Sample Category Title

Will Dollar Rally Or Fade On Fed Powell’s Comments?

Tuesday February 27: Five things the markets are talking about

New Fed Chair Jerome Powell makes his first public appearance as the central bank's new leader today.

He starts with the release of his prepared testimony at 8:30 am, EST followed by his appearance before the House Financial Services Committee starting at 10 am, EST.

Note: He returns Thursday to answer questions from the Senate Banking Committee, beginning at 10 am, EST.

Expect today's testimony to be heavily scrutinized as capital markets want to know Powell's views on inflation, and how much of a risk it is or is not, and his views on the need for banking regulation.

Investors will also want to know how he characterizes the implications of current market conditions for Fed policy – are easy financial conditions and elevated asset values reasons enough to hike rates more than would otherwise be the case? Fed fund futures are pricing in three Fed hikes (+58%) and the possibility of a fourth (+21%).

Does the new Fed chief view the recent market volatility as a healthy development for markets that had looked unusually good-natured over the past 12-months?

Ahead of the U.S open, Euro equities struggle for direction as the dollar edges a tad lower with Treasuries steady.

1. Stocks mixed results

In Asia overnight, equity markets traded generally higher after yesterday's U.S gains.

In Japan, the Nikkei share average hit a three-week high, led by gains in large-cap and exporters' shares as easing in U.S. bond yields overnight-improved sentiment. The Nikkei rose +1.1%, its highest close since Feb. 5. The broader Topix rose +0.9%.

Down-under, the Aussie ASX 200 closed at its highest in more than three-weeks on Tuesday, supported mostly by resources stocks which ticked up on a slight rise in metal prices. The index rose +0.2% at the close of trade. In S. Korea, the Kospi closed up +0.7% after the Bank of Korea (BoK) left their seven-day Repo rate unchanged at +1.5% as expected.

In Hong Kong, stocks fell from their three-week highs overnight, as investors took profit ahead of Fed Chair Powell's first congressional testimony. The Hang Seng index fell -0.7%, while the China Enterprises Index lost -1.5%.

In China, stocks snapped a six-session winning streak, led lower by real estate and resource firms. At the close, the Shanghai Composite Index was down -1.1%, while the blue-chip CSI300 index was down -1.4%.

Note: The market continues to ponder the impact of certain amendments in the wording of China's constitution, which would allow President Xi Jinping to stay in office indefinitely.

In Europe, regional bourses struggle for direction as investors await the first public comments from new Fed Chair Powell later this morning. The U.K.'s FTSE 100 Index increased +0.4% to the highest in more than three-weeks.

U.S stock futures are set to open in the 'red' (-0.3%).

Indices: Stoxx 600 -0.2% at 382.5, FTSE +0.1% at 7299, DAX -0.1% at 12517, CAC-40 +0.1% at 5349, IBEX-35 flat at 9900, FTSE MIB flat at 22713 , SMI -0.4% at 8993, S&P 500 Futures -0.3%

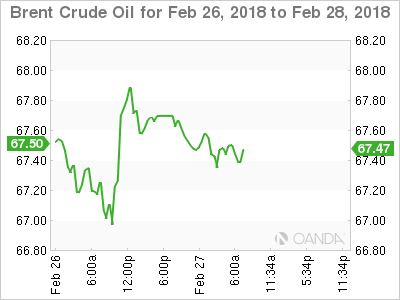

2. Oil prices lower as rising U.S supply outweigh demand, gold unchanged

Oil prices have erased their earlier overnight gains as investor concerns about rising U.S oil output offset signs of stronger demand and faith in the ability of OPEC production curbs to curtail supply.

Brent crude futures are down -12c, or -0.2%, at +$67.38 a barrel. While U.S West Texas Intermediate (WTI) crude for April delivery is down -13c, or -0.2%, at +$63.78 a barrel. The contract yesterday rose to its highest since Feb. 6 at +$64.24.

