Sample Category Title

UK’s Retail Sales Rises Less Than Expected In January

For the 24 hours to 23:00 GMT, the GBP declined 0.76% against the USD and closed at 1.4013 on Friday, after data showed that UK's retail sales came in worse-than-expected in January. Britain's retail sales grew at a slower than expected pace of 0.1% on a monthly basis in December, as a rise in inflation weighed on consumer spending. Retail sales had registered a revised drop of 1.4% in the prior month, while markets were anticipating for a gain of 0.5%.

In the Asian session, at GMT0400, the pair is trading at 1.4040, with the GBP trading 0.19% higher against the USD from Friday's close.

Overnight data showed that UK's Rightmove house price index rose 0.80% on a monthly basis in February, after recording a gain of 0.7% in the previous month.

The pair is expected to find support at 1.3976, and a fall through could take it to the next support level of 1.3913. The pair is expected to find its first resistance at 1.4124, and a rise through could take it to the next resistance level of 1.4209.

With no major macroeconomic releases in the UK today, investor sentiment would be determined by global macroeconomic news.

The currency pair is showing convergence with its 20 Hr and trading below its 50 Hr moving average.

Japan’s Trade Surplus Widened Above Expectations In January

For the 24 hours to 23:00 GMT, the USD rose 0.23% against the JPY and closed at 106.36 on Friday.

In the Asian session, at GMT0400, the pair is trading at 106.33, with the USD trading 0.03% lower against the JPY from Friday's close, after overnight data showed that Japan's adjusted merchandise trade surplus widened more-than-anticipated to ¥373.3 billion in January, after recording a surplus of ¥86.8 billion in the previous month. Markets were anticipating the country's adjusted merchandise trade surplus to drop to ¥143.9 billion. The nation's exports advanced 12.2% on an annual basis in January, higher than market expectations for a gain of 9.4%. In the previous month, exports had risen 9.3%. Also, the nation's imports climbed 7.9% YoY in December, beating market estimates for a rise of 7.7%. Imports had advanced 14.9% in the prior month.

The pair is expected to find support at 105.79, and a fall through could take it to the next support level of 105.24. The pair is expected to find its first resistance at 106.64, and a rise through could take it to the next resistance level of 106.94.

Going ahead, traders would focus on Japan's machine tool orders for January, scheduled to release tomorrow.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving average.

Swiss Franc Trading Marginally Firmer

For the 24 hours to 23:00 GMT, the USD rose 0.78% against the CHF and closed at 0.9281 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9276, with the USD trading 0.05% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9213, and a fall through could take it to the next support level of 0.9151. The pair is expected to find its first resistance at 0.9313, and a rise through could take it to the next resistance level of 0.9351.

The currency pair is trading above its 20 Hr and 50 Hr moving average.

Loonie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.67% against the CAD and closed at 1.2560 on Friday.

In the Asian session, at GMT0400, the pair is trading at 1.2536, with the USD trading 0.19% lower against the CAD from Friday’s close.

The pair is expected to find support at 1.2469, and a fall through could take it to the next support level of 1.2402. The pair is expected to find its first resistance at 1.2585, and a rise through could take it to the next resistance level of 1.2634.

In absence of any macroeconomic releases in Canada today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving average.

Asian Equity Market Gains And The U.S. Dollar’s Weakness

Asian equity markets continued to build on last week's gains, after U.S. stocks capped their best week since 2013. Investor sentiment has gradually improved after fears of rising inflation sent most global indices into correction territory. The Cboe's Volatility Index (VIX) ended Friday's session below 20, suggesting that indictments from Special Counsel Robert Mueller against 13 Russian nationals for alleged interference in the 2016 elections did little to impact investor decisions. With the U.S. markets closed on Monday for President's Day and the Greater China region remaining offline for the Lunar New Year, expect trading volumes to be below average.

The U.S. Dollar's weakness remained a bit of a mystery for many currency traders, as it is supposed to follow differential in yields. The gap between U.S. and German 10-year yields widened to 217 basis points, and had gained 28% since mid-July 2017. Similarly, U.S. – Japan 10-year yields widened 285 basis points, the highest increase since 2007. Still, the Dollar declined against the Euro, Japanese Yen and all other major currencies.

