Sample Category Title

EURUSD Intraday Analysis

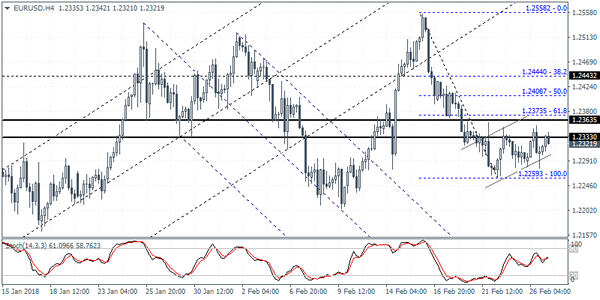

EURUSD (1.2321): The EURUSD attempted to rally to intraday highs but price action was seen closing lower on the day off the highs. On the 4-hour chart, we see the bearish flag pattern being formed, right below the main resistance level where the EURUSD has been consolidating. A break down below the base at 1.2260 could signal further declines targeting 1.2074. Alternately, EURUSD will need to close strongly above the resistance level in order to invalidate the downside bias. However, in this scenario, we still expect to see consolidation taking place unless the EURUSD manages to post fresh highs.

USD Steadies Ahead Of Powell Testimony

The U.S. dollar managed to hold its ground on Monday as investors brace for Fed Chair, Powell's semi-annual testimony to Congress later today. Although Powell hasn't yet officially chaired any FOMC meetings, his testimony could be seen as a major indicator of how monetary policy will be steered under his governance.

On the economic front, Mario Draghi gave his testimony to the European parliament on Monday. No major references were made to monetary policy. He however said that the central bank needs to remain patient with inflation. In the U.S. new home sales data showed a decline as home sales rose only 593k missing estimates of 655k.

Looking ahead, the economic calendar today is busy. The U.S. durable goods orders data will be coming out and forecasts point to a decline on the headline print. Germany and Spain will be releasing the flash inflation readings while Canada will be releasing its annual budget plans.

Currencies: Will Powell Give USD Some Downside Protection

Sunrise Market Commentary

- Rates: Powell to confirm Fed's path to policy normalization

Over the previous days, core bonds staged a cautious technical rebound as investors were looking forward to today's hearing of Fed's Powell before Congress. We expect the Fed chairman to hold a positive tone on the US economy, in line with the previous Fed minutes. If so, it probably doesn't leave that much room for further gains of US Treasuries. - Currencies: Will Powell give the dollar some downside protection

Yesterday, the dollar hovered up and down as investors awaited today's hearing of Fed's Powell on Capitol Hill. Will the Fed chairman signal a big enough Fed engagement on policy normalization to provide the USD some downside protection. UK labour leader Corbyn's preference for the UK to stay in a customs union with the EU doesn't help sterling for now

The Sunrise Headlines

- US equity markets started the week on a strong footing, extending the rally from the end of last week. Major US indices closed 1.15% (Nasdaq) to 1.58% (Dow) higher. Asian markets join the rebound from the US. China underperforms, trading in negative territory.

- At the last policy meeting of Governor Lee Ju-yeol, the Bank of Korea kept its policy rate unchanged. Lee said that the BoK was not obliged to follow a global withdrawal of stimulus. The Bank of Korea is expected to tighten policy only in a gradual way after its hike to 1.50% in November.

- The EU is said to publish a draft Brexit treaty on Wednesday in which it will set out in legal detail how it expects the U.K. to depart from the EU and the terms of a transition period that will follow, according to sources. The report probably won't meet the UK's demand on several key issues.

- According to Bloomberg, Apple is preparing to release a trio of new smartphones later this year: the largest iPhone ever, an upgraded handset the same size as the current iPhone X and a less expensive model with some of the flagship phone's key features. With the new line-up, Apple wants to appeal to consumers who crave the multitasking attributes of so-called phablets while also catering to those looking for a more affordable version of the iPhone X..

- Today's eco calendar is heavily packed containing, amongst others, German CPI data, EMU economic confidence and money supply data. In the US, the advance goods trade balance, US inventory data, durable goods orders, Housing data, the Richmond Fed manufacturing index and Consumer confidence (Conference Board) will be published. ECB's Merch and Weidmann are scheduled to speak. The focus of markets will be on the hearing of Fed Chairman Powell before the House Financial Services Committee

Currencies: Will Powell Give USD Some Downside Protection

Will Powell give USD some downside protection

The dollar started the week on a soft footing, but gradually received a better bid later in the session despite soft comments from Fed's Bullard. (FX) Markets were looking forward to today's hearing of Fed Chairman Powell on the Hill and to plenty of eco data scheduled later this week. Investors apparently didn't want to be too much short dollar going into these events. USD/JPY rebounded back to the high 106/low 107 area. EUR/USD reversed early gains and returned to the 1.23 area.

