Sample Category Title

USD/RUB 4H Chart: Likely Breakout

The US Dollar has started to gain strength against the Russian Ruble after the pair reached a five-years' low of 55.58. However, the surge was stopped by the weekly R2 at 58.62.

After reaching the 38.20% Fibonacci retracement level, the exchange rate made a U-turn south and has since been trading in that direction. A new junior pattern has been drawn to monitor the price movement. This retracement can be measured by connecting the low at 55.58 and the high at 60.43.

The currency pair has moved closer to the border of the junior pattern, as can be observed on the chart. Also, technical indicators suggest a breakout of the lower boundary is likely to occur during the next trading sessions.

CAD/CHF 4H Chart: Bearish Movement

The Canadian Dollar has been trading in a descending channel against the Swiss Franc since early January. During this period of decline, the currency pair has reached an eight-months low level of 0.7337.

The inability for the Loonie to make a new move upwards suggests that it might continue to fall. The CAD/CHF pair has reached the weekly S1 at 0.7344. If this support holds, there might be a brief retracement south to test the upper boundary.

Technical indicators flash bearish signals. This indicates bears' dominance over the exchange rate is likely to grow stronger during the following trading sessions.

USD/CAD: Canadian Core Retail Sales

Following the release of the Canadian core retail sales data, the Loonie showed a moderate post-reaction against the Greenback. USD/CAD jumped 40 base points, or 0.32%, reaching the intraday high of 1.2742.

Canada's core retail sales dropped by 1.8% in December, following the upwardly-revised 1.7% increase in the prior month. Statistics Canada stated that headline retail sales dropped 0.8% in the reported period, going against what economists had anticipated. Despite the fact that motor vehicle and parts dealers and food and beverage stores recorded gains, sales at general merchandise,health and personal care and electronics and appliance stores had low enough turnover for the general volume of sales to go down.

GBP/USD: UK Second Estimate GDP

The Sterling was seen weaker against the US Dollar after the UK GDP growth report came in on Thursday. The GBP/USD currency pair lost 13 base points, or 0.09%, to 1.3878 to continue fluctuating whileafter.

The UK Office for National Statistics said that the second estimate for Britain's GDP growth in the final quarter of 2017 reflected a short downward revision from the first estimate, falling to the 0.4% quarterly growth pace. However, business investment growth remained stand-still, expansion in business services and finance within the services sector was the largest contributor to the increase of the UK's GDP. In annual terms, the UK economy grew 1.7%, slightly lower than expected.

Market Sentiment Skittish But Dollar Edges Up

Fears revolving around rising inflationary pressures and rate hike jitters have certainly left investors skittish this trading week. Investors seem to be on edge about higher interest rates and as such, this continues to encourage global equity bulls and bears to engage in a tough tug of war.

Interestingly, Asian stocks ventured higher during early trading on Friday, after Wall Street bounced higher overnight from a two-day losing streak. European shares are set to open on a positive note, tracking gains from Asia this morning. While the bullish domino effect from Asia and Europe could support Wall Street this afternoon, it remains uncertain if such momentum will roll over into the new trading week.

With investors on guard as global stock markets become increasingly sensitive to the prospect of rising inflation and interest rates, equity bears could steal the show.

Dollar supported by rate hike expectations

The story defining the Dollar’s impressive appreciation this week continues to revolve around heightened speculations of higher US interest rates in 2018.

With January’s hawkish FOMC meeting minutes reinforcing expectations of an interest rate increase in March and of more rate hikes ahead, the Dollar could remain supported. Much attention will be focused on the speeches of three FOMC members this afternoon, which could offer fresh insight on rate hike timings. The Dollar could receive a boost this afternoon if Fed speakers adopt a hawkish tone and give signs of a fourth rate hike being on the cards in 2018.

From a technical standpoint, the Dollar Index remains under pressure below the 90.55 lower high. For bulls to be truly back in the game, prices need to break above 90.20 and 90.55, respectively. A failure to break above 90.20 could result in a decline back towards 89.60. Sustained weakness below the 89.60 has the ability to trigger a decline lower to 89.00.

Commodity spotlight – Gold

An appreciating US Dollar has punished Gold significantly this week, with the yellow metal currently trading around $1329 during early trading on Friday.

It is becoming clear that the prospect of higher US interest rates has soured appetite for Gold which is zero-yielding. With the Dollar likely to continue finding supporting rate hike talks, the yellow metal may be exposed to further pain moving forward. Focusing on the technical outlook, this has certainly been a bearish trading week for Gold, with prices struggling to keep above $1324.15. A breakdown below this level could encourage a decline lower towards $1310 and $1300, respectively. Alternatively, bulls have a chance to challenge $1340 if an intraday breakout above $1332 is achieved.

Bitcoin dips below $10,000

Bitcoin dipped below the psychological $10,000 level during Thursday’s trading session, with extended losses towards $9,600 during early trading on Friday.