One explanation for why the correlation between the Dollar and yield differentials has broken recently, is that financial market participants are forward-looking. Investors believe that rising inflation in the U.S. will spread to other economies, leading to tighter monetary policies elsewhere. When major central banks such as the European Central Bank, Bank of England and Bank of Japan begin normalizing policies, rate differentials will narrow at a fast pace, given that they are starting from a very low base.

Yields in the U.S. are not just rising because of higher inflation expectations, but also due to rising twin deficits – the fiscal and current account. This should make U.S. debt less attractive, and gold will likely become the primary beneficiary as it continues to benefit from inflationary pressures and budget deficit worries.

However, this view may change if the Fed decides to take a more aggressive approach in fighting inflation. Wednesday's FOMC minutes will likely reveal fresh hawkish insights, but for the dollar to make a U-turn, it requires the Fed to tighten policy faster than previously estimated. Any indication of four rate hikes instead of three in 2018 will do the trick, but this is unlikely to appear in Wednesday's minutes, and investors will probably need to wait until the March meeting.

USD/JPY Broke Below 106

Market movers today

We start the week in a quiet fashion on the data front . The main events will be the minutes of the latest Fed meeting on Wednesday, including the Fed governor’s view on inflation and impending fiscal expansion, as well as the ECB minutes on Thursday. Another highlight this week will be PMI and IFO releases in the euro area and Germany on Wednesday and Thursday, respectively, which will give signs of the continued momentum in the euro area economy.

The Eurogroup will convene today and recommend one candidate to replace Vítor Constâncio as the ECB’s Vice President in June. It is a race between the favourite, Spain’s Economy Minister Luis de Guindos and the Irish Central Bank Governor Phillip Lane. As the Eurogroup decides on the next Vice President , attention turns to Mario Draghi’s successor as President with a recent Bloomberg survey of economists showing Germany’s Jens Weidmann (über hawk) as the clear favourite. See the poll here.

In Sweden, we get data on residential permits, starts and completions

Selected market news

Japanese shares rose this morning, leading Asian stocks higher, while Brent oil advanced above USD65/bbl. Robert Mueller, the Russia probe special counsel, indicted 13 Russian individuals and three Russian entities for allegedly interfering in the 2016 US presidential election through an elaborate social media campaign to help Donald Trump. The indictment means that Trump can no longer credibly cast doubt on alleged Russian election meddling, although he continues to deny the allegations. On Friday, the S&P 500 erased a gain that reached 0.9% following the news, while 10-year Treasury yields fell below 2.9%. Nevertheless, US equity index futures climbed this morning, although sett ement will be delayed due to the Presidents’ Day holiday .

The US Commerce department recommended the Trump administration to impose steep tariffs of 24% on steel and 7.7% on aluminium imports on national security grounds. China has already threatened retaliation to such measures, risking further escalation of trade tension between the world’s top two economies.

On Friday, the Japanese government officially reappointed Bank of Japan governor Haruhiko Kuroda for another five-year term and chose an advocate of bolder monetary easing as one of his deputies in a strong signal to investors that policy makers are in no rush to end the stimulus programme. A vote in parliament on the appointments could happen before the end of the month. On the news, USD/JPY broke below 106, triggering a linguistic tweak by Finance Minister Taro Aso, who said the government will act when needed, a day after stating there is no need for intervention.

Supported by tax cuts and a strong jobs market , US consumer confidence rose further in January to the second highest level since 2004. This supports our view that private consumption will remain the main growth driver in the US, although long-term inflation expectations remained unchanged at 2.5%.