This morning, Asian equities join the rally from WS, with China underperforming. The dollar is losing a few ticks against the euro (EUR/USD currently 1.2330) and the yen (USD/JPY currently 106.85).

Today, there are plenty of data including German CPI, the US goods trade balance, durable goods orders and consumer confidence. However, the data will likely be overshadowed by the first semi-annual hearing of Fed Chairman Powell before the House financial services Committee. His testimony will probably be balanced. Even so, he will likely confirm that solid US growth requires further normalization of monetary policy. In the end, his message might be (mildly) USD supportive. Soft German inflation data might be a slightly negative for the euro. Of late,; we advocated some further consolidation of EUR/USD in the 1.25/1.2165 consolidation pattern. We maintain that view for now. We look out whether a positive assessment of Powell on the US economy and markets anticipating further US policy normalization might cause EUR/USD to go for a test of the 1.2165/1.2206 range bottom.

Yesterday, sterling initially profited from hawkish comments from BoE's Ramsden this weekend and from UK Labour Party leader Corbyn supporting the case for the UK to enter a customs union with the EU after Brexit. However, for now his approach doesn't break the UK political stalemate on Brexit. Sterling returned earlier gains. EUR/GBP rebounded north of 0.88. Today, there are no UK eco data. However, headlines suggest more headwinds from the EU to the Brexit agenda of the UK government. Over the previous days, sterling received a slightly better bid, but the move had no strong momentum. For now, the 0.8690 range bottom still looks a very solid support/GBP resistance

EUR/USD: dollar going nowhere. Will Powell provide the clue for a next directional move?

Elliott Wave Analysis: USDCHF And EURUSD Update

USDCHF and EURUSD are negatively correlated, which means if one makes a turn and goes higher, the other one will likely turn lower at the same time.

We see USDCHF. which can also be trading in a flat correction as EURUSD, but in a reversed one. We see recovery from 0.9256 as sub-wave a, followed by a sharp drop as b and now rally from the lows indicates that maybe blue wave c of 4 can be in progress. As such price can rally towards the 0.9473 level, before final drop lower comes in play as black wave 5 of C).

USDCHF, 4H

EURUSD, 4H

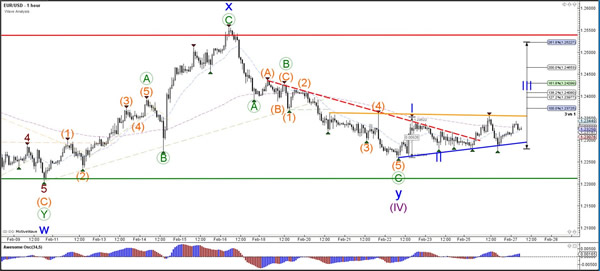

Daily Wave Analysis: EUR/USD Prepares For Breakout Of Triangle Chart Pattern

Currency pair EUR/USD

The EUR/USD has failed to break below the support trend line (blue), which could indicate a potential bullish reversal to test the previous tops (red line). A break below the previous bottom (green) would make a wave 4 (purple) pattern less likely.

The EUR/USD needs to break above the resistance trend line (orange) fora bullish breakout towards the Fib targets of wave 3 (blue). A strong bearish turn at 1.2475-1.25 could indicate that price has built an ABC rather than a 123.

Currency pair GBP/USD

The GBP/USD failed to break above the resistance trend line (red) and remains in a triangle chart pattern. Price will need to break the S&R before a new trend becomes visible.

The GBP/USD is broke below the support trend line (dotted green) and could be building a bearish ABC (orange) zigzag within a larger WXY correction (grey) unless price manages to break above resistance (red).

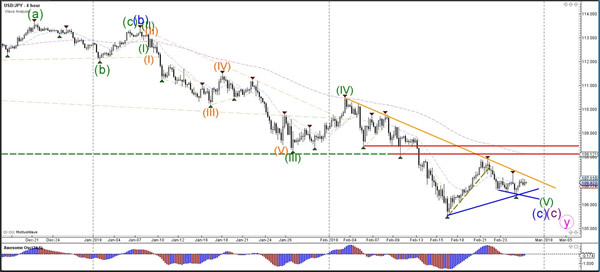

Currency pair USD/JPY

The USD/JPY could make one more lower low within wave 5 (green) if price manages to break below the support trend line (blue).

The USD/JPY bullish breakout would probably invalidate wave 4 (orange) whereas a bearish break could indicate a downtrend continuation.

