Sample Category Title

EUR/CHF Showing Signs Of Weakness

EUR/CHF declines following recovery slow down. The pair approaches hourly support given at 1.1487 (12/02/2018 low) while hourly resistance at 1.162 (07/02/2018 high) is maintained. The technical structure suggests further short-term downside moves.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support can be found at 1.0234 (20/04/2015 low).

EUR/GBP Declining

EUR/GBP loses ground, and slowly approaches hourly support at 0.8774 (11/12/2017 low). Hourly resistance at 0.8846 (12/12/2017 high) is distanced. The technical structure suggests further short-term downward moves.

In the long-term, the pair has largely recovered from 2015 lows. The technical structure suggests further upside pressure. Strong resistance can be found at 0.9500 (psychological level) while support remains at 0.8304 (05/12/2016 low). The pair is trading below its 200 DMA.

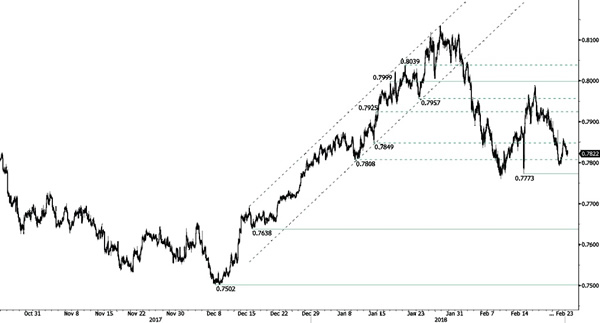

AUD/USD Downward Consolidation

AUD/USD recovery loses steam and approaches hourly support at 0.7773 (14/02/2018 low). Hourly resistance is maintained at 0.7999 (17/01/2018 high). The short-term technical structure suggests further downside moves.

In the long-term, the upward trend slows down after failing to reach key resistance at 0.8164 (14/05/2015 low). Key support stands at 0.6009 (31/10/2008 low). A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Bullish Trend Maintained

USD/CAD increases further after breaking hourly resistances at 1.2716 (04/12/2017 high) and 1.2748 (24/11/2017 high), recovering from December downward pattern. New hourly resistance is given at 1.2796 (25/12/2017 high) while hourly support is maintained at 1.2466 (15/02/2018 low). The technical structure indicates that continued rise is expected in the short-term.

In the longer term, the pair is trading between resistance point at 1.3805 (05/05/2017 high) and support at 1.2128 (18/06/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head lower. The pairs is trading above its 200 DMA.

USD/CHF Pushing Higher

USD/CHF ended its short-term downward trend, heading for further rise along 0.94. Hourly resistance stands at 0.9470 (08/02/2018 high) while hourly support remains at 0.9188 (16/02/2018 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support lies at 0.9072 (07/05/2015 low) while resistance at 1.0344 (15/12/2016 high) is distanced. The technical structure favours a long term bullish bias since the unpeg in January 2015.

USD/JPY Further Weakness

USD/JPY upward trend stops as bearish pattern resumes. Hourly support and resistance are given at 105.55 (16/02/2018) and 109.09 (31/01/2018 high). The technical structure suggests short-term downside moves.

We favor a long-term bearish bias. Support at 105.55 (03/05/2016 low) is almost reached. A gradual rise toward the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 101.20 (09/11/2016 low).

GBP/USD Edging Higher

GBP/USD is approaching the 1.40 range, still a long way to go before reaching hourly resistance at 1.4151 (05/02/2018). Hourly resistance is given at 1.3742 (16/01/2018 low). The technical structure suggests further short-term upside move.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Weak Recovery

EUR/USD is losing back its recovery gains from yesterday and is heading downward. Hourly support and resistance are maintained at 1.2165 (17/01/2018 low) and 1.2434 (06/02/2018 high). The technical structure suggests further downside moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Market Update – European Session: German Q4 GDP And Euro Zone Final Jan CPI Come In Unrevised

Notes/Observations

Euro Zone Jan CPI unrevised but still a distance from target

Germany Q4 Final GDP unrevised

Sweden Central Bank (Riksbank) Feb Minutes deemed dovish given recent disappointment with CPI data

UK PM May said to be getting her senior Cabinet ministers on board over the Govt’s approach to Brexit

Asia:

Japan Jan National CPI annual reading hits its Highest level since March 2015 (Y/Y: 1.4% v 1.3%e) while Core CPI Ex-Fresh Food) rose for the 13th straight month (Y/Y: 0.9% v 0.8%e,)

Japan Finance Min Aso stated that he wanted to raise nationwide sales tax as scheduled in Oct 2019; Reiterates important for BoJ to maintain current policy framework

China Communist Party said to be holding key meeting in coming days (**Note: National People Congress (NPC) to meet on March 5th. where the Chinese govt official releases its forecasts on growth and inflation for the year ahead)

Europe:

ECB's Smets (Belgium): Has full confidence ECB will reach inflation goal; Euro strength and volatility is not yet a concern