Climbing U.S production is overturning global oil markets, coming at a time when OPEC members – including Russia – have been withholding output to prop up prices.

According to the IEA's Executive Director Fatih Birol, the U.S will overtake Russia as the world's biggest oil producer by 2019 at the latest.

The market will take its cues from this week's inventory reports – the American Petroleum Institute (API) is scheduled to release its weekly data later on this afternoon, followed by the EIA on Wednesday.

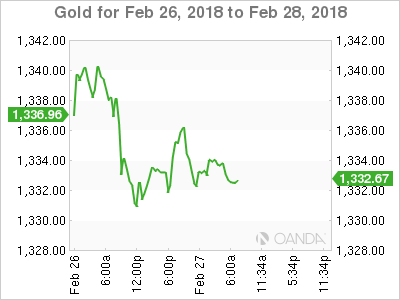

Ahead of the U.S open, gold prices are trading steady, as the 'big' dollar remains little changed while investors' await Fed Powell's first congressional testimony for clues on the future pace of monetary tightening. Spot gold is up +0.1% at +$1,334.26 an ounce.

3. Sovereign yields contained

According to the latest positioning data from the Chicago futures exchanges, speculators are making their biggest ever short-term bet on higher U.S interest rates and are also slowly beginning to rebuild their bets on lower U.S stock market volatility.

The amount of speculative net short positions in Eurodollar futures rose to record -3.65m contracts in the week ended Feb. 20.

Note: Money markets are pricing in a rate hike at the conclusion of the Fed's March 20-21 policy meeting – this will be the sixth hike in the current cycle, with another two this year factored into market pricing.

The CFTC data also showed that speculators continued to reduce the record long position in VIX futures. They reduced that net long position by 15,013 contracts in the week to Feb. 20, following a reduction of 11,255 contracts the week before. This brought the net long VIX futures position down to 59,550 contracts from a record high 85,818 on Feb. 6.

The yield on U.S 10-year Treasuries fell -1 bps to +2.86%, the lowest in two weeks. In Germany, the 10-year Bund yield advanced +1 bps to +0.66%, the first advance in a week and the biggest gain in more than a week. In the U.K, the 10-year Gilt yield fell -1 bps to +1.509%, reaching the lowest in four-weeks on its sixth consecutive decline.

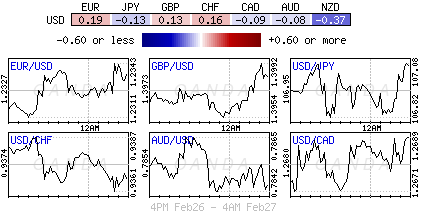

4. Dollars mixed results, waiting for Powell

The U.S dollar trades mixed ahead of the U.S open, rising slightly relative to most currencies and is down sharply versus Bitcoin (BTC +4% $10,731) as the market waits for the new Fed Chairman's “Humphrey-Hawkins” testimony before Congress.

Today, Mr. Powell makes his debut before the House Financial Services Committee beginning at 10:00 am. However, as is always the case in such instances his prepared text will be released at 08:30 am.

Dollar 'bulls' believe that his testimony could boost the dollar if he stresses a positive U.S economic outlook and the prospect of more interest rate rises.

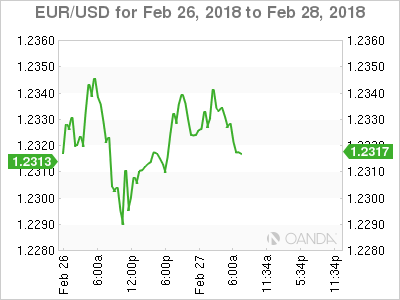

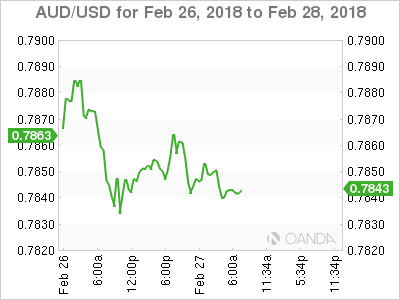

Dollar 'bears' would view any dollar rally as short-lived and a good opportunity to position for more USD weakness. In this scenario, the market has preferred to be buying EUR/USD and AUD/USD, and sell USD/JPY.