Equity Markets Expect A Dovish Powell, Currency Traders On The Sidelines

After a strong rally in U.S. equity and bond markets on Friday, the upward trajectory resumed on Monday. The S&P 500 gained 1.18% and the Dow added an impressive 400 points, ending the day 1.58% higher. Both indices are now 3.4% away from their record highs, after regaining more than two-third of their correctionlosses.

Investor appetite forrisk has returned strongly in the past two trading days,thanks to stabilizing interest rates. Not only didU.S. Treasury yields fell further away from last week's highs, but even high yield bonds attracted some decent inflows. Volatility fell to a three-week low, with the VIX Index ending the day below 16, having declined 68% from its 6 February peak.

Having beenwelcomed to office by the steepest correction in more than six years, equity investors feel that the new Fed Chair, Jerome Powell, will restore confidence. However, the reaction in currency markets was muted, with the EURUSD and USDJPY trading in narrow ranges as traders appear to be sitting on the sidelines until Powell provides a new catalyst.

Powell's first semi-annual monetary policy testimony to Congress later today is likely to be the most significant risk event of the week. The new Fed Chair will likely downplay the latest market correction and show confidence in highlighting improvements in the economy, but the markets' reaction will depend on how the Fed reacts against such a development.

Investor focus should be on whether recent inflation and wage growth figures are starting to become a concern forthe central bank. If Powell stated that faster-than-expected inflation would lead to a more aggressive tightening policy (suggesting four rate hikes instead of three) in 2018, investors will go back onthe defensive, and risk appetite will be killed. Such a scenario will see a sharp rally in the U.S. dollar, and a steep selloff in equities and bonds.

However, financial markets believe that Powell will not be this transparent regardingthe path of interest rate hikes, and that a gradual policy normalization with three rate hikes this year is likely to be the base case scenario in today's message. There's likely to be some room for disappointment here, especially if Powell feels that the Fed is slightly behind the curve and isn't overly concerned about investor response.

In Europe, the focus will return to macro data, with the German preliminary CPI release likely to show that inflation abated in February. Meanwhile, speeches from the ECB Governing Council members Jens Weidmann and Yves Mersch will be of greater importance to the Euro, especially if they provide fresh insights on the ECB's monetary policy outlook.

FX Markets Are Calm As They Wait For New Fed Chairman Powell

The ECB's Coeure spoke in Frankfurt at a working group meeting regarding euro risk-free rates. He said that a reform of reference interest rate will help to underpin good functioning euro area money markets and trust in its related products. He also added that it is vital since monetary policy is initially transmitted through financial markets. He added that smooth and successful reform of reference interest rate is vital.

The US Fed's Bullard made a scheduled speech from Washington with the following comments: The natural rate of interest is low and not likely to change, and the Fed guidance ought to describe a relatively flat rate path. Substantial Fed hikes risk making policy too tight, and weak productivity is one factor holding down natural rate of unemployment. It's a good idea to periodically review inflation framework but it would require a ‘buy-in' from the political and financial community. High demand for safe assets is a global issue. Proponents of changing framework would have to prove it would add benefits. The rise in 10-year rates is partially driven by the rise in inflation expectations among investors. He says he's sceptical that 10-year yields will break out from here and inflation expectations have moved up some.

US Chicago Fed National Activity Index (Jan) was 0.12 v an expected 0.15, from a previous 0.27, with EURUSD moving lower from 1.23228 to a low of 1.23016.

ECB President Marion Draghi testified on monetary policy and the inflation outlook before the European Parliament Economic and Monetary Affairs Committee in Brussels. His comments were: Growth is stronger than previously expected and the Eurozone economy is expanding robustly. At the same time, inflation has yet to show more convincing signs of a sustained upward adjustment. Given the uncertainty surrounding the measure of economic slack, the true number might be larger than estimated. We anticipate that headline inflation will resume its gradual upward adjustment. The Labour market is expected to improve further. The relationship between growth and inflation remains largely intact, even if it was temporarily weakened. ECB guidance on interest rates is ‘very important' and US Tax Reform will reshape the global Tax landscape.

US New Home Sales (MoM) (Jan) was 0.593M v an expected 0.645M, from 0.625M previously, which was revised up to 0.643M. New Home Sales Change (MoM) (Jan) was -7.8% v an expected 3.2%, from -9.3% previously, which was revised up to -7.6%. EURUSD sold off from 1.23033 to 1.22862 as a result of this data.

US Dallas Fed Manufacturing Business Index (Feb) was 37.2 v an expected 28.4, from 33.4 previously.