Labour Party (opposition) said to be planning a major policy announcement regarding the Customs Union on Monday, Feb 26th. Labour leader Corbyn might not necessarily going to back the customs union as it is, but a very close copy of it

Americas:

Fed's Kaplan (non-voter, dove) stated that still believed three 2018 hikes is a good base case but had not seen tight labor market fan wage growth yet

Fed's Bostic (2018 voter, dove): Fed was carefully calibrating a return to more normal policy

Economic Data:

(DE) Germany Q4 Final GDP Q/Q: 0.6% v 0.6%e; Y/Y: 2.9% v 2.9%e; GDP NSA Y/Y: 2.3% v 2.3%e

(DE) Germany Q4 Private Consumption Q/Q: 0.0% v 0.1%e; Government Spending Q/Q: 0.5% v 0.4%e; Capital Investment Q/Q: 0.0% v 0.5%e; Construction Investment Q/Q: -0.4% v -0.2%e; Domestic Demand Q/Q: 0.1% v 0.2%e; Exports Q/Q: 2.7% v 2.2%e; Imports Y/Y: 2.0% v 1.4%e

(DK) Denmark Jan Retail Sales M/M: -0.2% v -0.3% prior; Y/Y: 1.6% v 1.1% prior

(AT) Austria Jan CPI M/M: -0.7% v +0.4% prior; Y/Y: 1.8% v 2.2% prior

(ES) Spain Jan PPI M/M: 0.2 v 0.2% prior; Y/Y: 0.1% v 1.7% prior

(TW) Taiwan Q4 Current Account: $26.6B v $22.1prior

(PL) Poland Jan Unemployment Rate: 6.9% v 6.9%e

(PL) Poland Q4 Unemployment Rate: 4.5% v 4.4%e

(EU) Euro Zone Jan Final CPI Y/Y: 1.3% v 1.3%e; CPI Core Y/Y: 1.0% v 1.0%e, CPI M/M: -0.9% v -0.9%e

Fixed Income Issuance:

(ZA) South Africa sold total ZAR900M vs. ZAR900M indicated in I/L 2029, 2033 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 380.4, FTSE -0.2% at 7238, DAX +0.1% at 12470, CAC-40 flat at 5310 , IBEX-35 -0.2% at 9858, FTSE MIB +0.4% at 22541 , SMI -0.6% at 8917, S&P 500 Futures +0.3%]

Market Focal Points/Key Themes: European Indices trade mixed this morning with strength in the Italian MIB offset by weakness in the Spanish Ibex and FTSE. This follows on from a mixed Wallstreet session overnight and positive futures this morning. Banking name Royal Bank of Scotland reported results positing a full year profit for the first time in 10 years, however fears of upcoming fines sees shares off over 4%. Else IAG trades lower after results, with Valeo in France trading sharply lower after missing estimates. To the upside Pearson, Swiss Re and Standard Life Aberdeen trades higher following results. Phoenix Group trades higher after acquiring the insurance unit from Standard Life Aberdeen in a £3B+ transaction. Looking ahead notable earners include Huntsman, Entergy and RBC.

Movers

Consumer Discretionary [Pearson [PSON.UK[ +3.7% (Earnings), IAG [IAG.UK] -4.5% (Earnings)]

Industrials [Valeo [FR.FR] -9.3% (Earnings)]

Financial [ Rightmove [RMV.UK] +1.7% (Earnings), Swiss Re [SREN.CH] +2.7% (Earnings), RBS [RBS.UK] -4.5% (Earnings), Standard Life Aberdeen [SLA.UK] +2.4% (Earnings, sells insurance unit), Phoenix [PHNX.UK] +5.3% (Acquisition)]

Speakers

Sweden Central Bank (Riksbank) Feb Minutes: Saw slow rate hikes in H2 of 2018; to pay attention to downside risks on inflation

Riksbank Gov Ingves: Economic development abroad remained strong while global inflationary pressures were moderate

Riksbank Dep Gov Ohlsson (dissenter): Time to begin normalizing policy. Unemployment might not be cut using demand side policies

Riksbank Dep Gov Skingsley: Some concern for inflation pressures going forward; situation calls for caution on the start of rate hikes

Riksbank Jansson: Current picture for inflation remained bright with Oct meeting seen reasonable conditions for a rate hike

UK Health Min Hunt: Divergent views with Cabinet on Brexit. UK would keep EU rules on a voluntary basis and reject staying within Customs Union

Catalan official Puigdemont said to propose that Sanchez be the Regional President

Currencies

The GBP/USD was firmer but holding below the 1.40 level as reports circulated that UK PM May got her senior Cabinet ministers on board over the Govt’s approach to Brexit and ask for an ambitious trade deal with the EU.

EUR/USD steady just above the 1.23 handle and well contained within recent ranges. No surprises in the session from data as both German Q4 GDP and Euro Zone jan inflation data were unrevised.