Market Update – Asian Session: Japan Records First Trade Deficit In 8-Months

Headlines/Economic Data

General Trend:

Equities markets higher with China markets closed for holiday,US and Canada also closed for Monday session

Overall news light with, China, US and Canada closed for Mondayholiday

A$ is the outperformer rising as high as 0.7935, overall USD slightly weaker across the region

Strong yen weighing on manufacturers and exporters confidence

Japan

Nikkei 225 opened +0.8%; closed +2%

(JP) JapanJan Trade Balance: -¥943.4B v -¥1.02Te (1st deficit in 8-months);Adj Trade Balance: ¥373.3B v ¥144Be; Exports y/y: 12.2% v9.4%e, Imports y/y: 7.9% v 7.8%e; Exports to Asia +16%; China +30.8%; US +1.2%,EU+20.3%

(JP)Poll of analysts say a stronger yen may cause adelay in BOJ tapering of ultra easy policy - financial press

Korea

Kospi opened +1.3%

(KR) Bank of Korea (BoK)sells KRW410B in 6-month monetary stabilization bonds (MSB) at 1.63%

(KR) Bank of Korea(BoK) sells KRW1.0T vs. KRW1.0T indicated in 3-month monetary stabilizationbonds (MSB); Yield: 1.58% v 1.50% prior

(KR) Accumulated commission-related sales ofsome 30 cryptocurrency exchange operators in South Korea are thought to havereached KRW700B at the end of 2017 v KRW8B in 2016 - Korean press

China/HongKong

Hang Seng closed for holiday; Shanghai Composite closed for holiday

(CN) ChinaCommerce Ministry official Wang Hejun: if the final decision [about USrestrictions on steel and aluminum imports] hurts China’s interests, we willcertainly take necessary measures to protect our legitimate rights

(CN) China reiterates non-first-use on nuclearweapons

(CN) China Jan bond issuance totaled CNY2.5T(CNY2.4T through inter-bank, CNY190B through Treasury issuance) - Xinhua

Australia/NewZealand

ASX 200 opened -0.1%; closed +0.7%

(NZ) New Zealand JanPerformance of Service Index: 55.8 V 56.0 prior

Brambles(-3% ), BXB.AU Reports H1 (A$) Underlying Net 493.7M* v 295M y/y; Rev 2.75B v 2.52B y/y

(NZ) New Zealand expecting 'a lot of disruption' from Cyclone Gita

GWA Group (+12.5%), GWA.AU Reports H1 (A$) Net 27.7M v 27Me; EBIT 41.8M v 41Me; Rev 227.1M v 221Me;To divest Door & Access Systems business unit

(AU) Australia in talks about a project to counter China’s Belt and Roadprogram – AFR

LookingAhead: Tomorrow NZ PPI and RBA meeting minutes, miner BHP reports H1 results

Other Asia

Noble Group, NOBL.SG Updates on proposed financial restructuring: Entered ad hoc agreement withING for $700M facility; confident it can continue as a going concern; Guides Q4 net loss $1.93-1.73B

North America

DIS “Black Panther” top film at the box office over the weekend with $192.0Min North American sales

On Friday. US CommerceDepartment has recommended that President Donald Trump impose steep curbs onsteel and aluminum imports from China andother countries ranging from global and country-specific tariffs to broadimport quotas

NXPI Qualcomm said to be working on deal price for NXP, said to be in low$120/shr - CNBC

Europe

(UK) UKIP leader Boltonremoved by party members after less than five months in charge followingcriticism of his leadership and a scandal about racist comments made by hislover - press

(UK) Feb Rightmove House Prices m/m: 0.8% v 0.7% prior; y/y: 1.5% v 1.1% prior

(EU) IMF's Lagarde: Have no objection to plans to turn the euro zone’s bailoutfund into a European Monetary Fund – Swiss press

(UK) PM May rules out second vote on membership in EU, no going back on theJune 2016 vote - press

Levels as of01:00ET

Nikkei225 +2%, Hang Seng closed; ShanghaiComposite closed; ASX200 +0.7%, Kospi +0.6%

Equity Futures: S&P500 +0.4%; Nasdaq100 +0.4%, Dax +0.4%; FTSE100 +0.8%

EUR 1.2435-1.2399; JPY104.44-106.09; AUD 0.7935-0.7900;NZD 0.7409-0.7377

Apr Gold -0.5% at $1,350/oz; Apr Crude Oil +1.2%at $62.30/brl;Mar Copper -0.2% at $3.23/lb