Although the cryptocurrency has staged a recovery back towards $10,000 as of writing, the price action witnessed this week suggests that bulls are exhausted. Sustained weakness below $10,000 could spark discussions over the recent rebound being nothing more than a dead cat bounce.

Technical Outlook: AUDUSD Returns To Daily Cloud After Recovery Rejection, Near-Term Bias Remains Bearish

The pair turned to red on Friday and is back into daily cloud after failing to capitalize from Thursday’s rally and marginal close above cloud top.

Near-term focus shifts lower again, supported by bearish setup of daily MA’s (10,20,30) and negative momentum studies.

Close within daily cloud will be bearish signal for final push towards key supports at 0.7773 (converged 100/200SMA’s) and 0.7758 (09 Feb low).

The pair is also on track for bearish weekly close which would add on existing negative outlook.

To neutralize immediate downside risk, close above 10SMA (0.7875) is needed.

Res: 0.7847, 0.7875, 0.7906, 0.7940

Sup: 0.7813, 0.7790, 0.7773, 0.7758

USD Better Bid Ahead Of The Weekend

USD gets stronger as fears ease

After taking a breather on Thursday, the US dollar extended gains Friday amid easing rate concerns. US treasuries were better bid, which sent yields lower. The 10-year fell 3bps to 2.90%, while on the short-end of the curve the 2-year one was unchanged around 2.245%. Since the beginning of the week, the buck has extended gains higher against all G10 currencies, making the biggest gains against the Swedish krona (+2.25%), the Norwegian krone (+1.30%) and high quality commodity currencies such as the Canadian, New Zealand and Australian dollar (+1.20%, +1.10% and +1%, respectively).

With the exception of the publication of the January FOMC minutes on Wednesday, which didn’t really bring new information, it was a quiet week. However, several Fed members will have the opportunity to expose their view on the US economy and monetary policy today. Dudley and Rosengren will speak on Fed Balance Sheet, while Williams will speak on the US economic outlook. The three of them are voting members, so their opinion matters.

Next week will be busier in terms of economic data will the publication of January new home sales on Monday, wholesale inventories, durable goods orders for January on Tuesday, an update of Q4 personal consumption and GDP growth on Wednesday and personal income and spending as well as PCE for January on Thursday. The latter is by far the most anticipated report. Indeed, over the last few weeks market participants were quite nervous about a potential acceleration of inflation, since it could force the Fed to accelerate tightening, which could ultimately cap economic growth.

EUR/USD has stabilised around 1.2110 as selling pressure may have lessen for now. The currency pair is right in the middle of its monthly range (1.2165-1.2555), while the RSI has return at 50. We do not expect much movement today; however, this evening speeches from Fed members could trigger sharp movement, especially should they hawkish/dovish comments about the current situation.

Asian markets head higher on Friday

Asian markets were heading higher on Friday, led by South Korean Kospi, surging at 2’451 (+1.54%), followed by Hong Kong Hang Seng valued at 31’290 (+1.05%) and Japanese Topix increasing at 1’760 (+0.82%) while Nikkei 225 closed the day at 21’893 (+0.72%), supported by Energy (+2.98%), Real Estate (+1.84%), Materials (+1.50%) and Utilities (+1.35%) due to higher oil-related stocks performance after oil price overnight gains (JXTG Holding +3.64%, Showa Shell Sekiyu +2.88% and Inpex +2.39%).

On economic data side Japan’s January Core Consumer Price Index Y/Y rose by 0.90% (consensus: 0.80% - M/M basis: 0.10%), in line with previous month and confirming the view of a rather slow headline inflation rate.

US treasury yields decrease, as the 10-year and 2-year are given at 2.9080 (-1.55%) and 2.2420 (-1.07%), despite Fed’s minute on Wednesday that maintained the stance of improving economic conditions and confirming more rate hikes for the coming year. US Equities remained stable on Thursday: Dow Jones Industrial Average, S&P500 and Nasdaq were closing at 24’962 (+0.66%), 2’704 (+0.1) and 7’210 (-0.11%).

Euro Steady As German GDP, Eurozone CPI Match Forecasts

The euro has ticked lower in the Friday session. Currently the pair is trading at 1.2313, down 0.14% on the day. On the release front, German Final GDP dipped to 0.6% for the fourth quarter, matching the estimate. The markets also correctly predicted eurozone inflation reports, as Final CPI and Final Core CPI came in at 1.3% and 1.0%, respectively. In the US, there are no data releases, but we’ll hear from three FOMC members – William Dudley, Loretta Mester and John Williams. Traders should be prepared for possible movement if any of these policymakers weigh in on the Fed’s future monetary policy.

