Sample Category Title

EUR/GBP Weekly Outlook

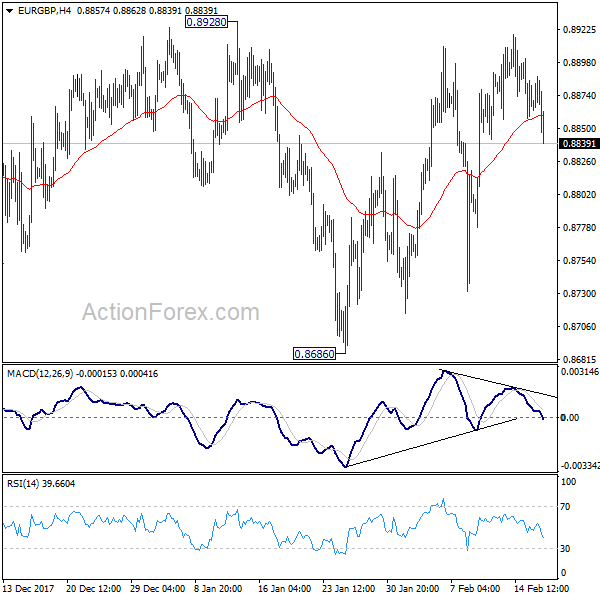

EUR/GBP edged higher last week but failed to take out 0.8928 resistance and reversed. As it's staying in range of 0.8686/8928, outlook is unchanged. Initial bias stays neutral this week first. Near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too, deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

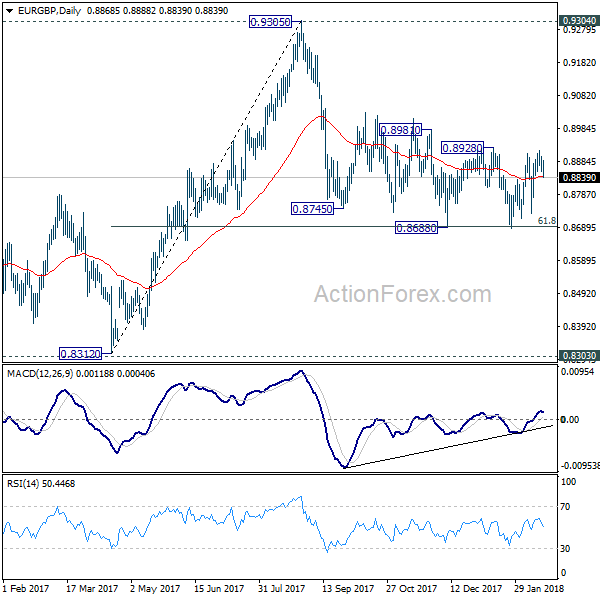

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

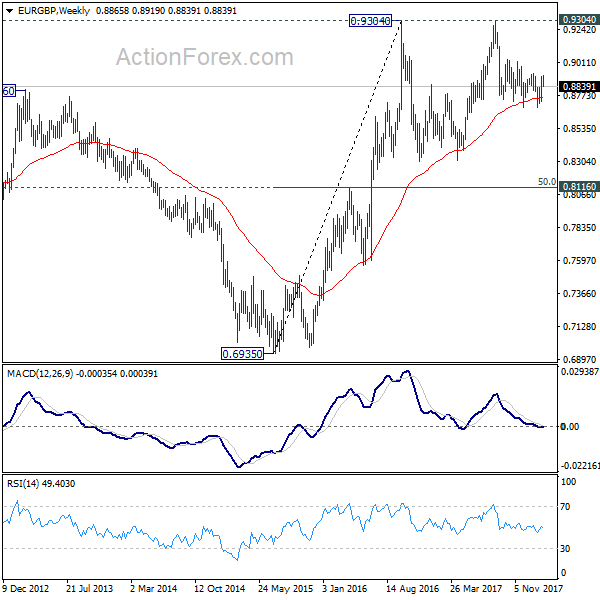

In the long term picture, we're holding on to the view that rise from 0.6935 (2015 low) is resuming the up trend from 0.5680 (2000 low). Hence, after the consolidation from 0.9304 completes, we'd expect another medium term up trend through 0.9799 to 100% projection of 0.5680 to 0.9799 from 0.6935 at 1.1054.