Ahead of the U.S open, the DXY dollar index trades -0.1% lower. The EUR/USD has rallied +0.2% to €1.2340, though the dollar has rallied against some other currencies: AUD/USD is down -0.1% at A$0.7847, USD/JPY is up +0.1% at ¥107.02.

5. ECB: Loans to firms, M3 money supply rose last month

Note: With the eurozone economy heavily dependent on bank lending, analysts watch lending data closely as an indicator of the economy's health.

Data this morning from the ECB showed that lending to firms picked up at the start of the year.

Lending to firms grew by +3.4% on the year in January after growing +3.1% in December. Lending to households rose +2.9% on the year in January, matching the pace set the previous month.

The ECB's key indicator of the money supply, M3, grew by +4.6% on year, in line with both the previous month and market expectations. The three-month average stood at +4.7% vs. +4.8% (e).

EUR/USD – Euro Quiet Ahead Of German CPI, Powell Testimony

The euro is showing limited movement in the Tuesday session. Currently, EUR/USD is trading at 1.2330, up 0.10% on the day. On the release front, German Preliminary CPI is expected to rebound with a gain of 0.5%. In the US, the markets are braced for weak data from durable goods. Core Durable Goods Orders are forecast to dip to 0.4%, and Durable Goods Orders are expected to decline 2.4%. Another key release is CB Consumer Confidence, which is expected to climb to 126.2 points. As well, Jerome Powell will testify before a congressional committee.

It hasn’t been a smooth ride for Jerome Powell, who took over as chair of the Federal Reserve from Janet Yellen earlier this month. Powell received a rude welcome from the markets just after moving into his new office, as the global stock market correction erased some $4 trillion in valuations. The volatility forced Powell to make a public statement, reassuring the markets that the Fed was closely monitoring the situation.

How will the dollar react to Powell’s testimony before the House Banking Committee? After the recent turmoil in the stock markets, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.

On Thursday, the ECB released the minutes of its January meeting. The markets were looking for some hints regarding future monetary policy, and policymakers indicated that they could re-examine the Bank’s monetary policy “early this year”. The ECB is keeping a close eye on inflation, which has been moving upwards. Still, with inflation below the ECB target of just below 2%, there is little talk about raising interest rates. Policymakers also indicated concern with exchange rates, a theme which has been addressed by Mario Draghi in recent weeks, given the appreciation of the euro – EUR/USD has climbed 2.8% since the start of the year. The minutes voiced “concerns about the recent volatility in the euro exchange rate, which represented a source of uncertainty that had to be monitored with respect to its implications for the medium-term outlook for price stability”. The euro has seen plenty of volatility in February, and currency volatility will likely be high on the agenda of the next policy meeting in March.

Market Update – European Session: German Inflation Data Lacks Convincing Signs Of A Sustained Upward Adjustment

Notes/Observations

Markets not anticipating any surprises in Chairman Powell’s inaugural testimony to Congress in the prepared remarks

Bulk of German Feb State CPI data generally coming below consensus for the composite reading of 1.5%; highlights Draghi view that inflation had yet to show more convincing signs of a sustained upward adjustment

Various European confidence data was generally better in the session: Euro Zone and Italy were slight beat while Sweden was mixed

Asia:

Bank of Korea (BOK) left the 7-Day Repo Rate unchanged at 1.50%; as expected. Reiterated to maintain accomodative policy stance. Would carefully judge if necessary to adjust policy rates further

China PBoC could again raise open market operation (OMO) rates following the expected Fed rate hike

Europe:

EU draft on Brexit treaty (to be released on Feb 28th) to set out its legal detail on how it expects the UK to depart in just over one year’s time with terms of a transition period that will follow. EU draft Brexit treaty said to ignore some of the UK PM most important demands. Likely to exclude May’s proposals for how the transitional phase would work and leave out a key compromise UK future land border with Ireland