US FOMC Member Quarles delivered a speech titled “An Assessment of the US Economy” at the National Association of Business Economics Policy Conference, in Washington DC. Audience questions followed and some of the comments made were: “With my current economic outlook, I anticipate that further gradual increases in the policy rate will be appropriate to both sustain a healthy labor market and stabilize inflation around our 2 percent objective”. He also said that “Some of the factors that have been holding back growth in recent years could shift, moving the economy onto a higher growth trajectory” and “I currently see this shift more as a clear possibility than an unarguable reality.”

New Zealand Trade Balance (MoM) (Jan) numbers were released at $-566M and were expected to be $-2710M. The prior number was $640M, which was revised up to $596M. Imports (Jan) were $4.87B v an expected $4.60B, from $4.91B previously, which was revised down to $4.89B. Trade Balance (YoY) (Jan) was $-3.220B v an expected $-2.711B, from $-2.840B previously, which was revised down to $-2.880B. Exports (Jan) were $4.31B against an expected $4.58B, from $5.55B previously, which was revised down to $5.49B. AUDNZD moved higher from 1.07364 to 1.07847 after this data release.

EURUSD is up 0.05% overnight, trading around 1.23236.

USDJPY is down -0.03% in early session trading at around 106.870.

GBPUSD is unchanged this morning trading around 1.39632.

Gold is unchanged in early morning trading at around $1,332.92.

WTI is down -0.28% this morning, trading around $63.81.

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.2% against the USD and closed at 0.7849.

LME Copper prices rose 0.5% or $37.5/MT to $7111.0/MT. Aluminium prices declined 1.0% or $21.5/MT to $2188.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7842, with the AUD trading 0.09% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7814, and a fall through could take it to the next support level of 0.7787. The pair is expected to find its first resistance at 0.7881, and a rise through could take it to the next resistance level of 0.7921.

Moving ahead, traders would keep a close watch on Australia’s private sector credit data for January, scheduled to release overnight.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Euro-Zone’s Economic Slack May Be Bigger Than Thought, Warns ECB’s Draghi

For the 24 hours to 23:00 GMT, the EUR marginally declined against the USD and closed at 1.2311, after the European Central Bank's (ECB) President, Mario Draghi, stuck to his pledge of pouring money into the Euro-zone economy.

The ECB Chief cautioned that the slack in the Euro-zone's economy may be wider than initially estimated and this could act as a temporary drag on inflation growth. Further, Draghi emphasised the need to maintain the central bank's ultra-loose monetary policy support despite acknowledging the robust and broad based economic growth across the Euro-zone.

In the US, data showed that new home sales unexpectedly fell by 7.8% on monthly basis to a level of 593.0K in January, hitting its lowest level since August 2017, thus stoking concerns that the nation's housing market is losing momentum. New home sales had registered a revised reading of 643.0K in the prior month, while markets were anticipating for an increase to a level of 647.0K.

Other economic data revealed that the US Dallas Fed manufacturing business index surprisingly advanced to a level of 37.2 in February, defying market consensus for a drop to a level of 30.0. The index had registered a reading of 33.4 in the previous month. On the other hand, the nation's Chicago Fed national activity index registered an unexpected drop to a level of 0.12 in January, compared to a revised reading of 0.14 in the previous month. Markets were expecting the index to rise to a level of 0.20.

In the Asian session, at GMT0400, the pair is trading at 1.2326, with the EUR trading 0.12% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2285, and a fall through could take it to the next support level of 1.2243. The pair is expected to find its first resistance at 1.2361, and a rise through could take it to the next resistance level of 1.2395.

Going ahead, traders would closely monitor the Euro-zone's final consumer confidence index for February, slated to release in a few hours. Moreover, Germany's flash inflation numbers for February, set to release later in the day, will be on investors' radar. Later in the day, market participants would look forward to the Federal Reserve Chairman, Jerome Powell's first congressional testimony to get better insights on the future pace of monetary policy tightening. Moreover, the US advance goods trade balance, flash durable goods orders, both for January as well as the CB consumer confidence index for February, would keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

UK’s BBA Mortgage Approvals Grew For First Time In 4 Months In January

For the 24 hours to 23:00 GMT, the GBP declined 0.26% against the USD and closed at 1.3963.

On the macro front, data showed that UK's BBA mortgage approvals jumped more-than-expected to a level of 40.12K in January, rising for the first time in 4 months. In the previous month, mortgage approvals had recorded a revised reading of 36.09K, while investors had envisaged for an advance to a level of 37.00K.

In the Asian session, at GMT0400, the pair is trading at 1.3958, with the GBP trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.3901, and a fall through could take it to the next support level of 1.3843. The pair is expected to find its first resistance at 1.4043, and a rise through could take it to the next resistance level of 1.4127.

Moving ahead, investors would eye UK's GfK consumer confidence index for February, set to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.