Sample Category Title

Canadian Dollar Edges Higher, US Housing Report Next

The Canadian dollar has recorded slight gains in the Monday session. Currently, USD/CAD is trading at 1.2663, up 0.22% on the day. On the release front, it's a quiet start to the week. There are no Canadian releases on the schedule. The US releases New Home Sales, which is expected to jump to 655 thousand. On Tuesday, Canada releases the annual budget. The US will release durable goods and consumer confidence reports. As well, Federal Chair Jerome Powell will testify before the House Financial Services Committee.

Canada releases its annual budget on Tuesday. In October, the Trudeau government revised downwards the deficit for the 2017-2018 fiscal year to C$19.9 billion. The Canadian economy was steady in the fourth quarter, so the deficit could be even lower. The budget is not expected to show any major spending, so it's likely that the release will not shake up the Canadian dollar. The Canadian currency lost ground last week, and touched its lowest level since late December.

Jerome Powell took over from Janet Yellen earlier this month, and will be on center stage this week, when he testifies before the House of Representatives and the Senate. After the recent stock markets volatility, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.53; (P) 106.83; (R1) 107.15; More...

Outlook in USD/JPY is unchanged and intraday bias remains neutral. Outlook also remains bearish with 108.27 resistance intact. On the downside, break of 105.54 will extend the larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 108.27 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

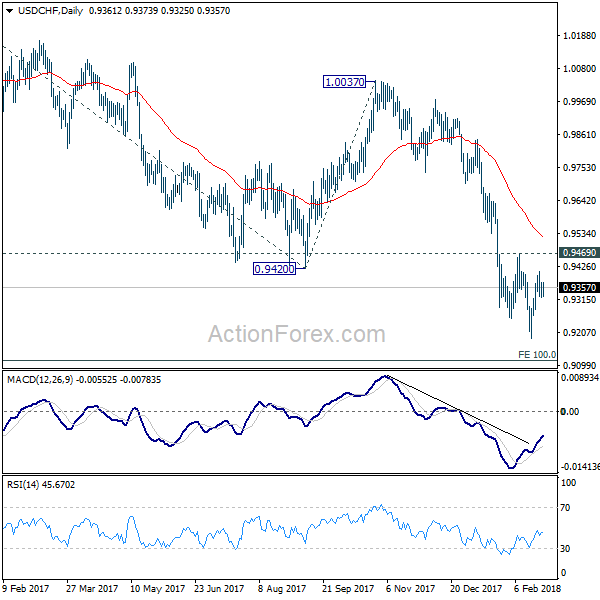

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9325; (P) 0.9349; (R1) 0.9379; More...

Outlook in USD/CHF is unchanged and intraday bias remains neutral. With 0.9469 resistance intact, deeper fall is still expected. On the downside, break of 0.9186 will extend the larger down trend to 0.9115 medium term projection level next. However, considering bullish convergence condition in 4 hour MACD, break of 0.9469 will indicate near term reversal and turn outlook bullish for 55 day EMA (now at 0.9520) and above.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