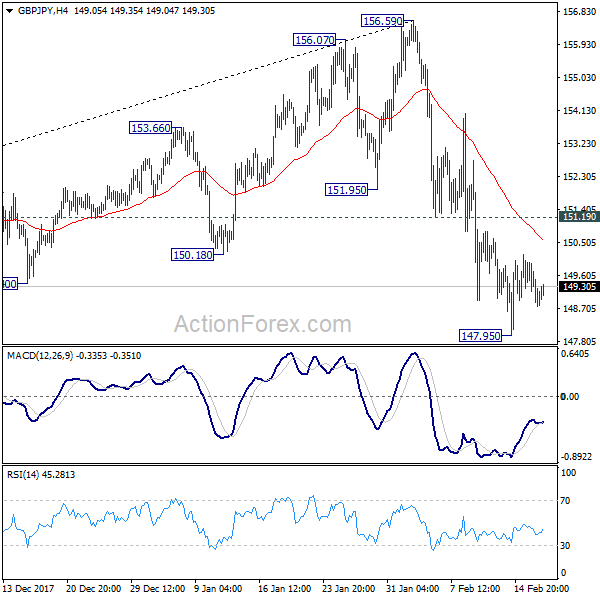

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.62; (P) 149.28; (R1) 149.80; More...

Intraday bias in GBP/JPY remains neutral for consolidation above 147.95 temporary low. Upside of recovery should be limited by 151.19 resistance to bring another fall. Below 147.95 will target 146.96 support next. Considering bearish divergence condition in daily MACD, firm break of 146.96 will be another sign of medium term trend reversal. On the upside, break of 151.19 will indicate short term bottoming and turn bias back to the upside for rebound.

In the bigger picture, the case for medium term reversal continues to build up on loss of medium term momentum as seen in 4 hour MACD. Also, firm break of 146.96 will indicate rejection by 55 month EMA and add to that case of reversal. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43. Meanwhile, break of 156.59 will extend the rise from 122.36 to 61.8% retracement of 195.86 to 122.36 at 167.78.