EU is to demand in a draft treaty document that the UK remains subject to indefinite European Court of Justice (ECJ) oversight after Brexit. Mechanism is back up by sanctions that cut off market access if Britain ignore court rulings and is among a host of issues included in the draft

IMF's Lagarde reiterated its WEO forecast for 2018 and 2019 global GDP growth of 3.9%

Americas:

Fed's Quarles (hawk, FOMC voter): expected further gradual rate hikes will be appropriate

Treasury Sec Mnuchin reiterates view that in the long term a strong dollar was good for the US; did not set policy to impact the dollar (left to market forces). Did not think people were concerned yet about inflation; if inflation showed up that could be a concern

Economic Data:

(NL) Netherlands Feb Producer Confidence: 10.9 v 10.3 prior

(FI) Finland Feb Consumer Confidence: 25.8 v 24.2 prior; Business Confidence: 15 v 15 prior

(TR) Turkey Feb Economic Confidence: 103.0 v 104.9 prior

(FR) France Feb Consumer Confidence: 100 v 103e

(DE) Germany Feb CPI Saxony M/M: +0.4% v -0.8% prior; Y/Y: 1.3% v 1.4% prior

(ES) Spain Feb Preliminary CPI M/M: +0.1% v -0.1%e; Y/Y: 1.1% v 0.9%e

(ES) Spain Feb Preliminary CPI EU Harmonized M/M: +0.1% v -0.2%e; Y/Y: 1.2% v 0.9%e

(SE) Sweden Feb Consumer Confidence: 104.7 v 107.0e; Manufacturing Confidence: 114.0 v 113.0e, Economic Tendency Survey: 109.5 v 110.0e

(HU) Hungary Jan Unemployment Rate: 3.8% v 3.9%e

(SE) Sweden Jan Household Lending Y/Y: 7.0% v 6.9%e

(SE) Sweden Jan Trade Balance (SEK): -1.8B v +1.5Be

(HK) Hong Kong Jan Trade Balance (HKD): -31.9B v -20.3Be; Exports Y/Y: 18.1% v 16.1%e; Imports Y/Y: 23.8% v 18.3%e

(EU) Euro Zone Jan M3 Money Supply Y/Y: 4.6% v 4.6%e

(DE) Germany Feb CPI Brandenburg M/M: +0.3% v -0.5% prior; Y/Y: 1.5% v 1.7% prior

(DE) Germany Feb CPI Hesse M/M: +0.4% v -0.8% prior; Y/Y: 1.1% v 1.3% prior

(DE) Germany Feb CPI Bavaria M/M: +0.5% v -0.7% prior; Y/Y: 1.6% v 1.8% prior

(IT) Italy Feb Consumer Confidence: 115.6 v 115.0e; Manufacturing Confidence: 110.6 v 109.2e, Economic Sentiment: 108.7 v 105.6 prior

(IS) Iceland Feb CPI M/M: +0.6% v -0.1% prior; Y/Y: 2.3% v 2.4% prior

(DE) Germany Feb CPI North Rhine Westphalia M/M: +0.5% v -0.6% prior; Y/Y: 1.3% v 1.5% prior

(PT) Portugal Feb Consumer Confidence: 1.3 v 1.3 prior; Economic Climate Indicator: 1.9 v 1.9 prior

(EU) Euro Zone Feb Final Business Climate Indicator: 1.48 v 1.47e; Consumer Confidence (Final): 0.1 v 0.1e, Economic Confidence: 114.1 v 114.0e, Industrial Confidence: 8.0 v 8.0e, Services Confidence: 17.5 v 16.3e

(DE) Germany Feb CPI Baden Wuerttemberg M/M: 0.5% v -0.7% prior; Y/Y: 1.6% v 1.7% prior

Fixed Income Issuance:

(DK) Denmark sold total DKK9.28B in 3-month and 6-month Bills

(ID) Indonesia sold total IDR23.1T vs. IDR17T target in 3-month and 12-Month Bills, 5-year,15-year and 20-year Bonds

(ZA) South Africa sold total ZAR3.3B vs. ZAR 3.3B indicated in 2026, 2030 and 2040 and 2048 bonds

(IT) Italy Debt Agency (Tesoro) sells total €6.0B vs. €4.5-6.0B indicated range in 5-year and 10-year BTP bonds

Sold €4.0B vs. €3.0-4.0B indicated range in new 0.95% Mar 2023 BTP bonds; Avg Yield: 0.89% v 0.66% prior;Bid-to-cover: 1.38x v 1.61 x prior

Sold €2.0B vs. €1.5-2.0B indicated range in 2.00% Feb 2028 BTP bonds; Avg Yield: 2.06% v 2.06% prior;Bid-to-cover: 1.37x v 1.25x prior

(IT) Italy Debt Agency (Tesoro) sells €1.711B vs. €1.25-1.75B indicated range in Apr 2025 CCTeu (Floating Rate Bonds); Avg Yield: 0.42% v 0.42% prior; Bid-to-cover: x v 1.63x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.2% at 382.5, FTSE +0.1% at 7299, DAX -0.1% at 12517, CAC-40 +0.1% at 5349 , IBEX-35 flat at 9900, FTSE MIB flat at 22713 , SMI -0.4% at 8993, S&P 500 Futures -0.3%]

Market Focal Points/Key Themes: European Indices trade mixed this morning in an active morning, following a mixed session in Asia and slightly lower US futures. Notable earnings this morning included German chemical giant BASF which trades lower after mixed results, with Fresenius Medical also trading lower after results and outlook. To the upside, Fresenius SE and UK Home builder Persimmon trades higher after results. Elsewhere Sky plc trades sharply higher after Comcast proposed a £12.50/shr offer representing a 16% premium over 21st Century Fox offer, while Provident Financial trades sharply higher after the it settled the FCA investigation into Vanquis. In the US reports that Microchip said to be near agreement to acquire Microsemi, while Toll Brother reported Q1 results and largely affirmed its outlook. Looking ahead notable earners include Autozone, Macy's and Discovery.

Movers

Consumer Discretionary [Sky Plc [SKY.UK] +22% (Increased takeover offer from Comcast), Inchcape [INCH.UK] -3.4% (earnings)]

Industrials [BASF [BAS.DE] -1.5% (Earnings), Meggit [MGGT.UK] -3.6% (Earnings)]

Healthcare [Fresenius SE [FRE.DE] +2.0% (earnings), Fresenius Medical [FME.DE] -4.0% (Earnings)]

Financial [Post Italia [PST.IT] +5.3% (Long term outlook), Direct Line [DLG.UK] -1.1% (Earnings), Bankia [BKIA.ES} +1.6% (Strategic update), Provident Finacial [PFG.UK] +70% (Earnings, Rights issue, Settles FCA investigation into Vanquis), Swiss Life [SLHN.CH] +1.8% (earnings), Stanchart [STAN.UK] +1.8% (Earnings)]

Real Estate [Persimmon [PSN.UK] +11% (Earnings)]

Speakers

ECB’s Weidmann (Germany) reiterated view that bigger QE reduction and clear end date would have been justifiable. Rapid economic growth in region confirmed that inflation would move towards target. Important to gradually and dependably reduce ECB stimulus when inflation picked up. Evidence that FX movements were having a smaller impact on inflation than compared to the past but reiterated that ECB would keep a close look at exchange rates

BOE Dep Gov Woods: Top priority is to avoid chaos from Brexit in insurance market; up to speed on contingency plans for insurance sector

UK Foreign Min Johnson: UK could not remain subject to European Court of Justice (ECJ) rulings

Sweden Central Bank (Riksbank) Dep Gov Jochnick: Needed inflation to pick up and stabilize before any rate hike. Current economic situation was good but Jan inflation data was a surprise. Riksbank prepared to change its policy if needed