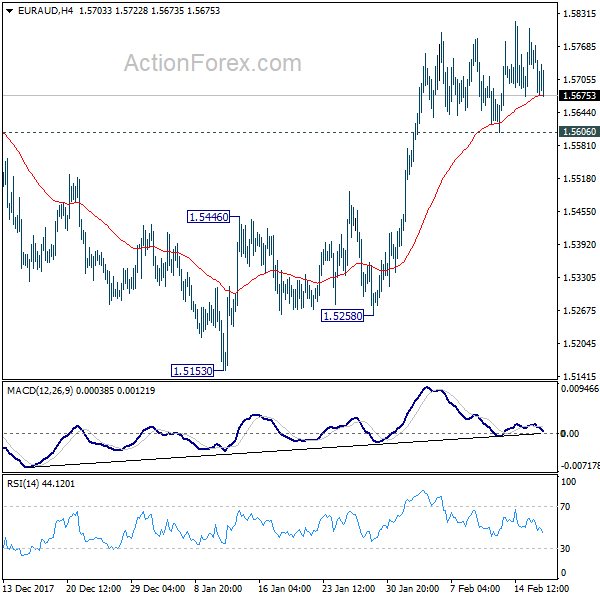

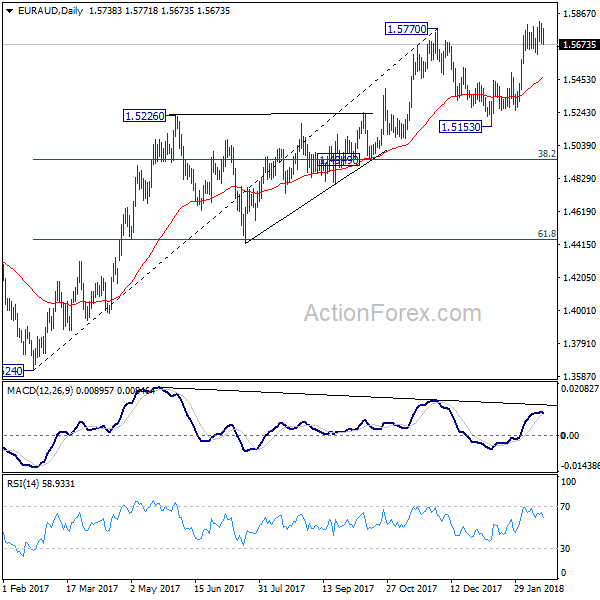

EUR/AUD Weekly Outlook

EUR/AUD edged higher last week but failed to sustained gain and retreated quickly. Nonetheless, with 1.5606 support intact, near term outlook stays bullish. Sustained trading above 1.5770 key resistance Sustained trading above 1.5770 will confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance. However, below 1.5606 minor support minor support will dampen this bullish case and turn bias to the downside for 55 day EMA (now at 1.5463).

In the bigger picture, medium term rise from 1.3624 is not completed yet. Sustained break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

In the longer term picture, the rise from 1.1602 long term bottom (2012 low) isn't over yet. We'll keep monitoring the development but there is prospect of extending the rise to 61.8% retracement of 2.1127 to 1.1602 at 1.7488 and above. However, sustained trading below 1.3671 should indicate long term reversal and target 1.1602 long term bottom again.

