The Euro-Yen (131.02), is again testing support on daily candles near 131 and in case, the Euro strengthens towards 1.25-1.26 in the coming week while the Dollar Yen stays in the 106-108 zone, Euro Yen could rise towards 132.

Pound (1.3895) has dipped below support near 1.39, and could now test lower support near 1.38 on daily and 3 day candles before seeing a bounce.

Dollar-Rupee (65.12): The Dollar Rupee NDF rose to 65.15 yesterday night after Powell’s comments. We retain yesterday’s projection for now: Medium-term bullish towards 65.40.

INTEREST RATES

US 10 Year Yield (2.9081), US 30 year Yield (3.1654), US 5 year yield (2.6788), US 2 year yield (2.2741) : As per our expectation yesterday, the 10 Yr, 30 Yr and 5 Yr did indeed move up. The 2 year yield is at a record high level (above the 2.25-2.26 levels seen last week after the auctions).

Powell’s comments might just prove to be the market mover for the 10 Yr yield to move towards 3%. In case the US GDP data later today matches upto Powell’s bullish outlook on the US economy, we might well see yields rise in this week itself. If it falls short of expectations, we might see the yields hover around current levels for few more days.

(Long term resistance levels for the 4 yields have been as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively – a decisive breach of these levels could happen sometime in March.)

Powell Says ‘Personal Outlook Has Strengthened’

Our interpretation of Fed Chair Powell's testimony before the House of Representatives' Financial Services Committee is that he was being slightly hawkish, especially during the following Q&A session (no big changes in the prepared speech). Being asked about what would cause the Fed to hike more than three times, he said that 'his own personal outlook has strengthened' since December, as economic data have been strong.

In his prepared speech, we want to highlight two things. Firstly Powell said that headwinds have turned into tailwinds due to a combination of stronger global growth and expansionary fiscal policy. Secondly, Powell used the words 'overheated economy' trying to describe the Fed's dilemma, as the unemployment rate and inflation are low at the same time (see our tweet). Also noteworthy was that Powell said that he 'personally' likes to look at different policy rules going into FOMC meetings. In its Monetary Policy Report – February 2018 (released Friday 23 February) the Fed describes a few rules – see our tweet. In the Q&A session, Powell said that 'all else being equal' looser fiscal policy should be offset by tighter monetary policy but did not directly answered whether it would be one-to-one.

Markets also interpreted Powell hawkishly, especially during the Q&A session. US 2yr Treasury yield rose 4bp to 2.26% while EUR/USD fell from 1.2320 to 1.2236 at the time of writing. S&P500 also fell 0.7% from its intraday peak during the Q&A.

We believe the Fed will stick to its '3 hikes' signal for 2018 at the upcoming meeting in March but that some of the six members currently indicating two or fewer hikes will lift their dots thus showing more confidence in the outlook. It will also be interesting to see what happens in relation to 2019 where the Fed currently indicates two hikes (taking the Fed funds rate to the longer-run dot of 2.75%, which is the level where monetary policy is neither expansionary nor contractionary). We think the signal for 2019 will be raised to three hikes (it was already borderline last time) hence signalling they want to start hitting the brakes by moving rates above the natural rate of interest due to expansionary fiscal policy. This should not change our view that fiscal policy is not offset one-to-one meaning inflation is still set to move gradually higher

Hawks 1 Doves 0

Hawks 1 Doves 0

Jay Powell testified before the U.S. House of Representatives’ Financial Services Committee stressing the Fed needs a policy anchor grounded in continuity. Indeed, the tone of Chair Powell’s written testimony suggests that on the whole, the Fed policy isn’t about to shift abruptly under his leadership and that the pace of gradual rate hikes will continue to be the mainstay of the Fed narrative. However, his pointer at the topside potential for both inflation and growth suggests the risks as skewed for a bolder montery policy response.

The shifting balance of risks has the market considering the possibility of more 2018 rate hikes than expected given his outlook on both growth and inflation. The Fed’s December economic outlook pointed to three rate increases this year, but with two surprisingly strong inflation prints between then and now, they have likely tipped the scales on the Feds inflation outlook.

