Sample Category Title

USD/JPY Trapped Within The Descending Channel

The USD/JPY has reached the upper part of a descending channel and we could see a rejection towards 106.40 M L4 level followed by 106.00. The POC zone is 107.00-20 and we might see a rejection from the zone. However, since it's Friday, we need to be wary of the profit taking. In that case ,buyers could possible get in control if W H4 107.75 breaks to the upside and the pair could target 108.13 followed by 108.50.

W H3 -Weekly Camarilla Pivot (Weekly Interim Resistance)

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

M H4 - Monthly Camarilla Pivot (Very Strong Monthly Resistance)

M L3 – Monthly Camarilla Pivot (Monthly Support)

M L4 – Monthly H4 Camarilla (Very Strong Monthly Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

EUR/USD Fails To Overcome 1.2350

Bulls managed to regain some of their lost positions on Thursday, as the pair bounced off the bottom boundary of the junior channel and tested the 1.2350 mark later in the day. The nearest resistance cluster formed by the 100-hour SMA and the 23.60% Fibo retracement proved to be an unbreakable barrier which sent the Euro for a slight decline.

Technical indicators demonstrate that the bullish sentiment should continue dominating in this session. However, the aforementioned resistance circa 1.2360, likewise reinforced by the 200-hour SMA, could put downward pressure on the rate once again, especially when no significant fundamentals are scheduled for today.

The Euro might even push lower just to reach the bottom boundary of the four-month channel near the 1.2250 mark.

GBP/USD Surrenders Near 1.40

Downside risks dominated USD/JPY on Thursday, as the pair closed the session with a 100-pip fall. Along the way, some significant support levels, such as the 55-, 100– and 200-hour SMAs, the monthly S1 and the weekly PP, were breached.

By Friday morning, the rate had returned near the 107.15 mark to re-test the longer-term moving averages. However, technical indicators flash strong sell signals, especially given the strength of the nearest resistance. Thus, traders might fail to see a test of the senior channel circa 107.50 today.

If looking at the nearest support, no southern barriers are restricting the pair until the 105.65 mark where the lowest point since November 2016 is located. In case bears prevail, the Greenback is unlikely to move below this level.

USD/JPY Strongly Bearish Today

Downside risks dominated USD/JPY on Thursday, as the pair closed the session with a 100-pip fall. Along the way, some significant support levels, such as the 55-, 100– and 200-hour SMAs, the monthly S1 and the weekly PP, were breached.

By Friday morning, the rate had returned near the 107.15 mark to re-test the longer-term moving averages. However, technical indicators flash strong sell signals, especially given the strength of the nearest resistance. Thus, traders might fail to see a test of the senior channel circa 107.50 today.

If looking at the nearest support, no southern barriers are restricting the pair until the 105.65 mark where the lowest point since November 2016 is located. In case bears prevail, the Greenback is unlikely to move below this level.

Gold Unlikely To Surpass 1,340.00

Following a test of the weekly S1 at 1,320.70, bulls took over the market and managed to push the yellow metal 0.8% higher within a couple of hours. The pair, however, stopped short of the expected daily high of 1.338.00, as the Asian session introduced some minor downward pressure.

By early Friday, Gold was testing the support of the 55-hour SMA circa 1,326.00. Even though technical indicators flash bullish signals in this session, the pair might fail to breach the massive resistance cluster formed by the 100– and 200-hour SMAs, the 23.60% Fibo and the monthly PP. Thus, this 1,340.00 might be the daily high for today.

In terms of support, the rate could halt near the weekly S1 at 1,320.00 and spend the day fluctuating between this level and the above 1,340.00 area.

Technical Outlook: GBPUSD – Fresh Rally Sidelines Downside Risk But Needs Close Above 1.40 To Confirm

Cable holds positive tone and rallies towards initial barrier at 1.3988 (30SMA/Thu high) after generating bullish signal on strong downside rejection at 1.3856 on Thursday.

Bullish acceleration in early European trading is forming reversal pattern on daily chart, confirmation of which requires lift and close above 1.40 barrier (20SMA /50% of 1.4144/1.3856 downleg).

Fresh bullish momentum is building (north-heading 14-d momentum is attempting to break into positive territory) and supports the notion, however, bulls need to clear 1.40 barrier to confirm scenario.

Broken 10SMA marks initial support at 1.3952, followed by session low at 1.3923 and 1.3900 support (50% of 1.3457/1.4344 rally) loss of which will generate bearish signal.