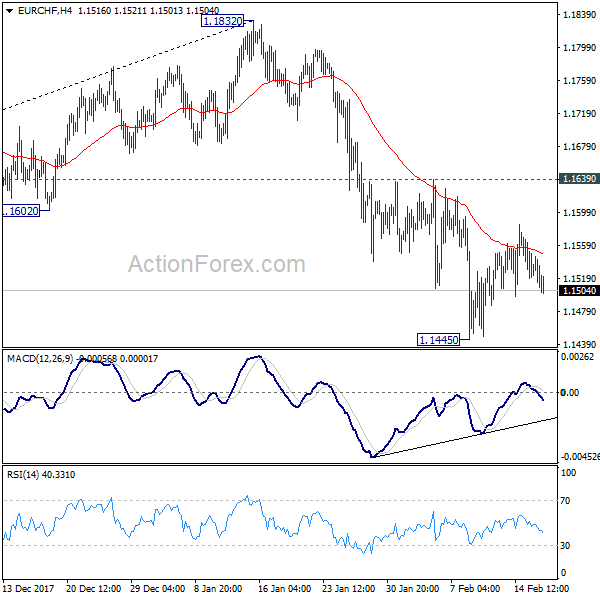

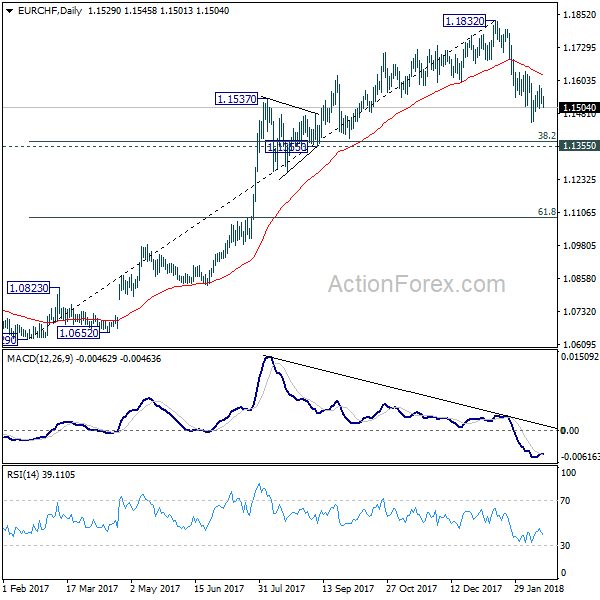

EUR/CHF Weekly Outlook

EUR/CHF turned into consolidation last week as it recovered. But upside was limited well below 1.1639 resistance. Initial bias stays neutral this week with bearish near term outlook. Break of 1.1445 will resume the corrective fall from 1.1832 and target 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Dollar Hit Three Year Low as Down Trend Resumed, No Clear Sign of Reversal Yet

Dollar's broad based weakness continued last week and ended as the worst performing major currency. Stronger than expected consumer inflation reading listed treasury yield and raised the chance of a March Fed hike. Fed fund futures are now pricing in 83% chance of a March hike. But that provided just very brief support to the greenback. Dollar index extended the long term down trend to new three year low, suffering the worst weekly decline since September. Some pointed to Friday's rebound as a sign of reverse in fortune in Dollar. But we'll, for now, take a more cautious stance on it first. Elsewhere, Canadian Dollar and Australian Dollar ended as the second and third weakest ones. Yen, Kiwi and Pound were the strongest.

The correlation between dollar and treasury yield continued to break down last week. Initial reaction to CPI release was as expected as both Dollar and yields surged. But then, while yields retreated, they stayed resilient. Dollar, on the other hand, suffered steep selloff and resumed recent down trend. There are various explanations to the break down in correlation. But we'd like to point out one fundamental question first. That is, does higher yield make dollar assets more attractive? Or does it reflect the relative unattractiveness of dollar assets?

Many, including us, got it wrong until recently. It worked before, in particular seen in USD/JPY in most of the low interest rate era, that higher US yields will lift the Dollar. But now, as we're existing this era, it's just reflection that Dollar assets are getting less attractive. In the background, Fed's shrinking of the balance sheet this year is going to flood the markets with extra supply in bonds. And then, investors, domestic and overseas, are getting more willing to take risks than parking them in bonds. The US markets, continuously making record runs, is a good place for investments. But some find other markets, like EU and Asia, at least as attractive. Also, the money flow could be seen as a vote of "no confidence" in US President Donald Trump in his deficit booming fiscal policies (with the tax cut), as well as protectionist trade policies. We're not expecting the positive correction to return, until we seen solid evidence.

10 year yield (TNX) edged higher to 2.888 before closing at 2.877. It's the second week that TNX closed lower than weekly open. And it's starting to look tired ahead of 3.036 key resistance. Nonetheless, as long as 2.736 near term support holds, outlook will stays bullish. Region between 3.036 and 3.318 (100% projection of 1.336 to 2.621 from 2.034) is the real long term trend defining junction for TNX. On the downside break of 2.7.36 will at least bring deeper correction towards 55 day EMA (now at 2.618) first.

Dollar index resumed last long term down trend from 103.82 and edged lower to 88.25 last week. Notable buying was seen last Friday to bring a recovery in the greenback. DXY closed back inside recently established rate at 89.10. 50% retracement of 72.69 to 103.82 at 88.25 could still be providing strong support to DXY. But it's far too early to talk about reversal. Near term resistance zone between 90.56 and 91.01 must be overcome first before having any chance of a trend reversal. That would be equivalent to a break of 1.2205 support in EUR/USD. Otherwise, the down trend from 103.82 is more likely than not to extend to next key cluster support at 84.75, 61.8% retracement of 72.69 to 103.82 at 84.58, before completion.