Czech PM Babis: Govt approved increase in pensions

Greece Economy Min Papadimitriou resigns (accepted by PM Tsipras)

Norway Sovereign Wealth Fund annual report: 2017 return +13.7% v 6.9% y/y

Philippines Central Bank (BSP) Guinigundo: Not seeing the point to adjust policy rate at this time; expect inflation to start easing by end 2018

Currencies

FX price action was limited as participants awaited the inaugural testimony from Fed Chair Powell. Overall markets were not anticipating any surprises in Powell’s prepared remarks. Key focus in Powell’s testimony will be his views on US tax reform and the weak USD.

GBP/USD was steady at 1.3950 ahead of the EU’s draft Brexit document forthcoming on Wed and PM May’s Brexit clarity speech on Friday.

EUR/USD was steady at 1.2325 area as German Feb State CPI data generally came in below the consensus for the composite reading of 1.5%; Dealers noted that CPI highlights Draghi concern that inflation had yet to show more convincing signs of a sustained upward adjustment

Fixed Income

Bund Futures trades down 14 ticks at 159.23 as markets prepare for Fed Chairman Powell’s inaugural testimony to Congress. Upside targets 159.75, while a return lower targets the157.75 level.

Gilt futures trade at 121.90 down 14 ticks as Gilts attempt to push higher on cash flow, supporting core bonds. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.00-122.25 zone then 122.85.

Tuesday's liquidity report showed Monday's excess liquidity rose to €1.848T from €1.834T prior. Use of the marginal lending facility fell to €25M from €37M prior.

Corporate issuance expects to see $18.3B in supply this week

Looking Ahead

(AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave 7-Day Repo Reference rate unchanged at 27.25%

(DE) Germany Feb CPI Baden Wuerttemberg M/M: No est v -0.7% prior; Y/Y: No est v 1.7% prior

(BE) Belgium Feb CPI M/M: No est v 0.3% prior; Y/Y: No est v 1.7% prior

(BR) Brazil Jan Central Govt Budget Balance (BRL): No est v -21.2B prior

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (EU) ECB allotment in 7-day Main Financing Tender

05:30 (BE) Belgium Debt Agency (BDA) to sell 3-month and 6-month Bills

06:00 (IE) Ireland Feb Unemployment Rate: No est v 6.1% prior

06:00 (BR) Brazil Feb FGV Inflation IGPM M/M: 0.0%e v 0.8% prior; Y/Y: -0.5%e v -0.4% prior

06:45 (US) Daily Libor Fixing - 07:00 (RU) Russia announces weekly OFZ bond auction

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (HU) Hungary Central Bank (NBH) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

08:00 (DE) Germany Feb CPI M/M: +0.5%e v -0.7% prior; Y/Y: 1.5%e v 1.6% prior

08:00 (DE) Germany Feb CPI EU Harmonized M/M: +0.6%e v -1.0% prior; Y/Y: 1.3%e v 1.4% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Jan Preliminary Durable Goods Orders: -2.0%e v +2.8% prior; Durables Ex Transportation: 0.4%e v 0.7% prior, Capital Goods Orders (Non-defense/ Ex-Aircraft): +0.5%e v -0.6% prior, Goods Shipment (Non-defense/ex-aircraft): 0.3%e v 0.4% prior; - Durables Ex-Defense: No est

08:30 (US) Jan Preliminary Wholesale Inventories: 0.4%e v 0.4% prior; Retail Inventories M/M: No est v 0.2% prior

08:30 (US) Jan Advance Goods Trade Balance: -$72.3Be v -$723B prior (revised from -$71.6B) - 08:30 (BR) Brazil Jan Total Outstanding Loans (BRL): No est v 3.086T prior; M/M: No est v 0.7% prior

08:30 (US) Fed Chair Powell text of testimony released

08:55 (US) Weekly Redbook Sales

09:00 (US) Dec FHFA House Price Index M/M: 0.4%e v 0.4% prior; Q/Q: No est v 1.4% prior