Res: 1.4000, 1.4034, 1.4049, 1.4076

Sup: 1.3952, 1.3923, 1.3900, 1.3856

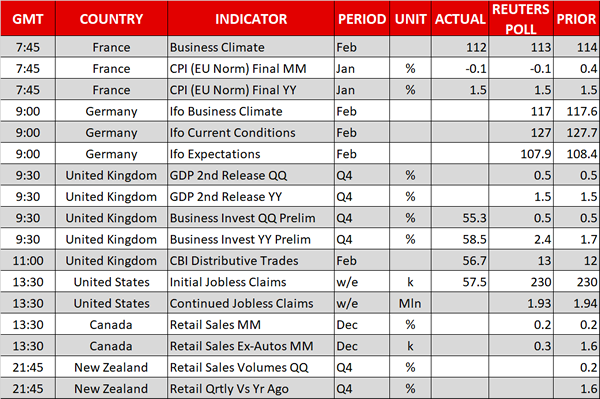

Dollar Looks To Fed Speakers For Direction, Eurozone And Canada Release Inflation Numbers

Here are the latest developments in global markets:

FOREX: The dollar index was nearly 0.4% higher on Friday, recouping some of the losses it posted earlier on Thursday. Kiwi/dollar was a notable mover as well, tumbling 0.6% despite stronger-than-expected data out of New Zealand overnight.

STOCKS: US markets were mixed on Thursday, providing yet another sign that investors' risk sentiment remains quite fragile still. The Dow Jones closed 0.7% higher, but the S&P 500 was barely in the green, rising a mere 0.1%, while the Nasdaq Composite fell 0.1%, recording its fourth straight day of declines, albeit the benchmark's losses were not sizable. That said, futures tracking the Dow, S&P, and Nasdaq 100 are all safely in positive territory at the moment, signaling that these indices may open higher today. In Asia, markets were a sea of green. Japan's Nikkei 225 and Topix closed up 0.7% and 0.8% respectively, while in Hong Kong, the Hang Seng was higher by 1.0%. Meanwhile in Europe, futures of all the major indices were flashing green.

COMMODITIES: In energy markets, oil prices were lower on Friday with both WTI and Brent crude declining 0.2%, giving back some of the gains they posted on Thursday after the weekly EIA inventory data showed a surprising drawdown in inventories. Today, oil traders will look to the release of the Baker Hughes oil rig count, in order to gauge whether the increase in US production continues unabated. In precious metals, gold was down almost 0.4%, last seen near the $1327 per ounce handle. Considering the absence of any major news lately on the geopolitical front to drive the yellow metal, its latest moves appear to be dictated solely by movements in the US dollar.

Major movers: Dollar whipsaws ahead of Fed speakers; ECB minutes pave the way for language shift

The US dollar climbed on Friday, regaining some of the ground it lost earlier on Thursday. Price action in the world's reserve currency has been particularly choppy ever since the FOMC minutes were released on Wednesday, something that may be a reflection of investors' indecisiveness regarding the outlook for US monetary policy. While the minutes were quite upbeat and heightened speculation that the Committee could deliver four quarter-point rate hikes this year, FOMC policymakers quickly stepped in to calm markets down yesterday.

St. Louis Fed President James Bullard (non-voter) pushed back against rate-hike expectations, noting that four hikes seem “like a lot” to him, and that for this to happen, “everything would have to go just right”. Although Bullard is a notorious dove on policy, other more neutral policymakers like Dallas Fed President Robert Kaplan (non-voter) also appeared quite cautious, indicating that his view of three hikes in 2018 could change, but only if economic data exceed his forecasts.

Without any major data on the US economic calendar today, the dollar will be looking for directional clues in the speeches of another four FOMC members, three of which hold voting rights this year. New York Fed President William Dudley (voter), Boston Fed President Eric Rosengren (non-voter), Cleveland Fed President Loretta Mester (voter) and San Francisco Fed President John Williams (voter) will all be delivering remarks. Investors will be looking for their outlook on policy in light of the latest acceleration in wages, as they try to gauge whether the Fed could upgrade its rate projections at the March meeting to signal four hikes in 2018.

The ECB minutes released yesterday confirmed some members wanted to alter the forward guidance around QE as early as at the January meeting. This enhances the case that the Bank may change its language in a more hawkish direction at the upcoming gathering in March. Euro/dollar spiked higher at the release, but quickly gave back its gains to trade lower in the following minutes.

Elsewhere, the Canadian dollar briefly stumbled yesterday, after the nation's retail sales for December disappointed. The core print fell by 1.8%, missing its forecast for a rise by 0.3%, and likely generating speculation that the economy may have ended 2017 on a soft note. As for the antipodean currencies, kiwi/dollar was more than 0.6% lower today, even though New Zealand's retail sales for the fourth quarter were surprisingly strong. Aussie/dollar fell 0.4%, pressured by the rebound in the greenback.