In the aftermath, we are in the midst of vintage cross-asset rotation as front-end treasuries sell-off, stock markets are discernably lower, and commodities are tanking in response to Powell hawkishness. Denuded of any significant fireworks, however, the message from Powell’s testimony was clear. With the economy in full swing, monetary policy needs to get back in the game. In fact, he’s not too concerned about risk aversion but factoring the economic upside from fiscal policy

After day one of the two-day policy test: Hawks 1 Doves 0

Equity Markets

US equity markets closed in a sea of red which is expected to engulf Asia markets today. No need to sugar coat this analysis as there was no rabbit out of the hat just the big bad bear. Investors may have been expecting some response to equity market volatility, but that was apparently of little concern to Powell. Indeed, no sign of a “Powell Put” in play, which is trading well out of the money at this stage. . With that in mind, the odds of four rates in 2018 rose to 33% from about 20% on Monday, according to CME Group’s data.

Oil Markets

The asset rotation out of commodity markets on the stronger USD narrative combined with the oil traders refocusing on shale production output as the US on course to be the worlds largest oil producer has prices convincingly moving lower.

Also, suggestions OPEC could taper production cuts early 2019 is weighing on sentiment this morning. Given that OPEC compliance is responsible for 40-50 % of recent oil price appreciation, Saudi oil minister Khalid al-Falih comments are not going without notice.

It’s a typical trader reaction, when markets flip upside down, all the negatives come to the fore.

Gold Markets

Gold found fresh session lows post-Powell testimony bottoming around 1313.5 before finding a bid and consolidating around the 1318 levels. All part and parcel of the classic asset rotation as the strong dollar pressured gold lower. While traders will wait for confirmation in tomorrows senate testimony which tends to be more telling, today’s discussion suggests we could see a higher interest rate profile and recovering dollar near term which could trigger a more profound move lower on Gold. Not the best of outcomes for Gold bulls

Currency Markets

The Euro

The combination of a hawkish Powell and uber ECB hawk Weidmann coming out dovish has convincingly toppled the Euro. Weidmann is in the running for the ECB president and likely becoming more moderate given that its ECB hawkishness that sends the Euro soaring which panics most ECB members.But let’s not lose sight that the recent German CPI missed expectation suggestion inflation in the EU largest economy is not an issue and no immediate need to raise rates

The Japanese Yen

Only moderate upward pressure on USDJPY and almost as everyone wants to stay away given that recent ranges continue to hold firm. Perhaps uncertainty over month-end flows or caught between equity sell-off vs higher US rate dynamics, but the balance of risk suggest a test of the 107.50-75 levels sooner than later

The Australian Dollar

Commodity currencies took it on the chin overnight, but the Aussie remains tentatively supported above the primary .7775 level. But one thing that tends to hold true for the A$, and hardly a scientific metric mind you, buy Aussie when you can’t find a bull

The Malaysian Ringgit

The Ringgit is holding up well this morning in pre-open trades despite the market increasing bets on an addition US rate hike in 2018 and oil prices moving lower.

The Ringgit external position remains very favourable and given market positioning is not excessive, one other Fed fund rate hike in 2018 is less impact the MYR than regional peers. Also, the BNM raised interest early this year and will do so again if inflation warrant. While a faster pace of US interest rate normalisation is not an ideal platform for region currencies, it’s not all doom and gloom for the Ringgit.

GBP/USD – Pound Dips As Powell Pushes Dollar Higher

The British pound has posted losses in the Tuesday session. In North American trade, GBP/USD is trading at 1.3925, down 0.28% on the day. In economic news, Federal Reserve Chair Jerome Powell made his first appearance before Congress. Meanwhile, durable goods reports were dismal. Core Durable Goods declined 0.3%, short of the estimate of +0.4%. This marked the second decline in three months. Durable Goods plunged 3.7%, missing the estimate of -2.4%. This reading was the sharpest decline since July. There was better news from CB Consumer Confidence, which improved to 130.8, well above the estimate of 126.2 points. Later in the day, the UK releases BRC Shop Price Index and GfK Consumer Confidence. On Wednesday, the US releases Preliminary GDP, with an estimate of 2.5%.

There were no dramatic moments during Jerome Powell’s testimony before a congressional committee on Tuesday. Powell was cautious, saying that the Fed planned to continue its current policy of gradual rate increases, despite the stimulus of government spending and recent tax reform. Powell sounded optimistic about economic conditions, noting that the US economy was benefiting from the global recovery as well as changes in fiscal policy. Importantly, Powell did not address the question of an acceleration of rate hikes. Currently, the Fed has projected three rate hikes in 2018, with a March hike priced in at 87%, according to the CME’s Fed Watch. However, with inflation moving higher and the economy continuing to perform well, many analysts expect the Fed to raise rates four or more times this year. Any hints at an increased pace of rate hikes could send the US dollar broadly higher.