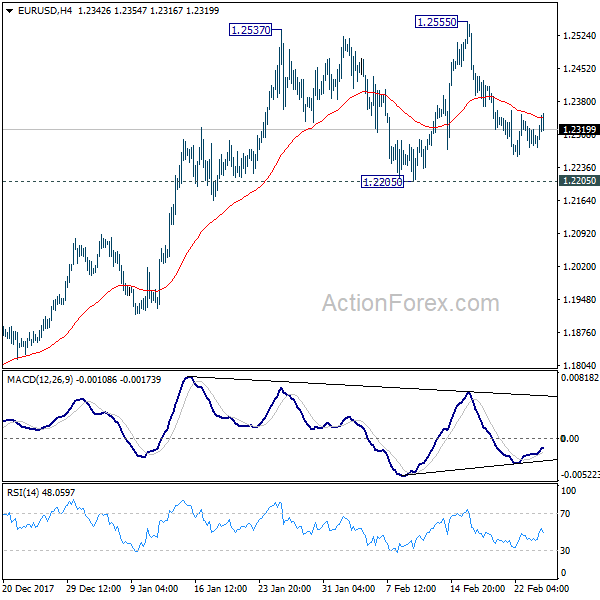

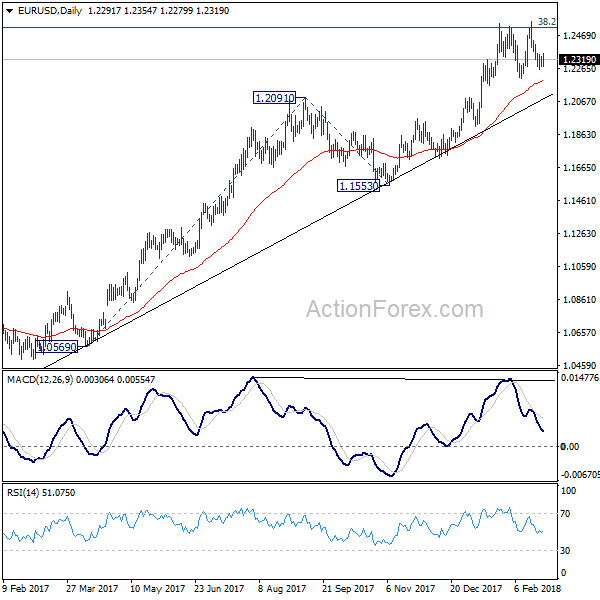

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2269; (P) 1.2303 (R1) 1.2327; More....

No change in EUR/USD's outlook and intraday bias remains neutral. On the upside, break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2205 will confirm rejection by 1.2516 key fibonacci level and trend reversal.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

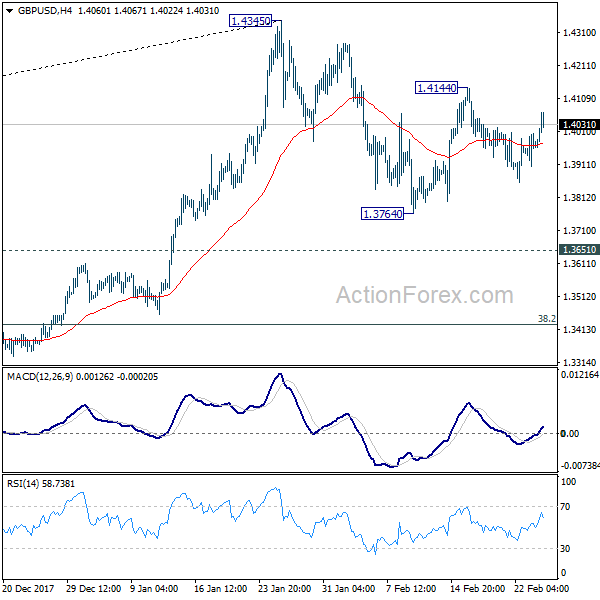

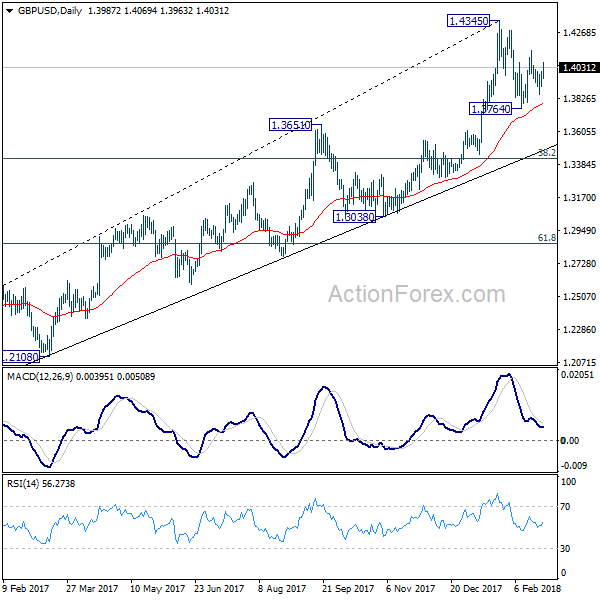

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3912; (P) 1.3958; (R1) 1.4014; More....

GBP/USD rebounds today but upside is limited below 1.4144 minor resistance. Intraday bias neutral first. On the upside, break of 1.4144 will extend the rise from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5056). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Dollar and Loonie Soft as Markets Tread Water

The forex markets are, generally speaking, rather quiet today. Dollar remains generally soft but no follow through selling is seen against it. Indeed, the greenback is trading mildly higher in the last few hours as consolidative trading extends. Canadian Dollar is the weakest one as weighed down by uncertainties over NAFTA renegotiations. Sterling takes over from Aussie and Kiwi as the strongest one for today but it's also bounded in recent range. The markets may continue to tread water until the batch of economic data and Fed Chair Jerome Powell's testimony tomorrow.