Day ahead: Eurozone and Canadian inflation due; Brexit developments eyed

Inflation figures out of the eurozone and Canada will perhaps be attracting most attention out of today's economic calendar.

Krona pairs will be in focus as the Swedish central bank's official record from its latest meeting will be made public at 0830 GMT.

The eurozone's final inflation figures for January are scheduled for release at 1000 GMT. Headline CPI is expected to be confirmed at 1.3% y/y, this reflecting a slowdown relative to December. Month-on-month, headline inflation is forecast to have contracted by 0.9%. Core CPI, the inflation measure that is calculated after excluding volatile items, will also be watched. It should be kept in mind that prices in the euro area often decline in January, so one might be justified not to place too much emphasis – at least in terms of ECB policymaking – on Friday's numbers.

Canadian inflation numbers for the month of January are due at 1330 GMT. On an annual basis, headline CPI is projected to have grown by 1.4%, easing from December's 1.9%. The Bank of Canada has a target for annual inflation of 2% with a 1% band around it (i.e. a 1-3% target band). Core inflation as well as the measures of inflation utilized by the BoC in its policymaking – common, median and trimmed CPI – will be generating interest as well. Loonie pairs will be watched, with an upside surprise in the readings anticipated to boost the Canadian dollar as market participants are likely to push closer in time their expectations for additional monetary policy tightening by the BoC.

Deliberations between UK PM Theresa May and her cabinet on arriving at the type of post-Brexit trade deal the nation wants with the EU will be closely watched. Sterling has proved extremely sensitive to developments on this front in the past. Also in politics, a meeting between US President Donald Trump and Australian Prime Minister Malcolm Turnbull could be attracting interest. The former might attempt to enhance cooperation between the two countries in an effort to “counter-weight” Australia's dependence on China and thus weaken the influence of the world's second largest economy.

In terms of policymakers' appearances: Bank of England Deputy Governor Dave Ramsden will be participating in a panel discussion on productivity and economic rebalancing at 1200 GMT. New York Fed President William Dudley and Boston Fed President Eric Rosengren will be talking on monetary policy at 1515 GMT; the former holds permanent voting rights within the FOMC, while the latter is not a voting member in 2018. ECB board member Benoit Coeure will be speaking at the 2019 US Monetary Policy Forum. Cleveland Fed President Loretta Mester will be participating in a panel discussion titled “A Review of the Objectives for Monetary Policy” at 1830 GMT and San Francisco Fed President John Williams will be speaking on the US economic outlook and monetary policy at 2040 GMT.

Oil traders will be paying attention to the US Baker Hughes oil rig count due at 1800 GMT.

In equities, companies releasing quarterly results will be attracting additional attention.

Technical Analysis: USDCAD bullish bias seems to ease as markets await Canadian inflation data

USDCAD reached a two-month high of 1.2755 during Thursday's trading. The Tenkan- and Kijun-sen lines are positively aligned, pointing to a bullish bias for the pair. However, the Kijun-sen has flatlined, indicating that the positive short-term momentum may be easing. The RSI supports this view: the indicator is well into bullish territory above 50, though it has halted its advance and is moving sideways.

If Canadian inflation figures surprise to the upside, the pair is anticipated to retreat. USDCAD could be finding support at the moment in the range between 1.2713 (the current level of the Tenkan-sen) and 1.2686 (a previous top). A violation of this range would shift the focus to the area around 1.2641 – where the Kijun-sen is situated at the moment – for additional support.

On the other hand, disappointing CPI figures could refuel the bullish momentum. In this case, the area around yesterday's high of 1.2755 could act as a barrier to the upside.

Technical Outlook: EURUSD Remains Biased Lower, EU Inflation Data In Focus

The Euro stands at the back foot in early Friday's trading and probes below 1.23 handle, focusing initial support at 1.2259 (22 Feb low).

Recovery attempts on Thursday were limited by 30SMA that kept bearish near-term bias in play, despite positive daily close.

Bearishly aligned daily techs along with hawkish Fed and benign ECB minutes weigh on Euro.

EU inflation data are in focus today. Forecasts are pointing to soft numbers (Jan CPI m/n -0.9% f/c vs 0.4% prev, Core y/y 1.0% f/c vs 1.2% prev) which could add to persisting pressure.

Below 1.2259, key supports lay at 1.2210/05 (20-d lower Bollinger band/09 Feb low) and 1.2173 (Fibo 38.2% of 1.1553/1.2555 ascend), break of which is needed to confirm reversal and trigger deeper correction.