The Federal Reserve did not raise rates in January, but the minutes of that policy meeting were highly anticipated, with investors looking for clues regarding upcoming rate hikes. Although the policymakers did not discuss a quicker pace of rate hikes, the minutes hinted that further rate hikes could be in the cards, due to strong economic conditions in the US. In the words of the minutes, policymakers “anticipated that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labor market conditions would strengthen further”. At the December meeting, the Fed penciled in three rate hikes in 2018, but there is growing sentiment in the markets that the Fed may have to raise rates four or even five times this year. As for inflation, the minutes did not reveal any concern, with most Fed members were of the opinion that inflation would rise towards the Fed target of 2 percent. Global investors, however, seem much more concerned about US inflation levels, as worries that higher inflation would trigger more interest rate hike precipitated the recent stock market correction, which wiped off some $4 trillion in valuations.

This week’s German and eurozone indicators have pointed downwards, and the euro has responded with losses of close to 1% this week. The well-respected ZEW economic sentiment reports dropped in February in Germany and the eurozone, although both indicators managed to beat their estimates. Eurozone consumer confidence remains weak, and the indicator dipped to zero, shy of the forecast of 1 point. On the manufacturing front, eurozone and German PMIs both fell in February and missed the forecasts. At the same time, both releases pointed to strong expansion, a reflection of strong global demand for European products, which has boosted the eurozone manufacturing and export sectors.

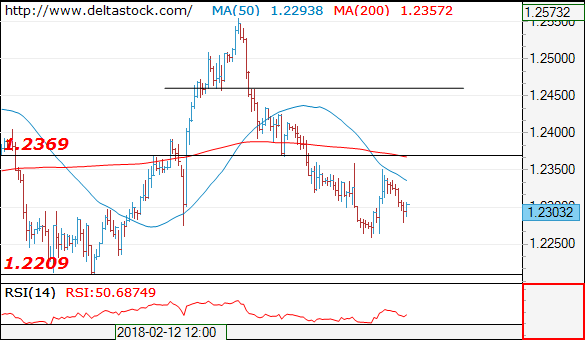

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2303

The violation of 1.2300 resistance imposes a risk of a more significant reversal and a break through 1.2370 crucial area will target 1.2460.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2370 | 1.2460 | 1.2260 | 1.2210 |

| 1.2460 | 1.2560 | 1.2210 | 1.2090 |

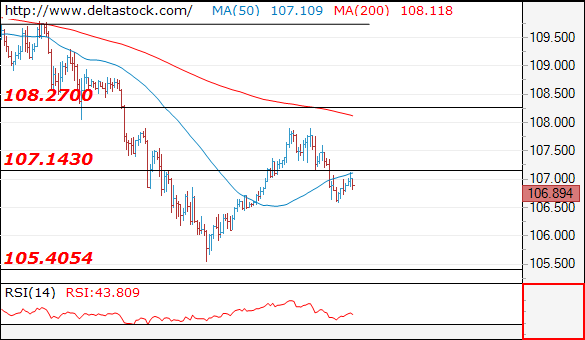

USD/JPY

Current level - 106.89

The bias remains bearish, for a slide towards 105.40 lows. Initial resistance lies at 107.15.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.15 | 108.30 | 106.40 | 105.40 |

| 108.30 | 110.40 | 105.40 | 102.40 |

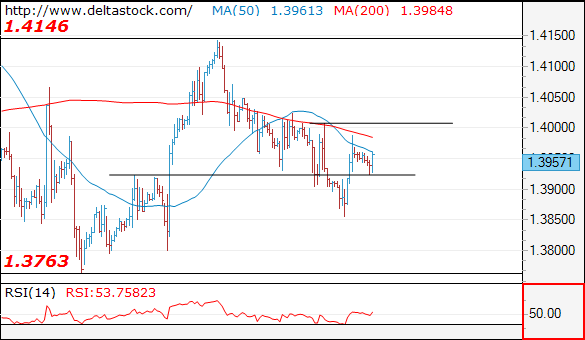

GBP/USD

Current level - 1.3957

The reversal at 1.3850 has initiated a break through 1.3920 and the bias is positive, for a rise through 1.4010 crucial high, towards 1.4150.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4010 | 1.4280 | 1.3920 | 1.3760 |

| 1.4150 | 1.4340 | 1.3850 | 1.3620 |

Technical Outlook: USDJPY – Near-Term Bias Turns Negative After Thursday’s Fall

The pair is consolidating on Friday after suffering heavy losses previous day. Near-term action is holding below 107 handle (broken Fibo 38.2% of 105.54/107.90 upleg, reinforced by falling 10SMA) for now and maintains downside pressure, following repeated failure under technical / psychological barrier at 108.00 (50% of 110.48/105.54 bear-leg) and subsequent strong bearish acceleration.

Underlying bear-trend received fresh negative signal on Thursday's fall which turned near-term bias to bearish mode.

Near-term action is weighed by Thursday's long red candle, keeping focus at next pivotal support at 106.44 (Fibo 61.8%) break of which would confirm lower top and open way towards key near-term support at 105.54 (2018 low, posted on 16 Feb).

Alternative scenario requires close above 108 barrier to sideline near-term bears.

Res: 107.00, 107.34, 107.66, 107.90

Sup: 106.59, 106.44, 106.10, 105.54