Merkel named cabinet ministers before coalition vote

German Chancellor Angela Merkel's Christian Democrats are set to meet to approve the coalition with the Social Democrats today. Ahead of the party conference, Merkel also announced her choice of six cabinet ministers. Merkel said that "it was my task to present a tableau of people that is future-oriented and that offers a good mix of experience and new faces." One particular member is Jens Spahn as health minister. The 37 year old Spahn is seen as an open critic who is viewed as Merkel's answer to the rise of the far right Alternative for Germany. Meanwhile, the SPD members are voting for the grand coalition too and results will be know on March 4.

UK Labour leader Corbyn backs customs union after Brexit

UK Prime Minister Theresa May is set to have a high profile speech this Friday regarding post Brexit relationship with EU. Her rival Labour leader Jeremy Corbyn expressed his backing of customs union member during the two year transition period. Corbyn said that "labour would seek a final deal that gives full access to European markets and maintains the benefits of the single market and the customs union... with no new impediments to trade and no reduction in rights, standards and protections."

He added that "we have long argued that a customs union is a viable option for the final deal. So Labour would seek to negotiate a new comprehensive UK-EU customs union to ensure that there are no tariffs with Europe and to help avoid any need for a hard border in Northern Ireland."

BoJ Kuroda dismissed review on policy framework

BoJ Governor Haruhiko Kuroda, recently reappointed for another five year term, dismissed the request by an opposition lawmaker to review the policy framework. Kuroda told the parliament that "it's unfortunate that achievement of our price target has been delayed. But thanks to the effect of our powerful monetary easing, Japan's economy is no longer in a state that can be described as deflation." He also pointed to recovery in the economy and said "things are proceeding smoothly". And therefore, "I don't have any plan at this stage to conduct another comprehensive review."

Fed Powell's testimony unlikely to deviate from the monetary policy report

New Fed chair Jerome Powell's testimony will be a major focus in the week ahead. As a prelude, Fed released its semi annual Monetary Policy Report last Friday. The report noted that "with inflation having persistently run below the 2% longer-run objective the Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal". It appears that similar reference had not been revealed in previous FOMC statement or minutes.

The Fed also warned of the elevated valuation of asset prices. As suggested in the report, "valuation pressures continue to be elevated across a range of asset classes even after taking into account the current level of Treasury yields and the expectation that the reduction in corporate tax rates should generate an increase in after-tax earnings. Leverage in the nonfinancial business sector has remained high, and net issuance of risky debt has climbed in recent months".

Powell's message in the testimony will likely not deviate much from the report regarding monetary policy. He's expected to reiterate the gradual path of monetary policy normalization. Yet, his comments about the growth outlook in light of the tax reform plan would be closely watched.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3912; (P) 1.3958; (R1) 1.4014; More....

GBP/USD rebounds today but upside is limited below 1.4144 minor resistance. Intraday bias neutral first. On the upside, break of 1.4144 will extend the rise from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5056). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:30 | GBP | BBA Loans for House Purchase Jan | 40.1K | 37.2K | 36.1K | |

| 15:00 | USD | New Home Sales Jan | 646K | 625K |

Dollar Broadly Weaker ahead of Powell’s Testimony; Stoxx 600 Hits 3-Week High

Here are the latest developments in global markets:

FOREX: The dollar remained broadly weaker against a basket of currencies, with markets eagerly awaiting Jerome's Powell congressional testimony for positioning on the US currency moving forward. Euro/dollar was 0.3% up and pound/dollar traded higher by 0.5%, hitting a 10-day high of 1.4069 earlier on Monday. Sterling was supported by hawkish-perceived comments by BoE Deputy Governor Dave Ramsden over the weekend, as well as the Labour party's support for a customs union after Brexit. Meanwhile, dollar/yen was 0.1% down at 106.76. this compares to a one-week low of 106.36 recorded earlier in the day. The decline in US Treasury yields contributed to dollar weakness.

STOCKS: Bullish sentiment from Asian markets reverberated into Europe, with equities trading broadly in the green in the old continent. At 1213 GMT, the pan-European Stoxx 600 was up by 0.5%, recording a three-week high of 384.13 earlier on Monday, while the blue-chip Euro Stoxx 50 traded higher by a similar proportion. The UK's FTSE 100, German Dax and French CAC 40 were up by 0.5%, 0.25% and 0.5% respectively. Companies continue to release quarterly earnings reports, though the markets' attention seems to be increasingly turning to central bankers and politics. ECB President Mario Draghi will be speaking to the European Parliament's ECON committee at 1400 GMT, while - and likely more importantly - the new Fed chief Jerome Powell will be giving his first testimony before Congress on Tuesday at 1500 GMT. Powell's comments will be closely watched as they come at a time of increasing equity market volatility. In politics, Brexit developments, the Italian elections and the outcome of the German SPD's vote on whether to re-enter a coalition with Chancellor Merkel's conservatives are on the agenda as the week unfolds. Lastly, futures markets were pointing to a higher open on Wall Street; contracts on the Dow, S&P 500 and Nasdaq 100 were trading higher by 0.6%, 0.4% and 0.3% respectively.