09:00 (US) Dec S&P/ Case-Shiller 20-City MoM: 0.60%e v 0.75% prior; YoY: 6.35%e v 6.41% prior; House Price Index (HPI): No est v 204.21 prior

09:00 S&P Case-Shiller (overall) HPI YoY: No est v 6.21% prior; Overall HPI Index : No est v 195.94 prior

09:00 (EU) Weekly ECB Forex Reserves

09:00 (MX) Mexico Jan Unemployment Rate (Seasonally Adj): 3.3%e v 3.4% prior; Unemployment Rate (unadj): 3.4%e v 3.1% prior

09:00 (MX) Mexico Jan Trade Balance: -$3.6Be v -$0.2B prior

09:00 (HU) Hungary Central Bank Gov Matolcsy post rate decision statement

10:00 (US) Feb Richmond Fed Manufacturing Index: 15e v 14 prior

10:00 (US) Feb Consumer Confidence: 126.4e v 125.4 prior

10:00 (US) Fed Chair Powell testifies to House Financial Services Committee

11:30 (US) Treasury to sell 4-week and 52-week Bills

12:00 SE) Sweden Central bank (Riksbank) Dep Gov Ohlsson (hawk)

15:00 (US) Jan Agriculture Prices Received: No est v 4.4% prior

15:45 (NZ) RBNZ Dep Gov Bascand

16:00 (CA) Canada Fin Min Morneau delivers Federal Budget

16:00 (KR) South Korea Mar Business Manufacturing Survey: No est v 77 prior, Non-Manufacturing Survey: No est v 78 prior

Traders Cautious Ahead Of Powell Testimony

- Powell Appearance Eyed For Interest Rate Clues;

- Data Takes Back Seat to Powell Testimony;

- $12,000 Key For Bitcoin.

Powell Appearance Eyed For Interest Rate Clues

US futures are slightly in the red ahead of the open on Tuesday as traders adopt a cautious approach ahead of Jerome Powell’s first appearance as Chairman of the Federal Reserve.

Twice a year the Fed Chair appears before the House Financial Services Committee and the Senate Banking Committee to discuss the semi-annual monetary report, events that often draw a lot of attention for obvious reasons. With Powell having just replaced Janet Yellen as head of the central bank – and not even led a meeting at this stage - today’s hearing will likely attract heightened attention as traders look for clues on the direction that he plans to take it.

The feeling so far is that Powell is unlikely to diverge from the current path which would imply three rate hikes this year but with the economy strengthening and tax reform potentially providing additional stimulus, a fourth hike may be warranted this year and along with additional increases further down the road. The market seems quite well positioned on this at the moment which may reduce the likelihood of significant shocks, although we’ve seen how vulnerable markets have shown themselves to be in recent weeks.

Data Takes Back Seat to Powell Testimony

With the event being largely unscripted and markets remaining a little on edge, there is the potential for plenty of volatility throughout today’s and Thursday’s sessions, all the more reason why Powell may well refrain from saying anything that could have adverse consequences on his debut appearance.

There is also some economic data being released today, although it will likely be largely overshadowed by the Powell testimony. Durable goods orders will be released around the start of Powell’s appearance, along with trade and inventories data. This will be followed shortly after the open by CB consumer confidence data and the Richmond manufacturing index.

$12,000 Key For Bitcoin

It’s been a relatively quiet session so far in Europe with no major economic data leaving markets trading mostly flat. Even bitcoin is having a quiet day so far by its own standard, with the cryptocurrency trading a couple of percent higher on the day and back above $10,000. Bitcoin rallied close to $12,000 last week before stalling and paring gains, having run into resistance around what was an equally tough hurdle in the second half of January.

On that occasion, the level proved too strong and prices fell back towards $6,000 shortly after. Whether it breaks above here on this occasion may be a good indicator of whether bitcoin has in fact bottomed, at which point it will be interesting to see how long it takes to reach its December peak in the absence of the euphoria that aided it last time around.