Brexit negotiations have been bumpy from the start, but matters seem to be deteriorating almost daily. Prime Minister May is in a tough spot, with the Europeans dismissing her latest proposals on a trade deal after Brexit, and many members of her party supporting playing hard with Europe. May has proposed that a trade deal would allow some divergence with EU regulations in certain industries, but the Europeans have dismissed this as ‘cherry picking’, which they say is a non-starter. May will lay out her post-Brexit vision of relations with the EU in a speech on Friday and if the Europeans pour cold water on her plan, the markets could react negatively.

Gold Slides As Powell Says Gradual Rate Hikes To Continue

Gold has posted sharp losses in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1314.53 down 1.40% on the day. In economic news, Federal Reserve Chair Jerome Powell made his first appearance before Congress. Meanwhile, durable goods reports were dismal. Core Durable Goods declined 0.3%, short of the estimate of +0.4%. This marked the second decline in three months. Durable Goods plunged 3.7%, missing the estimate of -2.4%. This reading was the sharpest decline since July. There was better news from CB Consumer Confidence, which improved to 130.8, well above the estimate of 126.2 points. On Wednesday, the US releases Preliminary GDP, with an estimate of 2.5%.

There were no dramatic moments during Jerome Powell’s testimony before a congressional committee on Tuesday. Powell was cautious, saying that the Fed planned to continue its current policy of gradual rate increases, despite the stimulus of government spending and recent tax reform. Powell sounded optimistic about economic conditions, noting that the US economy was benefiting from the global recovery as well as changes in fiscal policy. Importantly, Powell did not address the question of an acceleration of rate hikes. Currently, the Fed has projected three rate hikes in 2018, with a March hike priced in at 87%, according to the CME’s Fed Watch. However, with inflation moving higher and the economy continuing to perform well, many analysts expect the Fed to raise rates four or more times this year. Any hints at an increased pace of rate hikes could send the US dollar broadly higher.

Gold often moves higher when key US indicators point downward, but that has not been the case in the Tuesday session. Despite very soft durable goods reports for January, the dollar has posted gains against other major currencies and has surged against gold. Investors have given the greenback a thumbs-up after Jerome Powell’s testimony earlier, in which he pointed to solid economic conditions and reiterated the need for further rate hikes. Gold has dropped to a 2-week low, and the slide could continue if sentiment over the dollar remains positive.

USD/JPY – Japanese Yen Dips On Powell Testimony

The Japanese yen has lost ground in the Tuesday session. In North American trade, USD/JPY is trading at 107.45, up 0.48% on the day. On the release front, BoJ Core Inflation edged up to 0.8%, beating the forecast of 0.6%. In the US, durable goods reports were dismal. Core Durable Goods declined 0.3%, short of the estimate of +0.4%. This marked the second decline in three months. Durable Goods plunged 3.7%, missing the estimate of -2.4%. This reading was the sharpest decline since July. There was better news from CB Consumer Confidence, which improved to 130.8, well above the estimate of 126.2 points. In Washington, Federal Reserve Chair Jerome Powell made his first appearance before Congress. Later in the day, Japan releases Preliminary Industrial Production and Retail Sales. On Wednesday, the US releases Preliminary GDP, with an estimate of 2.5%.

All eyes were on Jerome Powell on Tuesday, and the new Fed chair played it safe in his written testimony before a congressional committee. Powell said that the Fed would maintain its policy of gradual rate increases, despite the stimulus of government spending and recent tax reform. Powell sounded optimistic about economic conditions, noting that the US economy was benefiting from the global recovery as well as changes in fiscal policy. Importantly, Powell did not address the question of an acceleration of rate hikes. Currently, the Fed has projected three rate hikes in 2018, with a March hike priced in at 87%, according to the CME’s Fed Watch. However, with inflation moving higher and the economy continuing to perform well, many analysts expect the Fed to raise rates four or more times this year. Any hints at an increased pace of rate hikes could send the US dollar broadly higher.

Bank of Japan Governor Harohiko Kuroda was recently reward with a second 5-year term, and has lost no time in defending his monetary policy. Speaking in parliament on Monday, Kuroda said he had no plans to conduct a review as to why the Bank’s massive stimulus program had failed to raise inflation to the target of just under 2 percent. Kuroda said it was “unfortunate” that the target had not been met, but argued that the BoJ’s “powerful” monetary easing had eliminated deflation. Kuroda’s comments were another clear message that the BoJ will not be reducing its massive stimulus program anytime soon. The Japanese economy has rebounded, but inflation has not kept pace, with BoJ core consumer inflation climbing just 0.8% in January.