COMMODITIES: WTI and Brent crude retreated after both reaching near three-week highs of $63.90 and $67.58 per barrel respectively. Despite the fall, both benchmarks traded not far below the aforementioned levels. Gold was 0.7% higher at around $1,338 per ounce. The dollar-denominated metal was benefitting on the back of a broadly weaker greenback and potentially the uncertainty ahead of key political and central banking developments.

Day ahead: US new home sales and New Zealand trade data due

The economic calendar is light on Monday, with some data out of the US and New Zealand attracting attention.

US new home sales for the month of January will be made public at 1500 GMT. Sales are expected to increase by 3.2% after declining by 9.3% m/m in December, this constituting their largest drop in around 1½ years. It should be mentioned though that December's fall was likely attributed to a fading out of the boost in sales from the replacement of flood-damaged houses in parts of the US hit by the hurricanes.

New Zealand trade data - on January's imports and exports - are scheduled for release at 2145 GMT. Kiwi/dollar last traded 0.5% higher at 0.7325. It would be interesting to see if the figures lend additional support to the pair.

DAX Higher As Investors Optimistic Ahead Of Draghi, Powell Testimony

The DAX index has posted gains to kick off the week. Currently, the index is trading at 12,533.00, up 0.40% since the Friday close. On the release front, it’s a light day, with no data releases. The markets will be all ears as ECB President Mario Draghi testifies before the European Parliament Economic and Monetary Affairs Committee. On Tuesday, Germany releases Preliminary CPI and the head of the German central bank, Jens Weidmann will speak in Frankfurt. In the US, Federal Chair Jerome Powell will testify before the House Financial Services Committee.

On Thursday, the ECB released the minutes of its January meeting. The markets were looking for some hints regarding future monetary policy, and policymakers indicated that they could re-examine the Bank’s monetary policy “early this year”. The ECB is keeping a close eye on inflation, which has been moving upwards. Still, with inflation below the ECB target of just below 2%, there is little talk about raising interest rates. Policymakers also indicated concern with exchange rates, a theme which has been addressed by Mario Draghi in recent weeks, given the appreciation of the euro – EUR/USD has climbed 2.8% since the start of the year. The minutes voiced “concerns about the recent volatility in the euro exchange rate, which represented a source of uncertainty that had to be monitored with respect to its implications for the medium-term outlook for price stability”. The euro has seen plenty of volatility in February, and currency volatility will likely be high on the agenda of the next policy meeting in March.

Jerome Powell will be on center stage this week, when he testifies before the House of Representatives and the Senate this week. After the recent stock markets volatility, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.

GBPUSD Now Strongly Bullish Above 1.4008

The British pound has continued to press higher against the U.S dollar during the European trading session, with price-action so far finding interim resistance around the 1.4060 technical region. The GBPUSD pair currently trades around the 1.4050 level, with the greenback under heavy selling pressure across board in early week trading. Moving into today's U.S trading session, the bullish sentiment behind the sterling recent rise is likely to remain intact whilst price-action holds above the key 1.4008 level.

The GBPUSD pair is strongly bullish whilst trading above the 1.4008 level, further upside towards 1.4079 and 1.4144 seems possible.

Should GBPUSD price-action move below the key 1.4008 level, a sharp decline towards the 1.3968 and 1.3938 levels appears likely.

Further USDJPY Losses Expected Below 106.60

The U.S dollar remains under heavy selling pressure against the Japanese yen on Monday, as the U.S dollar index again failed to find buying interest above the key 90.00 technical level. The USDJPY pair currently trades around the 106.60 support level, with bearish selling momentum set to increase below this key area. Moving into today's U.S trading session, financial markets are likely to focus on the release of monthly U.S New Sales data and a key speech from Fed member Bullard.

The USDJPY pair remains strongly bearish while trading below the 106.60 level, further losses towards the 106.18 and 105.90 levels appear likely.

Should price-action on the USDJPY pair move above the key 106.60 level for a sustained period, buyers may test towards 107.00 and 107.30 resistance areas.