Technical Outlook: WTI Oil – Risk Of Further Easing Exists Before Bulls Resume

WTI oil eases on Tuesday but holding near fresh three-week high at $64.22, posted on Monday. Oil price advanced strongly in previous few sessions, boosted by news about Saudi Arabia's commitment to continue with production cut program. Positive sentiment persists, with consolidation and possible deeper pullback on profit-taking and overbought conditions, expected to precede fresh upside. Daily MA's are in firm bullish setup while 14-d momentum is breaking into positive territory and underpinning bulls. On the other side, overbought slow stochastic suggests a pause in rally. Today's easing was so far shallow and holding well above initial supports at $63.06/$62.80 (30SMA/Fibo 23.6% of $58.19/$64.22 rally), lacking stronger bearish signal which could be generated on reversal of slow stochastic. Converged 10/20SMA which are about to create bullish cross at $62.27, mark next strong support, along with $61.92 (Fibo 38.2% of $58.19/$64.22 rally), where extended pullback should find ground to avert risk of deeper correction which would sideline bulls. Bulls keep in focus targets at $64.62 (Fibo 76.4% of $66.64/$58.06 fall) and $65.00 (psychological barrier).

Res: 64.07, 64.22, 64.62, 65.00

Sup: 63.62, 63.06, 62.80, 62.27

Technical Outlook: SPOT GOLD – Action Is Directionless Ahead Of Fed Chair Powell Testimony

Spot Gold trades in directionless mode on Tuesday, with the action being so far shaped I Doji candle.

Strong upside rejection at $1341and daily close below a cluster of daily MA’s (10/20/30 SMA, laying between $1333 and $1337 was negative signal, but limited downside action was seen so far. mentum studies are bullish).

Directionless near-term mode is supported by mixed daily studies (MA’s are in negative setup, while momentum studies are bullish).

Overall action remains underpinned by rising and widening daily cloud (cloud top lies at $1314), but recovery from $1320 (22 Feb trough) was so far limited and lacks stronger bullish signal on close above cracked Fibo 38.2% of $1361/$1320 downleg ($1336).

Traders are focusing on today’s testimony of Fed Chairman Jerome Powell, which could generate fresh signals for the greenback.

Stronger wording about increasing pace of rate hikes in 2018 would be supportive for dollar and deflate yellow metal’s price, while softer tone from Powell would have negative impact on US currency and would boost Gold’s price.

Session low at/hourly cloud base mark initial support at $1331, followed by $1326 zone (lows of 26/23 Feb) which guard $1320 trough.

Fibo 38.2% resistance at $1336 is reinforced by daily Kijun-sen and marks the first pivot ahead of $1341 (Mon high/daily Tenkan-sen) and $1346 (Fibo 61.8% of $1361/$1320).

Res: 1336, 1341, 1346, 1348

Sup: 1331, 1326, 1320, 1317

CRUDE OIL Consolidation

Crude oil upward trend is momentarily interrupted slightly below hourly resistance at 64.77 (11/01/2018 high) and is maintained at 63.60. Crude oil hourly support remains at 58.07 (09/02/2018 low). The technical structure suggests short-term sideway moves.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Declining

Silver is trading lower following a hike at 16.77 (26/02/2018), suggesting further short-term decline. Hourly support and resistance are given at 16.27 (07/02/2018 low) and 16.98 (15/02/2018).

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Stabilizing At 1333

Gold is trading lower following recent selling pressures, declining from 1341 high (26/02/2018). Hourly support and resistance are given at 1318 (14/02/2018 low) and 1351 (01/02/2018 high). The technical structure suggests further sideway moves.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

BITCOIN Riding Higher

Bitcoin recovers from recent decline below 9390, edging higher along 11500. Hourly support and resistance at 9022 (30/11/2018 low) and 12130 (18/01/2018 high) remain.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading above its 200 DMA (6'500 range).