Alternative scenario requires close above 30SMA (1.2342) to sideline immediate downside risk, while firm break above converged 10/20SMA's (1.2366) is needed to neutralize and shift near-term focus higher.

Res: 1.2342, 1.2366, 1.2407, 1.2442

Sup: 1.2279, 1.2259, 1.2235, 1.2205

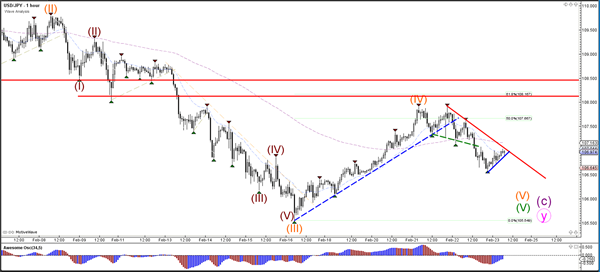

Daily Wave Analysis: Can USDJPY Continue With Downtrend After Bounce At 50% Fib?

Currency pair USD/JPY

The USD/JPY bounced at the resistance zone and is now building a lower high. Price will need to break below support (green) before a bearish breakout is likely.

The USD/JPY is testing a resistance trend line (red). A bearish bounce could see price continue with the downtrend whereas a bullish breakout could indicate a bigger reversal.

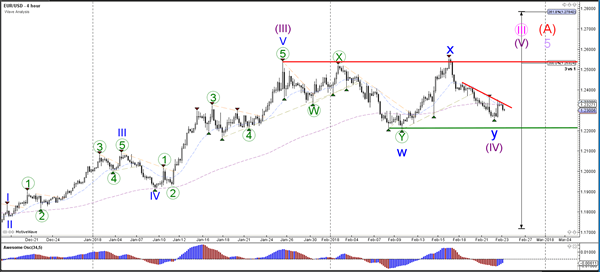

Currency pair EUR/USD

The EUR/USD made a bullish bounce at the support zone of the previous wave W (blue) bottom. A bullish breakout above the resistance trend line (red) confirms the potential start of a bullish wave 5 (purple) but one more push lower could occur to test the green support.

The EUR/USD could be developing a bullish reversal unless breaks below the 100% Fibonacci level.

Currency pair GBP/USD

The GBP/USD bounced at the long-term support trend line (blue) and is now retesting a resistance trend line (red). Price will need to break the S&R before a new trend can become visible.

The GBP/USD bounced at the bottom of the channel and has arrived at the top of the channel. Price is now at a bounce or break spot.

European Market Choppy | Gold & Oil Obey One Direction

US futures are set to close out a rather dull weak on a positive note

UK's GDP data failed to meet expectations yesterday

The ECB has things under control

European markets are choppy today. US futures are set to close out a rather dull weak on a positive note on Friday. Investors are still finding it difficult to make up their mind as the message from the Fed towards their monetary policy normalisation has any acute angle. Nonetheless, the dollar index has found a lot of love amidst speculators that the Fed could be aggressive this year.

Despite all this, the dollar index is still struggling to break above the 91 mark as the recent profit-taking started at a level of 90.17. However, the bargain hunters or shall we say speculators, have stepped back in fairly quickly as the price dropped to 89.64.

Although the UK's GDP data failed to meet expectations yesterday, a weaker dollar and a confident Mark Carney was enough to push GBP/USD past 1.395. The hawkish policy tilt has started to overshadow the drag from Brexit worries. Traders are open to the idea that there could be more strength ahead for the pair as they continue to price in the possibility of another rate hike by the Bank of England next month. The evidence that the BOE could be raising the interest rate next month is evident in the market implied volatility which has jumped to 83 percent. The number stood at 51 percent during the last month.

There were some brief spikes when the European Central bank published its minutes yesterday but overall the ECB had things under control. This statement looks relatively much stronger when we compare the market reaction to a similar event during the last month. The ECB has learned that it has to write its minutes very carefully otherwise the currency could explode in either direction. The ECB communicated that the governing council is fully committed to remove the expansion of the bond-buying program and any change in language is very much dependent on the inflation outlook. Given that there is no clear timeframe when the ECB will fully shut the shop of cheap money, investors are hesitant before entering longs with this pair.

Gold

The third weekly decline for the precious metal is on the cards as investors pay attention to speculators who are fuelling the dollar rally on the basis that the Fed could increase the interest rate four times this year. However, we think that this pullback could be an opportunity for the bulls to jump on the trade as this could be a buying opportunity.

Oil

The US is pumping out a record amount of oil and investors angst that these record amount would swell stockpiles. The bull rally which we have seen for the black gold could fade away as the US oil production undermines the OPEC production cut commitments.