The SEK currency was softer in the session as dealers felt the Riksbank Feb minutes were on the softer side with concerns lingering over inflation and the exchange rate given the recent negative surprise with Jan CPI data. EUR/SEK hit its highest level since Nov 2016 as the cross tested above 10.06 in the aftermath of the monutes

Fixed Income

Bund Futures trades up 47 ticks at 159.15 as Bund futures jump in large volumes after breaking key threshold. Upside targets 159.75, while a return lower targets the157.75 level.

Gilt futures trade at 121.80 up 16 ticks as Gilts remained capped by the 122.00 handle. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.00-122.25 zone then 122.85.

Friday's liquidity report showed Thursday's excess liquidity rose to €1.831T from €1.827T prior. Use of the marginal lending facility fell to €0 from €119M prior.

Corporate issuance saw equity fund inflows of $1.1B in w/e Feb 21st vs outflows of $4.6B in w/e Feb 14th

Looking Ahead

(EU) EU leaders meet in Brussels

06:00 (BR) Brazil Feb FGV Construction Costs M/M: 0.2%e v 0.3% prior

06:00 (BR) Brazil Feb FGV Consumer Confidence: No est v 88.8 prior

06:00 (UK) DMO to sell combined £3.0B in 1-month, 3-month and 6-month Bills (£0.5, £0.5B and £2.0B respectively)

06:30 (IS) Iceland to sell Bonds - 06:30 (IN) India Weekly Forex Reserves

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Mid-Feb IBGE Inflation IPCA-15 M/M: 0.4%e v 0.4% prior; Y/Y: 2.9%e v 3.0% prior

07:00 (CL) Chile Jan PPI M/M: No est v 0.4% prior

07:00 (UK) BOE’s Ramsden

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond auction (held on Thurs)

08:15 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Jan CPI M/M: +0.5%e v -0.4% prior; Y/Y: 1.5%e v 1.9% prior

08:30 (CA) Canada Jan CPI Core- Common Y/Y: 1.7%e v 1.6% prior, CPI Core- Trim Y/Y: No est v 1.9% prior, CPI Core- Median Y/Y: No est v 1.9% prior, Consumer Price Index: 131.5e v 130.8 prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (MX) Mexico Q4 Final GDP Q/Q: 1.0%e v 1.0% prelim; Y/Y: 1.8%e v 1.8% prelim; Nominal GDP Y/Y: 7.8%e v 7.1% prior; Overall 2017 GDP YU/Y: No est v 2.3% prior

09:00 (MX) Mexico Dec Economic Activity Index (Monthly GDP) Y/Y: 1.8%e v 1.5% prior

10:15 (US) Fed's Dudley (dove, FOMC voter): with Rosengren (non-voter) on panel

11:00 (US) Fed releases 2018 Monetary Policy Report to Congress

11:00 (EU) Potential Sovereign ratings after European close (Russia Sovereign Debt to be rated by Fitch; Russia and Turkey Sovereign Debt to be rated by S&P

(IQ) Iraq Sovereign Debt to be rated by S&P

13:00 (US) Weekly Baker Hughes Rig Count data - 13:30 (FR) ECB’s Coeure (France) on panel in NY

15:00 (CO) Colombia Central Bank Monetary Policy Meeting

15:40 (US) Fed's Williams (moderate, voter) speaks on Outlook for US Economy

DAX Edges Lower As German GDP Slows In Q4

The DAX index has posted slight losses in the Friday session. Currently, the index is trading at 12,437.00, down 0.20% on the day. On the release front, German Final GDP dipped to 0.6% for the fourth quarter, matching the estimate. The markets also correctly predicted eurozone inflation reports, as Final CPI and Final Core CPI came in at 1.3% and 1.0%, respectively.

This week's German and eurozone indicators have pointed downwards, weighing on the DAX. The index is enduring a dismal February, shedding 6.0% of its value this month. German GDP and Eurozone CPI managed to match their estimates, but lost ground compared to the previous releases. The well-respected ZEW economic sentiment reports dropped in February in Germany and the eurozone, although both indicators managed to beat their estimates. Eurozone consumer confidence remains weak, and the indicator dipped to zero, shy of the forecast of 1 point. On the manufacturing front, eurozone and German PMIs both fell in February and missed the forecasts. At the same time, both releases pointed to strong expansion, a reflection of strong global demand for European products, which has boosted the eurozone manufacturing and export sectors.

The Federal Reserve did not raise rates in January, but the minutes of that policy meeting were highly anticipated, with investors looking for clues regarding upcoming rate hikes. Although the policymakers did not discuss a quicker pace of rate hikes, the minutes hinted that further rate hikes could be in the cards, due to strong economic conditions in the US. In the words of the minutes, policymakers “anticipated that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labor market conditions would strengthen further”. At the December meeting, the Fed penciled in three rate hikes in 2018, but there is growing sentiment in the markets that the Fed may have to raise rates four or even five times this year. As for inflation, the minutes did not reveal any concern, with most Fed members were of the opinion that inflation would rise towards the Fed target of 2 percent. Global investors, however, seem much more concerned about US inflation levels, as worries that higher inflation would trigger more interest rate hike precipitated the recent stock market correction, which wiped off some $4 trillion in valuations.