DOW was initially sold off after strongest than expected US CPI release but quickly reversed. It indeed extended the rebound from 22360.29 to close solidly to 25219.38. As we pointed out during the week, the reactions could be interpreted as "the worst in stocks was over". The steep selloff from 26616.71 to 23360.29 was based on worries over tightening by Fed. As seen in fed fund futures, chance of a March hike continued to rise to 83% after the CPI release. But stocks were resilient. So, that selloff was probably an over-reaction. The coming days will be important as sustained trading above 61.8% retracement of 26616.71 to 23360.29 at 25372.75 will establish DOW in, at worst, a sideway consolidation pattern, rather than a downward correction pattern.

Position trading strategy

We're holding on to our GBP/CHF short (sold at 1.3105). We're still bearish in the cross for 38.2% retracement of 1.1638 to 1.3491 at 1.2783 as the first target, and 61.8% retracement at 1.2346 as second. But the lack of downside momentum is disappointing. And as mentioned above, there is a risk that the worst in risk markets was over. Hence, we'll lower the stop to break even at 1.3105. For those who'd like to move on, exiting on a dip this week is ok too. Though, we'll give it a little bit more time.

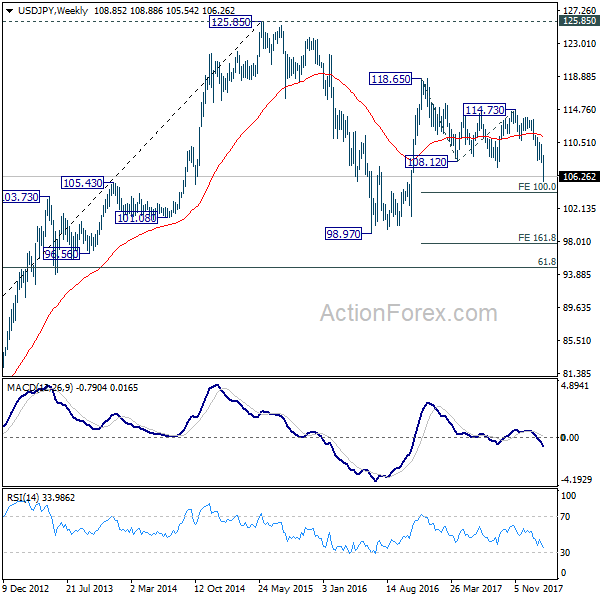

USD/JPY Weekly Outlook

USD/JPY's down trend continued last week and reached as low as 105.54. A temporary low was formed with 4 hour MACD crossed above signal line. Initial bias is neutral this week for consolidation first. But recovery should be limited below 108.72 support turned resistance and bring fall resumption. Below 105.54 will target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48. now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

Eco Data 2/23/18

[php_everywhere] [/php_everywhere]

Eco Data 2/22/18

[php_everywhere] [/php_everywhere]

Eco Data 2/21/18

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q4 | 0.60% | 0.50% | 0.50% | |

| 00:30 | AUD | Construction Work Done Q4 | -19.40% | -10.00% | 15.70% | 16.60% |

| 00:30 | JPY | PMI Manufacturing Feb P | 54 | 55.2 | 54.8 | |

| 04:30 | JPY | All Industry Activity Index M/M Dec | 0.50% | 0.40% | 1.00% | |

| 08:00 | EUR | France Manufacturing PMI Feb P | 56.1 | 58 | 58.4 | |

| 08:00 | EUR | France Services PMI Feb P | 57.9 | 59 | 59.2 | |

| 08:30 | EUR | Germany Manufacturing PMI Feb P | 60.3 | 60.5 | 61.1 | |

| 08:30 | EUR | Germany Services PMI Feb P | 55.3 | 57 | 57.3 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb P | 58.5 | 59.2 | 59.6 | |