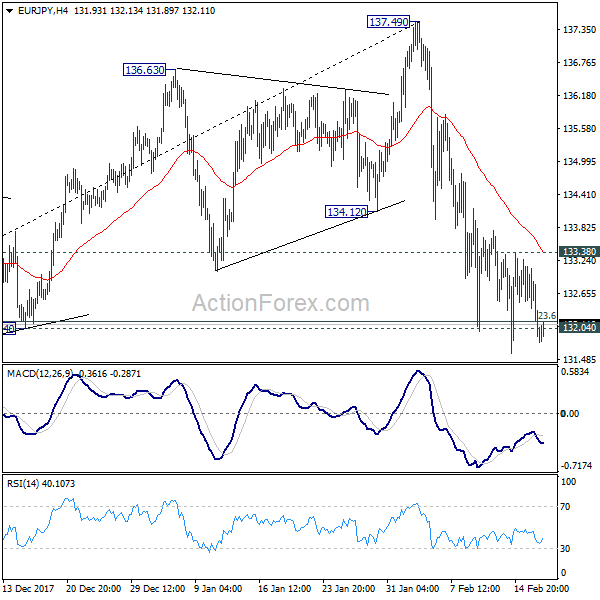

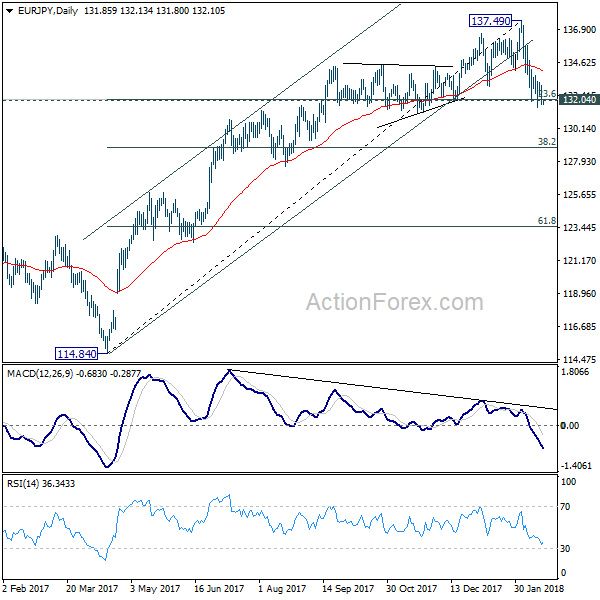

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.44; (P) 132.27; (R1) 132.73; More....

Near term outlook remains bearish with 133.38 resistance intact. Sustained trading below 132.04 cluster support (23.6% retracement of 114.84 to 137.49 at 132.14) will indicate larger trend reversal on bearish divergence condition in daily MACD. In such case, deeper decline would be seen for 38.2% retracement at 128.38 first. However, rebound from 132.04 will retain near term bullishness. Break of 133.38 minor resistance will turn bias back to the upside for 137.49 again.

In the bigger picture, bearish divergence condition in weekly MACD indicates loss of medium term upside momentum. Sustained break of 132.04 will be the early sign of long term reversal and should bring deeper fall back to retest 124.08 key support level. Meanwhile, break of 137.49 will resume the up trend from 109.03 to 141.04/149.76 resistance zone.

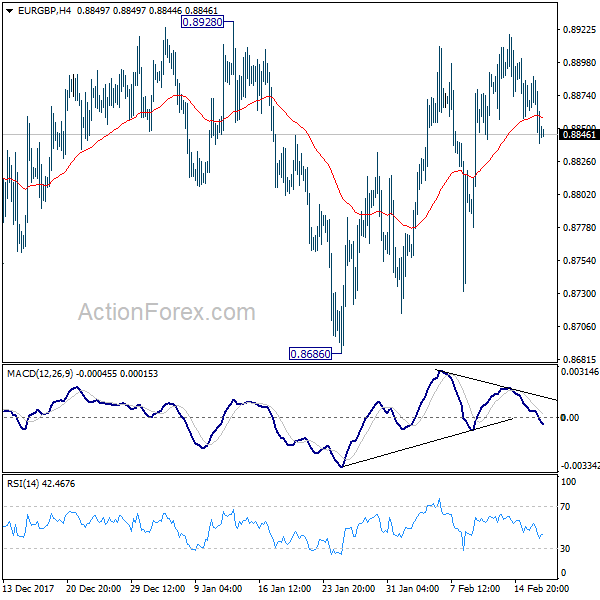

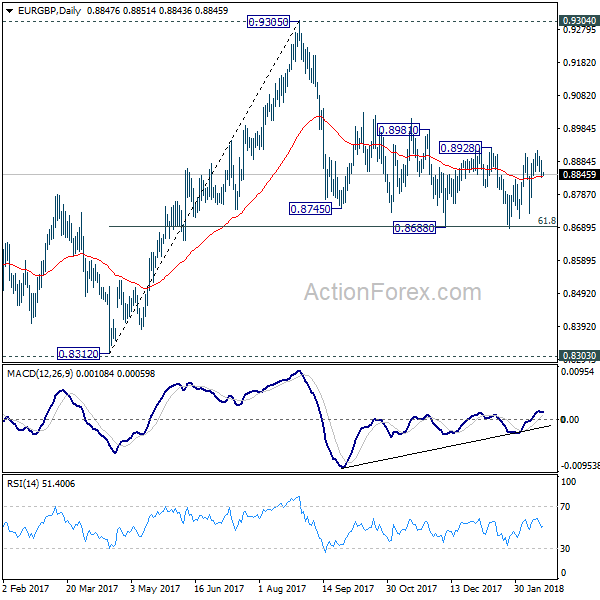

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8823; (P) 0.8855; (R1) 0.8872; More...

Intraday bias in EUR/GBP remains neutral as range trading continues. Near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too, deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.