| 09:00 | EUR | Eurozone Services PMI Feb P | 56.7 | 57.6 | 58 | |

| 09:30 | GBP | Jobless Claims Change Jan | -7.2K | 2.3K | 8.6K | |

| 09:30 | GBP | Claimant Count Rate Jan | 2.30% | 2.40% | ||

| 09:30 | GBP | Average Weekly Earnings 3M/Y Dec | 2.50% | 2.50% | 2.50% | |

| 09:30 | GBP | ILO Unemployment Rate 3Mths Dec | 4.40% | 4.30% | 4.30% | |

| 09:30 | GBP | Public Sector Net Borrowing Jan | -11.6B | -11.0B | 1.0B | |

| 14:45 | USD | US Manufacturing PMI Feb P | 55.9 | 55.5 | 55.5 | |

| 14:45 | USD | US Services PMI Feb P | 55.9 | 54 | 53.3 | |

| 15:00 | USD | Existing Home Sales Jan | 5.38M | 5.63M | 5.57M | 5.56M |

| 19:00 | USD | FOMC Meeting Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q4 | |

| Actual: 0.60% | Forecast: 0.50% | ||

| Previous: 0.50% | Revised: | ||

| 00:30 | AUD | Construction Work Done Q4 | |

| Actual: -19.40% | Forecast: -10.00% | ||

| Previous: 15.70% | Revised: 16.60% | ||

| 00:30 | JPY | PMI Manufacturing Feb P | |

| Actual: 54 | Forecast: 55.2 | ||

| Previous: 54.8 | Revised: | ||

| 04:30 | JPY | All Industry Activity Index M/M Dec | |

| Actual: 0.50% | Forecast: 0.40% | ||

| Previous: 1.00% | Revised: | ||

| 08:00 | EUR | France Manufacturing PMI Feb P | |

| Actual: 56.1 | Forecast: 58 | ||

| Previous: 58.4 | Revised: | ||

| 08:00 | EUR | France Services PMI Feb P | |

| Actual: 57.9 | Forecast: 59 | ||

| Previous: 59.2 | Revised: | ||

| 08:30 | EUR | Germany Manufacturing PMI Feb P | |

| Actual: 60.3 | Forecast: 60.5 | ||

| Previous: 61.1 | Revised: | ||

| 08:30 | EUR | Germany Services PMI Feb P | |

| Actual: 55.3 | Forecast: 57 | ||

| Previous: 57.3 | Revised: | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Feb P | |

| Actual: 58.5 | Forecast: 59.2 | ||

| Previous: 59.6 | Revised: | ||

| 09:00 | EUR | Eurozone Services PMI Feb P | |

| Actual: 56.7 | Forecast: 57.6 | ||

| Previous: 58 | Revised: | ||

| 09:30 | GBP | Jobless Claims Change Jan | |

| Actual: -7.2K | Forecast: 2.3K | ||

| Previous: 8.6K | Revised: | ||

| 09:30 | GBP | Claimant Count Rate Jan | |

| Actual: 2.30% | Forecast: | ||

| Previous: 2.40% | Revised: | ||

| 09:30 | GBP | Average Weekly Earnings 3M/Y Dec | |

| Actual: 2.50% | Forecast: 2.50% | ||

| Previous: 2.50% | Revised: | ||

| 09:30 | GBP | ILO Unemployment Rate 3Mths Dec | |

| Actual: 4.40% | Forecast: 4.30% | ||

| Previous: 4.30% | Revised: | ||

| 09:30 | GBP | Public Sector Net Borrowing Jan | |

| Actual: -11.6B | Forecast: -11.0B | ||

| Previous: 1.0B | Revised: | ||

| 14:45 | USD | US Manufacturing PMI Feb P | |

| Actual: 55.9 | Forecast: 55.5 | ||

| Previous: 55.5 | Revised: | ||

| 14:45 | USD | US Services PMI Feb P | |

| Actual: 55.9 | Forecast: 54 | ||

| Previous: 53.3 | Revised: | ||

| 15:00 | USD | Existing Home Sales Jan | |

| Actual: 5.38M | Forecast: 5.63M | ||

| Previous: 5.57M | Revised: 5.56M | ||

| 19:00 | USD | FOMC Meeting Minutes | |

| Actual: | Forecast: | ||

| Previous: | Revised: | ||

Eco Data 2/20/18

[php_everywhere] [/php_everywhere]

Eco Data 2/19/18

[php_everywhere] [/php_everywhere]

Summary 2/19 – 2/23

Monday, Feb 19, 2018

[php_everywhere] [/php_everywhere]

Tuesday, Feb 20, 2018

[php_everywhere] [/php_everywhere]

Wednesday, Feb 21, 2018

[php_everywhere] [/php_everywhere]

Thursday, Feb 22, 2018

[php_everywhere] [/php_everywhere]

Friday, Feb 23, 2018

[php_everywhere] [/php_everywhere].